Special Article: SpaceX, OpenAI, and Anthropic IPOs

Analyzing upcoming IPOs, whether their valuations are attractive, and the implications for global markets.

This is not our typical article, but the subject was too interesting to pass up.

Three of the most consequential companies in the world are heading to public markets within months of each other:

SpaceX just filed for what would be the largest IPO in history

OpenAI expected to file in the coming days, targeting a September listing

Anthropic is eyeing October at a $900B+ valuation

Combined, these companies are targeting a market cap of $3.5 trillion, and could collectively raise over $195 billion in fresh capital. To put that in context, the dot-com era’s three largest IPOs combined raised less than $30 billion.

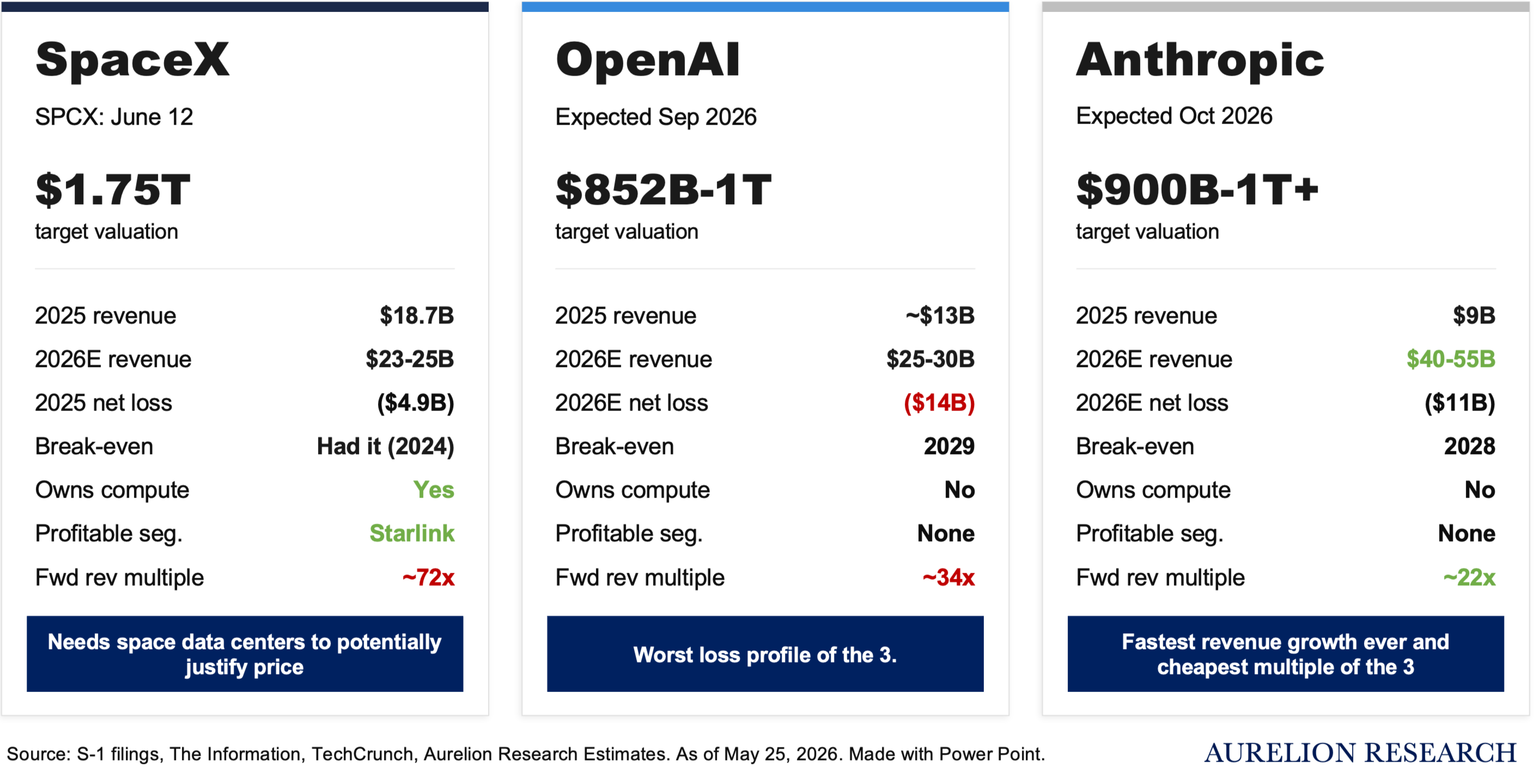

We created three summary cards to make comparisons easier. Some metrics are based on our estimates, explained in more detail further below.

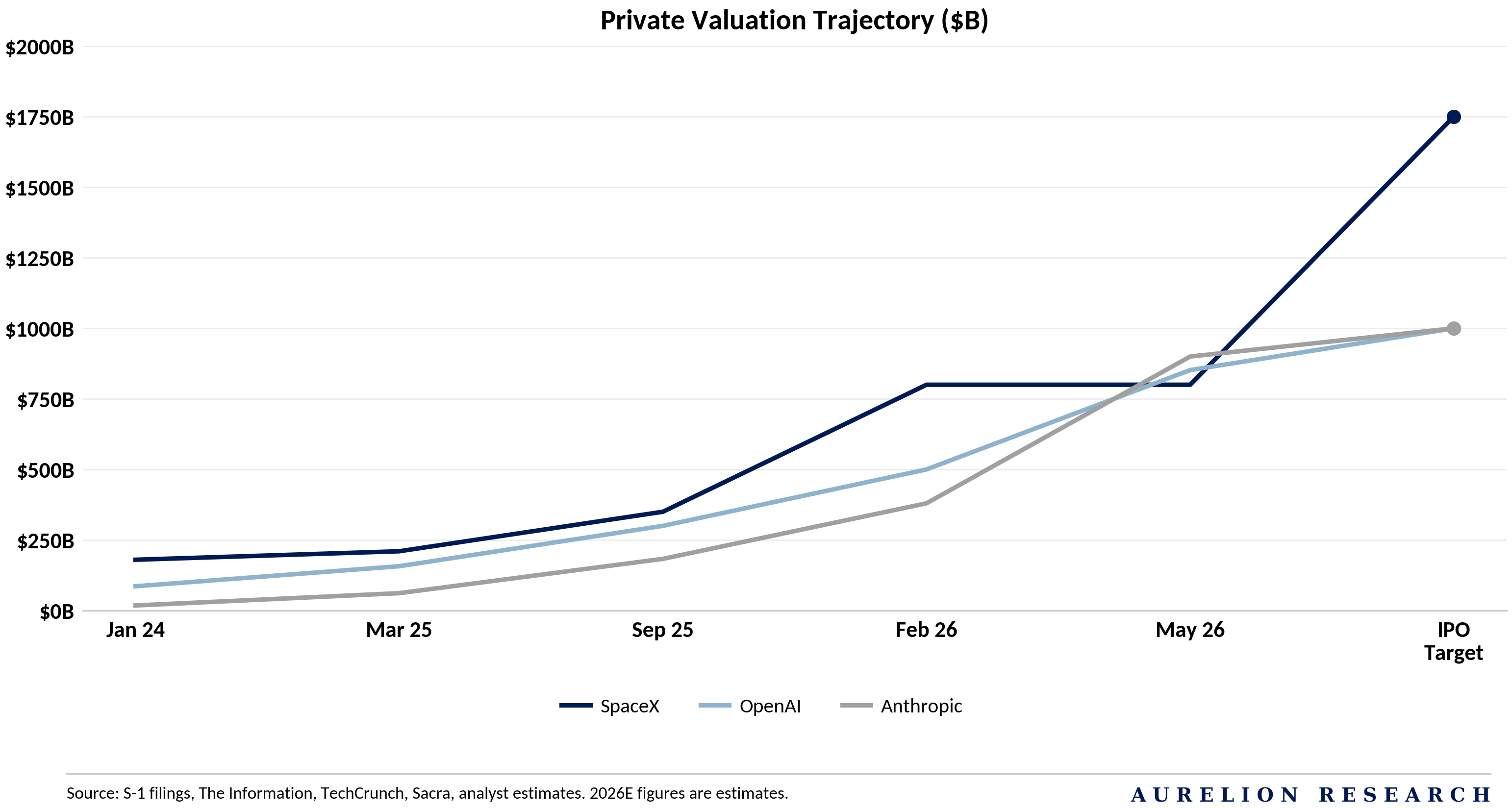

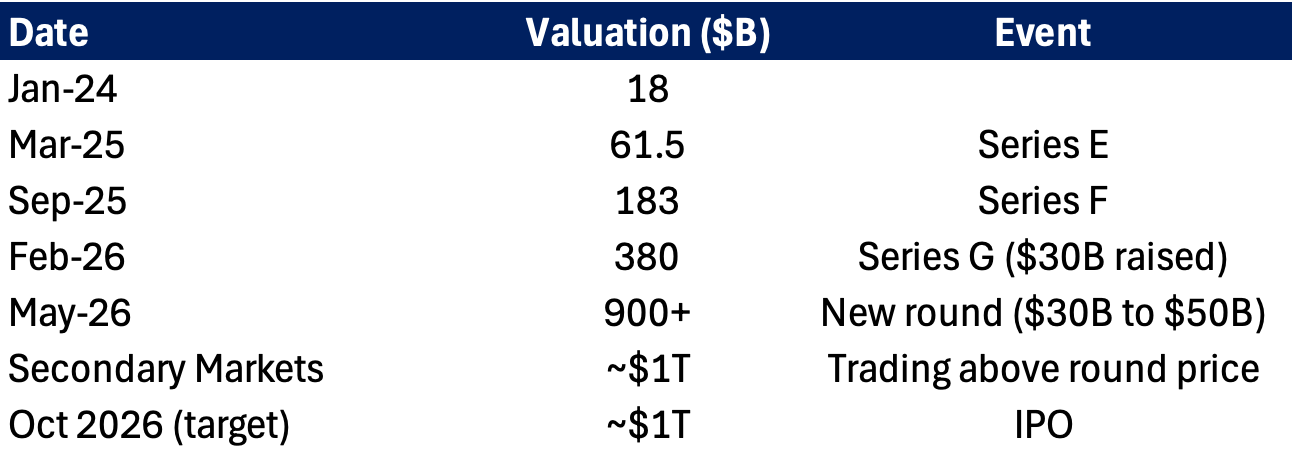

As the chart below outlines, the valuation trajectory has been spectacular across all three companies.

Below, we dive into each company’s financials and value them. More importantly, we explore how AI sentiment and thematic investing are shifting as these IPOs approach. In our view, several AI names will continue running up.

That said, to successfully make money with these companies, whether buying or shorting, investors need to understand where sentiment and the thematic narrative are heading, not rely on a financial model.

If you have been following our work, you would rightly guess these companies do not fit our typical investment criteria. However, we believe they carry significant implications for sentiment and the AI thematic across global capital markets.

We have argued for a long time that looking only at fundamentals, such as cash flow, margins, and multiples, misses the full picture. The vast majority of fundamental bottom-up funds have underperformed in recent years by ignoring broader market thematics and sentiment.

This is why thematic investing is becoming increasingly important.

Market themes are driving more and more of overall returns.

Which leads to a simple question: if you do not own these large-cap AI companies, will you get left behind?

Table of Contents

SpaceX: The Craziest IPO Ever Filed

OpenAI: The Billion-Dollar Loss Machine

Anthropic: The Fastest-Growing Company in History

IPOs Side by Side

Implications for the AI Thematic

How to Use Thematic Investing

Bubble or Not? A Simple Argument

1. SpaceX (SPCX): The Craziest IPO Ever Filed

The S-1 IPO filing reads like a sci-fi novel.

Here are some of the facts that caught our attention the most:

SpaceX filed for the biggest IPO in history.

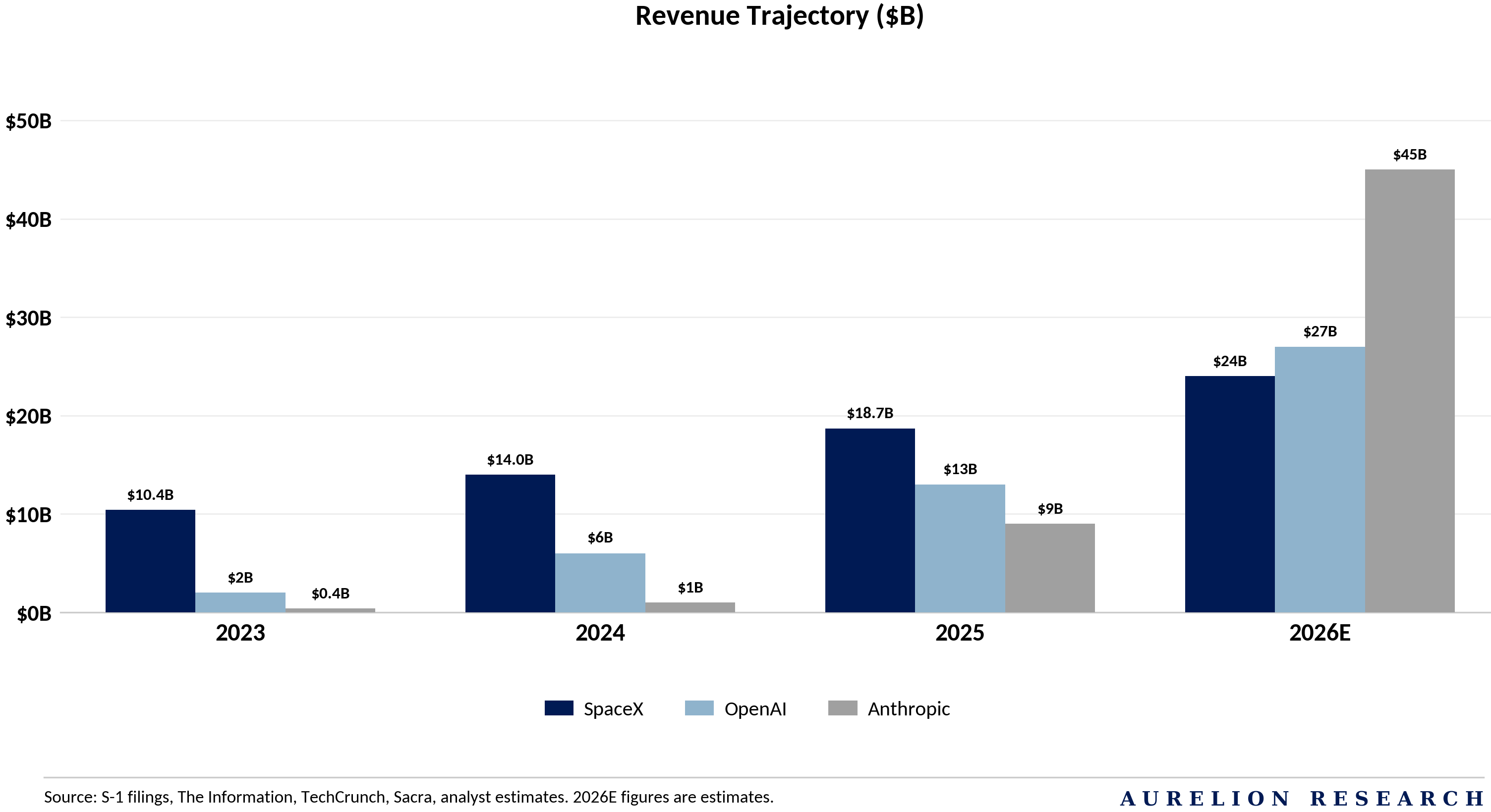

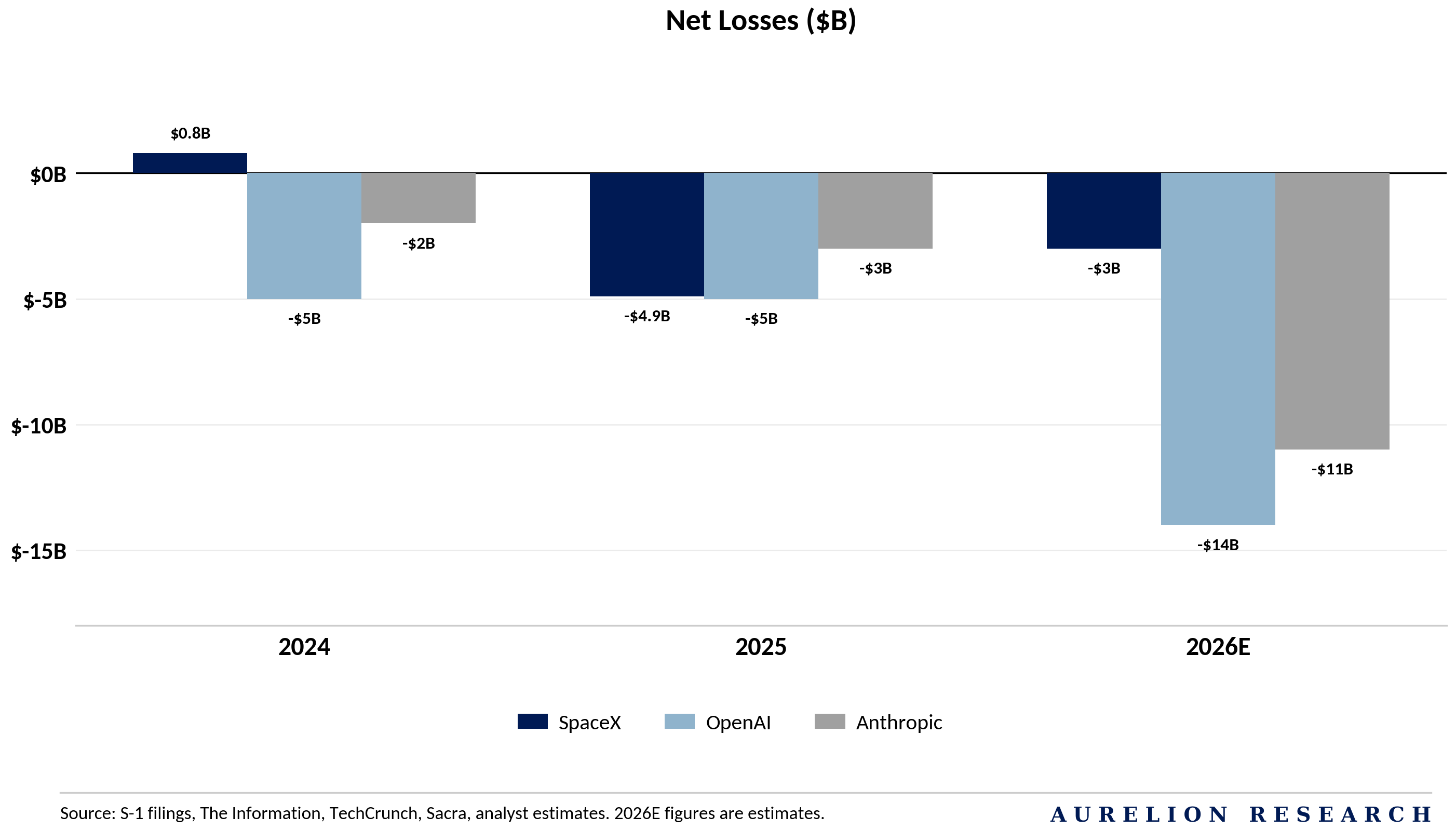

At a targeted $1.75T valuation, it would be the largest public offering ever. The company posted $18.7B in revenue in 2025 but still lost $4.9B, and has burned through $37B in cumulative losses since Musk founded it in 2002.

Musk’s bonus requires colonizing Mars. His compensation package, potentially worth $737B, is split into two milestones.

The first, worth ~$583B in stock, only vests if SpaceX reaches a $7.5T market cap and builds a permanent colony on Mars with at least one million inhabitants.

The second, worth around $154B, requires orbital data centers delivering 100 terawatts of annual compute. Without much research we can confidently say that “colonize another planet” is a first for a CEO performance metric.

Anthropic is paying $1.25B per month to rent Musk’s GPUs. The deal runs through May 2029 and could total over $40B, making it one of the largest compute contracts ever signed. X AI overbuilt its data center capacity, usage of its chatbot Grok declined, and the spare GPUs are now being rented to a direct competitor.

Musk holds 85.1% of voting power while serving as CEO, CTO, and Chairman simultaneously. His Class B shares carry 10 votes each. Even after the IPO dilutes his stake, voting control stays above 50%. He functionally cannot be fired, challenged, or overruled by any shareholder or board combination.

SpaceX spends more on AI than on rockets. AI infrastructure capex hit $12.7B in 2025 and $7.7B in Q1 2026 alone, roughly four times the space segment’s R&D budget for Starship. The company that put astronauts in orbit now pours the majority of its capital into GPU clusters on the ground.

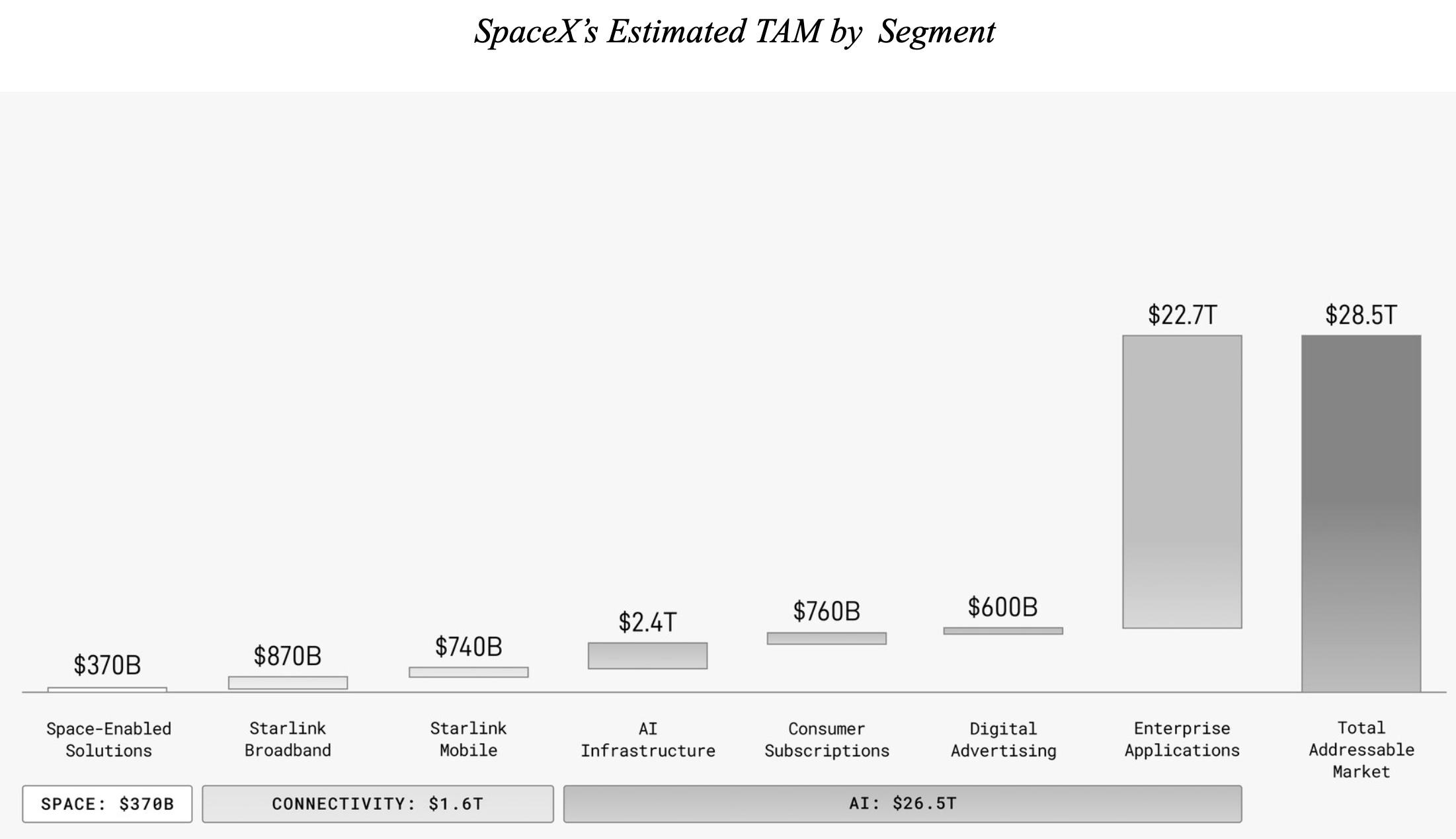

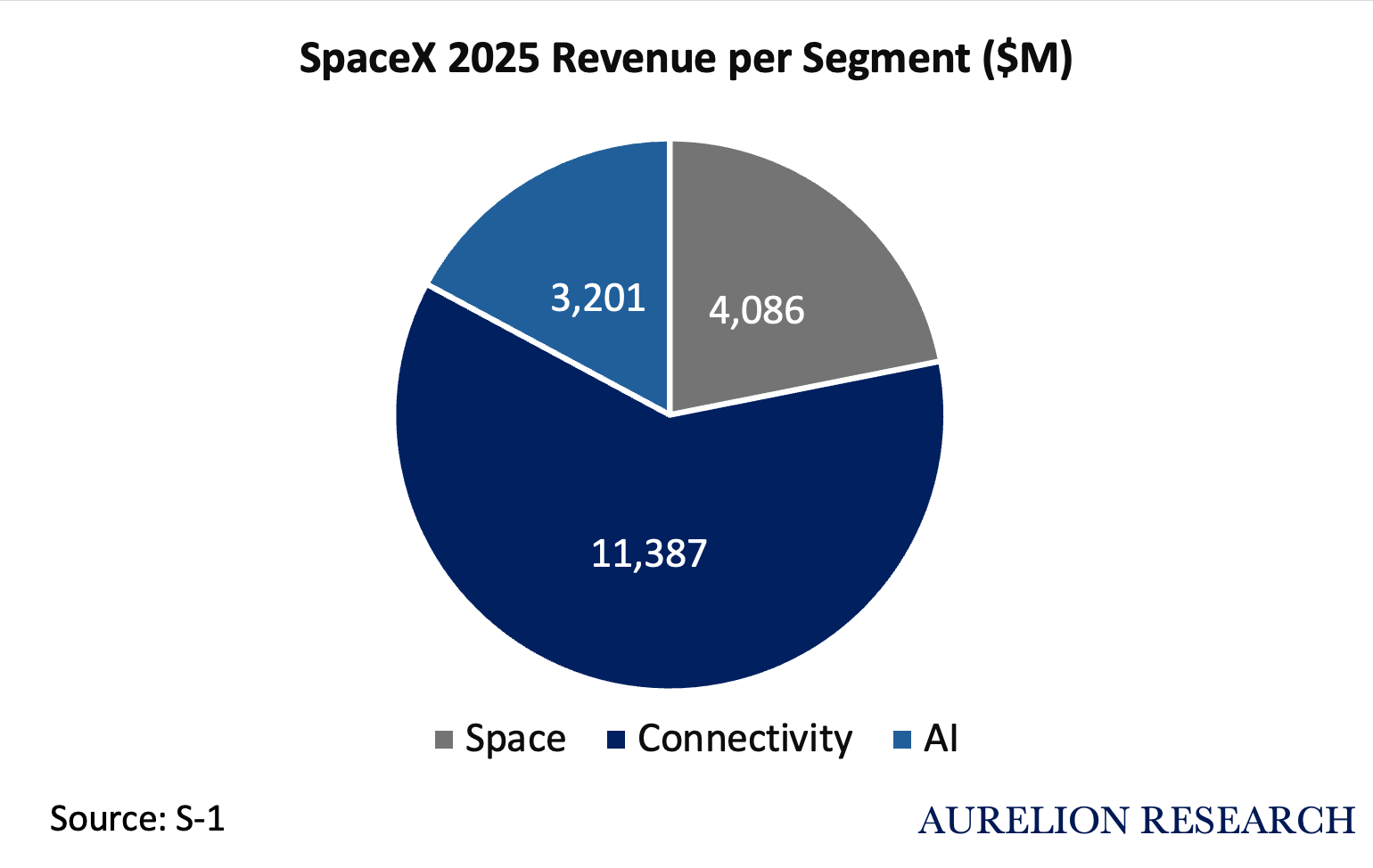

The claimed total addressable market is $28.5T, about 25% of global GDP. SpaceX calls it “the largest actionable total addressable market in human history.”

The breakdown: $26.5T in AI, $1.6T in connectivity (Starlink), and $370B in space launch. In other words, SpaceX is telling investors that rockets are the sideshow.

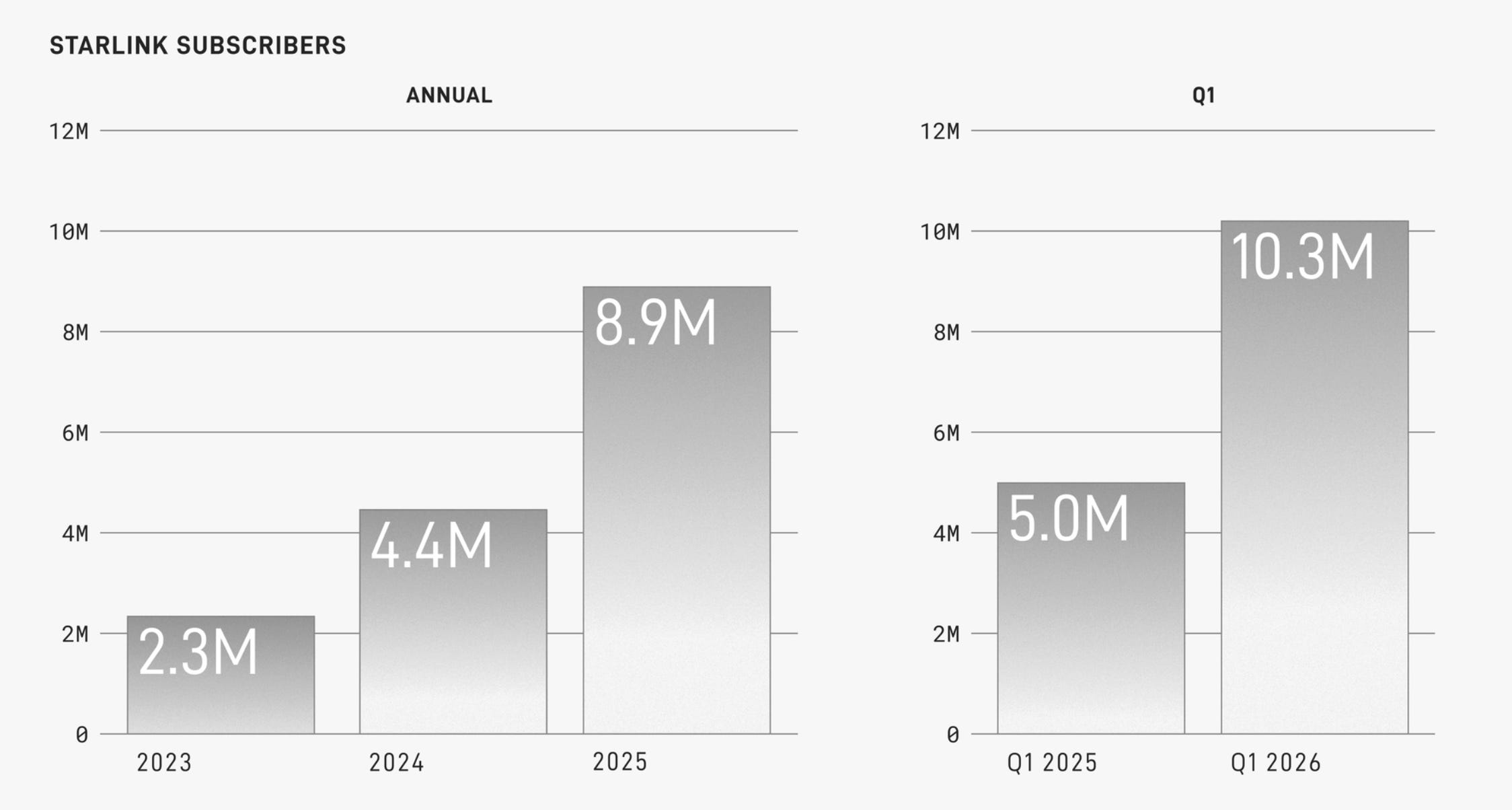

Starlink is enormous. Subscribers grew from 2.3M in 2023 to 10.3M by March 2026. The connectivity segment generated $11.4B in revenue in 2025, 61% of total company revenue, and unlike the AI division, it’s already profitable. Starlink alone would rank as one of the most valuable telecom businesses on Earth.

1.1 The AI Trojan Horse

Strip away the rockets and the Mars rhetoric. SpaceX is filing to go public as an AI infrastructure company that happens to own rockets.

In 2025, SpaceX spent $12.7B on AI infrastructure, four times what it spent on Starship R&D. In Q1 2026, $7.7B went to AI capex out of $10.1B total.

That’s 76 cents of every capital dollar flowing into GPU clusters.

The AI segment lost $6.4B in 2025 and another $2.4B in Q1 2026. But Starlink prints enough profit to fund the burn, and the IPO will pour gasoline on the fire.

The strategy has three layers.

Layer 1: Rent what you have. X AI overbuilt and Grok usage declined. So SpaceX turned its Colossus data centers into a cloud business overnight. Colossus is the world’s largest AI supercomputer cluster. Anthropic now pays $1.25B per month for access to 200,000+ Nvidia GPUs across Colossus 1 and Colossus 2 in Memphis.

Layer 2: Buy the application layer. Cursor is an AI-powered code editor that exploded across the software world, crossing one million paying users faster than almost any SaaS product in history. Revenue went from $500M in May 2025 to $3B by the time of the filing.

Cursor already uses X AI compute as a customer. If SpaceX owns it outright, it controls both the GPU infrastructure and the tool millions of developers use every day. Same logic that led Apple to build its own chips: control the full stack so nobody can squeeze you in the middle. SpaceX secured the right to acquire Cursor for $60B, 30 days after the IPO closes. That’s a 20x revenue multiple.

Layer 3: Move the data centers off the planet. In January 2026, SpaceX filed with the FCC to deploy up to one million satellites functioning as orbital data centers.

Solar-powered. In space, there are no cooling costs, water or permitting fights. Morningstar’s analysts noted this would require roughly 6,667 Starship flights per year, 530 times the current global launch mass to orbit.

SpaceX needs investors to believe it could work eventually, and the $26.5T AI TAM claim in the S-1 is designed to make that case. The filing even lists capital deployment targets for “Moonbase Alpha,” a lunar outpost intended to manufacture AI satellites and launch them via magnetic accelerator.

1.2 The Hidden Stakeholders

Before a single retail investor touches SPCX on June 12, a small group of early backers will be sitting on some of the greatest investment returns in history.

Alphabet: $900M to $100B+. In 2015, Google & Fidelity jointly invested $1B when SpaceX was worth ~$12B. In Q1 2025 alone, Alphabet booked $8B in unrealized gains from its SpaceX position, 25% of its total net income that quarter. Most Alphabet shareholders have no idea it’s there, buried in “other income.”

Founders Fund: $20M to roughly $60B. Peter Thiel wrote the check in 2008, after three consecutive rocket failures, when SpaceX was weeks from bankruptcy. Now diluted to roughly 3.5%, that stake is worth nearly $60B at IPO pricing. The single largest return on a single investment in venture capital history.

The Bitcoin stash. Buried in the balance sheet: 18,712 Bitcoin at a fair value of $1.29B. Cost basis was $661M, roughly $35,320 per coin.

This was more than double what on-chain trackers estimated. Over 10,000 BTC were sitting in custodial arrangements invisible to blockchain analytics. SpaceX now holds more Bitcoin than Tesla, making Musk the controlling figure behind the two largest corporate Bitcoin positions outside of Strategy.

1.3 One Man’s Company

Elon Musk will step onto the Nasdaq trading floor on June 12 holding more concentrated corporate power than any individual in modern American history.

He serves as CEO, CTO, and Chairman simultaneously, controlling 93.6% of Class B stock, which carries 10 votes per share, translating into 85.1% of total voting power. Even after the IPO, control remains above 50%. He cannot be removed, and he appoints the board.

On the capital allocation side, the company has also spent $131M on Cybertrucks from Tesla. We believe this raises questions about how capital is being allocated and shows how much spending happens within Musk’s own companies.

SpaceX Spent $131M on Cybertrucks

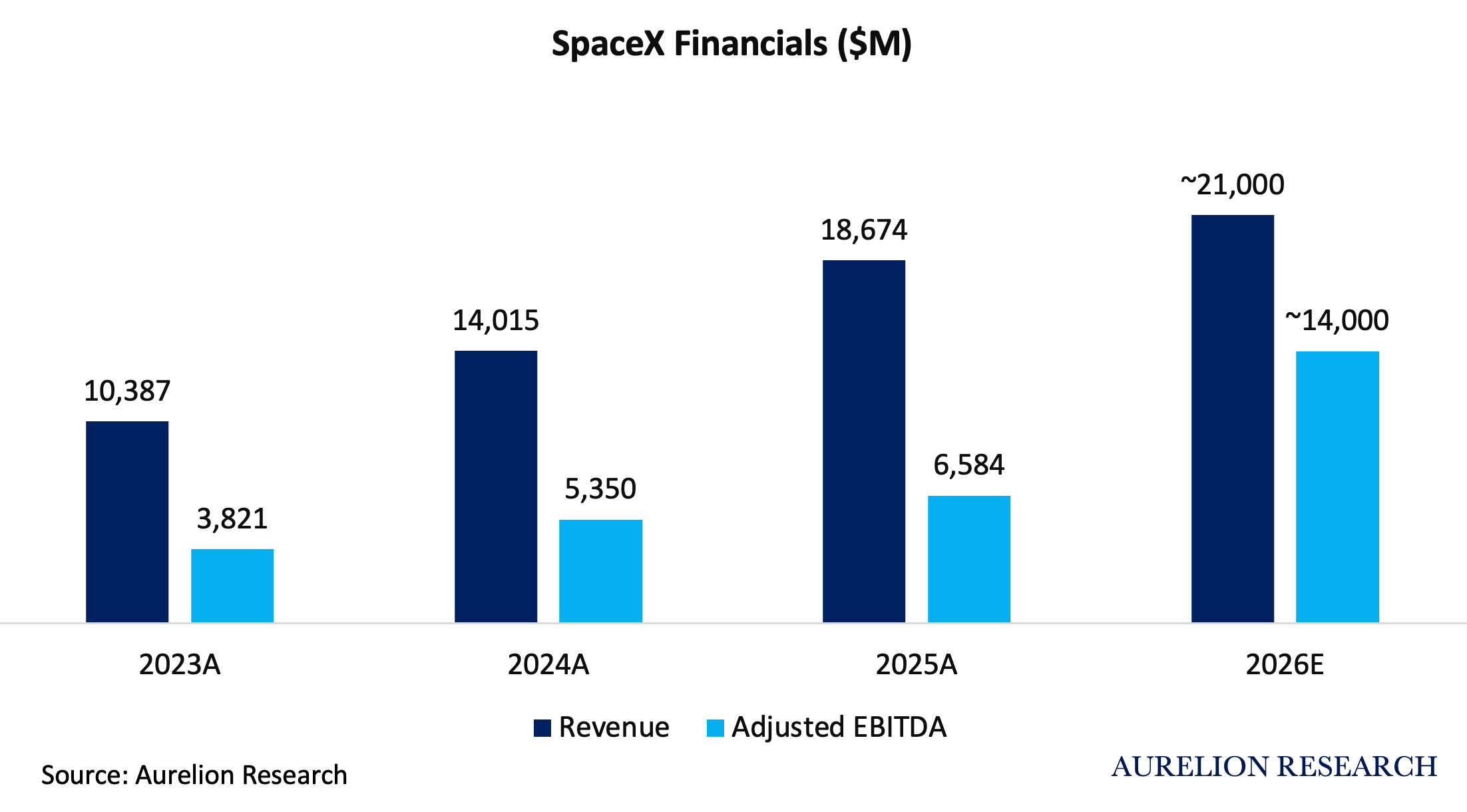

1.4 SpaceX Financials

A look at segments:

Space: Launches rockets for governments, NASA, and commercial customers, and is developing Starship, the next-gen vehicle designed to carry 100x more payload at a fraction of the cost.

Connectivity: Starlink, a global satellite internet service beaming broadband from 9,600+ satellites to 10.3M paying subscribers across 164 countries.

AI: The merged xAI and X (formerly Twitter) business, which includes the Grok chatbot, X’s advertising platform, and a massive GPU data center operation now being rented to outside customers like Anthropic and Cursor.

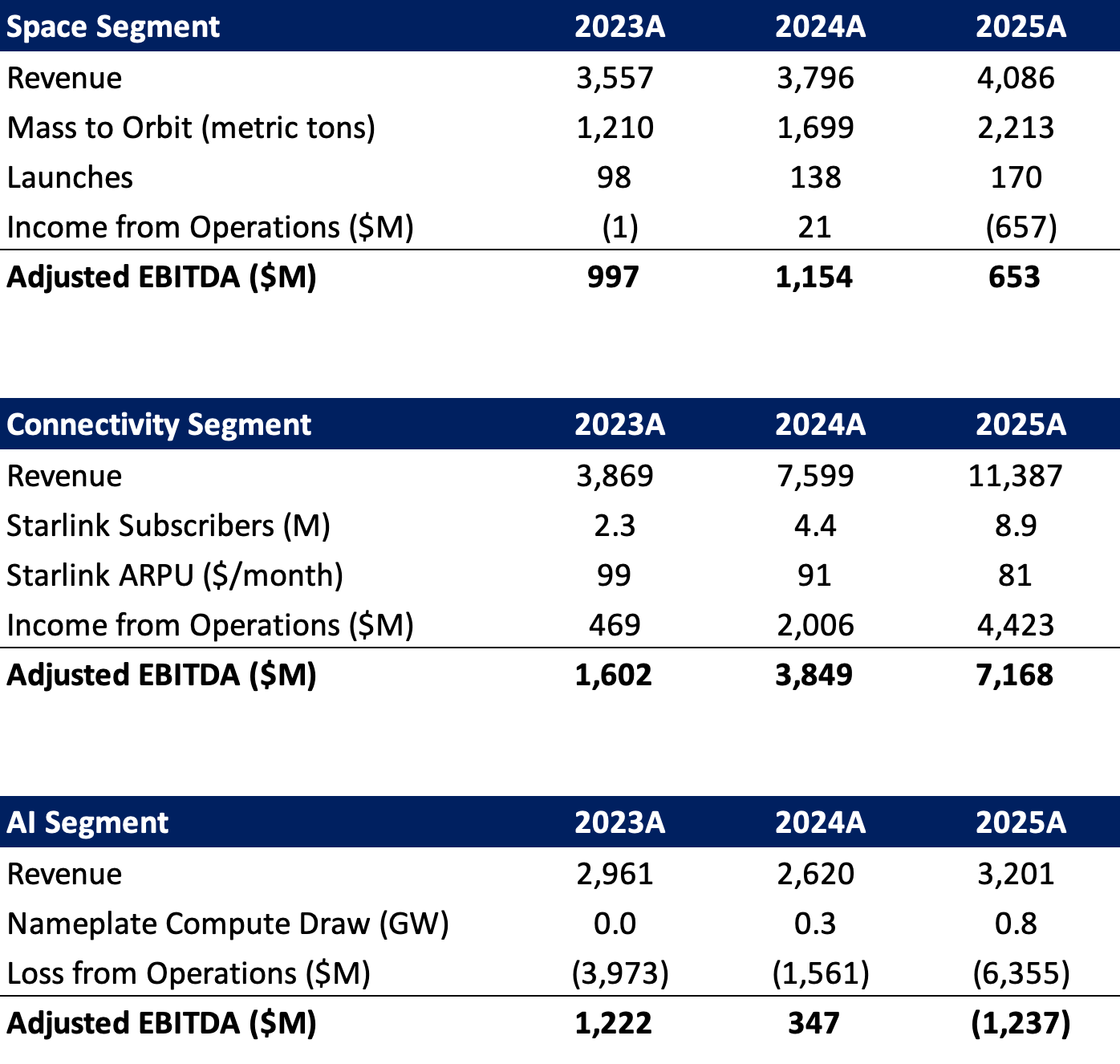

Starlink is the engine. Revenue nearly tripled from $3.9B in 2023 to $11.4B in 2025, with operating income going from $469M to $4.4B. It prints cash.

ARPU is declining ($99 to $81/month) as SpaceX pushes into cheaper markets, but subscriber growth (2.3M to 8.9M) is more than offsetting that.

$4.1B in revenue but it lost $657M in 2025 because Starship R&D is eating the profits from Falcon launches. The rocket business funds itself, barely.

AI is the money pit. $3.2B in revenue against $6.4B in operating losses in 2025. This segment didn’t exist at this scale until xAI and X were folded in.

Capex alone was $12.7B. The Anthropic deal ($1.25B/month starting mid-2026) should change this picture dramatically in the second half of this year.

At the total company level: $18.7B in revenue in 2025, up 33% from $14B in 2024. The company was actually profitable in 2024 ($791M net income) before the xAI merger dragged it back into the red. Total capex hit $20.7B in 2025, more than the company’s entire revenue the year before. SpaceX is spending faster than it earns, betting everything on the infrastructure paying off at scale.

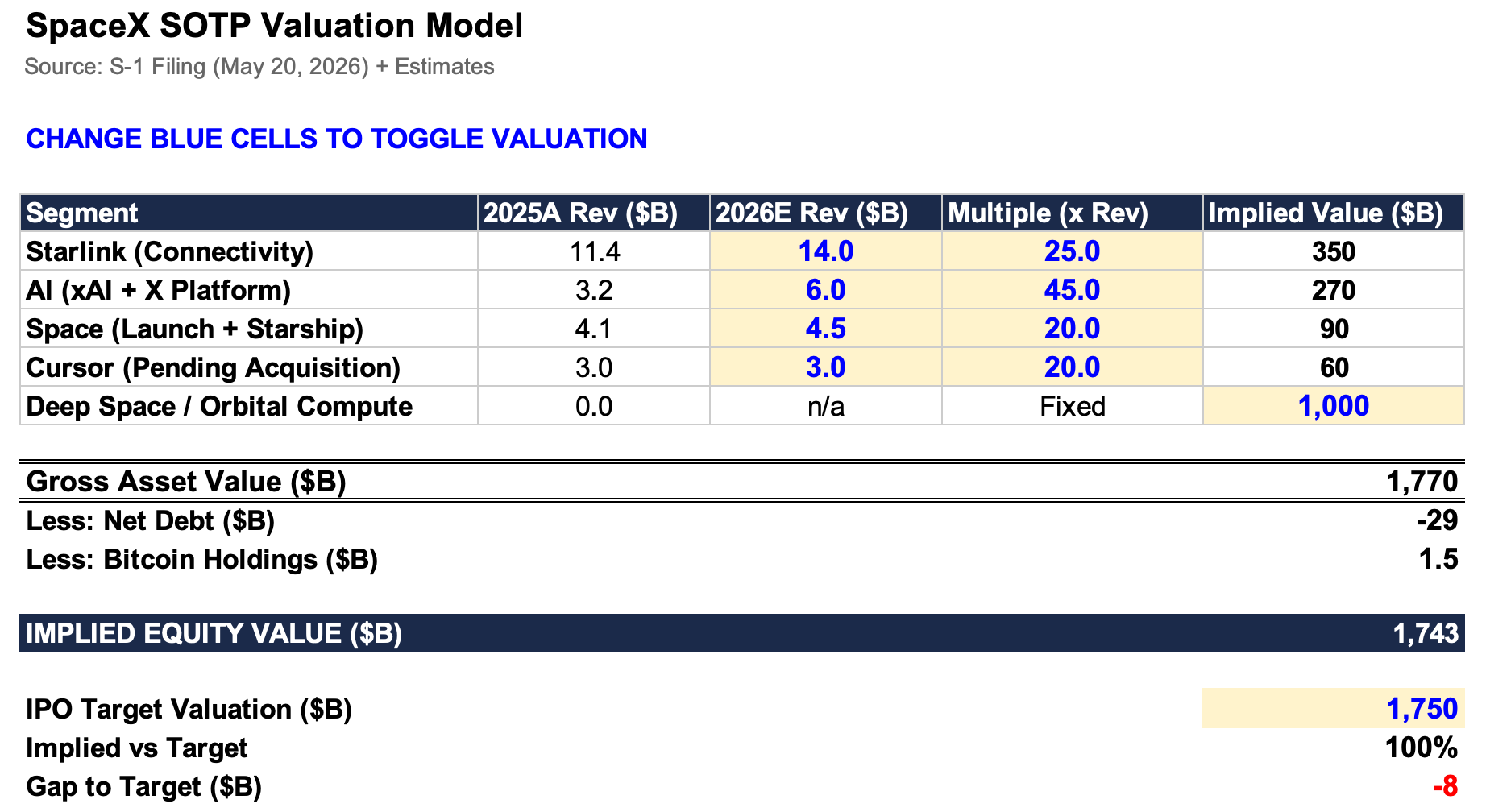

1.5 The $2T Valuation

The summary of SpaceX valuation is simple: standard DCF and SOTP models break down entirely here. The $1.75 - 2T valuation is entirely a momentum and sentiment play.

What Wall Street is Saying:

Dan Ives (Wedbush Securities) is a bull. He called it “the largest IPO in stock market history” and sees SpaceX at the center of a multi-decade AI and space growth cycle. He predicts an 80% chance SpaceX and Tesla merge by 2027.

Morningstar (Franco Granda) is more measured. They put fair value between $1.1T and $1.7T using a sum-of-the-parts model and flagged that only 3-4% of shares will float, meaning 20-30% price swings are likely (versus 10-15% for Tesla) simply because the tradeable supply is so thin.

Quilty Space (Chris Quilty), the satellite industry’s go-to analyst, projects Starlink alone tracking toward $20B revenue and $14B EBITDA in 2026 with 16.8M subscribers. His numbers imply Starlink could justify a $400B+ standalone valuation on its own.

The bear case, floated by several unnamed analysts, values SpaceX closer to $700–800B on a present-value basis, arguing the $1.75T target assumes too much speculative premium for orbital compute and Mars, which may never generate meaningful revenue.

Reconciling $2T

The only way to get close to a $1.75-2T valuation is to assign around $1T of value to the potential of space data centers. Otherwise, it makes no sense, even with absolutely ridiculous multiples.

We do not like using revenue multiples, but this was the only way to build some sort of framework here. If SpaceX does not develop space data centers, the company is worth at most $700B in our view.

We have added the excel spreadsheet if you want to play with multiples and revenues to see the valuation it implies.

What Is SpaceX Really Worth?

Here, it would be misleading to treat SpaceX like a normal company by evaluating fundamental cash flows and discounting them back. We know the company will not trade like this, so doing that is completely useless. It would probably give a valuation closer to one-fifth of the current $1.75-2T goal.

For reference, $175-185 per share is the current ballpark for the $1.75T target.

Forecasting a long-term growth rate is also completely useless and will depend heavily on geopolitics and the advancement of global technologies.

The real question is: what is the probability that the TAM materializes, and that SpaceX captures a large share of it?

Our biggest issue with this valuation is that every segment has to go perfectly and revolutionize its market. To justify a 25x revenue multiple, Starlink would need to become the most widely used data connection platform on the planet. The space launch segment also needs to continue growing and avoid pricing pressure or loss of market share to new competitors.

For the AI segment to be worth 45x revenue, it needs to maintain the current sentiment and hype in the market, while SpaceX also has to deliver new ways to monetize its AI infrastructure. And finally, SpaceX needs to become the dominant and first major player in space data centers.

Now that we have established that the financials do not support this valuation, the key question is whether continued support from Elon Musk, political tailwinds, and major AI players like Anthropic, OpenAI, and Microsoft will sustain momentum around the company. If that narrative remains intact, the stock could plausibly open near a $2T valuation and move higher from there.

It will all come down to sentiment and headlines.

Of course, we will not be adding this company to the Aurelion Index when it goes public. However, we will focus on themes and beneficiaries linked to it. We now have more visibility on suppliers, contracts, and spending patterns, which will help identify companies positioned to benefit from SpaceX’s massive spending.

SPCX lists June 12.

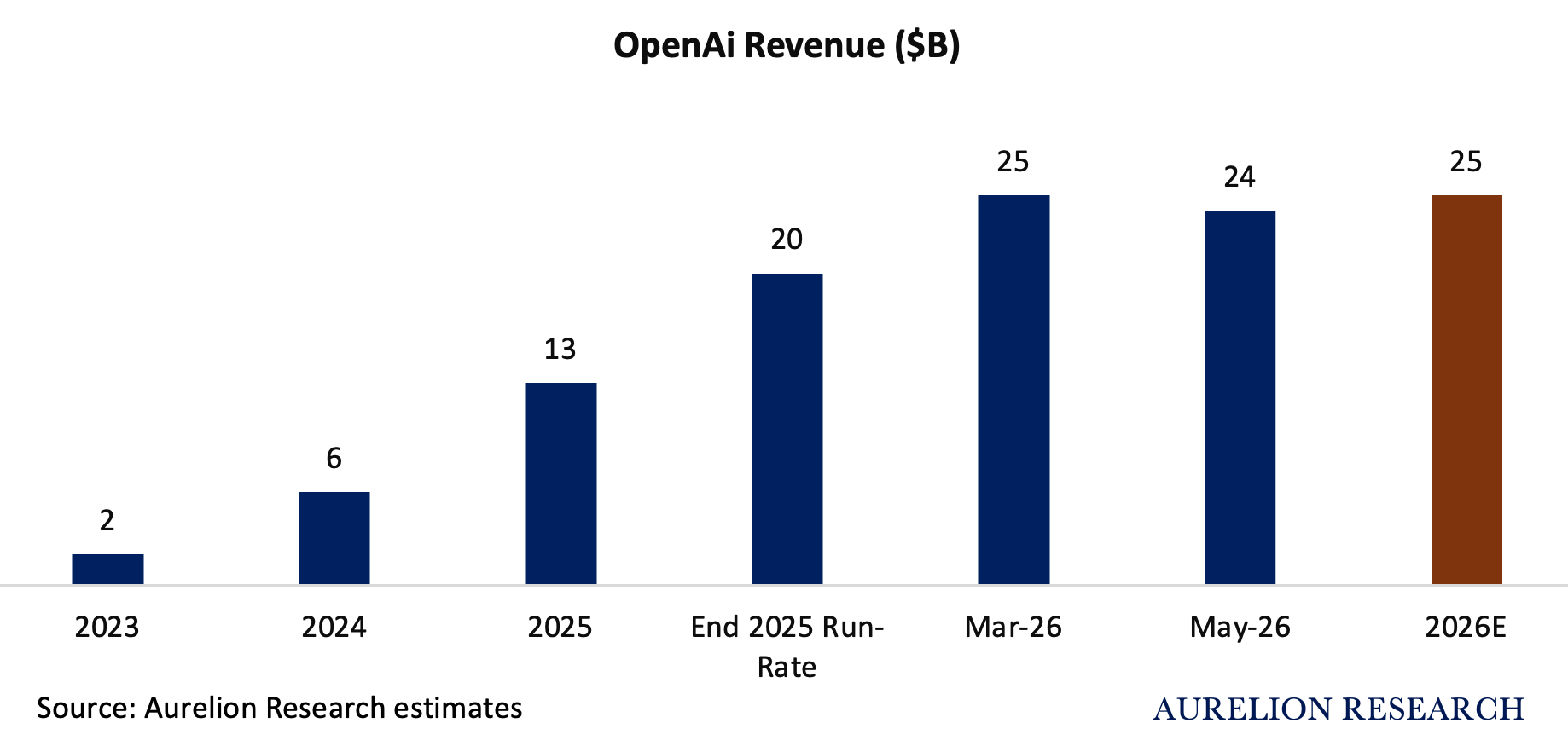

2. OpenAI: The Billion-Dollar Loss Machine

OpenAI is rumored to file in the coming days, just after SpaceX went public with its filing. Goldman Sachs and Morgan Stanley are leading. Target: Q4 2026 listing, possibly September, at a valuation between $852B and $1T.

The company is generating ~$2B per month in revenue, hit a $25B annualized run rate by March 2026, and counts 900M weekly active ChatGPT users, 50M consumer subscribers, and 9M paying business users. Enterprise now makes up over 40% of revenue and is on track to reach parity with consumer by end of 2026.

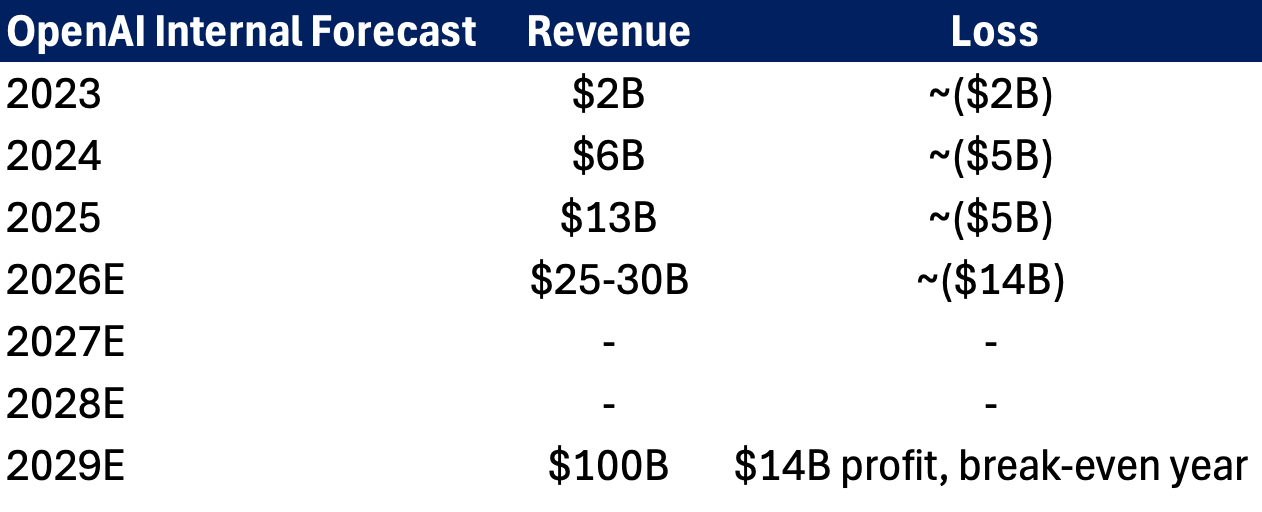

OpenAI is losing roughly $1.22 for every $1 of revenue. Internal forecasts project a $14B loss in 2026, roughly 3x worse than 2025. The company expects cumulative losses of $44B from 2023 through 2028 before turning profitable in 2029.

In March 2026, OpenAI closed the largest private funding round in history: $122B at an $852B post-money valuation. That round itself expanded from an earlier raise at $730B pre-money announced in February.

2.1 The IPO Race

This is a three-way race for public market capital. SpaceX goes first (June 12). OpenAI targets September. Anthropic is eyeing October at $900B+.

Dan Ives at Wedbush: “Getting to public markets first is very important. It sets a valuation, you’re the first to meet with investors, and there’s an advantage.”

OpenAI Revenue Path

The Loss Story

OpenAI’s own internal forecast leaked by The Information shows the company does not expect to turn a profit until 2029, at which point it projects $100B in revenue. To reach that level, it plans to spend $200B through the end of the decade, with 60–80% allocated to compute for training and inference.

OpenAI does not own its compute. Unlike SpaceX (which owns Colossus), OpenAI relies almost entirely on Microsoft Azure. CFO Sarah Friar has described this as a deliberate “light balance sheet” strategy, partnering rather than owning, with contracts structured flexibly across providers and hardware types.

The upside: no massive infrastructure on the books. The downside: no owned infrastructure as a moat, and Microsoft takes a cut of everything.

The Restructuring

As you might know, OpenAI was started as a non-profit with great goals and virtues. It turned into a for-profit organization to get ready for an IPO.

Sam Altman, who has repeatedly stated he’s not interested in wealth and took no equity in the company, was spotted driving a beautiful $4M Koenigsegg Regera, and the public perception officially went down the drain. While he was already wealthy prior to OpenAI this was just too much for the public eye.

2.2 Valuation

Private Valuation

OpenAI’s last private round valued it at $852B.

The IPO targets $1T+. Here is the rough math:

Our Take On Valuation

We are staying far away from OpenAI.

The first reason is that we believe revenue is at high risk due to increased competition from several other chatbots (Anthropic, Gemini, Grok, etc.).

Several initiatives have failed, such as their video creation tools. We believe the company’s recent announcement regarding the integration of ads into the platform is also a sign that the firm is in a difficult position.

Sentiment and public perception of the company are declining. We think that reaching $100B in revenue by 2029 is a far-fetched goal, and the revenue multiple could take a hit as well, implying a much lower valuation.

For example, if OpenAI misses consensus this year and the run-rate at year-end becomes $20B due to increased competition, we might apply “only” a 20x revenue multiple; the valuation would then be slashed in half to $400B.

Every dollar they invested in prior models has essentially gone to zero, as nobody uses those older versions anymore. If they cannot continue to improve their models and a competitor beats them, the company could lose significant value.

Anthropic faces the same issue, but its valuation looks more “attractive” in comparison to OpenAI.

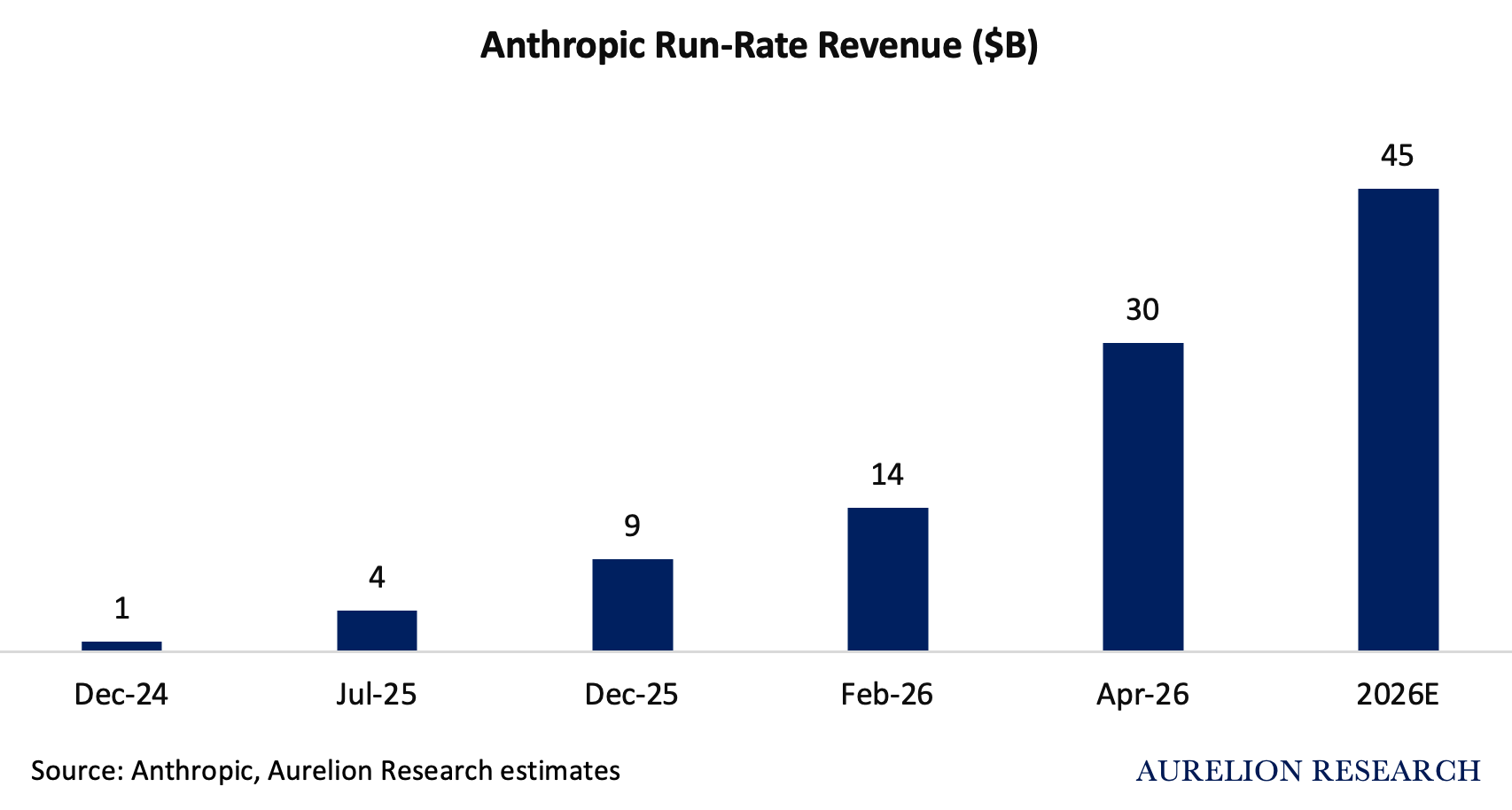

3. Anthropic: The Fastest-Growing Company in History

Anthropic has not filed an S-1. No listing date is set. But the trajectory is clear: the company is closing what is likely its final private round ($30-50B at $900B+ valuation), has engaged Wilson Sonsini for IPO preparation, and is in early talks with Goldman Sachs, JPMorgan, and Morgan Stanley. Target: October 2026 listing. Bankers expect the offering could raise more than $60B.

The numbers behind this are unlike anything private markets have ever produced. Anthropic grew from $1B in annualized revenue in December 2024 to $9B by December 2025 to $30B by April 2026. Sacra estimates the run rate hit $43B by April. TechCrunch’s sources put the real figure closer to $40B.

No enterprise technology company in recorded history has compounded at this pace and scale. The valuation has increased 16x in 14 months, while revenue has expanded roughly 45x over the same period.

Eight of the Fortune 10 are Claude customers. Over 1,000 enterprise customers now spend more than $1M annually, up from just a dozen two years ago. Enterprise now accounts for 80% of revenue.

Unlike OpenAI, which leads in consumer applications, Anthropic is positioned as an enterprise-first business. This is more sticky revenue.

The Claude Code Phenomenon

Claude Code, Anthropic’s agentic coding tool, launched publicly in May 2025. It reached $1B in annualized revenue within six months. By February 2026, it had grown to $2.5B in run-rate revenue.

3.1 The Loss and Spending Story

Anthropic is not profitable. Internal projections leaked by The Information show $11B in losses in both 2026 and 2027, with profitability expected in 2028.

But here is where Anthropic separates from OpenAI: the cash burn path is dramatically more efficient. Anthropic forecasts its burn dropping to roughly one-third of revenue in 2026 and 9% by 2027. OpenAI expects burn to stay at 57% of revenue in both years. By 2028, OpenAI projects operating losses equal to three-quarters of revenue. Anthropic expects to break even.

Compute Infrastructure

Anthropic does not own its compute. It rents capacity from Amazon (AWS), Google Cloud, and SpaceX.

50x valuation increase in 28 months. At $900B valuation on a confirmed $30B run rate, the company trades at 30x forward revenue. If the real run rate is closer to $40B, as TechCrunch reports, the multiple compresses to roughly 22x. Still expensive.

But Anthropic reaches profitability three years before OpenAI while generating higher revenue and spending roughly 4x less on training.

There are two key implications from this:

At both a $1 trillion valuation, we believe Anthropic is a much better investment than OpenAI.

You can lose your money and dominant position extremely fast in this chatbot era. This means those 30-40x revenue multiples are definitely not realistic over the long term. However, if OpenAI sustains around a 34x multiple, Anthropic is likely to trade at similar levels as well.

4. IPOs Side by Side

Anthropic leads the pack in revenue growth:

SpaceX could be profitable if it did not spend on AI:

We want to highlight that we used revenue multiples, which we do not typically prefer, to illustrate what they imply for valuation. However, these revenue multiples are highly uncertain, and both valuations and share prices are ultimately driven by sentiment rather than a financial framework.

At current expected IPO valuations, we believe the best investment is Anthropic, but it remains highly speculative and dependent on politics, technological advancements, and overall AI sentiment in global markets.

Of course, as a note, we always aim to be transparent, and we are not planning to buy Anthropic personally. We believe our portfolio offers a better risk/reward profile than those three.

5. Implications for the AI Thematic

1) These three companies will trade on sentiment.

If these companies IPO at the valuations they are targeting, they will largely trade on sentiment and AI-related news, as their valuations are not justified using a fundamental approach. Significant swings should be anticipated.

2) Large index concentration in AI will increase.

3) The AI theme will attract even more attention. With suppliers being discussed on earnings calls, customers becoming better known, and greater visibility into where capital is flowing from these companies, we believe several AI beneficiaries will continue to rally.

The bull case for the AI Thematic:

Three mega-IPOs (SpaceX, OpenAI, Anthropic) are all lined up for summer/fall 2026. Every AI CEO has a direct financial incentive to talk up AI valuations before and after their listing. That’s months of relentless positive narrative, roadshows, and media cycles, all hitting at the same time.

You should expect more Joe Rogan podcast appearances from those CEOs.

China re-entering the AI race is generally supportive for the AI thematic at a high level, as it reinforces demand and global adoption, but it can also introduce longer-term competitive pressure on pricing and margins.

Put it together: a hot IPO summer with the biggest listings in history, AI CEOs on every stage, and China confirming the thesis. That’s a strong tailwind for AI valuations through the end of 2026.

6. How to Use Thematic Investing

We have mostly been focusing on industries other than AI over the last year, as the argument was there were better risk/reward opportunities elsewhere.

We are currently working on potential AI beneficiaries. Our criteria are extensive, and finding the right company has taken time. We are looking for real demand, strong fundamentals, a company with a long history as well as a good valuation.

The portfolio has done very well without AI names, but adding some (limited) AI exposure before an IPO frenzy is a great capital allocation in our view.

Click here to view historical portfolio performance

Below, we are sharing our approach to thematic investing. Whether it is an AI company or a gold miner, the process uses the same framework:

1) Identify an attractive investment theme

There has to be an attractive entry point. It needs to answer the question: why is now the right time for this theme?

2) Pick companies benefiting from the theme through a fundamental approach

Using typical fundamental analysis such as competitive positioning, discussions with management, financial modeling, etc. The important point here is that we do not pick 50 companies tied to the theme. We pick 1 or 2 companies that should both perform well on their own and also benefit from the theme.

3) Actively monitor the company

The most important part of investing is knowing when to exit. Monitoring the company allows us to determine when it is time to exit based on the company’s fundamentals. However, another very important point is that this monitoring provides first-hand insights into the drivers of the theme.

4) Company insights flow back into the theme

Sometimes, you can be among the first to identify signals from a company indicating that a theme is ending or shifting direction. Then you come back to step 1: is the theme still attractive? Have the beneficiary companies changed?

You can see that this framework is more of a cycle than a simple sequence of steps. All of it is done through a concentrated approach.

You cannot do all of this for 200 stocks. But if you select your 20 highest-conviction stocks using this approach, we believe it offers a strong risk/reward framework for investing and outperforming the market.

Of course, sometimes standalone company opportunities are so compelling that they work extremely well even without being tied to a broader investment theme, and those opportunities should be pursued.

As you know, you can view the portfolio’s positioning here: Aurelion Index

Below is an example that fits our framework well, where we highlight a lesser-discussed AI beneficiary.

Bottleneck Opportunity in a New Healthcare Era

Artificial intelligence is actively discovering new drugs.

7. Bubble or Not? A Simple Argument

A simple argument for the case that there is still some leg up to the AI thematic is this chart below prepared by Roundhill investments.

In 2000, valuations ran far ahead of fundamentals. This time, fundamentals are largely driving the move.

This summer could be a driver of continued multiple expansion for large AI companies through ongoing marketing efforts.

However, it will be important to monitor whether earnings continue to grow at a strong pace, as otherwise sentiment could shift quickly.

We are aware there is much more to be discussed about these companies, the state of the market, and AI. So feel free to leave your comments or questions below. Always happy to discuss!

Excellent analysis. For fundamental investors with a 5-to-10-year horizon, how should we weigh the opportunity set between US AI infrastructure and emerging market equities? Do you view AI as a centralizing force that further concentrates capital in the US or potentially as a catalyst that accelerates growth in regions like LatAm through localized adoption?"

"In space, there are no cooling costs."

It's impossible to take someone who writes this seriously. In space there is no conductive or convective cooling, only radiative, which is is very inefficient, and it certainly is not free. Any investment in SpaceX is obviously a "greater fool" trade. Good luck.