The Next Inflection in Crude Oil: When Will the Hormuz Bottleneck Break?

Navigating the Volatile Balance of Geopolitics and Global Oil Inventories.

Last week, we had a call with who we consider one of the best crude oil shipping company CEOs in the world. We had a genuinely good conversation about Hormuz and where oil prices are heading. We had our thoughts, he had his.

That said, we did not agree on everything, and that is totally fine.

We spent a long time discussing the Strait of Hormuz, the timing, and exactly what happens to physical oil flows the day it reopens, whether fully or partially.

We debated how markets tend to react when a massive supply shock finally unwinds. The biggest takeaway from those discussions was the level of uncertainty, even among the people closest to the oil market.

Nobody knows the exact timing of a reopening, the early flow dynamics, or whether prices will overreact the way they always do in oil markets. And unless your name is Donald Trump, you’re not getting that answer anytime soon.

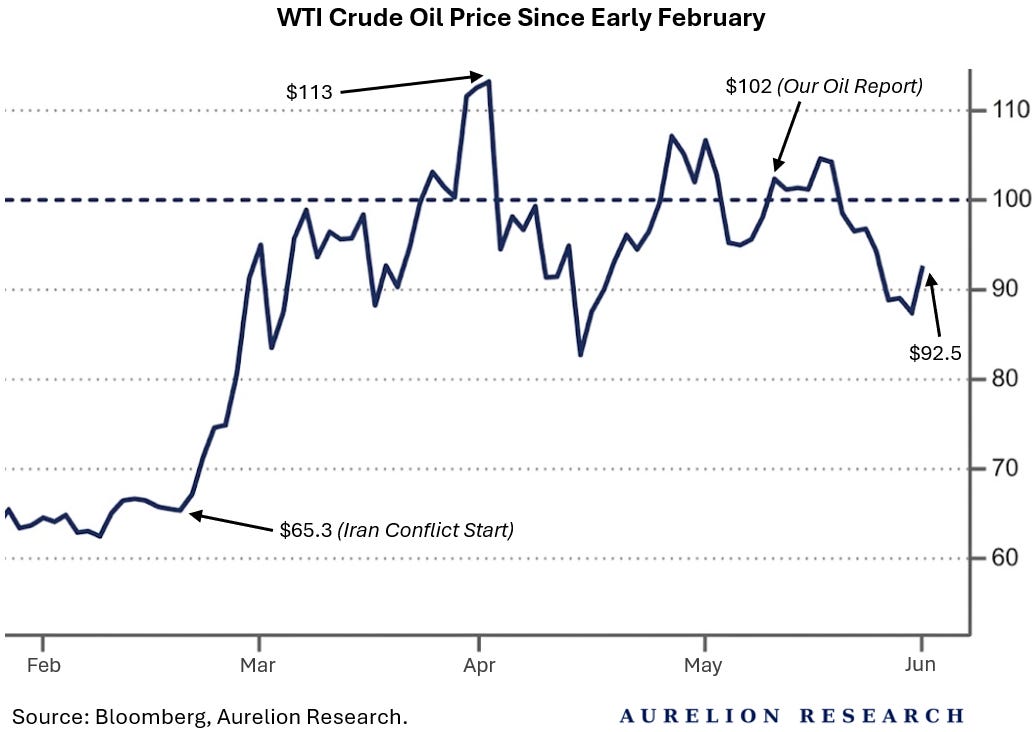

Three weeks ago, we were very vocal that oil prices were heading lower.

Unlike most institutional analysts, strategists, or macro experts, we gave you a definitive stance on the commodity. We did not stay safely neutral. As independant analyst, we have the freedom to call it exactly as we see it.

In our opinion, oil is easily the hardest commodity to predict or forecast because of how deeply it runs through the global economy. It is one of the world’s most important resource, directly tied to nearly everything we consume.

There is a loud contingent of oil experts who love to tell you that oil is headed straight to $150 per barrel. We have been hearing that same narrative for a long time now, but the market is clearly tired of it. Just look at the actual price action.

If you have been holding long oil positions for a while, hopefully it was not using short-term crude oil futures.

We got a lot of criticism for our view. Most of it came from oil bulls who took our bearish stance way too personally. Losing money can have that effect on people. The personal attacks were irrelevant to our thesis, but they were great free marketing for Aurelion Research, so we will take it.

Ultimately, the thesis played out. Oil went down. We nailed the direction.

But being right on a commodity price direction does not mean every argument that got you there was flawless, and a few people reminded us of exactly that.

We also received genuinely constructive feedback, which we always welcome, as we believe that is how analysts, fund managers, and anyone serious about this business improve over time. These discussions were highly valuable and are also part of why we are reassessing our view on oil prices today.

Table of Contents

Introduction: The Next Inflection in Crude Oil

What History Tells Us About Oil

2.1 How Iran’s Leadership Thinks About Oil

2.2 Oil Trade Under Iran’s Revolutionary Government

Supply vs Demand: Who Is Winning?

3.1 Where Global Oil Supply Stands

3.2 The Reality of Global Demand Growth

How Oil Inventories & Reserves Look

4.1 China Has Plenty of Oil in the Tank

4.2 The U.S. Has Limited Room for Error

Oil Prices: The Road Ahead

5.1 Scenario 1: Strait of Hormuz Reopens in June

5.2 Scenario 2: Strait of Hormuz Reopens in July

5.3 Scenario 3: Strait of Hormuz Reopens in August

5.4 Scenario 4: Strait of Hormuz Reopens in September

Our Final Take on Oil

2. What History Tells Us About Oil

We believe the current bullish oil narrative relies heavily on geopolitics while underweighting the physical market. In the short term, oil prices can react materially to headlines. Trump says something and oil moves higher or lower.

Iran responds and it moves again, higher or lower. That said, while geopolitics is always part of the equation, it isn’t what defines the underlying balance. The key drivers remain physical flows, production trends, and demand trends.

As the legendary oil trader Marc Rich (often referred to as the “King of Oil” and founder of what became Glencore) used to say, “I don’t trade politics, I trade oil.”

We believe the key dynamic is that production growth outside OPEC provides only a limited additional buffer and does not fully offset current supply disruptions, a factor we overlooked in our previous analysis.

As a result, while we remain bearish, the balance of risks is now less one-sided than before. The main offset instead comes from weaker demand across key consuming regions, which is declining in response to higher prices.

This creates a more complex setup than consensus positioning suggests and helps explain the relatively muted price action despite frequent references to supply disruption and elevated inventories.

Our initial view overemphasized the speed of demand destruction. We expected greater pressure in the $100 to $110 range, but demand has proven more resilient, with clearer signs of weakness likely emerging as prices approach $120 and becoming even more pronounced above $140.

The main bullish counter-argument remains a prolonged disruption to oil flows, such as a sustained closure of the Strait of Hormuz (SoH) extending through the summer. Even in that scenario, we believe the market retains some near-term defensive buffers, though they are not unlimited and would gradually erode if the disruption persisted into late summer and early autumn, becoming increasingly concerning from a market balance perspective.

China has quietly accumulated a massive strategic stockpile of over one billion barrels, while the US has historically shown a willingness to aggressively empty its Strategic Petroleum Reserve to cap skyrocketing prices.

However, we must also emphasize a key risk that was underweighted in our previous analysis. If the Strait of Hormuz remains closed into August, the market would face increasing supply stress as U.S. reserves would not last indefinitely.

Continued drawdowns would eventually push inventories toward operational minimums, tightening the physical balance and shifting the market regime.

For this reason, our bearish view is time-dependent. If a closure extends beyond the end of July, the depletion of these emergency buffers would materially change the setup, and we would need to reassess our view.

In the meantime, we see these oil reserves acting as a shock absorber. As a result, in most scenarios, politically driven price spikes are likely to run into demand destruction before becoming sustained moves. We therefore remain focused on the physical balance rather than headline volatility.

2.1 How Iran’s Leadership Thinks About Oil

Marc Rich is known for having traded extensively with Iran during periods of heightened geopolitical tension. As he described it: “We bought the oil, we handled the transport, and we sold it. They couldn’t do it themselves, so we were able to do it.”

Despite the strong anti-Western rhetoric coming out of Tehran, Marc Rich observed that oil trade remained highly transactional in practice. In his words, “They were very respectful. They were very correct. They needed to sell the oil, and we were able to buy it. We paid them in a way they could use, and they appreciated that.”

We believe this shows that even under intense geopolitical pressure, oil flows are ultimately driven by economic necessity rather than political rhetoric.

As a result, we view a prolonged and complete closure as a low-probability but high-impact scenario that would become material over time through more severe inventory depletion and extremely tight physical balances.

2.2 Oil Trade Under Iran’s Revolutionary Government

Rich revealed that the Iranian regime knew exactly where its oil was ultimately being sold. As the oil trader described, the regime prioritized cash flow over public rhetoric: “He [Ayatollah Khomeini] told me that he did business with us, and the Ayatollah regime knew I was going to sell it to Israel.”

This period points to a broader pattern in oil markets: even under strong political positioning, trade often remains driven by economic necessity. When fiscal pressures are high, revenue considerations tend to outweigh public rhetoric.

We believe this reflects well how geopolitical tensions interact with physical oil flows today, including key transit routes such as the Strait of Hormuz, where incentives still strongly favor keeping barrels moving.

3. Supply vs Demand: Who Is Winning?

The debate over whether supply tightness or weaker demand is driving the physical market has become more pronounced. Some sell-side research points to historically low inventories and scenarios of Brent reaching $140–150 per barrel, while macro analysis argues that such outcomes would normally require stronger confirmation from physical flows. In our view, the market is currently shaped by both tighter supply conditions in specific regions and more resilient demand, making the balance more nuanced than either extreme narrative suggests.

In practice, the key offset is demand resilience on one side and visible weakness in consumption on the other. While supply conditions remain tight in specific regions, broader demand trends are softer, which helps explain why prices have not sustained higher levels despite repeated supply disruption headlines.

Looking forward, short-term volatility linked to geopolitical disruptions, including risks around the SoH, may continue to create spikes in pricing. However, institutional estimates still point to a market that rebalances into surplus once logistical conditions normalize, implying that higher prices would eventually need to be met with demand adjustment or production response.

Also, we wanted to point out that it is a bit strange, while not surprising to us, that many investors seem to want much higher oil prices. Of course, the goal is to make money, but the higher oil goes, the more it hurts demand. Sustained levels of $150–200 would ultimately be negative for demand and global growth. It feels like, in practice, they are implicitly betting on a very extreme scenario.

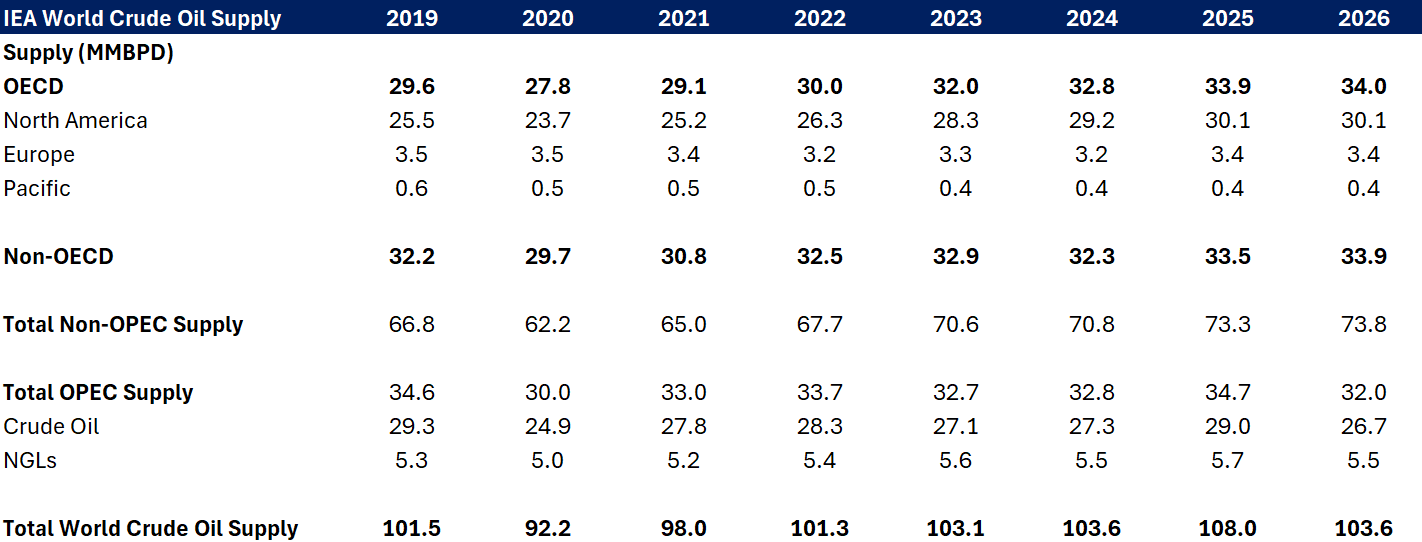

3.1 Where Global Oil Supply Stands

The IEA data provides a useful reference point, but it does not capture the full complexity of global oil flows, which are inherently difficult to measure precisely in real time. This is also supported by periods of SPR releases, which have helped stabilize markets but cannot be sustained indefinitely.

Within that context, non-OPEC supply has increased from 66.8M bpd in 2019 to 73.8M bpd in 2026, driven largely by North America, which rose from 25.5M bpd to 30.1M over the same period, providing a consistent buffer to global markets.

The table shows that global oil supply is not falling even though OPEC is producing less. Higher production from non-OPEC countries offsets that decline, keeping total supply broadly stable at around 103.6M bpd in 2026.

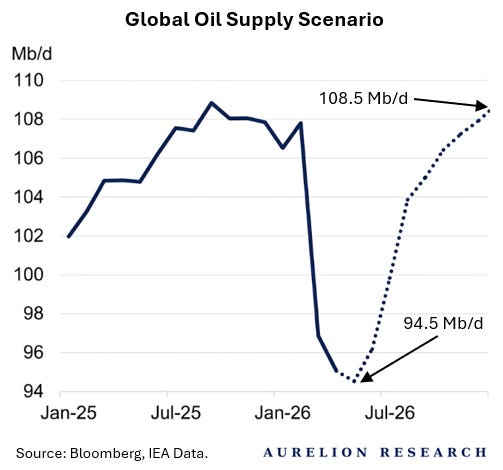

The following scenario illustrates how a supply disruption could evolve. Global supply declines to a low of 94.5M bpd in April 2026, reflecting the immediate impact of a transit chokepoint disruption before recovering thereafter.

However, the projection shows a rapid recovery, with production climbing back to 108.5M bpd by 2026 end. We believe this recovery is already reflected in prices, as the market is assuming a normalization of flows through the SoH as early as July or August. This explains the muted price action, as positioning already anticipates the return of disrupted barrels and the gradual rerouting of exports.

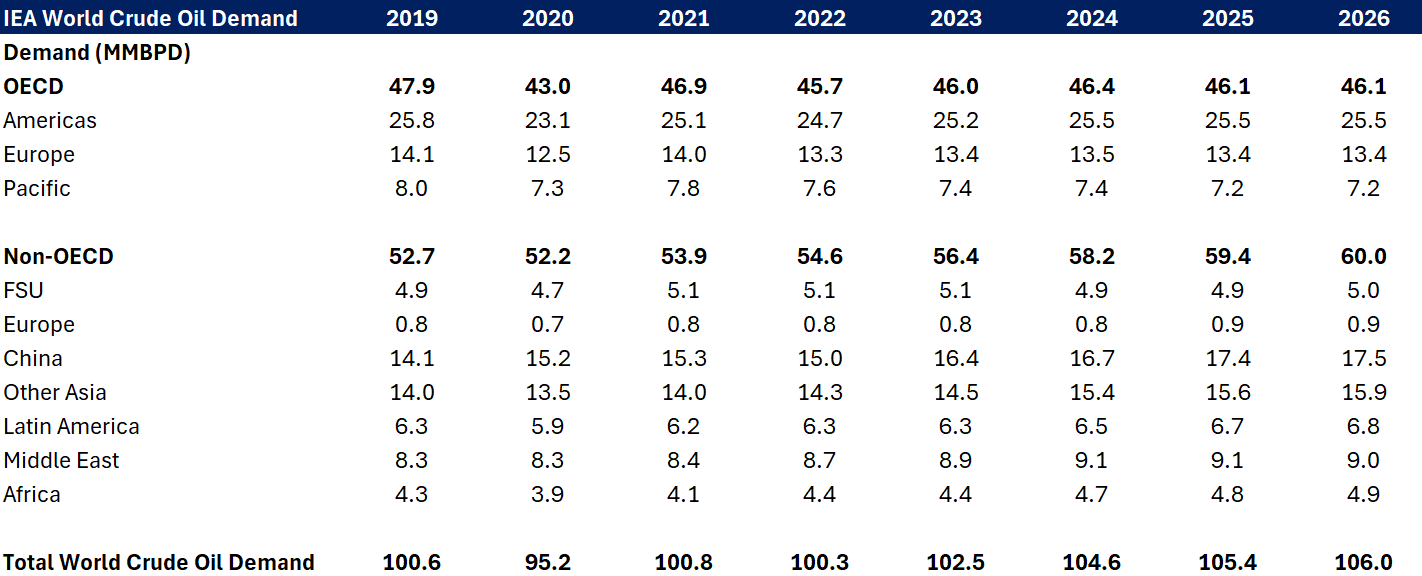

3.2 The Reality of Global Demand Growth

The baseline annual metrics show global oil demand increasing modestly rather than accelerating. Total World Crude Oil Demand has risen from 104.6M bpd in 2024 to an estimated 106.0M bpd in 2026. This limited progression is consistent with a gradual flattening in consumption, particularly across mature markets.

OECD demand remains broadly stable at 46.1M bpd, while China’s growth has essentially stalled, moving from 17.4M bpd in 2025 to 17.5M bpd in 2026.

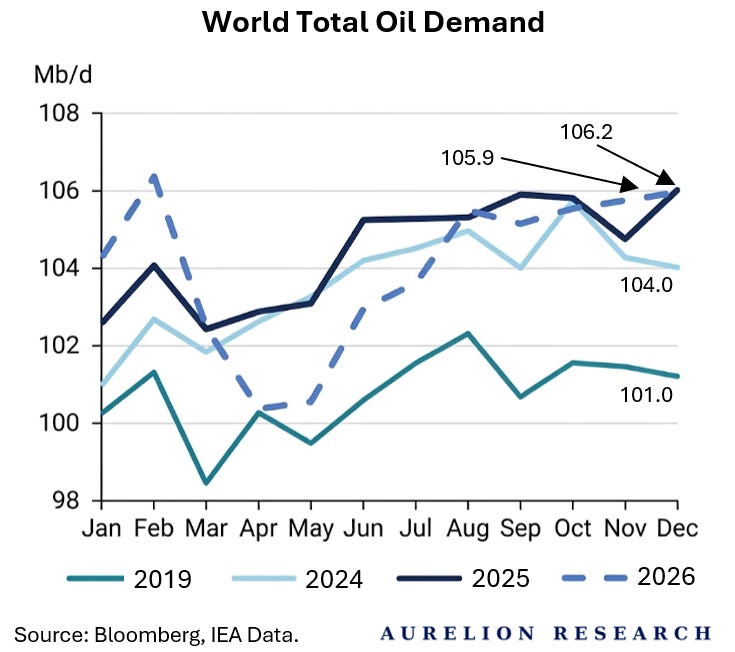

The seasonal trends show how demand evolves over the year.

After an early peak in February 2026, consumption declines through the spring months, bottoming near 100.5M bpd in April and May, reflecting the typical seasonal slowdown in a softer overall demand environment.

The pattern then typically recovers toward year-end levels of ~106.2M bpd, consistent with normal seasonality. However, what stands out is not the level itself, but the lack of upside acceleration relative to prior cycles. We believe this reflects a market where demand is becoming more price-sensitive, which helps explain why sustained higher prices tend to lose momentum more quickly.

4. How Oil Inventories & Reserves Look

So far, the global market avoided a massive shortage because of a few temporary fixes. Storage tanks are being drained, ships are taking longer routes around the Middle East, and Western countries are exporting more crude.

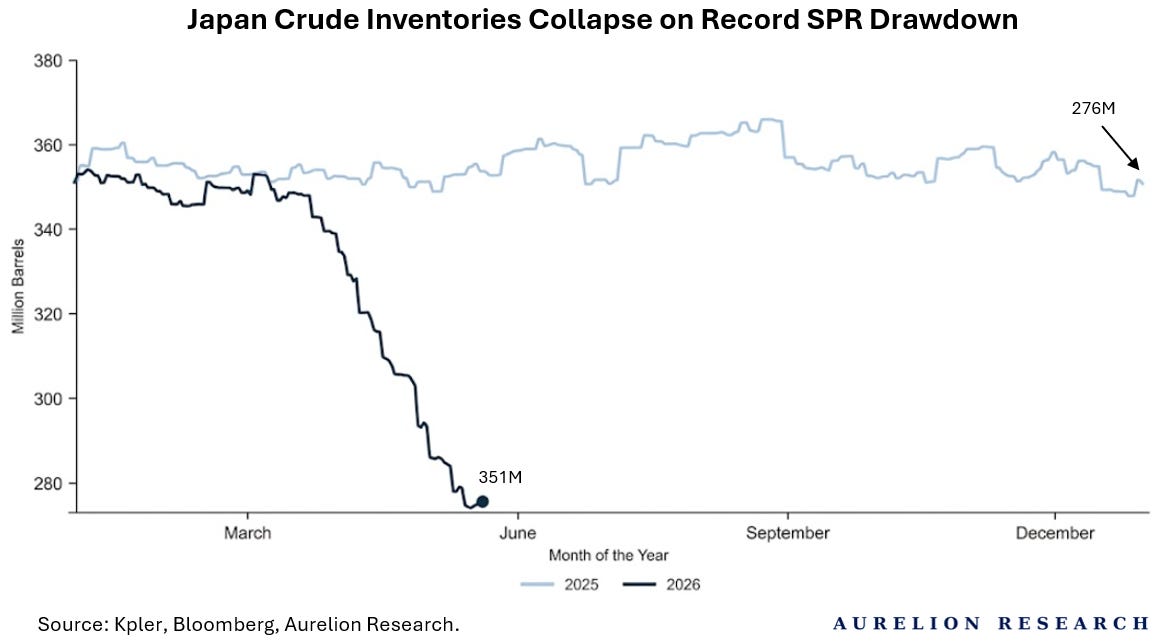

Recently, Japan’s crude inventories have broken away from historical trends. While 2025 levels remained stable around 351M barrels, 2026 data shows a sharp and unusual decline. Following a significant drawdown of its SPR, inventories fell from March highs to nearly 276M barrels by the end of May.

This dramatic draining of emergency reserves suggests the market has been operating on borrowed time. Once these strategic drawdowns slow and shipping lanes normalize, the return of normal flows will meet a global market that may lack the capacity to absorb them. This is also why we believe a reopening of the Strait of Hormuz, even partially, is becoming increasingly important.

Yet, focusing only on these reported oil inventories doesn’t tell the whole story, because relying strictly on reported figures misses a critical piece of the puzzle.

One of the true reason the physical market hasn’t completely broken is the volume of unreported flows, such as shadow fleets and alternative supply channels, quietly moving barrels outside the official reporting channels.

While the reported numbers make it look like there is very little room for error, these hidden barrels help absorb the impact of geopolitical shocks. This keeps the real-world market more insulated than the official inventory data suggests.

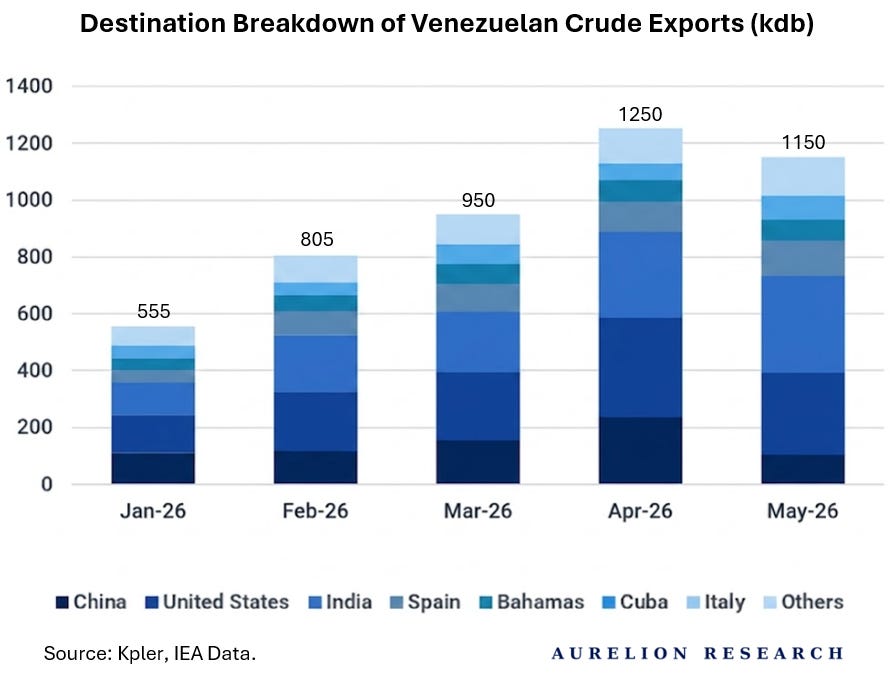

And here is some unexpected hope if things get really ugly, a scenario we didn't anticipate for 2026. We could potentially end the year with both Venezuelan and Russian oil either unsanctioned or seeing very loose enforcement, a prospect that seemed highly unlikely at the start of the year.

Venezuela’s crude output recovery is no longer speculative. Production rebounded swiftly following the capture of President Maduro and the lifting of the US naval blockade, reaching around 1.25 Mbd this month.

Driven by policy shifts in Washington and the issuance of new operating licenses, Venezuelan output has responded quickly, with production trending toward 1.5 Mbd by 2027. Current forecasts point to an increase of roughly 600,000 bpd from recent lows, bringing output to a near-term target of 1.3 Mbd.

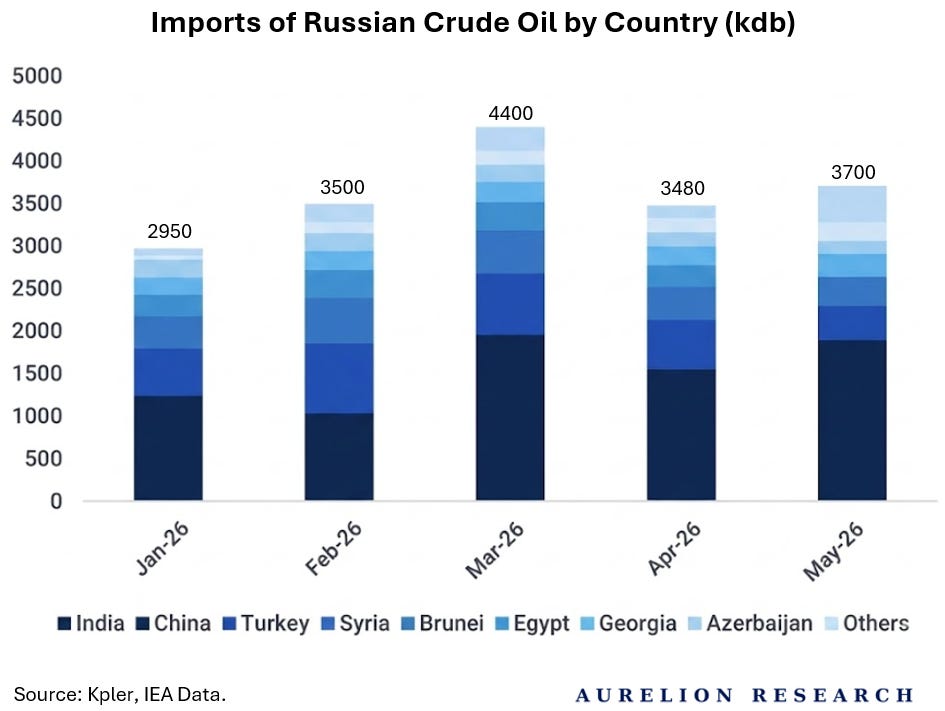

We can also see clear supply resilience in Russia, where seaborne exports have held steady at nearly 3.5M barrels per day. Even with ongoing Ukrainian drone attacks targeting key refinery and port infrastructure, Russian oil is flowing.

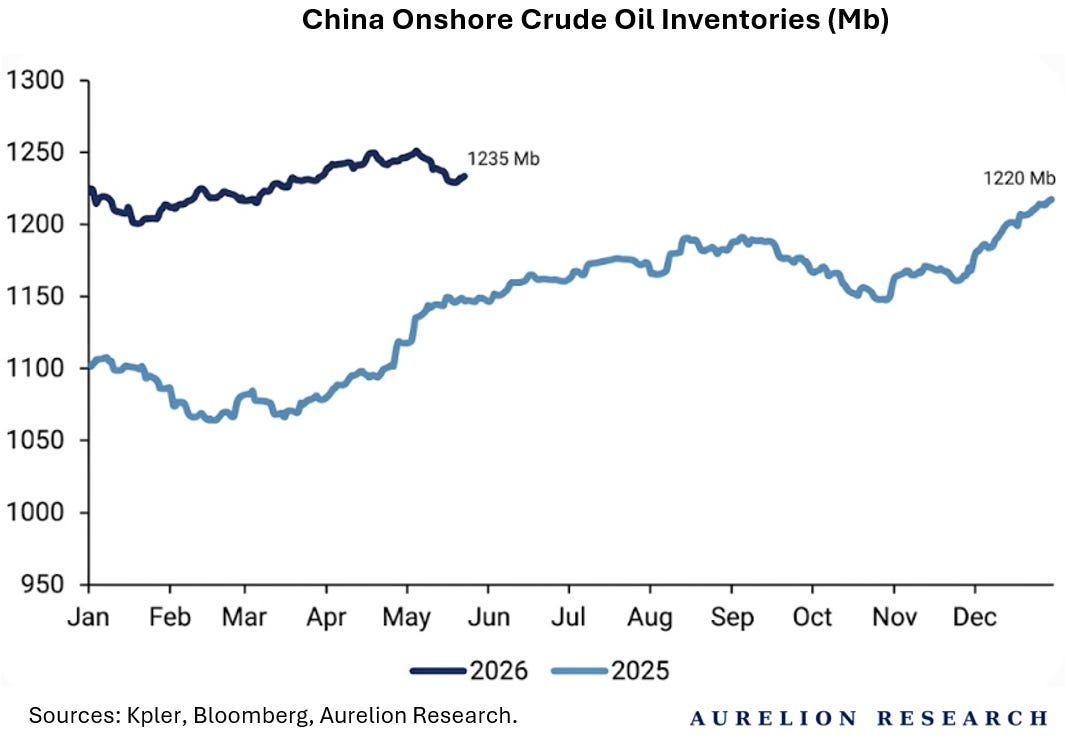

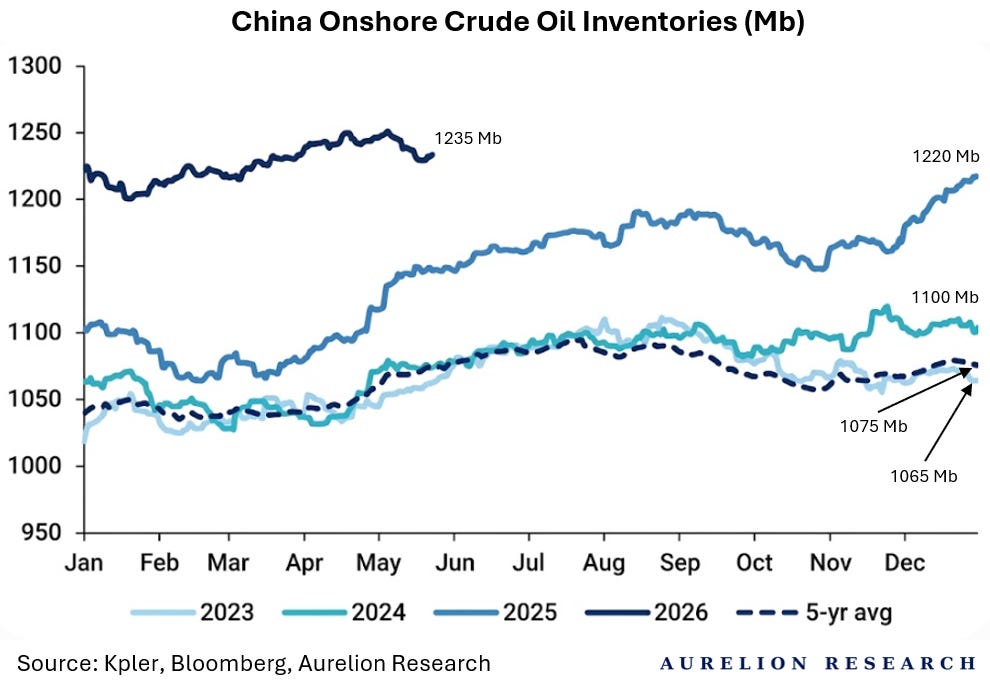

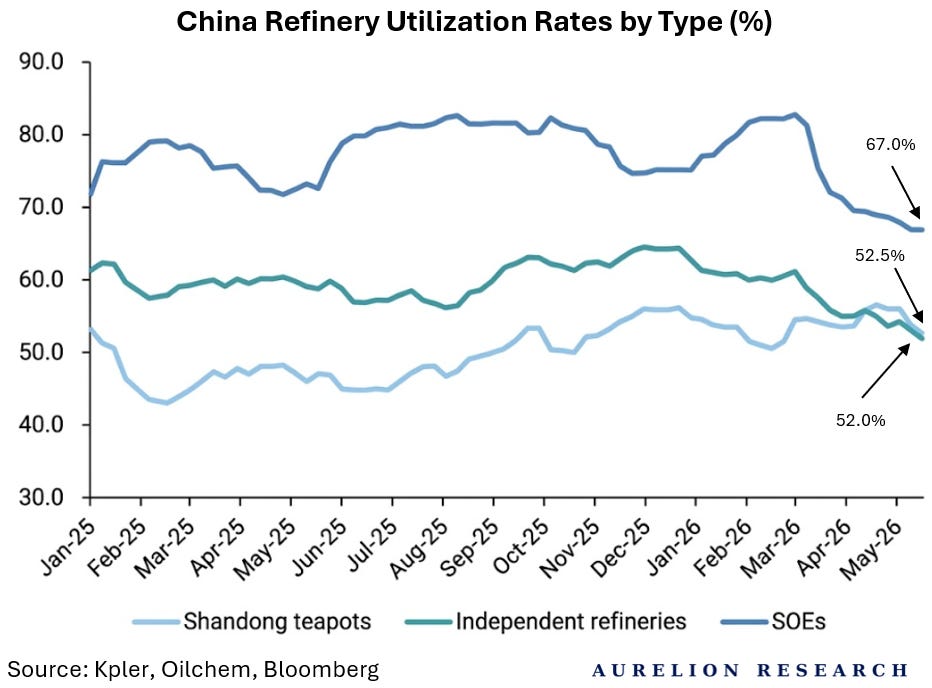

4.1 China Has Plenty of Oil in the Tank

Asian refineries are cutting back fuel production as margins weaken. However, the key point is that Chinese demand for refined products has not fully recovered, leaving a visible gap in regional demand.

We expect this trend to persist for some time.

Chinese refiners are keeping operations muted and remain on the sidelines. State-owned majors such as Sinopec plan to keep production flat through June and July. Typically, summer marks peak driving season and stronger fuel demand, but this year they are largely not following the usual seasonal pattern.

The issue is that refining in China is a difficult business right now.

High pump prices and a weak economy are weighing on consumption. On top of that, the accelerating shift toward electric vehicles (EVs) is further eroding what should be peak seasonal demand. The data shows that major state refiners missed transportation fuel sales targets in both April and May.

Despite production already being cut to multi-year lows, gasoline and diesel inventories remain near two-year highs. Supply is still exceeding domestic demand for transportation fuels.

To survive this, refiners stopped buying expensive crude.

That helped margins recover from a disastrous -$60/bbl in mid-April to -$2/bbl today. Even so, we believe Chinese refiners are unlikely to meaningfully increase throughput while they are still losing money on every barrel processed.

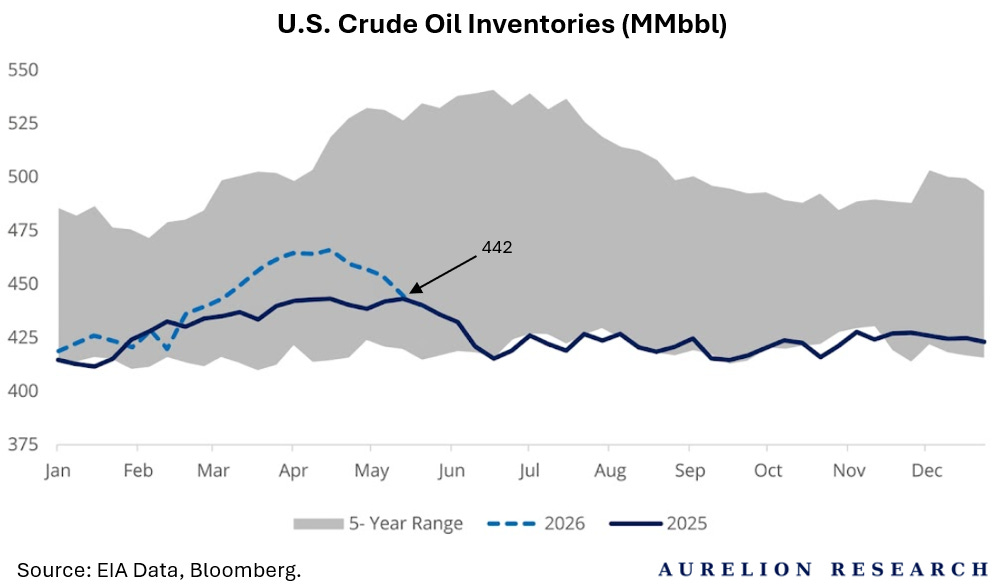

4.2 The U.S. Has Limited Room for Error

We would like to say official inventories are not approaching low levels, but the reported data suggests the Western safety buffer is gradually tightening.

Commercial inventories sit at ~442M barrels, near the lower end of the 5-year range, reducing the market’s flexibility to absorb disruptions when physical flows tighten. Despite this, we remain bearish on oil prices, as we expect the Strait of Hormuz to reopen. However, we believe near-term conditions are still tight enough that the market cannot comfortably absorb additional shocks.

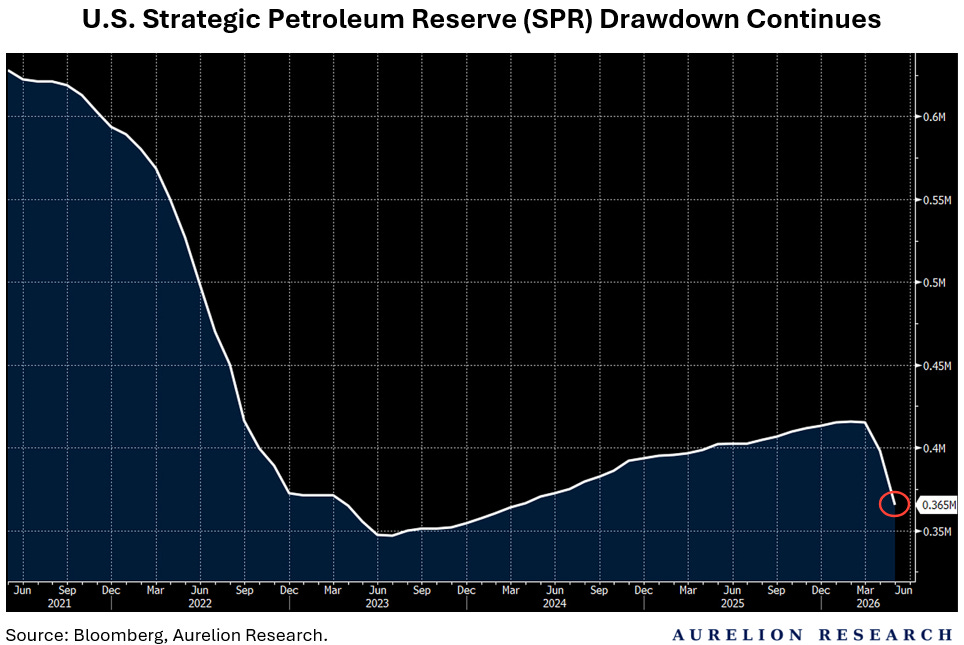

The SPR provides an additional layer of flexibility, though it has been materially reduced to ~365M barrels. Its role as a stabilizer remains relevant, but its ability to respond to a sustained disruption is more constrained than in prior cycles.

In our view, the SPR primarily buys time rather than offsetting a prolonged supply shock. This aligns with our earlier assessment that the situation was less extreme than initially feared, while still acknowledging that resilience fades the longer a disruption persists. Over time, economic incentives always matter.

A prolonged closure would represent an even more significant loss of revenue for Iran than current conditions, creating a financial incentive to restore flows and increasing pressure on key stakeholders to support a resolution.

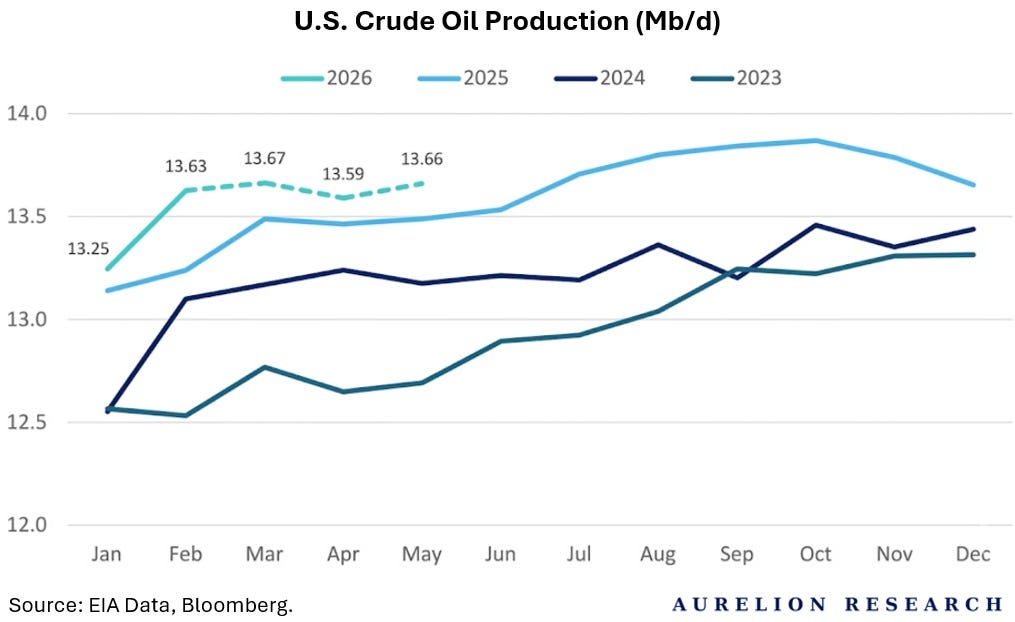

Now, let’s look at U.S. oil production, which looks much better than the SPR.

The production trajectory for 2026 clearly looks stronger than it did in prior years, or at least higher. Output is holding steady above 13.6M bpd through May, and we believe moving toward 14.0M in the near term is a reasonable outcome.

While the rapid growth rates of previous cycles have eased, U.S. crude production remains at record highs in absolute terms. We believe this sustained output continues to put steady downward pressure on global oil prices.

This also helps explain why bullish geopolitical narratives often fail to hold. U.S. producers are consistently adding a large base of supply each day, which cushions the impact of disruptions and reduces the longevity of news-driven price spikes.

With output already high, any further softening in global demand would quickly push the market into surplus, reinforcing our bearish view on oil prices.

5. Oil Prices: The Road Ahead

We think oil prices are entering a more uncertain phase, shaped by tight near-term balances, geopolitical risk, and shifting demand conditions. Near-term moves will depend less on narrative and more on how supply and inventories evolve through the summer. It will be an important period to watch.

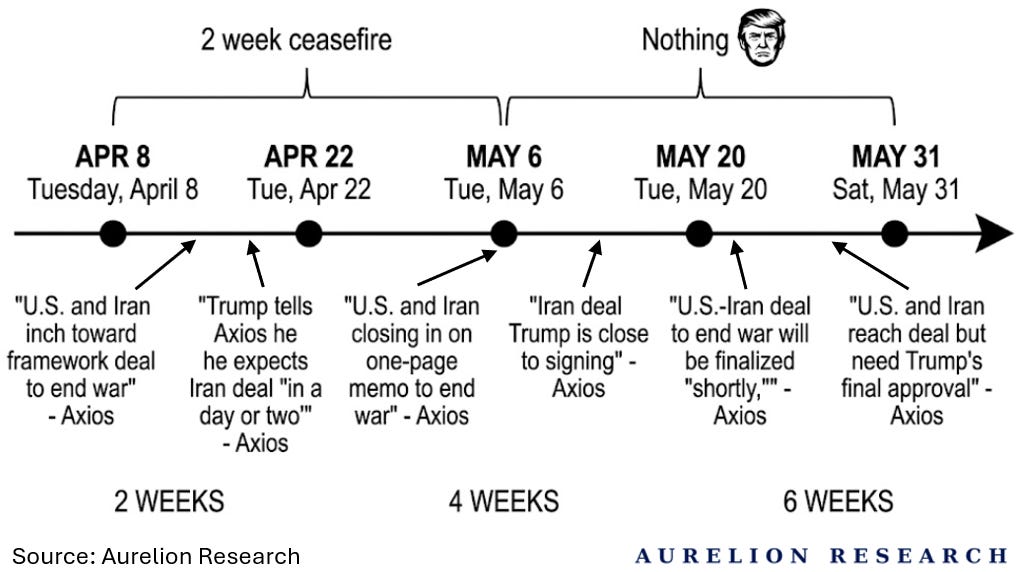

Our view is that the longer the SoH remains closed, the more pressure builds on global oil supply. We expect the Strait to reopen sometime in July, or at least in August. If we move through the summer without a resolution, the market would likely face a much tighter supply setup than what is currently priced.

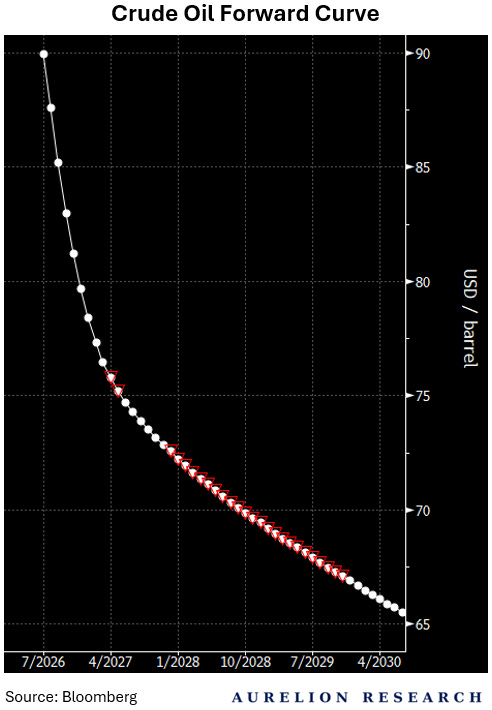

We are not perma bears, despite how some interpreted our last post. Our stance is more balanced. We are cautious on oil under current conditions, as we do not see the current setup leading to higher prices given expectations of a relatively quick reopening. That view is still reflected in the forward curve, where the market is pricing a gradual decline in crude oil prices over the next four years.

In other words, while spot oil remains high today, buyers are locking in progressively lower prices for future crude oil delivery.

Important: Every following oil price scenario is based on WTI crude oil prices in USD, not Brent crude or any other.

5.1 Scenario 1: Strait of Hormuz Reopens in June

We currently see oil trading in a volatile range between $85 and $105, driven by the ongoing US–Iran dynamic. If the Strait reopens in June, which represents our best case scenario, we would expect prices to steadily move down. However, we do not expect a total collapse to $60-65.

Under this best case scenario, we see oil at $80.

5.2 Scenario 2: Strait of Hormuz Reopens in July

A July reopening aligns with current baseline forecasts from geopolitical strategists, which assume the chokepoint remains closed through the end of next month. Under this timeline, we believe marginal price gains would likely peak early in the third quarter as congestion in the Persian Gulf begins to ease.

An early summer resolution would have a meaningful market impact. The release of barrels held up behind the chokepoint would immediately relieve the physical tightness that has characterized the first half of the year.

Under this scenario, we see oil at $85.

Because global demand cannot comfortably sustain these elevated price levels over the long term, a July normalization would likely trigger a relatively rapid correction toward historical averages, catching aggressive paper traders off guard.

5.3 Scenario 3: Strait of Hormuz Reopens in August

An August reopening pushes the timeline further into the summer and tests the limits of reported global inventories. We think this delay redirects attention toward political timelines, particularly as domestic cost of living pressures rise ahead of the upcoming US elections.

While Washington retains military options to attempt an earlier reopening, extending the closure into August means navigating a fragile ceasefire environment where the risk of indirect escalation remains elevated.

Financially, an additional month of closure forces commercial buyers to continue drawing down emergency reserves and rely more heavily on alternative, higher cost supply channels. Prices would likely remain high for longer, but would still face a clear ceiling rather than a sustained breakout.

Under this bear case scenario, we see oil at $100.

When the Strait eventually reopens in August, the return of normal flows would hit a market where demand has already been weakened by months of high costs, triggering immediate downside pressure on prices.

5.4 Scenario 4: Strait of Hormuz Reopens in September

A September reopening would trigger severe market tighteness, as a prolonged closure would deplete strategic reserves and drive widespread panic around global supply availability. Under this scenario, we see WTI at $110.

6. Our Final Take on Oil

W believe the market is currently driven more by headlines than by the underlying physical balance. Strong non-OPEC supply continues to provide a meaningful buffer to global markets, while demand has remained more resilient in the short term but shows signs of regional weakness.

Strategic reserves and inventories continue to absorb shocks, limiting the pass-through into prices. As a result, the market looks more balanced than the prevailing narrative suggests. We therefore remain focused on physical flows, where supply still appears sufficient in most reasonable scenarios.

The world needs lower oil prices to keep growing.

Reasonable oil prices have historically supported higher quality of life.

Find how our stock portfolio is positioned here.

Our Latest Commodity Research Report:

What you get as a paid subscriber:

Stock ideas, thematic research, commodity, and more.

Full access to our entire library of reports. Currently 100+ reports.

Live access to our actively managed portfolio: the Aurelion Index. All stocks are backed by in-depth research.

Access to our real-time trades & rationale. As a reminder, this is not investment advice, please conduct your own research.

Questions? Reach us directly on Substack or at contact@aurelionresearch.com.

Could you explain how a squeeze doesn't play out when the Cushing Oklahoma oil reservoir doesn't happen when it reaches it's functional bottom at the end of June to early July? We have thousands upon thousands of futures contracts created for WTI crude and what happens if a few people/refiners want physical delivery instead of rolling them over but there's no barrels? Under the contract they are mandated to deliver the barrels. They have to buy inventory at any price to fill their obligation or their broker will liquidate their account to settle the contract. A contract is a contract and most WTI futures contracts that are settled and want physical delivery go through Cushing.

Transiting VLCCs through the SoH at prewar volumes is not a light switch, it’s a well-choreographed waltz that has been massively disrupted. First you need a fairly reliable durable peace, not just an MOU. Insurance companies and ship owners don’t relish transit with mine and drone risk. Clearing mines takes time. You have to restart shut in wells. You have to line up a couple thousand hulls, and scrape off some barnacles. It will also take weeks-to-months for those barrels to hit their global destinations. I’m leaving out other obstacles, but even a peace deal today means the SoH maybe reaches 70% “open” by August at the earliest, probably September. Shouldn’t September be your “optimistic” case, and October the base case and November be the more pessimistic scenario? The substantial shortage of physical molecules until the Fall appears fairly baked in already. Oh, and we’re still seeing kinetic action on a shaky ceasefire and Trump constantly exhorting that we are “so close to a deal” just distorts the price signal when it’s clear that Iran is dragging things out, Israel/Bibi wants to sabotage any deal, and Trump can’t bring himself to sign any deal Iran would currently accept. What are your targets for crude given this additional information?