We are always on the lookout for the next big opportunity. Which market could be the next to outperform around the world? Right now, we believe there is one market that remains particularly undervalued and overlooked: Latin America.

Earlier this year, we published our Latin America Primer, laying out why the region was entering the early stages of a multi-year bull market.

Since then, much has changed.

Recent elections have provided greater clarity, and several catalysts we identified are beginning to play out. The timing to enter the region now looks much more compelling. However, that is not true for every country.

We have created the Aurelion LATAM Basket, which consists of 30 high-quality equities positioned to benefit from the region’s re-rating. All are Latin American companies that trade on U.S. exchanges, giving global investors easy access to the region. It also provides strong diversification from U.S. tech stocks.

We also provide a chartbook, containing all charts from this report, along with additional charts on the basket, in one place and in higher quality:

Latin America can be a difficult market to understand from the outside.

The region is made up of different countries, economies, and political environments, each with its own opportunities and challenges. Our focus is on Colombia, Chile, Argentina, Peru, Mexico, and Brazil.

That is why we leveraged our expertise to make this market easier to understand. One of our main goals as analysts is to go beyond the headlines, understand the complexity behind each market, and ultimately simplify it for our readers.

For this report, we dedicated significant time to analyzing the region, understanding the key trends shaping these markets, and speaking with analysts, economists, and portfolio managers based in Latin America. We believe these local insights are essential, as understanding a market goes beyond just looking at data. It requires understanding the people, businesses, and dynamics driving it.

Table of Contents

The Next Capital Destination

Equity Markets: A Decade of Opportunity?

Macro: The Pulse of LatAm Economies

Peru: The Cinderella Story of LatAm

Colombia & Argentina: Our LatAm Favorites

5.1 Colombia: At an Inflection Point

5.2 Argentina: The Turnaround Story

Brazil: Too Early to Call

Mexico & Chile: Waiting for Their Moment

7.1 Mexico: Caught Behind the Border Wall?

7.2 Chile: The Quiet Market

LATAM Equity Basket

Our Final Thoughts

Before starting, the most important thing to understand about LATAM is that being bullish on the region does not mean being bullish on every country.

Far from it. Each market has its own cycle, political environment, and investment drivers. Our view on the region is based on several structural trends that we believe are still underappreciated. We see a major mining and commodity cycle developing in the coming years, driven by the massive demand for the materials required to build global AI infrastructure.

At the same time, Latin America is benefiting from broader structural changes, including strong population growth, rising wages, and the expansion of its middle class. These trends could support capital inflows into the region as global investors look for new opportunities outside crowded markets.

The region is also going through a period of significant political change, with several elections already completed and more ahead. While this creates uncertainty in the short term, it also creates opportunities as markets often overreact to political noise.

To us, sentiment toward Latin America remains mixed, and that is precisely what creates the opportunity. The story is not obvious, but we believe the market is underestimating the potential across select countries.

1. The Next Capital Destination

To us, Latin America stands out within a broader diversification trend that is still underappreciated. Since 2025, some institutions have started reducing their concentration in U.S. equities and Big Tech, reallocating capital toward emerging markets, particularly Latin America.

From our conversations with investors, the message is mixed.

Some funds remain comfortable staying heavily invested in US equities and continuing to ride the AI wave, while others are starting to look for diversification, taking some profits from crowded technology positions and exploring markets that have been overlooked. This has started to create more interest and liquidity flows into Latin America, a trend we believe should continue as investors reassess risks in areas such as US private credit.

First, let’s have a look at what is going on with fund flows in Brazil.

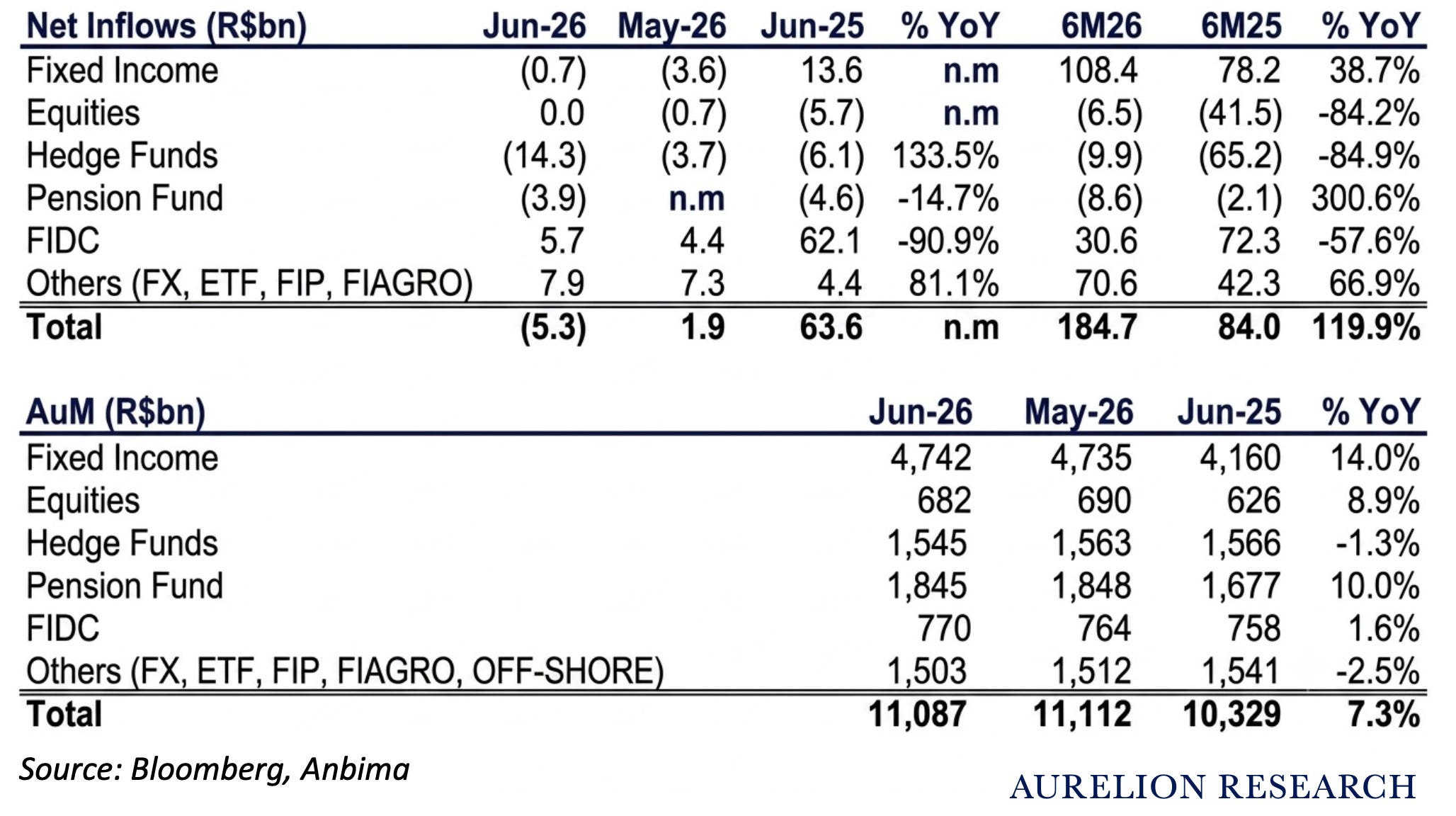

The ANBIMA data shows that investors are already positioning for uncertainty ahead of Brazil’s 2026 election. June saw broad-based outflows across fund categories, reflecting a risk-off mindset. However, we believe the market may be underestimating the opportunities that could emerge once political noise fades.

Looking more closely, most outflows came from hedge funds and pension funds, while ETFs and private equity funds continued to attract capital. We view this as a positive signal. Short-term investors are reducing exposure, while longer-term capital remains committed. From a market perspective, this creates a healthier ownership base, supported by more stable and patient investors.

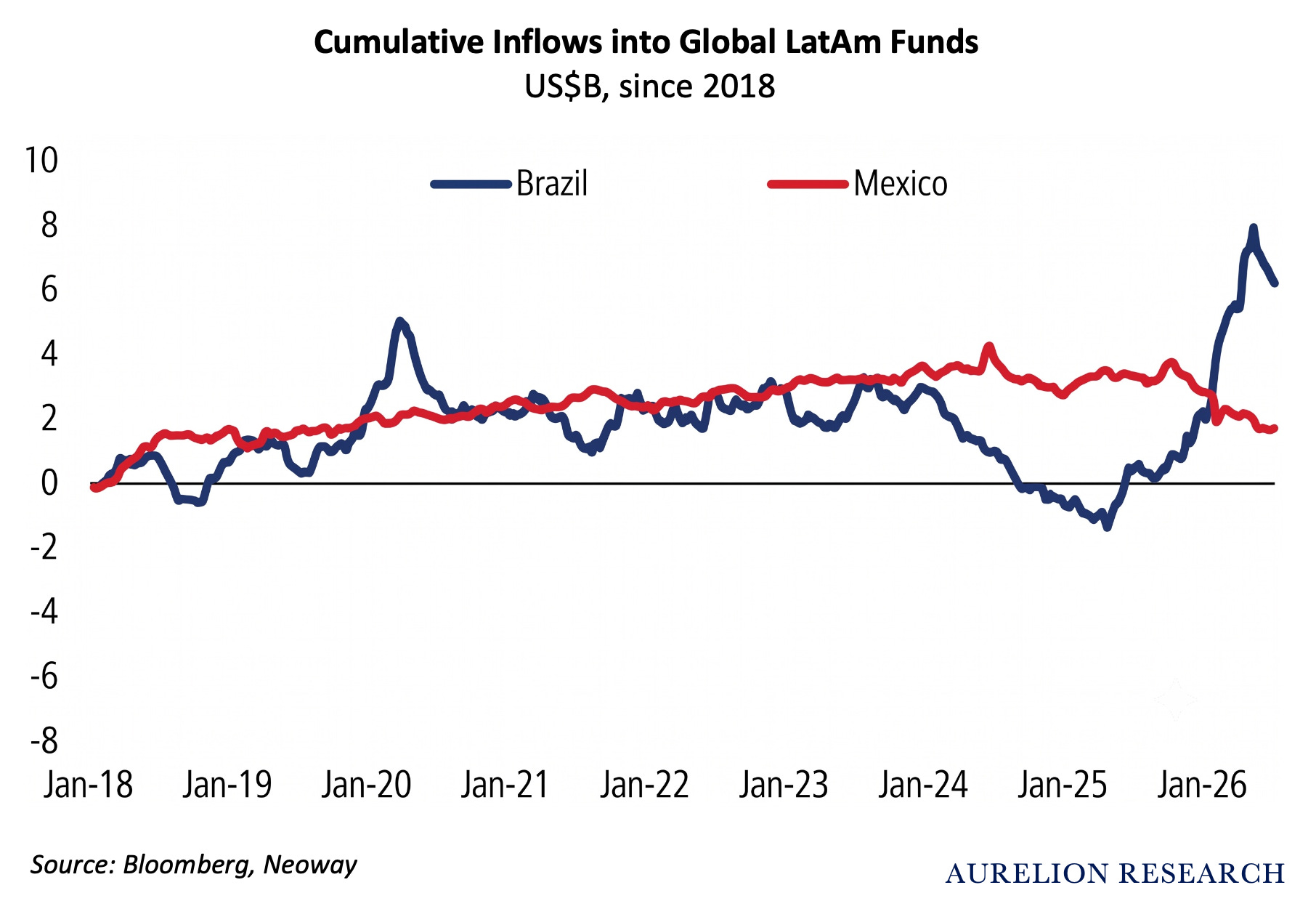

Now, looking at cumulative inflows into LatAm funds, there are no real surprises. Even though flows have slowed over the past couple of months, Brazil remains the most popular destination. Meanwhile, Mexico has been relatively stable, without much excitement, and is now starting to lose some momentum.

Mexico is not in the worst position, but it is certainly not in the best one either. Uncertainty surrounding its relationship with the US, combined with ongoing tensions with Trump, has created additional pressure on the economy.

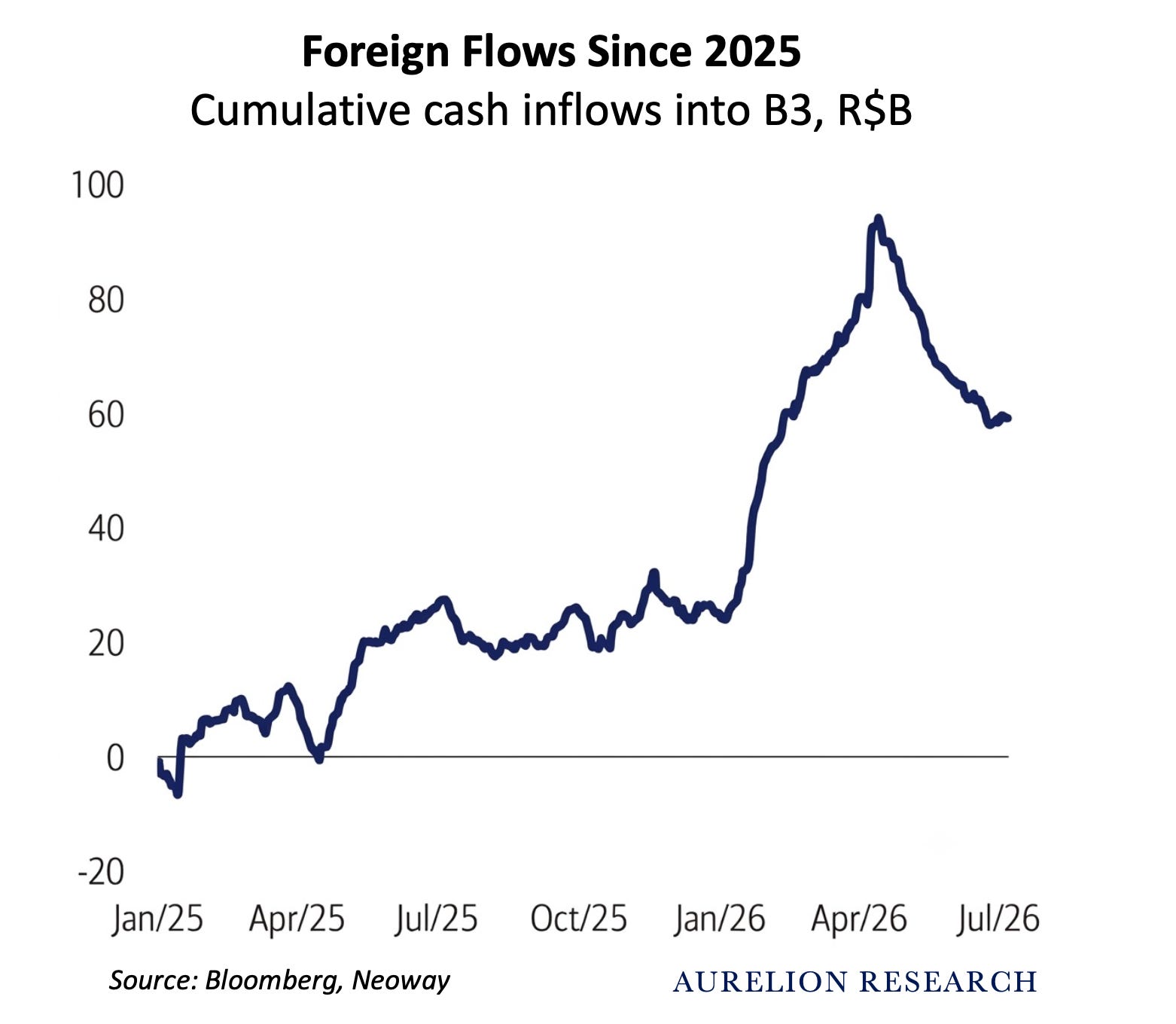

Then, looking at foreign cash inflows since 2025, we can see that the trend was consistently improving until May. However, since then, oil market turmoil driven by uncertainty surrounding Hormuz has put some pressure on LatAm, as markets became more cautious given the region’s exposure to energy markets.

That being said, we do not expect this downtrend to last for long. In our view, this is more of a temporary pullback driven by short-term uncertainty rather than a shift in the broader investment trend, so it is not a major concern for us.

An interesting view comes from BlackRock’s LatAm team, which sees a significant valuation gap between the US & LatAm:

“We continue to see Latin America as one of the most mispriced regions globally. Early action from LatAm central banks has created high real yields and room for rate cuts, providing a strong setup for domestic equities that US growth portfolios cannot replicate.”

On our end, we have always been selective when it comes to Latin America, but we are ready to increase our exposure when the right opportunities emerge. We do consider the country and political environment when thinking about timing, but our main focus remains finding great businesses, as it always should be.

In Brazil, for example, we can still find world-class defensive businesses with dominant market positions, strong ROEs, and high double-digit dividend yields, opportunities that are increasingly rare in the U.S.

Many of these companies still trade at single-digit earnings multiples, allowing investors to get paid while waiting for sentiment to improve. Do not be misled by the discouragement of global investors with LatAm due to short-term political noise and elevated interest rates, particularly in Brazil.

Lazard’s global strategy team highlights Latin America as an important diversifier for portfolios heavily concentrated in US tech:

“LatAm equities offer low correlation to the mega-cap tech trade dominating Wall Street. With investors seeking diversification, the region’s mix of commodities and undervalued businesses makes it an attractive allocation for 2026.”

2. Equity Markets: A Decade of Opportunity?

Let’s look at the most important markets in LATAM.

We can clearly see two groups emerging. Argentina, Peru, and Colombia have been leading the charge, delivering impressive gains since 2025.

Meanwhile, Brazil, Chile, and Mexico are still playing catch-up, with their markets remaining below their previous highs in 2025. The race has already started, and so far, only two countries are out in front: Peru and Argentina.

The key thing to remember is that Latin America is not one single market. Correlations across the region are generally much lower than what investors are used to seeing in the US or Canada. Each country has its own economic cycle, political environment, and policy decisions that can push markets in different directions. With elections happening at different times across the region, each market also creates its own unique catalysts and opportunities.

Here is a recent quote about Latin America that we particularly liked:

“The broader community of investors often sees emerging markets as chaotic, and that has traditionally also been the case for Latin America. But when you see structural changes, like the more market-friendly government in Argentina today and better-functioning institutions, that is the fuel for markets to start climbing.” - Franco Di Nicola, CFA, PM at Bishop Capital (July 2026)

We believe this creates an interesting opportunity: instead of treating LatAm as one single trade, investors can move from one market to another depending on where the next opportunity emerges. For example, if Brazil is heading into an election and we believe the outcome could be positive for equities, we can position ourselves accordingly. Then, a few months later, if Chile becomes the market with the next major catalyst, we can shift our focus there.

3. Macro: The Pulse of LatAm Economies

We are witnessing a setup that is still in its early stages.

Across Latin America, the outlook will depend on a combination of factors. Some variables are easier to anticipate, while others remain unpredictable and outside of our control. As analysts, we have to accept that uncertainty and focus on the key constraints and catalysts that are beginning to align.

Three key factors tie the whole story together:

Debt is at historical highs. Governments are carrying high debt levels, leaving them with less room to support their economies through spending.

Stock valuations are near historical lows. Markets have been depressed for so long that many investors are pricing in a scenario where nothing changes.

Investment growth is the missing piece. These countries cannot rely only on consumption or commodity exports. A new cycle of investment and capital spending is needed to restart stronger economic growth.

And we believe that process is already beginning. GDP growth may not fully reflect it yet, but the underlying signals are there. The timing feels right, and we believe the next few years could mark a meaningful shift for Latin America.

The key is understanding that an economy is more than just numbers.

Inflation can be high, growth can be weak, and a president can be unpopular. These things matter, but only to a certain extent. What counts most is understanding where a country is heading, its ambition, and its potential.

That is why we spend time speaking with local experts. We want to develop a real and tangible understanding of the markets we invest in, something that goes beyond the data and allows us to truly feel the opportunity.

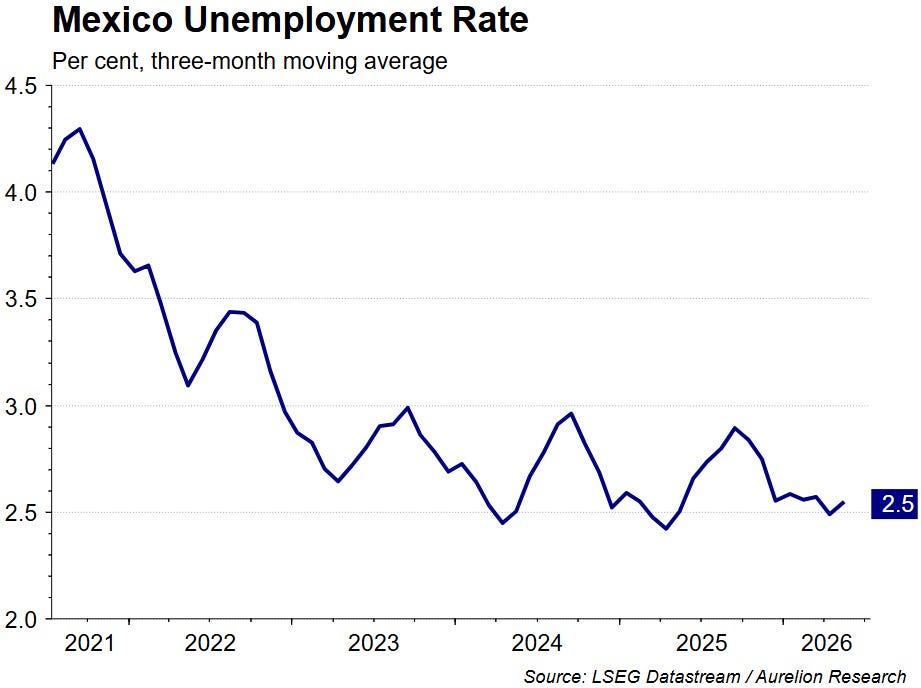

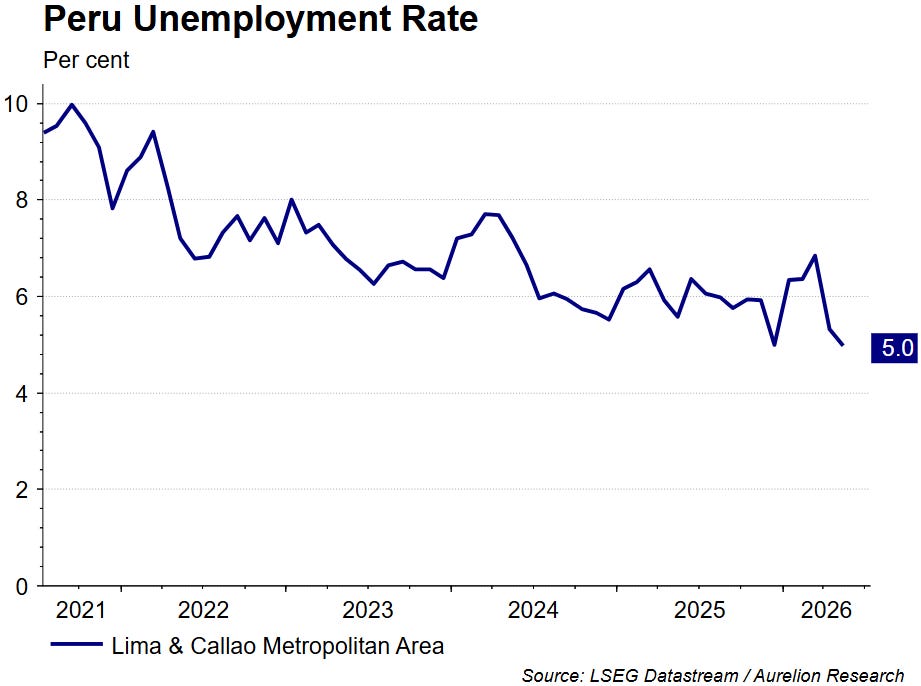

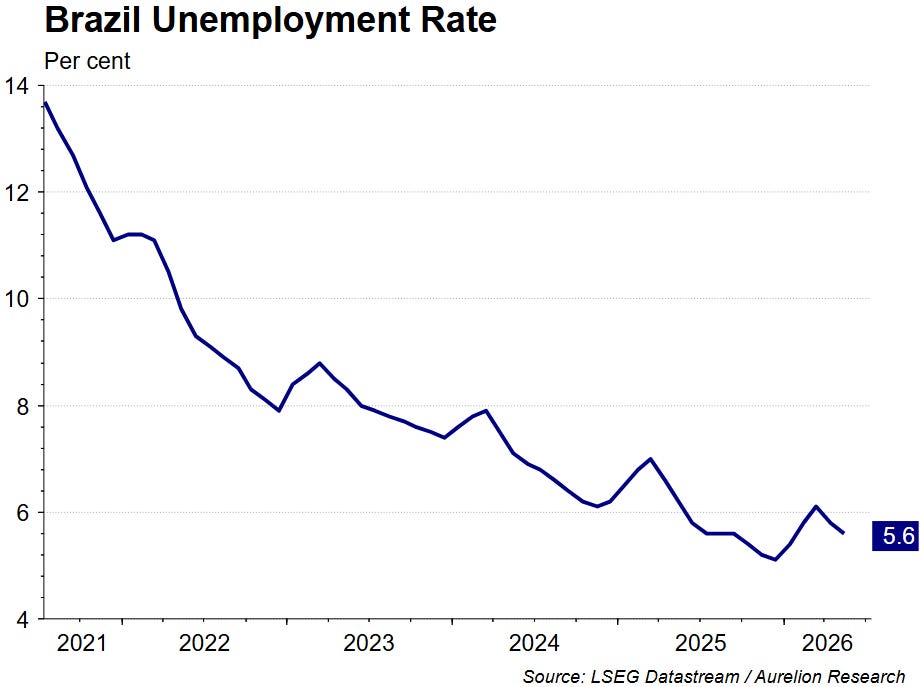

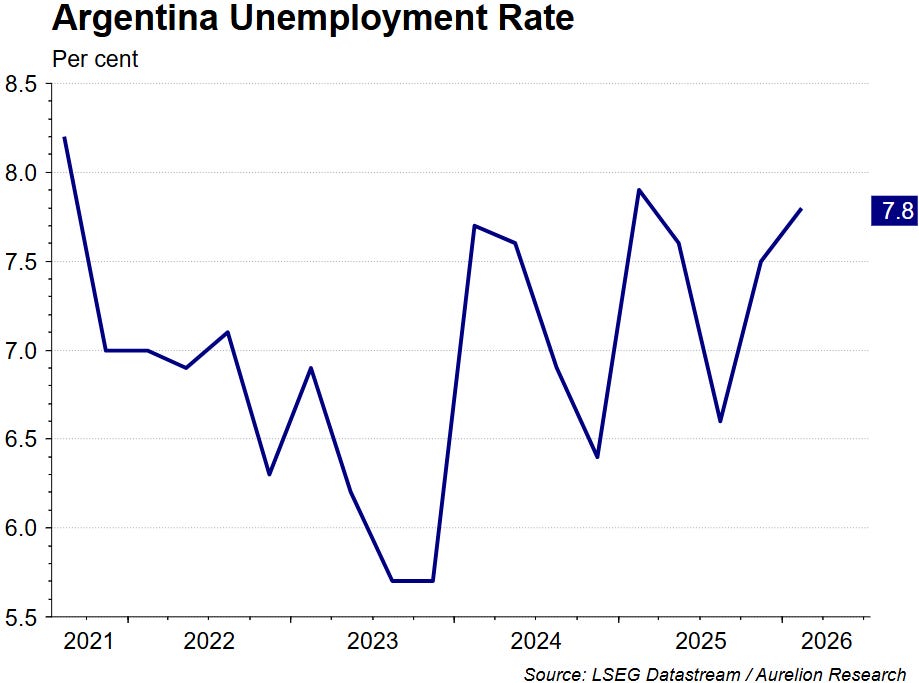

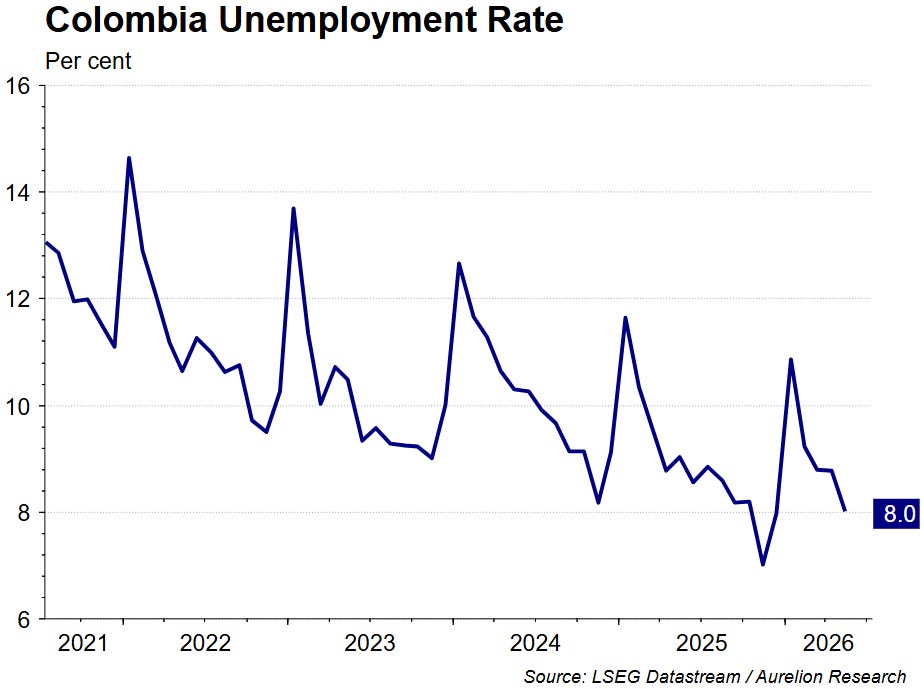

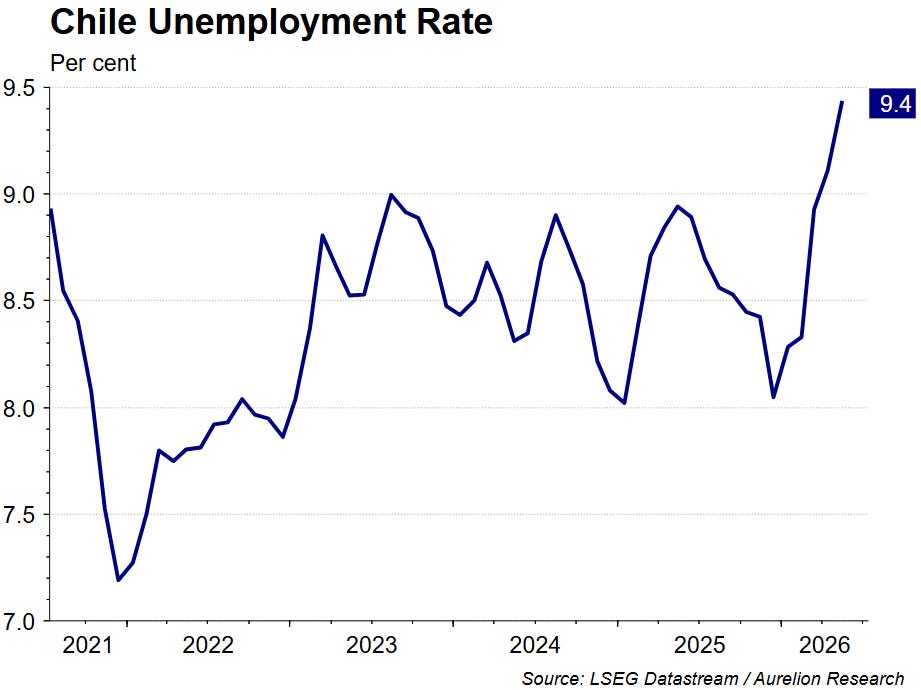

Let’s look at some numbers. Unemployment is one metric we always pay attention to, as it provides a simple but powerful view of what is really happening in an economy. It may not be the most exciting data point, but sometimes the less obvious indicators reveal the most important trends.

Mexico is at 2.5%.

Peru is at 5.0%.

Brazil is at 5.6%.

Argentina is at 7.8%.

Colombia is at 8.0%.

Chile is at 9.4%.

If there is only one thing we want you to take away from this section, it is that in Latin America, unemployment rates tell you a lot about where a country is in its economic cycle and where its financial markets could be heading.

Take Chile as an example. Chile was ahead of many of its regional peers, with a more developed economy and stronger growth profile. However, the economy has been cooling, and the labor market is now reflecting that, with unemployment reaching 9.4%. The situation could improve under President Kast, as markets are expecting a more business-friendly environment.

Mexico tells a different story. With unemployment at 2.5%, it looks more like a mature economy such as Canada, where the labor market tends to be more stable through different cycles. This does not mean there are no challenges, but it highlights a country with a stronger economic foundation.

The rest of the region is more mixed. In our view, Argentina and Colombia both have significant room for improvement, and we believe their unemployment rates should trend lower as their economies continue to recover.

4. Peru: The Cinderella Story of LatAm

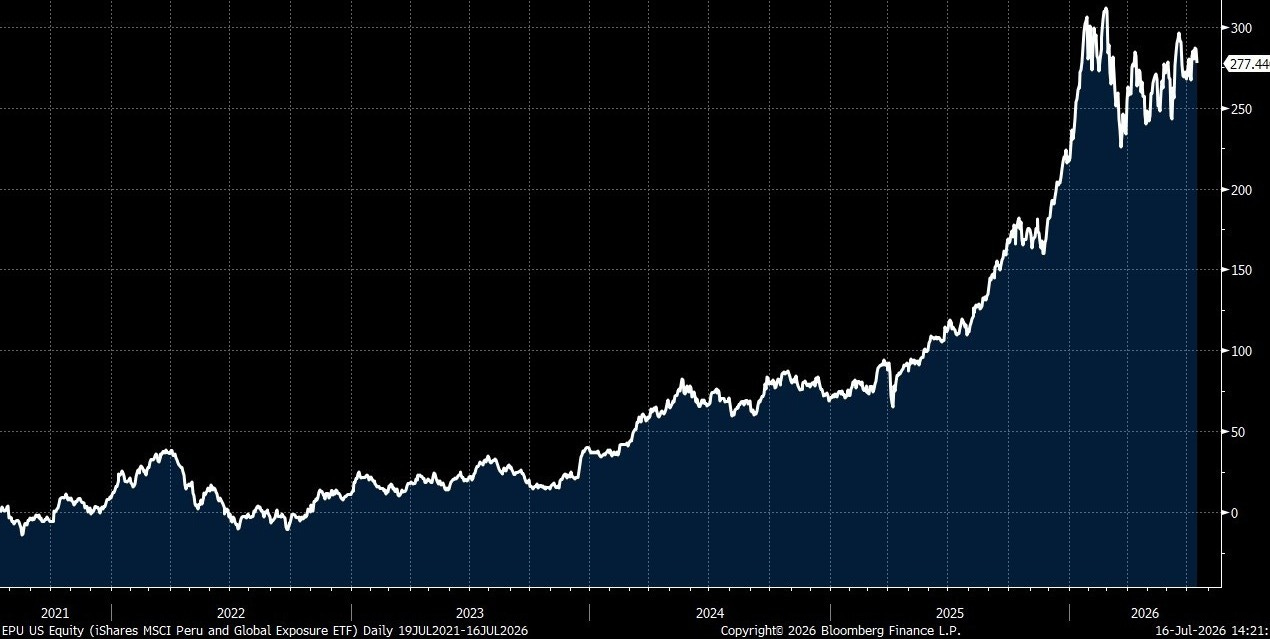

Peru is a market that is often left behind, forgotten, or simply overlooked, whatever word you want to use. It is a country that almost no one talks about. Yet, it is up 19% YTD, nearly 80% since last year, and more than 277% since 2021. Clearly, the Peruvian equity market (EPU) deserves far more attention.

Peru (EPU) Has Been One of LatAm’s Best Performers Since 2021

More recently, Peru held its elections in early June 2026, with a market-friendly candidate coming out on top. She is the daughter of former President Fujimori, and her campaign focused on two main priorities: restoring security through a tougher approach to crime and maintaining Peru’s market-oriented economic framework, which has supported private investment and business growth for the past three decades. Although the margin of victory was very narrow, we were told that institutional investors have reacted positively so far.

Let’s get to the good part: despite significant volatility and domestic political uncertainty during the first half of the year, we believe Peru’s economic fundamentals remain solid. Private demand is holding up, export conditions are improving, and the mining sector is emerging as a key driver of growth.

Mining & Metals: Strong global prices for copper and gold are keeping the country’s terms of trade strong and supporting a significant current account surplus, which reached 4.3% of GDP earlier this year, the highest level since 2006.

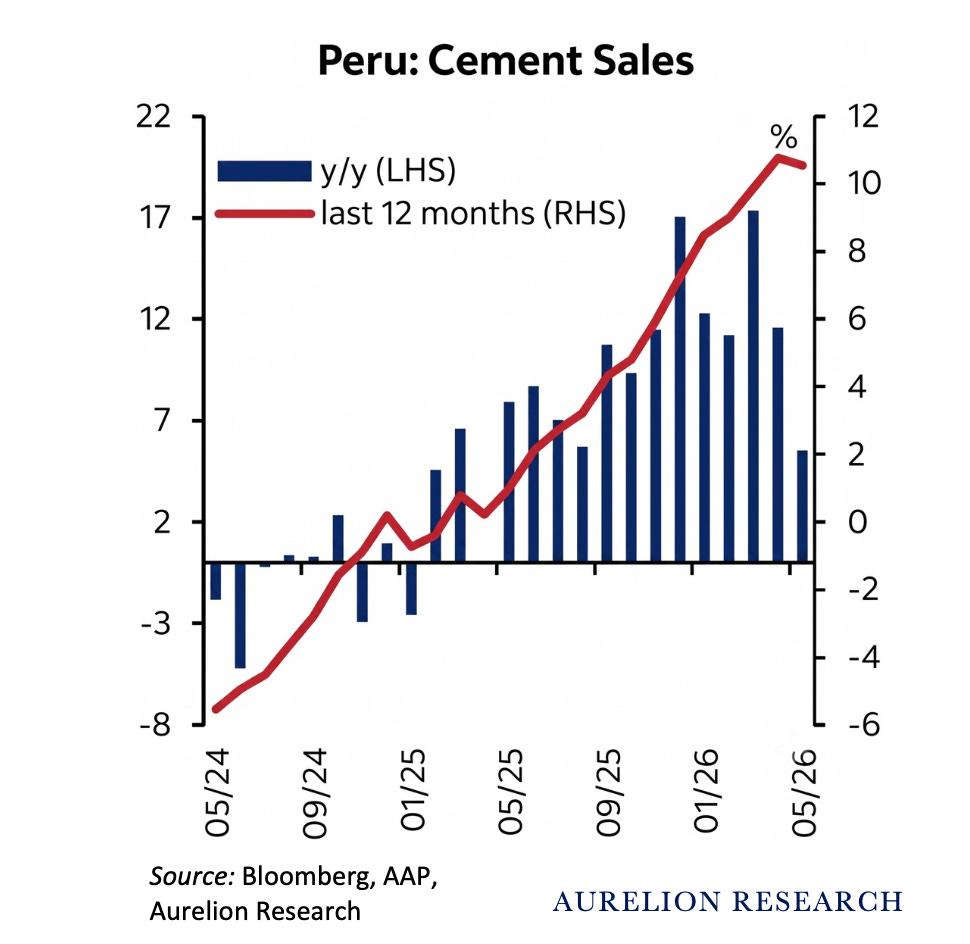

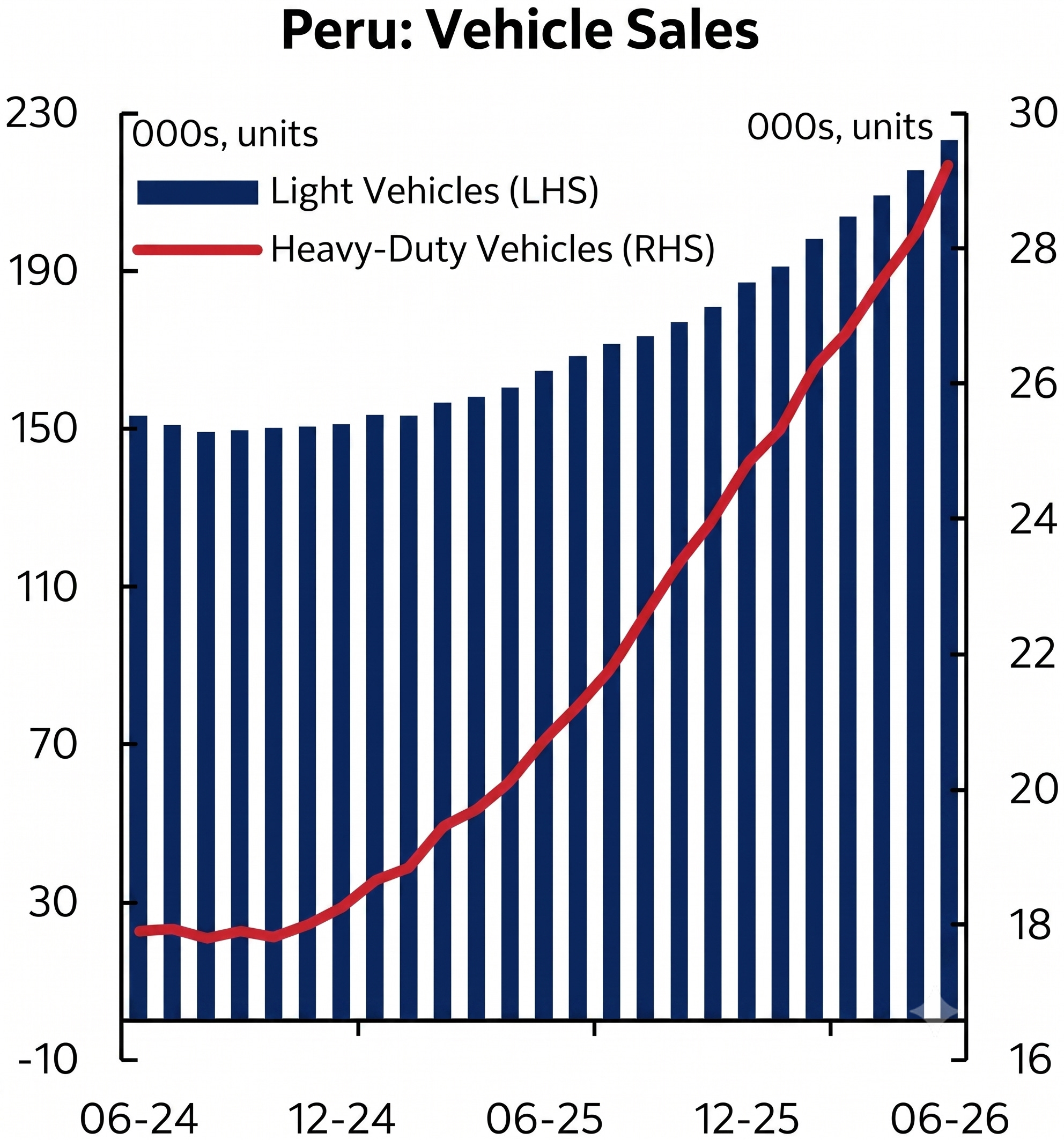

The Peruvian economy continues to build momentum. Business activity remains strong, cement sales are at record highs, and new vehicle sales reached an all-time high for the month of June. The data continues to point in the right direction.

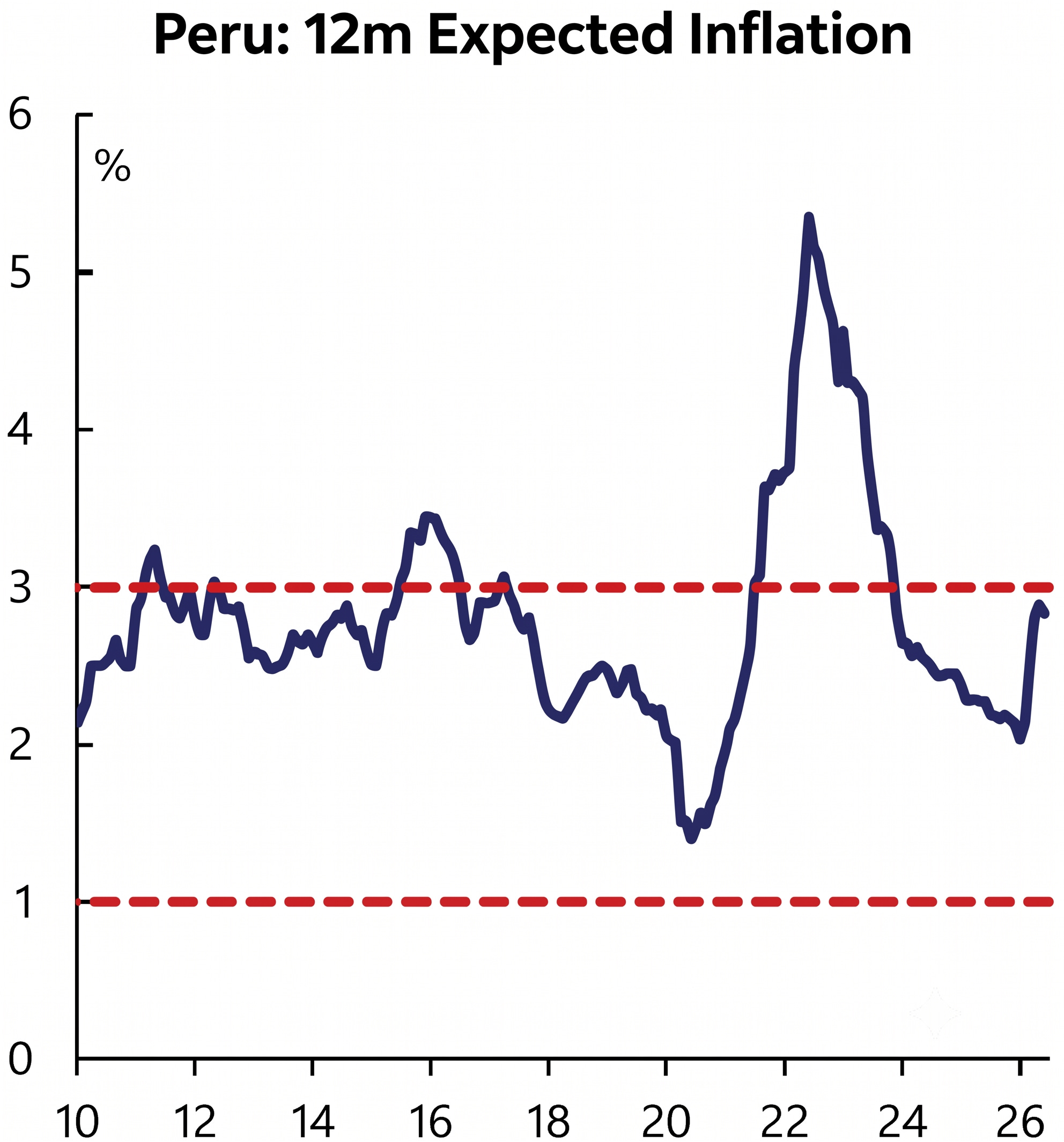

Inflation remains well under control. Headline inflation came in at 0.23% in June, while core inflation was just 0.08%, both remaining in line with the central bank’s target on an annualized basis. Inflation expectations also continued to move lower, giving the central bank more room to support the economy.

As always, there are risks.

El Niño (H2 2026): Looking ahead, one of the main risks for the second half of the year is a potential severe El Niño event, which could put pressure on key sectors such as agriculture and fishing, and drive inflation higher.

Illegal & Informal Mining: A significant portion of gold exports may come from informal or illegal sources (a negative for Peru), though the exact size is difficult to measure due to limited traceability. Some estimates suggest that, out of the $23.2B in gold exports in 2025, only $10.7B came from formal companies, with the remainder linked to informal or untraced production.

5. Colombia & Argentina: Our LatAm Favorites

You saw the title, these are our two favorite ones, where we believe there is the most upside and where equities are the most compelling right now.

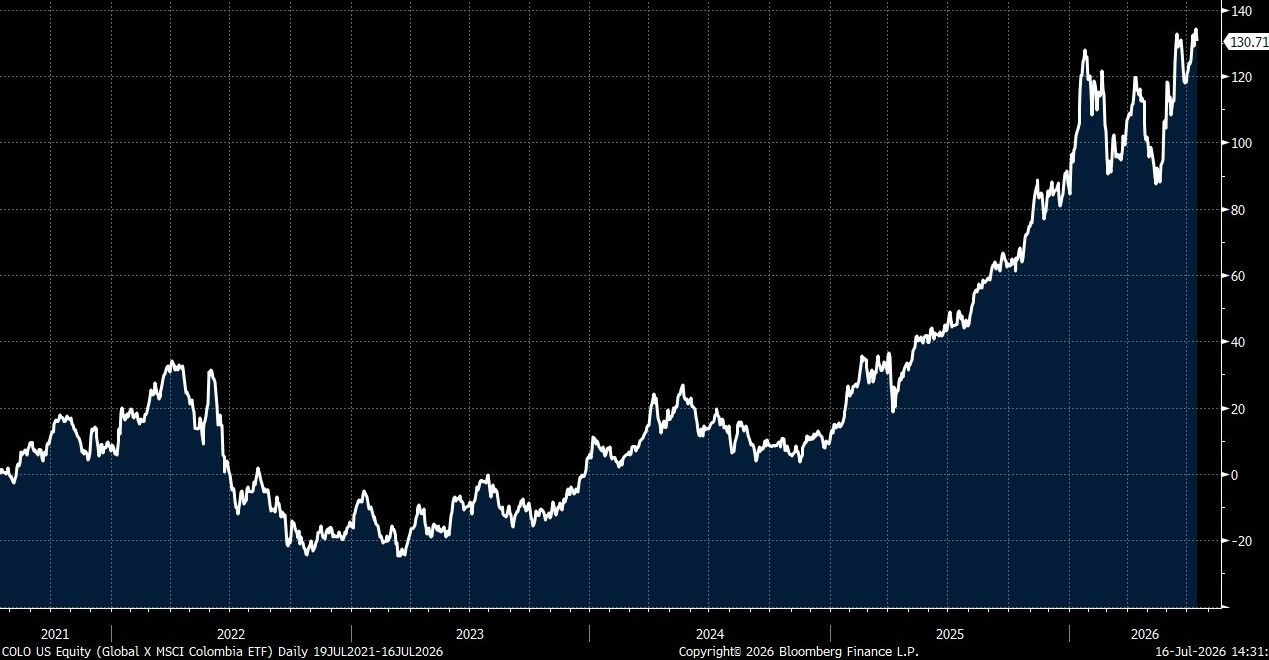

5.1 Colombia: At an Inflection Point

First, Colombia. The elections just happened in June, and the candidate we believed would be the most positive for equities came out on top. Abelardo de la Espriella is now the key figure for the Colombian market going forward.

We are already starting to see that reflected in the market, and we believe Colombia is one of the countries where the story is finally changing. There is something going on there, and we believe it is something good.

We expect the coming years to be bright for Colombia, both economically and in the markets. As investors, that is exactly the combination we want to see.

Colombia Equity Market Performance Since 2021

To better understand where Colombia is heading after the election, both politically and from a market perspective, we spoke with a Colombian analyst working at a hedge fund in Bogotá, who shared valuable insights on the market.

In Conversation: Colombian Analyst

He began by pointing out that although the right secured the presidency, the narrow victory shows Colombia remains deeply divided. The Espriella administration is expected to be more supportive of businesses, particularly in energy, mining, and financials. The main question now is whether it can secure enough congressional backing to implement its agenda.

He added that sentiment among both local and foreign investors in Colombian equities is better than it was before the elections. After years of uncertainty, investors now have more visibility on what to expect, making them more willing to allocate capital to equities instead of staying focused on fixed income.

In our view, Colombian equities are highly attractive right now.

We were waiting for a Petro victory, and now that it has happened, we believe the timing is right to get allocated to this market. Valuations are compelling, and investor sentiment around the country has improved.

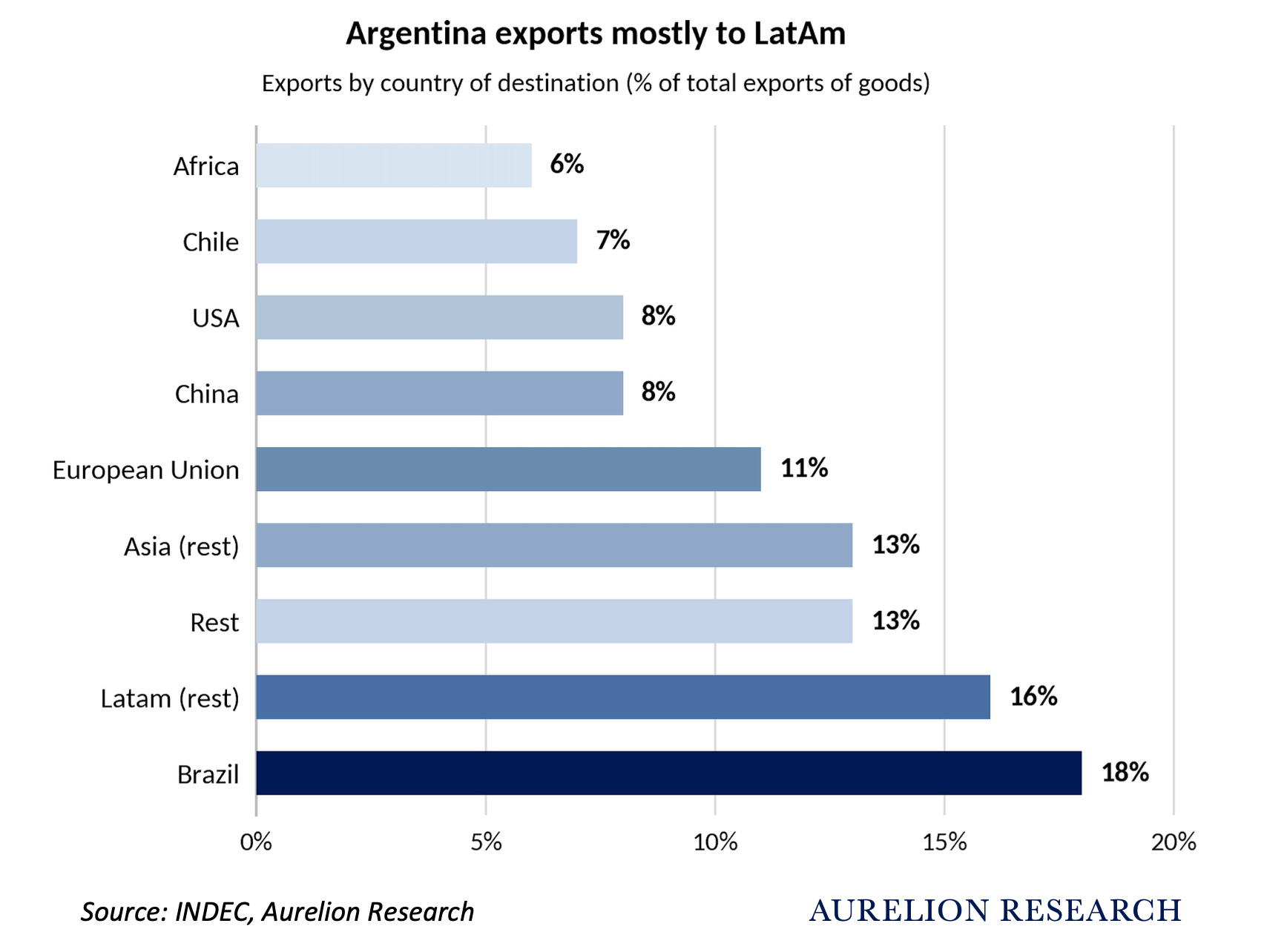

5.2 Argentina: The Turnaround Story

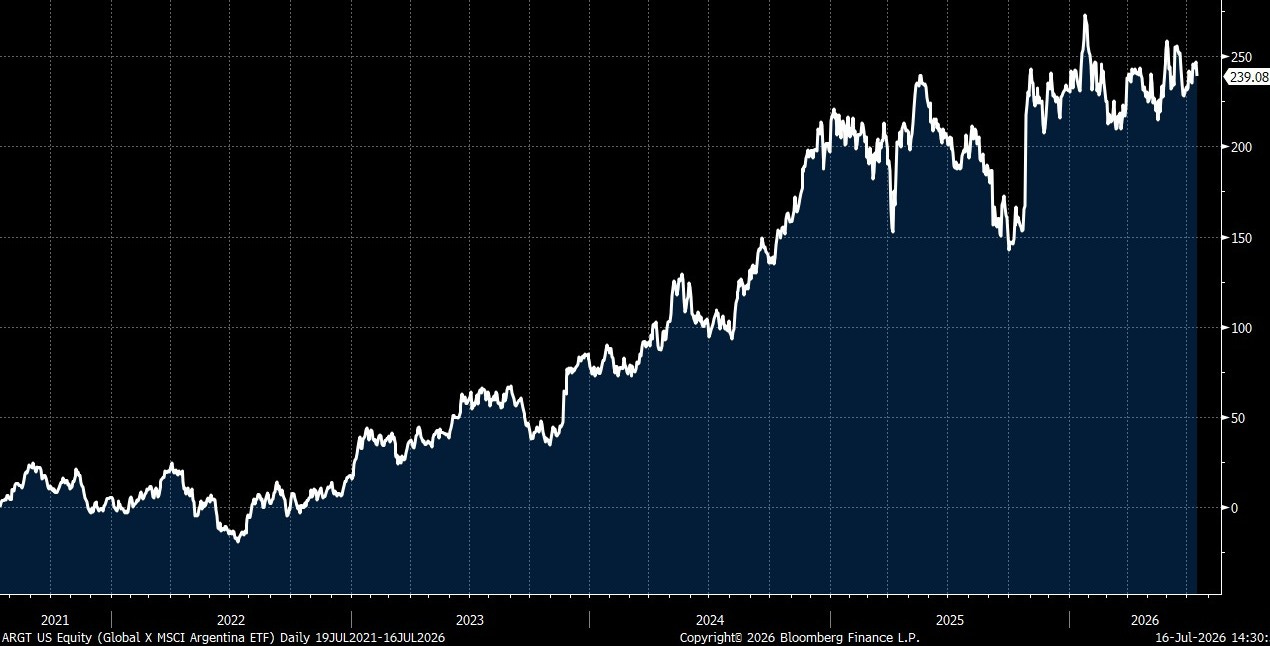

For Argentina, the story is different. When Javier Milei first entered office, let’s say it was loud. The market reacted immediately, investors got excited, and equities started booming as the country entered a new phase. However, that momentum faded over time as investors started waiting for real progress and confirmation that the reforms could translate into stronger economic conditions.

Trump Meets with Argentina’s President Javier Milei

Now, we believe this momentum is starting to return. Argentina remains one of the highest risk/reward opportunities in the region: the upside could be substantial if reforms continue to progress, but investors need to be patient as the economic recovery takes time to translate into stronger fundamentals.

ARGT Is Among LatAm's Best Performers Since 2021

Our Conversation with a Political Analyst:

We spoke with a political analyst who mentioned that the slowdown in economic activity and the increase in inflation earlier this year had a negative impact on Milei’s approval ratings. However, he also believes that this could improve as inflation continues to come down and growth starts to recover, which would support Milei’s chances heading into the next election.

He also highlighted that the government will likely need to build stronger relationships with governors to improve governability and push its agenda forward. Overall, there is a broad view that, regardless of who wins the 2027 elections, Argentina should be in a much stronger position than four years ago, with better export dynamics and a greater focus on fiscal discipline.

Also, something to consider with Argentina is that its economy is less tied to the US manufacturing cycle compared to countries like Mexico. Argentina’s growth story is being driven more by domestic reforms, energy, agriculture, and improving economic conditions. The country is increasingly following its own path, and so far, that direction has been positive for the economy.

In our view, Argentine equities are attractive right now. While commodities are not where we see the biggest opportunity, we believe banks, utilities, and telecom are the areas to be positioned in.

6. Brazil: Too Early to Call

Brazil is the most unpredictable market among all the countries we focus on. The upcoming October election is the biggest variable, but the truth is, we simply cannot predict the outcome between Bolsonaro and Lula. It is impossible to know.

And this uncertainty will remain an important factor going forward.

When investors do not have visibility on what comes next, they usually become more cautious. That said, it is important to remember that the Brazilian market was performing very well before the Hormuz situation and the energy market turmoil. The market had been on a strong run since the end of 2024.

So what do we do from here? We believe the key is to focus on quality businesses that can move on their own, without being too affected by the broader Brazilian market. That is what we like about Brazil right now: many companies are still trading at depressed valuations, creating attractive opportunities. The banking and energy sectors are probably the only areas we would be more cautious on for now, but outside of that, there are plenty of names worth looking into.

7. Mexico & Chile: Waiting for Their Moment

We covered our two favorite markets earlier. Now, it is time to look at the two that are more difficult to assess. This does not mean we are uncertain about them, but rather that the investment case is much more nuanced.

Both markets offer interesting opportunities, while also facing a more complex set of challenges. One is often described as America’s backyard, while the other operates almost as a world of its own. Let’s take a closer look at each of them.

7.1 Mexico: Caught Behind the Border Wall?

Mexico is a country we look at a little differently compared to the rest of Latin America. Its biggest advantage is its proximity to the US, but the story goes beyond geography. Over the years, Mexico has become a major manufacturing hub, producing goods that are eventually exported to the US.

Mexico plays an important role in the growth story of the US because it helps supply many of the goods and resources needed to support the “Trump economy.” When the U.S. economy is strong, Mexico is usually one of the countries that benefits the most, although the relationship is not always that simple.

Mexico has a strong economy, high-quality businesses, and many factors working in its favor. However, we believe one should be careful about becoming too comfortable, as the relationship with the U.S. can change quickly.

Our Conversation with a Mexican Fund PM:

The biggest concern is the USMCA, the free trade agreement between the United States, Mexico, and Canada. With the agreement now set to be reviewed every year, many businesses are delaying new factories, expansions, and other investments until there is more clarity. As long as companies do not know what the future trade environment will look like, many are choosing to wait.

Another topic that came up was Mexico’s manufacturing future. Autos have been the country’s biggest success story for decades, but investors are now asking whether AI and IT hardware could become the next major growth opportunity.

On our end, we believe it is still too early to tell.

That said, Mexico remains home to some of the highest-quality companies in Latin America, and we have given them a special place in our LatAm Equity Basket, which we will explore in the next section.

Just one month ago, we published a report on one of our Mexico holdings: a company we believe is a hidden beneficiary of the upcoming World Cup. It is a great example of the type of opportunities we look for: high-quality businesses with unique catalysts that the market may be underestimating.

7.2 Chile: The Quiet Market

For Chile, there is not as much to say compared to the other markets we cover. It is the “boring” one in Latin America, and that is not necessarily a bad thing. It is a more stable country, with stronger institutions, and it generally does its own thing without being heavily affected by regional noise. For us, the challenge is that there is less of an investment edge. Chile is not a place where you typically see major surprises or dramatic changes, which also means the upside is likely to be more limited than in some of the other opportunities across the region.

We believe Chile can continue to grow over time, but we see the upside as more limited compared to markets like Colombia or Argentina, where the investment story is earlier and the potential rerating could be larger.

Another challenge with Chile is accessibility. Unlike other markets in the region, fewer Chilean companies trade through U.S. ADRs, which can make it more difficult for international investors to build meaningful exposure.

That said, Chile remains a quality market in Latin America.

It may not be the market with the biggest near-term catalysts, but it offers stability, strong businesses, and a more predictable environment, which still has value in a region where uncertainty is often the biggest risk.

8. Latam Equity Basket

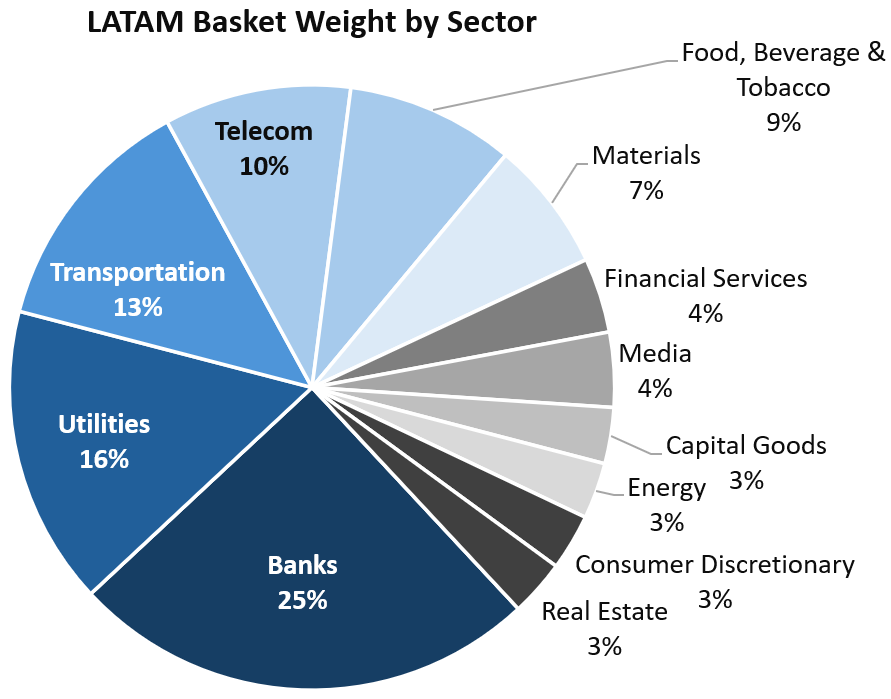

We built a diversified equity basket focused on companies we believe offer the most compelling combination of quality, upside potential, and exposure to the Latin American growth story.

Investors can implement it on Plutus here.

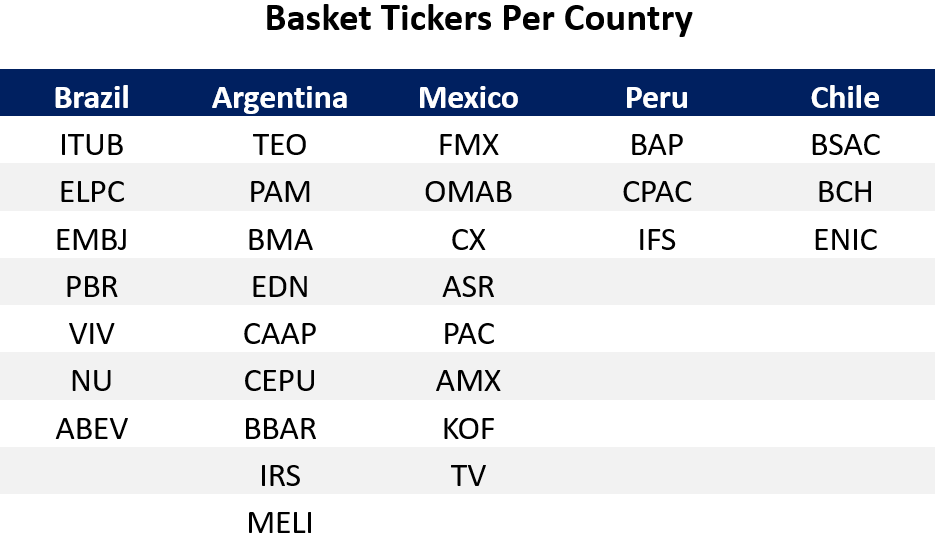

There are certainly other companies we would have liked to include; however, we decided to focus exclusively on U.S. ADRs. This not only ensures accessibility for most investors but also provides greater liquidity.

In Latin America, some of the biggest upside opportunities are often found in banks. Once political uncertainty clears and elections are behind them, banks are usually among the first sectors to react, and they can move quickly. Utilities are another area we find particularly attractive, offering strong businesses, reliable cash flows, and dividend yields that are difficult to find in US equities today.

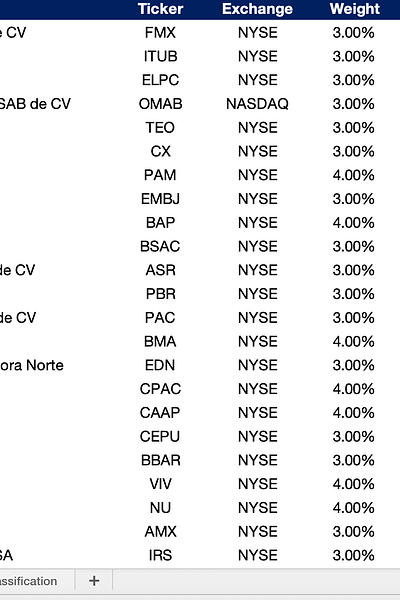

Here below, you can find the tickers included in the basket by country:

As you can see, there is a strong presence of Brazilian and Mexican companies in the basket. Some might ask: if we were not the most bullish on these two markets in the report, why include so many companies from them?

The answer is simple: in Latin America, some high-quality companies behave differently from their home markets. They are influenced by their country, but only to a certain extent. Many of the best businesses in the region have diversified operations, international exposure, and revenues coming from multiple markets.

Brazil and Mexico are also the two largest equity markets in Latin America, which naturally means they are home to many of the region’s strongest companies. A company can be listed in Brazil or Mexico while still benefiting from growth across the entire region. For us, the focus is where a company’s business is actually coming from, rather than simply where it is based.

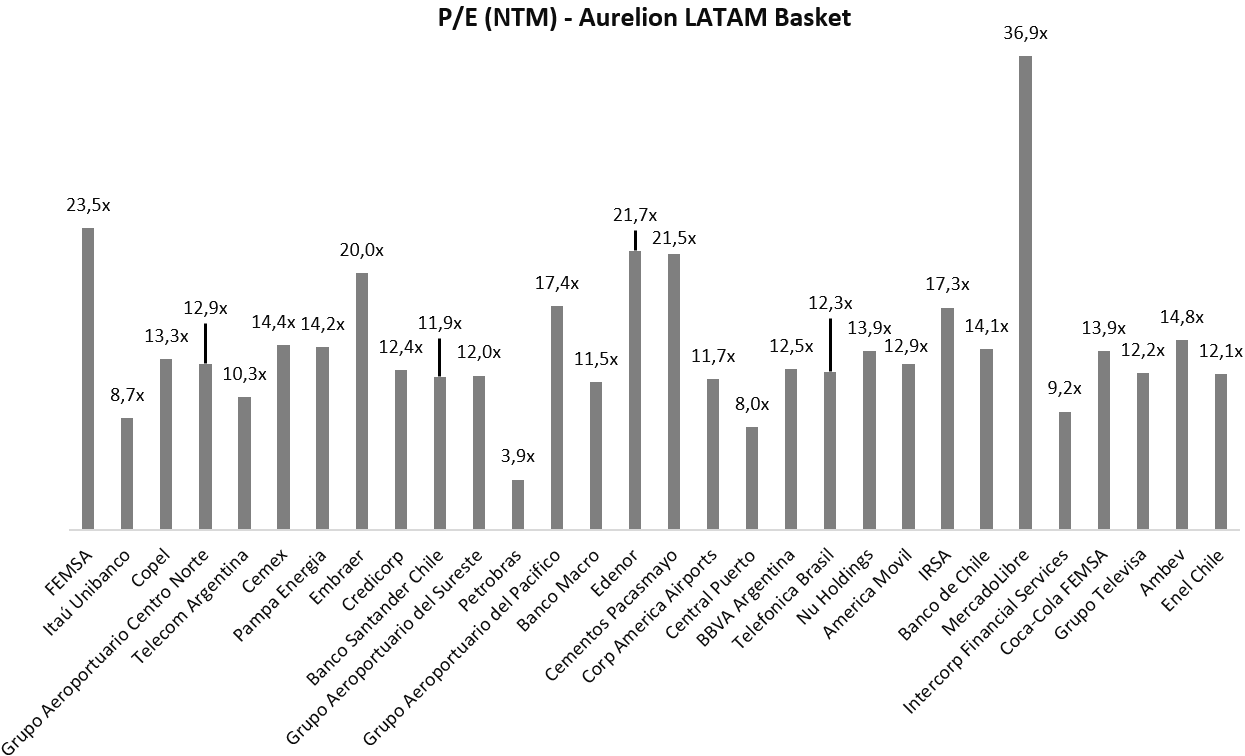

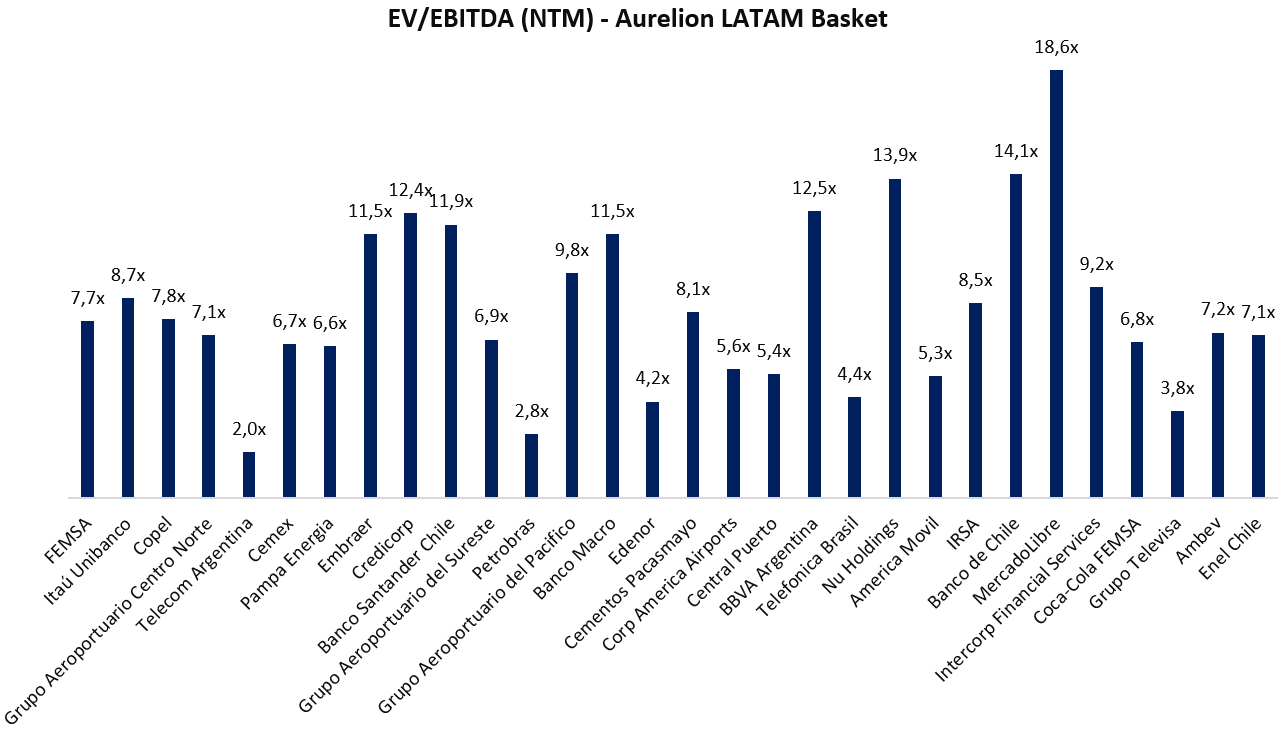

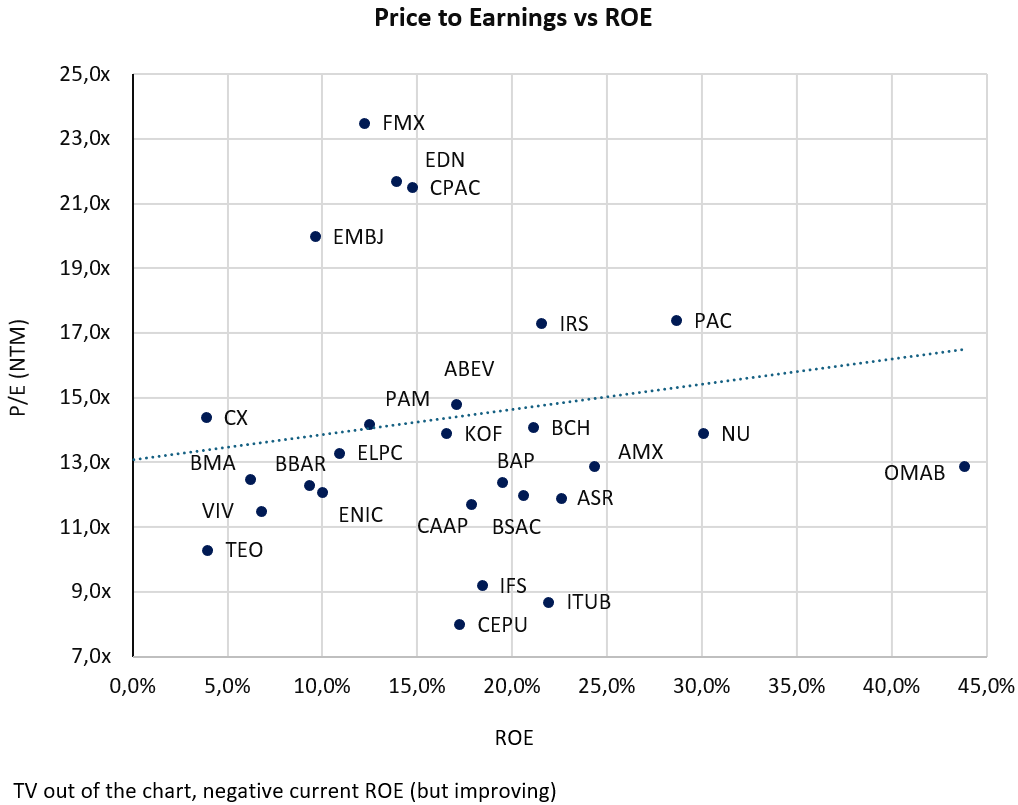

Below, you can see an overview of the forward P/E and EV/EBITDA multiples for every company included in the Aurelion LATAM Basket. As you can see, most of these companies are trading at attractive valuations.

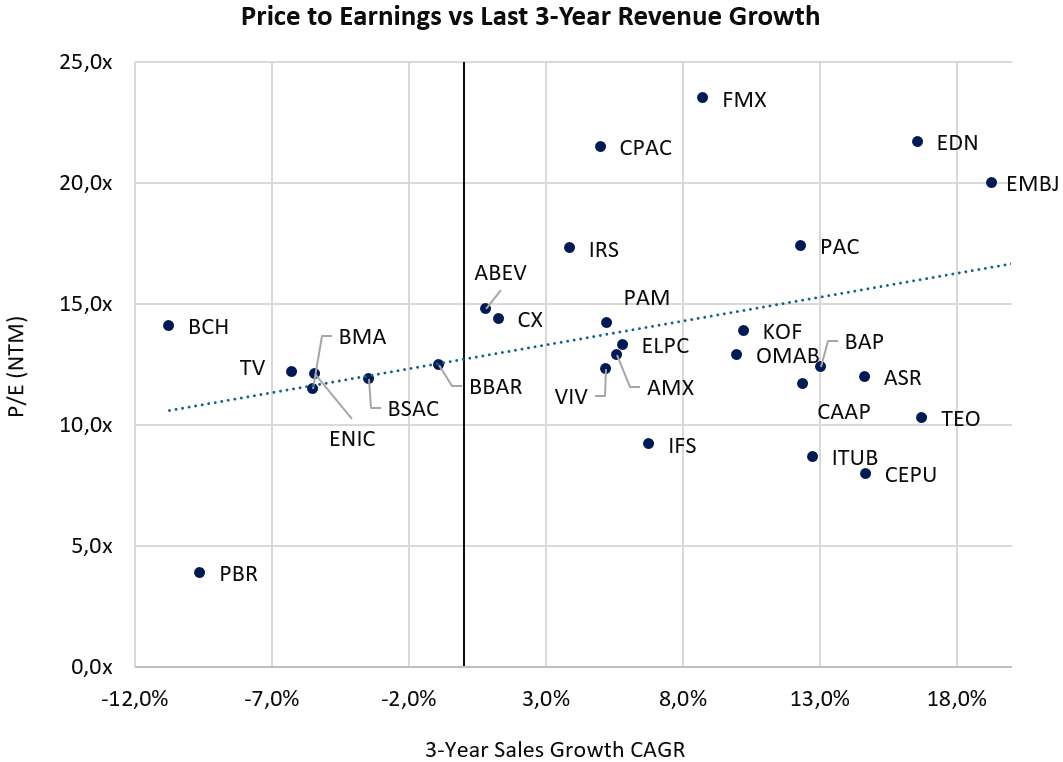

We also included P/E multiples compared with historical revenue growth and ROE. We thought these were particularly interesting because they give a different perspective on the companies in the basket. Some names are already established, high-quality businesses, while others are earlier in their story and could offer more upside if the market starts recognizing their potential.

Here is the full Aurelion LATAM Basket, presented in a different format.

As always, you can search through the table and navigate it to explore each company in more detail.

9. Our Final Thoughts

Latin America is not an easy market. It is complex, volatile, and often uncomfortable to own. But for investors who understand the region and position themselves correctly, the opportunity can be substantial. We wrote this piece to serve as a practical playbook for navigating the region, separating the noise from the opportunities. Today, Colombia and Argentina represent our highest-conviction markets, where we see the most attractive risk-reward.

We see Mexico & Chile as less compelling markets today, but that does not mean there are no attractive companies in these countries. It simply means the current risk-reward is less favorable compared to other opportunities across the region.

View how the portfolio is positioned here: Aurelion Index link.

The Aurelion Team

Questions? Reach us directly on Substack or at contact@aurelionresearch.com.