Japan’s Great Reallocation: 3 Ways to Play the ¥1,100 Trillion Shift

Rising volumes, higher interest rates, and inflecting returns meet a powerful demographic tailwind. 3 stocks & 1 basket set to outperform.

By Jack Maxwell, our analyst specializing in market infrastructure.

We start with a simple thought experiment to make a complex shift easy to understand.

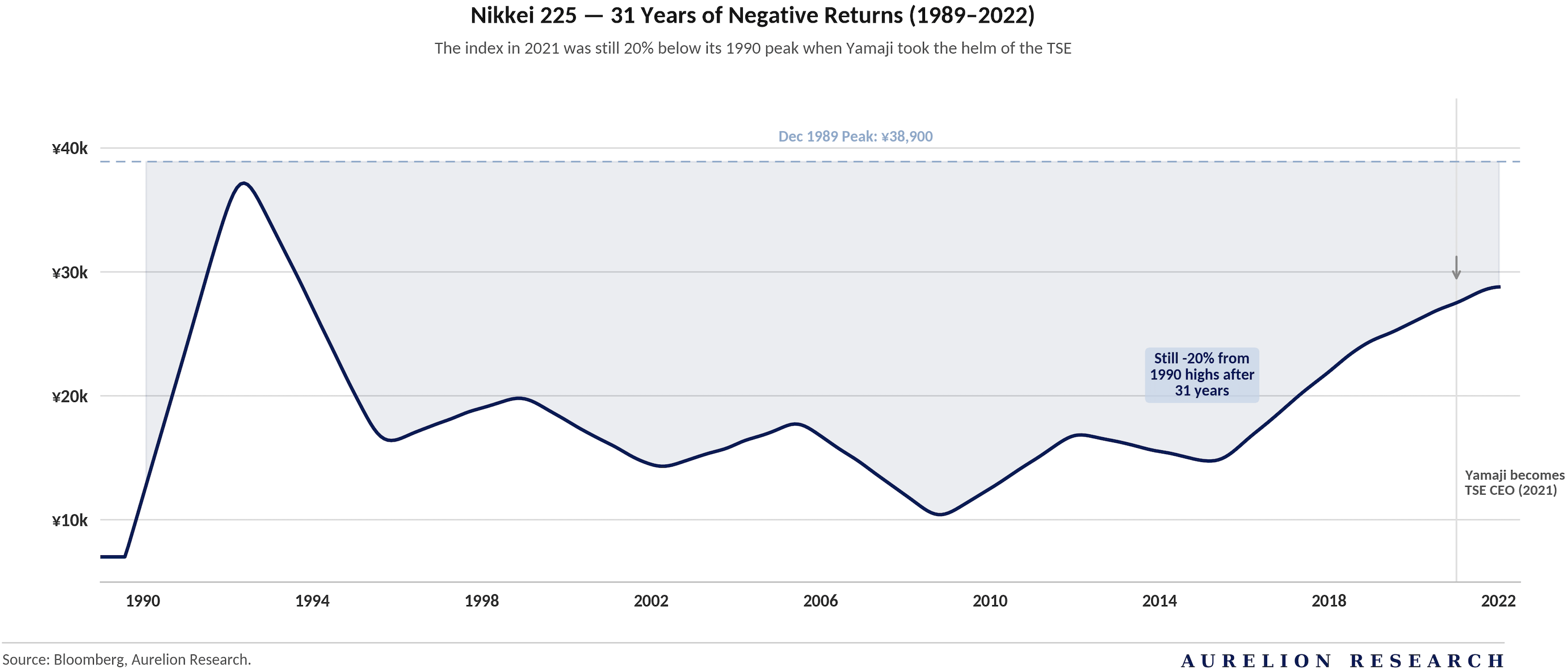

The year is 2021. You are Hiromi Yamaji, incoming CEO of the Tokyo Stock Exchange under Japan Exchange Group. At this time, the Nikkei index is still down 20% from highs last seen in 1990, marking 31 years of negative returns.

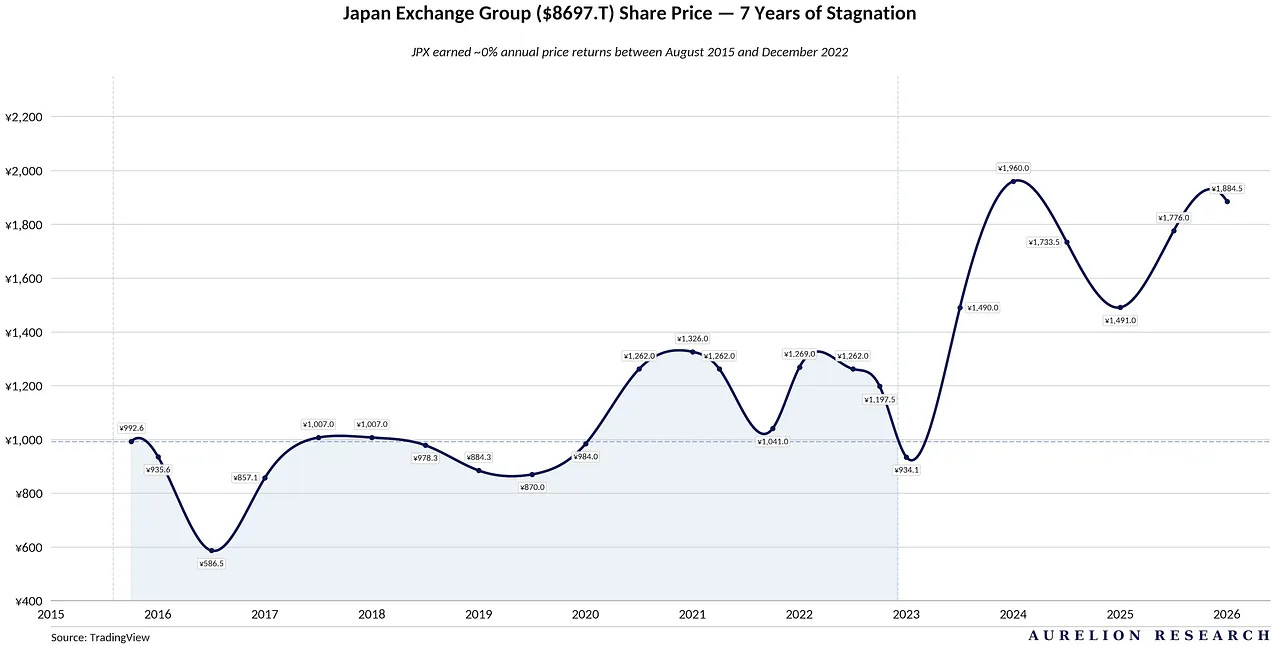

By 2022, the share price of Japan Exchange Group (JPX) itself has been stagnant since highs in August 2015, earning around 0% annual price returns over 7 years. If you want to create shareholder value in this situation, you clearly have a difficult task ahead of you.

First, let’s rewind a bit. The Japanese equity market has been stagnating for decades - why? Though the issue has been multifaceted, two primary reasons come to mind:

Firstly, the risk-averse tendency of many Japanese executives, a trait shared with much of the rest of Asia, has led to many companies hoarding cash or investment securities earning low returns, strangling shareholder value, instead of returning cash to shareholders or investing for new growth. This works against shareholder value because equity investors fundamentally need a return of capital at some point, or else there is no reason to invest. This dynamic created years of stagnant stock prices and low economic growth.

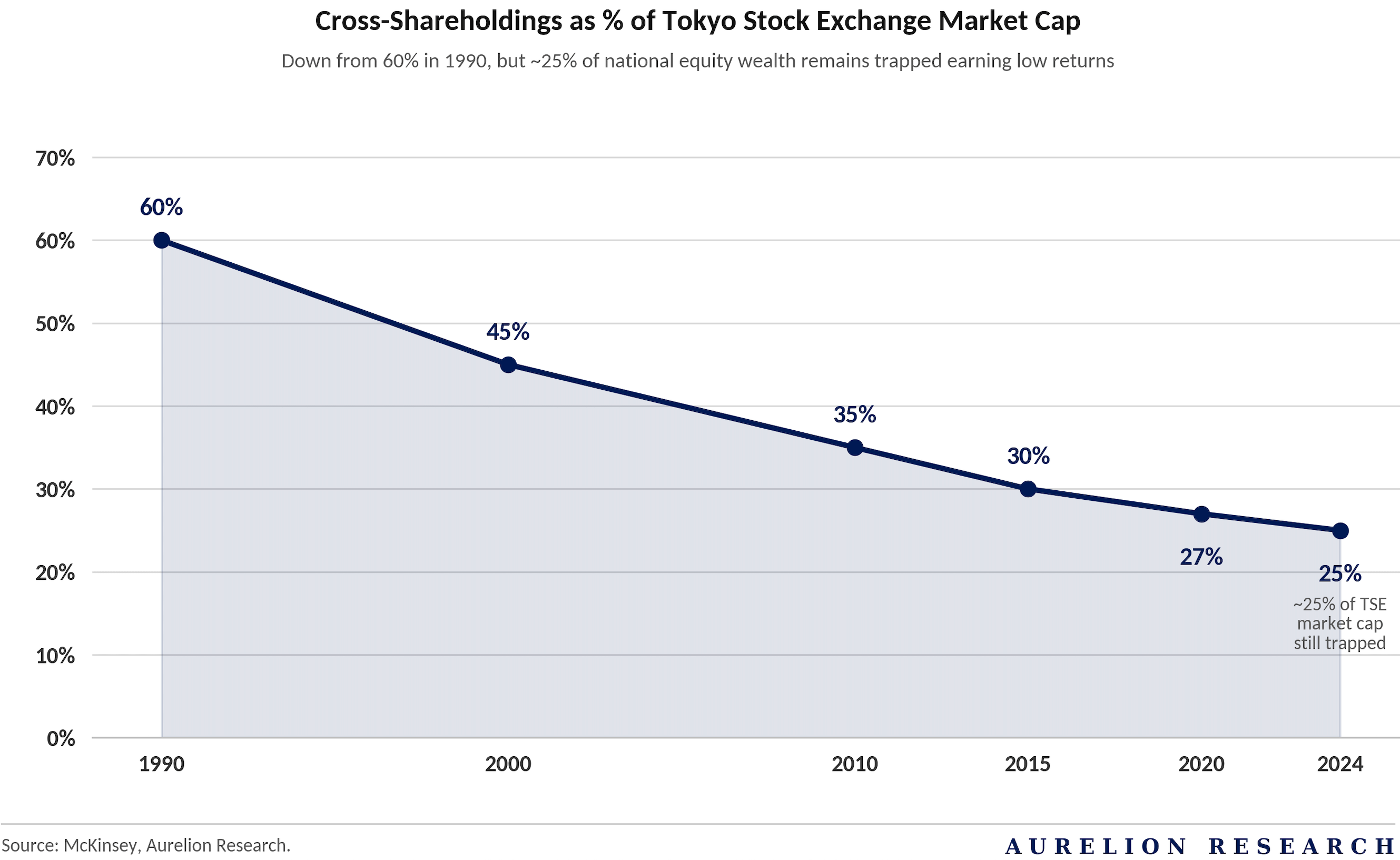

Secondly there is the cross-shareholding issue. Many Japanese companies are publicly traded subsidiaries of much larger parent corporations, usually controlled by said corporations. This works against shareholder value in two ways. For one, it decreases the free float of company shares, making them more illiquid, and illiquidity always carries lower valuation multiples with it.

More importantly, public market investors prefer to feel confident that if necessary, corporate policies can be changed by the democratic process of the market. Shareholders vote to elect board members to represent them and oversee corporate processes. If necessary shareholders can generally vote out board members who do not act in the shareholder’s fiduciary interest, at least in the U.S. In Japan, things have been different.

Take Toyota Boshoku (3116.T), Toyota's primary seat supplier. Toyota Motor owns 31% of the company, with the broader Toyota group controlling well over 40%. The result is a supplier whose margins have been compressed to a fraction of what comparable independent peers like Adient or Lear earn globally. Every year Toyota demands price-downs from its suppliers, and Boshoku has no leverage to resist — Toyota is simultaneously their largest customer and their largest shareholder — any price increase would be seen as a slap in the face.

Minority shareholders watching gross margins erode have had no recourse: they cannot vote out the board because Toyota controls the vote, and they cannot demand strategic change because Toyota's interests as a customer override their interests as fellow shareholders.

Decades of value transfer from minority Boshoku shareholders to Toyota Motor shareholders is the visible cost of this governance structure. Toyota Boshoku is one example among many in Japan.

Today roughly 25% of the entire market capitalization of the Tokyo Stock Exchange consists of cross-shareholdings, down from 60% in 1990 (per McKinsey). That is 25% of the publicly traded economic might of an entire nation sitting trapped, earning low returns, stagnate on the balance sheet.

These dynamics work against the market and the economy as a whole, and they work directly against you, the Japan Exchange Group. You want people to trade more stock. You want people to invest, to take risks, to put money to work in the economy — but if any shareholder value that gets created is dampened by these forces, almost nobody has a real reason to own Japanese equities, and your profits stagnate. So… what can you do about it?

Table of Contents

The Reforms

The Results

Japan Exchange Group

Stock Idea #1: Ichiyoshi Securities (8624.T)

Stock Idea #2: Nomura TOPIX Banks ETF (1615.T)

Stock #3: Our Favorite Idea Added to the Portfolio Today

Basket Positioning

Key Risks to the Thesis

Our Final Take on the Japan Financials

1. The Reforms

Being Japan’s only stock exchange operator, you control exchange listings for the entire equity market. You also control the TOPIX index, a prestigious index inclusion for Japanese companies.

Beginning in April 2022, you restructure the 5 segments of your equity market into a simpler 3 segments — Prime, Standard, and Growth.

You change listings and delisting criteria for these segments, essentially forcing listed companies into compliance with these criteria, including mandates against cross-shareholdings. This began the unwinding of cross-shareholdings, which has been a massive boost to Japanese equity valuations on its own over the past four years.

In October 2022 you begin overhauling the TOPIX index to hold more compliant companies, to hold them in a more efficient manner. The TOPIX tracks the broad Japanese equity market as the preferred index over Nikkei.

If a company can get into the TOPIX, passive institutions across Japan regularly buy their shares, supporting stock prices, and it brings a similar level of prestige as an S&P 500 inclusion might for an American company.

Following your promotion to Group CEO of the Japan Exchange Group, in March 2023 you tell corporate executives to stop destroying shareholder value. Literally, the reform is titled “Action to Implement Management Conscious of Cost of Capital and Stock Price”, telling corporate managers almost flat-out, “change your policies to generate returns above your cost of capital and increase your stock price, or get delisted.” Scorched earth tactics, but it has worked wonders.

2. The Results

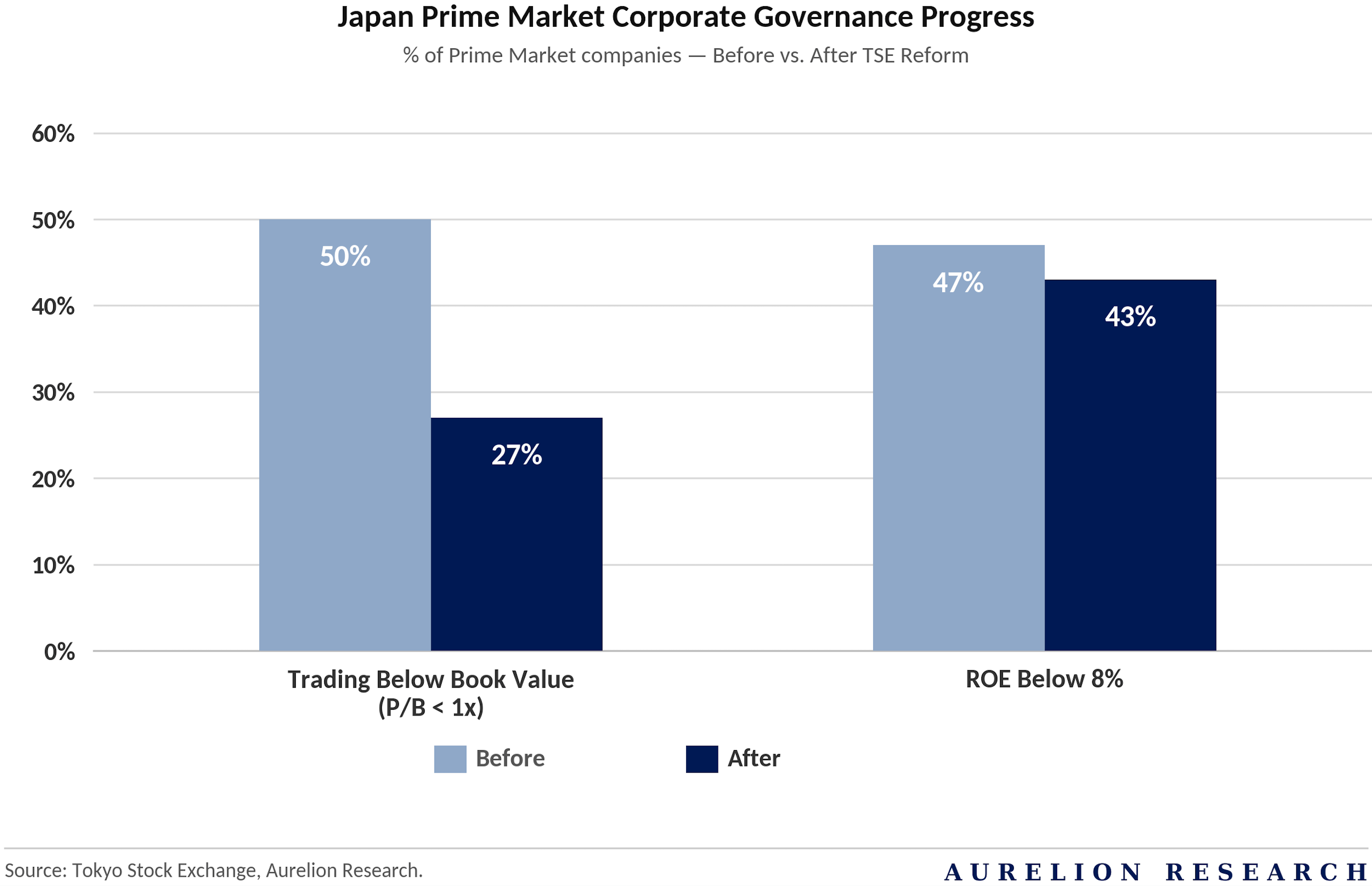

Today many Japanese companies have successfully implemented these reforms, and those that didn’t bother have been delisted or moved to lower market tiers. The percentage of Prime Market companies trading below book value has decreased to 27% (down from 50%) and the percentage of companies with ROEs below 8% has also declined, to 43% (down from 47%).

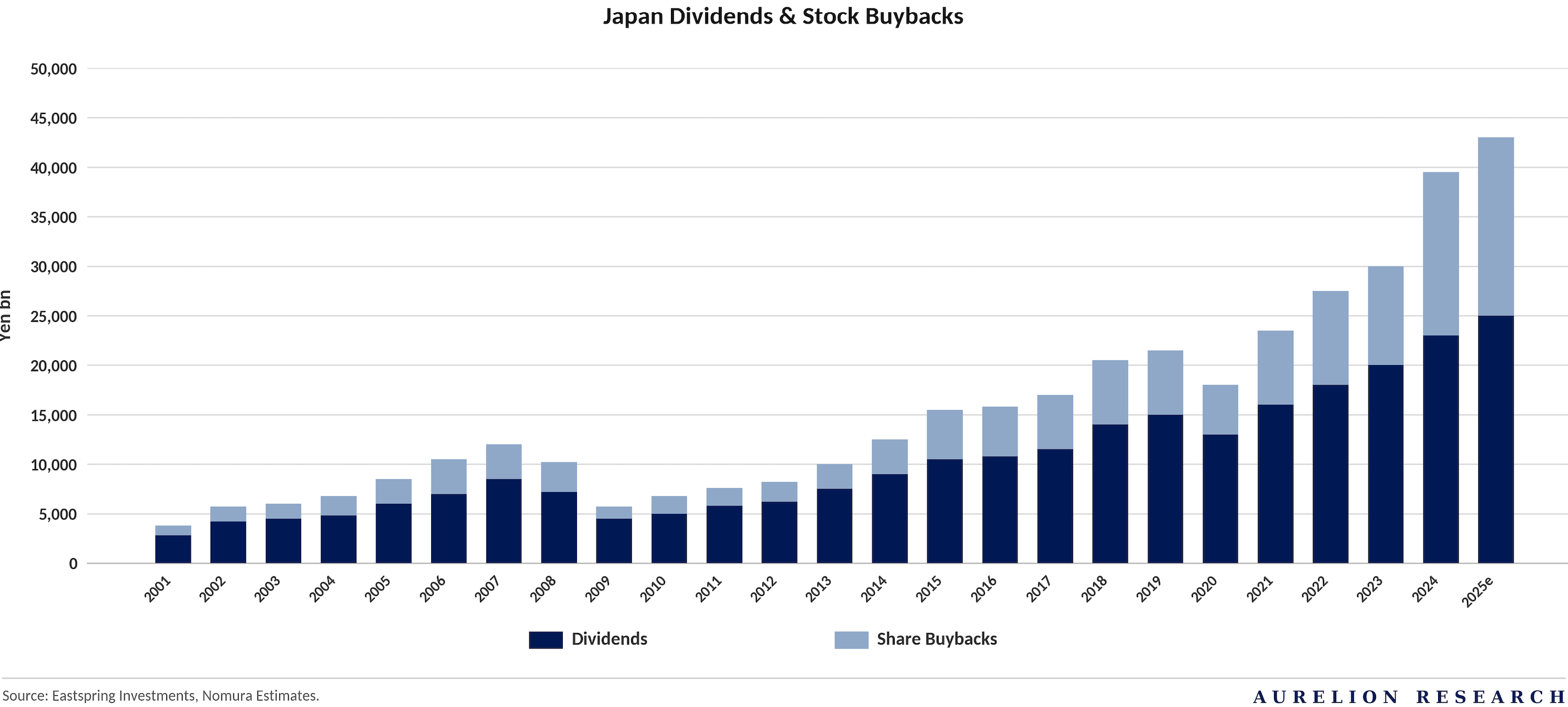

The majority of unwound cross-shareholdings have been deployed into record dividends and buybacks. In just a few years, you have made the Japanese equity markets significantly more attractive.

Standing here today in April 2026: equity trading volumes are up significantly. Activists and other foreign investors have poured capital into Japan at the highest pace in 22 years — even household equity ownership is increasing. Trading profits are up, and thanks to a rise in interest rates, yields on clearing balances are boosting profits further.

The Nikkei index finally broke through its 1990 highs in early 2024, after a staggering 34 years, and it has since rallied a further 50%. M&A volumes are skyrocketing. In 2024 corporate stock buybacks doubled over 2023 and they remained strong in 2025.

These impressive results have led to total shareholder returns running at a cool 17% annually from the Japan Stock Exchange Group since the implementation of the April 2022 reforms, beating many other global exchange operators over that timeframe.

Despite the impressive progress that has been made, the work is far from over. More cross-shareholdings need to be unwound. Many companies still hold 15-25% of their assets in cash and equivalents. Interest rates likely have further to rise. In a June 2025 interview with Nikkei Asia, you acknowledge that despite the strong pace of progress, the overall reforms are still only 20% of the way there.

“Our reform has just started, and we are not satisfied with the current situation.” — Hiromi Yajami, JPX Group CEO

The Japan re-rate trade isn’t over just yet. So how can we still play it?

In this report we are covering the exchange itself, 2 small-cap brokers, and the TOPIX banks, all direct beneficiaries of higher trading volumes, higher interest rates, and higher JGB yields.

Let’s kick things off by discussing Japan’s monopoly exchange itself.

3. Japan Exchange Group ($8697.T)

Japan Exchange Group is different to American exchanges in that it has a monopoly over equities and derivatives trading and clearing in the country, whereas in the U.S., the big four exchanges (ICE, NDAQ, CME, CBOE) are locked into an oligopoly, and the clearing of equities and options is handled by regulated infrastructure corporations owned by the exchanges themselves as well as other financial institutions.

However in Japan, the JPX Group controls everything. All cash equities trading, functionally all listed derivatives trading, and their subsidiary the Japan Securities Clearing Corporation is Japan’s sole central counterparty through which every single JPX listed financial asset in the entire country must be routed. The JPX Group even controls the dominant regional index, TOPIX.

This gives the JPX Group a much stronger position than non-monopoly exchanges that fight tooth and nail for trading volumes. The JPX Group is the bedrock infrastructure layer of Japan’s entire public capital markets stack. It owns all the economics between trading, clearing, listings, and market data and other services. The JPX Group operates the Tokyo Stock Exchange, the Tokyo Commodities Exchange, and the Osaka Securities Exchange, in addition to the Japan Securities Clearing Corporation.

Financial Profile

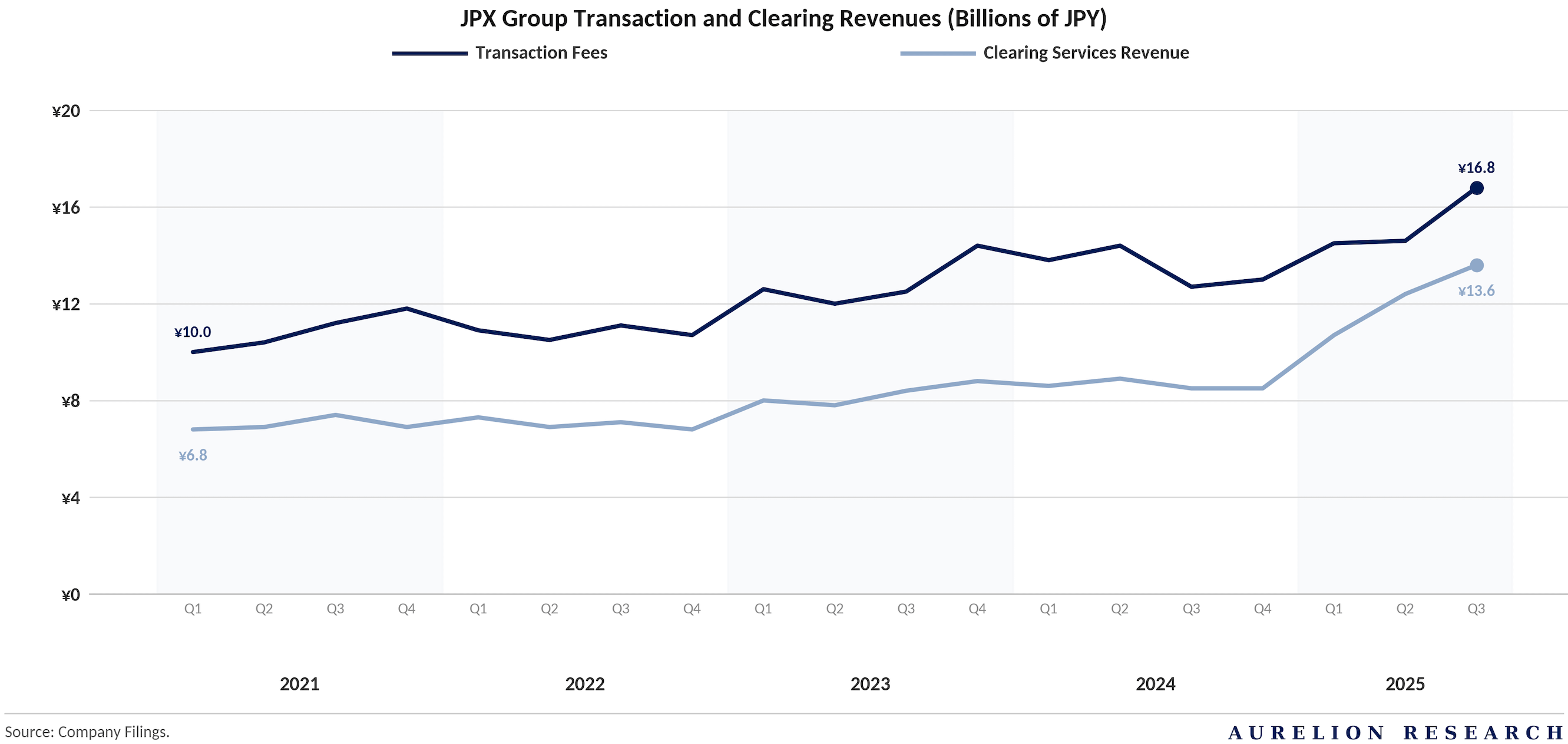

As mentioned above, thanks to reforms driven largely by the exchange itself, trading volumes and transactional revenues are up significantly over the past few years, and clearing income has been boosted by rising interest rates.

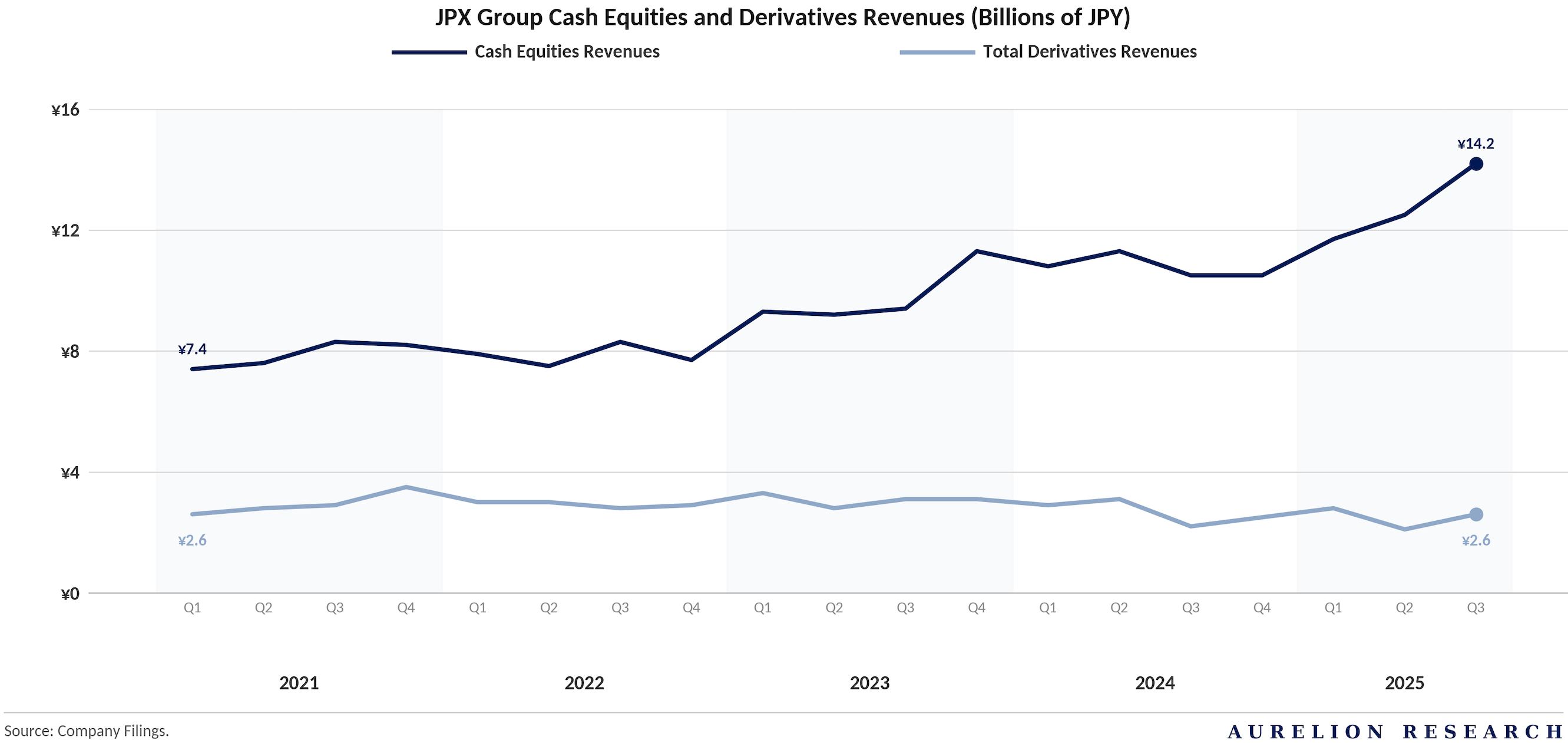

Trading revenue growth has been driven entirely by cash equities trading (14.8% CAGR since Q1 2021), while listed derivatives revenues have been flat over the same period.

Within listed derivatives, 87% of trading revenues come from financial derivatives (TOPIX and Nikkei futures and options, JGB futures) and the remaining 13% comes from commodity derivatives (energy, precious metals, and agriculture). Broadly, over 75% of revenue comes from the typical exchange transactional, clearing, and data fees, with a smaller share coming from listings, systems, and access fees.

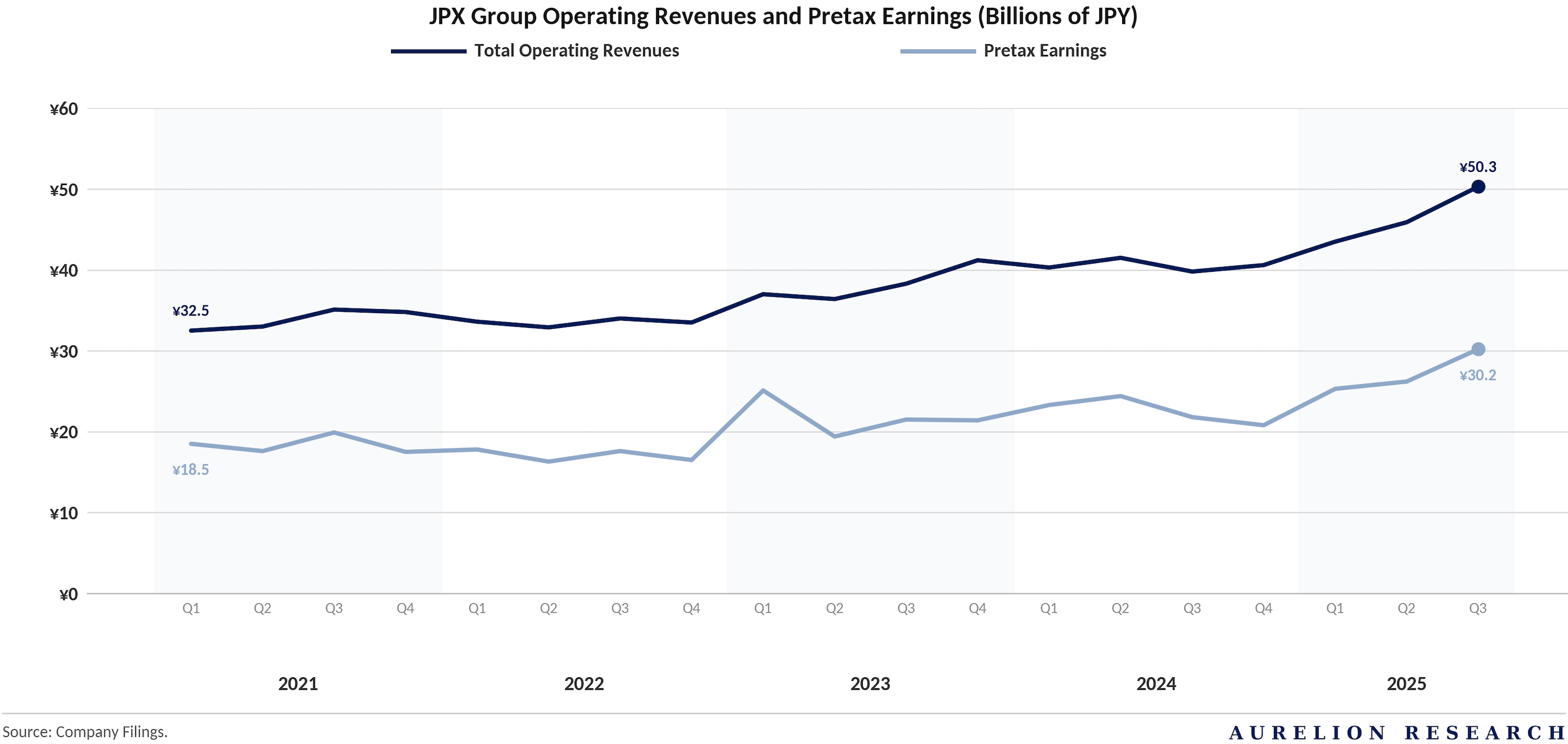

Given the impressive strength in trading volumes, the JPX Group has posted a revenue CAGR of 11.58% with steady margins. In Q3 2025, revenue increased 14.8% Y/Y with operating income up 17.1% due to record high margins.

Given the high incremental margins of the exchange business, as well as an increase in high-margin clearing interest income due to increases in interest rates, profitability has remained strong, with 2025 YTD pretax margins through Q3 reaching a strong 58.5% keeping pace with the three large U.S. exchanges with large market shares in equities and options, ICE, NDAQ, and CBOE. In Q3 2025, pretax margins reached a record 60%.

JPX Group generates significant cash and returns the majority of cash to shareholders through dividends (3.2% yield, 60% stated target payout ratio) and buybacks. Capital investment requirements are relatively minimal, with capex running at 9% of revenues in 2025.

The Japan Exchange Group trades today at 22x forward earnings, a premium multiple. Strong, diversified exchanges typically trade at premium multiples because they will be operating and producing cash flows long after we are around to collect them (The Osaka Exchange predates the founding of America by about 80 years), their cash flows usually scale at or beyond the pace of long term economic growth due to increasing financialization, and they are realistically impossible to displace, in this case due to liquidity network effects and regulatory lock-in.

Assets like this have earned a bit of premium, or at least, the reasonable expectation that premium exit multiples can be assumed in valuation.

Our Final Take on JPX Group:

While it may not be the most exciting Japanese Financials investment in this environment given the premium already in the price, we see JPX Group as a solid way to earn market or potentially above-market returns, given strong revenue growth as trading volumes continue increasing long-term, the prospect of slight margin expansion, and a 3%+ dividend yield.

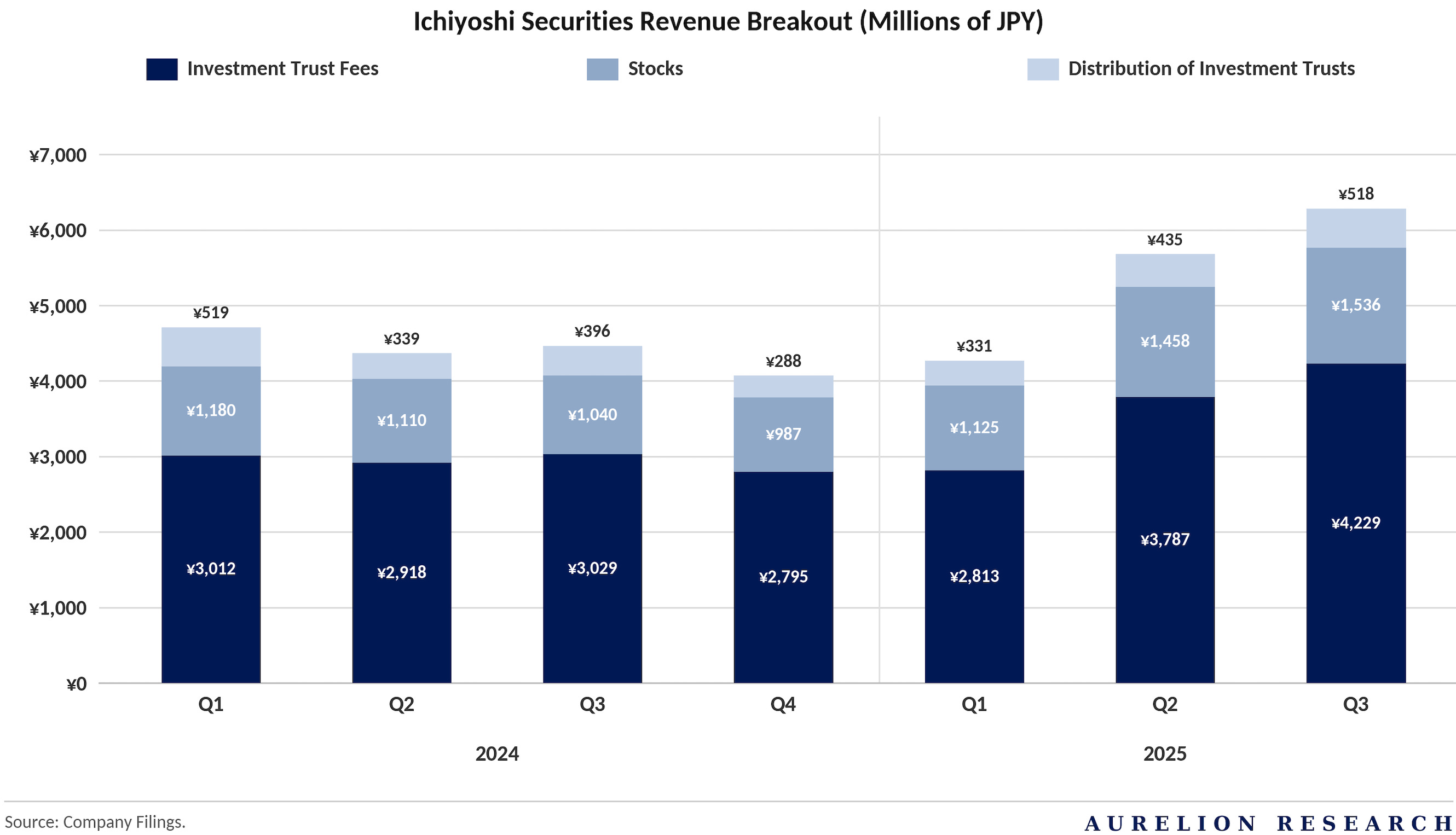

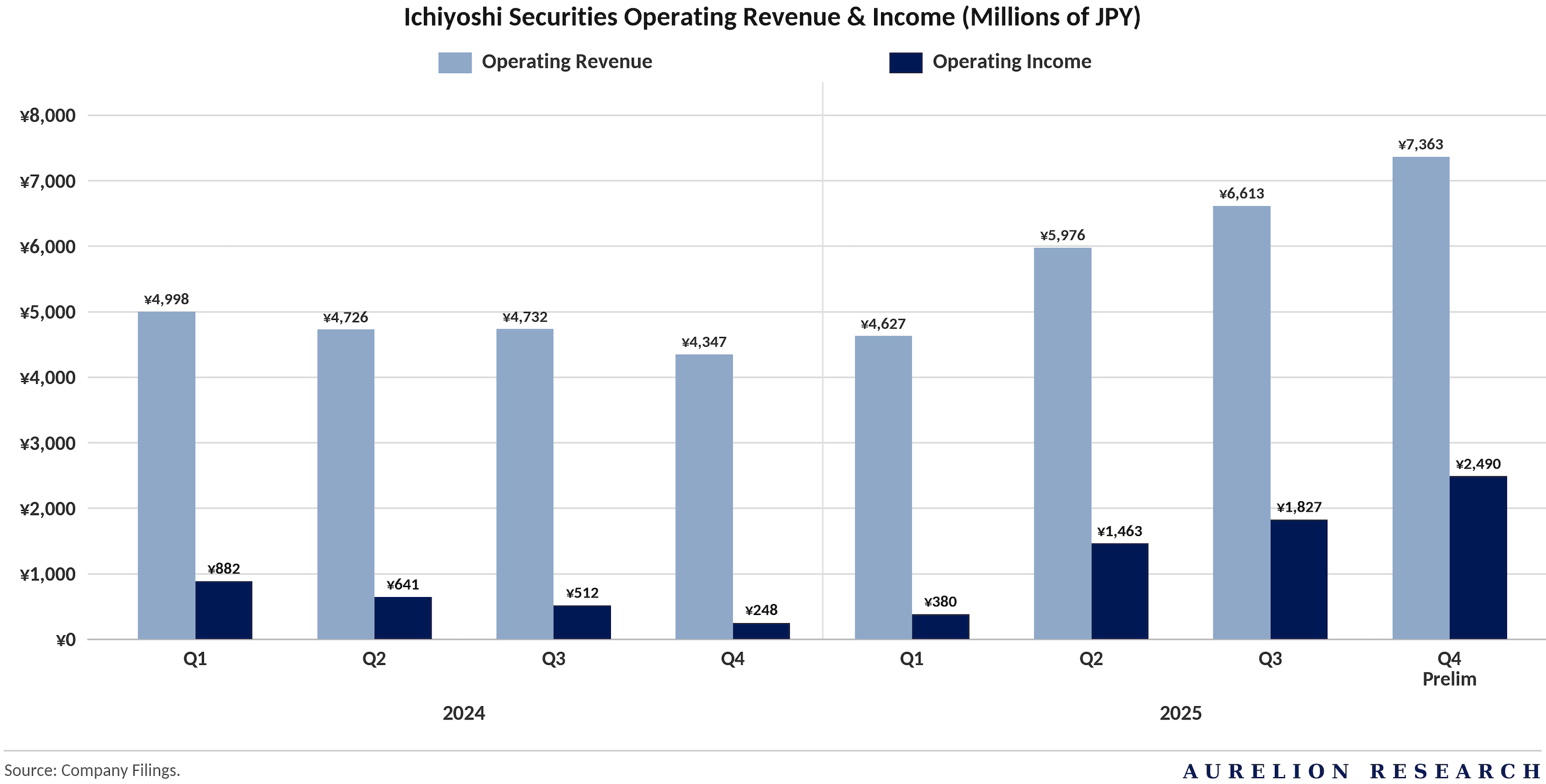

4. Ichiyoshi Securities ($8624.T) — Idea #1

The first pick we discuss is Ichiyoshi securities, a Tokyo-based retail broker with a $259M market cap trading at 11x trailing earnings. As the company has been transitioning toward a “stock-type” business model in recent years, the Japanese equivalent of a wealth management business in the U.S. or Canada, their recurring AUM fees have grown strongly in recent years to the point that they now cover 80.2% of total operating costs (up from 60% in 2023), approaching the structural 100% breakeven where incremental fee revenue flows through at near-pure margin.

Customer AUM has grown from ¥2.26Tn in 2023 to ¥2.6Tn in Q3 2025, driven by growth across all asset classes, including investment trusts at ¥860Bn, stocks at ¥1.27Tn, and the newest fund wrap at ¥420Bn in assets.

With its portfolio of custom offered fund wraps including the popular “Dream Collection”, Ichiyoshi is specifically cashing in on demographic wealth transfer in Japan as older retirees pass wealth to younger family members. Specifically, their ‘“Dre-Colle Pass” product which offers succession of funds to the next generation without realizing taxes.

“With regard to “Dream Collection,” a fund wrap account vehicle and a core of “Stock-Type Business Model” with its ten-year anniversary behind, it enjoys an increasing popularity among customers as a medium- to long-term investment vehicle for customers’ conservative assets. Its outstanding balance as of December 31, 2025, amounted to 421 billion yen, up 33.8%.

The Company started new services from 2024: namely, “Dre-Colle NISA” (which can be used as a growth investment frame for NISA investments) and “Dre-Colle Mini” (which is an automatic monthly subscription type).

By combining “Dre-Colle Pass” (which makes the succession of the fund to next generations possible without cashing in the fund) with the new two services, the Company can support its clients’ asset-formation for a medium- to long-term across generations.” — Q3 2025 Earnings Report

High net worth accounts have grown 12.5% since Q4 2024 while total accounts have decreased a very small amount, similar to other Japanese retail brokers.

Due to strong growth in revenues and 72% of costs through Q3 2025 being fixed, Ichiyoshi has demonstrated strong margin expansion as revenue has grown, a trend that is highly likely to continue as recurring AUM-based revenue continues to increase. Operating expenses increased just 9% through Q3 2025 primarily due to higher compensation.

As of the FY 2025 earnings pre-release, Ichiyoshi grew revenue 30.7% in 2025, and as you can see in the chart, operating income grew an astonishing 170% Y/Y driven by massive leverage around the fixed cost base.

Considering the recent earnings pre-release Ichiyoshi trades at 11x trailing earnings and as of Q3 earnings, 1.7x book value per share, earning a very strong TTM ROE of ~14.5% with negligible non-operating earnings from interest income and sales of investment securities — an excellent ROE that shows Ichiyoshi is deserving of a premium book value multiple.

Over the past year the company has significantly increased their biannual dividend as earnings have grown, from 17¥ per share in 2024, up to 30¥ in November 2025, and finally to 58¥ in March 2026, from a 48¥ regular dividend and an extra 10¥ each period to commemorate the company’s 75th anniversary. Given a targeted 50% payout ratio, if earnings sustain, the 48¥ biannual dividend would equal a 6.4% forward yield which we find highly attractive.

In a similar vein to other Japanese brokers, we think the trend of Japanese household participation in the equity and investment trust markets will only increase, and Ichiyoshi is well positioned to capture their share of that volume.

Given that 67% of TTM revenues are high-quality, relatively stable and recurring wealth management fees, and given a very strong ROE, we think Ichiyoshi deserves to trade for a good bit more than 11x trailing earnings. Assuming modest earnings growth and the 6%+ dividend, even a 14-15x multiple re-rate could generate fantastic shareholder returns from here.

5. Nomura TOPIX Banks ETF ($1615.T) — Idea #2

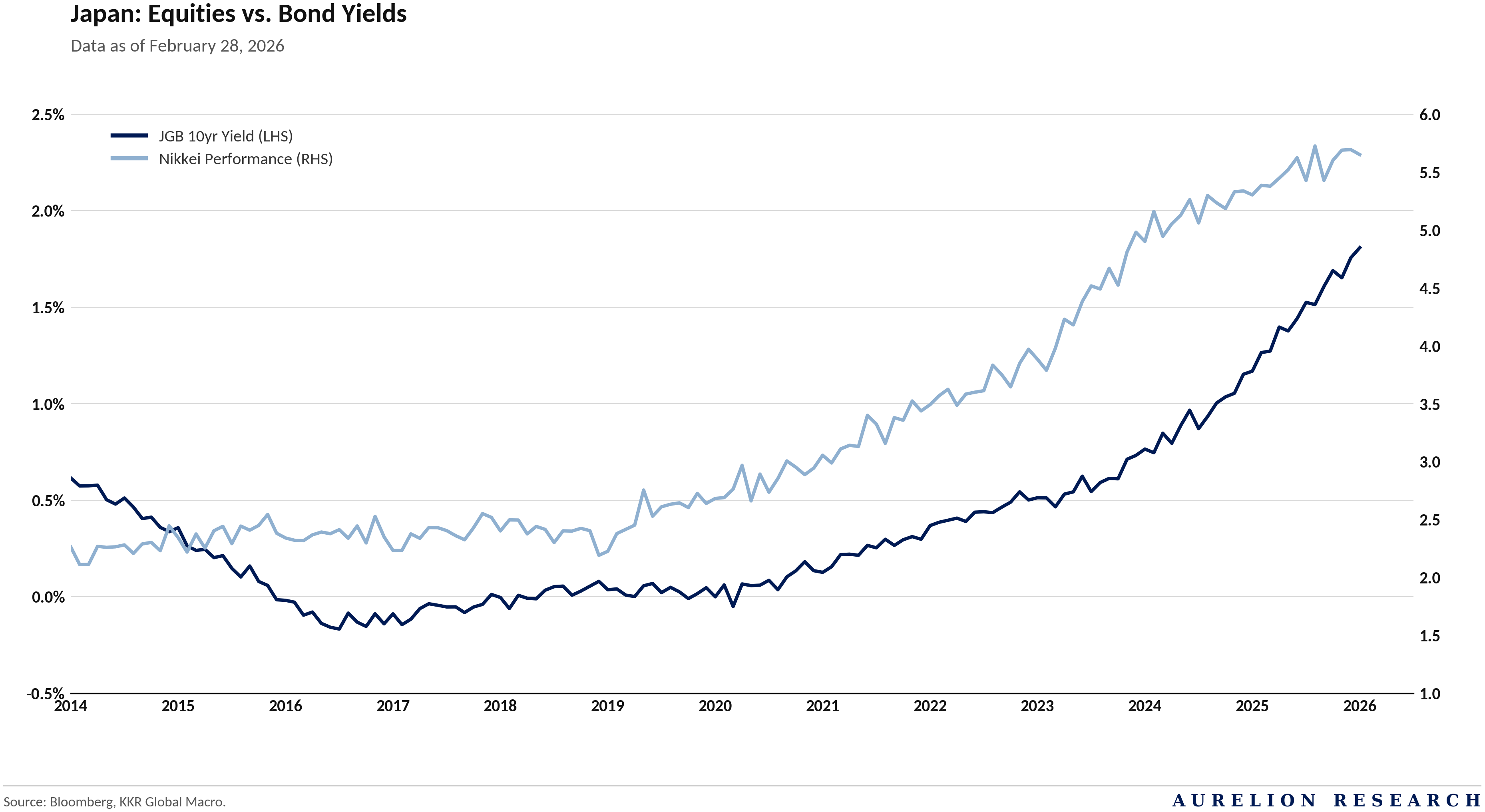

While other companies we have covered benefit primarily from higher benchmark interest rates and higher trading volumes, TOPIX banks benefit from higher Japanese Government Bond (JGB) yields, because they may reinvest maturing loan balances at higher yields to earn significantly wider spreads than they have historically earned.

Pictured below is the yield on 10-year JGBs, driven higher by increases in inflation and benchmark interest rates in Japan as well as the formal ending of Yield Curve Control (YCC) policy.

Combined with increasing capital return trends among Japan’s financial institutions driving increasing ROEs, warranting higher BVPS multiples, the TOPIX Banks have performed incredibly well over the past year and we think they are likely to continue to do so. We see the Nomura TOPIX Banks ETF ($1615.T) as an elegant way to express the trade, given relatively diversified exposure across 70+ banks. The fund’s 3.2% dividend yield covers the 0.22% expense ratio with plenty of extra yield.

Next we are covering a small cap Japanese retail broker trading at 8.4x TTM earnings and just 1.24x book value despite recently pre-releasing a 25% increase in revenue and a 50% increase in operating income. This broker sports a 14.4% (and improving) core ROE, with ambitious and capable management who have taken reforms very seriously, committing to a 6% dividend yield.

We dive deep into why we think this broker is simply far too cheap given the company’s strong growth, execution and quality of earnings.

Our Favorite Japanese Stock Added to the Portfolio

We are adding this stock to the Aurelion Index today.