Vale: The Iron Ore Giant

We believe the market is underestimating Vale, one of the world’s largest miners, and its true earnings power. This report explains why.

While we do believe Vale is trading at a cheap and attractive valuation, it will not be added to the Aurelion Index at this stage, as we think a deeper analysis is required before taking a position.

Introduction : 4Q Operations & 2025 Turnaround

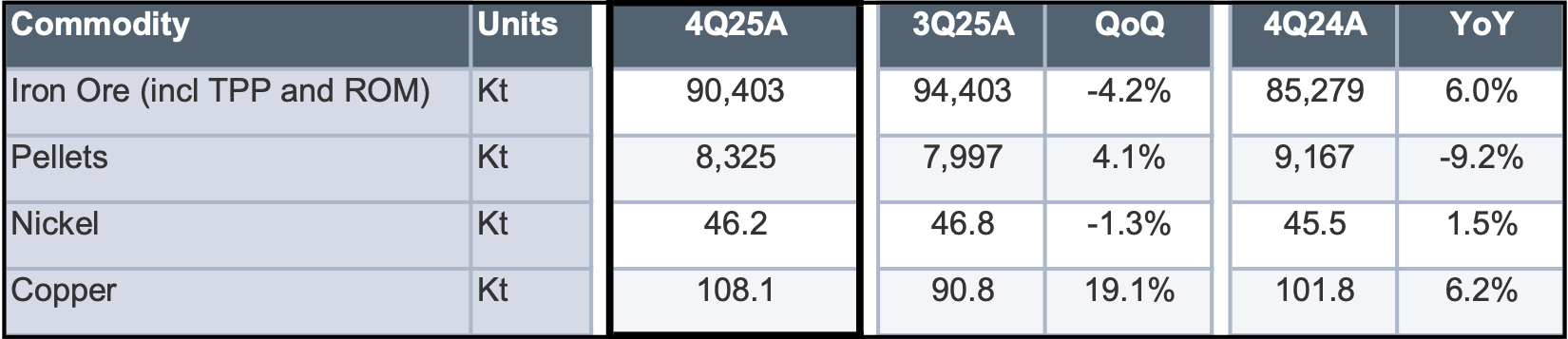

Vale’s fourth-quarter production results showed strong momentum, with volumes across all segments exceeding the revised full-year guidance. While iron ore sales were slightly below consensus, copper was a primary driver of growth, reaching its highest quarterly production levels since 2018. After the operational turnaround in 2025, we’re very optimistic about the stock. Fiscal 2026 guidance remains unchanged from the latest investor update.

1. Iron Ore: Multi-Year Production Highs

Quarterly iron ore production rose 6% YoY, largely meeting market consensus. This performance was supported by strong output at Brucutu and the continued ramp-up of the Capanema and VGR1 projects.

For the full year, iron ore production reached its highest level since 2018, with realized pricing for the quarter at $95.4/t. Operations in the Southern System were recently impacted by a sediment overflow at the Fábrica mine.

There were no injuries, but the local government has suspended operating permits at the Fábrica and Viga units. Guidance has not been updated following this event. Additionally, pellet volumes beat expectations, and annual production met the revised guidance of 31Mt.

2. Copper & Nickel Performance

Copper output surged 19% sequentially in 4Q, reaching a quarterly high not seen since 2018. This performance was driven by record-level operations at Salobo and steady output from Sossego and the Canadian assets. Total copper production significantly exceeded consensus expectations for the period. While nickel production also beat consensus, both output and realized pricing saw sequential declines.

Vale 4Q25 Production Results

Our View: Vale's recent share performance is driven in part by favorable macro tailwinds across the sector. The company's operational standing is also improving as it consistently hits iron ore targets and executes on its copper growth strategy in Brazil. This steady execution is expected to support a higher equity valuation over the long term.

Investment Thesis

The investment case for Vale rests on the premise that it has moved beyond its most difficult operational stretch to prioritize excellence and profitable growth. This shift indicates that the corporate narrative is turning the page on a period of remediation to refocus on core portfolio strengths. Management is now in a position to narrow the valuation gap between the current share price and the intrinsic value of these high-quality assets.

Vale at a Glance

Vale is a global mining leader and a premier supplier to the seaborne iron ore market. As the largest producer of iron ore and pellets, it also holds a significant position in nickel and maintains meaningful copper exposure through its base metals platform. Since its founding in 1943, Vale has operated an integrated business model that combines mining, logistics, and distribution to ensure cost efficiency and reliability of supply.