Japan Field Trip: One of the Most Compelling Opportunities in Global Equities

Best-positioned sectors, top stock ideas, and a full Japanese equity basket from our analyst in Japan.

Aurelion Research’s goal has always been to identify the best risk-to-reward investments across sectors or geographies. Because we cast such a wide net (and this is what we do every day), we are able to catch compelling setups across investment themes before they get crowded.

However, this can come with a downside, as sometimes you miss local expertise and what is actually being said on the ground. While we like calling someone in that geography, it is never as good as being there multiple days and seeing it with your own eyes.

We have already highlighted Japan in three articles this year (mainly the capital markets side, we go into many other sectors here) and since then, their index and markets are up significantly YTD. Despite the recent increase, we believe the timing is right to enter more significantly Japanese equities given the improved visibility on what is setting up as a fabulous coming years for the country.

This is not just some travel notes. We discuss:

Why Japan is such a strong opportunity

Attractive sectors in Japan and well-positioned companies

Our complete Japanese equity basket

If you are only interested in the concise, actionable part of this thematic equity primer, you can have a look at the more detailed table of contents below. However, you’ll better understand in this intro why the opportunity in Japan is so compelling that we sent our analyst there.

Sadly we do not have Goldman Sachs’ million-dollar travel budget, so why Japan?

Japan is known for a more reserved investor relations culture. Many smaller public companies do not provide English translations. The focus is strongly long term, which makes timing investments more difficult. It may be one of the most widely invested markets globally that local investors have a substantial informational advantage over foreign investors. Right now, Japanese households are increasingly allocating capital to equity markets, which is another reason, in addition to macro factors we discuss below, why the country is well positioned.

The Tokyo Stock Exchange is now forcing companies to improve their financial metrics. While every company claims they are complying on paper, many smaller firms lack English investor relations teams. Being there in person allows you to meet management teams directly to see which company has created plans just to comply and which ones have actual plans to drive shareholder returns.

Global mega-funds have poured billions into Japan over the last year, but they have crowded into the same few massive, famous ones. Hundreds of smaller, highly profitable companies are completely ignored by foreign analysts. International investors are starting to enter Japan, and companies are beginning to shift their marketing and communications toward English:

Our analyst has been learning Japanese for a while and wanted to visit the country, so that makes for a great two-in-one. Also, you should expect another article related to Japanese equities (maybe a stock added to our portfolio), as we have quite a few meetings with Japanese companies coming up.

We also want to note that we are not adding a stock to our main portfolio, the Aurelion Index, but rather creating an equity basket to express our bullish view on sectors in the country. The main reason is that most of the Japanese stocks below exceed the minimum investment on Plutus, where the platform is hosted. We also have meetings coming up with other Japanese equities (that have lower minimum investments) that could potentially be added.

Our analyst landed in Tokyo on June 4, 2026, has spent a few days there, and is now in Osaka, the second-largest city and, according to him, much more friendly than Tokyo. He says the most important thing to do when visiting the country is to arrive with an empty stomach since the food is just so good.

For some of the companies discussed below, he was able to visit their headquarters and sometime speak with employees (in his limited Japanese).

Table of Contents

Japan Research Trip: Introduction

Thematic Approach: Top-Down & Bottom-Up

Theme 1: Automation & Robotics

2.1 Stock Idea: NSK Corp. (6471-JP)

2.2 Stock Idea: Nabtesco Corp. (6268-JP)

Theme 2: Glass & Ceramic (Materials)

3.1 Stock Idea: Nichias Corp. (5393-JP)

Theme 3: Banks & Financials in Transition

4.1 Stock Idea: Mizuho Financial (8411-JP)

4.2 Stock Idea: Suruga Bank (8358-JP)

4.3 Stock Idea: Nomura Holdings (8604-JP)

4.4 Stock Idea: Ichiyoshi Securities (8624-JP)

Japan’s Economy: Where Does It Stand Today?

Japanese Equity Basket: Top Ideas from the Ground

On-the-Ground Findings

Key Risks

Our Final Take on the Japanese Market

1. Thematic Approach: Top-Down & Bottom-Up

Our investment process combines top-down macro analysis with bottom-up fundamental research. The goal is to make sure every position is supported by a strong long-term theme while also meeting strict valuation and company quality criteria. We treat both approaches as one framework to identify high-conviction ideas, focusing on areas where shifts are still underpriced by the market.

The top-down stage focuses on identifying large macro trends and fundamental shifts in the economy. This includes areas where investment has been limited for years, or where new technology is creating strong demand for specific physical components. Examples include automation, semiconductor equipment, and industrial logistics. In Japan, these trends are especially important given the country’s deep industrial base and role in global supply chains. This step helps narrow the investable universe to sectors with clear long-term tailwinds.

Once a theme is identified, we move to bottom-up analysis.

This focuses on individual companies, looking at financial strength, cash flow generation, market position, and management quality. In Japan, this often highlights firms with strong balance sheets, niche global dominance, and improving capital allocation through dividends and buybacks.

We prefer businesses that sit in critical parts of global supply chains and are starting to shift toward higher-value products or services.

By combining both approaches, we aim to avoid overpaying for hype and instead focus on companies that are both structurally supported and financially strong.

2. Theme 1: Automation & Robotics

Everyone loves hyping up the artificial intelligence boom and smart factory software. Writing the most brilliant code on earth becomes completely useless the moment a robotic arm shakes while trying to tighten a bolt. The entire automation boom actually bottlenecks at the physical joints and gears.

Evaluating this sector requires drawing a strict line between the companies that assemble the final robots and the companies that forge the internal parts.

For decades, Japanese brands defined the modern factory floor by building massive, single purpose industrial arms. Today, that legacy manufacturing business faces significant challenges. The big money is rapidly pivoting away from machines that blindly repeat one programmed motion. The global market is chasing general purpose robots powered by advanced artificial intelligence. We are talking about agile systems that learn from experience and perform a wide range of tasks across completely different settings.

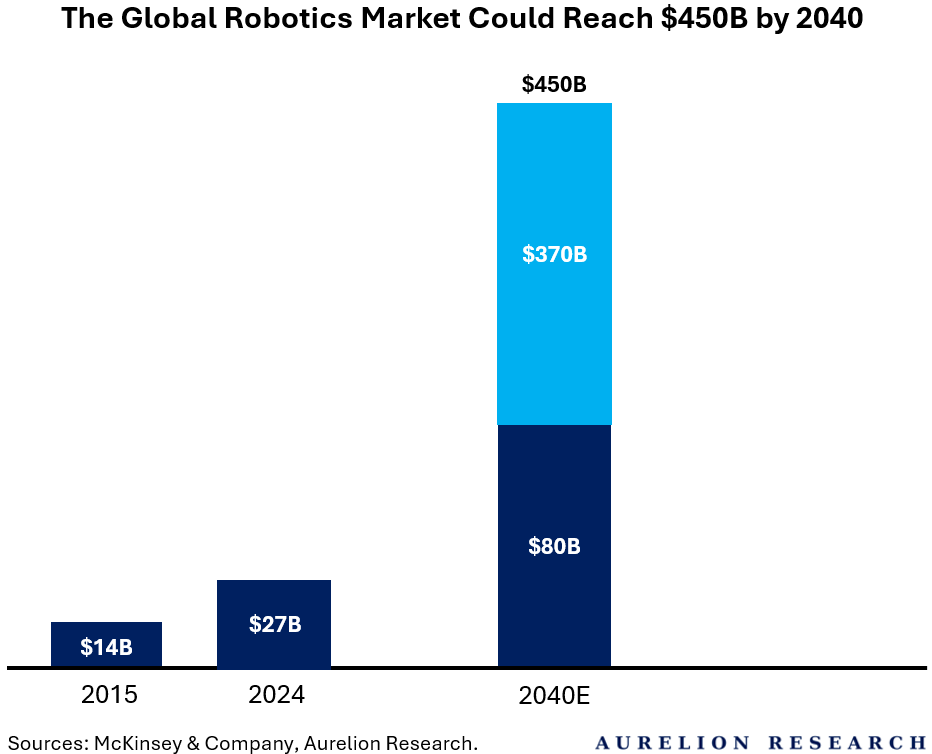

The numbers show a growing challenge for traditional robotics manufacturers. Industrial robot demand is expanding at a relatively modest pace compared with the broader intelligent automation market, projected to reach $370B by 2040.

China continues to invest aggressively in manufacturing scale and cost competitiveness, while the US is directing significant capital toward AI and software development. In this environment, Japanese robot manufacturers will need to strengthen their software capabilities and AI integration to maintain their competitive position as automation systems become increasingly intelligent.

We believe this dynamic creates a challenge for investors seeking exposure to automation. Rather than focusing on companies competing to sell the final assembled robot, we prefer to focus on specialized component suppliers.

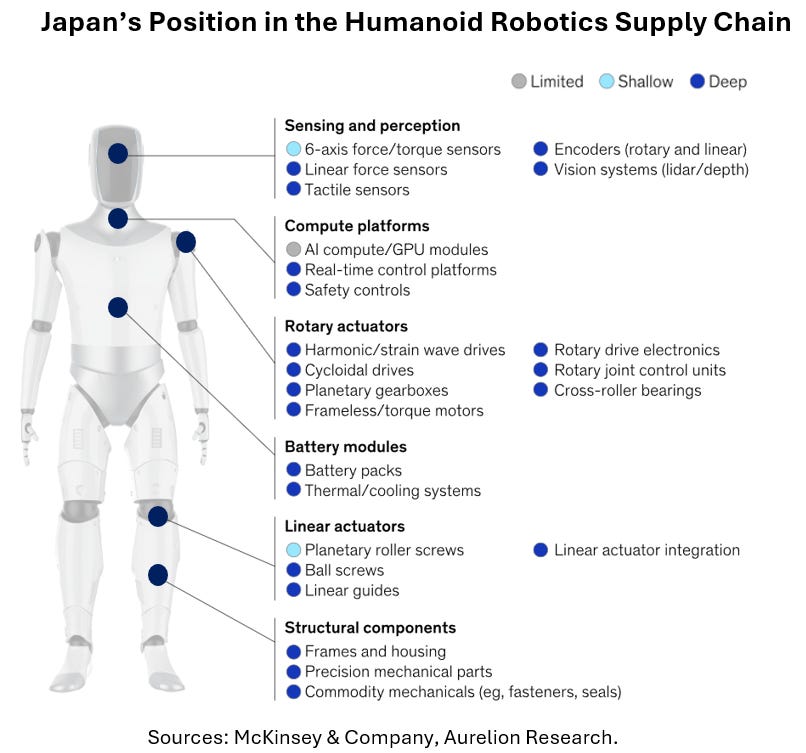

For Japanese equities, these businesses provide exposure to the growth of automation and robotics while benefiting from a broad customer base and limited dependence on any single platform. We see the most compelling opportunities in companies producing precision gearboxes, linear motion guides, and heavy-duty bearings. These components translate digital commands into precise physical movement at the mechanical level.

Precision Gears for Robotics

The durability of this model is based on physical constraints.

Unlike software, precision hardware cannot be updated quickly; it requires long development cycles, specialized metallurgy expertise, and highly capital-intensive manufacturing. These components also operate under constant mechanical stress, often running 24 hours a day, which places strict demands on reliability.

As a result, once a supplier proves consistent performance, particularly in components such as harmonic drives or strain wave gears, relationships tend to last due to strict qualification requirements and high switching costs.

Beyond core motion systems, component manufacturers are expanding into higher-value areas such as planetary roller screws, multi-axis force sensors, and tactile sensors that enable robotic feedback. This reflects a gradual shift from standalone parts toward more integrated subsystems that combine hardware and built-in control functions. These companies also benefit from strong positions in high-reliability end markets such as healthcare, elder care, and defense, where purchasing decisions prioritize proven performance over cost.

High-Precision CNC Manufacturing for Humanoid Robots

Ultimately, advanced robotics systems cannot function without ultra-precision mechanical components. While global competition is intensifying in robot platforms and software systems, the underlying motion hardware remains highly specialized. China may lead in scale, and the U.S. in software, but both still depend on high-precision mechanical suppliers to build working systems.

And this is where Japan enters the game. This supports focusing on the component level, where exposure is linked to the broader expansion of industrial automation rather than competition between individual robot manufacturers.

We now turn to our first stock idea, which best represents this core thesis.

2.1 Idea: NSK Corp. (6471-JP) - Machinery

NSK is a compelling industrial transformation story, sitting at an inflection point between its legacy automotive-heavy business and a growing exposure to robotics and advanced motion systems. While bearings remain the core profit base today, it is gradually repositioning toward higher-value applications in actuators, integrated motion systems, and product lifecycle management (PLM).

We see the key investment case in the gradual upgrading of its product mix. Demand is shifting toward more precise and intelligent motion systems, particularly in robotics and advanced manufacturing equipment.

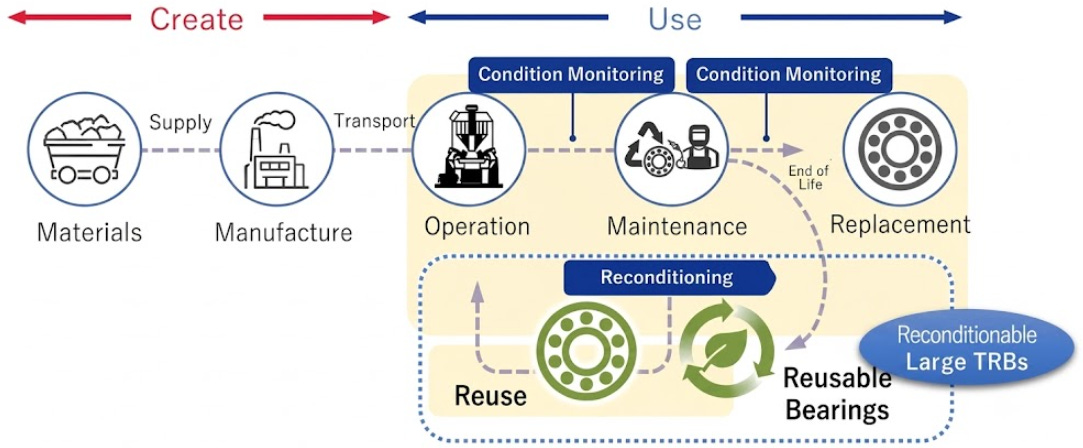

Actuators, which function as the mechanical “muscle” of robots, are a key focus of this transition, alongside system-level solutions that integrate motion and control rather than individual components. At the same time, NSK is developing PLM capabilities that extend the business model beyond one-off hardware sales toward longer-term service relationships, including monitoring, maintenance planning, and replacement cycles. This increases the connection between installed equipment and recurring revenue streams over time.

PLM (Product Lifecycle Management) Model

Overall, we view NSK as being at an early-stage inflection where its stable but mature bearings business continues to generate cash, while incremental exposure to robotics and advanced automation creates a longer-term re-rating opportunity.

We believe this shift is important because it moves the business model from selling individual parts to providing more complete motion solutions. Bearings remain the main source of stable cash flow, but are increasingly viewed as a mature, lower-growth segment that helps fund the transition.

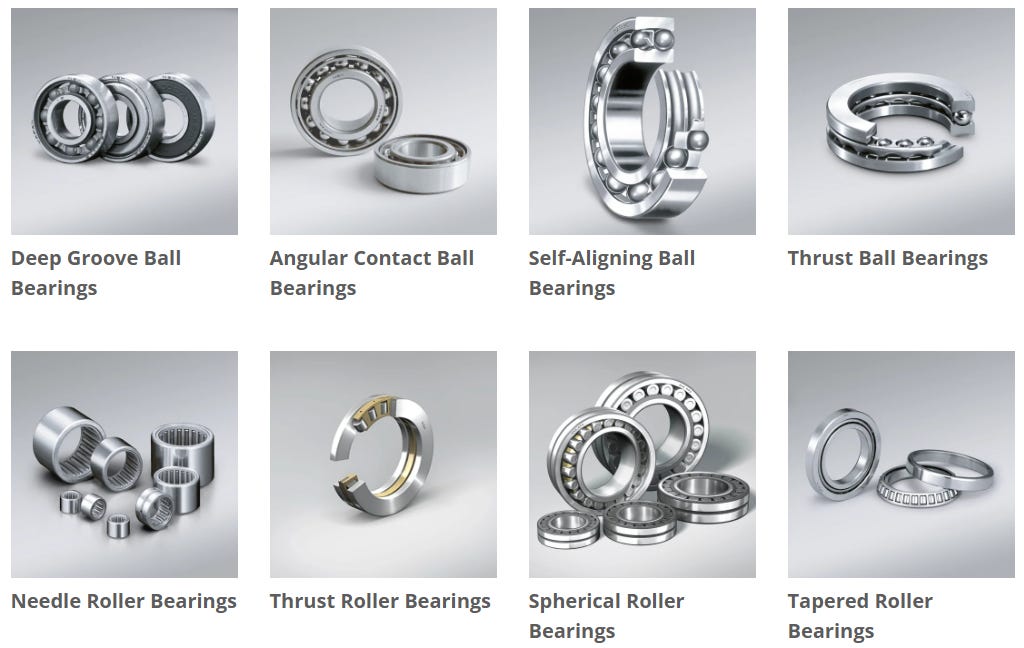

Here is an example of the products they manufacture, which include core mechanical components such as bearings that are widely used in robotics, machine tools, and a broad range of industrial applications.

Main Catalysts Ahead

The most important catalyst is the planned integration with NTN Corporation. Announced in May 2026, the companies signed an agreement to create a joint holding structure, with completion expected in October 2027. The combined group would generate over ¥1.7T in annual revenue.

We see this as a major consolidation step in the Japanese bearing industry, aimed at reducing direct competition, improving scale efficiency, and strengthening the combined group’s ability to invest in next-generation motion technologies such as robotics and advanced industrial systems. The main objective is scale and efficiency: reducing overlap, improving procurement, and increasing investment in next-generation technologies such as robotics and predictive maintenance.

Another key initiative is the partnership with Accenture.

This focuses on improving efficiency through automation and artificial intelligence across manufacturing and internal operations.

“Partnering with Accenture represents a bold step in NSK’s evolution toward a management model that continuously drives structural reform and growth investment in tandem,” said Akitoshi Ichii, President and CEO of NSK. “At its core, this collaboration is about management reform that unlocks the full potential of our frontline workforce. Through talent development and skills advancement, we will strengthen operational capabilities.”

The goal is to reduce costs and redirect resources toward higher-value product development. Finally, NSK is simplifying its business structure. We believe the separation of the automotive steering business into a standalone unit reflects a gradual move away from lower-growth legacy activities, allowing the company to focus more on robotics, actuators, and advanced motion systems.

The Financials: Funding the Transition

The near-term financial outlook shows a stable business, providing a reliable cash base to support its long-term transformation. Management expects net sales of around ¥1T and operating income of ¥42B for the upcoming year. This should generate sufficient cash to fund investment in new growth areas, while demand in traditional machine tool markets continues to stabilize globally.

The core operation of making bearings and heavy mechanical parts is acting like a steady, predictable cash machine right now. Instead of borrowing money or taking on heavy debt to kickstart their robotics pivot, they are completely self funding the entire operation. They are taking the predictable profits from their old school factory clients and using that cash to build out the high tech supply chain of tomorrow. This financial cushion gives them a secure runway to shift toward higher margins without worrying about near term market disruptions.

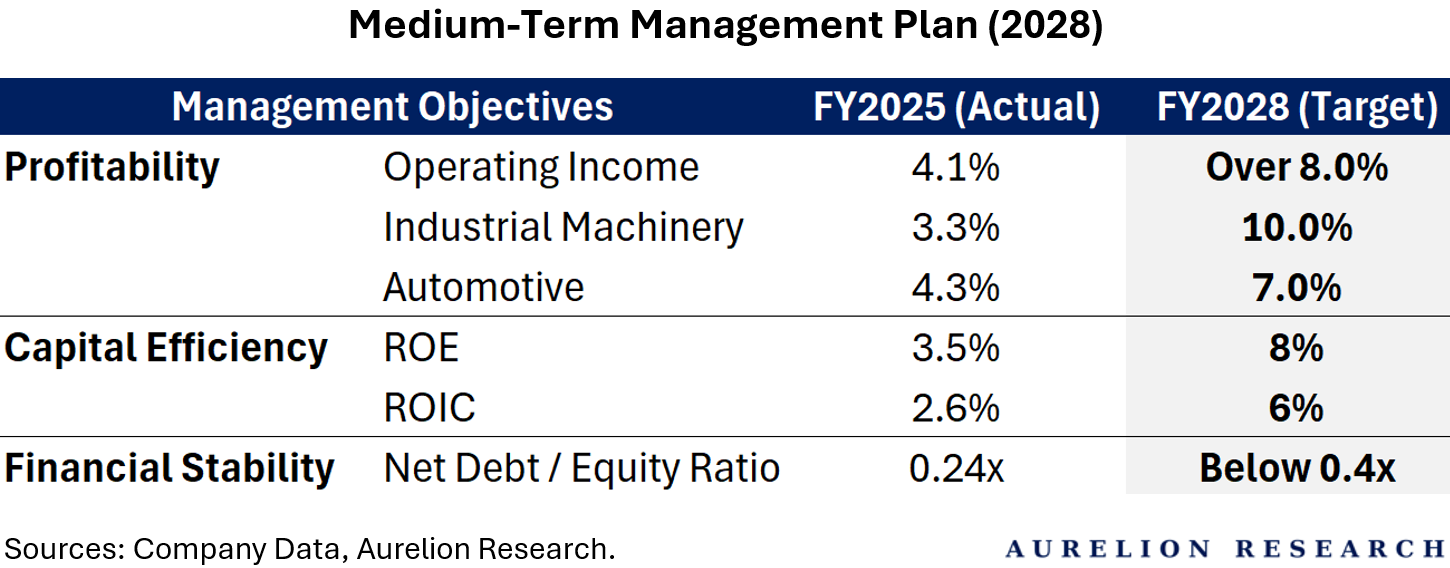

Medium-Term Management Plan (2028)

NSK’s plan outlines a clear push to reshape the profitability profile of the business by FY2028, with a focus on turning scale into higher-quality earnings.

Profitability: Operating margins are expected to more than double from 4.1% to above 8.0%. The main driver is the industrial machinery division, where margins are targeted to rise from 3.3% to ~10% as higher-value automation components gain share. The automotive segment is also expected to improve, moving from 4.3% to 7%, supported by a continued exit from lower-margin products.

Capital efficiency: The focus is on making capital work harder. ROE is targeted to rise from 3.5% to 8%, while ROIC increases from 2.6% to 6%, reflecting more disciplined capital allocation and improved returns from core operations.

Financial discipline: This improvement is expected to be achieved without stretching the balance sheet. Net debt-to-equity is expected to remain below 0.4x, keeping the company flexible while it executes this transition.

What About Valuation?

NSK currently trades at an NTM EV/EBITDA of 3.3x, a level we view as reasonable given the company’s transition toward higher-value robotics and automation exposure. This valuation is further supported by a very conservative balance sheet, with minimal net debt and a solid cash position. In our view, this creates an attractive risk-reward setup, with limited downside given the balance sheet strength and meaningful optionality from the ongoing business mix shift.

Our Final Take on NSK

Overall, we see NSK as an industrial business in transition, with a stable bearings base continuing to generate cash while incremental exposure builds in robotics, actuators, and more advanced motion systems. The opportunity lies in this gradual mix shift, where improving capital efficiency and optionality in next-generation applications support the longer-term equity story.

2.2 Idea: Nabtesco Corp. (6268-JP) - Heavy Robotics

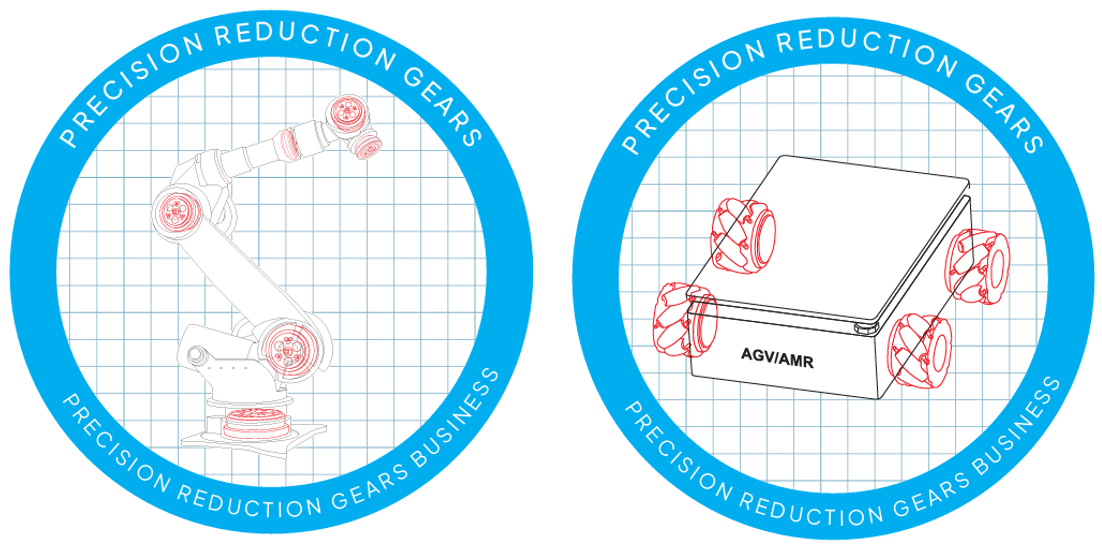

We think Nabtesco plays a critical role within the robotics ecosystem. Nabtesco is an industrial equipment company currently going through a massive transformation. The core of their business is making precision reduction gears for heavy robotics. To put it simply, these gears act as the joints of a robot arm.

They take the fast spinning of an electric motor and turn it into smooth, heavy lifting power that can stop exactly where it needs to down to the millimeter. Because these parts require extreme precision, Nabtesco holds a massive global market share and faces very little direct competition.

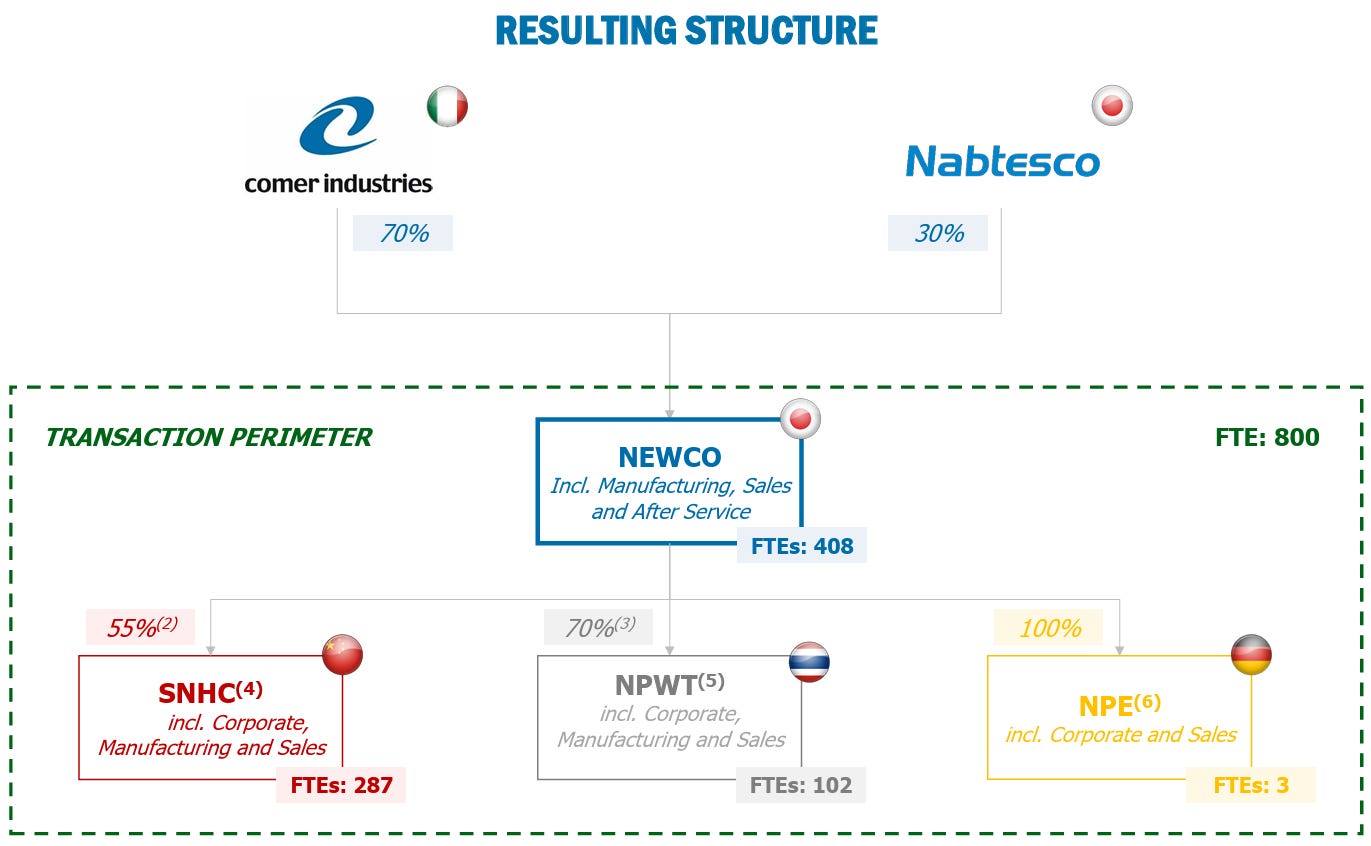

The main reason we are looking at them now is a major change in what they sell. On January 1, 2026, management finalized a deal to move 70% of their older, less predictable hydraulic equipment division into a joint venture with Italy based Comer Industries. By removing this volatile construction machinery segment, Nabtesco becomes a much cleaner and highly focused robotics company.

We expect this deal to free up cash and management focus, allowing the company to concentrate more on the higher-value automation market.

The financial results are already showing that the business is turning a corner. On April 30, Nabtesco reported first quarter revenue of ¥83B, beating market expectations easily. Their operating profit jumped nearly 70% to reach ¥8.2B.

The most important detail from that report was the gear division, which saw sales grow by ¥4.8B in just three months. This growth tells us that the long period where customers were just burning through old inventory is officially over. Factories are finally spending money again and ordering new parts.

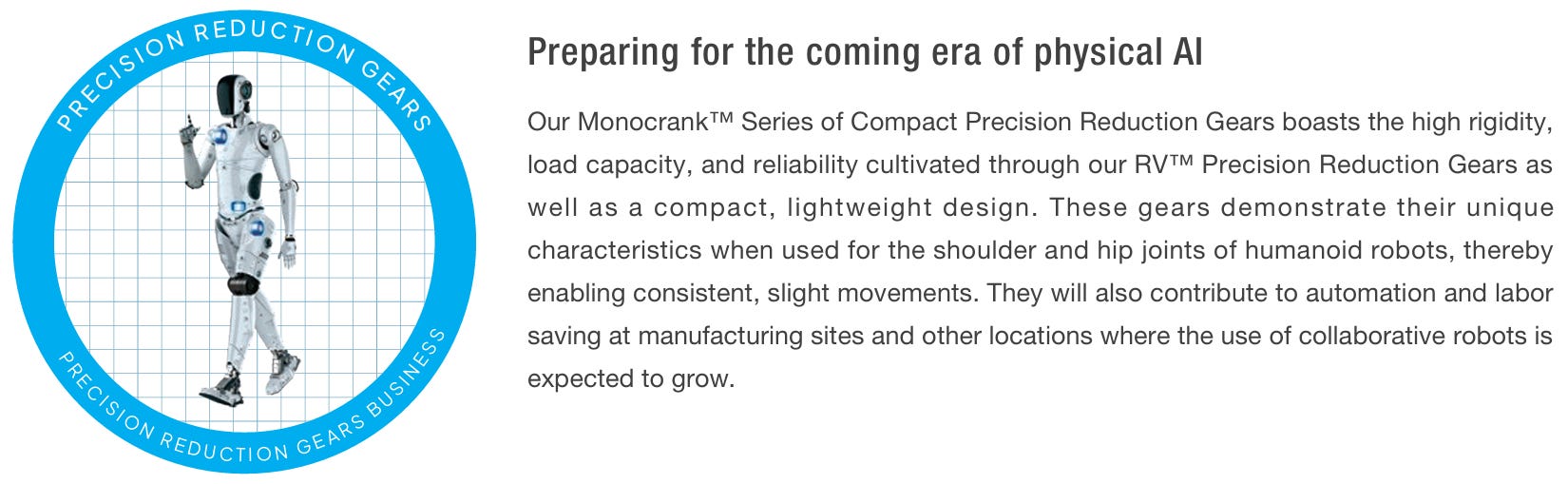

They are also preparing for the coming era of physical AI, which in our view is already at the door. The company has developed a Monocrank product, a series of compact precision reduction gears designed for high-precision motion control.

These systems are engineered to deliver high rigidity and strong load capacity in compact formats, making them suitable for advanced robotics and automated machinery where accuracy and durability are critical.

Looking ahead, management expects to bring in ¥327B in sales and ¥27.7B in operating income for the full year 2026. Because they dominate their specific niche, their operations generate enough cash to fund their own growth.

They do not have to rely on expensive debt to build new factories or develop new technology. They have a very clean balance sheet, and the market is still pricing them as a slow moving industrial conglomerate rather than a focused automation play. We view this as a great opportunity to own a critical piece of the global robotics supply chain right as factory demand is waking back up.

What About Valuation?

Nabtesco currently trades at a next twelve months EV/EBITDA multiple of 10.3x, which we view as reasonable given its ongoing business mix shift. The company holds a strong position in critical motion control components used in factory automation, placing it within an important part of the robotics supply chain.

While software and cloud businesses continue to trade at higher multiples, we believe long-term value also exists in the physical infrastructure that enables automation. At current levels, investors gain exposure to core robotics hardware at a relatively modest valuation. In addition, the separation of the legacy heavy machinery division reduces cyclicality and simplifies the business profile.

This makes Nabtesco easier to understand as a more focused automation components company. Overall, we see a stable setup, supported by solid cash generation and some optionality if the market begins to re-rate the business toward its automation exposure.

Our Final Take on Nabtesco

Nabtesco generates stable industrial cash flow while gradually increasing its exposure to precision components used in factory automation. The business remains tied to mature end markets, but its role in robotics-related systems gives it a clearer direction over time. Recent simplification of the business improves visibility and reduces cyclical noise. Overall, we see a steady industrial name with optionality linked to automation demand over the medium term.

3. Theme 2: Glass & Ceramic (Materials)

The global expansion of artificial intelligence infrastructure is accelerating a critical transition within the glass and ceramics sector. While software and applications capture public attention, we believe the physical bottleneck remains centered on advanced hardware production. The market focus slowly but surely is shifting away from speculative software models and moving directly toward the specialized materials essential for manufacturing next generation processors. We expect the accelerating buildout of data centers to eventually translates directly into surging demand for semiconductor production equipment (SPE) components.

Why We Believe This Theme Is Compelling

We see this theme as a compelling investment case, offering a pure “picks and shovels” exposure to the AI buildout. Designing faster chip architectures is of limited value if fabrication facilities cannot physically manufacture the silicon at scale. As semiconductor geometries continue to shrink toward increasingly advanced nodes, the manufacturing process requires higher levels of thermal stability and chemical purity. Glass and ceramic material suppliers play an important role in enabling this technological progress.

Specialized materials, including high-purity quartz and advanced technical ceramics, are essential inputs used in the extreme environments of modern lithography and etching equipment. By focusing on the material layer, we gain direct exposure to the billions of dollars flowing into data center infrastructure while avoiding the binary risks tied to software platforms or individual chip designers. These suppliers benefit from strong underlying advantages, high switching costs, and meaningful pricing power, which supports their ability to capture a durable and highly profitable share of the technology cycle.

Current Inflection & Macro Drivers

The transition from factory construction to active equipment installation marks a key catalyst for the sector. Global semiconductor manufacturing capacity is experiencing a major geographic expansion, with large-scale capital expenditure turning into physical tool orders. Like we said earlier, these specialized glass and ceramic parts are consumable elements that degrade during production, meaning a larger installed base of equipment directly triggers a compounding replacement cycle. We are witnessing an inflection where volume demand accelerates as advanced manufacturing facilities scale up operations.

Automation in Semiconductor Manufacturing

The Industrial & Energy Baseline

Complementing this growth, the defensive portion of the sector is supported by shifting global utility frameworks, particularly the accelerating momentum behind nuclear power plant restarts. Nuclear energy infrastructure operates under strict regulatory mandates that dictate scheduled component updates irrespective of macroeconomic trends. We believe this dynamic creates a reliable consumption cycle for premium seals, specialized gaskets, and insulation. This baseline provides a great counterweight to the cyclical semiconductor market, stabilizing overall corporate cash flow and protecting aggregate margins.

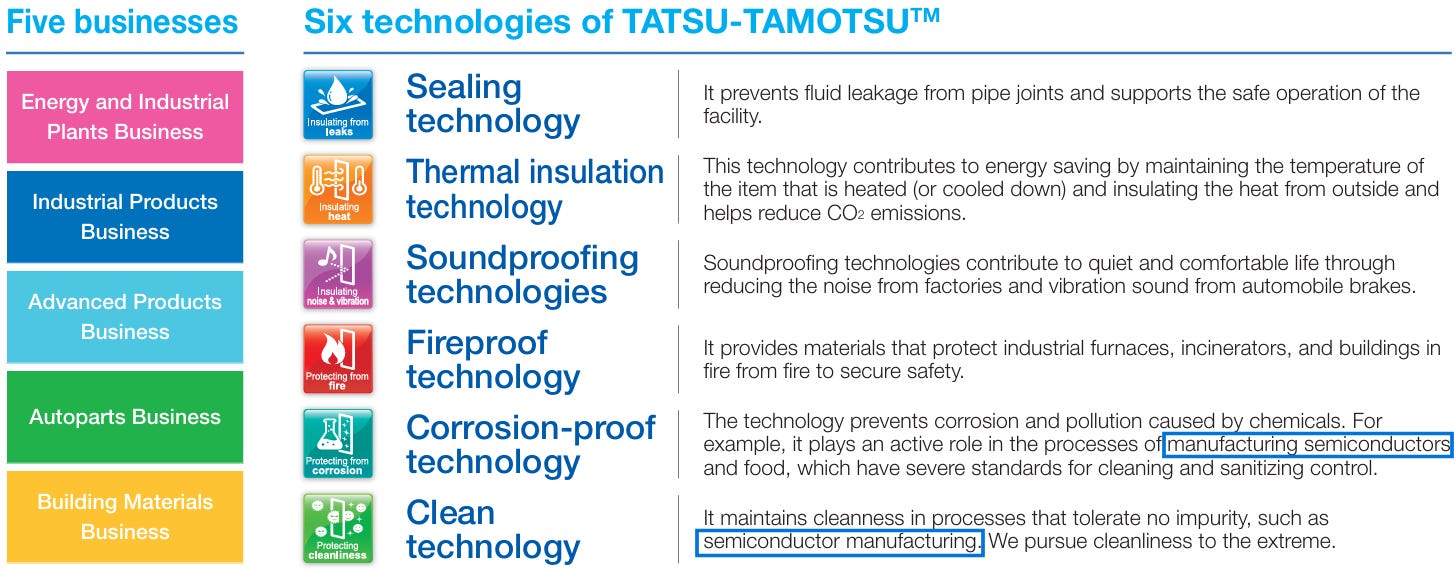

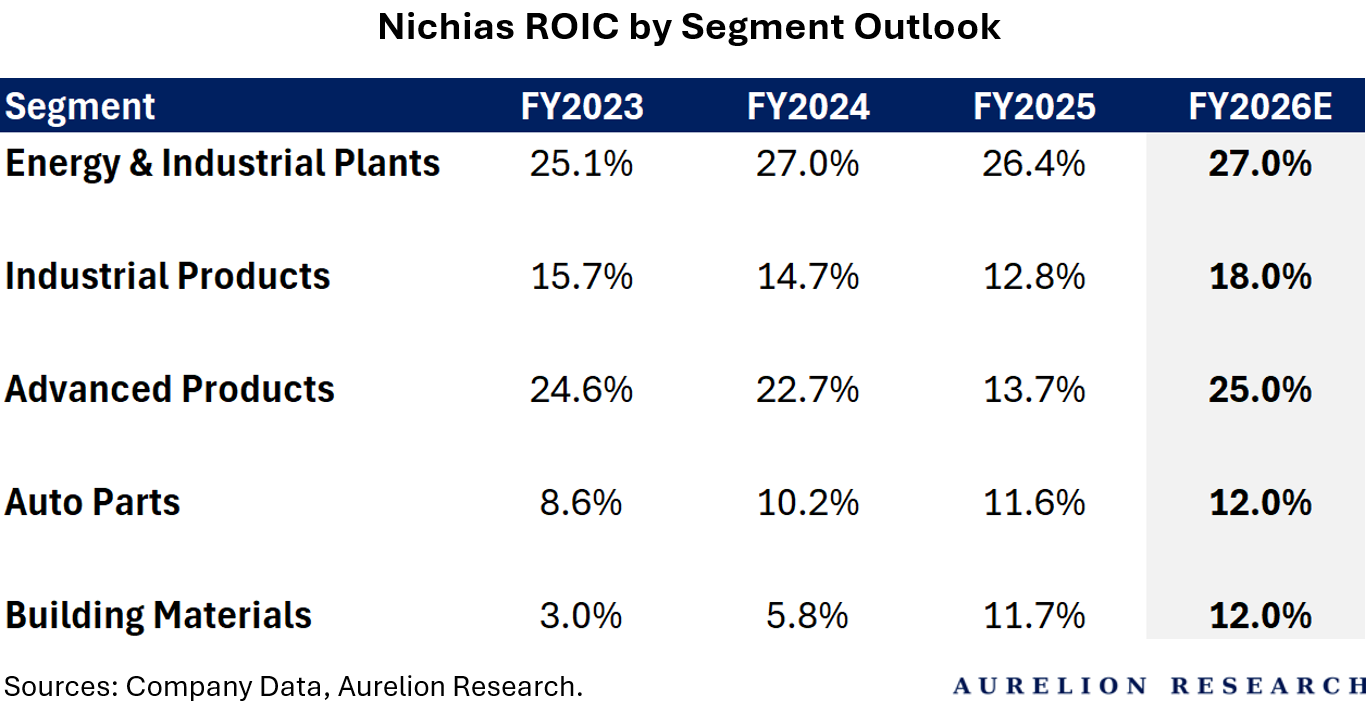

3.1 Idea: Nichias Corp. (5393-JP) - Thermal Insulation

Nichias aligns well with our investment thesis in the glass and ceramics sector. It operates across five segments: plant construction and sales, industrial products, high performance products, automotive parts, and building materials.

While legacy activities provide a stable earnings base, the main growth drivers are concentrated in the high performance and industrial segments. These divisions position the company to benefit from demand in advanced Semi manufacturing as well as nuclear energy-related maintenance and restart activity.

Key Product Categories

Semiconductor Equipment & Material Advantage

Within the high-performance products segment, Nichias is exposed to the Semis equipment supply chain through high-purity seals and precision thermal insulation used in production tools. However, it is not a direct pure-play, which in our view adds a degree of diversification and reduces single-end-market risk.

As chip manufacturing shifts to more advanced nodes, process conditions become more demanding, which increases wear on these components and drives a replacement cycle linked to fab utilization rates. This positions Nichias within a consumable part of the Semi value chain, linking it to capital investment in chip manufacturing capacity and the ongoing expansion of data center infrastructure.

Energy & Industrial Plants Business (31.6% of Revenue)

This division stabilizes corporate earnings by turning heavy industrial engineering projects into a predictable maintenance service. The team specializes in thermal insulation work, meaning they wrap massive factory piping networks in heat trapping materials to prevent energy loss and reduce carbon emissions.

To minimize disruption for clients, technicians use a specialized heat retention recovery method to fix or replace insulation on active, fully running pipelines. They also deploy mobile service trucks that act as rolling fabrication shops, driving directly to a customer site to cut and fit custom seals immediately.

We think the primary driver to monitor here is the expanding schedule of nuclear power plant restarts in Japan. Nuclear facilities are subject to strict safety regulations that require routine component updates and insulation replacements on a fixed timeline, largely independent of economic conditions.

Through close integration with these high-security utility networks, we expect Nichias to secure long-term, high-margin maintenance contracts that help stabilize revenues even during broader economic slowdowns.

Industrial Products Business (19.6% of Revenue)

This business serves as the foundational cash cow that funds the company’s broader capital allocation strategy. The product catalog centers on everyday, high volume safety consumables that heavy factories require to remain operational.

This includes industrial gaskets, which are specialized sealing rings squeezed between pipe joints to stop high pressure steam, oil, or toxic chemicals from leaking out into a facility. It also covers rock wool insulation, created by melting natural stone and spinning it into fireproof fibers to protect industrial furnaces, as well as durable pipe linings that protect steel infrastructure from corroding when transporting abrasive fluids.

While we believe this segment does not offer the same growth pace as the semiconductor-related division, it provides a stable and defensive revenue base. Heavy manufacturing plants simply cannot operate without these sealing and safety products. They depend on them for continuous operation and safety compliance. Because these components must be regularly replaced as they wear out, the division generates recurring cash flows over time.

Advanced Products Business (16.8% of Revenue)

This segment is the company’s main growth engine and serves as a key partner to semiconductor equipment manufacturers. Instead of producing basic materials, it focuses on advanced components that chip factories need to replace regularly.

For example, it manufactures fluid transport systems made from PFA, a high-performance plastic designed to withstand very high temperatures and strong chemicals without breaking down or contaminating silicon wafers. It also produces piping heaters that keep process gases at stable temperatures to prevent blockages in production lines, as well as advanced chemical filters that remove microscopic particles before they can damage chips.

As semiconductor features continue to shrink, we expect the manufacturing environment to become more demanding. The specialized plastic and rubber components supplied by Nichias naturally wear out under these conditions, meaning they must be replaced regularly. This creates a steady replacement cycle, turning what would otherwise be a traditional industrial business into a more recurring revenue stream that grows alongside global data center demand, while reducing exposure to the boom-and-bust cycles of the broader technology sector.

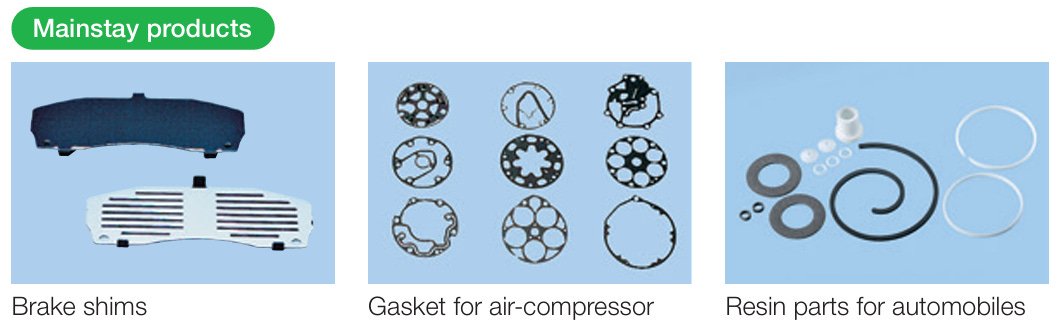

Autoparts Business (20.7% of Revenue)

This is a mature legacy division that functions as a near term cash contributor rather than a target for future expansion capital. Nichias supplies major automakers with brake shims, air compressor seals, and heat resistant resin parts.

Brake shims are thin rubber or metal layers fitted onto the back of brake pads to dampen vibrations and stop cars from squealing when they slow down. The division also produces protective barriers that insulate delicate vehicle electronics from intense engine compartment heat.

Profitability remains stable today, supported by decades-long relationships with leading automotive manufacturers. However, the automotive industry is undergoing a gradual shift from internal combustion engines toward electric powertrains. Since EVs do not require conventional gas engines, complex air compressors, or traditional surrounding insulation systems, we expect part of this product range to face a shrinking addressable market over the next decade.

As a result, we view this segment more as a steady source of cash to be harvested and reinvested elsewhere, rather than a driver of future equity upside.

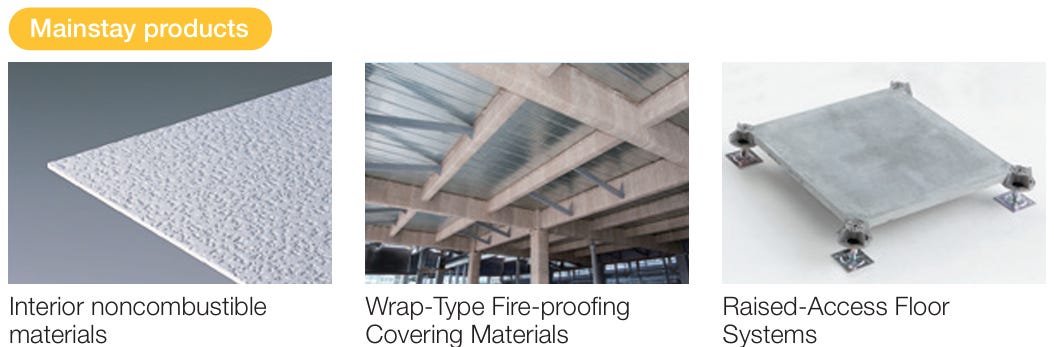

Building Materials Business (11.3% of Revenue)

This division is the least critical element of the core investment framework, operating as a localized domestic business inside Japan. The portfolio includes fireproof ceiling and wall panels for commercial buildings, flexible fireproofing wraps for structural steel beams, and raised access flooring systems.

We think this segment faces growth limitations as it is closely tied to commercial office construction and renovation cycles within a highly mature Japanese real estate market. This limits its global scalability and pricing power compared with segments such as semiconductors or nuclear energy.

Its primary role within the corporate structure is to keep local factories operating at high utilization and absorb manufacturing overhead, rather than to act as a meaningful driver of future earnings growth.

That said, there is one positive: it provides a stable, predictable base of activity that helps overall group operations through the cycle. This includes products such as raised flooring systems, which are widely used in corporate offices and data centers to create underfloor space for power and data cable management.

Capital Allocation & Enhanced Returns

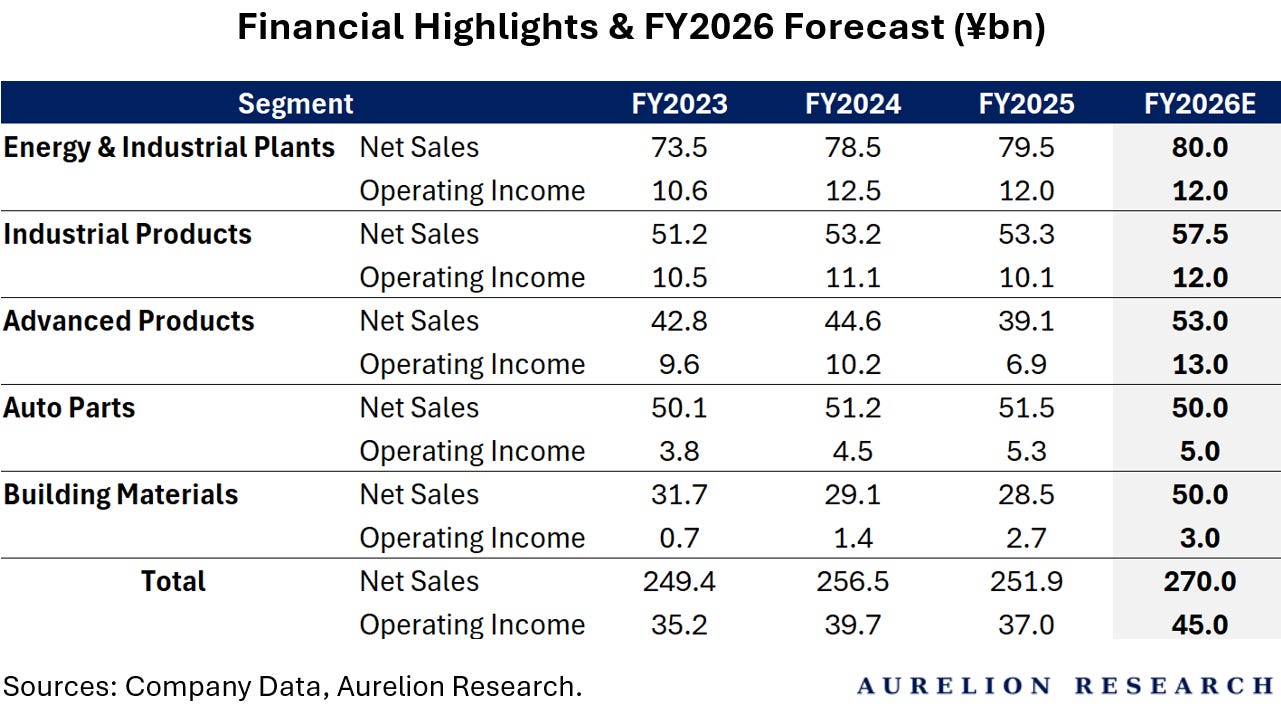

Nichias is currently shifting its business mix from a stable industrial player toward a higher-margin technology supplier. For FY2026, the company targets net sales of ¥270B, representing an increase of ¥18.1B YoY. Growth is primarily driven by the advanced products segment, which contributes ¥13.9B, offsetting softer trends in legacy automotive and building materials businesses.

This shift supports stronger operating leverage, with operating income forecast at ¥45B, up ¥8B versus FY2025, helping absorb rising domestic labor costs.

Nichias has structured this expansion within a disciplined two-year capital framework of ¥83B. This is funded by ¥66B in operating cash flow and ¥17B in cash on hand. Capital is allocated across three areas:

Growth investment (¥24B): Capacity expansion and recurring capex to support demand visibility.

Strategic investment (¥29B): R&D and automation initiatives, including infrastructure such as its liquid hydrogen experimental facility.

Shareholder returns (¥30B): Direct returns to investors through dividends and buybacks, with ¥18.4B already distributed through FY2025.

For FY2026, management is increasing distributions.

The company is guiding to a total annual dividend of ¥65 per share, consisting of a ¥58 ordinary dividend and a ¥7 special dividend linked to its 130th anniversary. In addition, Nichias is launching a share buyback program of up to ¥5B.

This mix shift is already flowing through the income statement. Operating income is forecast at ¥45B, up ¥8B versus FY2025, giving the company more flexibility to absorb higher costs while continuing to invest in growth areas.

Expected Recovery Across Key Segments

The Energy & Industrial Plants segment remains the stable earnings base of the business. The main focus, however, is the FY26E recovery profile across the rest of the group. Following a weaker FY25, both Advanced Products and Industrial Products are expected to rebound, while Building Materials and Auto Parts continue to show steady, gradual improvement.

That said, the assumptions for Advanced Products are demanding. A near doubling in returns within a single year is a high bar, and it will depend on whether demand actually picks up as expected. At this stage, delivery on execution and demand trends matter more than the upside shown in the model.

A Look at Valuation

The stock trades at 11.5x NTM EV/EBITDA and 20.4x NTM P/E. While the EV multiple looks reasonable for an industrial transitioning into higher-value components, the earnings multiple reflects that a lot of the re-rating is already priced in. At this level, returns depend less on multiple expansion and more on execution in the advanced products segment and continued margin delivery.

4. Theme 3: Banks & Financials in Transition

We believe the narrative for Japanese financials is shifting away from a simple recovery trade toward a more durable margin expansion story, driven by Bank of Japan rate normalization. In simple terms, rates are moving up from extremely low levels toward more normal conditions after years of near-zero policy, which allows banks to earn more on loans and reinvest cash at higher yields.

A terminal policy rate of 1.25% and 10-year JGB yields above 2.0% by early 2027 would meaningfully improve earnings for megabanks, as higher domestic yields feed directly into lending spreads and reinvestment income. Under a 1.5% policy rate scenario, and excluding volatile equity gains, this translates into stronger net interest income and improved profitability.

The key point is operating leverage: as interest rates rise, revenue increases faster than costs. This supports a path for ROE to move toward the 13% range, which in turn could justify higher price-to-book multiples above 2.0x over time.

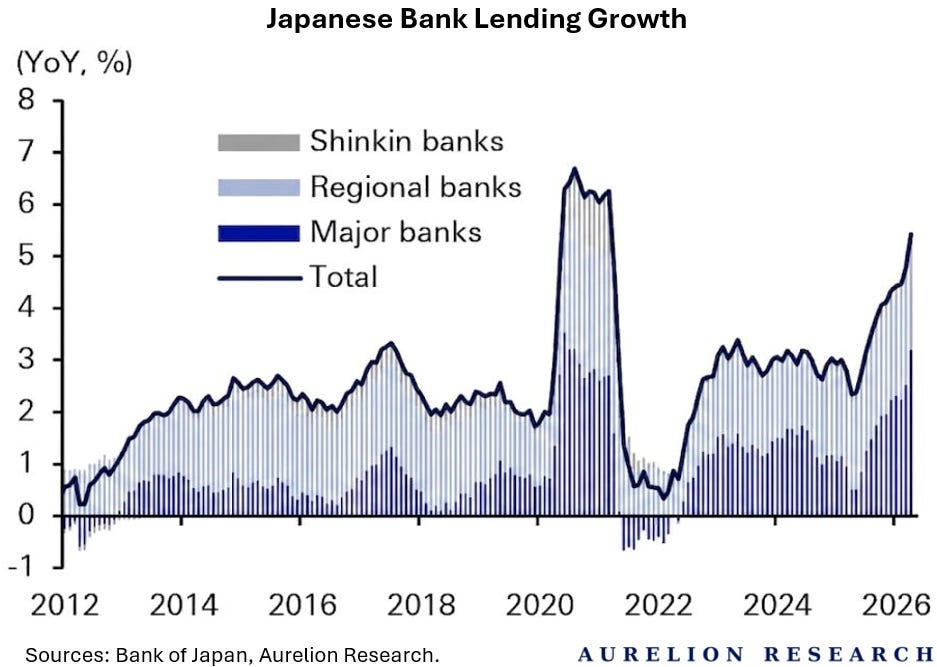

This improvement is also happening alongside a clear pickup in domestic lending, with Japanese bank loan growth rising to over 5% YoY in 2026.

The key shift is that banks are increasingly relying on real loan growth rather than financial market income or portfolio effects. In other words, they are deploying more capital into a growing domestic credit market, where higher interest rates also improve returns on each loan they make.

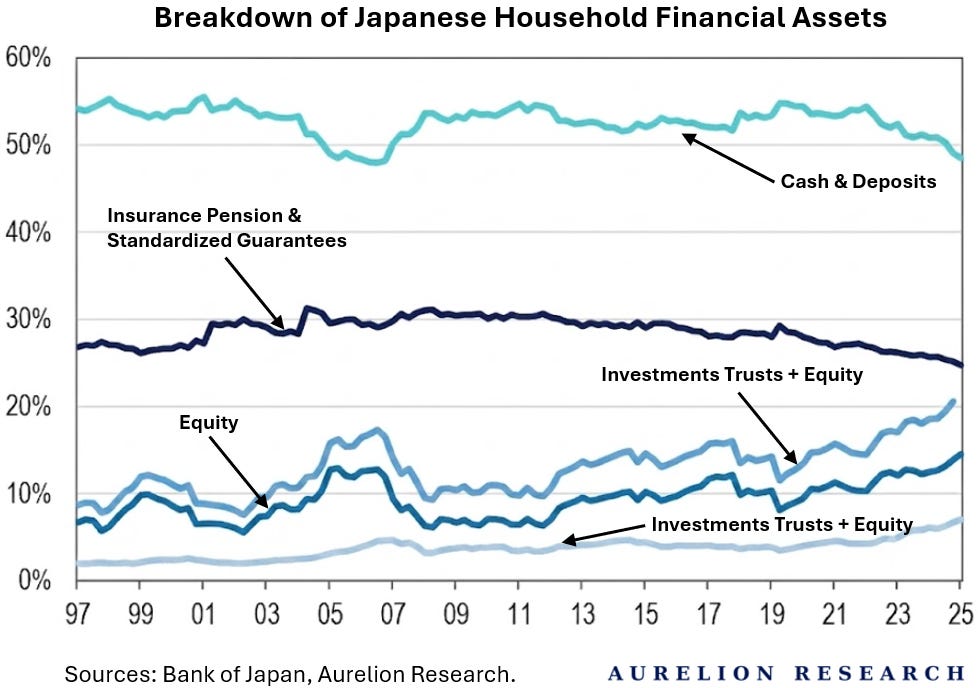

At the same time, household financial behavior is changing in a more supportive direction for banks. Cash &deposits have fallen below 50% of total financial assets, while investment trusts and equities have risen above 20%. This gradual reallocation supports higher fee income through wealth management platforms and increases the importance of distribution and advisory businesses within Japanese banks.

There are still transitional challenges. Banks will need to actively manage large JGB portfolios as the Bank of Japan reduces its market presence, which can create short-term volatility in earnings. However, this impact is increasingly offset by stronger core lending income and growing fee-based revenue.

Offshore risks remain an important offset, particularly exposure to the US credit cycle, private credit markets, and areas such as data center financing. These segments can introduce earnings volatility if global credit conditions tighten.

However, we believe the domestic setup continues to look strong, supported by rate normalization, improving loan growth, and a steady shift in household capital allocation toward investable assets.

4.1 Idea: Mizuho Financial Group (8411-JP)

Mizuho FG’s share price has come under pressure recently due to (1) declining expectations for a BoJ rate hike and (2) reports of insider trading involving employees at Mizuho. We view this weakness as an attractive entry point to accumulate the stock. We expect EPS growth to continue outperforming market expectations, supported by ongoing share buybacks and upside in net profit.

Within the megabank space, Mizuho retains strengths in large corporate banking and global investment banking, while combining relatively high sensitivity to interest rates with a conservative credit profile. Although the recent misconduct-related headlines have weighed on sentiment, we believe the market reaction is excessive when viewed against historical precedents. Continued buybacks and earnings upside should support further EPS growth and drive positive estimate revisions, leaving additional upside potential from current levels.

4.2 Idea: Suruga Bank (8358-JP)

Suruga Bank is in the middle of a turnaround, moving from restructuring into a more stable growth phase. The key driver is its Mid-Term Business Plan (April 2026–FY2028), where management targets a consolidated ROE of 11% or higher. Alongside this, the bank is strengthening shareholder returns, with a payout ratio expected to rise toward 40% or more, supported by ongoing share buybacks.

Several catalysts could support a re-rating. A potential removal of remaining FSA administrative actions would fully clear past regulatory overhangs and improve operational flexibility. At the same time, Suruga is expanding through partnerships, most notably with Credit Saison, aiming to build new retail channels, expand fee-based income, and reduce reliance on traditional lending.

Despite improving fundamentals, the stock continues to trade at a discount to book value. If management delivers on ROE targets, continues to clean up legacy credit costs, and sustains capital returns, the gap between valuation and earnings power should narrow over time. This makes Suruga a classic recovery setup, where execution on a clearer strategy is the main driver of upside.

4.3 Idea: Nomura Holdings (8604-JP)

Nomura Holdings is Japan’s largest brokerage and investment bank, combining domestic wealth management with global wholesale operations. Over the past year, it has benefited from stronger retail participation in Japanese markets, as households gradually shift savings from cash into investment products.

This provides a solid base for the wealth management business, although overall earnings remain cyclical and sensitive to market conditions and cost pressures.

For FY2026, results were mixed but solid. Net revenue rose 15% to ¥2.16T, with net income reaching ¥362.1B, translating into a return on equity of 10.1%, in line with long-term targets. However, momentum weakened in Q4, where net income fell 19% QoQ to ¥73.9B. Costs also increased, with full-year non-interest expenses up 15% to ¥1.62T, driven by higher compensation, acquisition-related costs, and an impairment in the investment management division.

Nomura currently trades at ~11x earnings and offers a dividend of ¥51 per share, implying a payout ratio of 41%. While the valuation and yield look reasonable, they also reflect the cyclical nature of the business and earnings volatility typical of global brokerage operations. International operations were notably weak in Q4, with pretax income from overseas down 82% QoQ.

Overall, the investment case depends on whether Nomura can control costs and stabilize its international business, while continuing to benefit from steady growth in domestic investment activity. We still see the setup as attractive.

4.4 Idea: Ichiyoshi Securities (8624-JP)

Ichiyoshi Securities is a Tokyo-based retail broker with a $259M market cap, currently trading at 11x trailing earnings. The business has been steadily shifting toward a “stock-type” model, closer to a wealth management structure, with recurring AUM fees now covering 80.2% of operating costs, up from 60% in 2023.

This brings the company closer to breakeven on fixed costs, where incremental fee income flows through at high margin. On profitability, it earns a TTM ROE of ~14.5% and trades at 1.7x book value, supported by a clean earnings profile with limited reliance on non-core income such as investment gains or interest income.

Dividend momentum has been strong. Payouts have increased from ¥17 per share in 2024 to ¥30 in November 2025, and most recently to ¥58 in March 2026, including an anniversary-related top-up. With a 50% payout target, the implied forward yield is around 6%, which remains attractive.

Looking ahead, rising participation in Japanese equity and investment trust markets should continue to support flows into retail brokers like Ichiyoshi.

With over two-thirds of revenue already coming from recurring wealth management fees and a strong ROE profile, we see scope for the stock to trade at a higher multiple than the current 11x earnings, with potential re-rating toward 14–15x if execution and market conditions hold.

Back in late April, we published a more in-depth report on the Banks & Financials transition (reallocation) theme, along with what we see as some of the best ways to position for this major shift in Japan’s capital allocation.

5. Japan’s Economy: Where Does It Stand Today?

Japan is often a difficult market to read. What looks strong at first glance is not always strong underneath, and in other cases the opposite is true. It is rarely a simple or linear story. The main questions today are how long the AI-driven rally in Japanese equities can continue, and what direction interest rates and Bank of Japan policy will take. These two factors are now central to market direction.

At the same time, Japan offers a broader set of investment themes beyond AI and Semis. These include rising interest rates, ongoing corporate governance reform, and growth concentrated in specific strategic sectors of the economy.

Within this, the AI and semiconductor cycle remains a key driver of sentiment and earnings. AI-related exports now account for roughly 20% of Japan’s total exports, placing the tech supply chain on similar footing with the automotive sector. Strength is also spreading across the value chain, from semiconductor equipment and memory to tighter bottlenecks such as optical components, testing tools, and cooling systems.

Japan’s Semiconductor Toolmakers

Corporate earnings are already reflecting this momentum, with domestic electrical equipment and precision instrument companies guiding for strong profit growth into FY2026. At the same time, capacity expansions in memory and related segments are expected mainly from 2028 onward, keeping supply conditions relatively tight in the medium term.

Overall, we see the durability of the AI-driven cycle as an important driver for Japanese equities going forward, alongside the path of monetary policy.

We believe the government agenda in Japan is only just getting started, or at least that is the hope. Over the past six months, activity has been dominated by budget work and election-related processes, which have limited visible policy progress. Attention now turns toward agenda-setting and execution.

Japan’s Prime Minister Takaichi

The post-election “honeymoon” period is fading, and the coming months will be an important test of follow-through from policymakers. The current growth strategy is increasingly shaping around industrial policy with a stronger defense component. We are witnessing a gradual shift toward using defense demand to support dual-use technologies, linking national security priorities with broader industrial innovation. Don’t be fooled, it won’t be all perfect.

Overall, policy is moving toward a more competitive and resource-focused approach, with greater emphasis on fiscal discipline and sovereignty. This marks a shift away from the more traditional, broad-based fiscal growth policies of the past, and we see this as supportive for investors and the market.

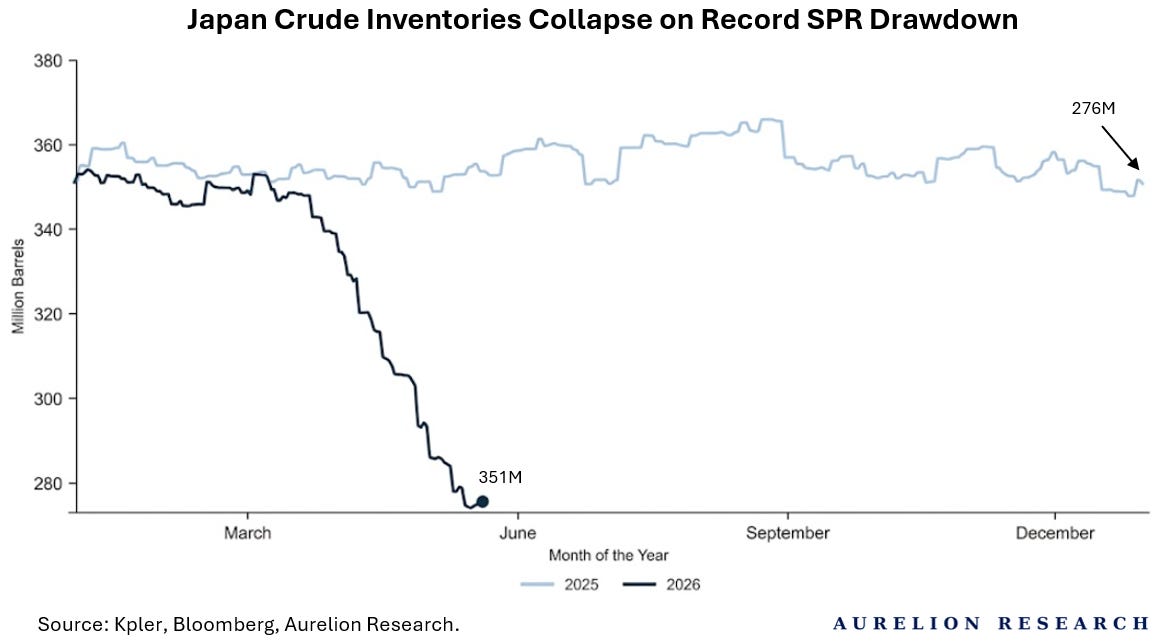

Then, of course, when we talk about the Japanese economy, one key point is energy security. Japan produces very little oil domestically, so it relies heavily on imports, making it more exposed to global supply shocks, particularly from the Middle East. Strategic oil reserves also offer only limited flexibility in a disruption scenario.

Japan Steps In Again as Yen Slides on Oil Prices

Recently, Japan’s crude inventories have moved away from historical patterns. While 2025 levels remained stable ~351M barrels, 2026 data shows a sharp and unusual decline. Following a significant drawdown of its SPR, inventories fell from March highs to ~276M barrels by the end of May.

That said, we are confident Japan will continue to diversify its energy sources. The country is already restarting and building new nuclear plants, while also scaling renewable energy capacity. Over time, this should provide a more balanced and resilient energy mix.

Now, on the economic growth level, that is where things can become more complex. There is still a meaningful degree of uncertainty around Japan’s growth outlook, which is also one of the key reasons we sent an analyst on the ground in Japan, to build our own view of how the economy is actually evolving in real time. The objective is to go beyond headlines and get a direct read on conditions as they are experienced on the ground.

Japan’s economy has held up relatively well despite several challenges in recent years. Growth is expected to continue at a moderate pace, supported mainly by consumer spending and domestic demand, even as global conditions remain less supportive. As wages and prices gradually rise after years of low inflation, policymakers face a balancing act between keeping inflation near the 2% target, maintaining fiscal stability, and supporting long-term growth in the context of an ageing population and a shrinking workforce.

On the positive side, Japan is in the process of gradually building what we believe will become a more resilient economy. This is being supported by targeted strategic investments designed to help offset potential risks such as demographic pressure, weaker purchasing power, and external shocks, including disruptions in regions like the Strait of Hormuz.

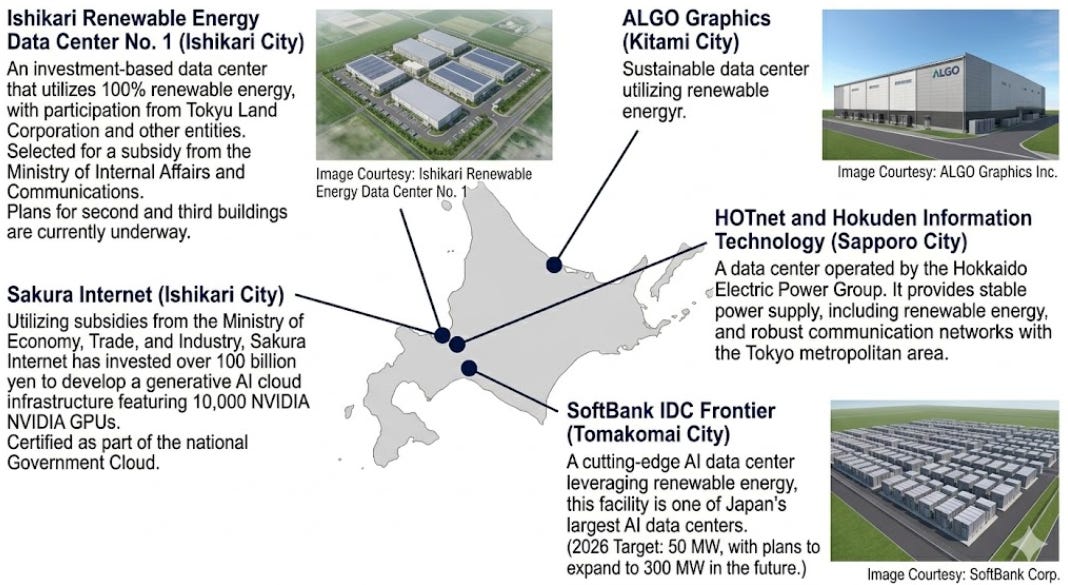

On the policy side, the government is actively supporting the development of large-scale data centers outside of major hubs like Tokyo and Osaka, with new projects emerging in regions such as Hokkaido and Kyushu. These programs are designed to reduce developer costs and can offset construction expenses by up to ¥30B, while also encouraging regional investment.

Hokkaido Data Center Development Map

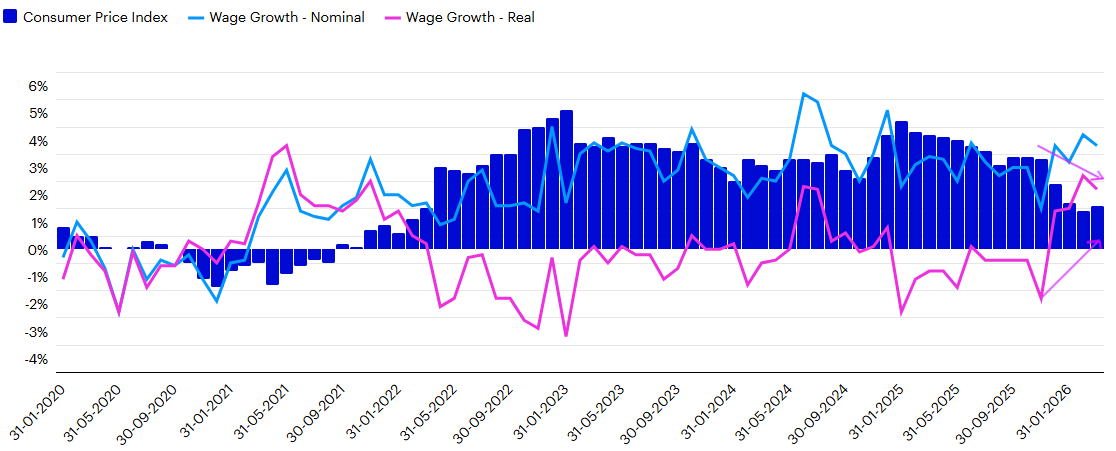

Looking at near-term macro tailwinds for 2026, real wage growth is starting to materialize, with real wages now back above 2%. The Prime Minister’s accommodative fiscal and monetary stance is aimed at supporting domestic demand, while inflation remains relatively stable. Importantly, real wage growth has recently returned to positive territory over the past months.

Consumer Price Index (CPI) & Wage Growth

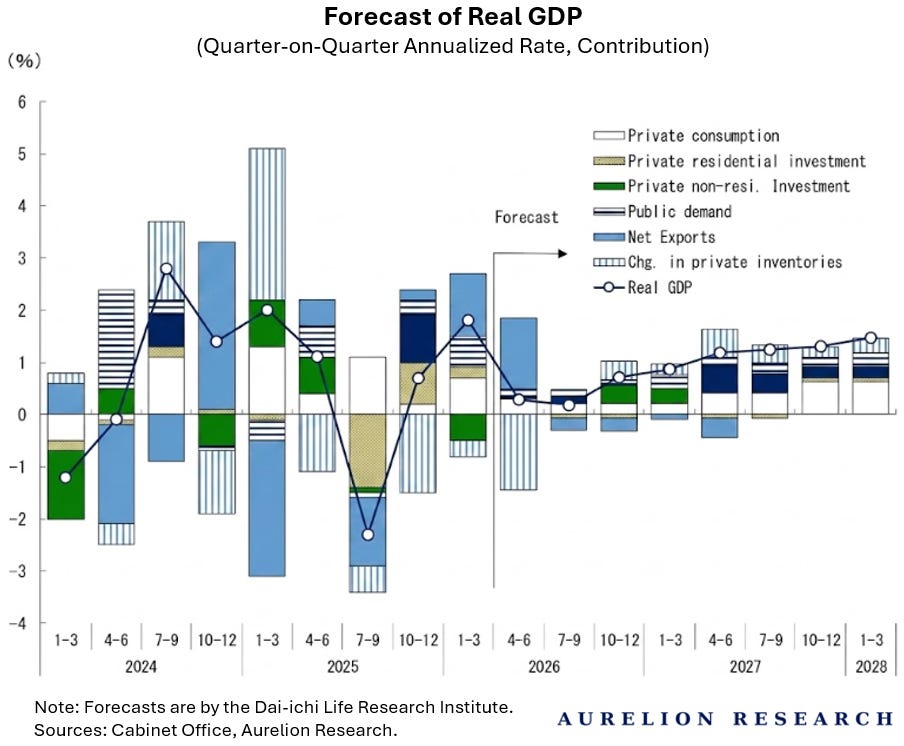

Finally, on the real GDP outlook, the picture is stable rather than exciting. Growth is expected to average around 1% in real terms over 2026 to 2028. It is not a high-growth environment of course, but this remains consistent with Japan’s profile as a mature, ageing economy with slower expansion.

The support comes mainly from domestic demand, particularly consumption and wage growth, while external demand remains more uneven. In this context, Japan is less about strong cyclical acceleration and more about steady, low but positive growth, which we believe will continue to be supported by policy stability and gradual improvements in real income conditions.

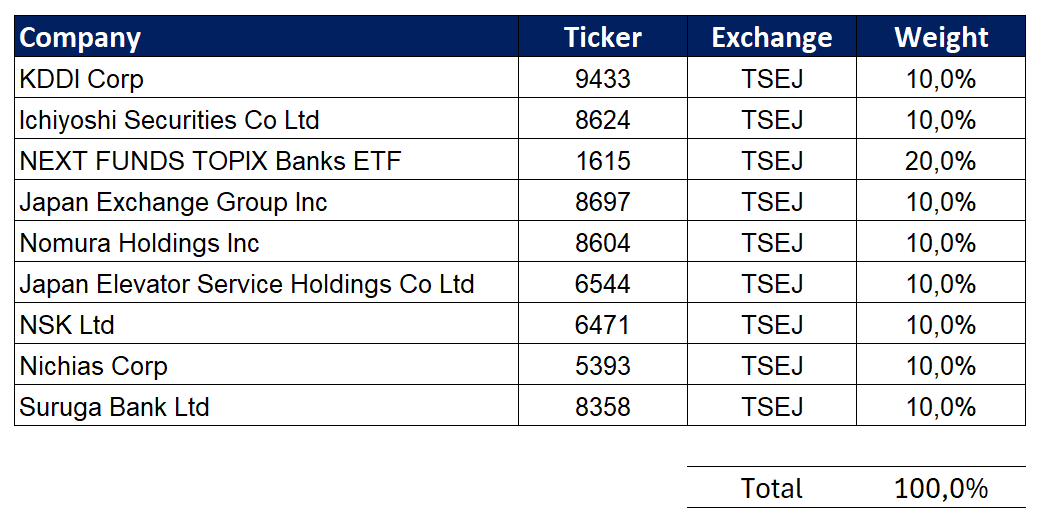

6. Japanese Equity Basket: Top Ideas from the Ground

We have built a 9-stock equity basket of Japanese companies that we believe are well positioned to benefit from a market that remains somewhat overlooked, but still offers significant pockets of value and opportunity.

You can download the spreadsheet here as well:

Detailing what we said in the introduction, we are not adding any of these stocks to the Aurelion Index, our main portfolio.

Readers may ask why, given our positive view on the country.

First, our analyst still has time on the ground engaging directly with company management, which remains important in refining conviction and identifying the strongest near-term setups.

In addition, adding certain Japanese equities on Plutus (where our portfolio is hosted) increase the minimum investment threshold for APAC names, and we prefer to keep accessibility as broad as possible. That said, we view this equity basket as an attractive way to express the improving backdrop in Japan.

It offers diversification across key themes, reducing the impact of company-specific volatility while maintaining exposure to higher-quality opportunities. In our view, it provides a more targeted and potentially more efficient way to play the cycle compared to broad index exposure.

(Readers can decide to automatically replicate this basket in their brokerage account through Plutus at runplutus.com)

Now let’s go through the companies we selected.

You’ll notice the 9-stock basket doesn’t carry every name we covered in depth. For Mizuho, we remain constructive on it, but the NEXT FUNDS TOPIX Banks ETF (20% of the basket) already holds Mizuho at roughly 16% of the fund, so we capture that exposure through the ETF instead of doubling up with a concentrated single-name position. The name we left on the sidelines is Nabtesco mainly because it creates a very high minimum investment for our Japanese equity basket. With those two exceptions, the basket reflects essentially all the ideas in this report.

It would be too repetitive to go through each company one by one, as we have already covered most of them either in this report or in our previous Japan Financials report. Instead, we will step back and explain the framework more broadly, which we think is more useful for readers. When it comes to finding investment ideas in Japan, the key is not to approach it like the US market.

The dynamics are different, and what works in one does not necessarily translate to the other. Japan does have a large number of net-nets (companies trading below net asset value), but that is not our main focus. Many of these names are also too small in market cap and liquidity for us to include in our portfolio.

As a result, our basket is deliberately diversified across sectors.

In automation and robotics, for example, we prefer not to own the most direct pure plays. Instead, we focus on adjacent companies that supply critical components needed to build these systems.

In glass and ceramics, Nichias is a good example. It is a large, diversified industrial company with exposure across multiple end markets. While diversification can sometimes dilute focus, in this case we see it as a strength, giving the company multiple levers of demand and stability across cycles.

Then, on the financial side, including insurers, non-banks, and banks more broadly, this is one of the largest sectors in Japan, alongside autos and other major industries. Given what is happening in the economy, the new political leadership, and the renewed upward pressure on interest rates, we think this area still has meaningful upside. In our view, there is fuel left in the tank.

6. On-the-Ground Findings

Inflation in Japan appears to be in an early but noticeable phase after decades of near-price stability. A clear example is the restaurant sector, where ramen shops have historically anchored prices around the ¥1,000 level, effectively positioning ramen as an affordable “working-class meal.” Operators are now struggling to maintain this price point as input costs rise, forcing gradual menu adjustments and, in some cases, pushing consumers toward cheaper alternatives or reduced discretionary spending.

Food inflation is also visible in staples such as rice, which has seen sharp price increases. In response, the government has released portions of its national rice reserves to stabilize supply. This reflects a shift toward more active intervention after years of deflationary pressure and limited price dynamics.

Wage growth, however, remains limited. Based on local discussions, salary adjustments are not keeping pace with rising living costs, which suggests that real income pressure is beginning to build. The combination of higher prices and stagnant wages is creating a mild squeeze on household purchasing power, even if from a very low inflation base. Despite this shift, Japan remains significantly cheaper than Western economies on a broad basket of everyday expenses. Food, transport, and housing costs are still materially lower than in Canada.

However, imported or globally priced goods such as electronics (e.g., iPhones) stand out as disproportionately expensive relative to local income levels, highlighting the gap between Japan’s domestic cost structure and global pricing benchmarks. This also reinforces the pressure on household purchasing power, particularly for high-value discretionary items.

From a macro perspective, demographics remain a key constraint. The population is aging rapidly, increasing reliance on public spending and raising long-term fiscal pressure. At the same time, political sentiment on immigration appears to have shifted, with less openness compared to previous cycles, limiting one potential adjustment mechanism for labor shortages and population decline.

Energy security is another important consideration, but government support has so far helped limit the impact on households. Costs have remained manageable for citizens, and a large share of daily mobility relies on public transport rather than private car usage. Japan still maintains significant exposure to imported energy and has historically relied on diversified supply agreements and strategic reserves. While there are ongoing partnerships and efforts to diversify supply, dependence on imports remains a key vulnerability, particularly in the event of geopolitical disruptions affecting key shipping routes such as Hormuz.

Overall, the field observations point to a transition economy: moving away from prolonged price stagnation, facing emerging inflation pressures, constrained wage dynamics, and persistent demographic headwinds, while maintaining fundamental strengths in affordability and industrial organization.

7. Key Risks

The biggest risk scenario remains energy.

Japan has so far avoided a real supply shock, helped in part by its large oil reserves, which cover roughly 200 days of demand. At the same time, the government has stepped in to limit the impact on households, introducing subsidies to keep energy prices lower since March, including a US$19B supplementary budget to fund additional electricity and gas support during the summer peak period, as well as an extension of gasoline subsidies.

A Look at Shibushi National Oil Storage Station in Kyodo

This helps smooth the short-term impact on consumers, but it also highlights the underlying exposure Japan still has to imported energy. If global supply conditions tighten further, or if geopolitical tensions persist, the pressure on both inflation and public finances could increase. In that context, delays in Middle East peace talks, if prolonged, could become a more material risk for supply stability and pricing, especially given Japan’s reliance on imported energy inputs.

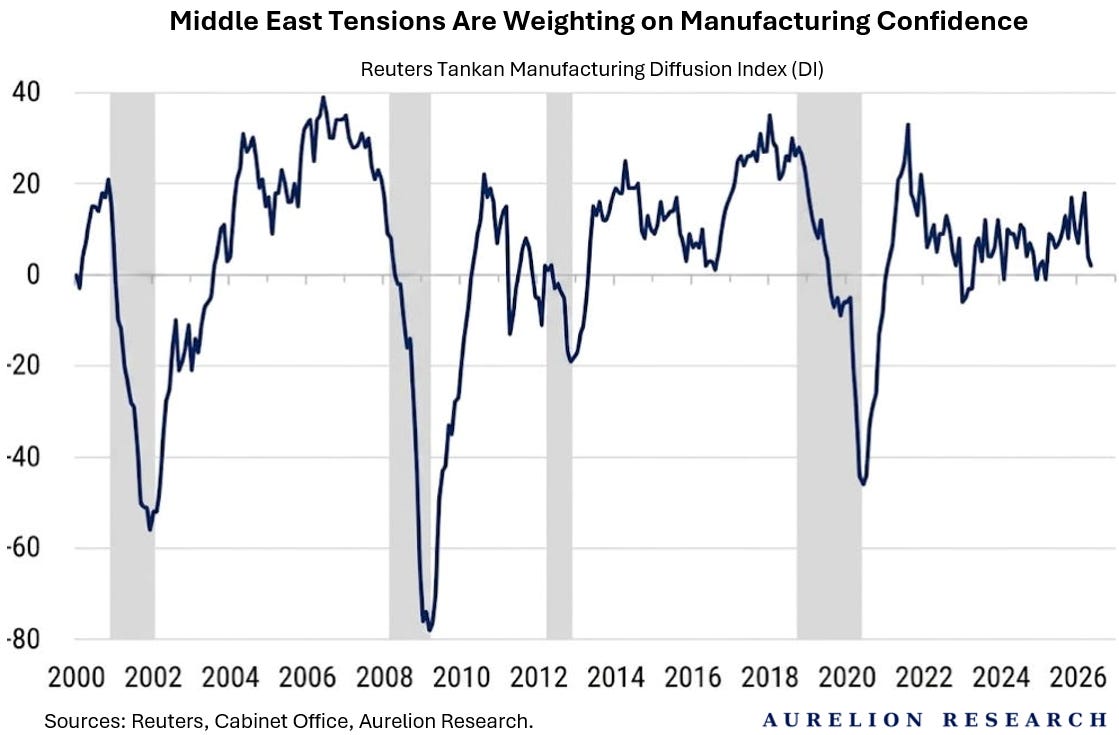

We can see below that Middle East tensions are weighing on the Reuters manufacturing confidence index. Not as severe as 2020, of course, but the trend is clearly weakening, with confidence falling at a steady pace in recent months. If the conflict between Iran and the US persists for too long (which remains uncertain), we believe the index could easily move below zero.

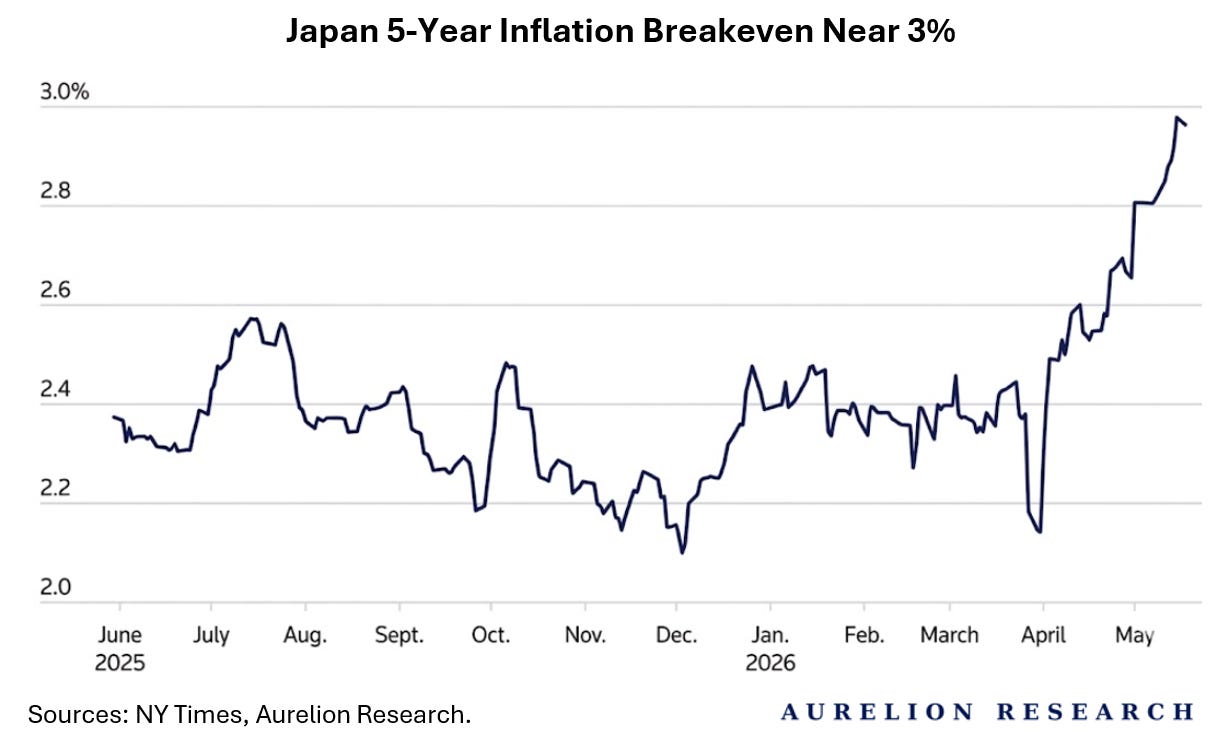

Lastly, another risk is that Japan’s 5-year inflation breakeven has been rising toward nearly 3%, up from around 2% before the recent Iran-related spike in energy prices. This suggests that medium-term inflation expectations are becoming higher and more sensitive to global commodity and geopolitical shocks. Nothing alarming enough to cause major concern at this stage.

That said, we view this more as something to monitor rather than a change in our broader outlook. From what we are observing from the ground, it is not a major concern, but it is noticeable.

8. Our Final Take on the Japanese Market

Overall, we are bullish on the Japanese market and economy.

At first sight, from abroad, looking at our screens, the picture was less clear, but with our analyst on the ground, we are more confident in our view that the market is no longer a simple recovery story. It is instead a mix of improving domestic demand, gradual policy normalization, and strong industry-specific growth pockets, particularly in AI-linked hardware and selected industrial segments. At the same time, macro conditions are becoming more balanced, with wage growth, inflation, and capital flows slowly moving in the right direction.

However, Japan is not a linear story. Energy exposure, global credit conditions, and the strength of external demand remain important factors. The key, in our view, is that Japan now offers a wider set of opportunities beyond traditional recovery trades, with more dispersion and more bottom-up alpha.

If there’s anything you’d like to learn more about in Japan, or any specific companies you’d like us to look into, let us know in the comments below. Our analyst will be there for some time.

Our Latest Thematic Research Report:

The Next Inflection in Crude Oil: When Will the Hormuz Bottleneck Break?

Last week, we had a call with who we consider one of the best crude oil shipping company CEOs in the world. We had a genuinely good conversation about Hormuz and where oil prices are heading. We had …

What you get as a paid subscriber:

Stock ideas, thematic research, commodity, and more.

Full access to our entire library of reports. Currently 100+ reports.

Live access to our actively managed portfolio: the Aurelion Index.

All stocks are backed by in-depth research.

Access to our real-time trades & rationale. As a reminder, this is not investment advice, please conduct your own research.

Questions? Reach us directly on Substack or at contact@aurelionresearch.com.

Hi,

I just wanted to tell you that Aurelion does great, quality research. I worked as an equity research partner at the world's second biggest hedge fund years ago. Pretty confident I know great research.

Best,

Tom tom@northsound.com

Great! I also recommend to check mitsumi minebea (ball bearings for drones, robots, phones etc market leader), and Niterra (spark plugs for automobiles etc - global leader) which funds their next Gen tech (ceramics, battery tech). Awesome companies.