Bottleneck Opportunity in a New Healthcare Era

An emerging investment theme in clinical research, attractive near-term sector dynamics, and a new stock addition.

Artificial intelligence is actively discovering new drugs.

Both biotech startups and large pharmaceutical companies are seeing returns from AI, which is reducing drug discovery timelines by several multiples compared with traditional approaches.

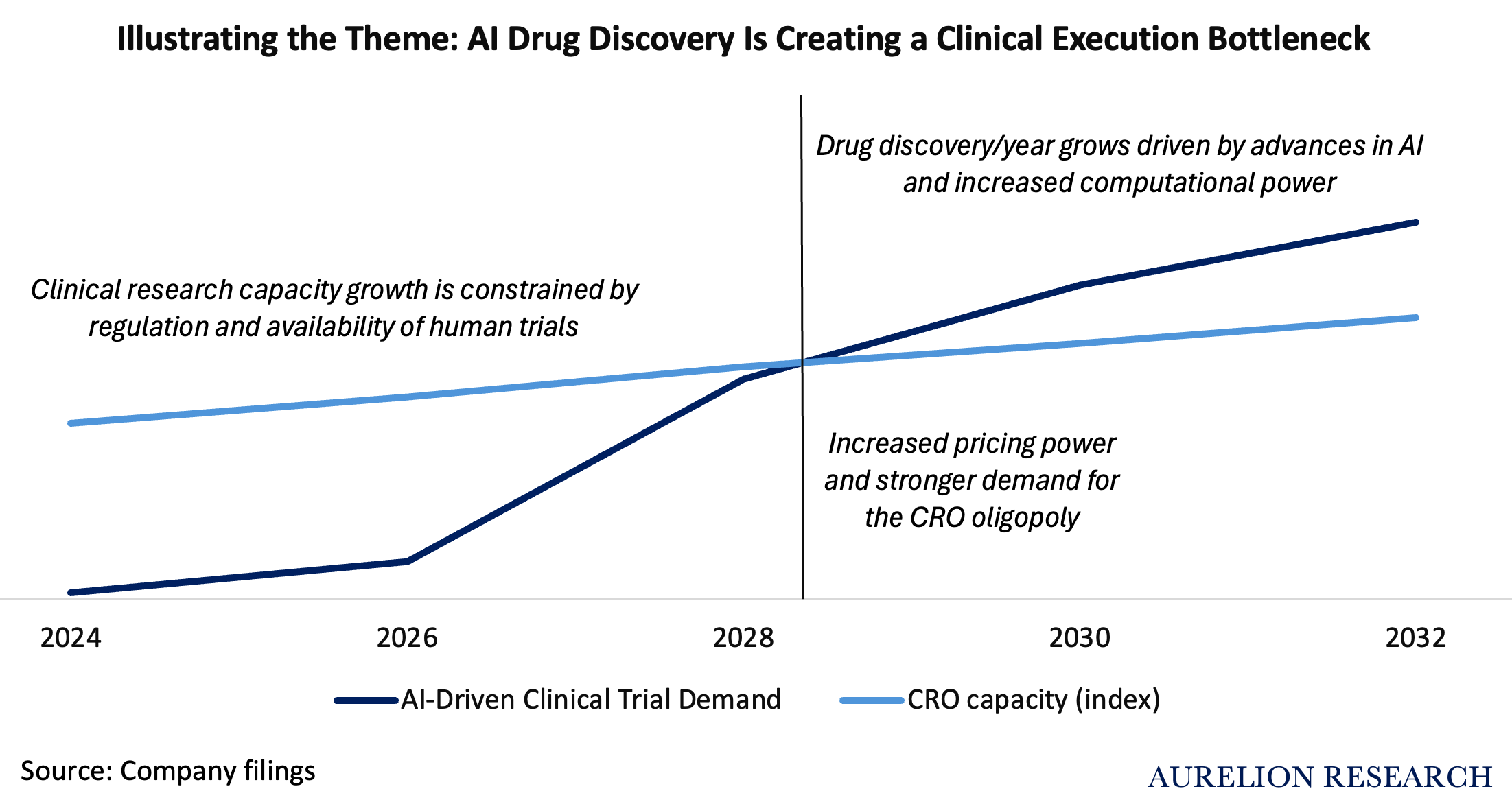

We believe the trend is clear: a surge of new potential drugs will come to the market in the coming years. However, there is a clear bottleneck. Who will run the trials for these drugs?

Contract research organizations (CROs), which benefit from strict FDA regulation and an oligopolistic structure.

This report outlines our investment thesis across three sections:

The Thematic: How the AI-driven surge in drug discovery translates into long-term demand for CROs. And why CROs have been unjustifiably punished.

Industry Dynamics: A dive into the current 2026 landscape, biopharma funding trends, and the operational realities of the CRO oligopoly.

New Aurelion Index stock: The addition of a high-quality differentiated CRO to the portfolio, positioned to benefit from this thematic while currently trading at a cyclical discount.

We avoid gaining exposure to this theme through single biotech names, which carry higher company-specific risk tied to individual drugs.

Three premises are required for the bottleneck to occur:

Premise A: AI increases the volume of preclinical molecular candidates.

Premise B: The FDA requires physical human testing. AI-driven simulations cannot replace biological validation.

Premise C: Clinical trials cannot scale like software. They depend on a finite supply of patients, physicians, and clinics, which makes clinical trials a capacity-constrained process managed by CROs.

Conclusion: The economic bottleneck shifts from drug discovery to clinical trial execution, increasing demand for CROs.

In our view, the most common mistake in thematic investing is timing. Even if the long-term thesis is correct, near-term outcomes are still heavily influenced by industry cycles and CRO operational dynamics. The short to medium term therefore remains critical in this space, and misreading it can lead to poor returns.

For this reason, we also analyze the current 2026 CRO landscape, biotech and biopharma funding trends, and the competitive positioning of key players. We then assess expected returns for leading CROs such as ICON, IQVIA, and CRL.

Table of Contents

Introduction

What is a Contract Research Organization (CRO)

Premise A) Can AI Really Discover Drugs?

Premise B) Regulation and the FDA

Premise C) Physical Limit

The Bottleneck

5.1 The Market’s View

A look at The Bear Case

Recurring Mistake in Thematic Investing: Timing

CRO Industry Overview

8.1 Biotech Funding Trends

8.2 Largepharma Funding Trends

The CRO Market Is Growing

9.1 Biopharma R&D: Where the Growth Is Coming From

9.2 Where Outsourcing Is Growing and Where It Is Not

9.3 Bioprocessing Is Recovering

9.4 Drug Approvals

Diving into Industry Leaders

10.1 ICON ($ICLR)

10.2 Iqvia Holdings ($IQV)

10.3 Charles River Laboratories ($CRL)

10.4 Fortrea Holdings ($FTRE)

New Stock Addition: Best-in Class CRO

11.1 Company Overview

11.2 Why It Is Well Positioned for the Theme

11.3 Competitive Landscape

11.4 Financial Analysis

11.5 Investment Thesis

11.6 Why Now & Recent Developments

11.7 Financial Forecasts and Price Target

11.8 The Bear Case/Risk

11.9 Conclusion

Forecasting Total Return For Major Public CROs