Don’t Fall for the Oil Bulls

We believe the current cycle of demand destruction in oil markets creates a natural ceiling, limiting how long prices can remain elevated.

The loudest voices are claiming that oil will soar. From what we read and hear, most believe $100 per barrel is only the beginning and that the rise in oil prices is only a matter of time.

We think the complete opposite. We believe oil prices will not sustain these levels and that the market is heading lower. We have held that view since the conflict began in early March, and our approach has been proven right, consistent with our track record of predicting where oil prices are actually going.

The reason is simple: while the consensus chases headlines and extreme forecasts, we stay focused on the actual flow of oil and what the data is saying.

The bull case assumes lost production will trigger a massive shortage, pushing prices toward $150 or even $200. That kind of thinking fails the moment prices stop cooperating with the forecast. You cannot fight where prices want to go. The faster you accept that, the better your chances of being right.

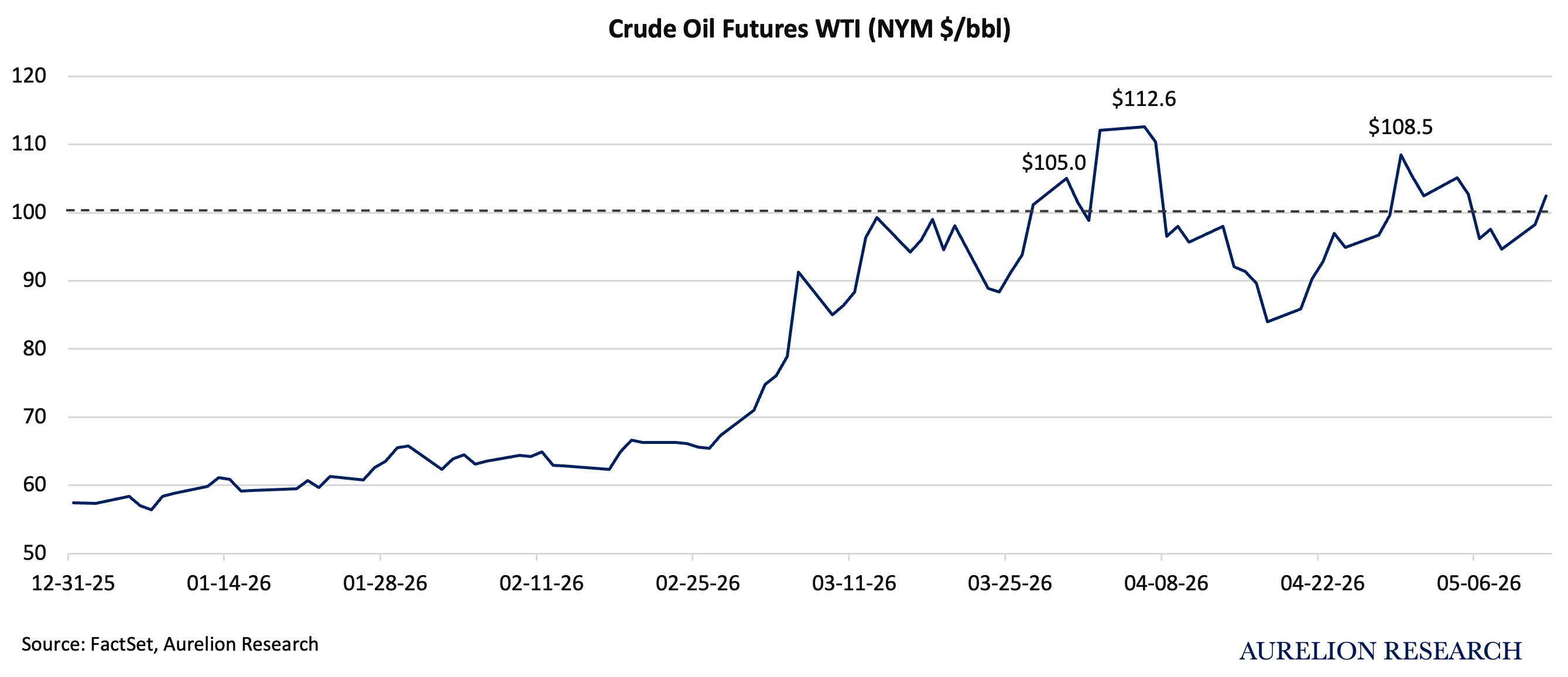

Since the start of the Iran-US conflict, oil prices have moved above $100 WTI on three occasions: $105 on March 30, $113 on April 6, and $109 on April 29.

Each time, prices quickly fell back below $100. Fear moves markets fast, but it cannot hold prices at levels the real economy does not support. Demand, supply, and what the consumer can actually afford are what move oil over time.

We are now back over $100, with prices around $102 on May 12, and we do not expect this level to hold. From the start, we knew that a weakened Iran could not sustain a permanent supply shock. The Strait of Hormuz risk premium pushed the price floor higher, but a higher floor does not mean prices can stay wherever the market wants to push them.

We made this point clearly on March 12, in our LatAm Oil & Gas report:

"We do not see oil staying higher for longer. Iran is now too weakened to sustain this move. While the market is reacting to headlines, the reality of a diminished Iran will eventually bring prices back down. The fundamentals simply do not support a permanent shift to triple-digit oil, and we expect this premium to fade."

Table of Contents:

Introduction: Don’t Fall for the Oil Bulls

How We Analyze the Oil Market

The Importance of Simplification

Why We Have a Contrarian View on Oil

3.1 Trump & the Midterm Pressure

Expertise and the Oil Market

The Market Is Missing the Bigger Picture

How We See Oil Price Scenarios Playing Out

How China Is Rebalancing the Global Oil Market

Geological Constraints & the Cut Profile

Asia Is Moving Away From Middle Eastern Oil

Our Final Take on Oil

1. How We Analyze the Oil Market

Oil is the world’s most important commodity, and it is always the first market people turn to when a major global event unfolds. Our approach is simple: we follow the data and the macro picture, even when that leads us to a contrarian position. That is exactly where we stand today.

We believe oil prices above $100 per barrel are unsustainable. At those levels, energy costs begin to weigh on global growth, and consumers and businesses are forced to cut back on fuel consumption. That drop in demand is what brings prices back down. It has happened before, and we believe it is happening now.

The Evolution of Oil Prices Since 2020

While many focus on supply disruptions, we look at how the global economy reacts to higher price levels. History shows that $100 oil triggers a slowdown that eventually pulls prices back down. This cycle of demand destruction acts as a natural ceiling, preventing prices from staying elevated indefinitely.

Focusing on these economic reactions helps us anticipate shifts that the broader market often misses. When prices rise to a point where consumers and businesses start pulling back, spending data and real demand figures will show it before any forecast does. We watch for those signals carefully.

We believe an analyst should look past the fear and focus on what supply, demand, and inventory levels are actually saying. That is what keeps our positioning grounded when sentiment runs ahead of reality.

2. The Importance of Simplification

Since 2020, our approach to forecasting oil has been to keep things simple. It is easy to become overly bullish on oil. It can lead investors to ignore warning signals or dismiss them entirely, even when they are meaningful. We stay focused on the data and on real-world market conditions.

Our approach proved correct. We remained bearish from the peak in June 2022 all the way to the bottom in December 2025, and we have maintained that same view since the conflict in Iran began in late February 2026. Headlines move fast, but economic reality is what ultimately moves the market.

We believe successful analysis requires paying attention to changes in consumer behavior. High prices eventually reach a point where people can no longer maintain normal consumption. Tracking these real-world signals alongside the data helps identify the limits of oil prices before the broader market reacts.

In our view, keeping that focus on the consumer is what keeps analysis grounded in reality rather than in models that assume demand never breaks.

Key macro takeaway: Successful commodity analysis often requires looking beyond the desk and observing real-world conditions. What happens on the ground usually reflects the true picture more closely than models alone.

3. Why We Have a Contrarian View on Oil

Since the start of the conflict in Iran, we have maintained a bearish outlook on oil. The common bull argument suggests that lost production will lead to a massive shortage, forcing prices toward $150 or $200 as supply fails to meet global demand. We understand the logic, but we disagree with the conclusion.

The problem with many of these forecasts is that they stop adapting the moment prices do not cooperate. You cannot fight where prices want to go. It is like water.

Oil prices have not reached the extreme levels many predicted, and we do not see that changing. A shortage exists, but the data shows it is not severe enough to justify $150 or $200 oil. Markets tend to overestimate how bad a disruption will be and underestimate how fast buyers and sellers find alternatives. We have seen that happen repeatedly, and this time is no different.

3.1 Trump & the Midterm Pressure

Another major reason we are not bullish on oil prices is Donald Trump.

In the United States, midterm elections take place halfway through a presidential term. Every seat in the House of Representatives and a third of Senate seats are up for vote. They are essentially a public verdict on how the president is performing. For Trump, that vote happens in early November 2026, and oil prices are becoming a serious problem.

High energy prices hit American consumers directly, at the gas pump and in their electricity bills. When people feel that pressure in their daily lives, they blame the person in charge. Trump knows this. His approval ratings are already slipping, and the longer oil stays above $100, the more damage it does to his political standing going into November.

This gives Trump a real incentive to find a deal that reopens the Strait of Hormuz and brings prices back down before voters go to the polls. The Iranian regime understands this too. They follow American politics closely, and Trump’s midterm timeline is one of the few pieces of leverage they have left.

The clock is running. If Trump does not find a way to reopen the Strait before the summer, the damage at the polls will already be done. We do not think the market is fully pricing that pressure in yet.

4. Expertise and the Oil Market

A common question is what makes our view different from traditional experts. Oil is a commodity where excessive specialization can create blind spots.

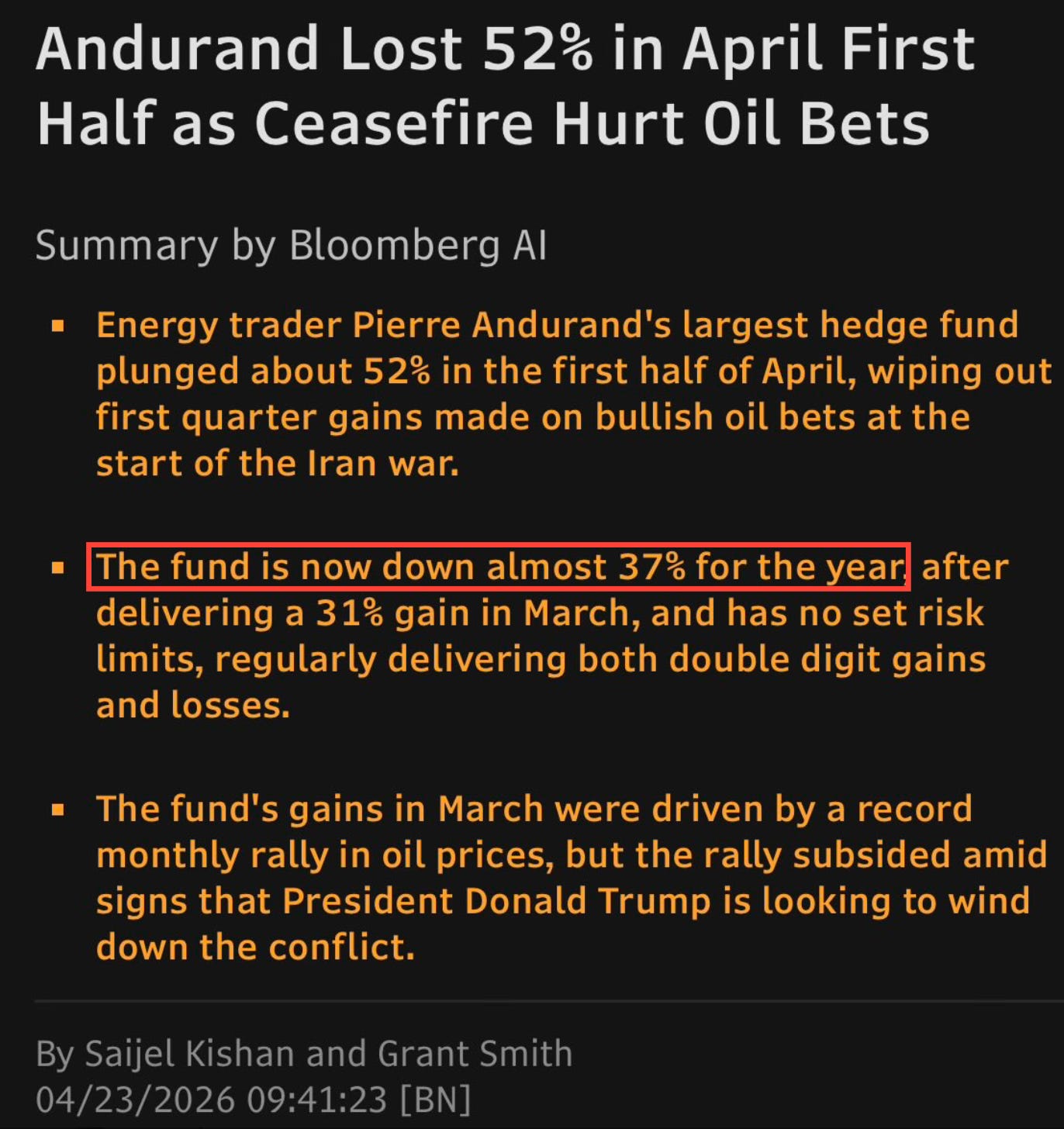

We have seen this repeatedly across the industry, with Pierre Andurand being the most notable example. Andurand is widely considered a genius, holding 4 Masters degrees in fields like Mathematical Physics from Oxford and Astrophysics from London. Yet that depth of expertise can push an analyst toward complex models that end up missing the bigger picture.

The results speak for themselves. His flagship fund was down 15% in 2019, 55% in 2023, and 40% in 2025. The fund gained 31% in March, only to give it all back and more, slumping 52% in just the first half of April as prices retreated.

Volatile performance like that is a sign that the model is fighting the market instead of following it. Being an expert in a single field creates a narrow perspective that prevents seeing how different global forces interact.

Our approach avoids this by maintaining a flexible framework. We look at the entire macroeconomic picture instead of getting lost in the technical details of a single asset, and we believe that is what keeps our positioning accurate over time.

5. The Market Is Missing the Bigger Picture

Most people are only looking at a part of the picture. The data that supports a bullish view is easy to find right now, but the data that challenges it is just as important. We believe that when you look at both together, the case for extreme oil prices becomes much harder to make.

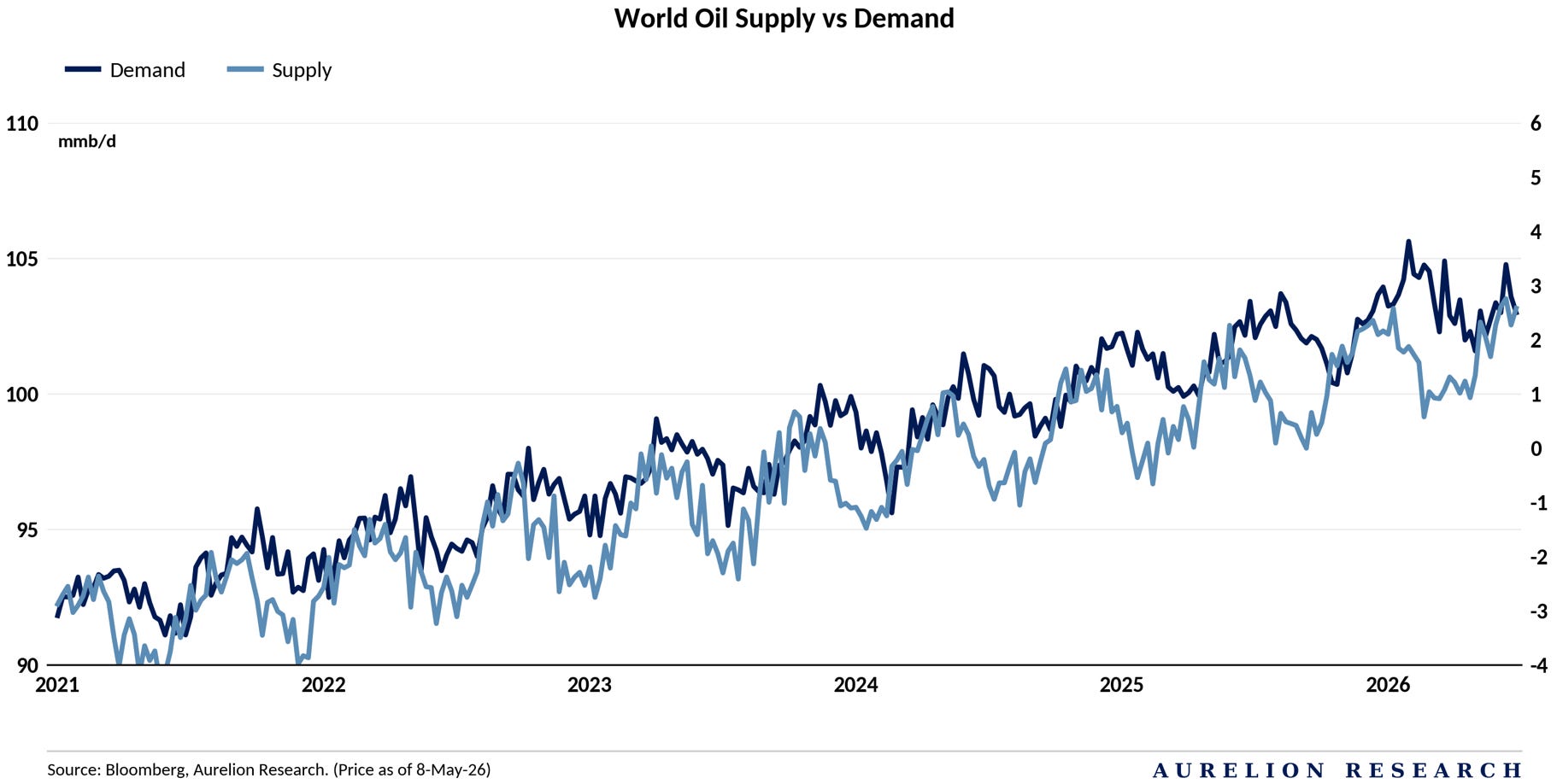

1. World Oil Supply vs Demand

Yes, a supply gap exists. Since 2021, global oil demand has consistently run above supply, meaning the world has been consuming more oil than it produces. That deficit has not disappeared with the conflict. What has changed is the direction. The gap has been narrowing steadily through 2025 and into 2026.

Supply from non-Middle Eastern producers has been growing, gradually closing the distance between what the world produces and what it consumes. The gap is narrowing, and that matters when assessing whether $150 or $200 oil is a realistic outcome. We do not believe those levels are realistic under current conditions.

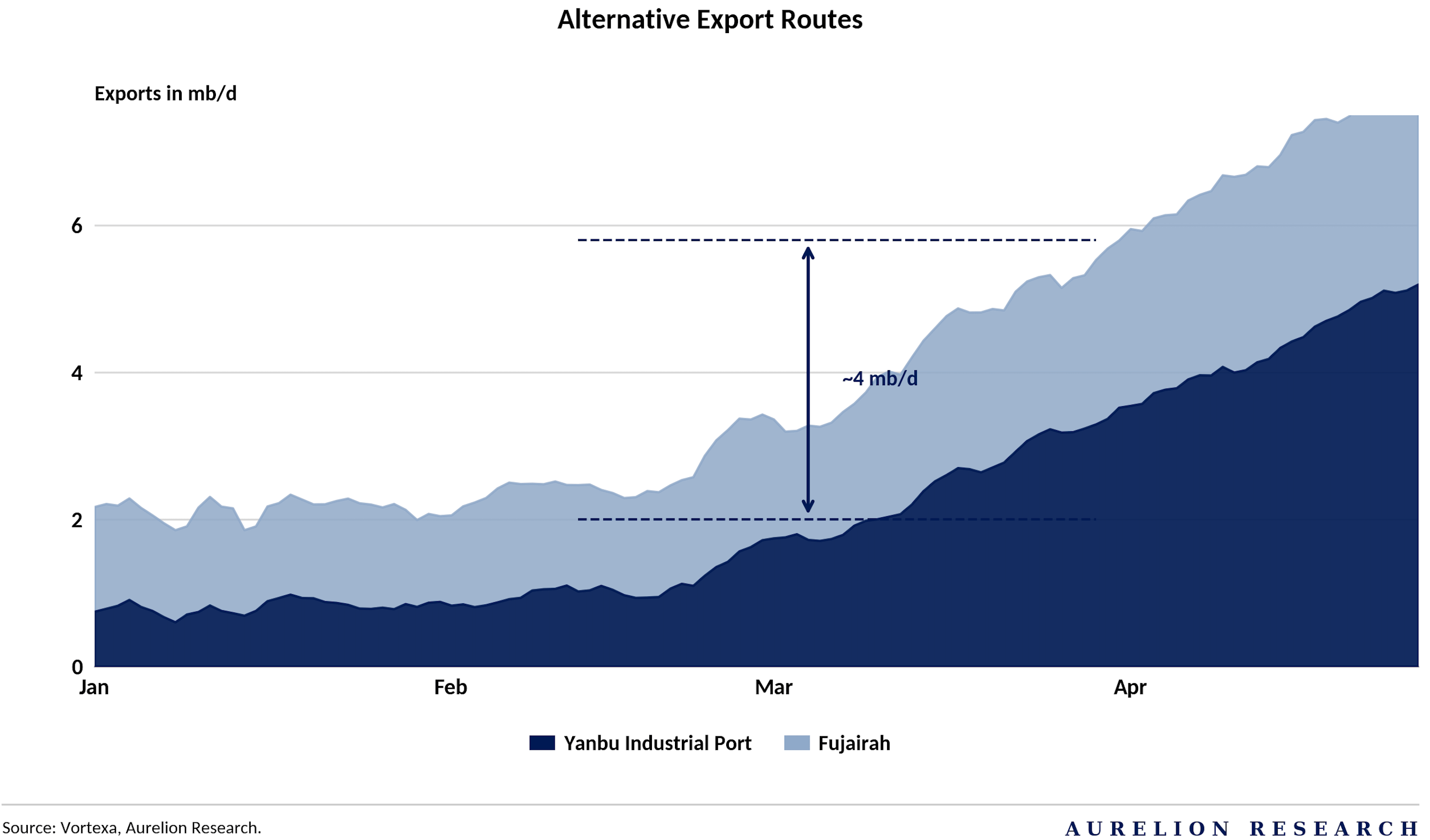

2. Alternative Export Routes

This is the part of the story we think most people are missing. When the Strait of Hormuz closed, the assumption was that the oil stopped flowing.

But producers had other plans. Within weeks, exports were being redirected through two alternative routes: Yanbu Industrial Port on Saudi Arabia's Red Sea coast and Fujairah on the UAE's eastern coast.

The results are significant. Combined exports through these two routes have grown from around 2 mb/d in January to nearly 7 mb/d by April, adding roughly 4 mb/d of new export capacity in just a few months. That is a substantial and rapid adjustment that the market has been slow to price in.

The world adapted faster than most expected. Inventories remain comfortable, the supply gap is narrowing, and producers found alternative routes within weeks. The disruption was real, but the market absorbed it. That is why we do not see a fundamental case for oil staying above $100.

6. How We See Oil Price Scenarios Playing Out

We see oil prices staying in the $85 to $100 range for as long as the conflict in Iran remains unresolved. Even when the Strait of Hormuz reopens, we believe the damage to infrastructure and supply chains will take time to repair, and prices will not fall back to $70 quickly. We do not see oil breaking above $120 to $130 under current conditions. In our view, that kind of move would require the conflict to escalate into a much broader regional war involving multiple countries. We are not there, and we do not think we are heading there.

To support our view, we are going to walk through the data, because we think it challenges most of what you are hearing right now.

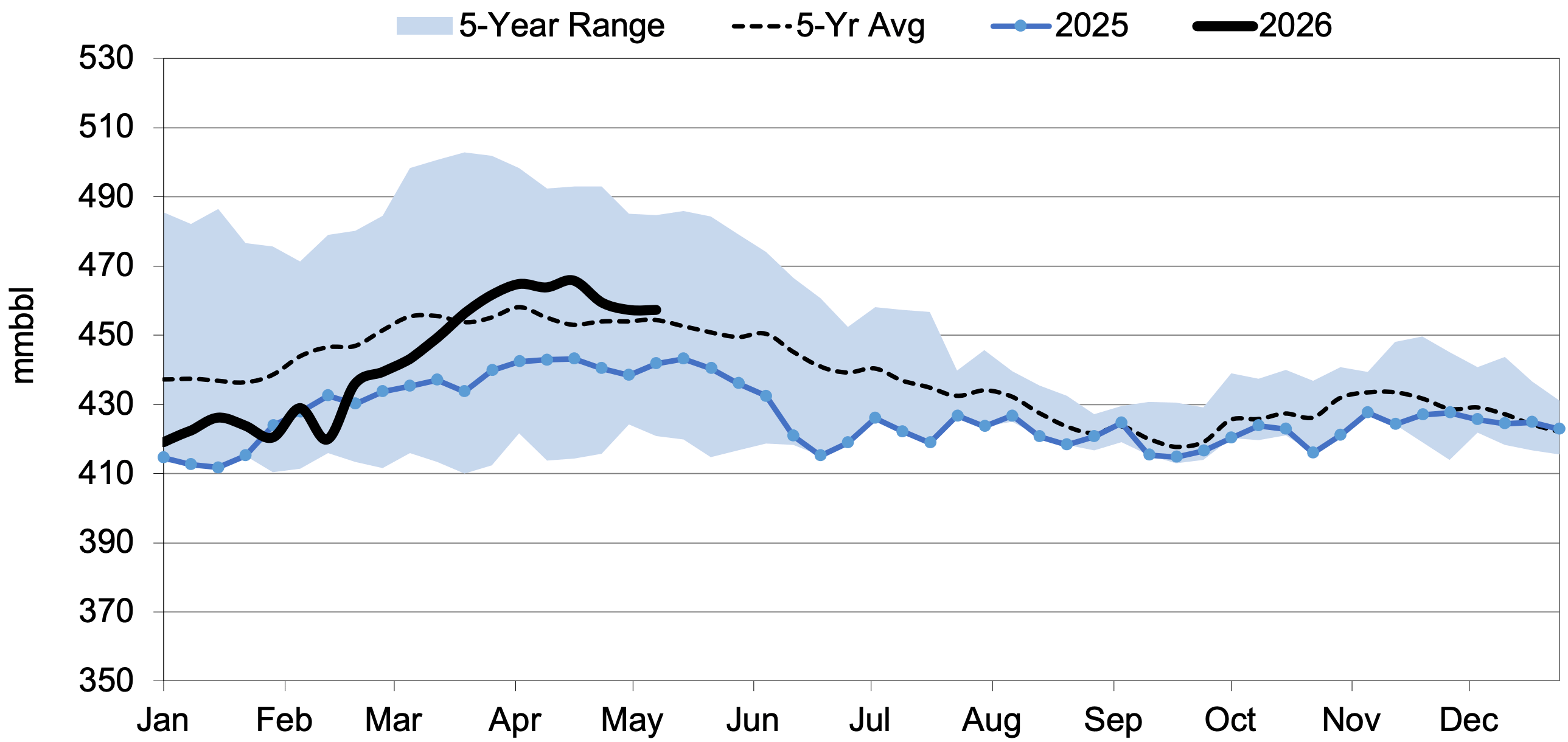

Start with US crude oil inventories. Levels in 2026 have been running above both the 5-year average and 2025 for most of the year, only beginning to ease slightly around April. They are one of the most reliable indicators in the oil market.

US Crude Oil Inventories

The logic is simple: when supply is genuinely tight and demand is outpacing it, stocks fall. Buyers draw down what is sitting in storage because there is not enough coming in to meet their needs. That has not happened here.

Despite the Strait of Hormuz closure, the US has maintained comfortable inventory levels throughout. In our view, that is a strong sign that the actual supply disruption is nowhere near as severe as the market has been pricing in.

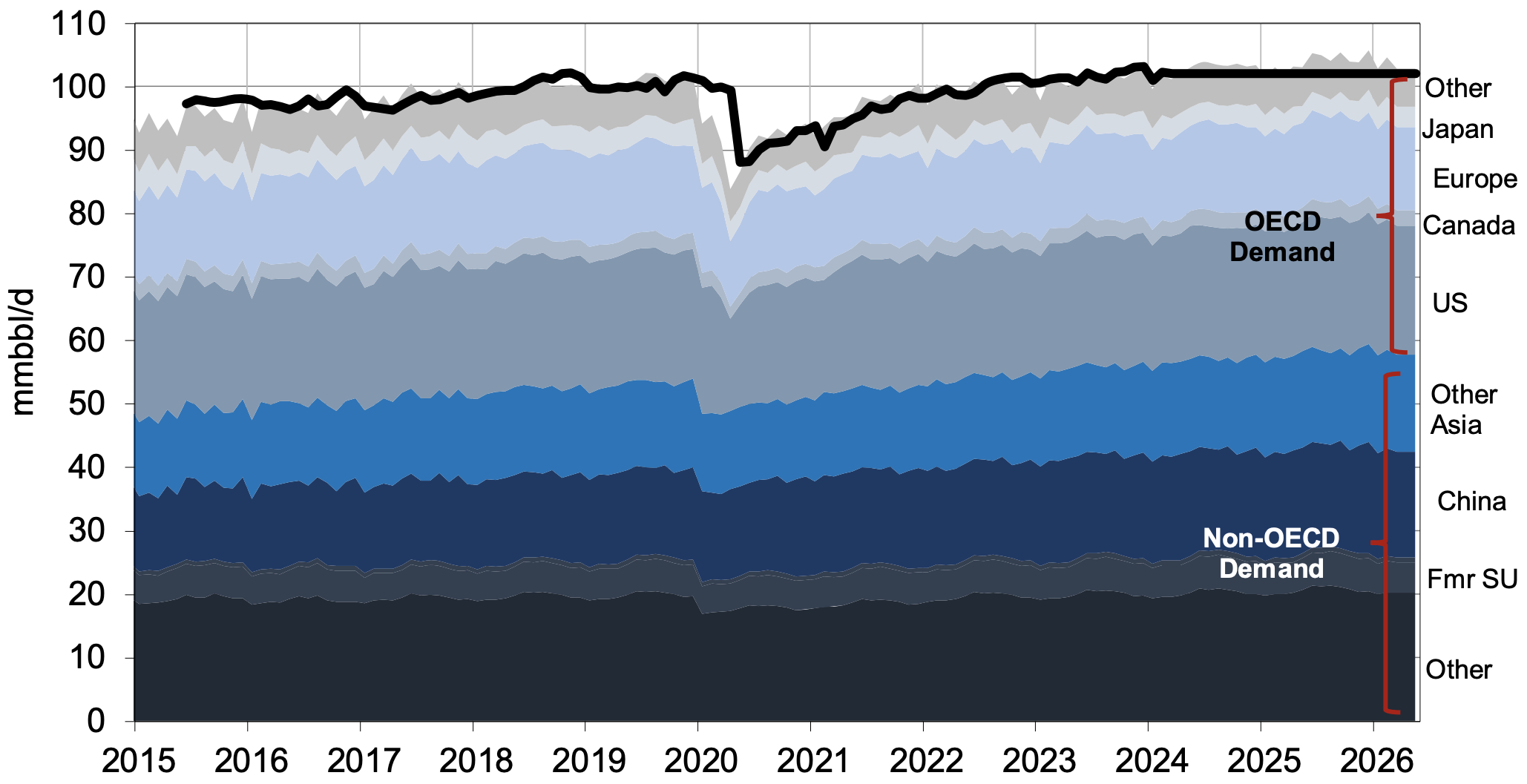

The global picture confirms what the US data is already showing. Since 2022, world crude oil supply has consistently kept pace with demand, and that balance has held into 2026 despite the conflict. The demand line has been flat to slightly declining, while supply from multiple regions, including the US, China, and other non-OECD producers, has remained robust. A market where supply is meeting demand is not a market that justifies triple-digit panic pricing.

World Crude Oil Supply vs Demand

Taken together, these two charts make our case clearly. The fear driving oil prices right now is not supported by what is actually happening in the physical market. In our experience, that kind of gap between sentiment and reality always closes, and when it does, prices follow the fundamentals back down.

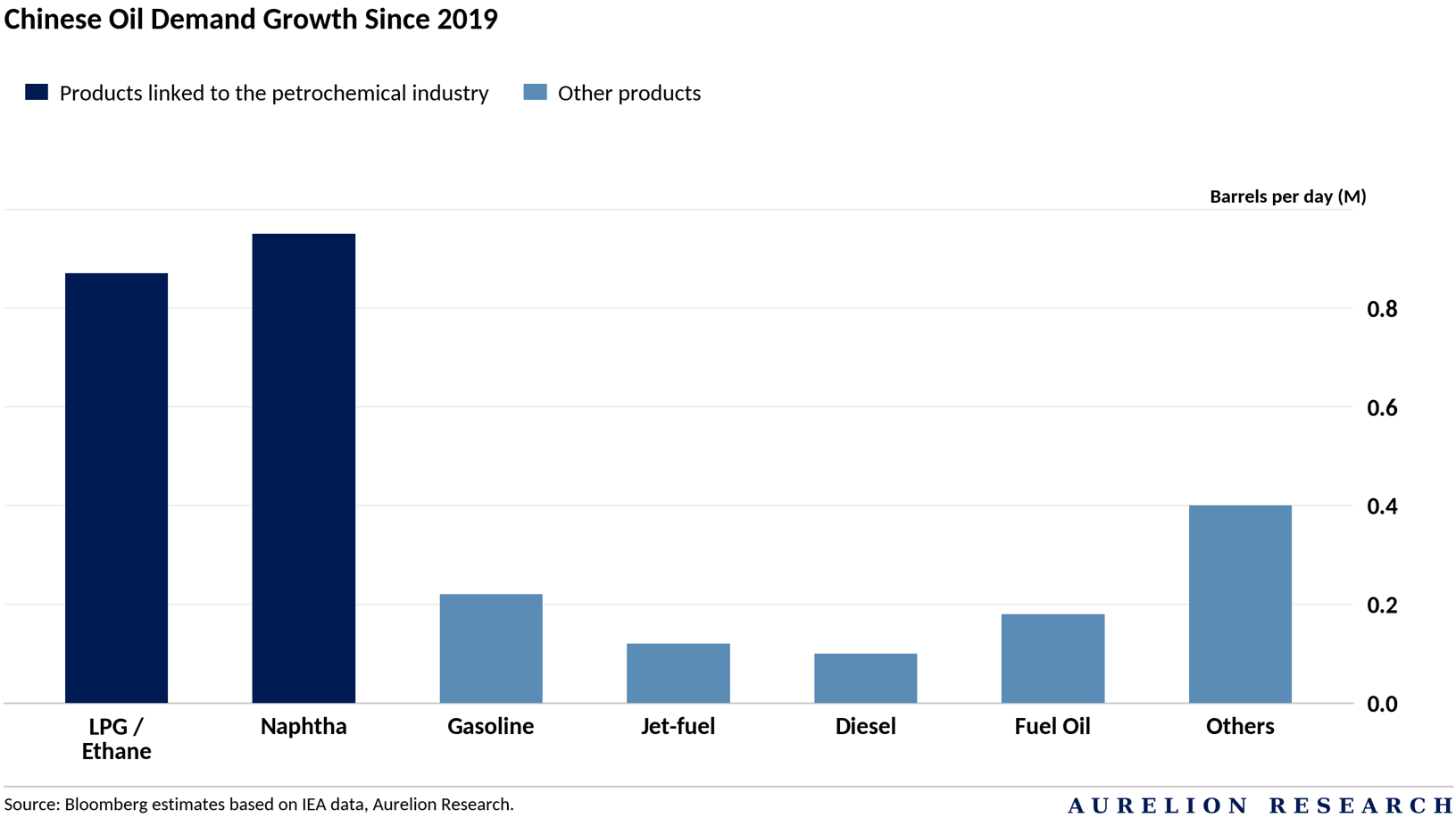

7. How China Is Rebalancing the Global Oil Market

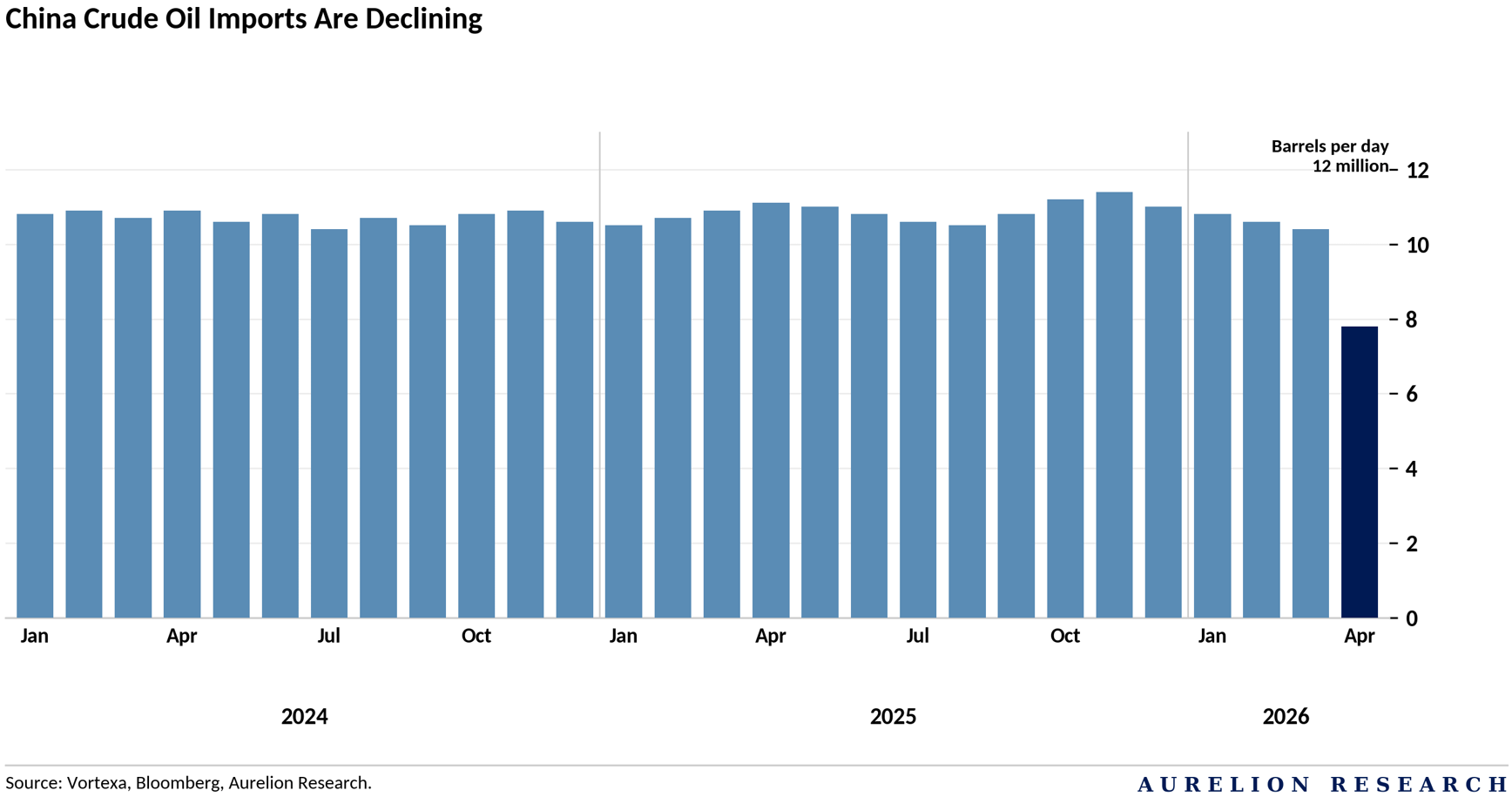

China’s crude oil imports are falling, and this is the first time we have seen a decline of this magnitude since 2024. The easy explanation is to blame the Strait of Hormuz closure, and while that plays a role, the Chinese economy was already slowing before the conflict began.

The Chinese economy is weak. Domestic demand for fuel is soft, and that was true before the conflict began. What China actually needs right now is LPG, ethane, and naphtha, the building blocks for its petrochemical industry. Crude oil and refined fuel products are a different story. We believe demand for both will remain limited, and the import numbers already reflect that.

We believe the difference between what China needs and what it is actually buying is important for anyone trying to read the oil market through the lens of Chinese demand. China is selectively importing what its petrochemical industry needs and pulling back on crude and fuel products.

The Strait of Hormuz disruption adds pressure, but the weakness in Chinese oil demand was already there before the conflict began. We think that ignoring this leads investors to overestimate where oil prices are heading.

8. Geological Constraints & the Cut Profile

Iran cannot cut production evenly across its oil fields. The nature of its reservoirs makes that impossible. Iran relies heavily on mature carbonate reservoirs, mainly the Asmari and Bangestan formations, which naturally decline at between 4% and 12% per year without constant pressure support.

Because oil flows through complex fracture networks in these rocks, any interruption in pressure maintenance can cause rapid and permanent damage. Once that damage occurs, that production capacity cannot be recovered.

Prioritizing Field Survival

Iran’s national oil company (NIOC) is focused on protecting three categories of fields above everything else:

Shared Reservoirs: Fields like Azadegan and Yadavaran stay active because shutting them down risks losing oil to neighboring countries who share the same reservoir.

Pressure Sensitive Fields: Bangestan group fields need constant pressure to keep oil moving through their networks. Any pause risks permanent loss.

Gas Injection Fields: Iran reinjects billions of cubic feet of gas daily to keep fields productive. Stopping that process accelerates decline and reduces how much oil can ever be recovered.

Protecting these priority fields forces cuts onto a smaller group of assets, mainly older onshore southern fields like Ahvaz-Asmari and Gachsaran. These fields offer more operational flexibility, but decades of production have left them requiring more maintenance and less able to absorb sudden changes.

Impact on Export Blends

The geology determines what Iran can actually sell. Bangestan reservoirs produce the heavier Iran Heavy blend, while the shallower Asmari formations produce Iran Light, which normally makes up around 55% of exports. Because cuts are concentrated in specific areas, the mix of oil reaching Asian refineries will shift, with lighter grades likely seeing the biggest reduction.

Outlook: Higher Costs & Uncertain Recovery

With storage full and reservoirs at their limits, production cuts will begin immediately and deepen fast. President Trump has said the blockade stays until a deal is signed. Iran refuses to negotiate while the blockade is in place. That standoff is pushing Iran’s national oil company into costly workarounds.

Keeping reservoirs healthy during a shutdown requires constant well work and pressure management. Rather than shutting assets down completely, the company has to cycle production on and off, which drives operating costs higher.

As oil revenue shrinks, less money is available for the maintenance needed to protect long term capacity. The short term decisions being made today will result in permanently higher costs and lower production capacity for years to come.

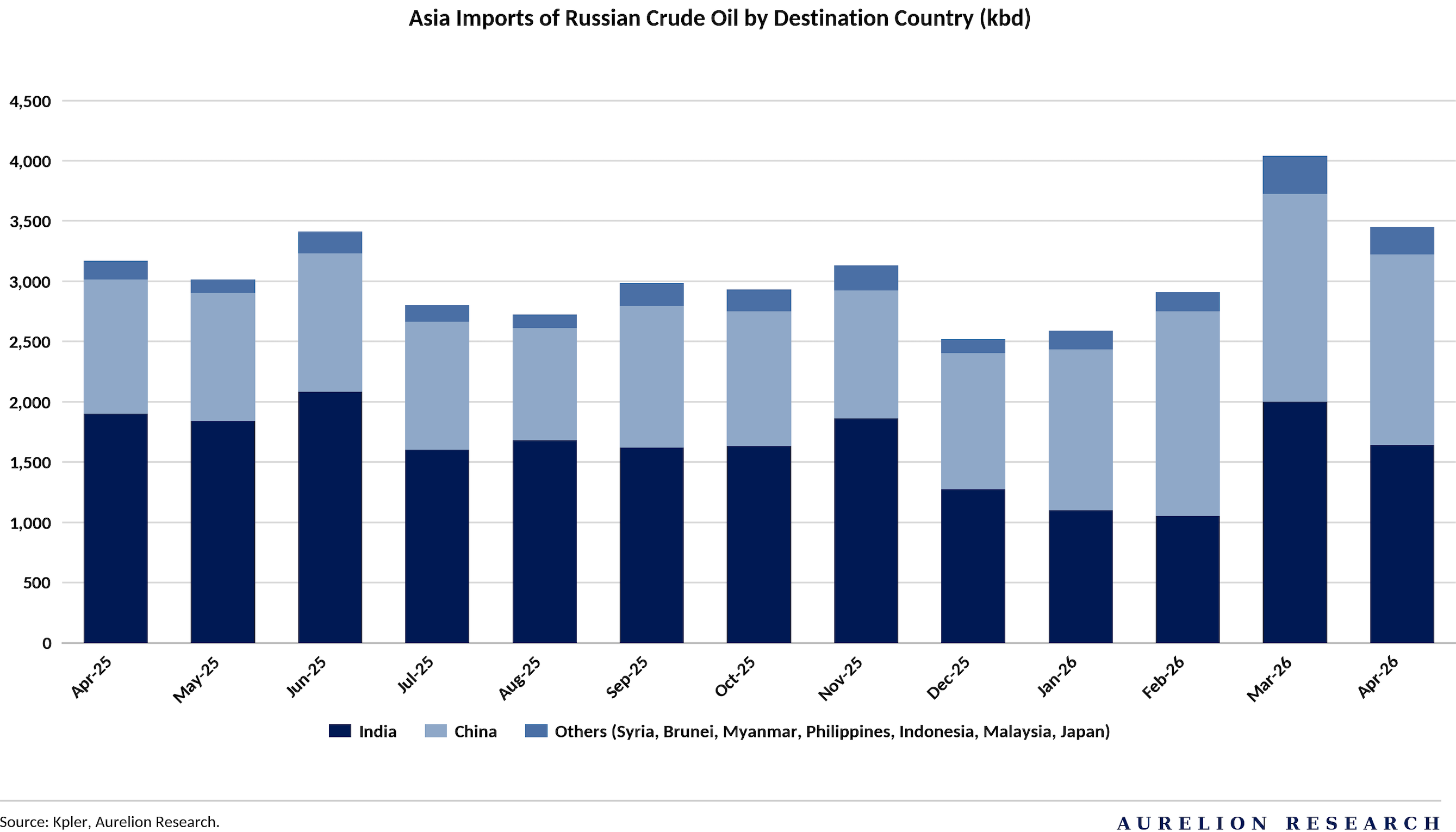

9. Asia Is Moving Away From Middle Eastern Oil

India keeps buying Russian oil, and the volumes are growing. The thinking among Indian refiners is simple: keeping fuel affordable and supply reliable at home is more important than worrying about Western sanctions.

You can see it directly in the numbers. In March 2026, Russian crude imports into India surged by over 900kbd, pushing total Russian volumes to a record 2.25 Mbd. That is nearly half of everything India buys. These numbers have been building for months and show no sign of reversing.

Pricing & Sanctions Risk

Indian buyers are well aware of the sanctions risk and have been factoring it into their pricing for weeks. Premiums for May arrival Urals are currently averaging around $6/bbl above ICE Brent. Even after the record volumes seen in March, April arrivals held strong at 1.5 Mbd. India is paying a premium to keep the oil flowing, and that tells you how seriously it takes supply security.

Southeast Asia Joins In

When the Strait of Hormuz closed, Southeast Asia felt it immediately. With Middle Eastern barrels suddenly harder to access, countries across the region turned to Russia to fill the gap. Malaysia, Indonesia, and the Philippines are all actively securing Russian crude. Philippine refiner Petron bought over 2 Mbbls as an emergency measure. We think these countries will continue buying Russian oil even as the situation evolves.

Making It Permanent

India is now putting the infrastructure in place to keep these flows going. Its shipping authority recently added a Russian insurer to its approved list, allowing Indian tankers to move Russian crude without relying on Western financial systems. Supply security and cost come before anything else for India, and that decision reflects it directly. We believe the shift toward Russian energy in Asia is becoming a permanent feature of how the region sources its oil.

10. Our Final Take on Oil

Our view on oil has not changed. We remain bearish. The shortage is real, but manageable, and nothing in the data supports a permanent shift to triple-digit oil. China’s demand is weaker than most assume, Trump has a political deadline to resolve the conflict, and consumers are already feeling the weight of elevated prices. All of this points in the same direction. We see prices heading lower from here, and we will keep following the data as the situation develops.

The Aurelion Team

Disclosures & Methodology

1. What happens if Trump decides his legacy is more important than the midterms and he commits in the hopes of a full Iranian capitulation?

2. What is Trump thinks he can win the mid terms with higher gas prices?

The above are obviously not likely but if they do occur, does that change your oil outlook?

This may sound counter-intuitive, but the cure for high prices IS high prices.

When commodities move to new price levels, there is an impetus for bringing more of that item to the market. Either the additional product comes to market, lowering its price; or it doesn't, and prices go even higher. But there is a point where buyers cut back because of (usually) reduced demand for their end-products, which will cause a back-up in the supply chain.