U.S. Unemployment Surges: Is AI to Blame?

We break down what February’s weak jobs report means for the U.S. labor market and why the slowdown may be broader than it first appears.

So, today, we finally got something to sink our teeth into that is not about Iran, Israel, US or oil and shipping. We got some bad FED Employment data.

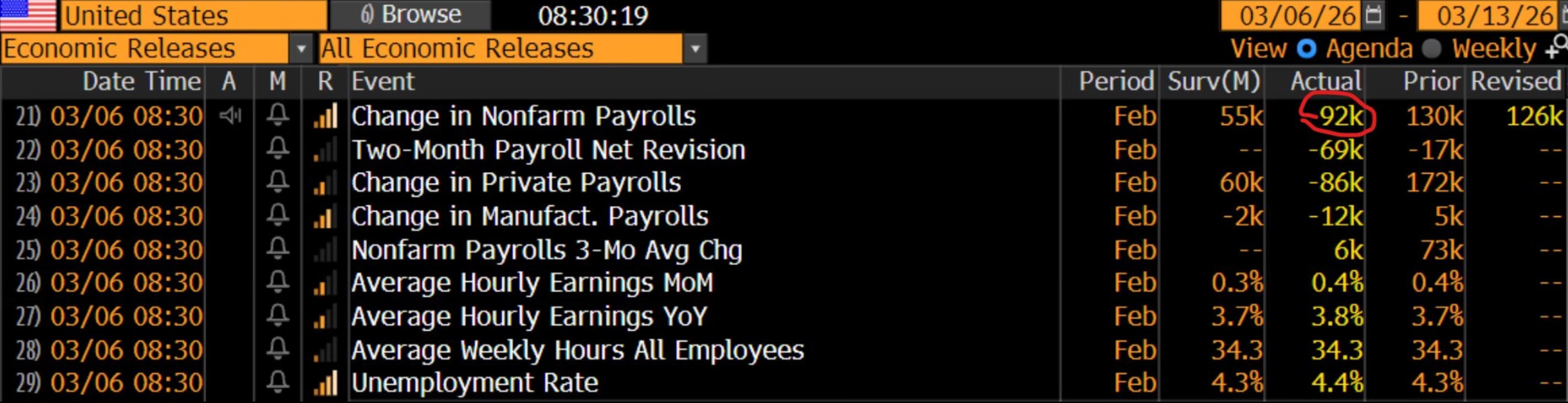

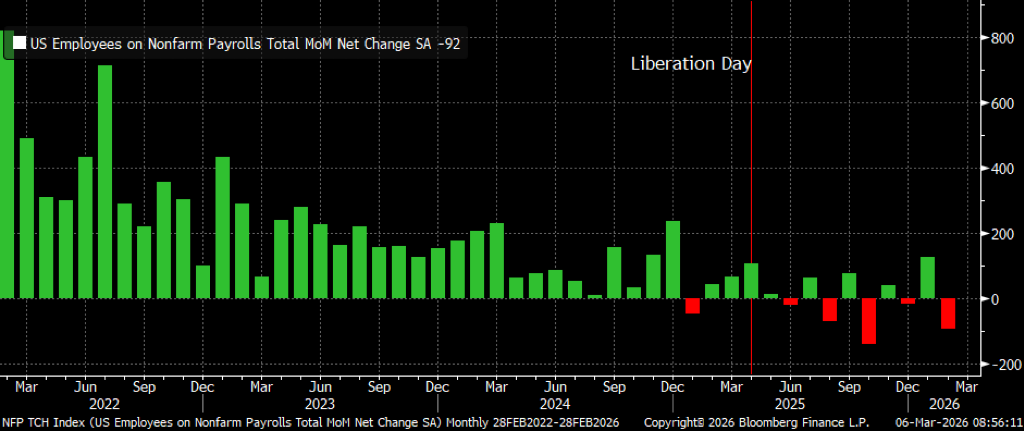

February’s employment report signals a definitive shift in the U.S. labor market. Payrolls fell by 92,000 as the unemployment rate rose to 4.4%, effectively reversing the optimism generated by January’s performance.

FED Employment Report

This data confirms the thesis for 2026 that hiring is now driven mostly by non cyclical sectors. When healthcare, education, and government are excluded, cyclical hiring across both goods and services has slowed meaningfully. While a localized healthcare strike removed 31,000 jobs that should return next month, the broader indicators are more concerning.

U.S. Employers Cut Jobs Unexpectedly as Unemployment Rises

Jobless claims during the February reference week were significantly higher than in January, which accurately predicted the upward pressure on the unemployment rate. Specific sectors are now flashing warning signs about the health of the broader economy. Manufacturing, transportation, and warehousing lost a combined 23,000 jobs.

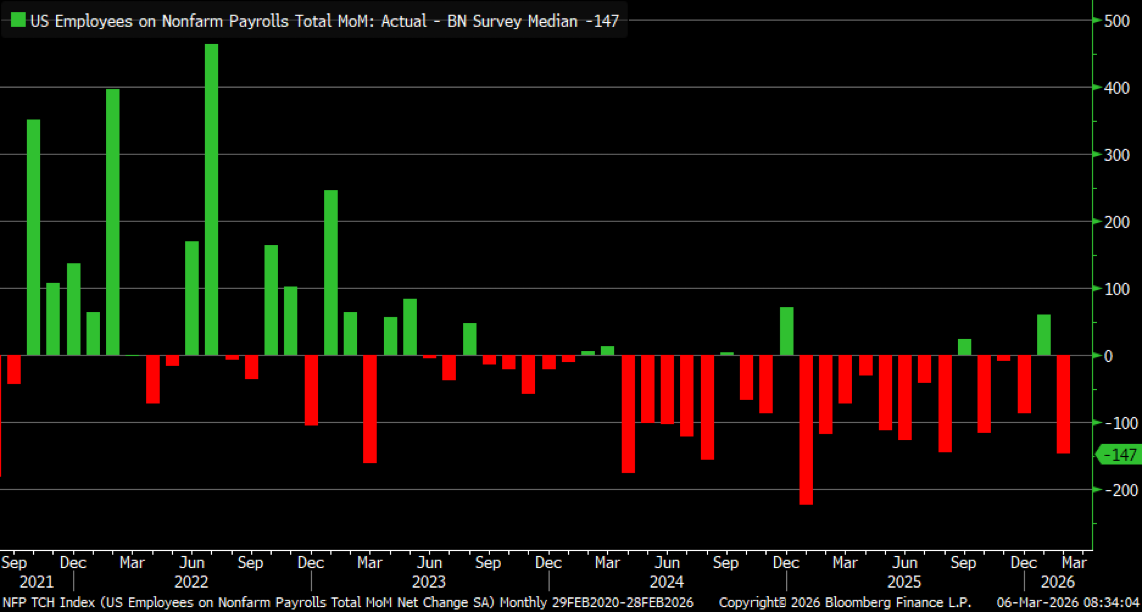

We believe the chart below adds to that message. Payroll releases are now coming in below consensus far more consistently than they did earlier in the cycle, and the magnitude of those misses has also increased. This is usually what labor market normalization looks like once it moves beyond moderation and begins feeding a more tangible loss of momentum.

Expectations are still catching down to reality.

U.S. Payroll Misses Are Becoming More Frequent

Temporary help services, which often serves as a leading indicator for industrial health, dropped by 6,500 jobs. Perhaps most telling is the decline in leisure and hospitality, a sector that has contracted in three of the past four months. We believe this suggests that discretionary spending is slowing even among higher income households.

The AI Disruption & Structural Shifts

The labor market is also facing a deep disruption from artificial intelligence. Recent productivity gains show how AI investments have allowed firms to operate with leaner staffing levels. Companies are increasingly following through on previously announced layoffs as technology automates routine tasks. This shift means that while net job openings are scarce, demand for highly specialized technical skills continues to rise. Workers are being pushed to become more specialized in an environment where many entry level and administrative roles are disappearing.

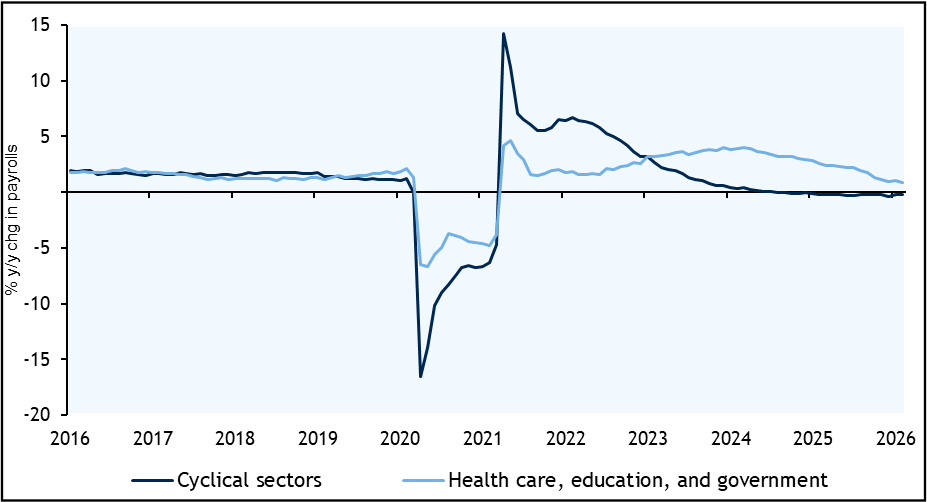

Cyclical Job Growth Lagging Structural Since 2023

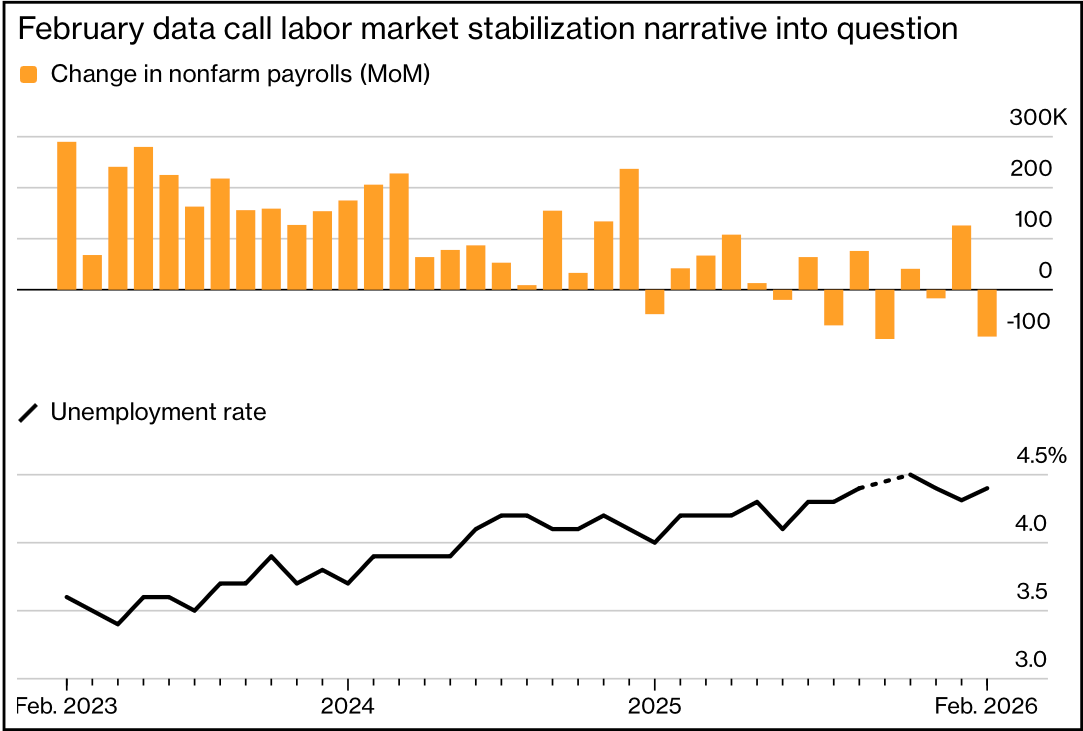

The data captures that deterioration clearly. Payroll growth has turned far more volatile and recently moved into negative territory, while the unemployment rate continues to push higher. The stabilization narrative that followed January now looks increasingly fragile. Labor demand is no longer broad enough to offset weakness across more cyclical parts of the economy.

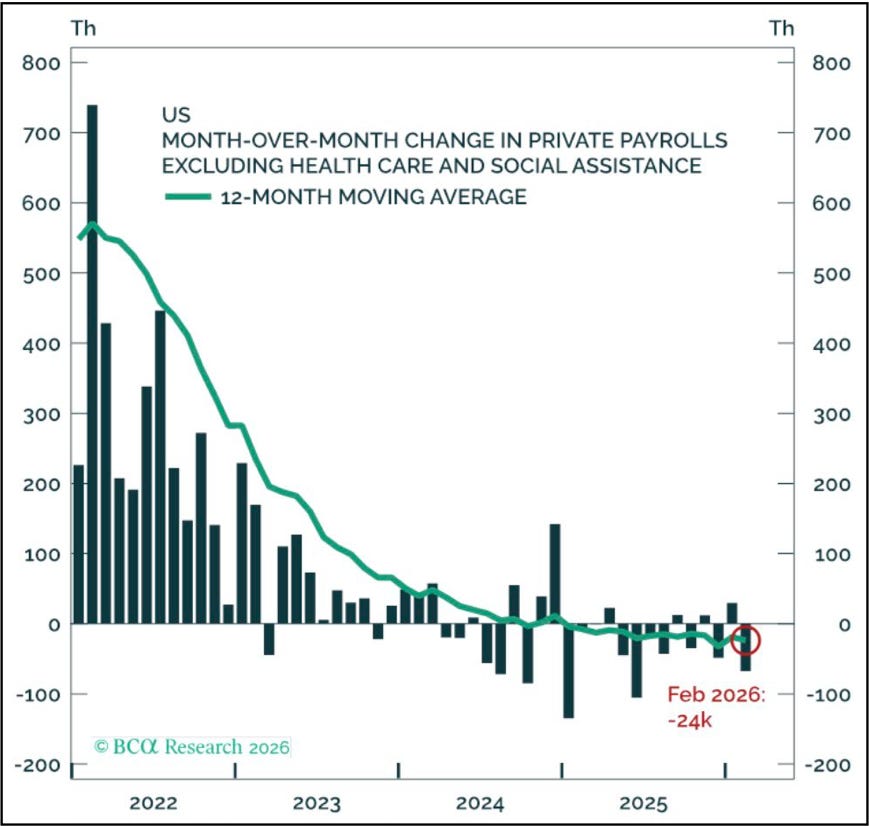

Since 2023, cyclical job growth has consistently lagged hiring in healthcare, education, and government. Much of the apparent resilience in the labor market has come from categories that are less tied to underlying private sector demand. Hiring tied to the economic cycle has been losing momentum for some time. Payrolls excluding healthcare fell by 67,400 in February, bringing the 12-month moving average down to -23,750.

U.S. Private Payroll Growth Ex-Healthcare Turns Negative

This reinforces the view that underlying private sector labor demand has been losing momentum for some time. When these structural buffers are removed, the vulnerability of the broader economy becomes clear.

The heavy concentration of growth in non-cyclical sectors means the labor market is increasingly unable to withstand even minor shocks, such as localized strikes or shifts in consumer behavior. We believe this divergence suggests that while the headline numbers may appear stable, the core engine of private sector employment is effectively stalling.

The New Normal for Labor Market Health

Recent population adjustments revealed that the labor force was smaller than previously estimated, overstated by around 1.4M people as of late 2025. This shift reclassified many individuals from unemployed to not in the labor force, largely due to 2M retirements in 2025. Because of this retirement surge and lower immigration, the breakeven employment level, which is the amount of new jobs needed to keep unemployment steady, is now exceptionally low.

That changes how payroll growth should be interpreted.

The labor market no longer needs the same pace of monthly job creation to keep the unemployment rate stable. In this environment, modest payroll gains are the new normal. We believe much of today’s hiring simply reflects retiree replacement, with limited net new job creation.

Payroll Growth Has Reset Lower

That shift is now visible in the payroll data itself. Monthly job creation has slowed sharply from the levels seen in 2022 and 2023, with recent prints clustering around much lower levels and at times slipping into negative territory. Labor demand has not collapsed, but it has clearly reset to a weaker range. That is also why the unemployment rate is becoming a more accurate gauge of labor market health than the headline payroll number alone.

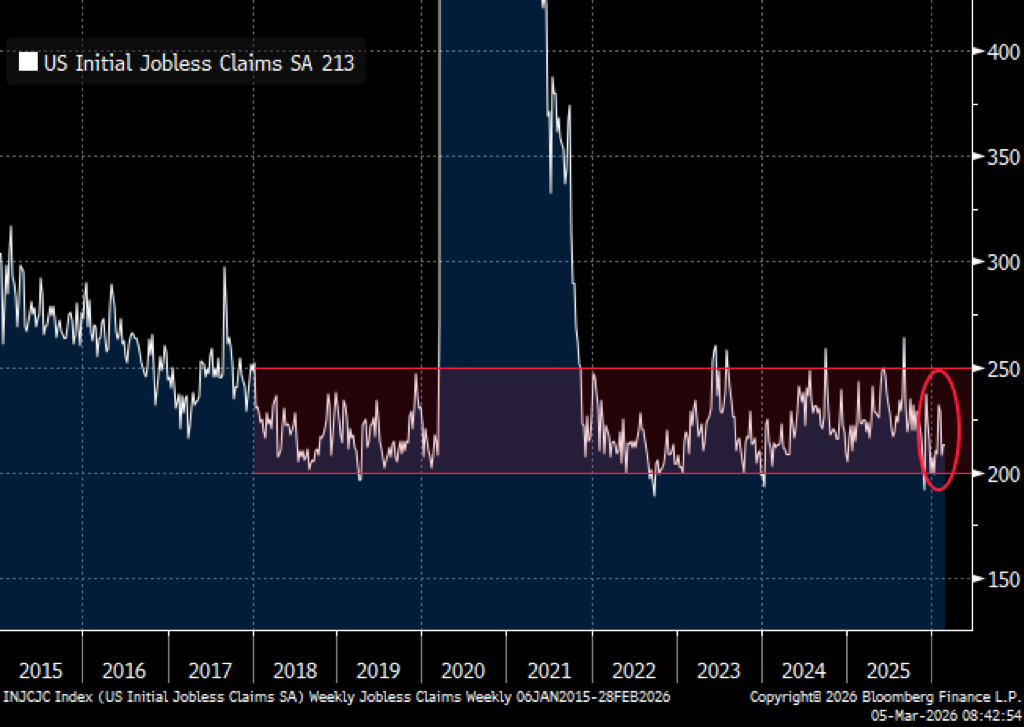

Initial Jobless Claims Are Moving Back Into Warning Territory

The claims data reinforces that message. Initial jobless claims have moved back toward the upper end of their post-2022 range, suggesting layoffs are no longer as contained as they were earlier in the cycle. Claims remain well below recessionary levels, but the recent move is enough to indicate that labor market conditions are becoming less stable at the margin.

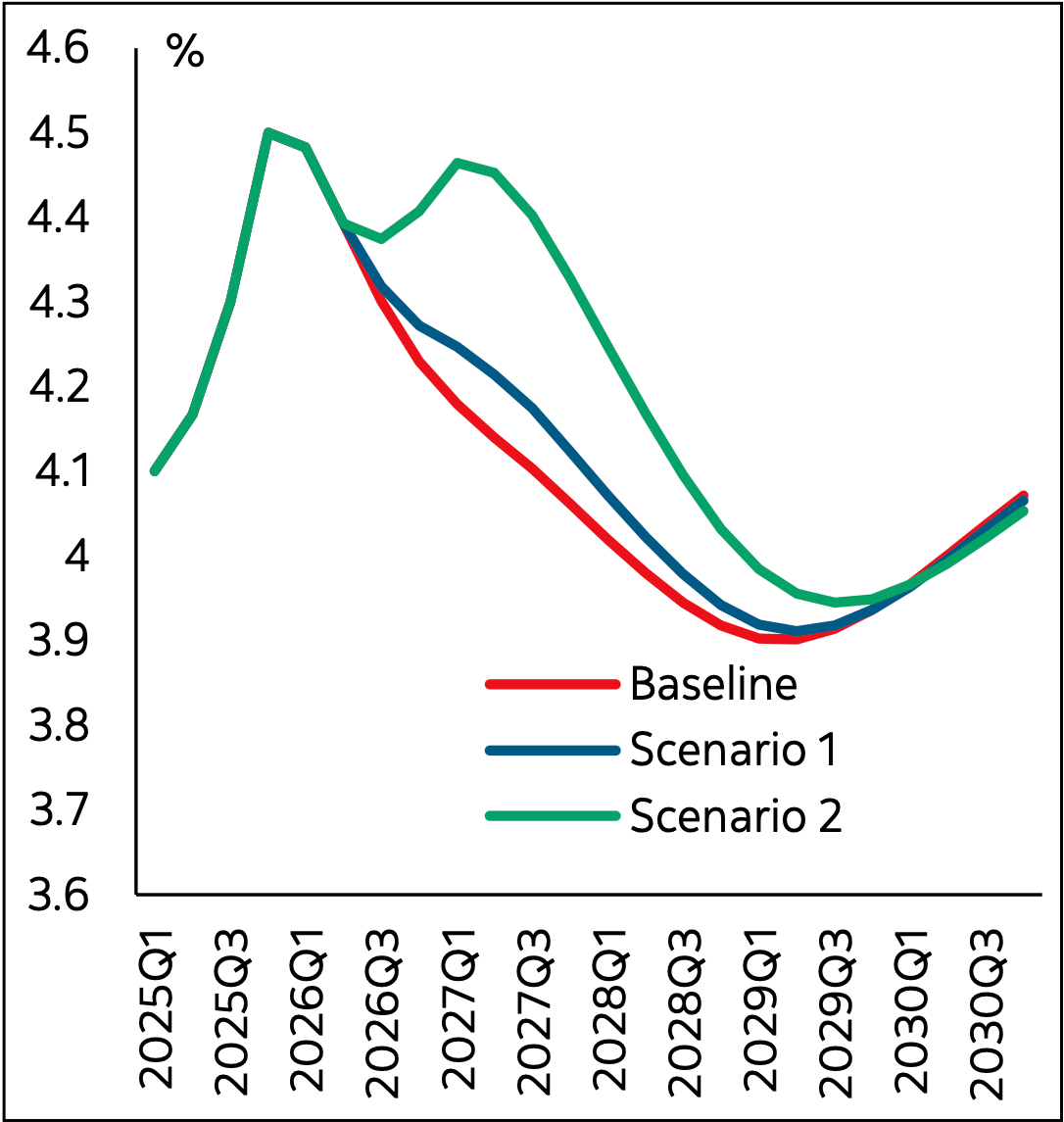

Scotiabank’s unemployment scenarios point in the same direction.

Even under a baseline outcome, the unemployment rate remains elevated through 2026 before improving only gradually. The alternative scenarios suggest a labor market with limited room for disappointment and a recovery path that could prove slower than consensus still expects.

U.S. Unemployment Rate

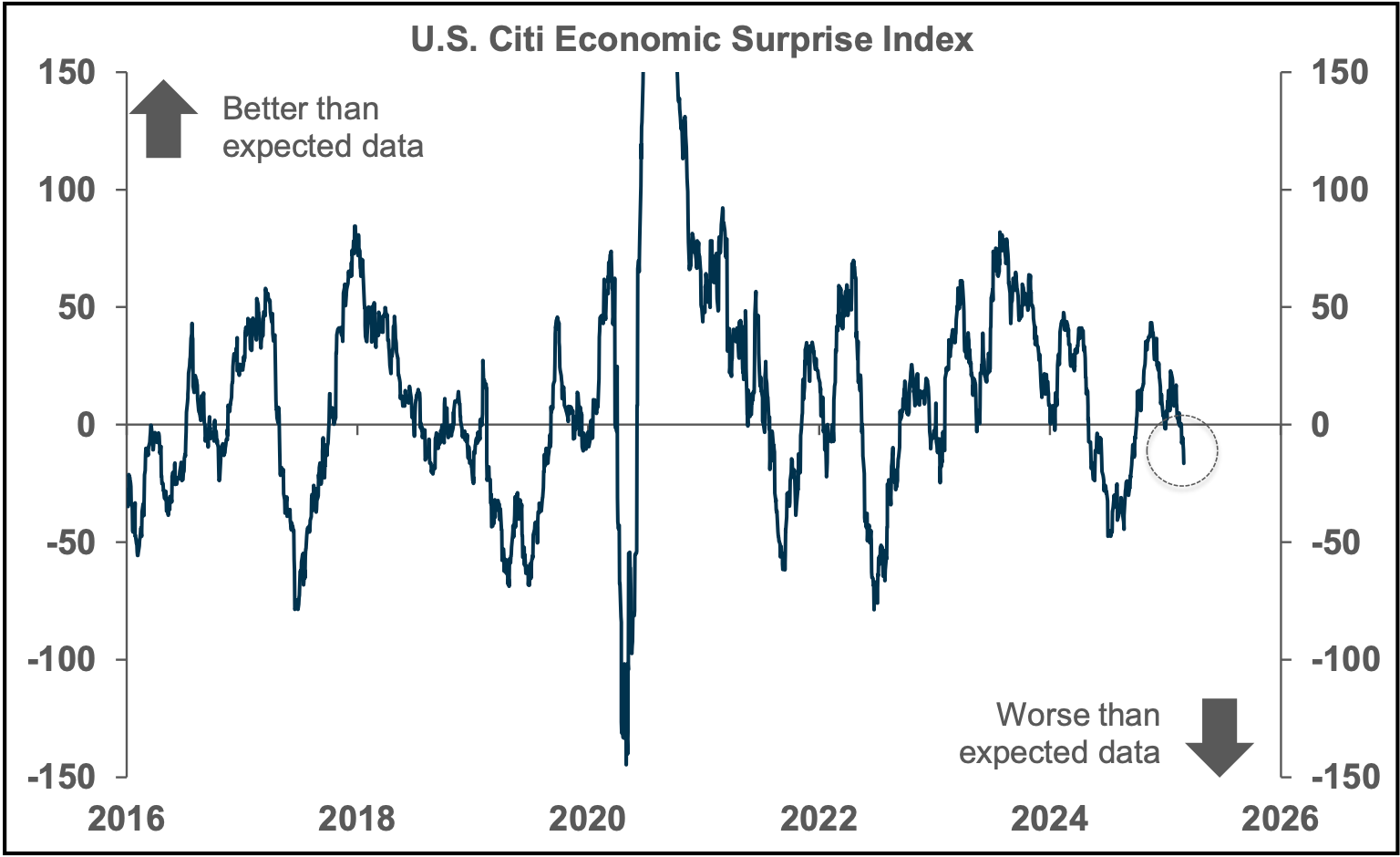

U.S. Economic Data Is Starting to Disappoint

The U.S. Citi Economic Surprise Index has moved back into negative territory, showing that incoming data is increasingly coming in below expectations. The weakness in the labor market is now being echoed more broadly across the economy, pointing to a backdrop that is losing momentum and becoming less supportive than it appeared only a few months ago.

Taken together, these indicators suggest that the February employment report was not a one month anomaly. It looks more like part of a broader slowdown in hiring, cyclical demand, and overall labor market momentum.

While the U.S. economy is still creating jobs in specific areas such as healthcare and government, we are starting to see a broader picture that is becoming more selective and more fragile. The current trajectory looks less supportive than it did just a few months ago and leaves the economy more exposed to further disappointing data releases.

The Aurelion Team

Disclosures & Methodology