Latin America Primer: Why the Region is the Most Obvious Bet for the Next Decade

This is intended to be the most comprehensive piece on the sector. We have dedicated a tremendous amount of effort to producing what we believe is the ultimate LATAM playbook.

Investors often stay away from Latin America due to economic or political risks, but we view those exactly the opposite way: as opportunities. Since this is a market we understand deeply, we decided to write a complete playbook on how to play the next bull cycle, which we believe is still in its early innings.

To make this piece more valuable, we spoke with analysts across Argentina, Brazil, Chile, and Mexico. While we could not always get full on-the-ground coverage, we place strong weight on perspectives from people who live and invest in these markets, as they often pick up signals that data alone misses.

At Aurelion Research, we focus on real-world insights, whether from analysts we respect with local experience, portfolio managers who regularly travel across LatAm, or investors with direct exposure to these markets.

Data is important, but it is only part of the picture.

We know this may seem quieter compared to the focus on AI, software, semiconductors, and data centers. Every investor has their own view of the market, and we respect that, but we see significant value in focusing on a region that remains under-covered by most analysts. That is where more attention should be directed. One of the clearest advantages is that LatAm remains largely insulated from the geopolitical instability in the Middle East.

You may refer to the table of contents below the introduction, as several topics, countries and dynamics are discussed.

Introduction: Why LatAm and Why Now?

LatAm is experiencing a notable shift in geopolitics and domestic policy.

LatAm is heavily shaped by politics and elections, which makes getting the macro view right essential. Without it, portfolio outcomes can start to resemble a lottery. Looking ahead, 2026 is set to bring a meaningful political shift, as reflected in the changing alignment shown in the maps below.

Latin America Poised for a 2026 Political Shift

As shown above, Latin America shifted from a largely Right leaning map in 1999 to a broad Left leaning majority by 2023. The areas marked on the 2026 map show where elections are coming up this year, including in key markets like Brazil, Mexico, Colombia, and Peru. We believe this busy election cycle points to higher volatility and another possible shift in the political landscape.

We are also seeing improving interest rates, which supports the bull case for the region. We are looking at a cycle driven by investment and spending.

Every capital market is set to outgrow its underlying economy.

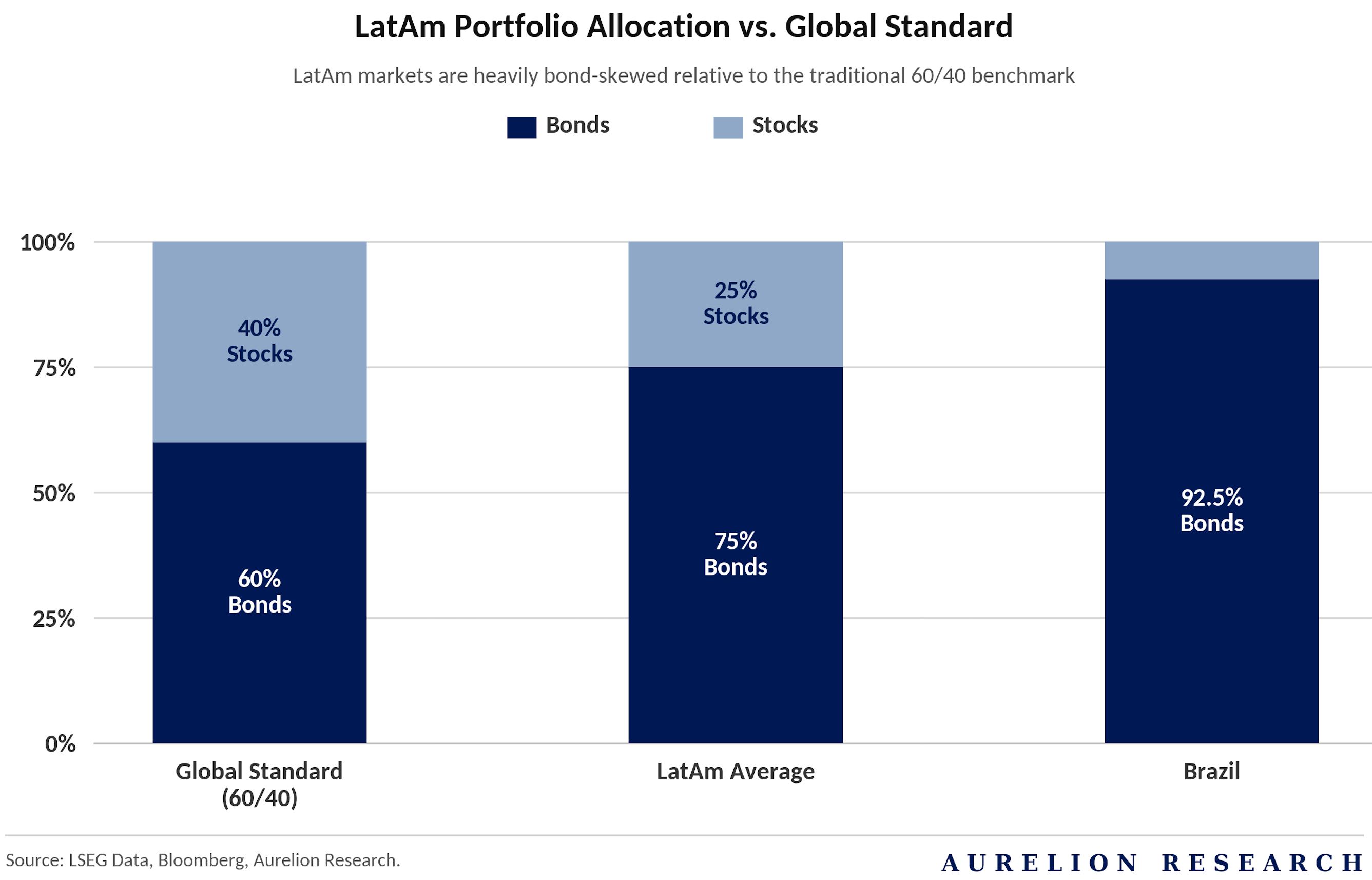

In many cases, that growth may even accelerate due to new regulations, as seen in Chile and Mexico. These markets are highly unbalanced. Traditional portfolio guidance suggests a 60/40 split between stocks and bonds, yet LatAm is closer to 75% bonds. In Brazil, it reaches ~90% to 95% bonds.

The US capital market is now an integrated part of the LatAm story. US venture capital is actively funding new regional business models that challenge the old way of doing things, mostly around digital services.

New IPOs are increasingly happening in the United States. Capital market growth is expected to be the engine for this investment cycle. Historically, this has moved in waves, but right now, stocks as a percentage of total assets are near all-time lows. Returning to those normal levels would represent more capital than LatAm markets could even handle right now.

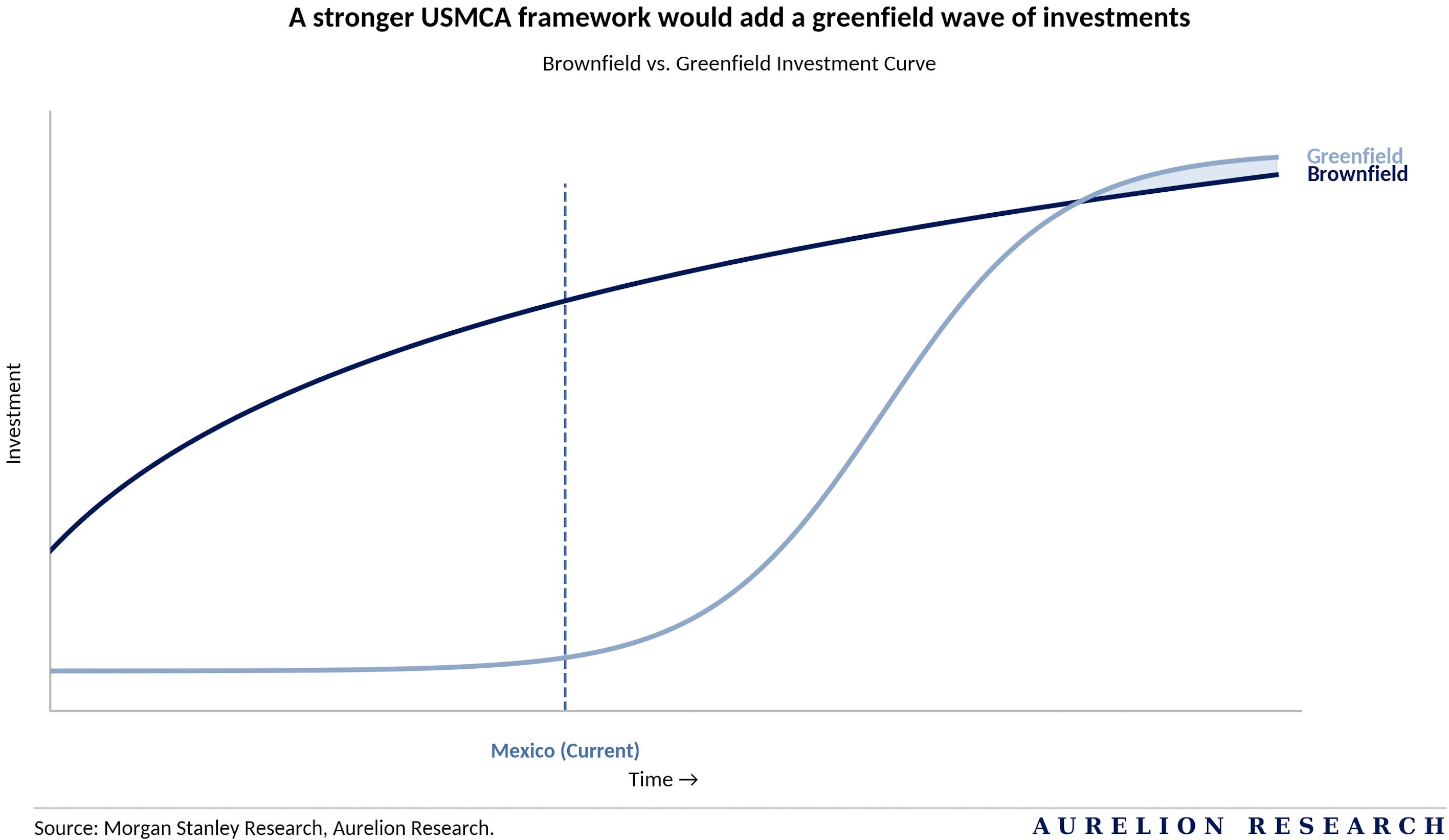

This policy shift across the Americas could be a major turning point. Even if LatAm is not at the center of global change, that change is still central to the region. You can see it clearly as US companies move their supply chains out of Asia and into Mexico to be closer to home. You also see it in the tension heading into the 2026 Brazilian presidential election, where a divide is emerging between the Global South and the US over tariffs and trade threats.

Interest rates look to be peaking and could start to head lower through 2026. LatAm capital markets are far deeper today than they used to be, and we expect them to outgrow their underlying economies. We do not take it for granted that leaders will play their cards right. There is a lot of work left to do, and we are concerned that local regulations are still stuck in the past while the markets themselves become too dependent on the US.

The Regional Breakdown

Chile is starting to turn the corner. After a period of heavy uncertainty, things are beginning to stabilize.

Brazil is essentially running out of room to borrow. The government is reaching the limit of what it can spend, meaning growth has to come from private companies rather than the state.

Mexico needs to move past its current slowdown. To fully take advantage of US companies moving production closer to home, the country needs to speed up spending on infrastructure and energy.

Argentina needs a genuine investment cycle. For any recovery to actually last, it has to move beyond short-term fixes and build a foundation for long-term growth.

The bull case is not a guarantee, but the path is definitely starting to show. It is going to take real political will and a change from how things were done in the past. If the region actually delivers, the upside is massive. LatAm could move away from just being a source of cheap labor and raw materials to becoming a dynamic engine of growth driven by investment.

Table of Contents

Intro: Why LatAm and Why Now?

The LatAm Bull Case (2026-2035)

1.1 Potential Returns: The 2030 Outlook

1.2 Valuation: Room for Re-Rating

Brazil Is Our Top Pick

2.1 Brazil is Just Too Cheap

2.2 The Spring Bull Case

2.3 Supply & Demand Squeeze

2.4 Great Capital Rotation

2.5 Brazil’s Fiscal & Inflation Outlook

2.6 Resolving the Crowding Out Problem

2.7 Our Favorite Brazilian Stock: A New Portfolio Addition

2.8 Perspectives on Cost of Capital

2.9 Our Final Take on Brazil

The Argentina Experiment

3.1 Opening Up the Economy

3.2 A Concrete Economic Recovery

3.3 A History of Turmoil

3.4 Debt Profile & Liquidity Squeeze

3.5 Argentina Bull Case

3.6 Energy Turnaround

3.7 Mining & RIGI Catalyst

3.8 Our Final Take on Argentina

Colombia: High Upside on Hold

4.1 Colombian Energy Squeeze

4.2 Election Catalysts & LT Optionality

4.3 Debt Profile Ahead of the Vote

4.4 Our Final Take on Colombia

Chile: A Safe Haven in Latin America?

5.1 Unlocking the Investment Backlog

5.2 Copper Prices & Sovereign Strength

5.3 Tax Cuts & Capital Market Reforms

5.4 Our Final Take on Chile

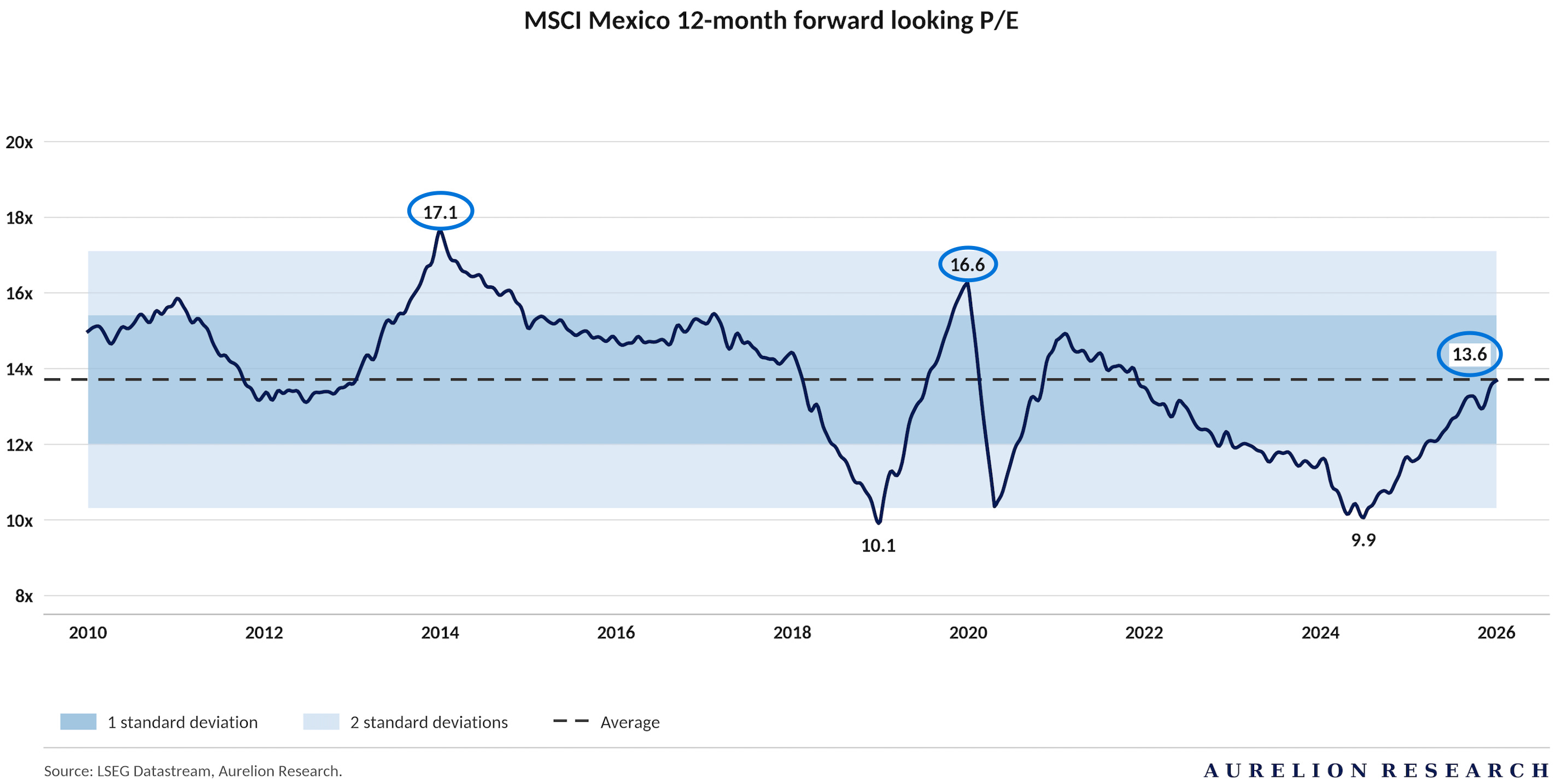

Mexico: At a Turning Point

6.1 The Current Reality

6.2 Scenarios & Regional Upside

6.3 Our Final Take on Mexico

Our Final Take on Latin America

1. The LatAm Bull Case (2026-2035)

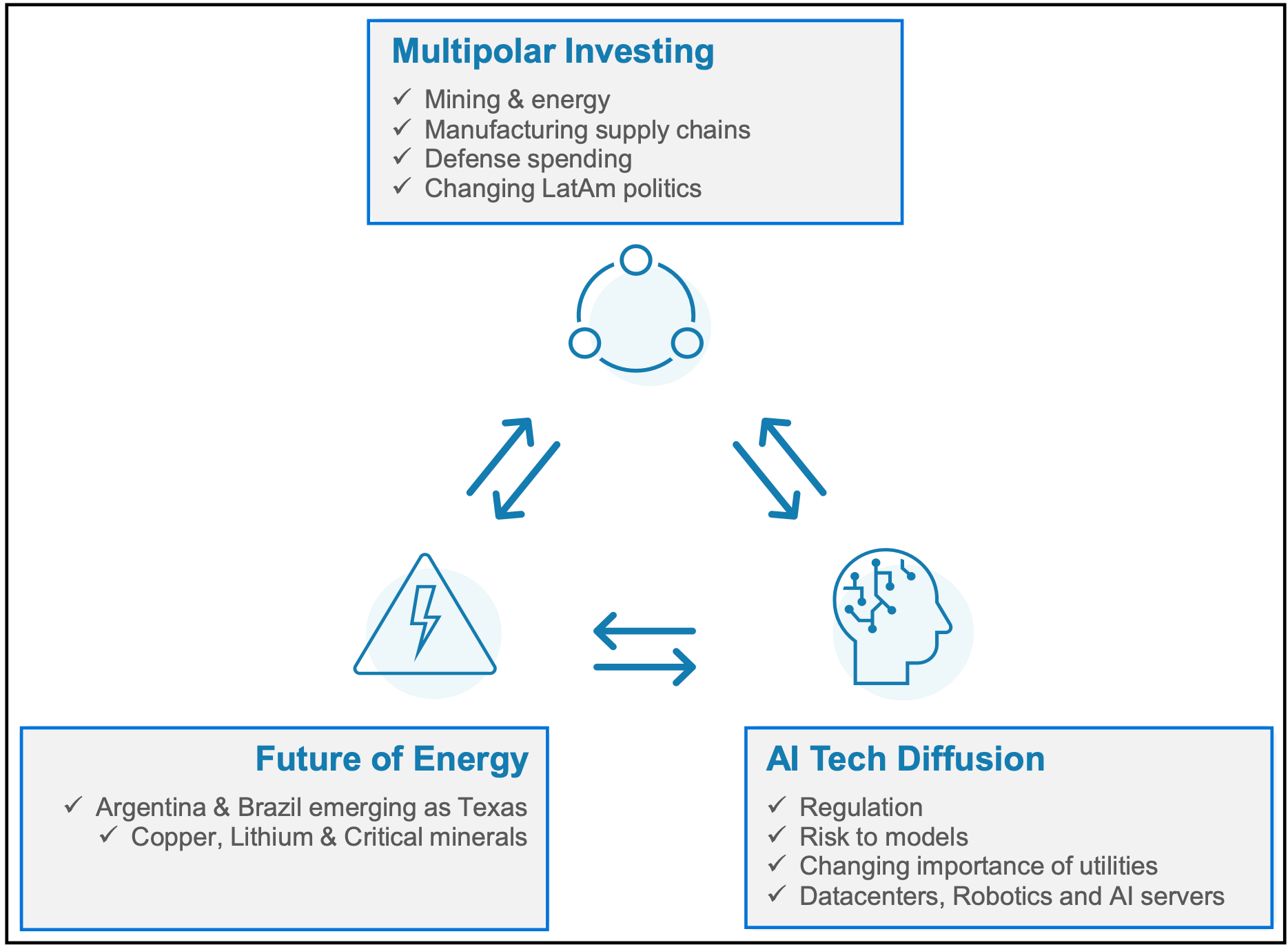

As you already know, we believe LatAm is positioned as the most obvious bet for the rest of the decade. The bull case for the region between 2026 and 2035 rests on a convergence of powerful global forces that have been building for years. We are looking at a fundamental turning point driven by three massive themes that are completely reshaping the global economy.

Key Themes Converging in LatAm

These three drivers are redefining the landscape and creating a durable foundation for massive growth.

First is the shift toward Multipolar Investing. Global supply chains are actively rewiring. With rising global tensions, manufacturing is moving closer to the final consumer, and Latin America is capturing this capital directly. At the same time, shifting local politics and a rising focus on defence spending are changing how capital flows into these countries. The region is becoming a necessary alternative to traditional Asian manufacturing hubs.

Second is the Future of Energy. The global energy map is being redrawn, and Argentina and Brazil are rapidly emerging as massive energy powerhouses, drawing real comparisons to the output potential of Texas. Beyond traditional oil and gas, Latin America controls a dominant share of the copper, lithium, and critical minerals that the world absolutely requires to build the next generation of energy infrastructure.

Third is AI Tech Diffusion. The artificial intelligence boom requires heavy physical assets. As you can imagine, the rapid rollout of data centers, robotics, and AI servers demands massive amounts of reliable power.

This dynamic completely changes the importance of utility companies across the region, turning them from boring local businesses into highly valuable global tech infrastructure. We are also monitoring how regulation and potential risks to AI models will dictate where these physical assets are built.

The true power of this bull case is that these three themes feed directly into each other. The aggressive expansion of AI drives an insatiable need for energy, the future of energy requires critical minerals, and the multipolar shift directs global capital to build it all locally. This rare combination creates a massive engine for growth that the market is currently underpricing.

1.1 Potential Returns: The 2030 Outlook

We are witnessing a setup that is still in its early stages. Across Latin America, the outlook is increasingly defined by a small number of macro constraints and catalysts that are starting to converge. Instead of being driven by a single variable, it now comes down to how these three forces interact over time.

Three specific threads tie the whole story together:

Debt is at historical highs. Governments are stretched thin, so they cannot just spend their way out of trouble anymore.

Stock valuations are near all-time lows. Prices have been held down for so long that the market is basically expecting things to stay stuck forever.

Investment growth is the only move left. These countries cannot rely on people just buying things or selling raw materials alone. They need a real cycle of building and spending to start the next phase.

In a world where the benefits of globalization are fading, these countries have to take greater responsibility for their own growth. Ironically, that external pressure may be the catalyst that finally forces the reforms they need.

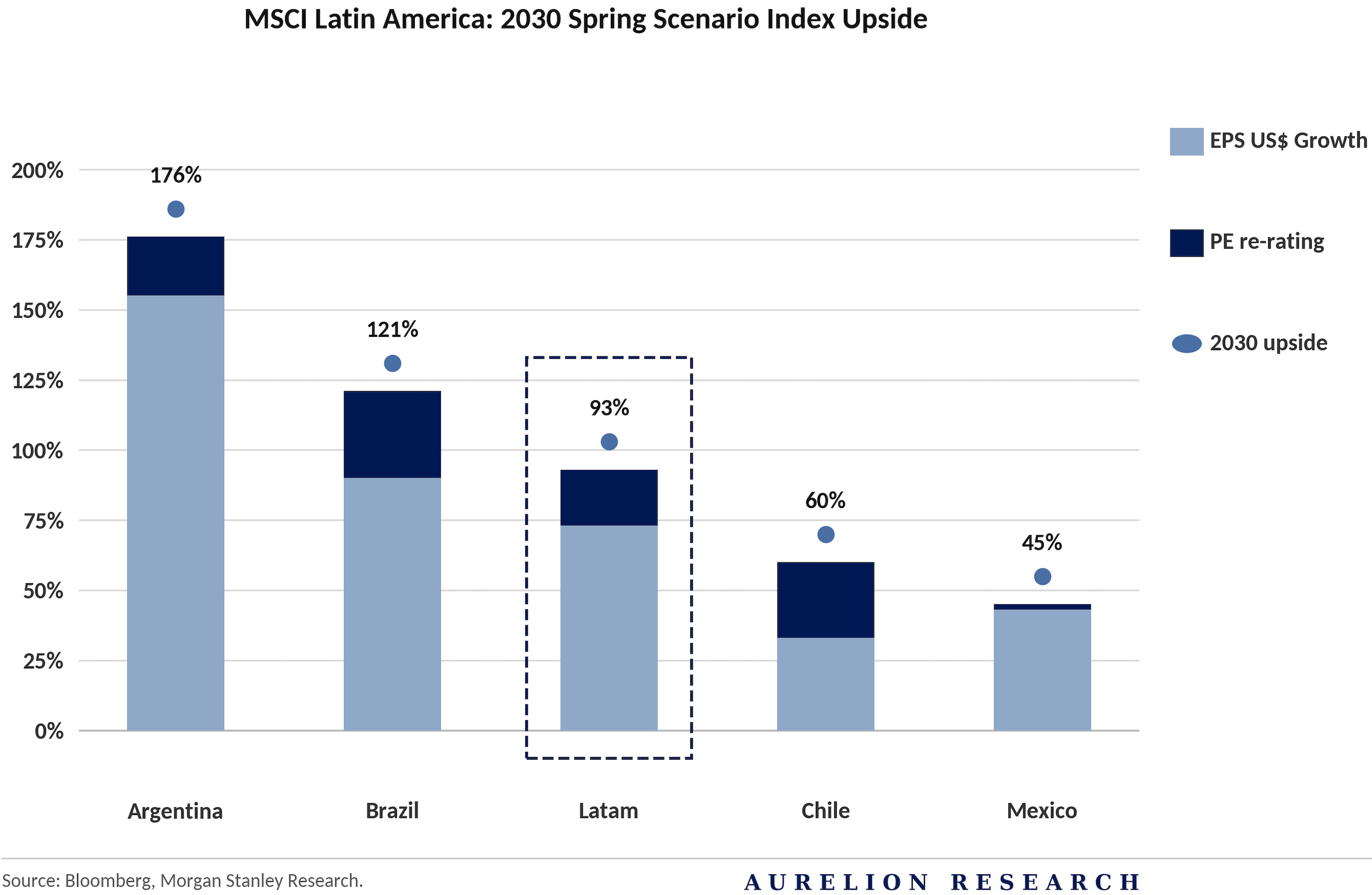

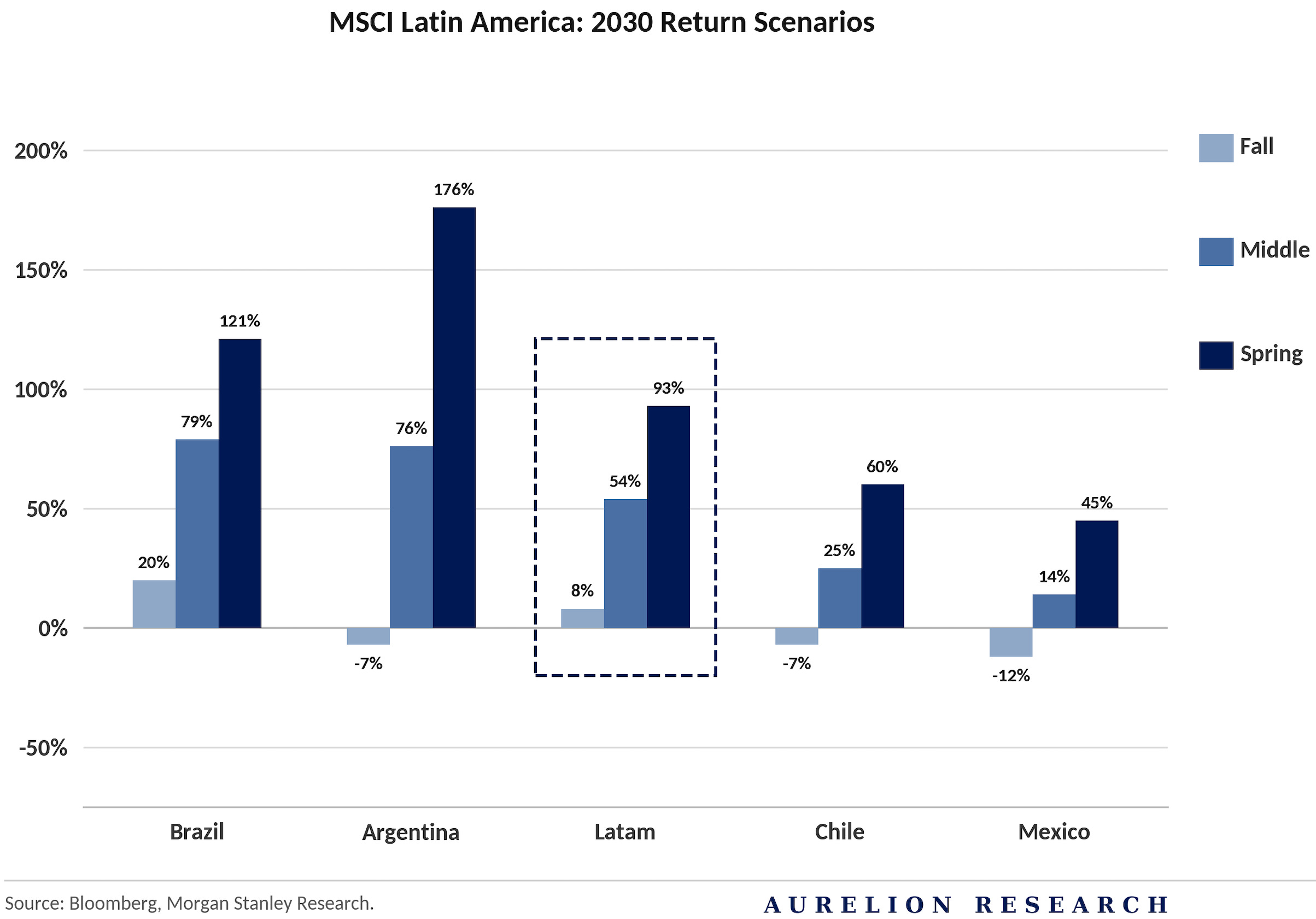

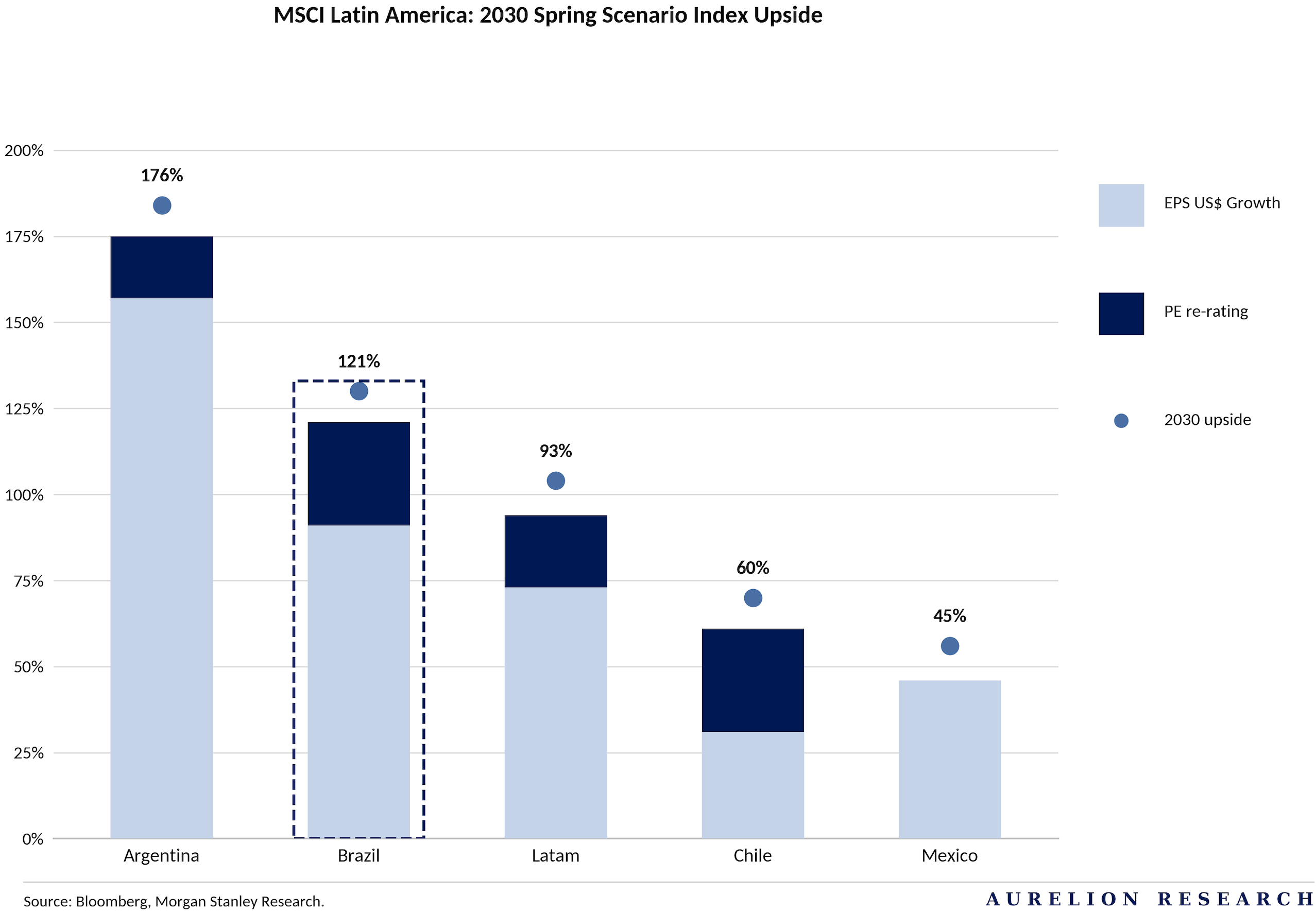

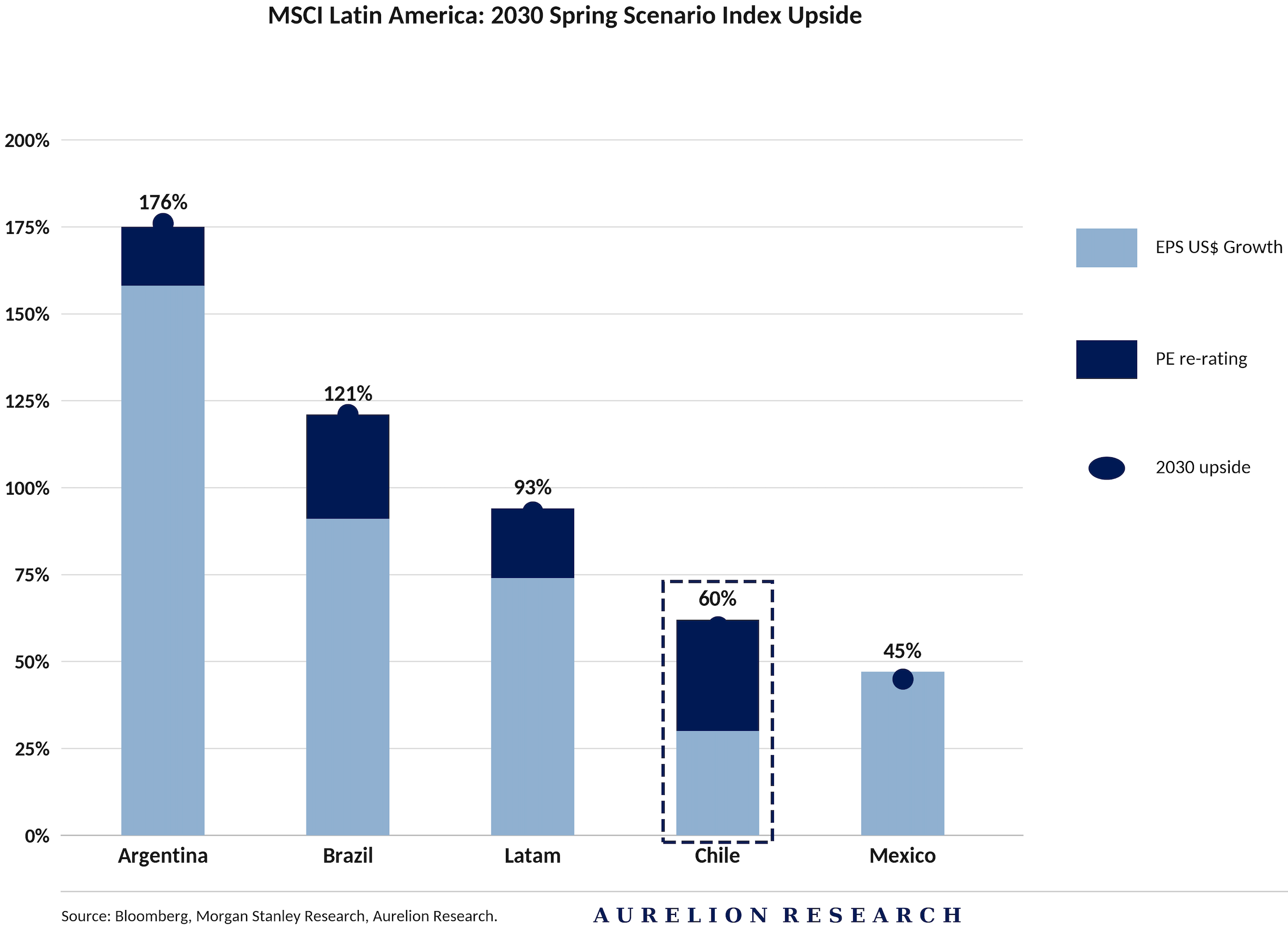

If the region successfully delivers on these reforms, the potential for returns is massive. Morgan Stanley’s “Spring” scenario suggests that by 2030, we could see a total index upside of 93% for Latin America as a whole.

While the “Middle” case still offers a solid 54% return, the “Spring” scenario is where the real upside is. This growth comes from two main drivers: earnings growth (EPS) and a re-rating in valuation multiples (P/E).

When you break it down by country, the numbers are even more striking:

Argentina leads the pack with a potential 176% upside in a bull case. Most of this comes from a massive jump in earnings as the economy resets.

Brazil shows a potential 121% return. Even in a “Fall” scenario where things stay difficult, Brazil is the only major market expected to remain positive with a 20% return.

Chile & Mexico offer more measured but still strong bull case returns of 60% and 45% respectively. In these markets, the growth is almost entirely about earnings rather than just valuation changes.

The bottom line is that the market has priced these countries so low for so long that even a partial return to normal could trigger a major move upward. If the “LatAm Spring” actually takes hold, the region moves from being a forgotten corner of the global market to one of its top performers.

1.2 Valuation: Room for Re-Rating

Latin American equities still have massive room for multiple expansion.

While the region is currently trading near its long term average of 11x to 12x forward earnings, previous bull cycles have seen valuations push much higher. During strong periods, like the mid 2000s and the recovery following the global financial crisis, multiples expanded well into the mid teens.

This history highlights the clear upside potential as macroeconomic conditions improve today. Morgan Stanley projects that LatAm equities could return to that 14x multiple by 2030. This upward move will be driven by three clear catalysts: shifting global politics, the normalization of interest rates, and pivotal elections across the region.

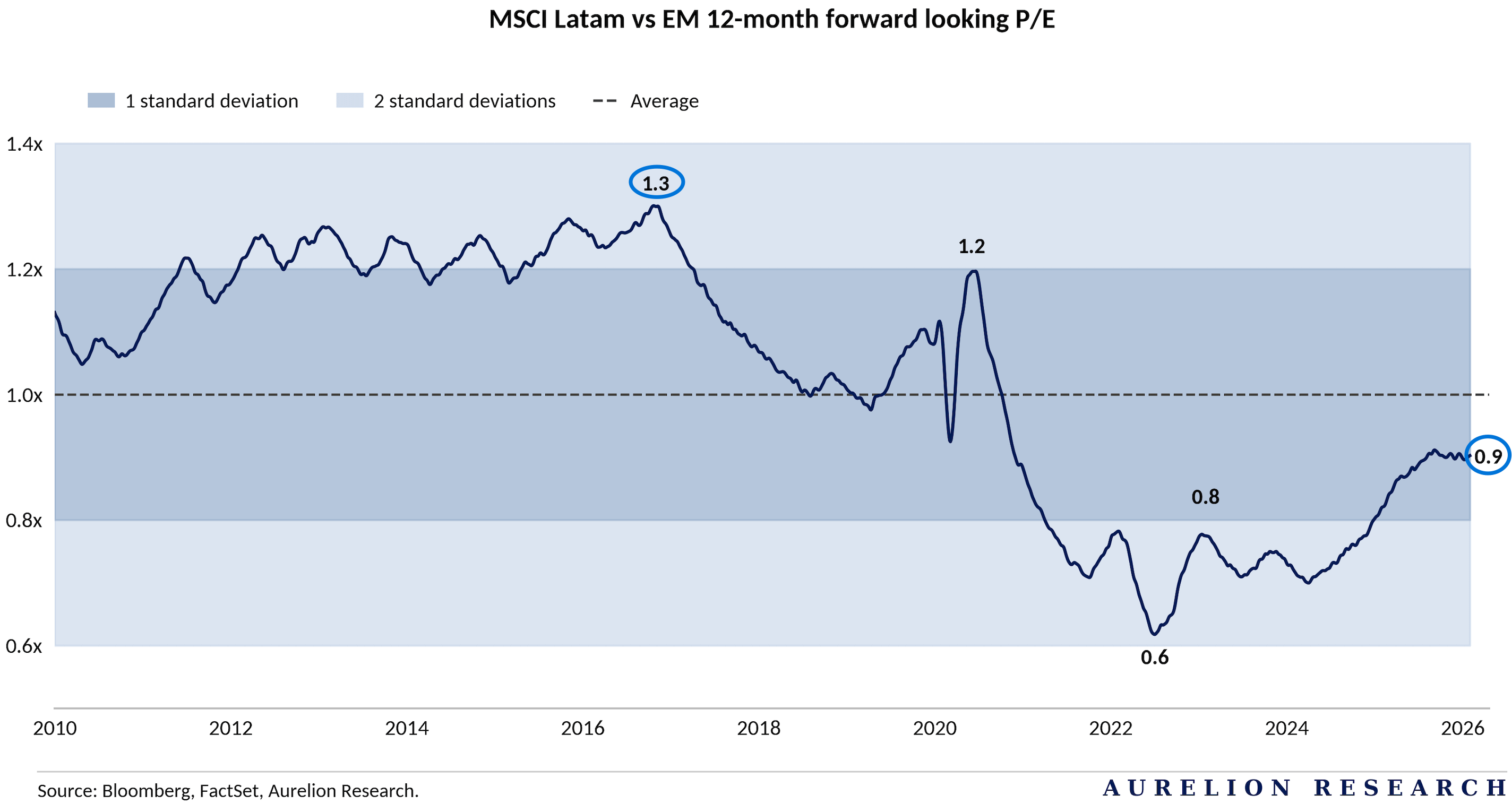

We believe the most important re-rating will happen relative to the broader Emerging Markets (EM), and that catch-up phase has already started. Right now, LatAm stocks trade at just 0.9x the valuation of their EM peers.

This leaves the region sitting half a standard deviation below its 20-year historical average. To put this in perspective, for the majority of the decade between 2010 and 2020, Latin America actually traded at a premium to the rest of the emerging world. That relative valuation peaked at 1.3x in 2017.

The market has priced the region at a steep discount since 2020, bottoming out at 0.6x in 2022. Simply returning to the historical average gives these markets a huge runway for growth, completely separate from the actual earnings the companies will generate.

2. Brazil Is Our Top Pick

Brazil enters a high-stakes phase as the 2026 presidential election looks set to be another binary contest. President Lula has confirmed his intention to run for reelection, focusing on continuity of his social and economic agenda.

On the other side, Flávio Bolsonaro has emerged as the main challenger from the right, officially carrying the mantle for his father’s movement.

While a few prominent governors are mentioned as middle-ground options, that part of the field remains too fragmented to call a definitive third-party threat. We believe this environment ensures that political polarization will remain a core theme for the market throughout the year.

The real issue is that the country is running out of room to borrow. Brazil’s debt has climbed to nearly 79% of GDP, up from 56% just ten years ago. The budget is incredibly tight because over 90% of government spending is mandatory, leaving leaders with almost no room to move money around.

To fix this, the government needs to make major changes to how it spends, like unlinking pensions from the minimum wage and cutting back on tax breaks. Brazil has passed some big reforms lately, like the VAT tax change in 2023, but the momentum is starting to feel hit or miss.

However, there is a clear path forward. Interest rates are likely at their peak, with the Selic rate currently sitting at a high 15% to keep prices under control. Since inflation is cooling off and the economy is slowing down, we expect a big cycle of rate cuts. We could see rates drop by as much as 4.5% by mid 2027. Inflation ended 2025 at 4.26%, which is right where it needs to be, though growth is expected to slow from 3% last year down to 2% by 2026.

Even though the stock market has done well recently, local investors are still mostly staying away. Domestic allocation to stocks is near all-time lows at 8%. Most people are still hiding out in fixed income because the interest rates are so high. To get people to move their money back into stocks and help companies raise fresh capital, interest rates have to come down and stay down. Until that happens, most of the action in the market is being driven by foreign investors, who currently make up 60% of the trading volume.

If Brazil successfully delivers on these reforms and navigates the next election, we believe the upside is significant. The MS bull case scenario points to ~121% total index upside by 2030.

In this Brazil section, we give credit in part to our friends at Morgan Stanley, who were the first to develop the bull case.

We remain optimistic, but also recognize a more cautious view. Even if conditions stay difficult, Brazil is still one of the few major markets expected to deliver positive returns of around ~20%. This comes from a mix of real earnings growth and a needed re-rating in how the market values these businesses. The path is there, it just depends on political will to follow through, and we are highly confident that it will happen.

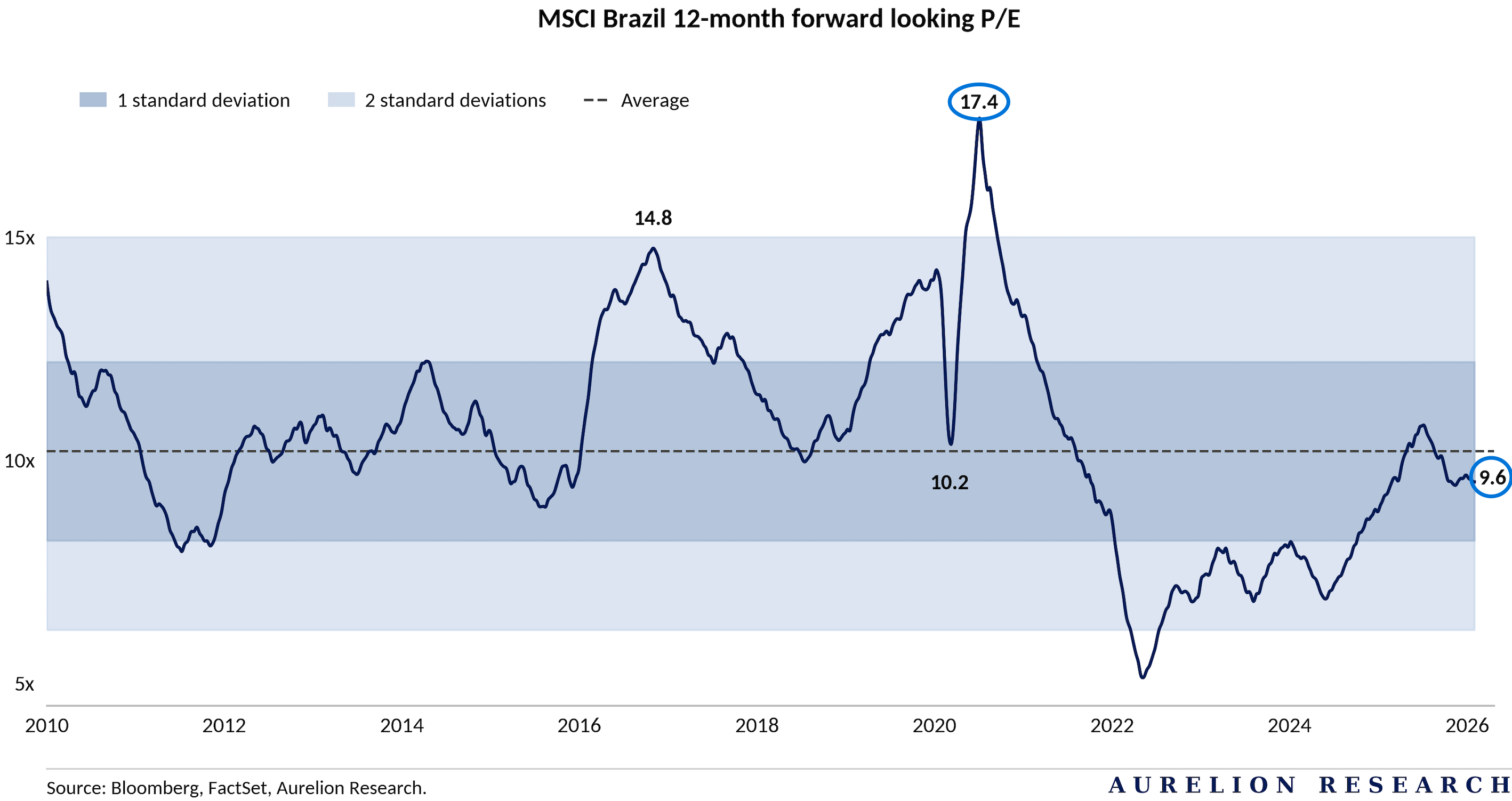

2.1 Brazil is Just Too Cheap

Brazil is a bargain. The market is currently trading at a forward P/E of 9.6x, which is sitting well below the historical average. For context, we have seen this same market climb as high as 17.4x when the narrative shifts.

Even with the recovery since 2022, valuations are still stuck near the bottom of their historical range. It feels like the market is still pricing Brazil as if it will never grow again, largely ignoring the potential for a strong re-rating as interest rates start to come down. When you combine these low entry levels with the earnings growth we see ahead, the setup for a meaningful rally is hard to ignore.

2.2 The Spring Bull Case

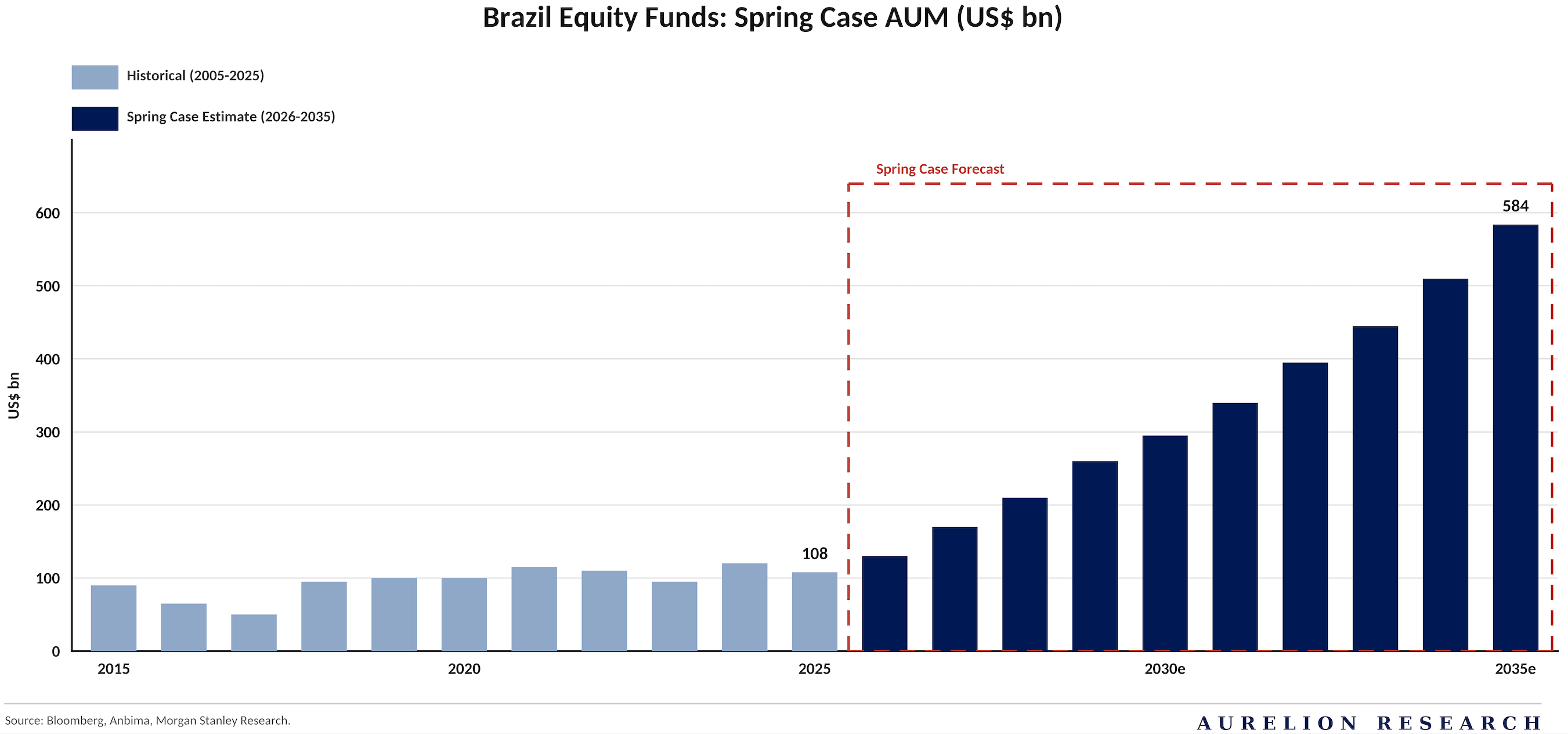

In its Spring bullish scenario, MS analysts believe domestic equity funds in Brazil could increase roughly sixfold by 2035. That implies a move from $100B to around $584B, or nearly ~18% annual growth over the next decade. This would represent a meaningful shift in local participation and would far exceed the ~8% growth seen between 2005 and 2025.

However, the macro thesis is not without challenges. We estimate that Brazil needs to find savings equivalent to 3.4% of GDP just to stop the debt from growing. Turning these fiscal dynamics around will be a long process that stretches well beyond the next five years. The depth and scale of the market on the other side of this transition would be massive.

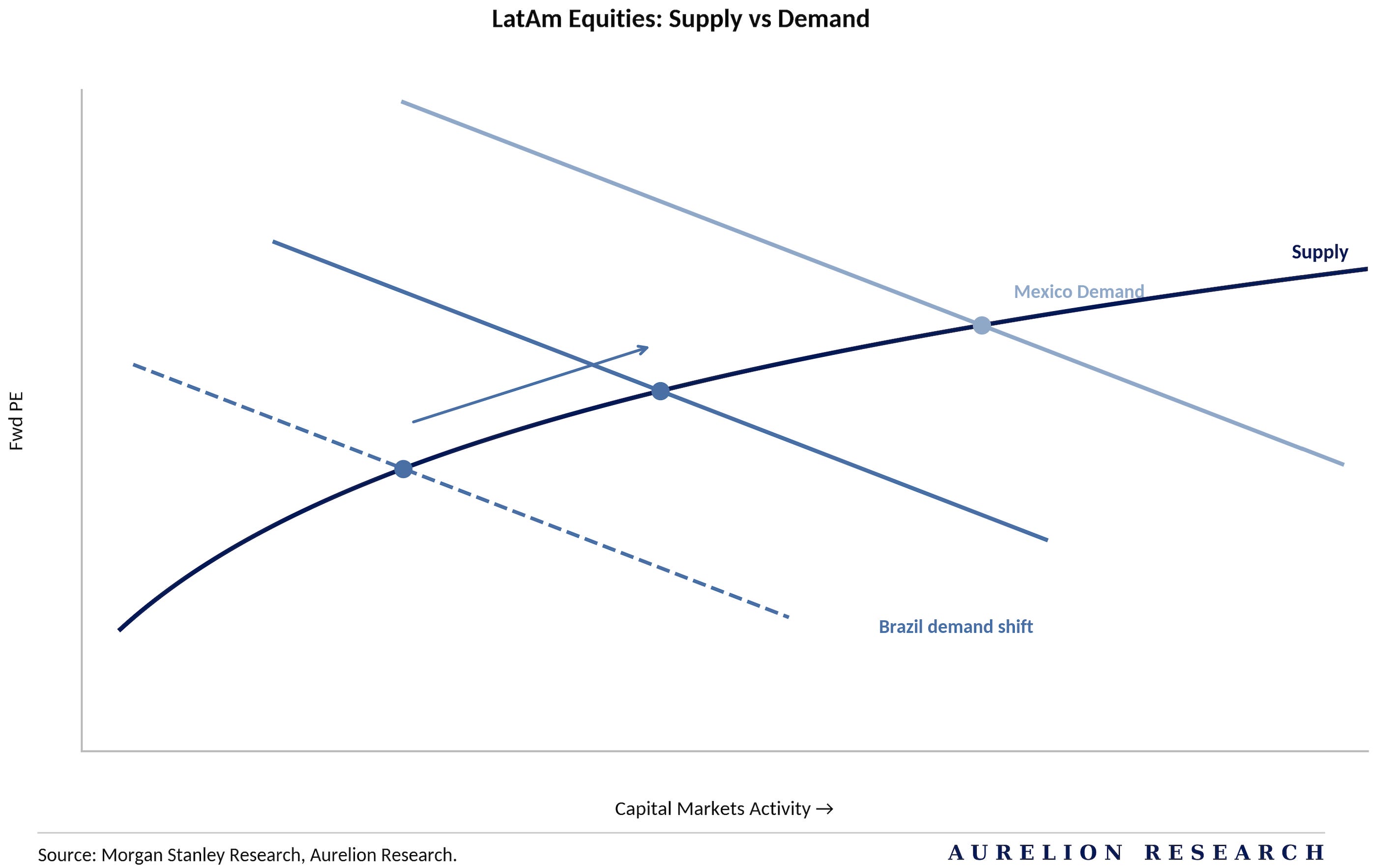

2.3 The Supply & Demand Squeeze

The setup suggests Brazil has significant further upside. MS supply curve for LatAm equities shows the market sitting on the steep, near-vertical part of the curve. At this point, even modest incremental demand can translate into outsized price moves as valuations re-rate and risk premiums compress.

Three catalysts are driving that demand. First is the rising probability of a policy shift that moves Brazil into a sustained bull case. Second, interest rates have peaked, and the start of the easing cycle in March is already forcing a rebalancing of local portfolios. Third is a broader rotation of global capital into emerging markets as investors look to diversify their holdings.

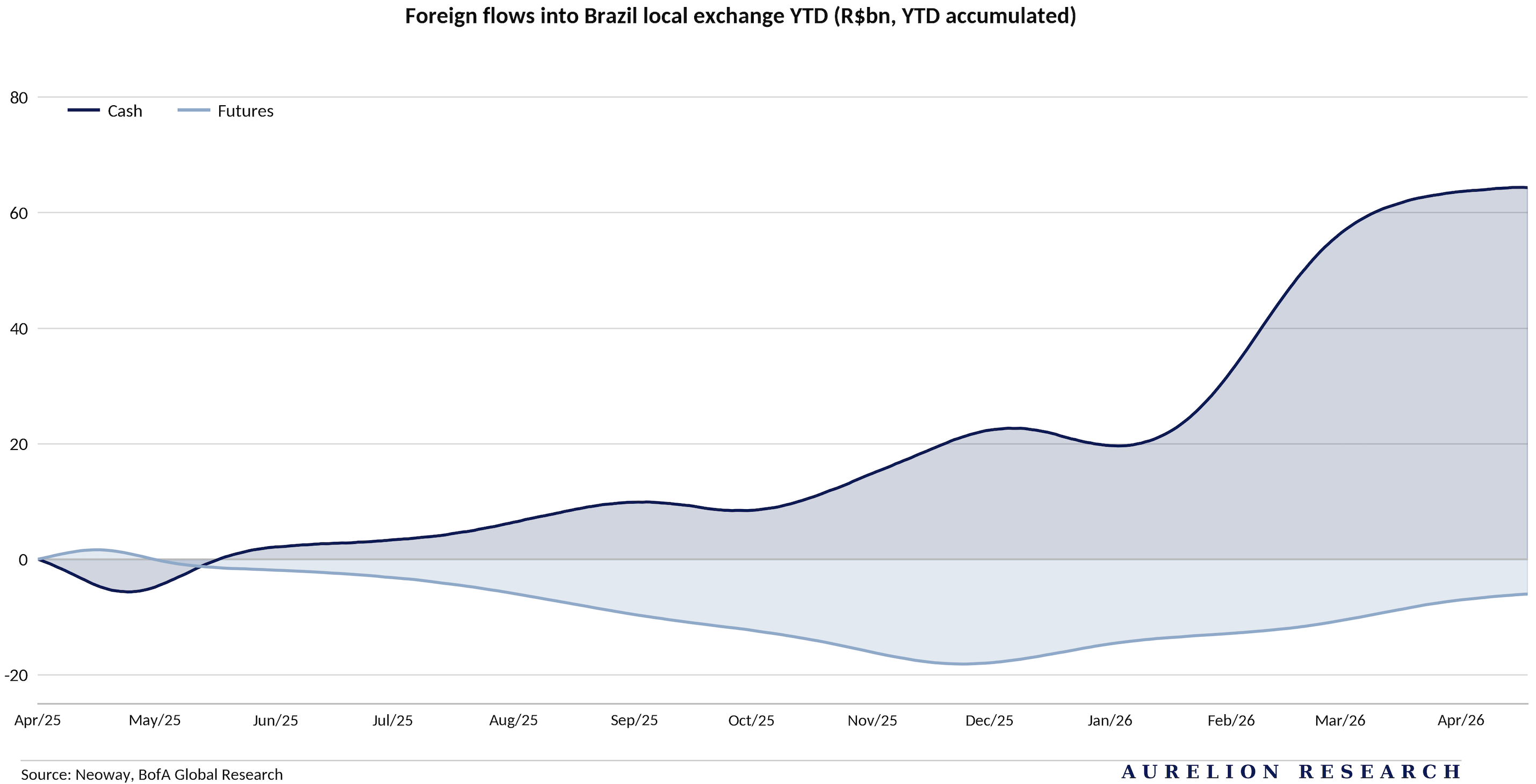

This trend is becoming a primary driver for the next leg of the rally. Foreign capital is flowing into the local exchange at a strong pace, with cash inflows reaching new highs into early 2026. While futures positioning is still adjusting, spot inflows signal that conviction is building. We think this is the type of demand shift that drives a rapid move up a steep supply curve.

When these inflows enter a market with limited free float, the result is a sharp repricing rather than a gradual climb. With domestic investors underweight for an extended period, they are now forced to chase the market higher, adding further momentum to the move. We believe this combination of foreign conviction and local rebalancing is creating a squeeze effect that reinforces the bull case for the rest of the decade.

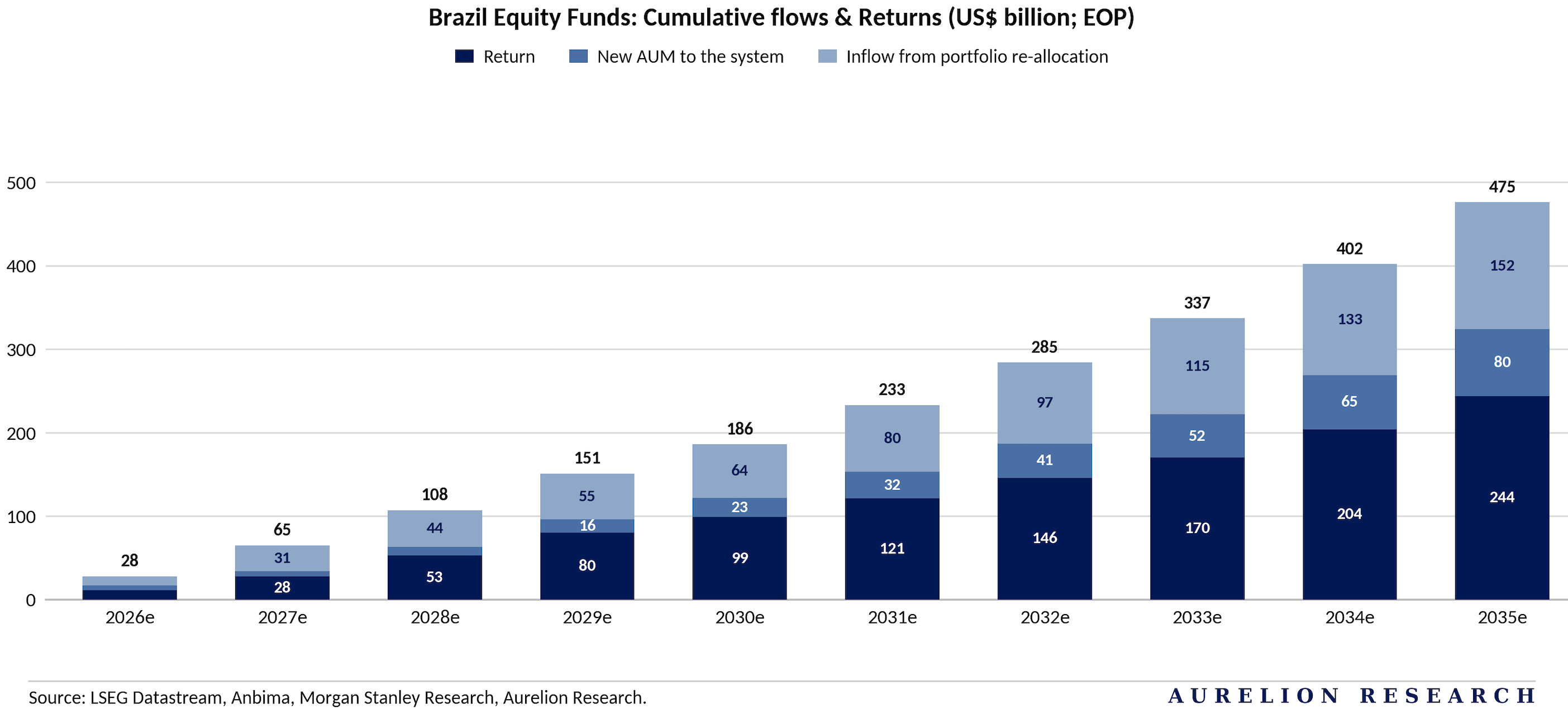

2.4 The Great Capital Rotation in Brazil

If the Spring bull case plays out as we expect, Morgan Stanley projects the overall Brazilian mutual fund industry will double its total asset base.

Forecasts show a jump from ~$1.7 trillion today to $3.2 trillion by 2035, representing a steady 8% annual growth rate. While that headline expansion is strong, the most powerful change will happen entirely beneath the surface.

The real story is a massive, forced reallocation of capital. For years, high policy rates have kept domestic capital parked in fixed income.

When double-digit returns are available risk-free, there is little incentive to allocate to equities. We are now seeing that dynamic start to shift. As fiscal discipline improves and the debt trajectory stabilizes, the central bank gains room to lower interest rates more aggressively.

This policy shift effectively closes the fixed income hiding place. As bond yields compress and safe returns dry up, local funds have no choice but to move up the risk curve to hit their return targets.

This creates a massive rotation of capital directly into public equities. Money that has been sitting comfortably on the sidelines for a decade will be forced to move, providing a massive domestic bid for Brazilian companies.

Driven by this rotation, equity assets are expected to grow at an aggressive 16% annual rate over the next decade. This pace completely doubles the 8% historical growth rate seen over the last twenty years.

Equity market growth is expected to outpace the broader fund industry, driven by this large internal transfer of capital. The domestic market is waking up, and the flow of money from bonds into stocks creates a powerful, sustained tailwind for the entire region.

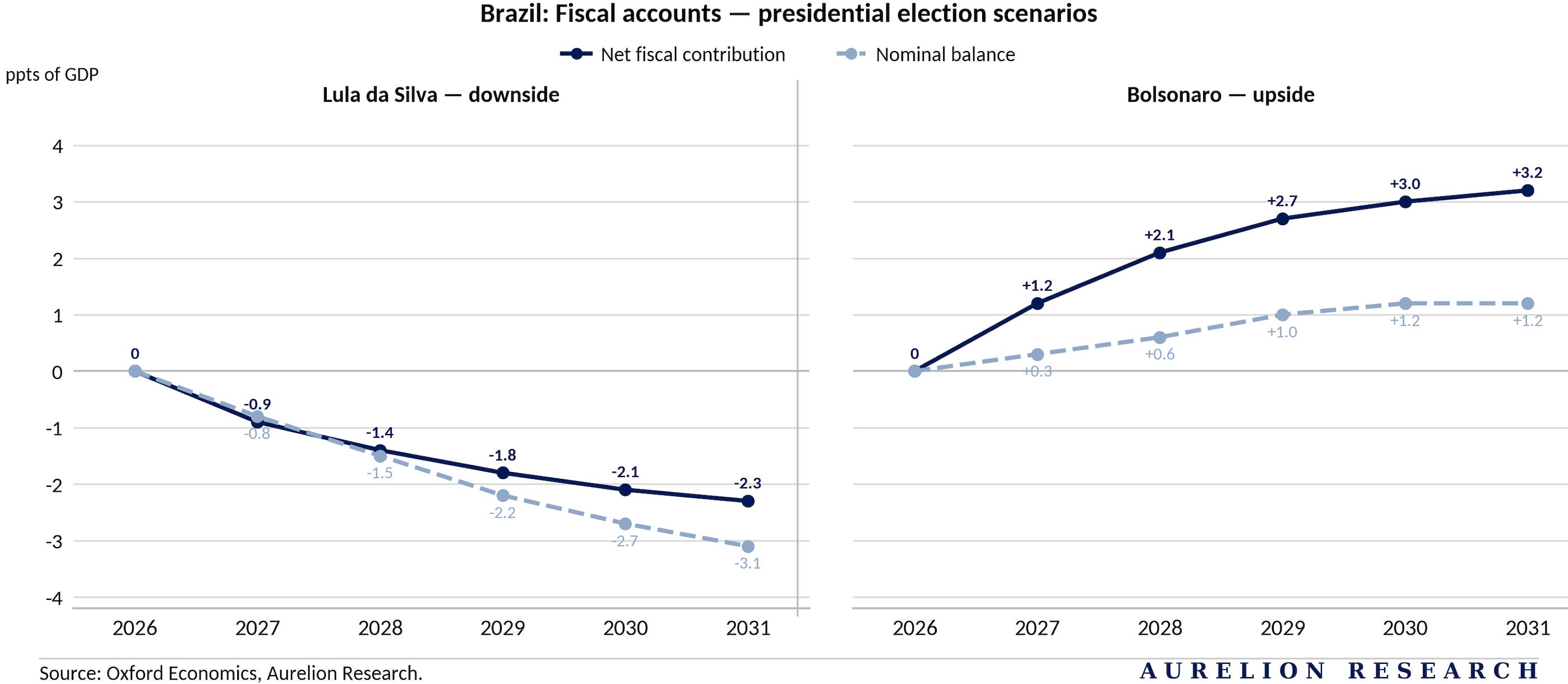

2.5 Brazil’s Fiscal & Inflation Outlook

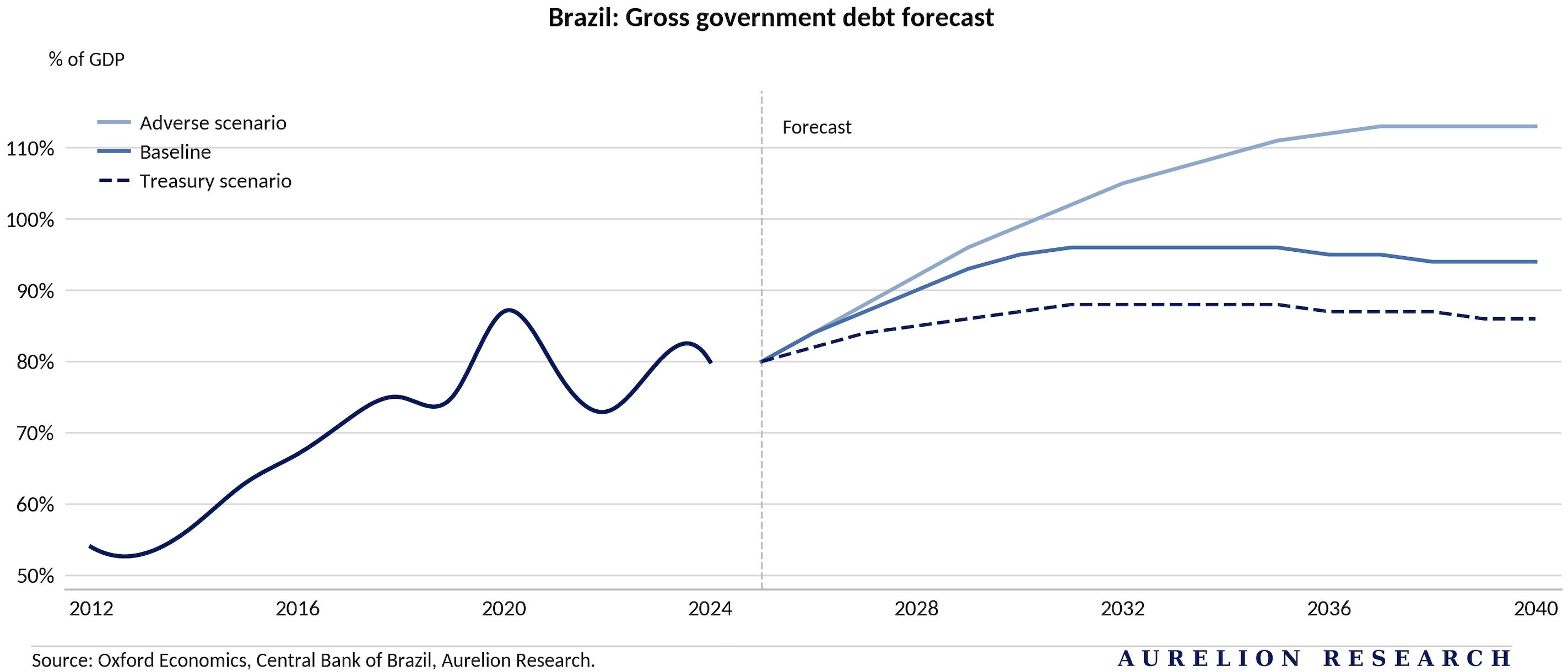

We see the upcoming election as a key turning point for Brazil’s fiscal outlook. On current projections, gross government debt continues rising and stabilizes near ~95% of GDP by the mid-2030s.

In an adverse scenario where spending accelerates, it moves above 110%. Under a tighter fiscal path consistent with Treasury assumptions, debt could peak just below 90% before gradually declining.

The path Brazil takes depends almost entirely on the 2026 presidential race. We are looking at two very different fiscal outcomes based on who wins.

If Luiz Inácio Lula da Silva secures reelection and maintains a looser fiscal stance, we see a clear downside case. Primary spending remains elevated, interest costs compound, and the nominal balance deteriorates.

By 2031, this path would add around 3% of GDP to the deficit, with rising interest payments weighing on activity and keeping the economy in a high-rate, low-investment environment. If Flávio Bolsonaro wins and implements a more fiscally disciplined agenda, the outcome flips. Tighter spending control and improved revenue dynamics drive a steady improvement in the fiscal position, moving the nominal balance into surplus by the end of the decade.

This implies an improvement of nearly ~3% of GDP versus the baseline by 2031. Lower primary spending combined with stronger fiscal credibility would also create room for a faster and deeper rate-cut cycle.

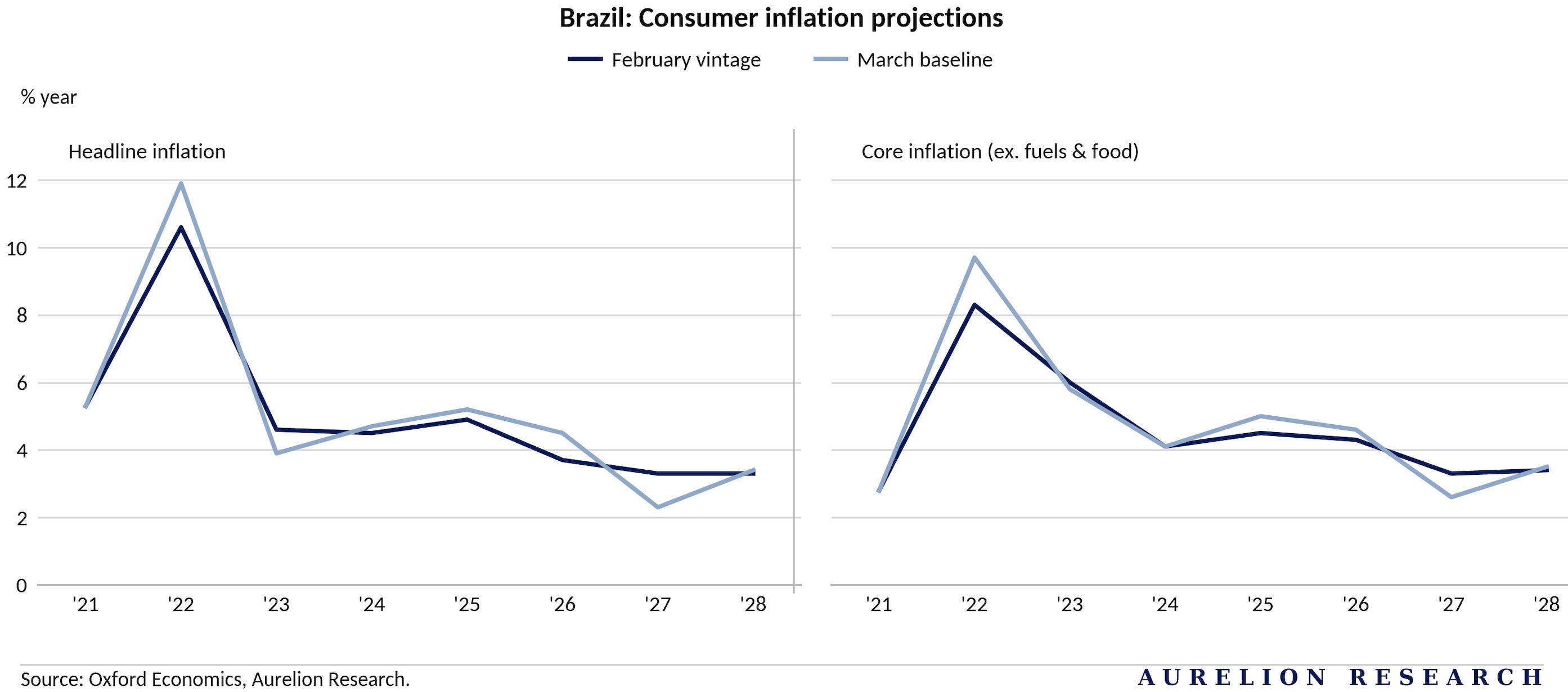

Fiscal policy is only one half of the equation. The other half is inflation, and here the outlook is actually much better than the consensus suggests.

While we respect the perspective from Oxford Economics, their inflation outlook feels overly cautious because it assumes oil rising toward $100 per barrel. We do not see that as a base case. In our view, oil remains on a softer trajectory and well below triple digit levels. That high oil assumption drives a highly negative transmission into their model, where higher fuel costs feed into core goods, pressure real wages, and keep rates elevated.

We see a different path for Brazil. If oil remains in its current range, the trajectory toward the 3% inflation target becomes significantly clearer.

That clearer trajectory in turn gives the central bank maximum room to continue cutting rates, lowering borrowing costs, supporting household spending, and reinforcing the investment cycle. A more grounded view on commodities shifts the narrative away from a sticky inflation regime and toward a sustained recovery.

Right now, the market is largely pricing in the baseline fiscal path and a cautious inflation outlook. This creates a massive setup. Any concrete shift toward the upside austerity scenario, combined with soft oil prices, will be the exact catalyst needed to trigger a massive bull run.

This political green light would force a broad upward rerating across Brazilian equities. When capital realizes the debt trajectory is actually under control and rates are heading lower, the rush to own these assets will be aggressive.

2.6 Resolving the Crowding Out Problem

Brazil is the deepest capital market in LatAm, but it is currently operating at an extreme point. Government spending and nominal deficits are near record highs, pushing debt and interest rates higher. As a result, the investment-to-GDP ratio is among the lowest in the region, while local equity ownership has fallen to cycle lows. These conditions contributed to the sharp currency selloff in late 2024, with valuations now compressed to historically low levels.

The main issue is a persistent crowding-out effect. With long-term rates between 12% and 14%, capital can double every six to seven years risk-free, making equities less competitive. Financing the state absorbs a large share of domestic savings, limiting liquidity for risk assets. This weighs on valuations, reduces market activity, and keeps the IPO window effectively closed. Capital markets are now operating at levels last seen during the 2014–2016 downturn.

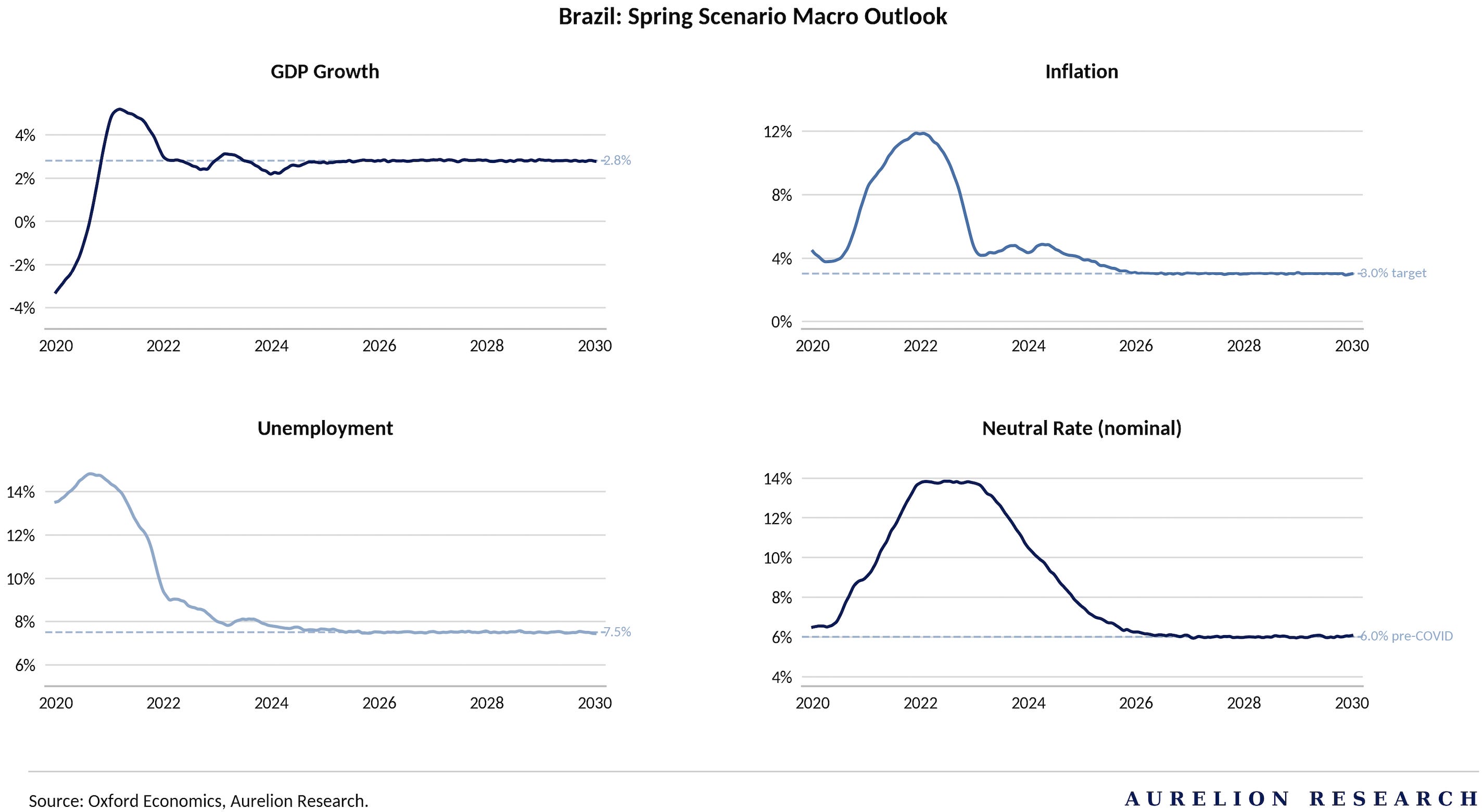

The Path to Rebalancing

The bull case depends on restoring fiscal discipline and allowing rates to normalize. In the Spring scenario, Brazil follows a credible adjustment path that rebuilds confidence and supports a recovery in private credit.

Capital allocation shifts away from government financing toward productive business investment. Under this rebalancing, the macro picture improves meaningfully. Long-term growth stabilizes near 2.8% annually, while inflation remains around the 3.0% target, reinforcing monetary credibility. This allows the neutral rate to return to pre-COVID levels, ~6.0% nominal and 3.0% real.

At the same time, the labor market remains resilient, with unemployment stabilizing near 7.5%. The combination of lower rates, stable inflation, and steady employment is the setup that unlocks the equity re-rating ahead.

2.7 Our Favorite Brazilian Stock

We are adding Embraer (NYSE: EMBJ) to the Aurelion Index.

Embraer: A Multi Decade Growth Story

Embraer is a company we have been watching for a while, and we feel like now is finally the right time to pull the trigger. We believe the stars are more aligned than ever, and the business has evolved into a much more balanced aerospace player with several high margin revenue streams.

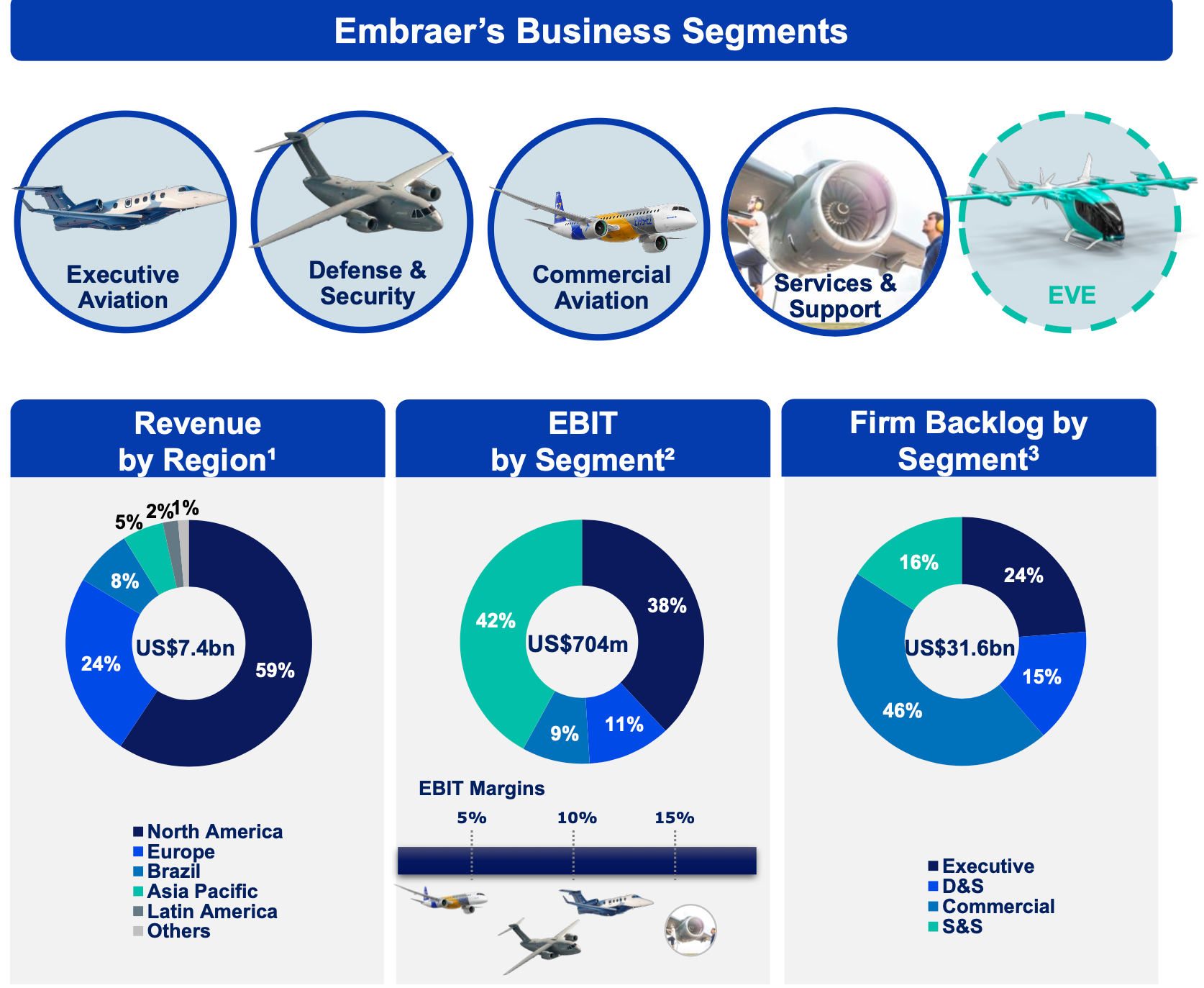

A Balanced Business Mix

They no longer rely solely on selling aircraft. The Services and Support division has become a major profit driver, accounting for 42% of total EBIT with margins around 15%. While Commercial Aviation makes up nearly half of the $31.6B backlog, it currently operates on tighter 5% margins, which gives it room to grow profits as it scales production. Meanwhile, the Executive Aviation segment is already performing well with 10% margins.

Geographically, it is very well positioned in the West. North America accounts for 59% of its $7.4B in annual revenue, followed by Europe at 24%. This footprint allows the company to capitalize on the massive demand for private jets and the need for airlines to replace aging regional fleets in the US.

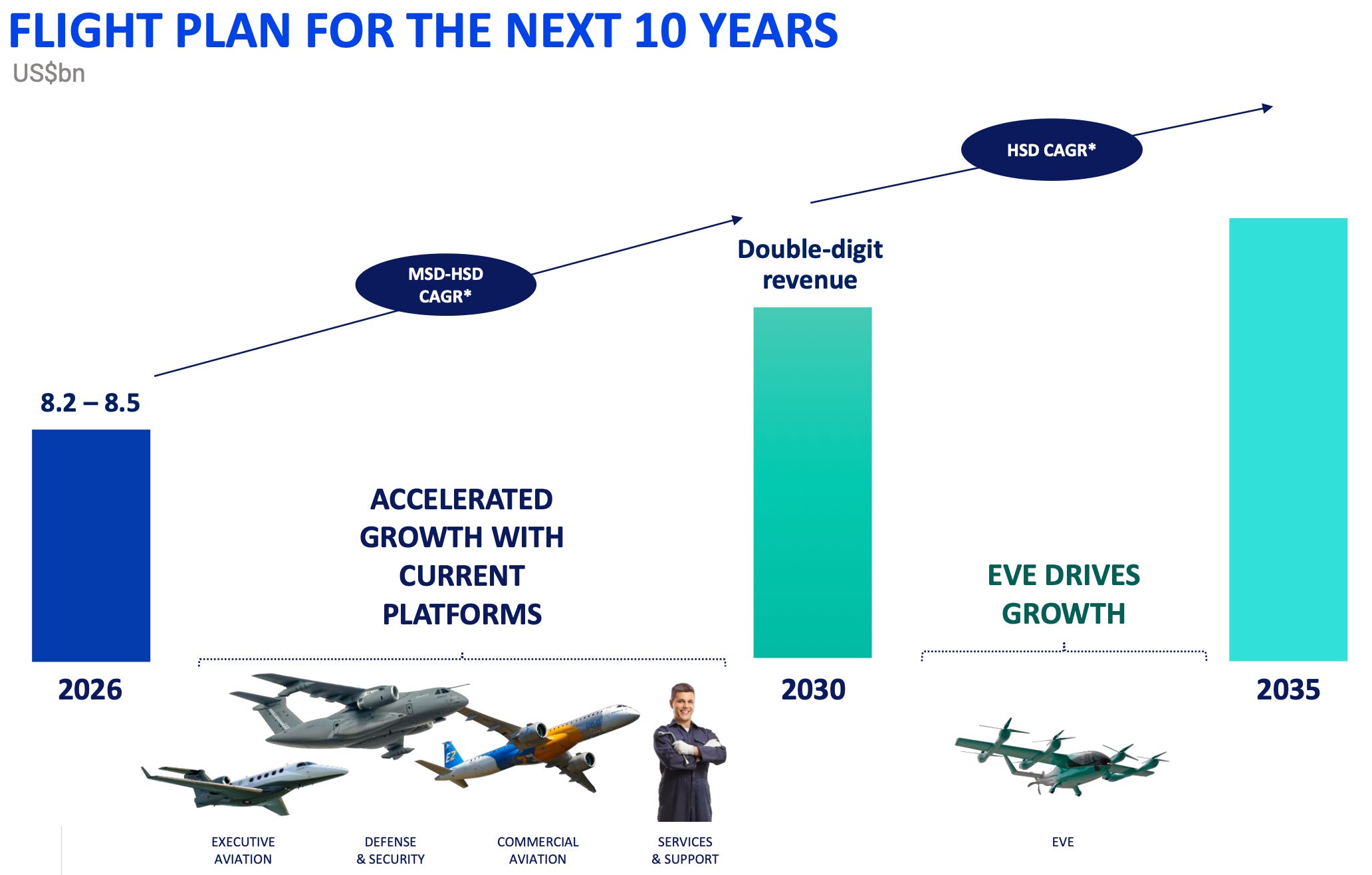

The Ten Year Roadmap

Embraer has a very clear plan for the next decade.

For 2026, revenue is expected to reach between $8.2B and $8.5B. This near term growth is being driven by its current successful platforms, including the E2 commercial jets and the Praetor executive line.

Looking further ahead, it expects to hit double digit revenue by 2030 as it accelerates deliveries of its current aircraft. By 2035, the focus shifts to Eve Air Mobility, its subsidiary developing electric vertical take off and landing (eVTOL) aircraft. Eve is expected to be the main driver of growth in the next decade as urban air travel takes off. With a huge $31.6B backlog and a high margin services business to lean on, it is moving from a period of recovery into a decade of serious expansion. We find the setup very compelling.

Financial Performance & Cash Generation

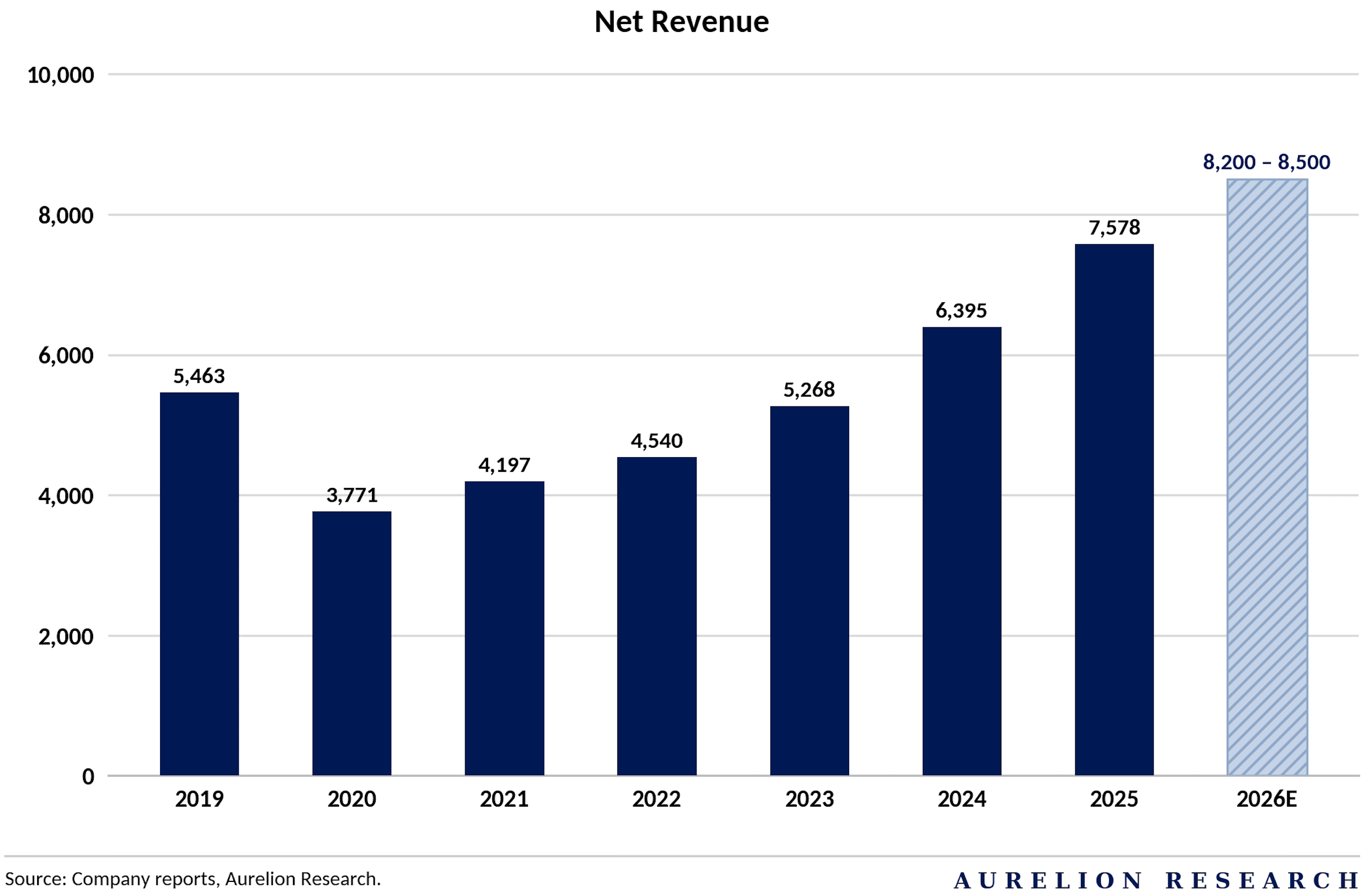

The company’s financial recovery is clearly visible in the steady climb of revenue over the last few years. After hitting a low point in 2020 at $3.77B, sales have grown every year to reach $7.57B in 2025.

For 2026, EMBJ expects this momentum to continue with a target range between $8.2B and $8.5B. This growth shows a business that has moved past its recent struggles and is now operating at a much larger scale.

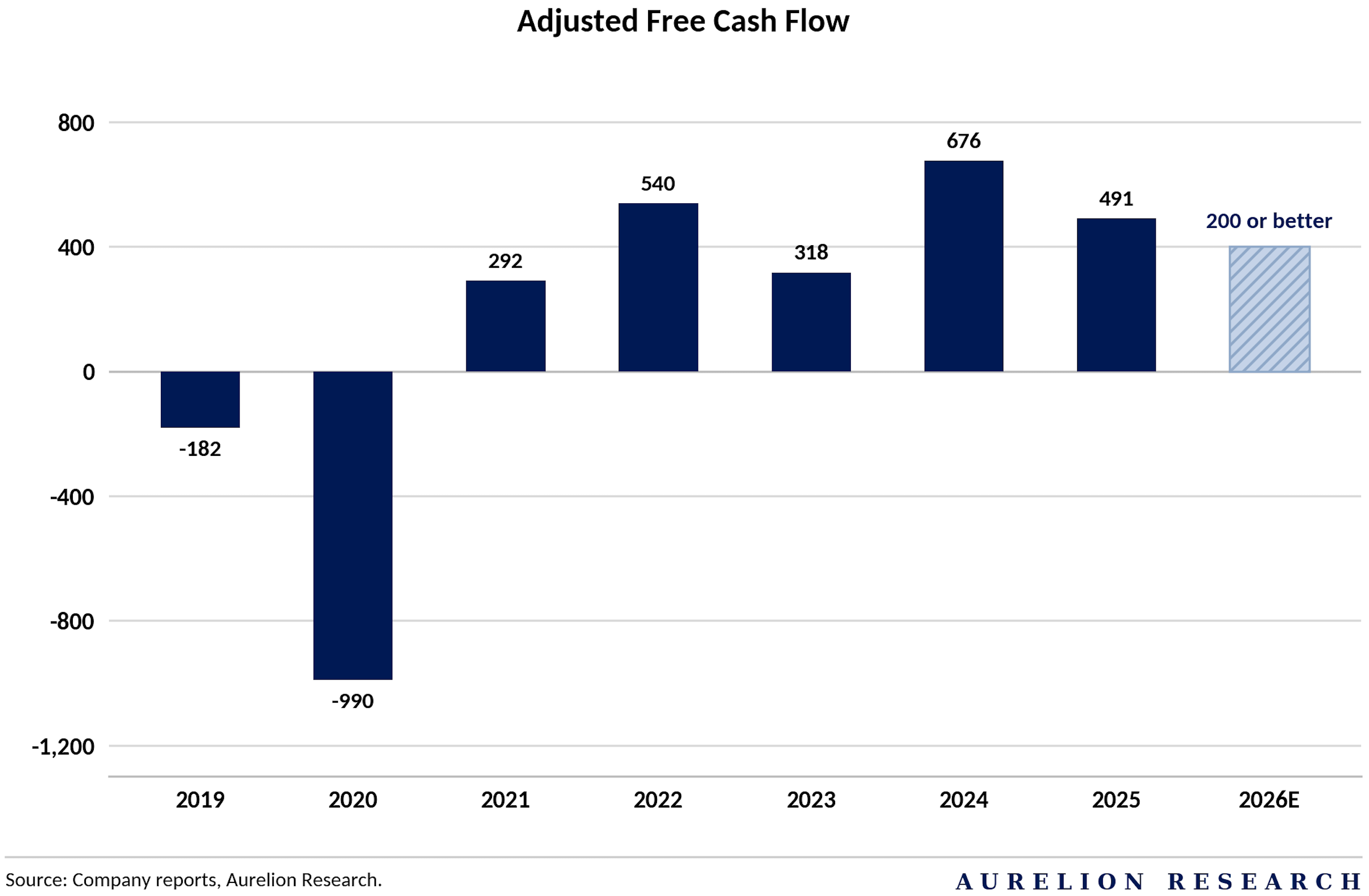

Equally important is the company ability to generate cash. After heavy losses in 2019 and 2020, the business has remained cash flow positive for five straight years. Even with elevated spending to ramp up production, it generated $491M in free cash flow last year. For 2026, management expects at least $200M in free cash flow. While conservative, this allows the company to fund growth and support its $31.6B backlog without adding debt.

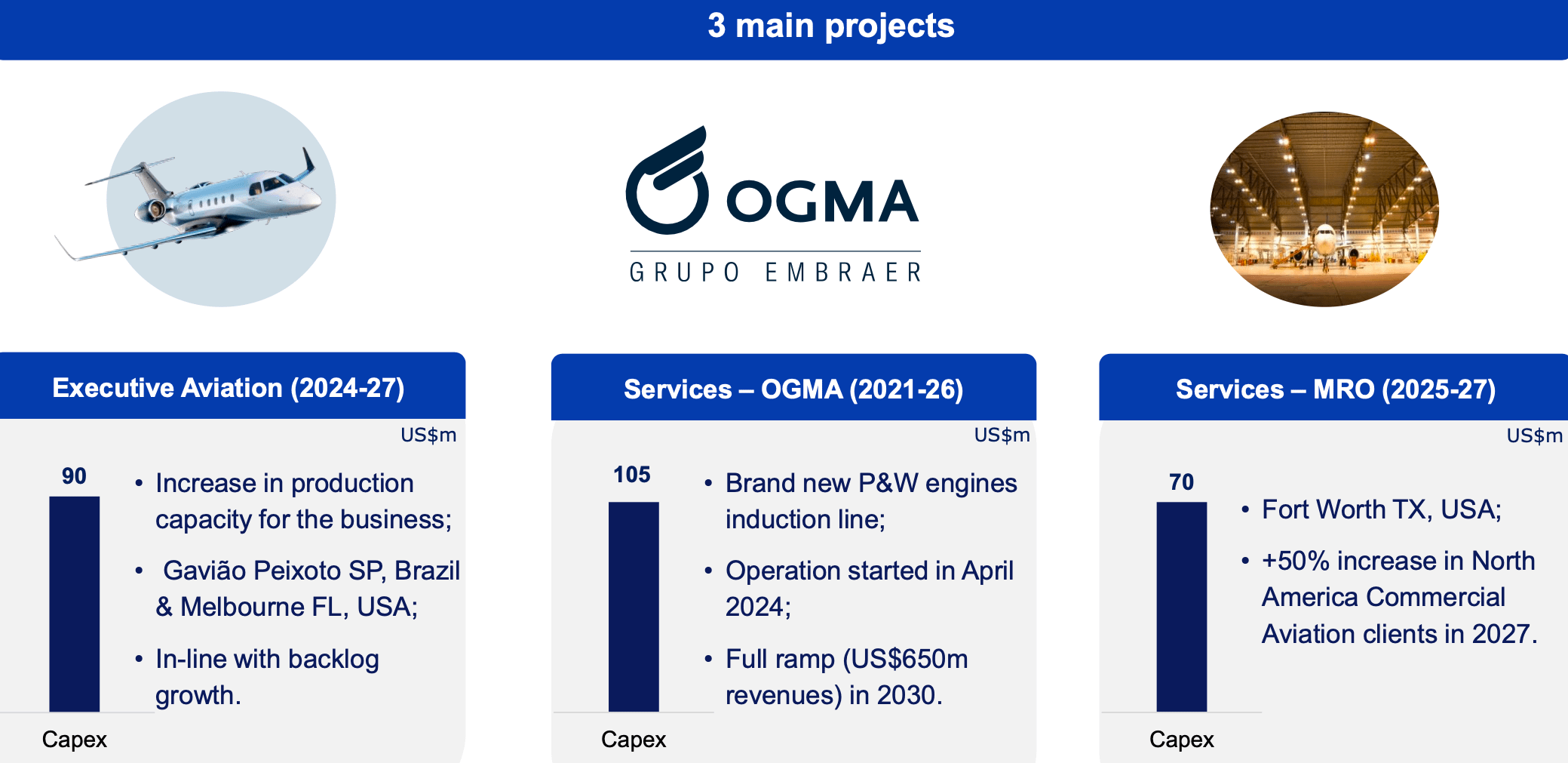

Strategic Backlog & Expansion Projects

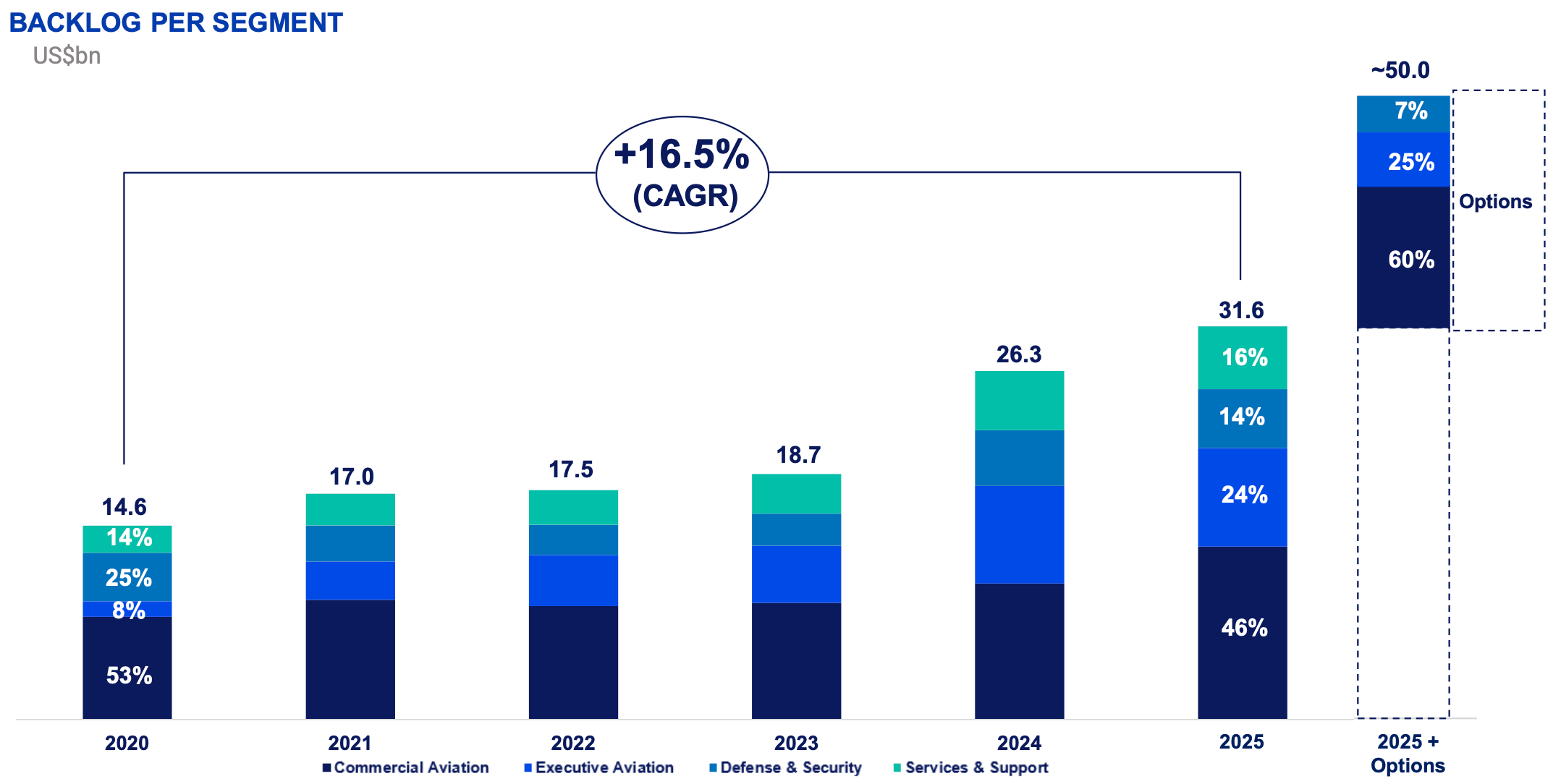

EMBJ’s order backlog has grown at a 16.5% CAGR since 2020, reaching $31.6B in 2025. It could approach $50B when including existing purchase options.

The backlog is also becoming more diversified. While commercial aviation remains the largest segment, we believe growth in executive aviation and defence adds a more stable, long-term revenue base.

To convert this massive backlog into actual sales, the Brazilian company is focusing its capital spending on three major expansion projects.

Executive Aviation Production. A $90M investment is currently underway to increase production capacity in both Brazil and Melbourne, Florida. This expansion is designed to match the rising demand for private jets and ensure the company can meet its delivery targets through 2027.

Services: OGMA Engine Line. Through its OGMA subsidiary, it has invested $105M in a brand new Pratt & Whitney engine maintenance line. This facility began operations in April 2024 and is expected to reach full ramp up by 2030, contributing roughly $650M in annual revenue as it services the global fleet.

Services: North American MRO. It is also investing $70M to expand its Maintenance, Repair, and Overhaul (MRO) capabilities in Fort Worth, Texas. This project aims to support a 50% increase in NA commercial aviation clients by 2027. By positioning these services close to its largest customer base, it is securing high margin, recurring income for years to come.

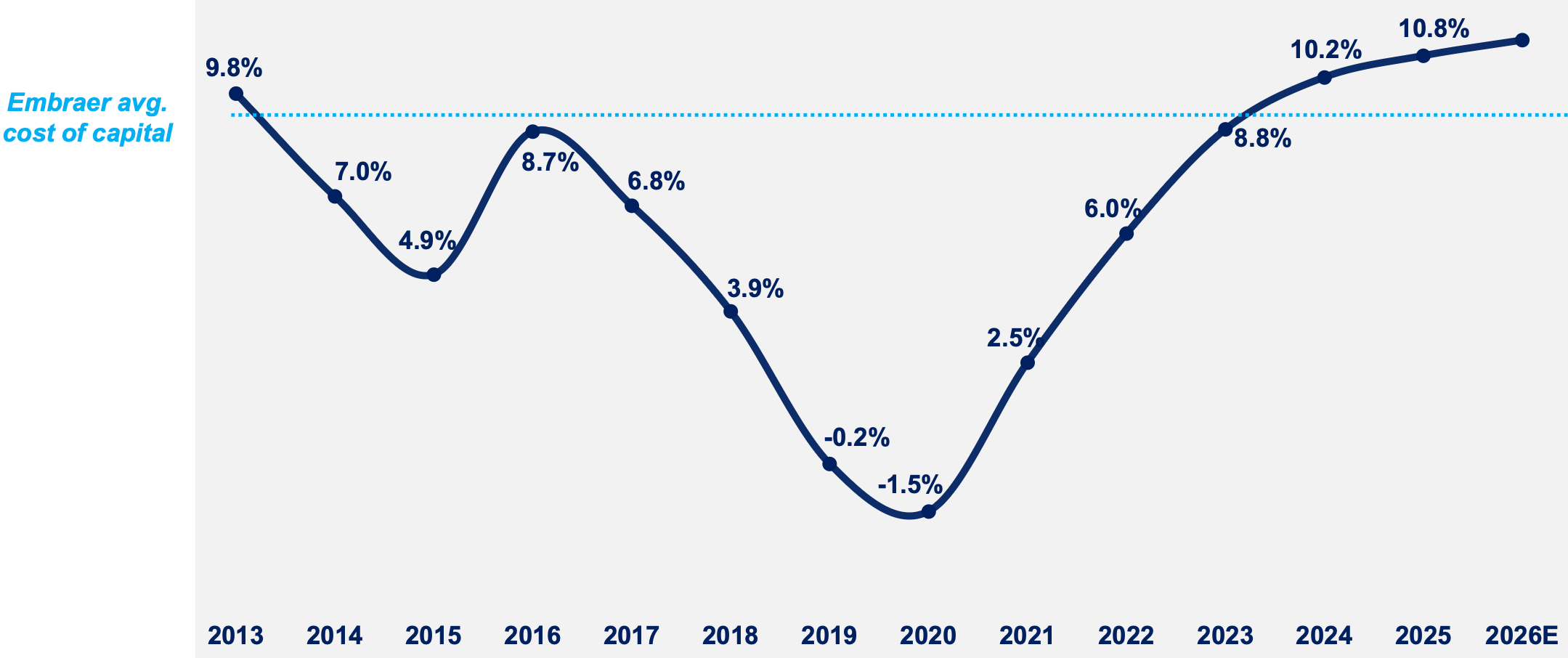

Improving Returns & Market Consensus

The company is now consistently creating value for its shareholders by keeping its Return on Invested Capital (ROIC) well above its cost of capital.

After a difficult period with negative returns in 2020, the business has staged a strong recovery. By 2024, ROIC rose to 10.2% and is expected to reach 10.8% by 2026. We see this as confirmation that Embraer is not only growing, but also becoming more efficient at turning investments into profit.

Return on Invested Capital (ROIC)

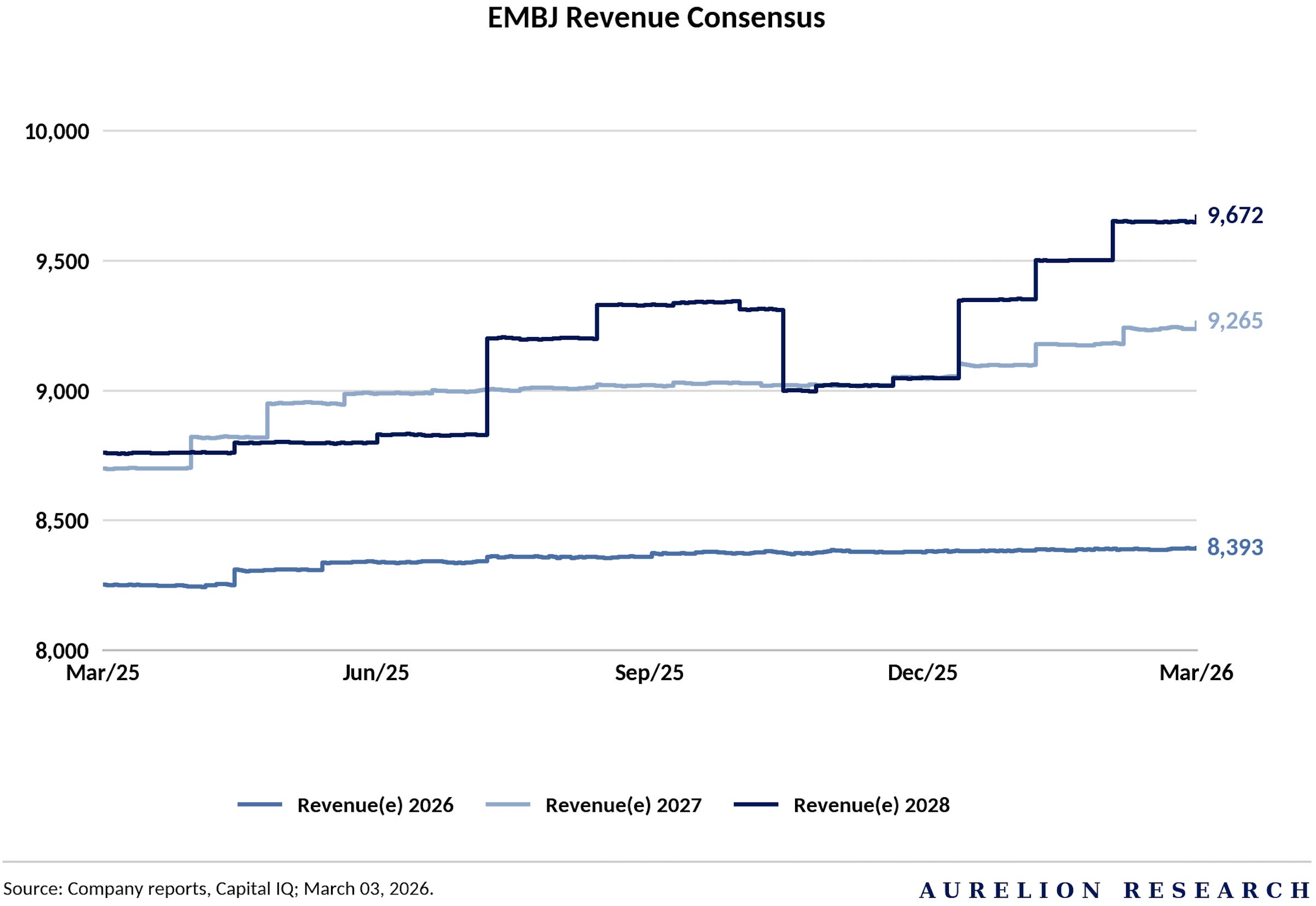

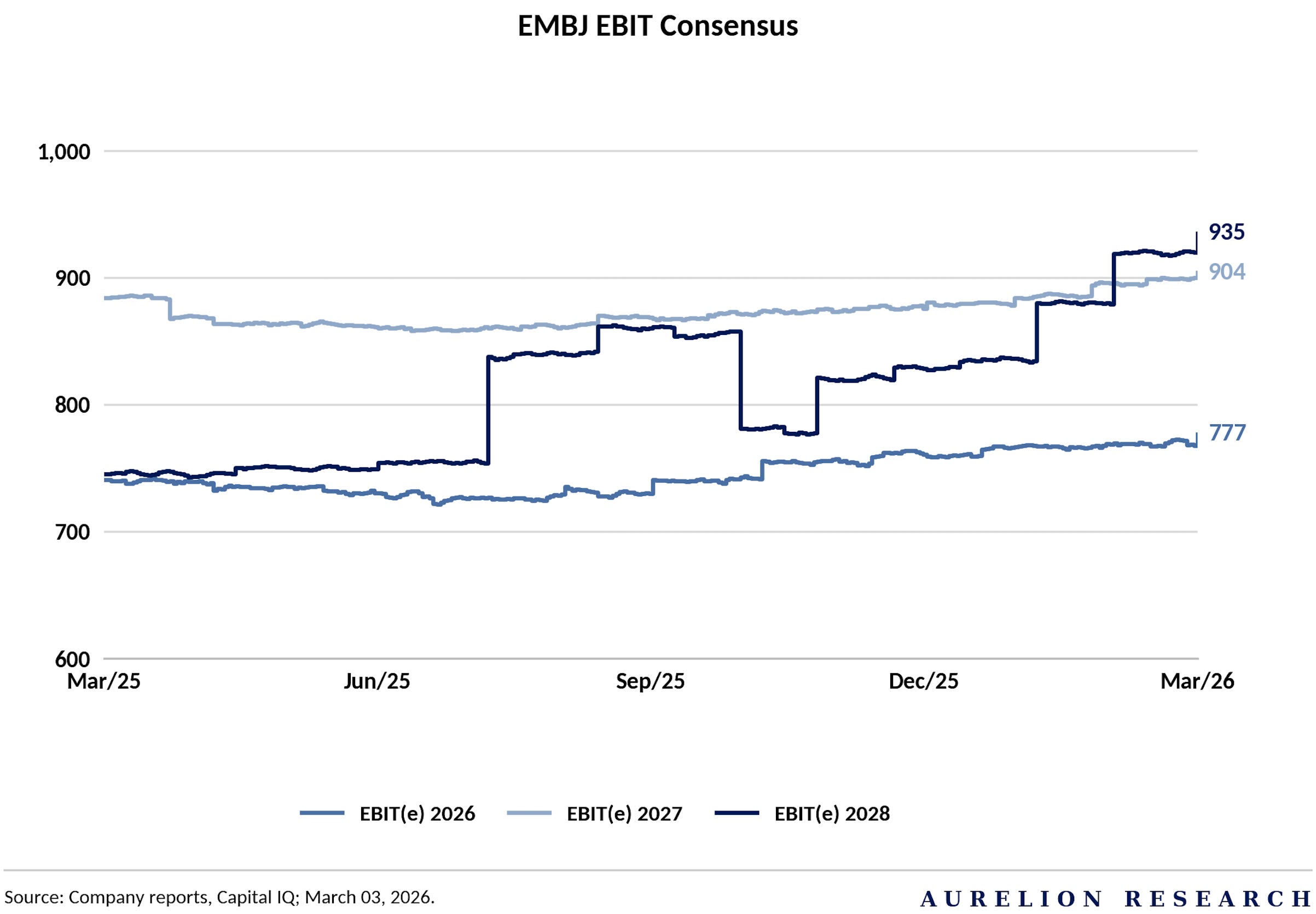

Market expectations for the business are also on the rise.

Analysts have steadily increased their forecasts for both revenue and earnings through 2028. Revenue consensus for 2026 sits at ~$8.39B, with projections climbing toward $9.67B by 2028.

Similarly, EBIT forecasts show a strong upward trajectory, with earnings expected to grow from $777M in 2026 to $935M by 2028. We believe these rising estimates reflect a growing confidence in the company’s ability to execute its massive backlog and maintain its current momentum.

Financial Projections & Valuation

Our estimates reflect a business entering a period of steady, profitable expansion. We project total sales to grow from $8.4B in 2026 to over $13B by 2030, maintaining a low double-digit growth rate throughout the decade. This top-line growth is accompanied by expanding margins, with Adj. EBITDA margins expected to climb from 12.3% to nearly 15% as it benefits from its high-margin services business and more efficient aircraft production.

Historical Context

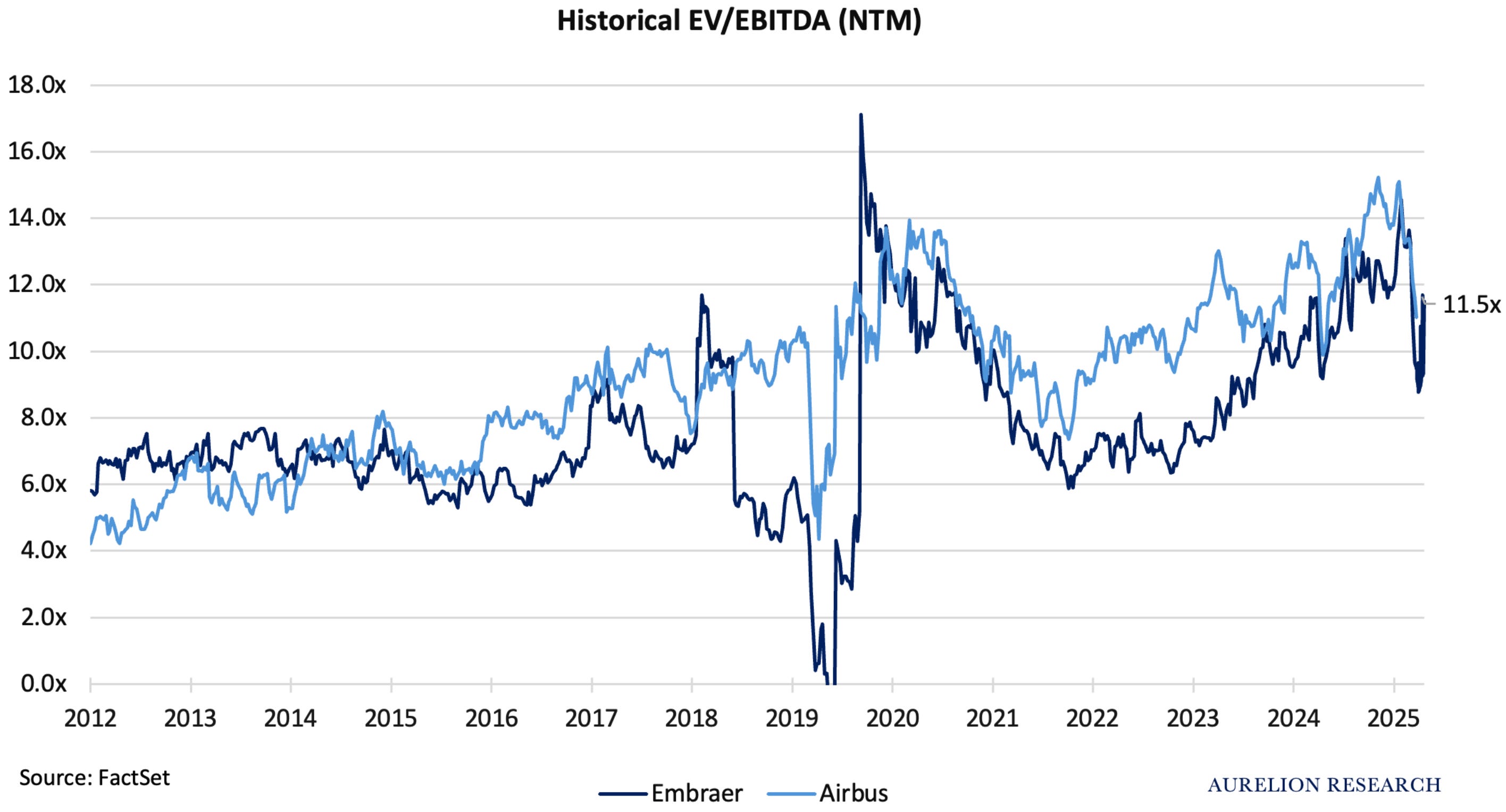

Looking at the historical EV/EBITDA multiples, the company currently trades at 11.5x, which is in line with its long-term average and closely tracks its peer, Airbus. After the extreme volatility of 2019-2020, the valuation has stabilized. We believe this multiple is well-supported by its improving Return on Invested Capital (ROIC) and its clear path to reaching $13B in revenue by 2030.

Key Valuation Assumptions

Predictable Revenue: The confirmed $31.6B backlog provides high visibility for continued sales growth over the next several years.

Margin Expansion: We expect margins to continue scaling, following a similar trajectory to Airbus as production efficiency improves.

Cash Flow Strategy: While heavy capital investment will impact free cash flow conversion in the near term, the company has already successfully paid down its debt.

Shareholder Returns: With a clean balance sheet, cash generated after capital investments is expected to be directed toward share buybacks.

This operational strength translates into significant cash generation. Free Cash Flow is projected to rise steadily, reaching nearly $1B annually by 2030. This strong cash position allows the company to maintain a very clean balance sheet, with net debt expected to stay below $300M.

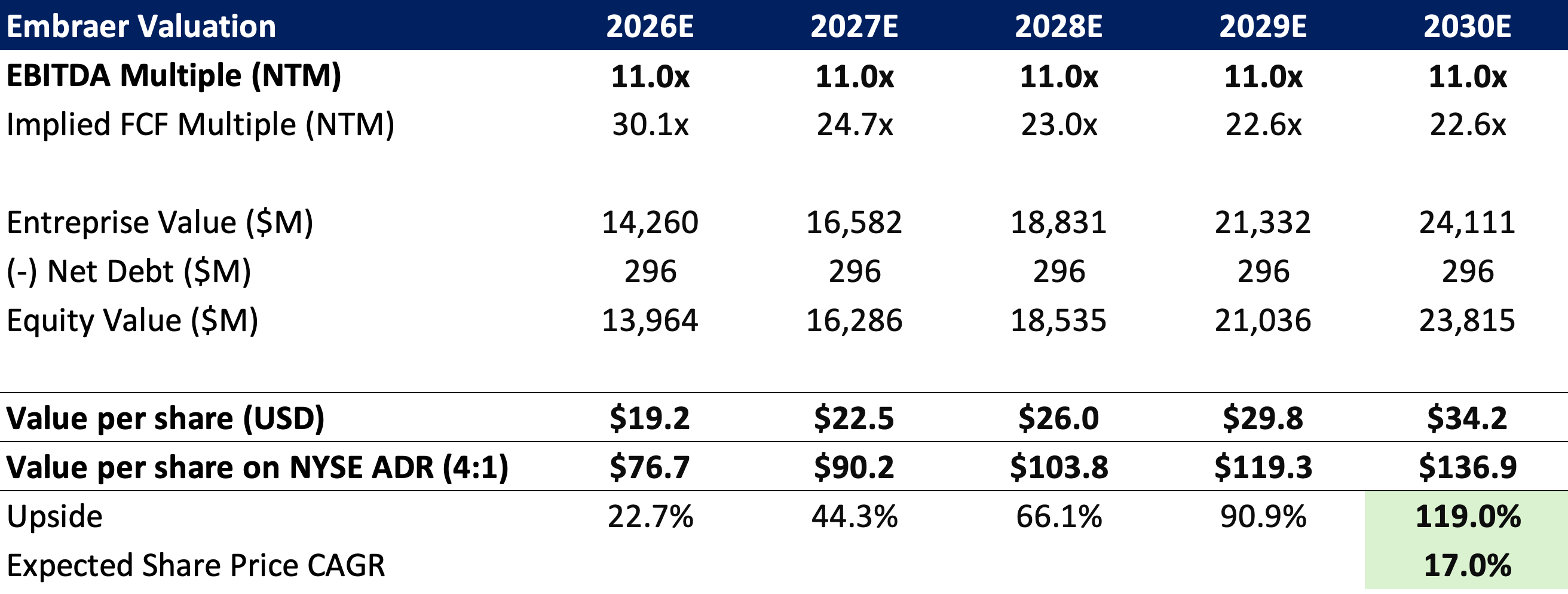

Quick technicality: Embraer trades on the NYSE at a 4:1 ratio relative to its shares on the Brazilian stock exchange. Therefore, to arrive at a comparable price target, we have multiplied our derived per-share value by 4 to get $76.7 in 2026. If you want to buy it on the Brazilian stock exchange, our price target would also need to be converted using the current BRL/USD exchange rate, which is around 4.98. This results in a price target of approximately R$95.

Based on these projections, we see a highly compelling valuation.

Using an 11.0x EBITDA multiple, our model points to a value per share of $19.2 in 2026, scaling to $34.2 by 2030. This represents a total upside of 163.8% over the next four years, or an expected share price CAGR of 21.4%.

We believe this more than justifies our bullish stance on the stock as it delivers on its long term flight plan.

2.8 Perspectives on Brazilian Cost of Capital

A great way to look at the Brazilian market is through different tiers of capital. Morgan Stanley compares this to how TV rights work in European football. While there are hundreds of clubs, the few that make it into the Champions League get a disproportionate share of the money.

The “Champions League” of Capital

In LatAm, getting into the MSCI index is like winning those TV rights.

It opens the door to a global audience and an investor base that can diversify risk much more easily. Companies that operate globally and earn in hard currency benefit from a lower cost of capital because they can lean on the US risk-free rate and stay insulated from local volatility.

On the other hand, domestic mid and small-cap companies are in a different league. They are mostly funded by local players who are stuck with a 14% Brazilian risk-free rate plus a high risk premium. These local investors have fewer ways to diversify, so they see risk through a much narrower lens and demand much higher returns to compensate.

MS strategy has been to identify stocks that are transitioning from local players into the global “Champions League” category. Axia (AXIA3) is a clear example of this migration. In 2022, its ownership was 91% local. Today, that has fallen to 72% as foreign investors have stepped in.

The growth of AI is the main driver here. It has turned the utility sector into a global play, allowing companies like Axia to diversify domestic risks better than any local investor could. In just three years, Axia’s P/E has jumped from 4x to 13x. This has closed the valuation gap with its US peer, Sempra, from 70% in 2023 to just 30% today.

We are not saying this is necessarily the best way to frame it, but we found it interesting to highlight, as we always like to look at how different investors are positioning across markets.

2.9 Our Final Take on Brazil

Brazil remains the heavyweight of the region, offering a mix of steady growth and attractive valuations. While the economy is expected to slow slightly toward ~1.6% growth, its scale and leadership in global commodities make it a core allocation in any Latin American portfolio.

The story is mainly about interest rates and fiscal policy. The central bank has begun cutting rates from a 15% peak, but they remain elevated to contain inflation. At the same time, public debt sits near 80% of GDP, with markets waiting for greater fiscal clarity before increasing exposure.

The overall foundation, however, remains solid.

Brazilian equities currently trade at a steep discount to historical levels. There is value in major iron ore and oil producers, which generate strong cash flows regardless of domestic conditions. Large banks remain resilient in a high-rate environment, while quality retailers should benefit as rates decline and consumption improves.

Brazil does not offer the near-term upside of Argentina, but it provides greater stability and liquidity. It acts as the region’s main stabilizer, and current valuations offer an attractive entry point for long-term positioning.

3. The Argentina Experiment

Argentina provides a fascinating look at a country attempting to force a massive economic shift. The political changes and deep fiscal reforms happening under Javier Milei represent the most significant transformation Latin America has seen in nearly thirty years. However, for this narrative to hold up over time, the country desperately needs to kick off a new cycle driven entirely by capital deployment.

The primary challenge is incredibly simple. Argentina just needs cash. The local pension fund system is a shadow of its former self, and the mutual fund industry is virtually nonexistent. While the everyday retail crowd is active, you cannot build a reliable long term market on that kind of volatility. Right now, locals heavily prefer trading crypto or simply hoarding US dollars. Neither of those habits creates a foundation for a healthy domestic market.

Because of this dynamic, we believe Argentina stands apart from the rest of the region. It is pursuing one of the most aggressive growth agendas, while remaining heavily dependent on external financing to sustain it. This creates a fragile setup, as foreign capital tends to exit quickly at the first sign of instability. Developing a domestic capital market grounded in credible governance is the most urgent and complex challenge ahead.

Everything comes down to a complete lack of trust in the local monetary system. Rebuilding that confidence is the only way forward. Whether the Milei administration pursues this through a truly independent central bank or full dollarization, both paths are highly complex and would require significant constitutional changes. That is the key test we are watching.

Political Momentum and the 2026 Legislative Push

Argentina enters 2026 with a highly clarified political landscape and a strengthened reform mandate following the October 2025 midterm elections.

The vote confirmed broad public support for President Milei, with his coalition securing over one third of the seats in both chambers. Its share rose from nearly 28% to 42% in the lower house and from 18% to 33% in the Senate, materially reducing impeachment risk and improving governability.

Since the midterms, Congress has already approved the 2026 national budget, a labor reform aimed at lowering costs and encouraging formal job creation, and the Law of Fiscal Innocence Presumption, which facilitates the return of US dollars into the formal financial system.

The momentum is accelerating. In his March address to Congress, Milei announced a plan to submit 9 consecutive rounds of ten bill packages every month through 2026. This aggressive agenda targets a complete overhaul of the Penal Code, alongside comprehensive tax and electoral reforms, aiming to fully modernize institutions and reorganize the state.

The Macroeconomic Turnaround

The policy objectives for 2026 are clear.

The goal is to establish a baseline for sustainable growth, regain normal market access, protect the disinflation trend, and maintain fiscal discipline. The central bank is focused on rebuilding reserves and remonetizing the economy, targeting between $10B and $17B in purchases.

The underlying macro conditions are improving.

Fiscal accounts are in surplus, and GDP growth for 2026 is projected at ~3.5%. Inflation has converged to ~3% per month, with further disinflation expected through the second half of the year.

After declining 29% in 2025, the sharpest drop in the region, the peso has stabilized since the midterms and has recently appreciated alongside reserve accumulation. With IMF support and a clearer FX framework, Argentina is positioned to regain access to international capital markets this year.

The Valuation Disconnect & Upcoming Catalysts

It is not too late to lean into the Argentina trade. Confidence has surged since October, pushing country risk down dramatically.

The EMBI spread has compressed to ~6.0%, a massive recovery from the 27.0% seen in late 2023. With government approval holding above 40%, the combination of a fiscal surplus, lower risk premiums, and ongoing reforms will support a deep earnings recovery and significant valuation upside.

Currently, a glaring performance gap exists between equities and bonds. While sovereign fixed income has rallied hard, pushing bonds to ~70 to 80 cents on the dollar, MSCI Argentina remains practically flat in USD terms, trailing its Latin American peers. We view equities as severely undervalued relative to fixed income right now.

The primary reason for this lag is a lack of passive flows. While the rest of the region benefited from massive inflows early this year, Argentina was excluded due to its status as an MSCI standalone market.

The ultimate catalyst for the equity market will be the initiation of an MSCI reclassification consultation. If reform momentum and policy continuity hold, this consultation could begin later this year. A successful move would put Argentina back on the radar of passive investors, potentially unlocking $2.3B in inflows with an upgrade to Emerging Market status by 2027 or 2028.

To get there, authorities are actively lifting capital and foreign exchange constraints while improving regulatory clarity. While hurdles remain, including limitations for foreign institutions and the need for greater English language disclosures, the direction of travel is undeniable.

A more predictable managed float regime, continued reserve accumulation, steady legislative progress, and alignment with the US administration provide a highly constructive setup for the rest of 2026.

3.1 Opening Up the Economy

Historically, Argentina has kept its economy closed off.

The ratio of trade to GDP is surprisingly low at just 25% for a small country, largely because of heavy protectionist policies. The Milei administration is making a massive push to change this by slashing tariffs, cutting taxes, and signing new trade deals to finally open the country to the rest of the world.

Agriculture & the LatAm Connection

Right now, the economy leans heavily on commodities. Of the $87B in goods exported in 2025, ~60% came from primary products and agriculture.

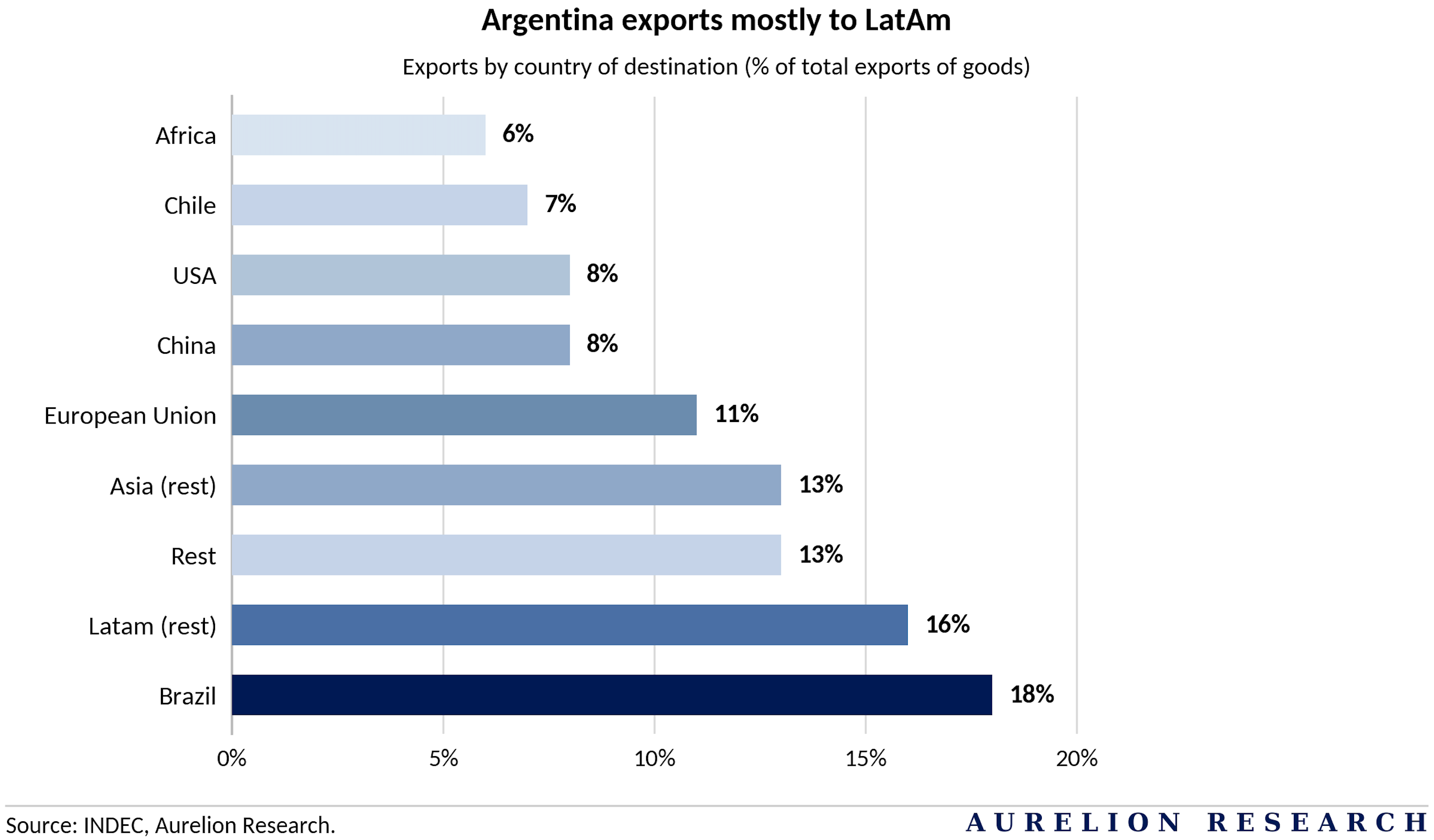

The oilseed complex, which is mostly soy but includes wheat and corn, pulls in ~$26B a year. That makes up 30% of all exports, leaving the country highly exposed to droughts and shifting commodity prices. Interestingly, over 40% of these exports stay right here in Latin America. The Mercosur agreement plays a big role in this. Over the last thirty years, Argentina has expanded its footprint in LatAm and Asia while losing ground in Europe.

Brazil is the absolute biggest buyer, taking 18% of total exports in 2024, mostly in industrial goods and autos. The US and China follow at 8% each, with China mainly scooping up food products like soy.

3.2 A Concrete Economic Recovery

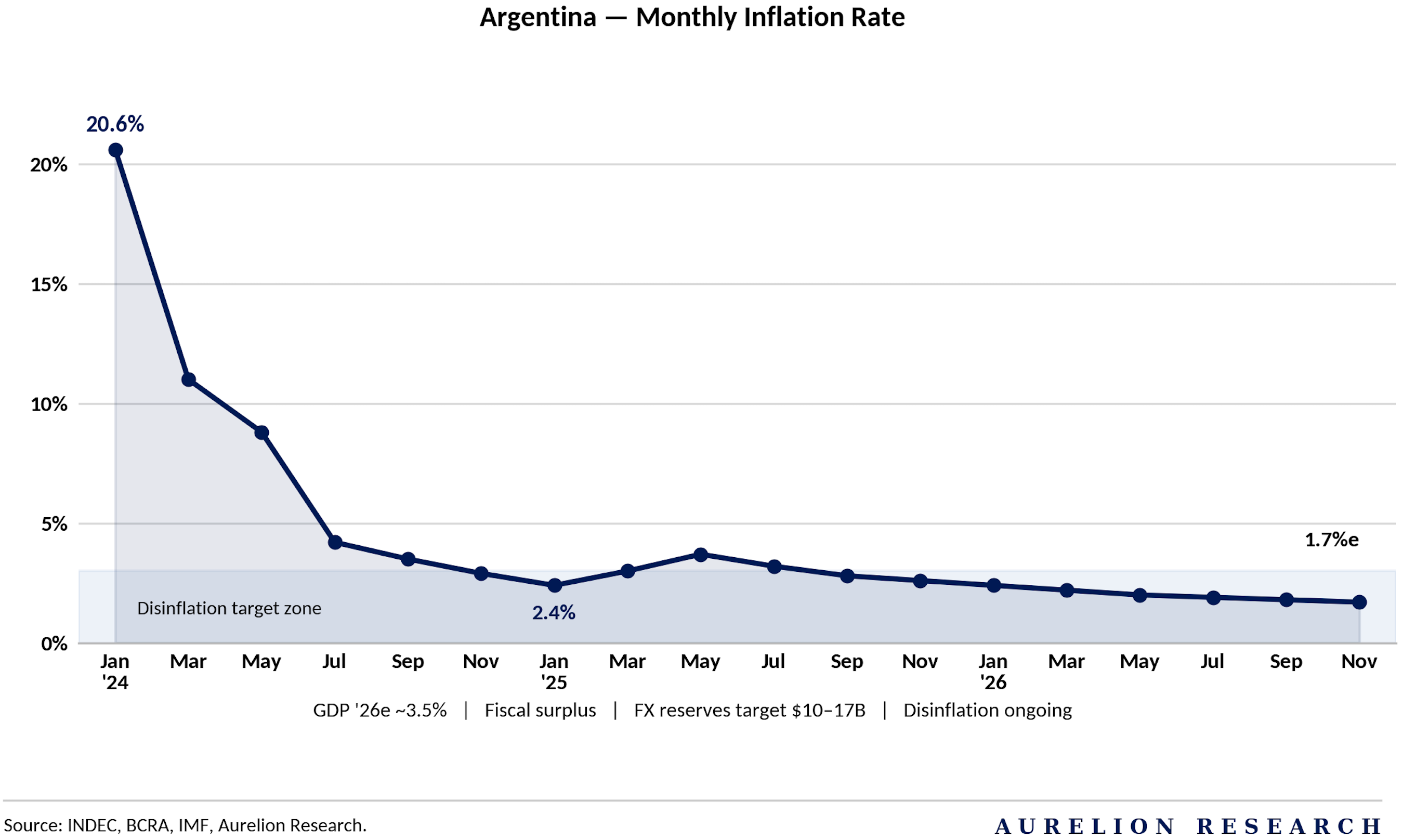

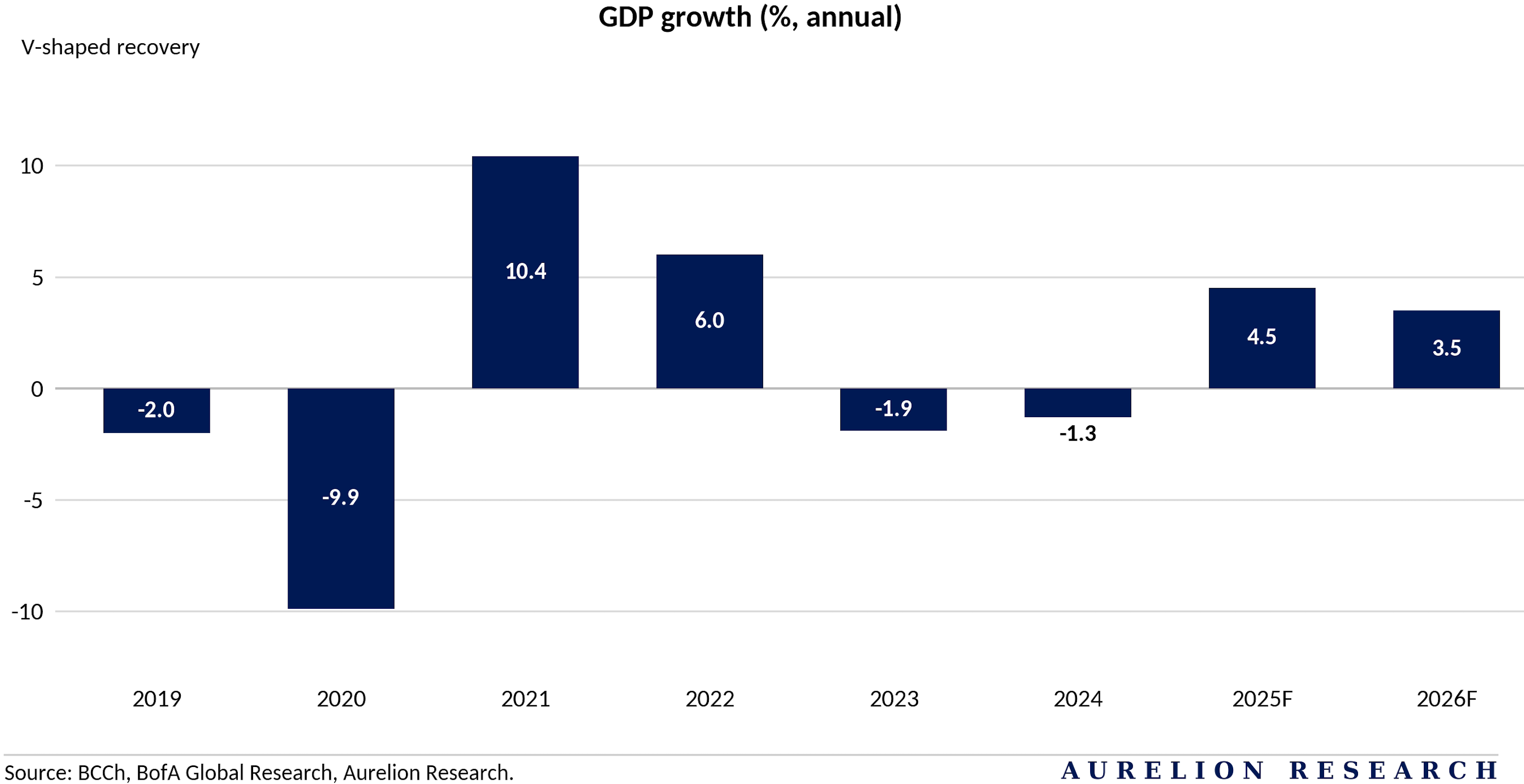

The data below shows a clear V-shaped recovery taking hold. After a tough period where the economy fell by 1.9% in 2023 and 1.3% in 2024, reforms are starting to show results. Growth is expected to bounce back strongly, with GDP rising 4.5% in 2025. Instead of a one-time spike, this then levels off into steady growth of 3.5% in both 2026 and 2027. This shift from decline to stable growth is the foundation of the investment thesis.

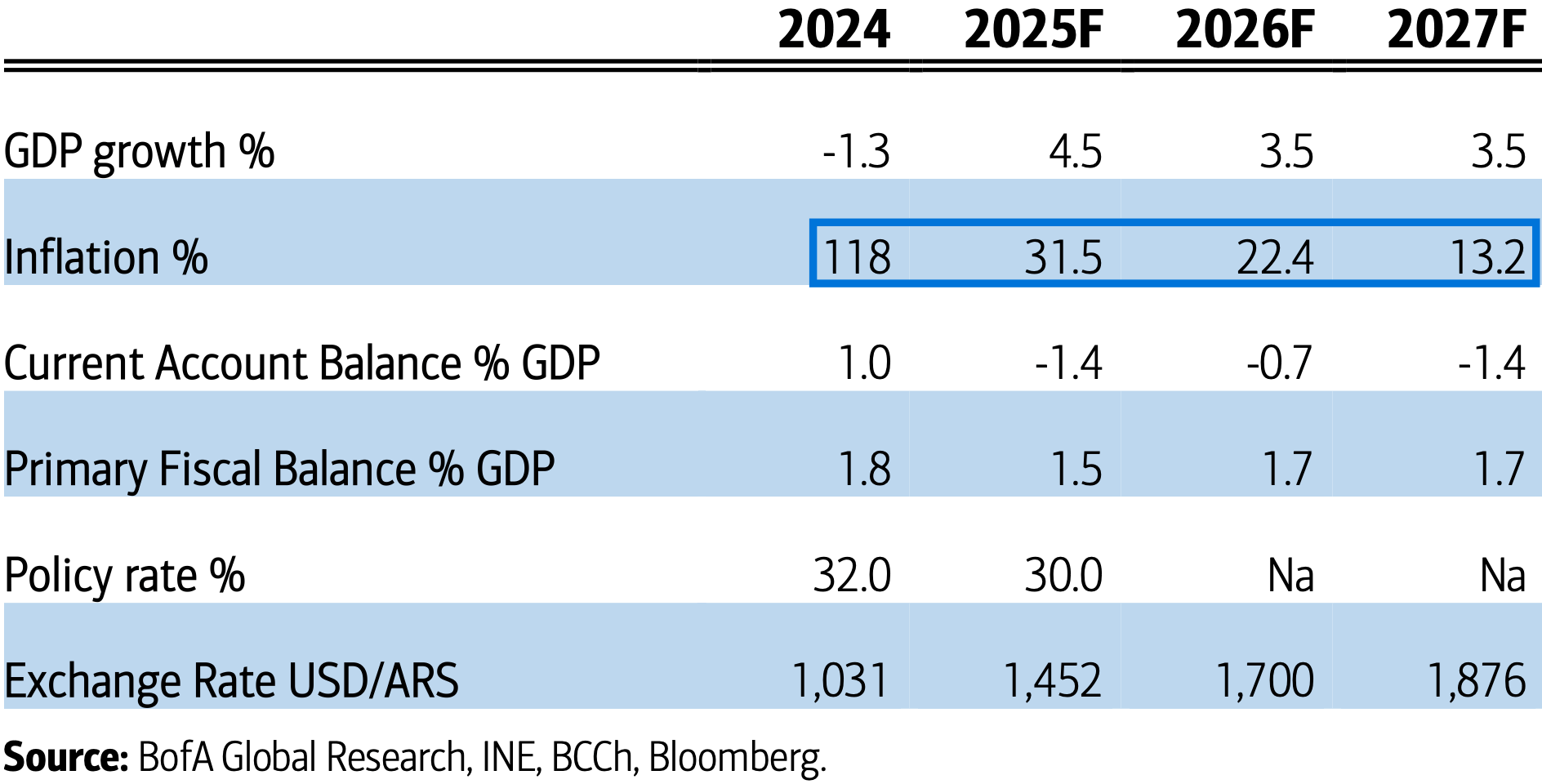

The most impressive change is happening with inflation.

The stabilization plan is steadily reducing price pressures across the economy. From a peak of 118% in 2024, inflation is expected to drop to 31.5% in 2025. It continues trending lower from there, reaching 22.4% in 2026 and a more manageable 13.2% by 2027.

Argentina Macro Forecasts

This rapid disinflation is not what we would consider an accident. Strict fiscal discipline is what is driving the disinflation in inflation entirely.

The government is maintaining a primary fiscal surplus, at 1.8% of GDP in 2024 and projected to stay between 1.5% and 1.7% through 2027. By refusing to overspend, the administration has removed the main driver of historical inflation, helping convince the market that this time is different.

Alongside cooling prices, the currency environment is becoming more predictable. The official exchange rate is following a controlled adjustment path, moving from 1,031 pesos per US dollar in 2024 to an expected 1,700 by 2026. This gradual adjustment, combined with a stabilizing current account, gives foreign investors greater visibility and confidence to enter the market without the risk of sudden currency shocks.

3.3 A History of Turmoil

Argentina has a long history of economic turmoil despite being incredibly rich in natural resources. The country has faced frequent currency crashes, massive budget gaps, high inflation, and multiple defaults over the last two decades. The core issue usually traces back to the government spending far more than it brings in, and then trying to mask the problem by artificially controlling the exchange rate.

The 2023 crisis is a perfect example of this dynamic. The government ran a deficit near 4.5% of GDP while actively holding the currency down. That combination completely drained their international reserves to a negative $11B by November 2023 and pushed inflation to an aggressive 25% month over month by the end of that year.

The Human Cost and the Rebound

These constant shocks have hit the population hard. Real wages collapsed by 40% from their 2017 peak, crushing purchasing power across the board. This severe drop pushed the poverty rate to a peak of roughly 50% in 2024.

We are finally seeing a real turn. As the recent stabilization plan takes hold and the economy actually rebounds, inflation is cooling off. This direct improvement allowed poverty to decline below 31.5% in the first half of 2025, showing that the core economic engine is starting to work again.

The Banking Challenge and the Opportunity

Years of high inflation and past banking shocks, like the forced conversion of dollar deposits to pesos back in 2002, have completely stripped money out of the official economy. People simply stopped trusting the banks.

By December 2025, the total supply of money in the system dropped to just 16% of GDP, which is well below the 21% average we saw from 2010 to 2019. US dollar deposits are also incredibly low at a mere 6% of GDP.

A shallow banking system is a huge drag on business growth because companies cannot get the credit they need to expand. It also severely limits the ability of the government to refinance its debt obligations locally.

But this extreme low base is exactly where the upside lies. Because the system is so empty right now, there is massive room to remonetize the economy and expand credit as confidence returns. Locals currently hold an estimated $200B in assets safely tucked away outside the country.

The government just passed a tax amnesty law specifically designed to convince people to bring those hidden dollars back into the formal banking system. If even a small fraction of that wealth returns, it will flood the local market with liquidity and completely transform the credit landscape.

3.3 The Debt Profile and the Liquidity Squeeze

At first glance, central government debt appears elevated at roughly $455B, or ~70% of GDP. That headline overstates the true burden. Once intra-public sector holdings are excluded, which carry minimal refinancing risk, the effective debt stock falls to about $255B, or nearly 40% of GDP.

Within that, ~$96B is owed to official creditors such as the IMF, with longer maturities and more structured repayment profiles. This framing excludes central bank liabilities, provincial debt, and potential legal obligations tied to past disputes, all of which sit outside the core sovereign balance but remain relevant for the broader macro picture.

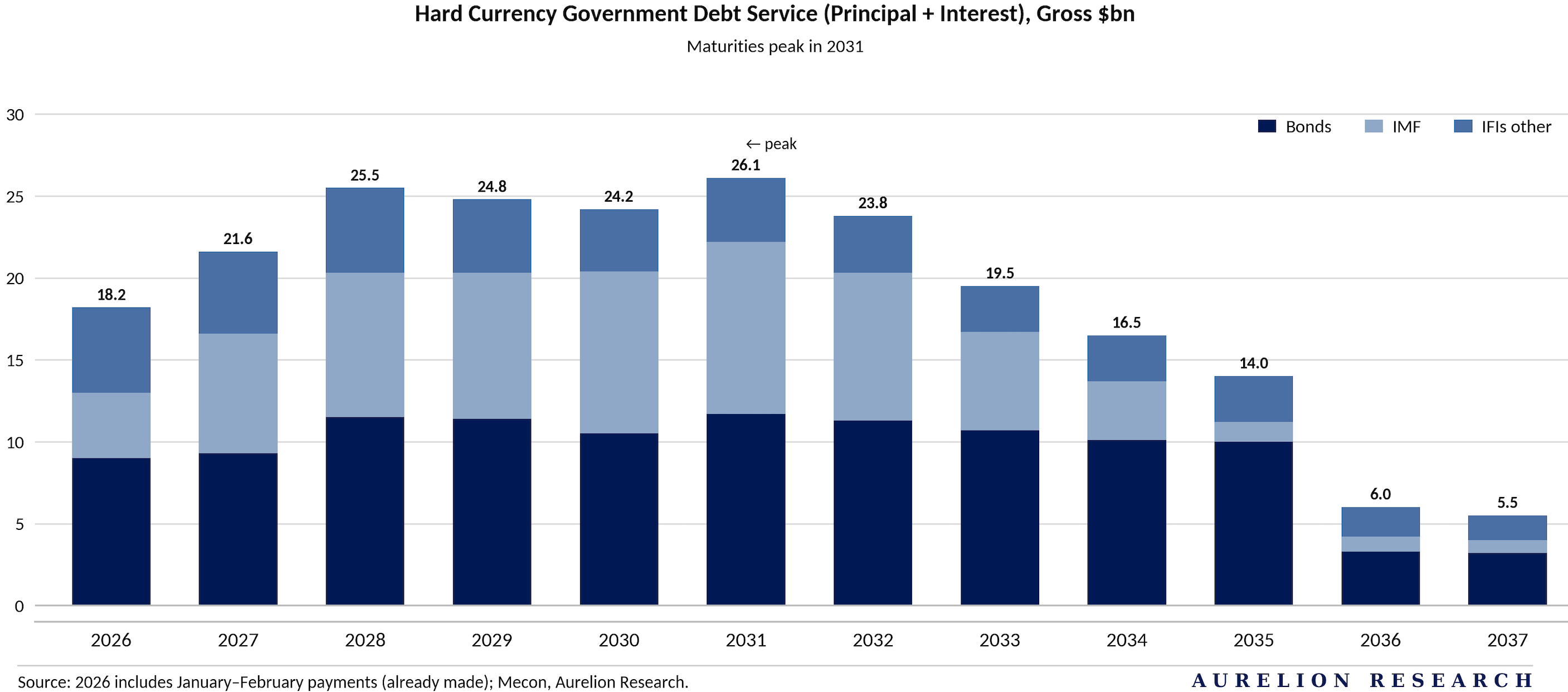

The real problem is liquidity. The debt profile is heavily front loaded with an average maturity of just five years. On top of that, ~60% of it is denominated in hard currency. When you combine those fast approaching due dates with severely low international reserves, it creates a massive liquidity squeeze.

Navigating the IMF

The country has a long and complicated history with the IMF. After a massive $56B agreement in 2018 and a failed attempt to refinance it in 2022, the program completely fell apart by 2023 because the previous government missed almost all of its targets.

The Milei administration managed to revive the relationship.

In April 2025, they secured a fresh $20B agreement, cleverly front loading $15B of those funds directly into 2025. This new plan focuses entirely on keeping the budget balanced and stacking up foreign exchange reserves. In total, Argentina owes the Fund nearly $56B, with these specific loans typically paid back over a seven to eight year window.

Returning to the Global Bond Market

The local bond market has been through massive swings. After a long lockout, the country finally regained access to global debt markets in 2016, only to restructure almost all of its foreign currency bonds again in August 2020.

Recently, government dollar bonds have rallied hard on the back of the new stabilization plan, hitting their highest prices since that 2020 restructuring.

While the sovereign government is still fighting to get fully fluid market access due to low reserves and near term maturities, the momentum is clearly building. In the meantime, the private sector is stepping up. Corporations and provinces have successfully issued nearly $10B in global bonds since October 2025.

The Political Calendar Hurdle

The biggest obstacle to lasting change is the incredibly short political cycle. Frequent elections make it exceptionally difficult to pass deep economic reforms through Congress. It also creates a bad habit where governments often increase spending right before elections.

The calendar is packed. The country elects one third of the Senate and half of the Lower House every two years, with presidential elections every four years. Because primary elections happen months before the general vote, the campaigning cycle drags on for a long time. All eyes are now on the October 2027 presidential election, which will be the ultimate test to see if this new economic direction has the political backing to last for the rest of the decade.

3.4 The Argentina Bull Case: Unmatched Upside

When you look across the Latin American landscape for the rest of the decade, the upside potential is incredibly asymmetric, and Argentina sits entirely in a league of its own. In the Spring bull case scenario for 2030, the projected returns for the region are strong across the board.

The broader Latin American index is expected to nearly double, but Argentina completely shatters the curve, projecting a massive 176% total upside over the next few years.

What makes this projection so powerful is the actual composition of that return. This is not just a story about cheap stocks getting slightly more expensive. If you look at the breakdown in the data, the vast majority of that 176% upside is driven directly by explosive US dollar earnings per share growth, rather than just a simple valuation rerating. While multiple expansion will certainly play a role as country risk drops and foreign capital returns, the core engine of this massive bull run is pure fundamental business growth.

This earnings explosion perfectly captures the fundamental shift happening on the ground. As the administration executes its deep economic reforms, stabilizes the currency, and unlocks massive sectors like energy and mining, corporate profitability is positioned to skyrocket. Companies that have survived decades of severe capital controls and hyperinflation are suddenly being unleashed into a normalizing pro business environment.

We believe this creates a rare setup. For capital willing to position ahead of the crowd, Argentina offers the most compelling high conviction growth story in the entire emerging market universe. The scale of the earnings growth potential completely separates it from its regional peers, making it one of the most obvious bet for the rest of the decade.

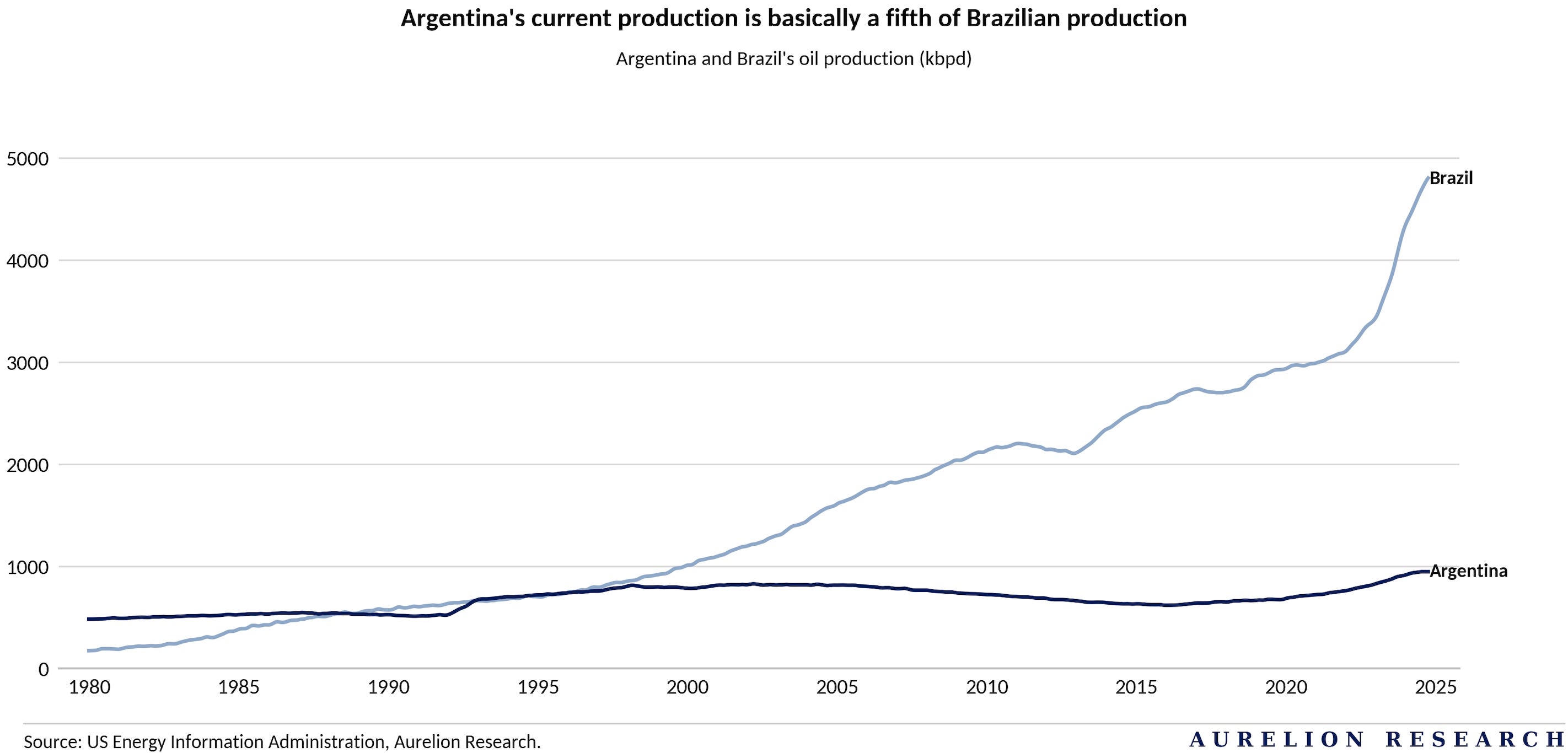

3.5 The Energy Turnaround

The energy picture is where the Argentina story gets really exciting. Thanks mostly to the Vaca Muerta shale formation, the country holds the second largest unconventional gas reserves and the fourth largest unconventional oil reserves globally. We are watching a massive turnaround play out in real time.

The energy trade balance completely flipped from a $4.4B deficit in 2022 to an $8.6B surplus in 2025. That is the highest number on record, and the trajectory suggests it will keep growing. Total oil production has surged to ~850,000 barrels per day. To put the impact into perspective, fuel and energy now make up 12% of exports. That is a huge jump from just 4% back in 2016.

On top of that, new domestic infrastructure like the Moreno pipeline is actively boosting local gas supply. This completely eliminates the need to buy expensive fuel from outside the country. Looking further ahead, new floating LNG projects could push export capacity even higher starting in late 2027.

The Historical Gap

To understand the true scale of this opportunity, you have to look back at the history. Argentina has a long legacy with oil and gas. They made their first discovery over a century ago. At one point, the country actually produced more oil than Brazil. Today, the situation is completely reversed. Brazil pumps out ~4.8M barrels per day, which is roughly 5x more than Argentina.

The reason for that massive gap comes down to decades of policy instability and heavy energy nationalism. Privatizing the state energy company YPF and then nationalizing it again 13 years later severely crushed the potential of the entire industry. For the past two decades, energy companies operated under incredibly difficult conditions. Growth was suffocated by regulated prices at the pump, strict capital controls, and severely restricted access to the heavy equipment needed to actually drill. But that history is exactly what makes the current setup so powerful. Unlocking the oil and gas sector is one of the clearest paths to bringing real stability to the broader Argentine economy.

The Vaca Muerta Catalyst

The entire bull case rests squarely on Vaca Muerta.

While geologists knew the formation was rich in hydrocarbons all the way back in the 1930s, the true scale was not confirmed until around 2010 when fracking technology finally took off in the US.

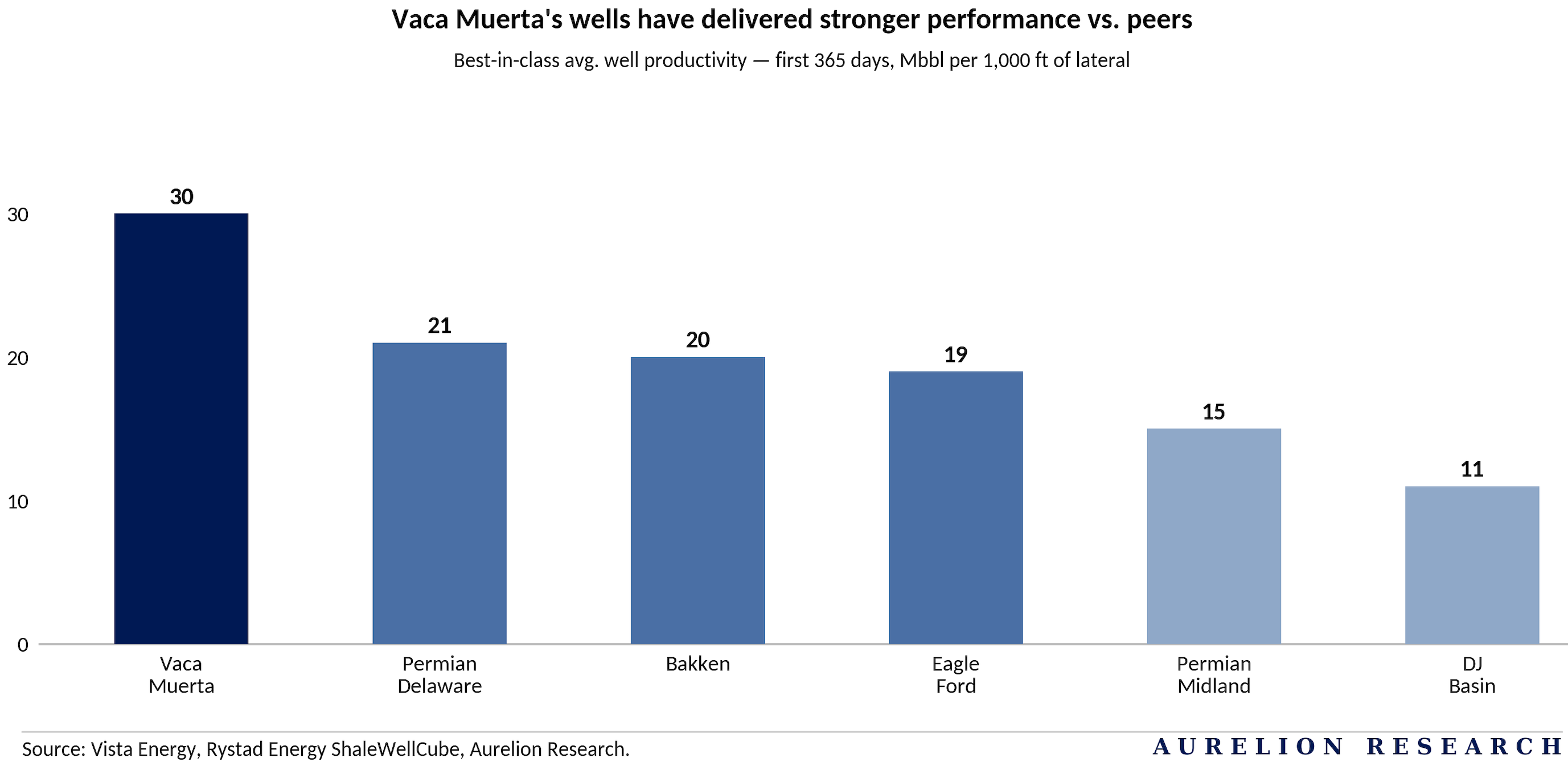

From a geological standpoint, Vaca Muerta rivals major US shale basins such as the Permian, Eagle Ford, and the Bakken. But when we look at actual well data, Vaca Muerta is outperforming US peers.

Over the past few years, the local teams have really figured out the rock. Productivity and extraction rates have improved dramatically. Looking at the best in class average well productivity for the first year of production, Vaca Muerta is delivering 30,000 barrels per 1,000 feet of lateral.

That completely blows past the Permian Delaware at 21,000 and the Bakken at 20,000. The rock quality here is undeniably world class, and the formation is widely viewed as one of the most promising shale plays in the entire world.

Now that the productivity is proven and the political backing is firmly in place, the next step is actually moving the oil. The historical bottleneck for Vaca Muerta has always been evacuation capacity. You can pump all the oil you want, but you need pipes to get it to the coast. This is exactly where the massive capital expenditure is going right now.

The existing infrastructure, including the Oldelval pipeline and local refineries, handles the current load but caps future growth. The real game changer is the upcoming Vaca Muerta Sur pipeline project, known as VMOS. This specific project completely unlocks the basin. Starting in Q4 of 2026, VMOS will add 180,000 barrels per day of new evacuation capacity.

It is going to scale incredibly fast from there.

By 2027, that pipeline alone will carry 550,000 barrels per day. By 2028 and beyond, VMOS reaches a massive 700,000 barrels per day. When you combine this new pipe with the existing network, it essentially doubles the total takeaway capacity of the entire region compared to where it sits today. This massive infrastructure buildout is the exact catalyst needed for Vaca Muerta to finally reach its full production potential.

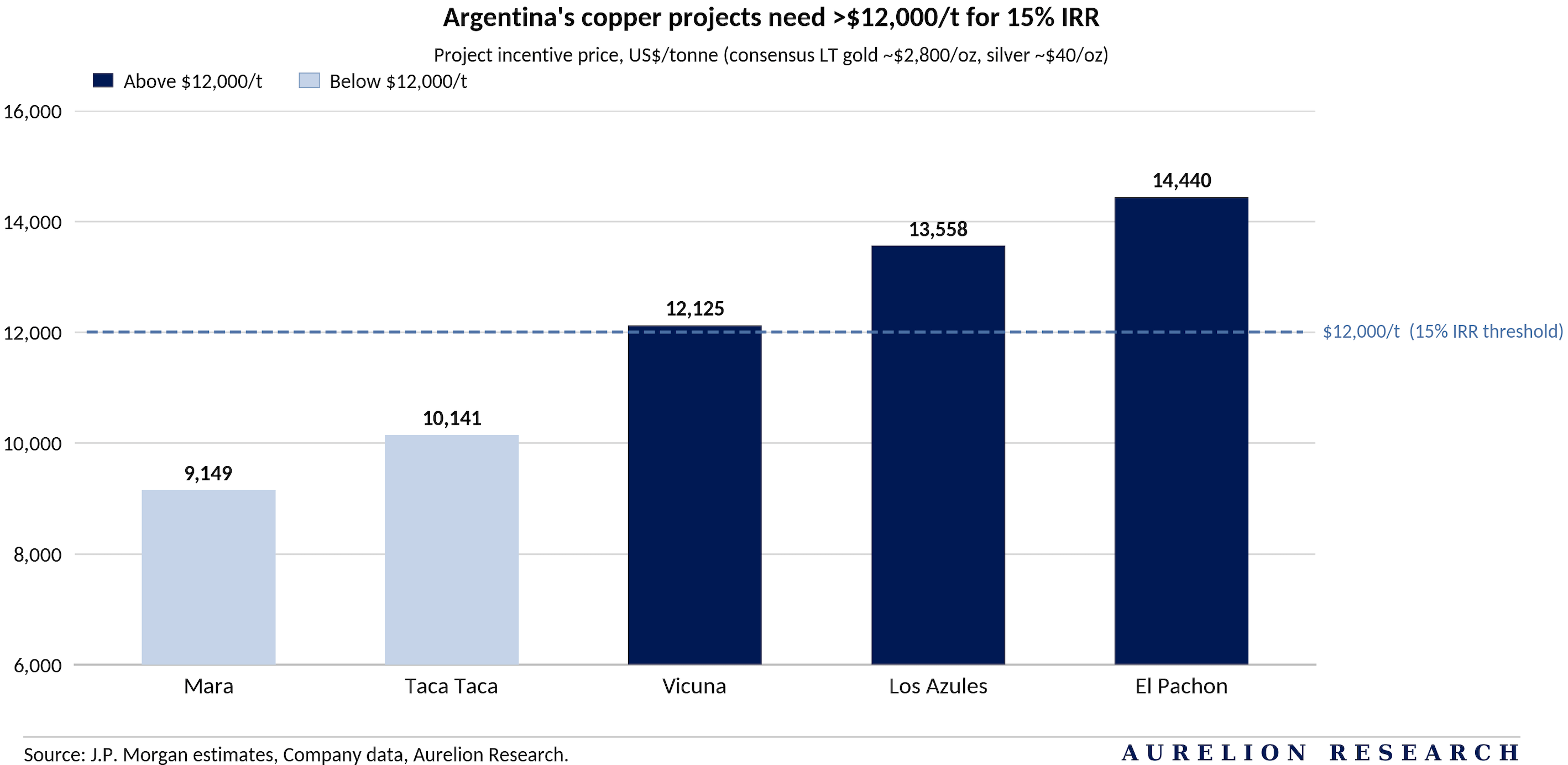

3.6 Mining and the RIGI Catalyst

Mining is the next massive catalyst for foreign capital.

Argentina sits on the third largest lithium reserves and the sixth largest copper reserves in the world. Metals exports hit $6.4B in 2025, driven mostly by gold, but the central bank projects the mining trade balance could top $15B by 2030 as copper and lithium rapidly scale up.

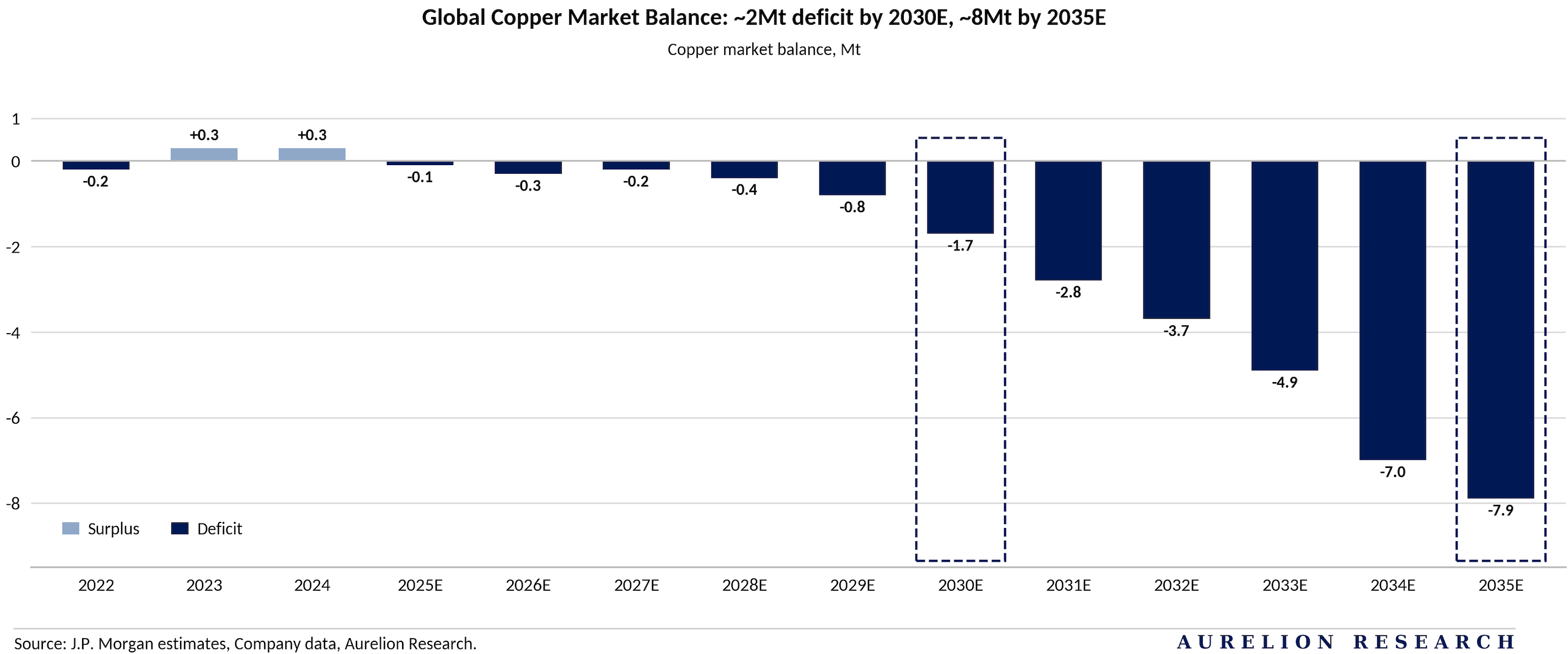

To understand the urgency behind this push, you have to look at the global copper market. Following unprecedented supply disruptions in 2025, the market has officially shifted into a steep deficit. Demand is set to expand ~3% annually for the rest of the decade, driven heavily by rising electrification, the global energy transition, and massive power needs for artificial intelligence and data centers. Forecasts show the global copper deficit widening to 2M tonnes by 2030 and hitting a staggering 8M tonnes by 2035.

Argentina is perfectly positioned to help fill this massive gap, representing over 1M tonnes of potential new supply over the next decade.

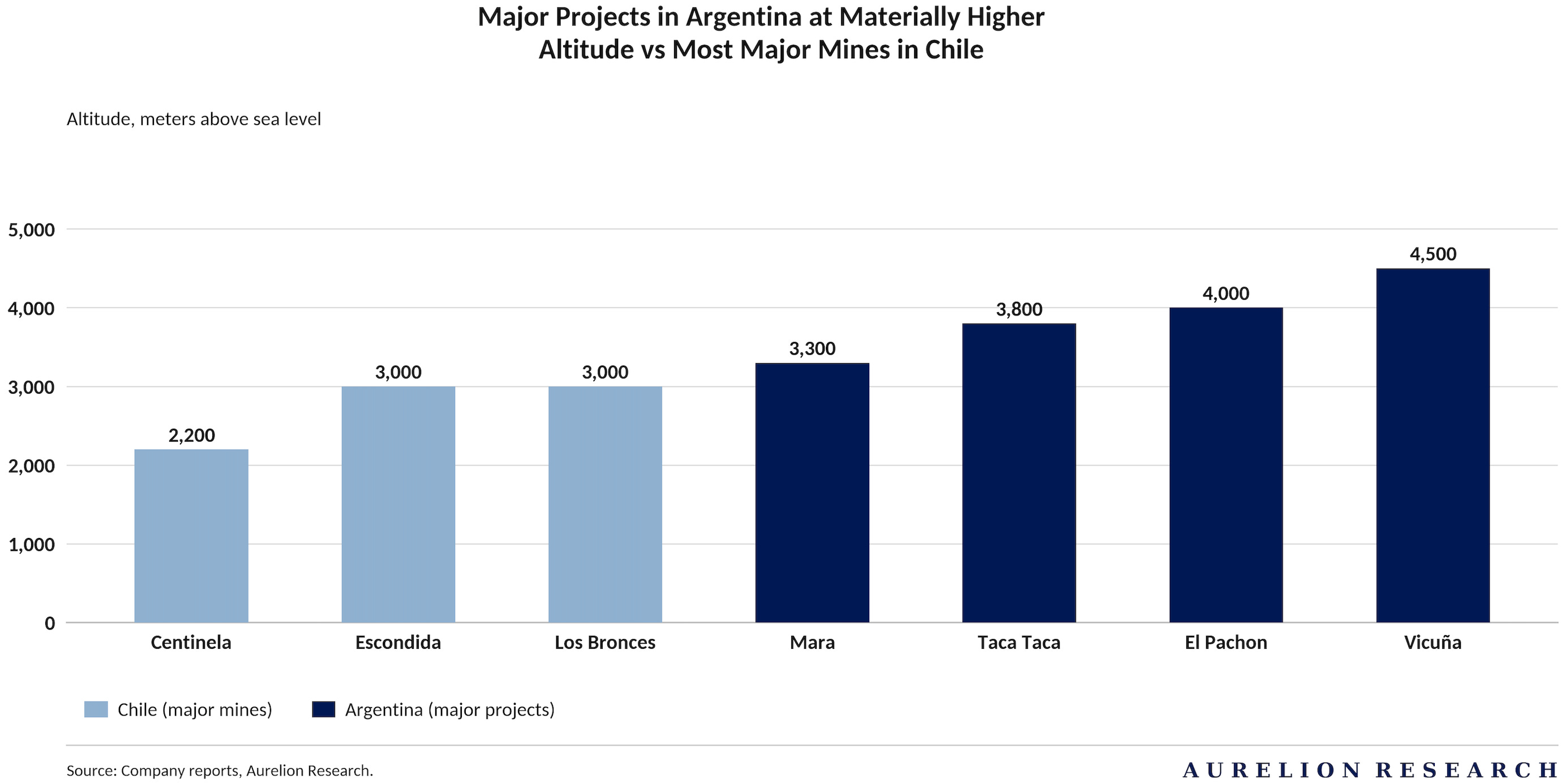

However, developing new greenfield projects in the country comes with significant technical hurdles. The local mining industry is less developed compared to neighboring jurisdictions. Miners face a challenging starting point, often needing to build entirely new infrastructure like water desalination plants and pipelines coming all the way from the Pacific.

Furthermore, these projects sit at significantly higher altitudes than most active operations on the Chilean side. Because of these logistical hurdles, future supply additions face steep costs. The average capital intensity sits ~$27,000 per tonne, which is 30% higher than 2020 levels. For completely new greenfield projects, that cost pushes well above $30,000 per tonne.

Given the massive expense and the long duration of mining investments, securing firm legal and fiscal protection is an absolute requirement for developers to commit capital. This is exactly why the government launched the Regime of Large Investments, known as RIGI. We believe this framework provides the exact incentives needed for strategic projects requiring over $200M in capital.

In February 2026, the government formalized an expansion of this decree to include upstream hydrocarbon activities on underdeveloped blocks, setting a minimum commitment of $600M for those specific energy plays. To keep the momentum going, the administration recently simplified the rules and extended the entire program through July 2027.

The financial perks within RIGI are highly attractive. Companies get their corporate income tax rate slashed from 35% to 25%. They receive total exemptions on export tariffs after three years, the removal of value added tax prepayment requirements, and accelerated depreciation.

Crucially, the regime grants them free access to US dollars linked to their project export revenues starting in the third year, while guaranteeing absolute legal and fiscal stability for thirty years. The framework is working, and capital is already moving fast. Most major copper projects have already submitted applications to secure these protections. So far, RIGI has received over $70B in project proposals, with $26B already officially approved. Almost 70% of this total is tied directly to mining, while energy makes up the rest.

We are seeing concrete timelines form rapidly.

The Vicuna mining project in the San Juan province has already mapped out $7B in capital expenditure between 2027 and 2030. In the energy space, a massive $15B liquefied natural gas project is actively moving forward, and the government expects even more capital to flow in shortly as these regulatory frameworks cement confidence.

3.8 Our Final Take on Argentina

The country is executing the most aggressive and necessary economic pivot in recent history. While the historical risks are well documented, the market is severely underpricing the actual progress happening on the ground right now. We are officially moving past the fragile early stabilization phase and directly into a period of massive capital deployment.

With inflation rapidly cooling, a sustained fiscal surplus, and billions in foreign direct investment actively lining up for energy and mining, the foundation for a sustainable economic boom is firmly in place.

The combination of world-class hard assets, a deeply undervalued equity market, and a government committed to lasting economic change creates a rare setup. For capital willing to look beyond recent history, Argentina stands out as one of the most compelling asymmetric growth stories in the emerging world for the rest of the decade, though it is not without risks.

4. Colombia: High Upside on Hold

While Colombia has significant upside potential in a true bull scenario, we believe it remains too early to position aggressively. Notably, the country was largely excluded from major regional 2030 upside projections due to high political volatility. Realizing its full potential requires the next administration to enforce strict fiscal adjustments and reduce fixed spending to bring the debt-to-GDP ratio closer to 40%.

The market is currently pricing in a B+ rating, implying more than two full downgrades. If a market-friendly outcome materializes, we could see spread tightening of around 150 basis points, back toward levels not seen since 2021. However, until valuations become more attractive or clearer political signals emerge, we think patience is still required.

The Political Catalyst

Political cycles completely dictate equity performance in Latin America. Center right victories consistently trigger massive rallies, while leftward shifts lead to heavy selloffs. After a rally driven by pure business fundamentals in 2025, the local COLCAP index is now moving entirely on election expectations and foreign capital flows.

Our base case points toward a potential regime change, which would force a major upward rerating for Colombian equities. Conversely, a continuation of the current leftist policies presents severe downside risk for the market.

The State of the Race & Legislative Safety Net

Currently, Ivan Cepeda leads the first round polling, but the landscape is highly fluid. The ultimate deciding factor will be the massive block of undecided and centrist voters. Because rejection rates remain elevated across the board, the candidate who successfully consolidates the orthodox vote has the absolute clearest path to winning the final runoff.

Fortunately, regardless of the presidential outcome, the recent legislative elections created a powerful safety net. Congress is divided. This split legislature provides immediate institutional checks against extreme policy proposals from the executive branch, effectively forcing the next administration to negotiate and govern closer to the political center.

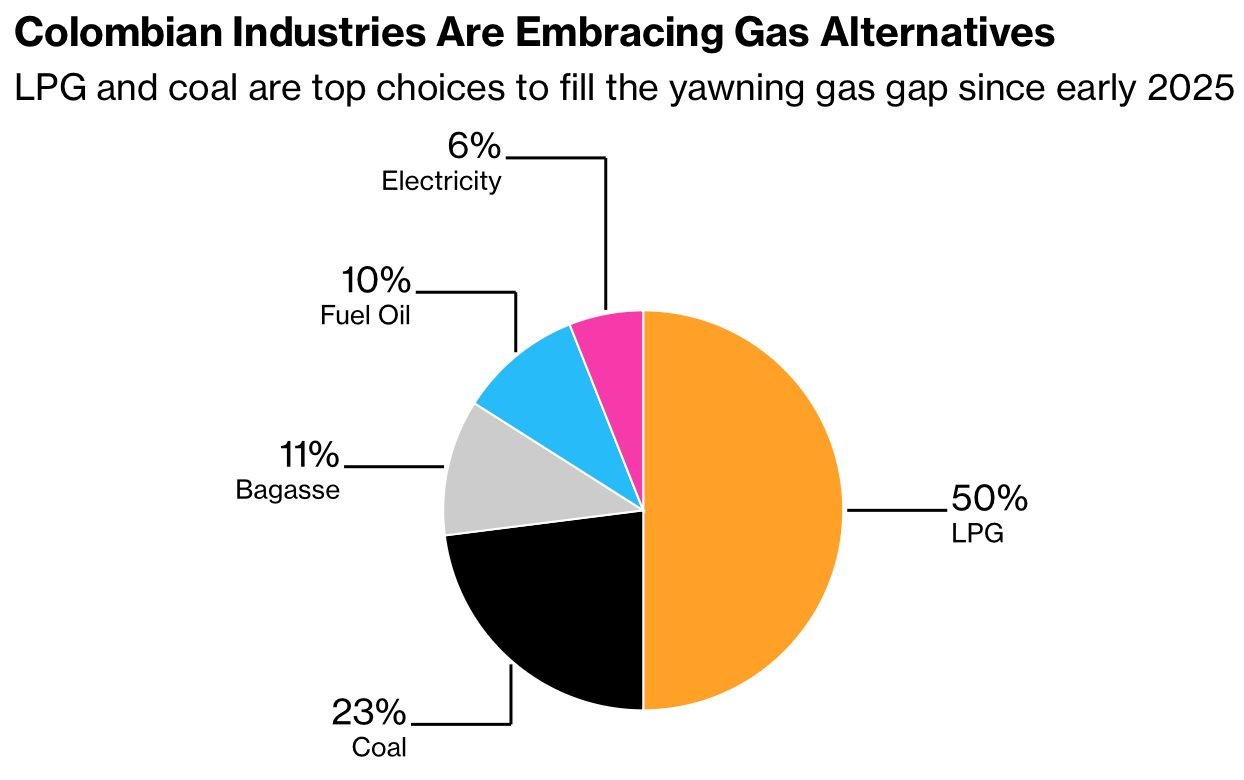

4.1 The Colombian Energy Squeeze

Colombia is facing a severe domestic gas shortage that is forcing a complete rethink of its energy strategy. Domestic gas production fell 17.1% YoY to ~794M cubic feet per day in 2025. The reserve picture is also weak.

As of 2024, the country only had enough gas reserves to last 5.9 years at current consumption levels, down from 6.1 years in 2023. The daily supply shortfall is already near 200M cubic feet, roughly 20% of total demand, and is expected to rise to 310M next year according to the national commodities exchange. We see this widening gap as increasing pressure on imports and forcing a rapid shift in how the system is being supplied.

The Forced Return to Coal

To keep operations running, local industries are abandoning the idea of cheap domestic gas and turning to alternatives. LPG and coal are the top choices to fill the yawning gap. Because domestic coal is significantly cheaper than imported LPG, which is partly sourced from the US Gulf Coast, small and medium sized businesses are actively reverting to burning it.

As the head of the National Federation of Coal Producers, Carlos Cante, noted, industries realize the era of cheap gas is over. This industrial pivot represents a massive defeat for the Petro administration and its aggressive push to completely eliminate fossil fuels, especially since solar energy still accounts for a tiny fraction of the overall energy mix.

The LNG Bridge

To address the immediate gap, the country is working to expand its import capacity. The existing 475M cubic feet per day SPEC terminal outside Cartagena will increase by about 12% next year, with generators absorbing most of the supply to prepare for El Niño events. A wave of new offshore liquefied natural gas projects is also moving forward.

Two smaller 60M cubic feet per day projects have reached final investment decisions and will begin operations in September. This includes Caribe LNG, led by Course2 Energy LLC and Andalusian Energy, which will supply distributor Empresas Publicas de Medellin. Ecopetrol will launch a similar facility at Buenaventura on the Pacific coast.

The outlook for larger scale proposals is much less certain.

Ecopetrol and Frontera Energy aim to kick off a 400M cubic feet per day floating terminal in Cartagena in December. Transportadora de Gas Internacional is planning a similar sized project off La Guajira for January.

Further out, Amazonica LNG is pushing a 150M cubic feet per day project near Barranquilla for late 2027, backed by supply agreements with Vitol Group, while Cienaga LNG hopes to dock a 400M terminal in 2028. While these proposals far exceed actual requirements, project directors openly admit that many will fail to secure necessary financing to reach construction.

4.2 Election Catalysts & Long Term Optionality

The ultimate fix for the gas deficit depends heavily on the upcoming May elections. The Petro administration banned hydraulic fracturing back in 2022, but leading presidential candidates are actively looking to bring it back to unlock domestic supply. Looking further out, Ecopetrol and partners like Brazil’s Petrobras are targeting deepwater Caribbean gas deposits by 2030.

Gustavo Petro at the UN General Assembly in New York

Furthermore, pending cross border pipeline repairs, the easing of US sanctions could eventually open the door for direct pipeline imports from neighboring Venezuela.

4.3 Smoothing the Debt Profile Ahead of the Vote

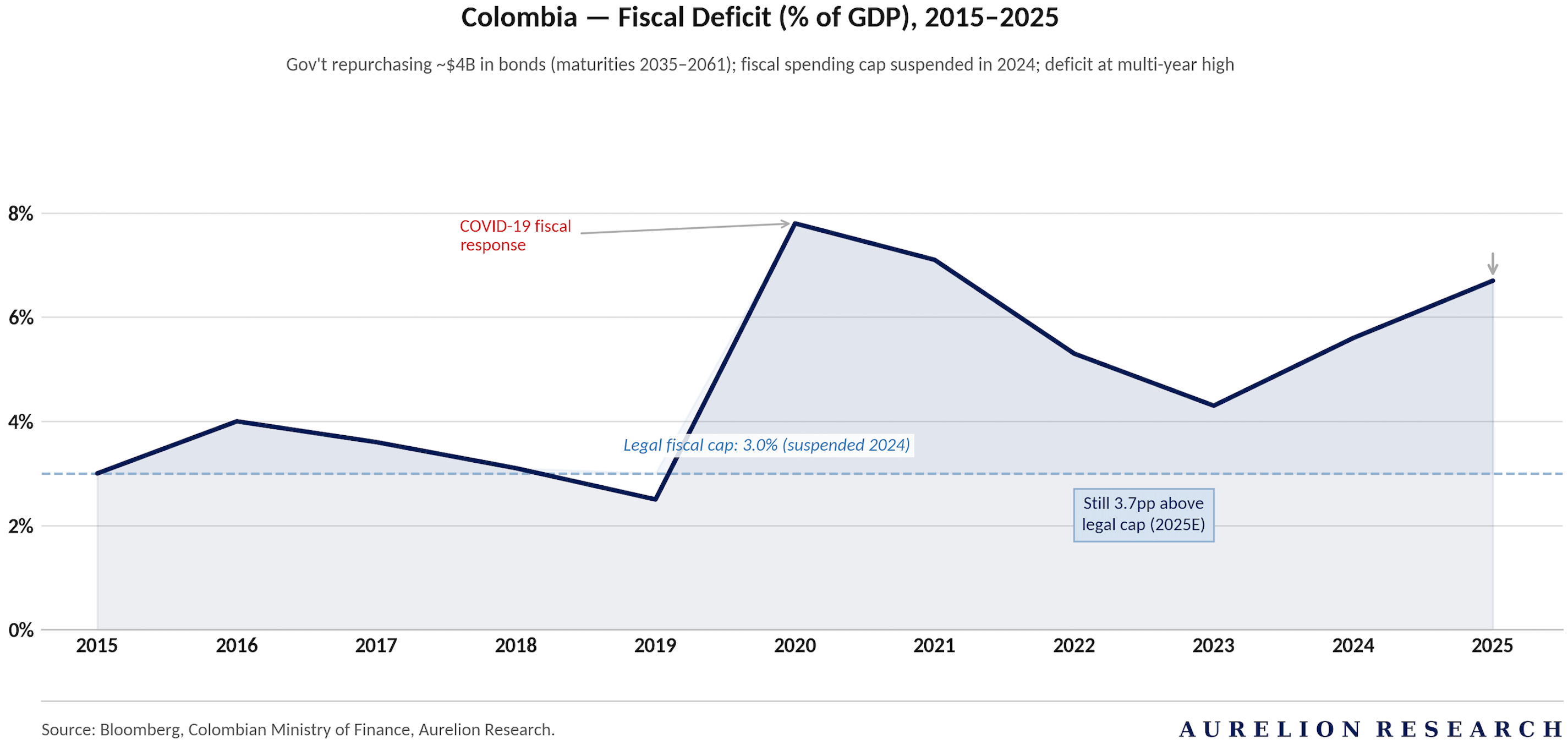

Colombia is actively buying back a portion of its outstanding global bonds. This marks the third operation of its kind over the past year as part of a broader strategy to reduce borrowing costs right before a highly contested presidential race. The government is using cash to repurchase notes with maturities ranging from 2035 all the way to 2061. Public credit chief Javier Cuellar stated last week that authorities expect to retire roughly $4B in bonds, with the current tender offer set to expire at 5 PM on April 24.

The main goal is to reassure bondholders and stabilize markets amid rising concern over the national accounts. The budget deficit is now projected at 6.7% of GDP this year. Investor concerns intensified last year after the administration suspended the legal fiscal spending cap.

That deteriorating financial picture recently prompted S&P Ratings to cut the sovereign credit score further into junk territory. The agency explicitly cited the persistently large fiscal gap and a high overall debt burden. Given this immense pressure, the buyback serves as a strategic defensive move.

As UBS strategist Pedro Quintanilla noted, the tender is structured to encourage participation without requiring the government to overpay. In practice, clearing these maturities is a sensible step for a sovereign facing rating pressure and elevated political uncertainty ahead of the May election.

4.4 Our Final Take on Colombia

While Colombia can screen as a market with deep value opportunities, we do not believe the current risk profile is attractive, and patience is the right approach. Our strategy is to wait out the political noise.

We prefer to stay on the sidelines until the upcoming elections are complete and the policy direction becomes clearer. Once that uncertainty fades, high-conviction opportunities will be easier to identify and act on with conviction.

From a positioning standpoint, we are not a big fan of large state-backed energy players and avoid names like Ecopetrol (EC). That said, we do see strong value in select local Colombian equities that trade outside US ADRs, but we prefer to cover those in a follow-up report.

5. Chile: A Safe Haven in Latin America?

Chile is currently enjoying strong momentum backed by clear policy direction and a wave of investor optimism. During the 2025 fiscal year, the local IPSA index delivered an exceptional 72% return in US dollar terms.

This rally was remarkably broad, with every single component of the index posting gains. The banking, retail, and real estate sectors led the charge, alongside industrial giants like LATAM Airlines and SQM.

The Political Turning Point

The primary driver of this performance was a major shift in investor positioning ahead of the presidential election. Markets anticipated a move toward a more pro investment administration, a view that was confirmed by the election of Jose Antonio Kast. Confidence remains high as the market looks toward his economic policies for the 2026 to 2030 period, supported by the appointment of a highly technical and proficient cabinet.

Macroeconomic Resilience & Tailwinds

The Chilean economy proved much tougher than expected throughout 2025. While initial estimates pointed to 2% growth, the economy is now on track to expand by as much as 2.3% thanks to a surge in investment during the second half of the year. Several key factors are supporting this recovery:

Copper prices remain at record highs, providing a meaningful boost to the national accounts and export revenues.

New pension reforms are increasing savings within the $239B private pension system, strengthening domestic capital formation.

The adoption of a new sectoral permitting law is beginning to cut regulatory delays and unlock project execution across key industries.

Business confidence has broadly improved, supporting stronger corporate profitability and improving investment across the economy.

The 2026 Trajectory

As we move into 2026, Chilean equities are expected to continue their upward trajectory. Early indicators point to corporate earnings growth in the high single digits, providing a solid base for the market.

Beyond strong commodity prices, the economy is also benefiting from the restart of previously stalled infrastructure projects, particularly data centers and transportation. Economic projections for 2026 remain positive, with GDP growth expected at 2.5%. This expansion is driven by a 4.6% increase in capital formation and a steady rise in consumption. While constraints in copper production might slightly moderate the overall headline numbers, the broader economy is showing consistent improvement.

There is also a major potential catalyst on the horizon.

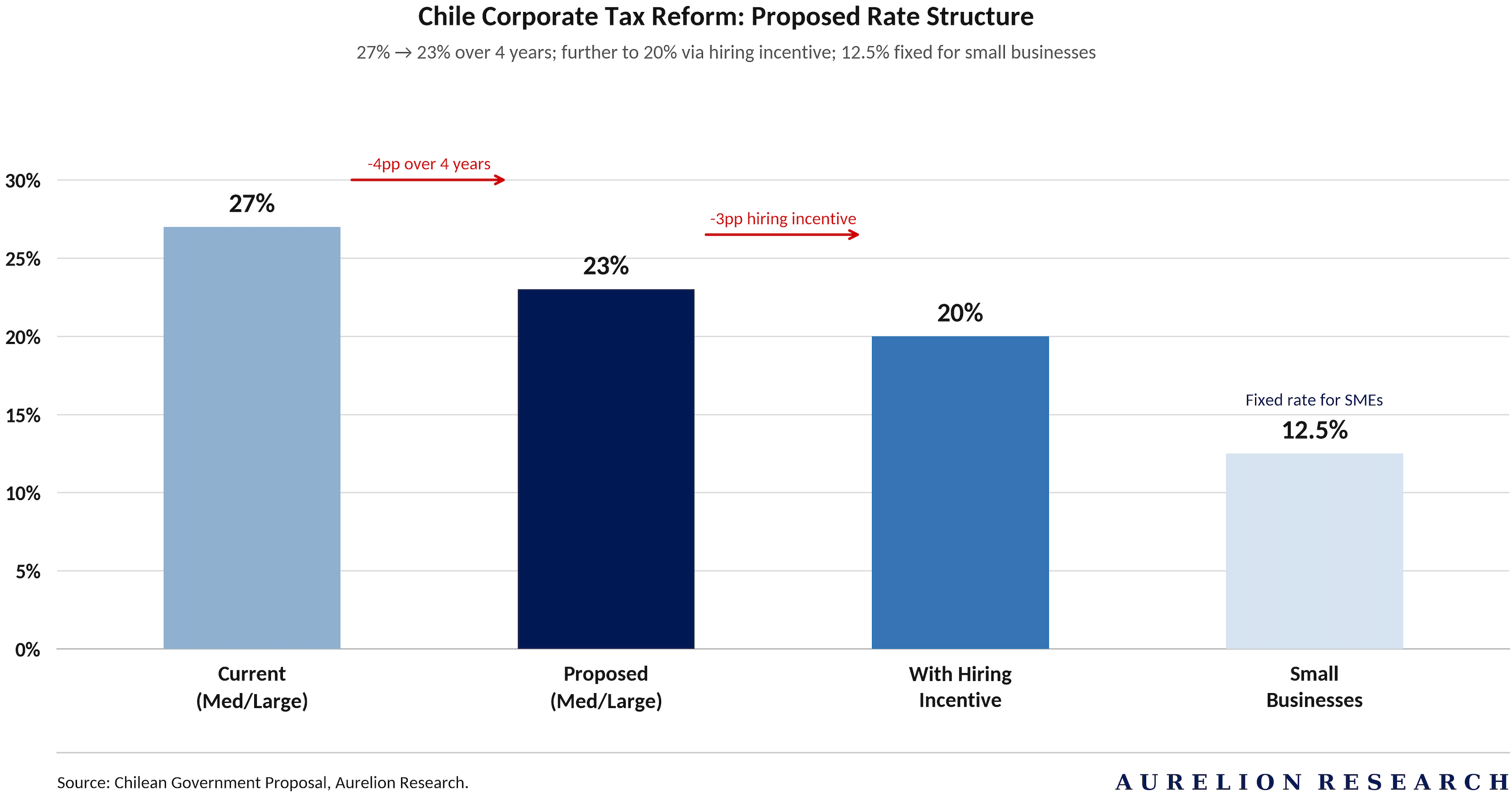

The administration is pursuing a politically sensitive tax reform aimed at lowering corporate tax rates. If this legislation passes, it would likely trigger another significant move higher for equity valuations by immediately boosting earnings per share and stimulating further domestic investment.

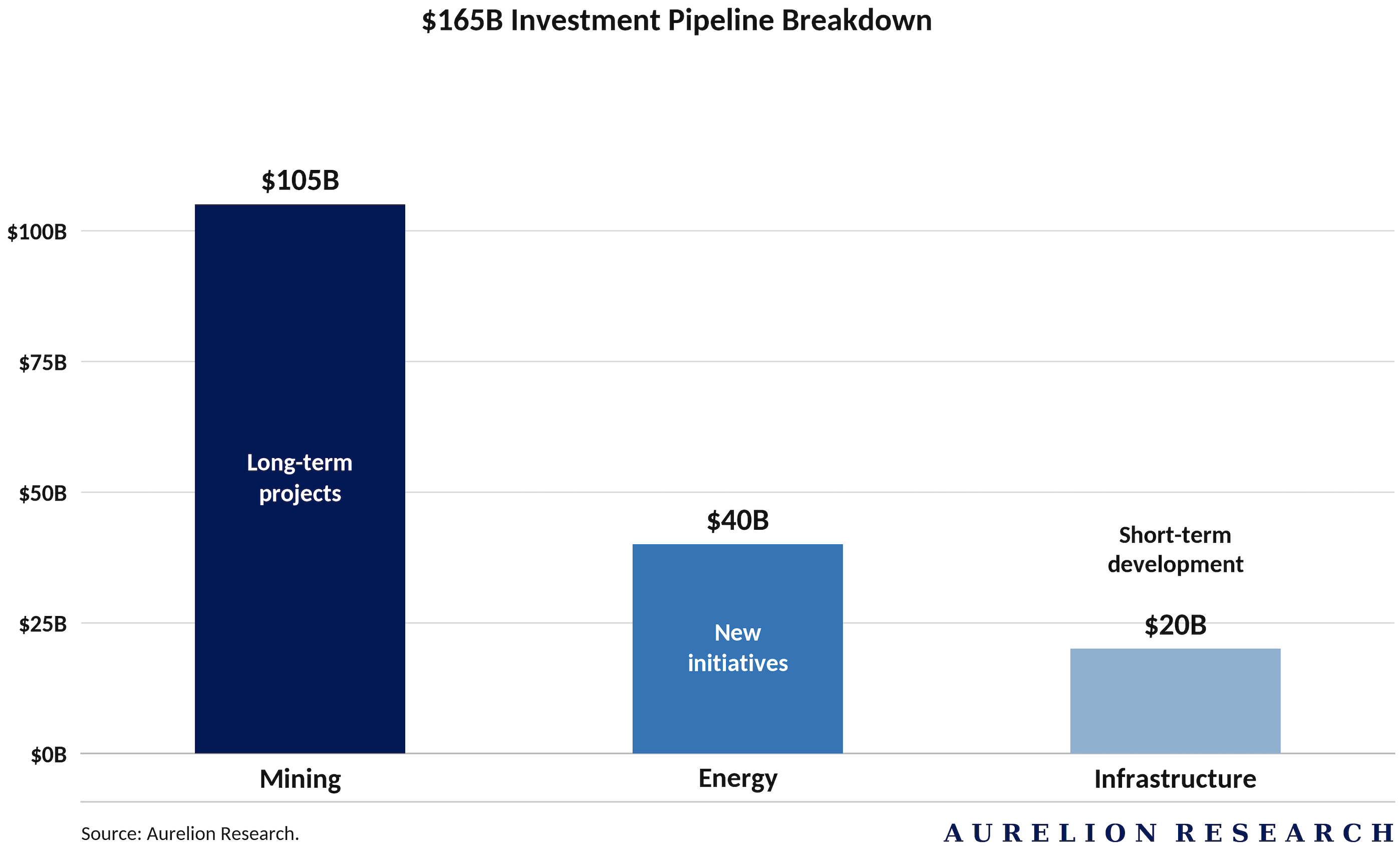

5.1 Unlocking the Investment Backlog

A principal driver for 2026 is the implementation of new permitting legislation designed to cut through years of bureaucratic red tape.

This framework is expected to reduce processing times by 30% to 70%, effectively unlocking a massive investment pipeline valued at $165B.

The timing is critical. The convergence of a new administration with a more efficient regulatory system is a major catalyst for accessing an expanded investment backlog that has been stalled for years.

This $165B pipeline is broken down into 3 major categories:

While this capital will be deployed over the next decade, it provides an immediate and substantial stimulus to the heavy construction and engineering sectors. The downstream effects will likely drive increased employment and consumer spending, supporting a tactical bias toward the banking and consumer discretionary sectors.

Strategic Commodities & Infrastructure

The incoming Kast administration is moving to leverage record high global prices for copper, molybdenum, and silver. These commodities are vital to both Chile’s export portfolio and global technology supply chains. To support this growth, significant investment is flowing into essential infrastructure, including port facilities, desalination plants, and logistics networks.

Chile is also emerging as a key player in the rare earth elements market through the Penco module owned by Aclara Resources. This project offers a high quality, non Chinese supply of heavy rare earths. By April 2026, Aclara reached the final stages of the environmental review process, positioning Chile as a critical partner for Western supply chains.

The Green Hydrogen Frontier

New industries are also beginning to expand the investment backlog.

A major milestone occurred in December 2025 with the approval of a bill promoting the green hydrogen industry. This legislation includes a $2.8B tax incentive program designed to stimulate domestic demand through 2030.

The bill creates a targeted tax framework to encourage producers to set up operations in the Magallanes and Chilean Antarctic regions, leveraging strong wind resources. It includes corporate tax exemptions and VAT relief on imported equipment. While it is in the final stages of Senate approval, it already adds to Chile’s investment appeal.

5.2 Copper Prices & Sovereign Strength

The Kast administration is well positioned to restart mining investment after a decade of stagnation, supported by copper prices at record highs of $6.03/lb as of April 22 2026. This environment attracts capital while also improving public finances through higher export revenues, royalties, and corporate taxes. These inflows are rebuilding fiscal strength.

By early 2026, Chile’s sovereign wealth funds reached a combined value of around $14.1B, with the Pension Reserve Fund (FRP) rising above $10.5B.

The budget was based on a conservative copper assumption of $4.35/lb. With spot prices nearly $2.00/lb higher, Chile is generating a significant fiscal windfall. This is improving government finances and supporting the country’s stable A-range credit rating outlook.

Market Dynamics & Deficits

After averaging $4.51/lb in 2025, copper prices are projected to average $5.00/lb throughout 2026 and 2027. Several factors are pushing prices higher:

Supply Constraints: Persistent mine disruptions and regional supply bottlenecks are tightening the market.

Global Demand: Massive growth in electric vehicles, power generation, and grid infrastructure continues to soak up available supply.

Refined Deficit: The global market for refined copper is facing an estimated deficit of 350,000 metric tons for 2026.

Speculative interest also remains high, with thousands of net long positions across the London Metal Exchange (LME) and COMEX, signaling expectations of further gains and reinforcing the upward momentum in copper prices.

Production Challenges & Recovery

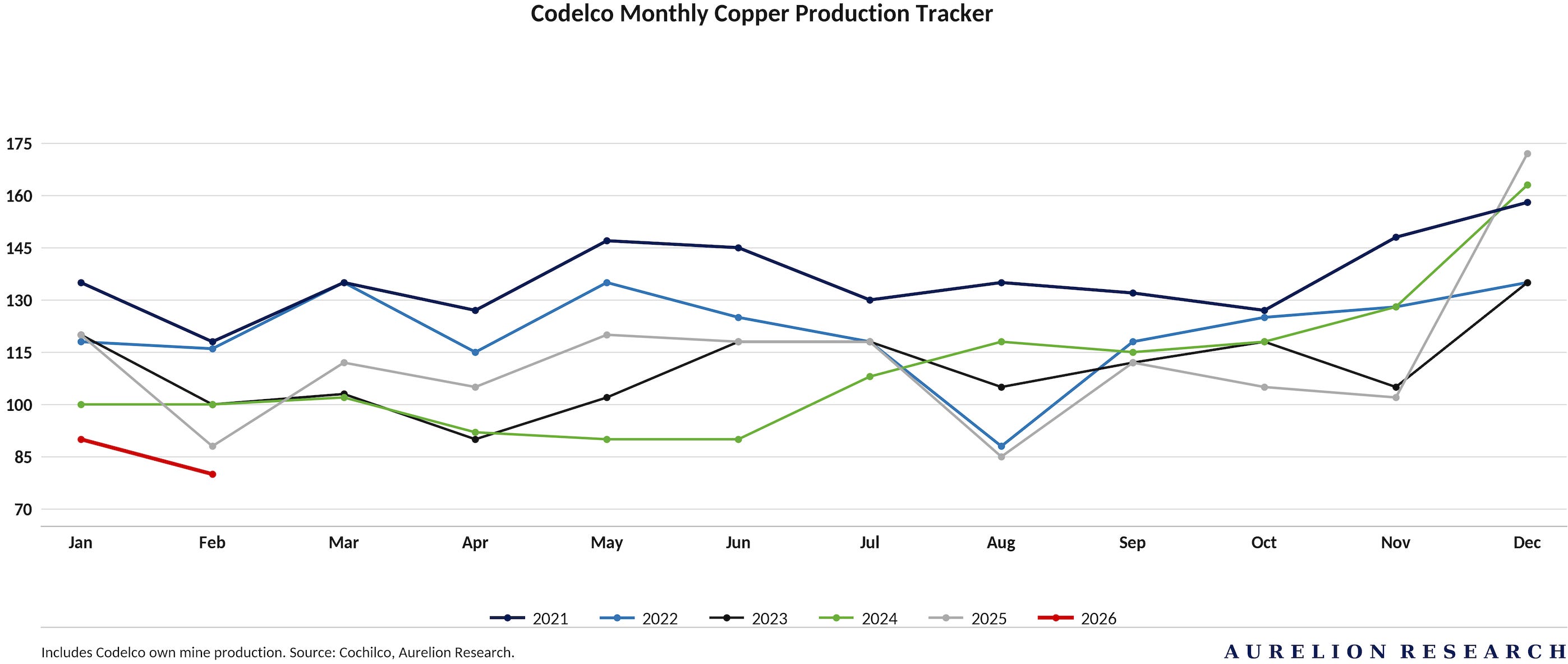

While copper prices remain high, production volumes have faced significant volatility. As shown in the monthly tracker, Codelco mine production in early 2026 started at levels notably lower than previous years, following a trend of persistent output decline that bottomed out in 2023 and 2024.

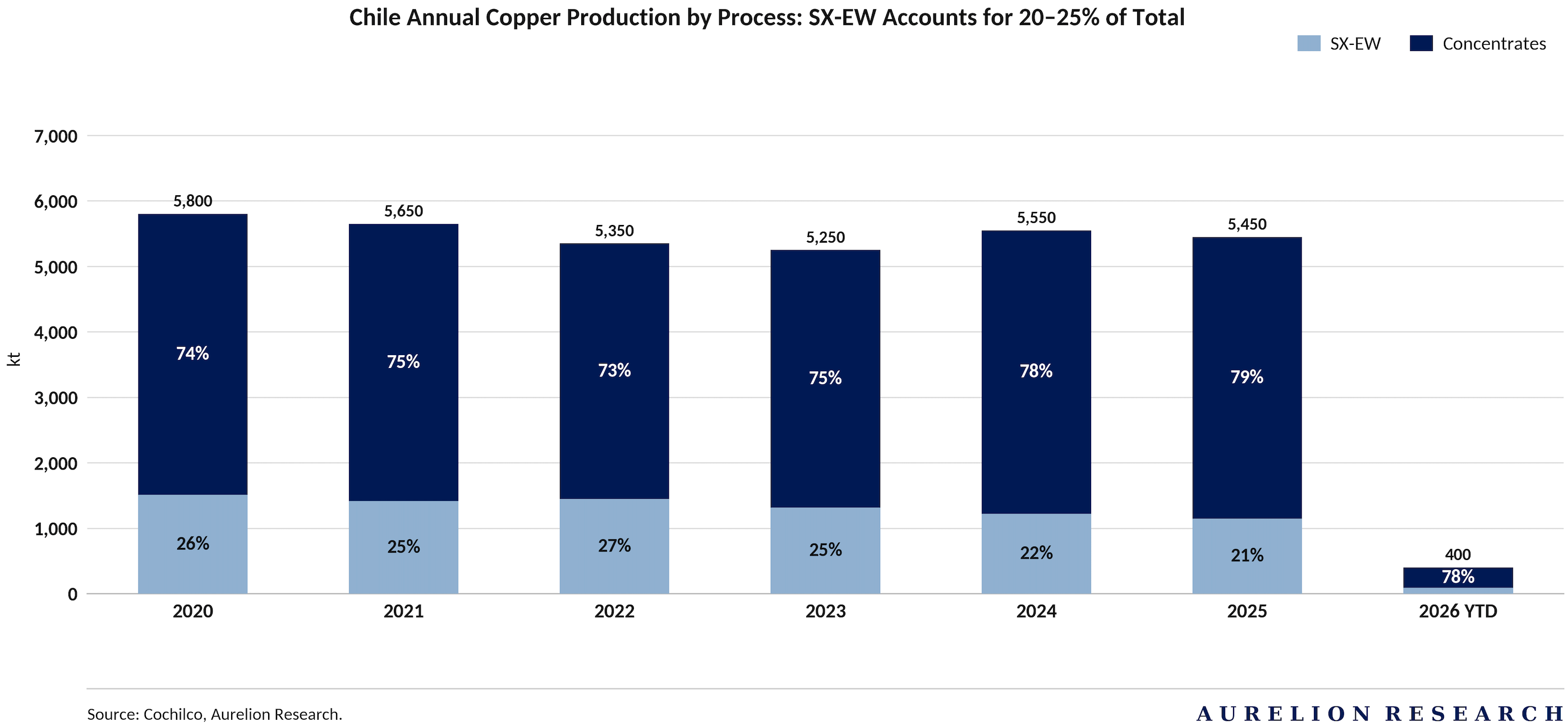

However, there are signs of stabilization. Yearly production data indicates that while output dipped to 5.25M metric tons in 2023, it recovered to 5.55M in 2024 and 5.45M in 2025. A critical component of this output is the split between concentrates and SX EW production.

Currently, copper concentrates account for ~75% to 79% of total Chilean production, while SX EW (a leaching and refining process) makes up the remaining 21% to 25%. Maintaining the scale of concentrate output is key for Codelco to benefit from the current market deficit and elevated prices.

This production recovery, paired with the surge in copper prices, is providing the financial momentum necessary for Codelco to manage its debt load.

As of late 2025, the company net financial debt stood at ~$23.8B. Improving production figures throughout 2026 will be essential to ensure the company can continue to improve its earnings and slowly work down this leverage, maintaining its role as the primary engine for the Chilean state coffers.

5.3 Tax Cuts & Capital Market Reforms