Uranium Primer: The Nuclear Renaissance Powering AI

Macro policy is finally turning, and AI-driven power demand is accelerating. We expect uranium prices to rise and identify several ways to benefit.

Uranium is quickly becoming one of the world’s most important commodities again, and we have a strong conviction on where the market is headed.

We start from the ground up, explaining the industry and its dynamics so anyone can get up to speed. We then dive into what matters, where we believe the industry is heading, and how to benefit through actionable stock ideas, including a new portfolio addition in the Aurelion Index.

Why uranium today? With the rise of data centers, AI, quantum, and everything around it, power demand is going up fast. We think we’re going to face a real shortage sooner than later. The issue is simple: we don’t yet have the capacity to produce enough energy, especially clean energy, to support what’s coming.

Uranium has been hated for a long time. In Europe especially, nuclear energy is still very unpopular among politicians, which, in our view, makes little sense given the situation. A lot of it comes from past incidents like Chernobyl, which still shape how people think about nuclear today. But that was in 1986. We are now in 2026, and technology has evolved a lot since then.

The Chernobyl Disaster (April 26, 1986)

At some point, that fear starts to look overdone. If we are serious about meeting future energy demand without relying on coal and oil, nuclear has to be part of the conversation. It is also a very competitive source of power on a cost basis.

The laws of thermodynamics do not negotiate. Every step forward in human progress has demanded more energy. A smarter world is a hungrier one, and uranium is among the most energy-dense fuels on Earth.

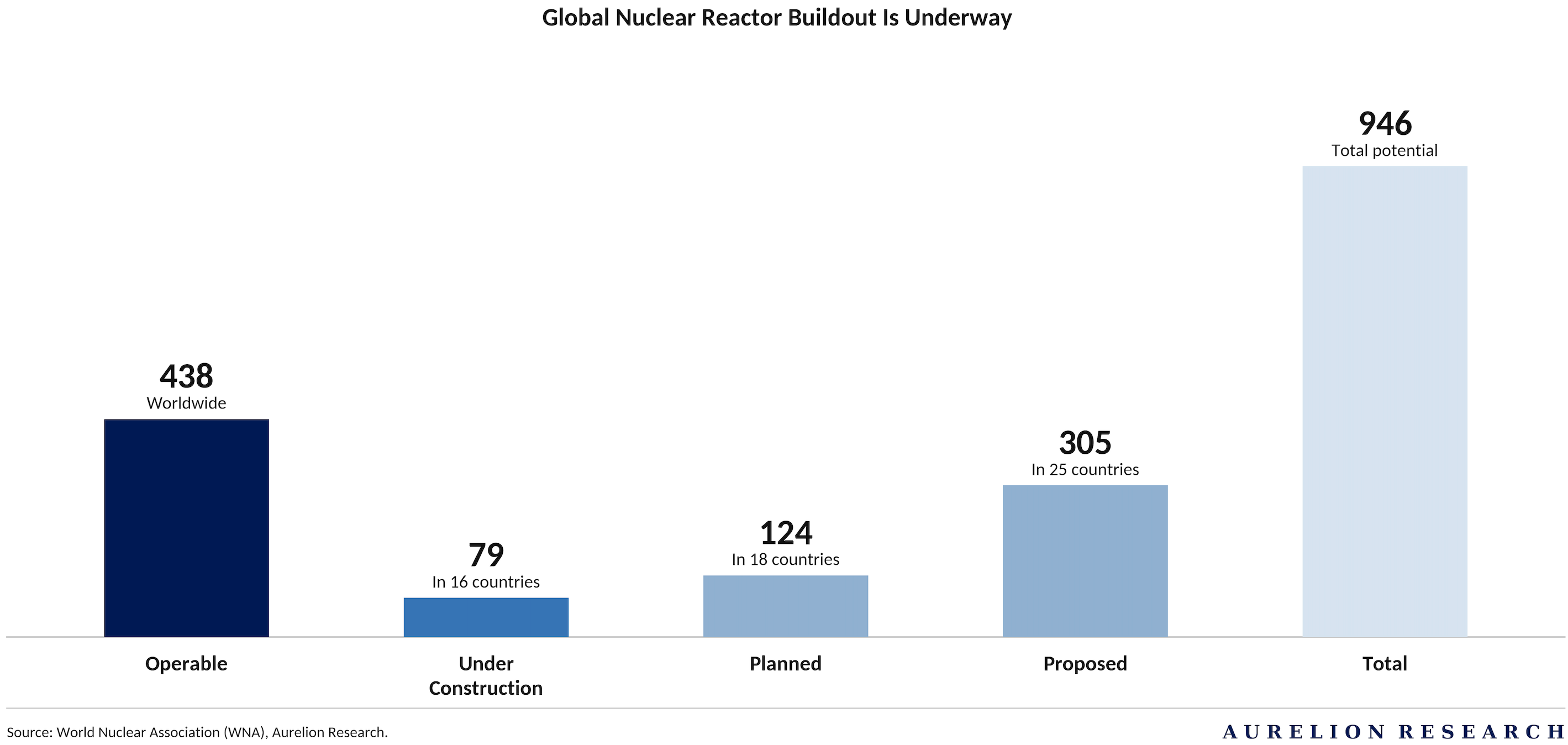

There are around 438 nuclear reactors operating worldwide today, and the vast majority run reliably without major issues. This already shows that nuclear technology is well proven and significantly safer than it was decades ago. The kind of disaster we saw in the past, like Chernobyl, is now extremely unlikely with modern reactor design and safety standards.

Table of Contents

Introduction

Why Uranium, and Why Now?

1.1 The Timing Looks Right

1.2 Supply Can’t Keep Up With Demand

1.3 The AI Electrification Boom

What Is Uranium?

2.1 Origins & Physical Traits

2.2 The Power Of Uranium

2.3 The Lifecycle of Uranium

Nuclear Energy 101

3.1 Inside the Power Plant

3.2 Reactor Types in the U.S.

Uranium Global Demand Outlook

4.1 The U.S. Needs More Nuclear Power

Uranium Global Supply Outlook

5.1 The Supply Story Will Break

Who Are the Big Players?

6.1 Cameco (Canada)

6.2 Kazatomprom (Kazakhstan)

Where Uranium Prices Are Headed Next

Our Favorite Stock Ideas

8.1 Uranium Stock: Top Idea #1

8.2 Uranium Stock: Top Idea #2

A Look at Uranium Energy Corp. (UEC)

Why Only Nuclear Meets AI’s Power Requirements

10.1 Nuclear vs Solar: The Reality of Scalable Power

What About Kazakhstan?

Key Risks to the Bull Case

Our Final Take on Uranium Market

1. Why Uranium, and Why Now?

Uranium has been a recurring theme over the past decade. It used to be dead money, but since 2020, uranium stocks have surged, with most major companies delivering around 5x returns and some junior miners closer to 10x.

1.1 The Timing Looks Right

Timing is everything in commodities. We have spent years building our framework that spans multiple asset classes, precisely because staying broad keeps us from getting attached to any single trade. Specialists who live and breathe one commodity tend to be perma-bulls on it, and that bias costs them.

Our approach is to rotate and wait for a setup that’s actually turning before committing capital. Getting in too early is one of the most common mistakes in this space. It ties up money for years in trades that go nowhere, and in some cases, the thesis never plays out at all.

With uranium, the re-rating has already begun.

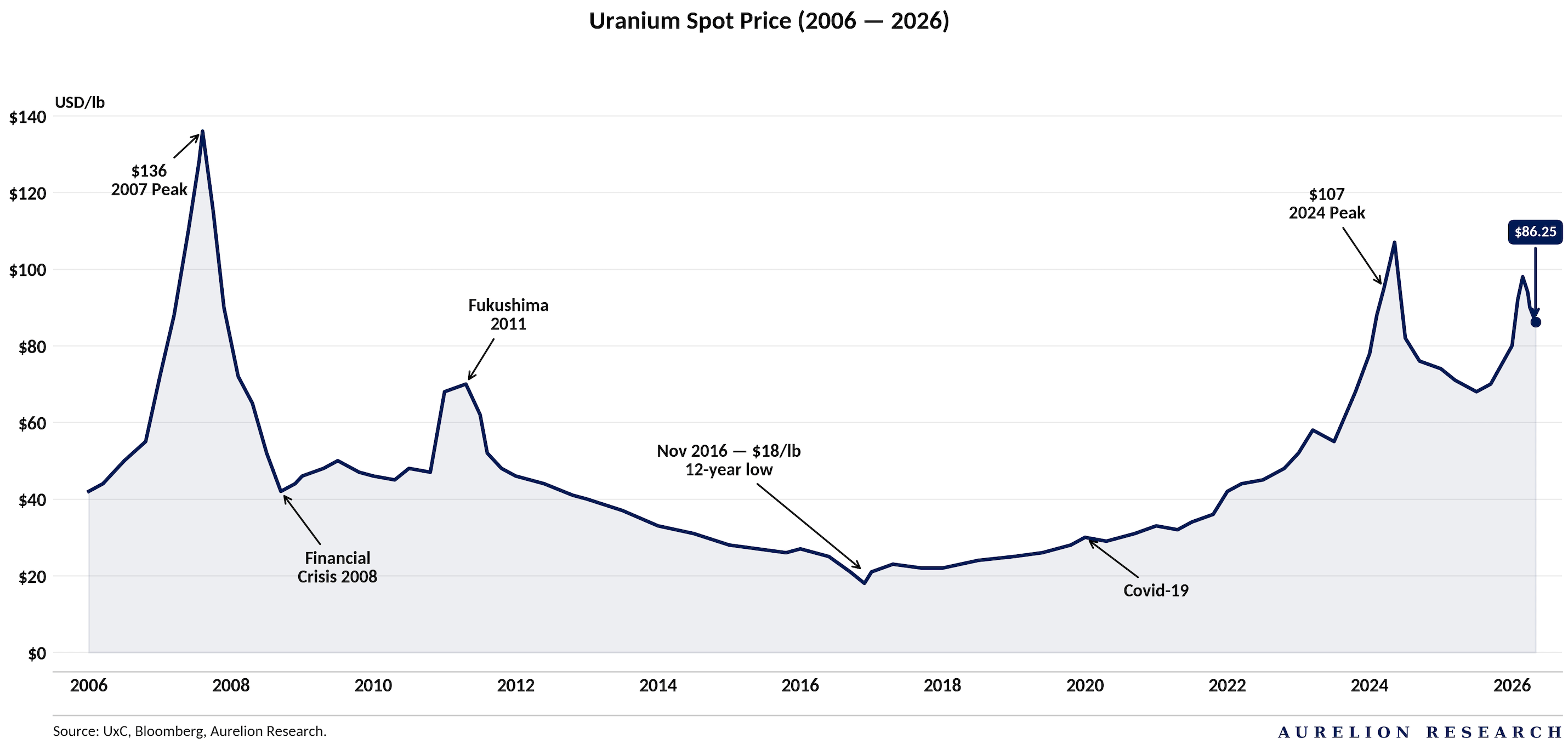

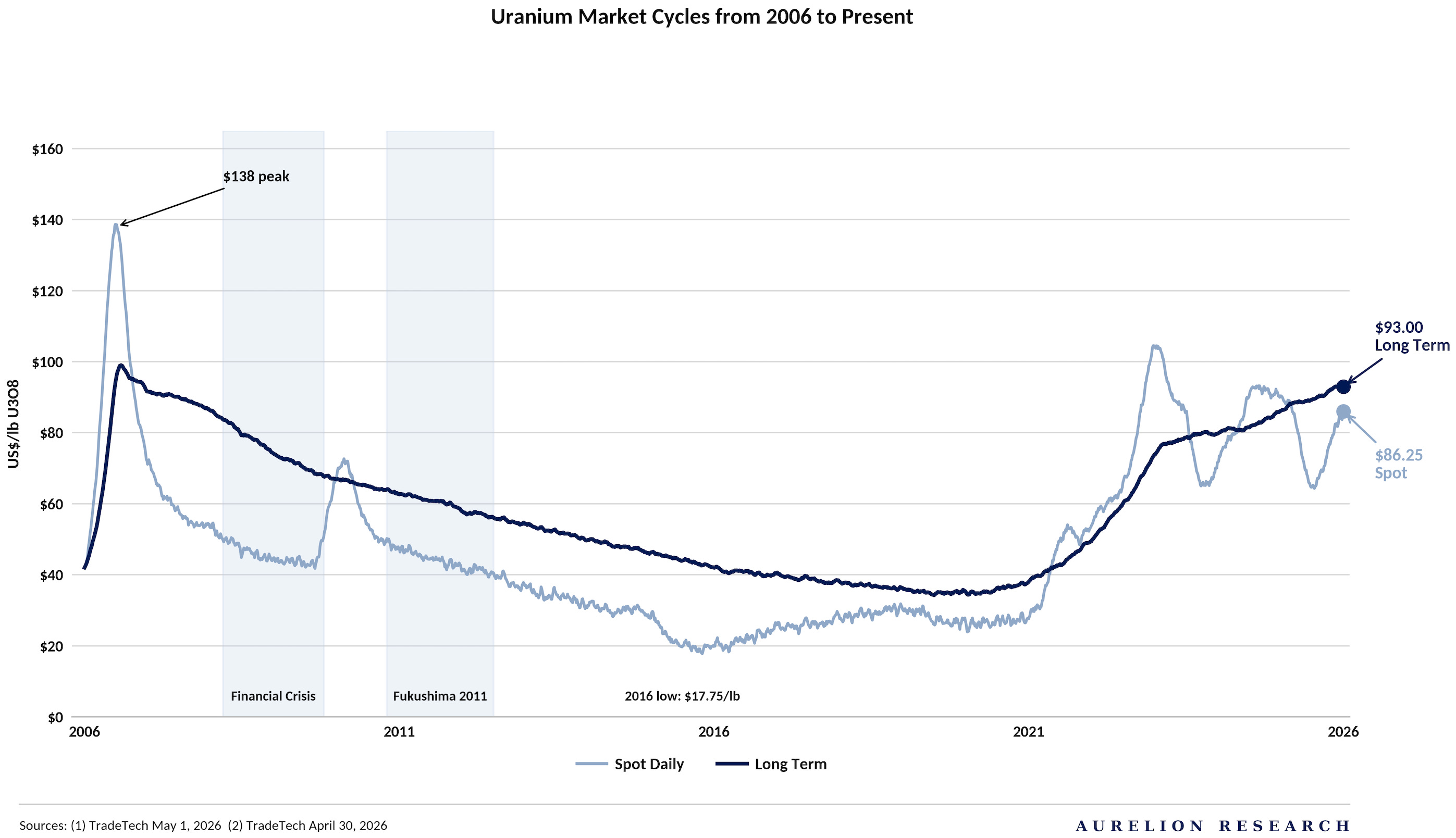

Those who waited for momentum to build between 2023 and 2024 have seen strong performance as the spot price moved toward the $90 level. On the other hand, investors who bought during the 2014 to 2021 period had to endure a long stretch of weak price action, including the 2016 low at $17.75 per pound.

The chart also shows how different the current cycle is compared to past peaks. The 2007 spike to $138 was fast and was followed by a long decline through the financial crisis and Fukushima. So far, the current cycle has been more gradual, with a steadier recovery over time.

As of May 2026, the long-term price sits at $93.00, with the daily spot price at $86.25. We believe this strength reflects a tighter balance between supply and demand, driven by the energy transition and rising power demand from AI.

That does not mean the move is over or that the opportunity is gone, far from it. The sector has clearly turned, with capital starting to follow after years of neglect. Policy support has also strengthened, with the U.S. government openly backing nuclear energy and domestic supply, reinforcing its strategic importance.

1.2 Supply Can’t Keep Up With Demand

The primary driver for the uranium market is the rapidly growing global demand for power. Even before the current tech boom, the shift toward carbon-free energy had already led to a wave of new nuclear plants being announced and brought under construction. While the outlook was already strong, the rise of artificial intelligence has increased the scale of energy demand significantly.

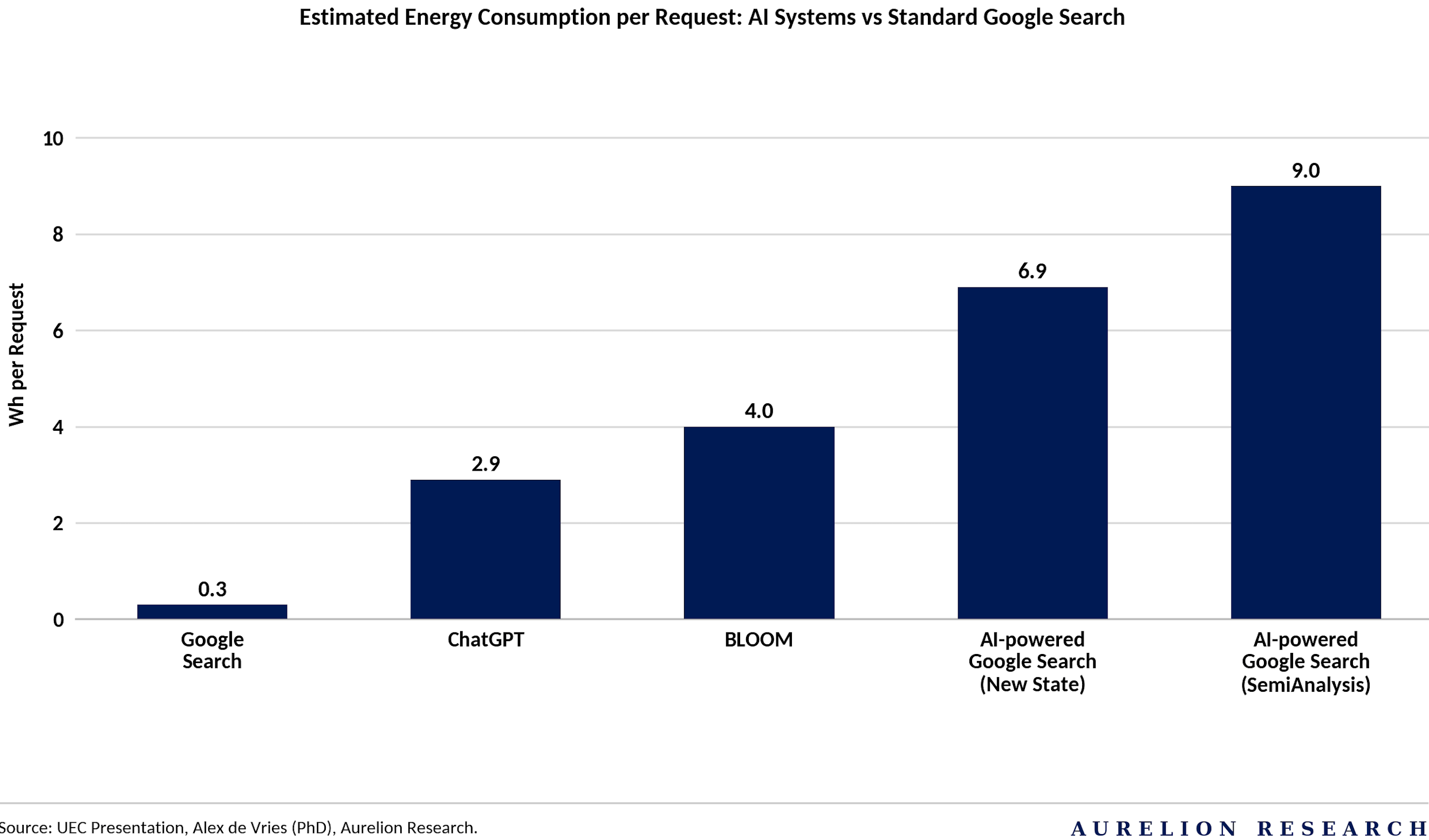

The following chart on energy consumption per request illustrates this gap clearly. A standard Google search requires about 0.3 watt-hours per request, while an AI-powered search can reach up to 9.0 watt-hours. That is a significant step up in energy intensity as these systems become more integrated into everyday use.

This surge in AI intensity is translating into much higher electricity demand. Data center power consumption alone is expected to rise by ~165% by 2030, creating a strong need for reliable, around-the-clock power. Nuclear is one of the few carbon-free sources that can provide this level of consistent output, which is why the imbalance between supply and demand in uranium continues to widen.

Nuclear is not power that can be turned on and off.

It must be constant, and intermittent sources cannot meet that requirement on their own. As a result, large technology companies are stepping in directly, funding the restart of older nuclear plants and building data centers next to reactors to secure a stable, always-on supply.

On a global scale, nuclear capacity could reach nearly 1,446 GW by 2050 if government targets are met, surpassing the goal of tripling capacity set at COP28. While this reflects a massive expansion, achieving these targets will require more than ambition as the industry scales to meet future energy needs.

This expansion, which is expected by almost every analyst, involves extending the operational life of existing reactors, in some cases up to 80 years, while also building new plants at scale. It also requires the deployment of small modular reactors and the advancement of next-generation technologies like fusion.

In our view, the most likely path forward: demand continues to rise, supply must follow, and nuclear is one of the few sources capable of closing that gap.

As noted earlier, nuclear energy is currently in a strong phase, with AI expected to further increase global demand. However, the market does not yet fully reflect this growth, which suggests we are neither too early nor too late in the cycle. In our experience, that often represents one of the more attractive points for positioning before the broader market prices in the shift.

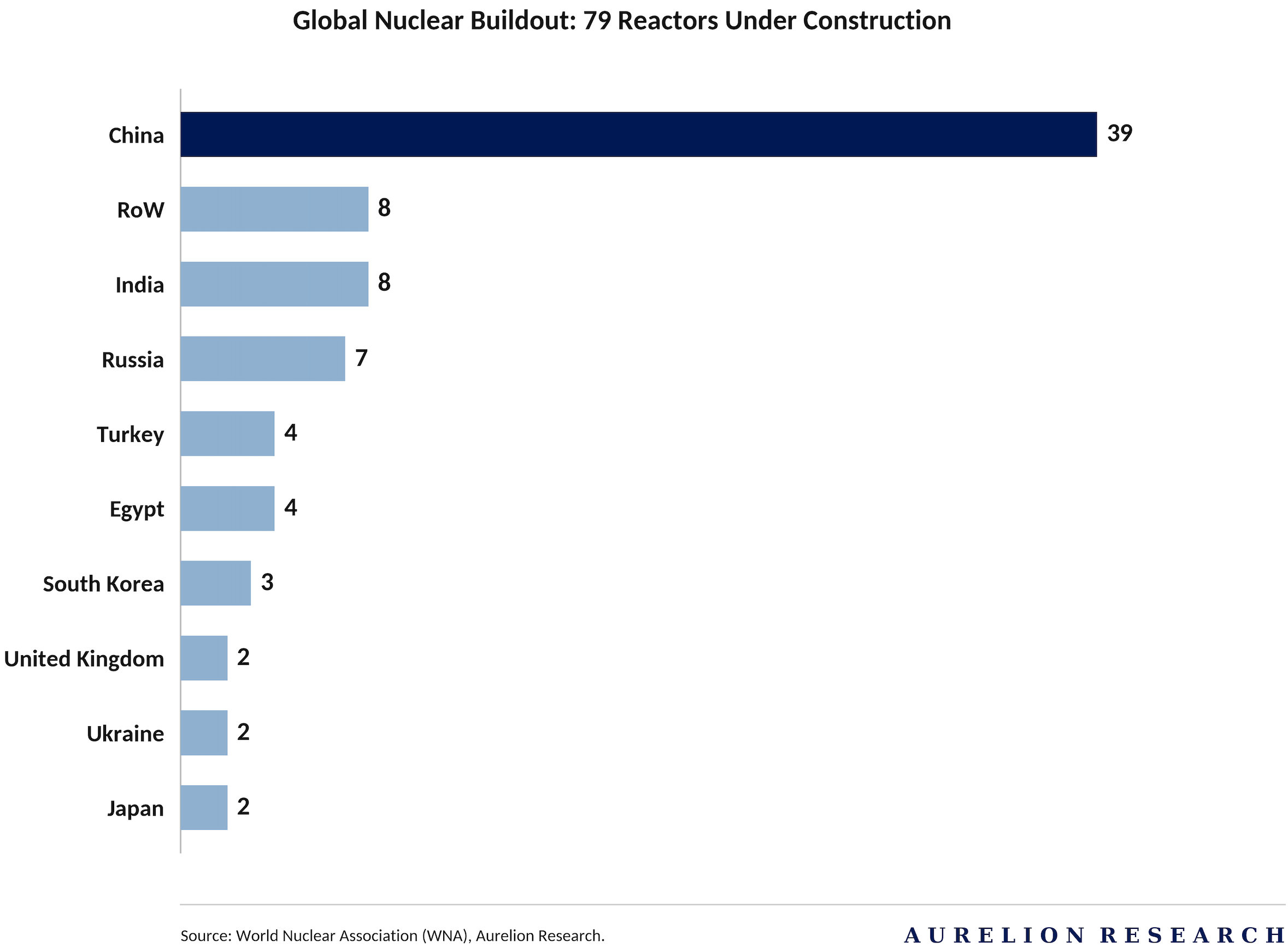

According to the World Nuclear Association (WNA), there are currently around 79 reactors under construction worldwide, expected to add 86 GW of new capacity. This would result in an estimated 21% increase in global capacity by 2030, which implies an additional ~43M pounds of uranium demand annually.

But we believe this is only the beginning.

More than 39 countries have stated ambitions to triple nuclear capacity by 2050, from about 380 GW today to nearly 1,446 GW. That implies close to 1000 GW of additional capacity over the coming decades. These are long-dated forecasts, and while 2040 or 2050 can feel far away, even the 2030 timeframe is much closer. And even there, we are still going to need significantly more uranium.

The key point is that all of this new capacity will require significant uranium supply. If AI-driven electricity demand in the U.S. were to be met entirely by nuclear power, which is unlikely but illustrative, it would require up to 60M pounds of uranium annually by the end of the decade.

1.3 The AI Electrification Boom

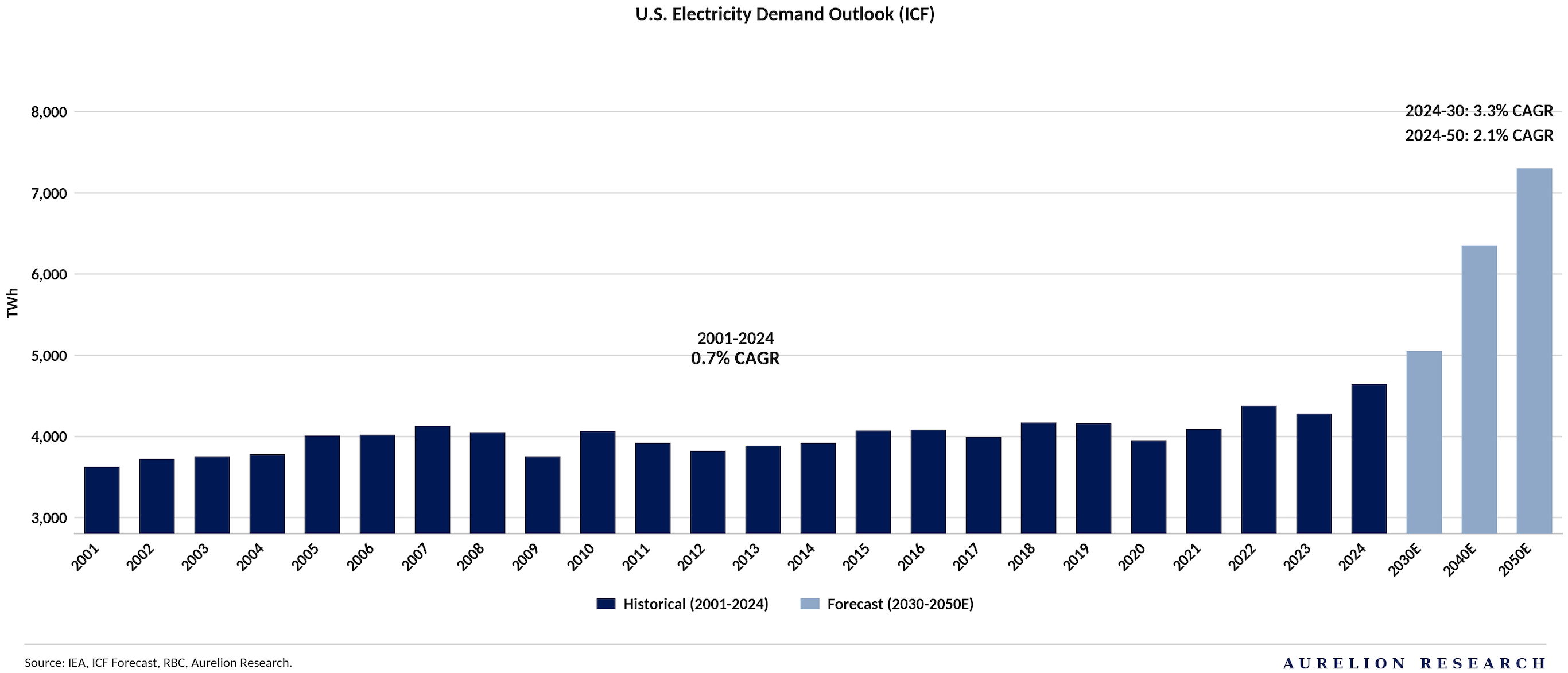

We are currently seeing energy providers revise their demand forecasts more frequently than in the past, which we think reflects the urgency of the rising need for nuclear power to support the electrification boom we are experiencing, both in the U.S. and globally. Looking at the exhibit below, we can see that the U.S. electricity demand outlook data from ICF looks pretty clear, it’s going higher.

Now, to match demand, supply will of course need to follow.

The rise of AI and the electrification of key sectors globally is making past forecasts increasingly outdated. Growth is accelerating, and demand is moving to levels we have not seen before. In AI in particular, where data centers require massive and constant amounts of power, the increase is already material.

Nuclear energy stands out in this environment. It is far less exposed to disruption than natural gas or oil, and it requires far less land than wind power.

It is a source of power that provides stable, reliable baseload electricity, which is exactly what the system increasingly needs. It is also a low-carbon source of energy, meaning it can play a direct role in meeting global climate targets.

At the same time, the technology itself is evolving. Advanced nuclear designs are emerging that were not available in the past, including smaller and more flexible reactors built for this new energy landscape, most notably small modular reactors.

We’ve done our best to make the following sections as accessible as possible. However, you don’t need to be a uranium expert to follow the thesis or to benefit from it.

2. What Is Uranium?

Uranium is a heavy metal that has served as a powerful, concentrated energy source for over sixty years. It is much more common than people realize, appearing in most rocks at about the same frequency as tin or tungsten. It even exists in our oceans, where it can be recovered directly from the seawater.

2.1 Origins & Physical Traits

This metal was formed billions of years ago during massive star explosions called supernovae. While it is rare in space, the heat produced by uranium decaying naturally is actually the main reason the inside of the Earth stays hot. This internal heat is what drives the movement of our continents.

Uranium is extremely heavy, about 18.7x denser than water. Because of its density, it has uses beyond energy. It can be used as added weight in ships, as counterweights in airplane wings, and as protection against radiation.

2.2 The Power Of Uranium

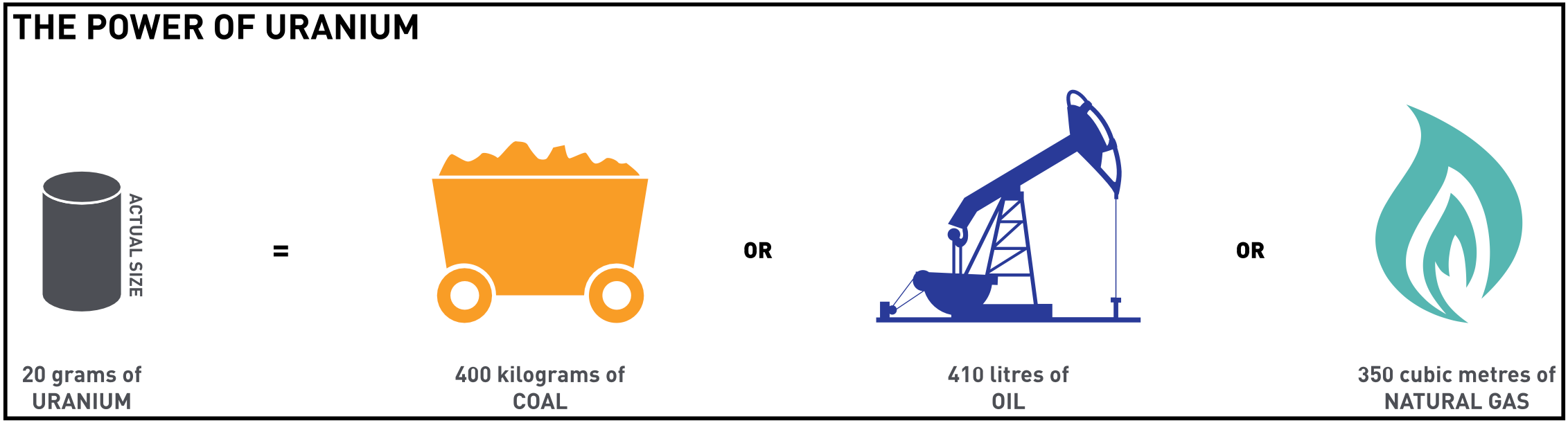

Nuclear fuel is extremely energy-dense, so a reactor needs very little of it. Uranium pellets weigh about 20 grams each, slightly less than an AA battery.

Fewer than 10 pellets can power the average Canadian home for a year. To produce the same amount of electricity, you would need about 410 litres of oil or 350 cubic metres of natural gas, showing just how energy dense nuclear fuel is.

2.3 The Lifecycle of Uranium

Uranium is a heavy metal that provides a concentrated source of energy. It is about as common in the Earth’s crust as tin and was formed billions of years ago in exploding stars. The process of turning this metal into electricity involves several steps and industrial processes, collectively known as the nuclear fuel cycle.

Nuclear Fuel Cycle:

Refining the Raw Material

The journey begins when uranium ore is mined and refined into a solid material called yellowcake. To prepare this for a reactor, the solid yellowcake is converted into uranium hexafluoride gas.

This gas is spun in large machines to enrich it, which increases its efficiency by concentrating the most powerful parts of the metal. Once this step is complete, the gas is processed into a black, powder-like substance called uranium dioxide.

Manufacturing the Fuel

The final transition from powder to power involves precise mechanical steps:

The black powder is squeezed together and heated until it forms small, hard cylinders known as uranium pellets.

These pellets are stacked one by one into long tubes made of metal.

Many of these filled tubes are bundled together to create a fuel assembly.

Energy Production & Recycling

These assemblies are the primary source of energy for a nuclear reactor. They are placed inside the heart of the power plant, where they provide the heat necessary to produce steam and electricity for years at a time. Once the fuel has been used, it is removed and stored to cool down. At this stage, it can either be recycled to extract remaining uranium for future use or disposed of safely as waste.

3. Nuclear Energy 101

Nuclear energy is a power source derived from uranium, a heavy metal found in rocks and seawater. It produces electricity through fission, where splitting atoms releases large amounts of heat. Although the science is advanced, the plant works much like a coal facility, using heat to boil water into steam that spins a generator.

3.1 Inside the Power Plant

A nuclear power station functions much like a coal or gas plant because both systems use intense heat to boil water and produce steam. That steam then spins a turbine to generate electricity. The main distinction is that a nuclear plant uses the energy from splitting atoms instead of burning fossil fuels to create that heat.

Inside the Core of a Nuclear Reactor

3.2 Reactor Types in the U.S.

In the US, most facilities are light-water reactors, which use normal water to manage the reaction and keep the system cool. The most common design is the pressurized water reactor (PWR), shown below, which pumps water into the core under high pressure to prevent it from boiling. This hot water travels through tubes to heat a separate water system, creating the steam for the generators.

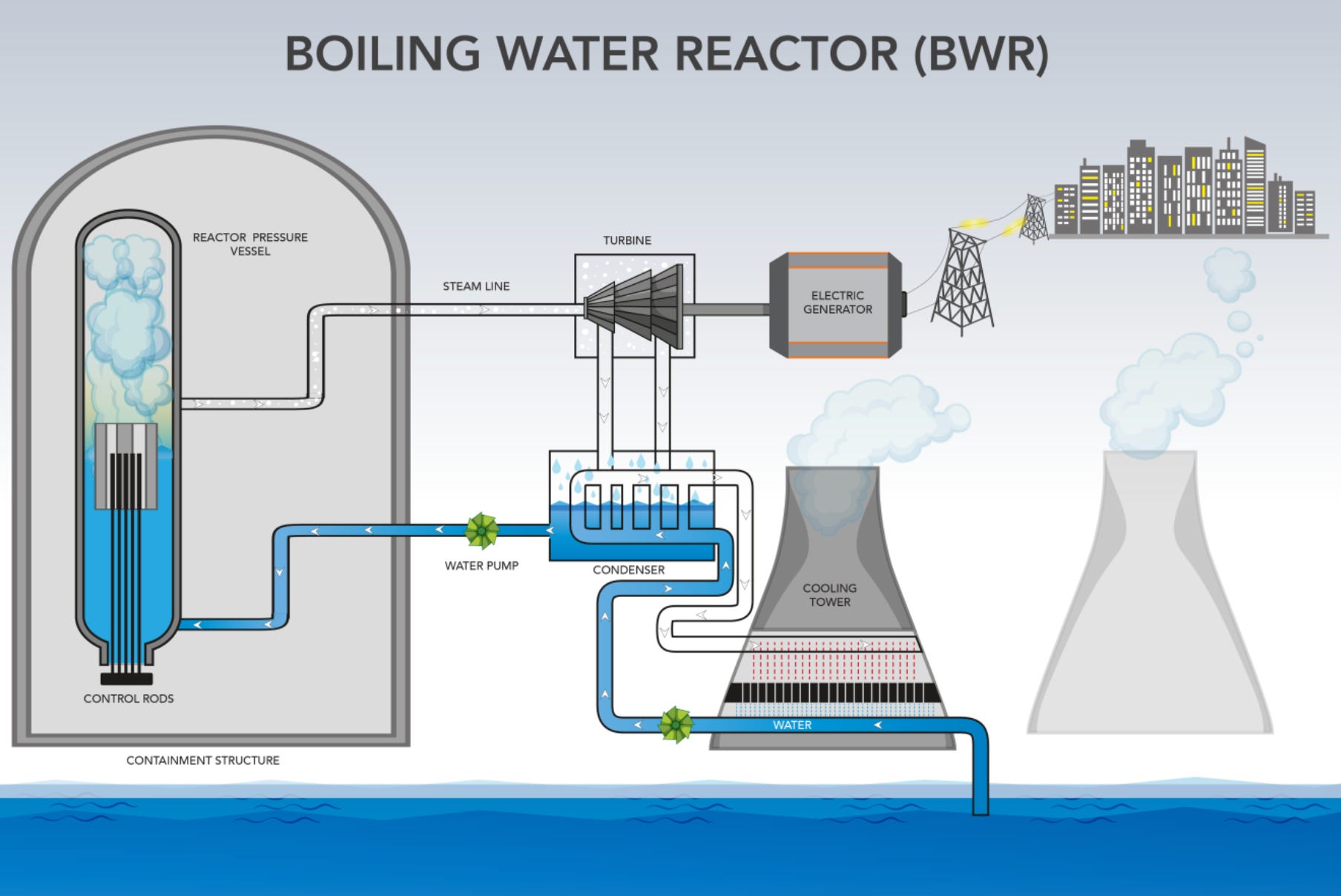

Another design, the boiling water reactor (BWR), allows the water to turn into steam directly inside the reactor vessel, as illustrated below.

To keep these systems steady, engineers use control rods to soak up particles and slow the reaction, while moderators like water or graphite ensure the process moves at the right speed. The fuel itself is designed so that it is physically impossible for the reactor to explode like a weapon.

The thing to remember: One single large reactor can produce enough electricity to power a city of a million people, which just proves how crazy it is that we do not use this highly efficient source of energy, and that governments are still reticent to use it more.

4. Uranium Global Demand Outlook

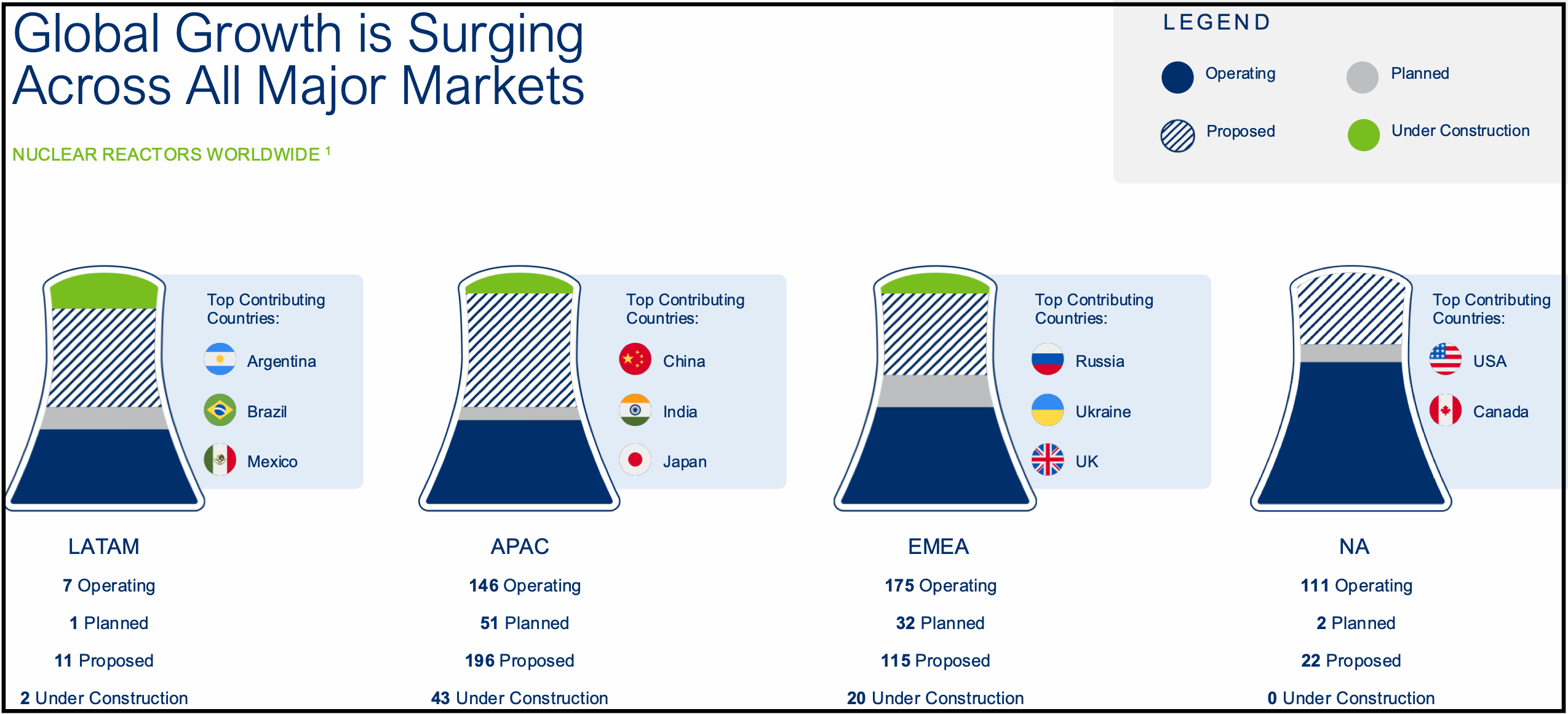

At this point in the report, it should not be a surprise that global growth is accelerating across all major markets for nuclear reactors worldwide, and we think the exhibit below illustrates it clearly.

What we are seeing is happening globally. Reactor growth is surging across every major region, led by APAC and EMEA, which have been the most active in terms of new builds, planned units, and reactors under construction. But we believe what makes this moment particularly significant is that North America (NA) is now re-entering growth mode after a long period of stagnation.

That is a major shift. For years, the conversation around nuclear in NA was largely about keeping existing plants alive. Now we are talking about new capacity coming online, and that changes the demand picture meaningfully.

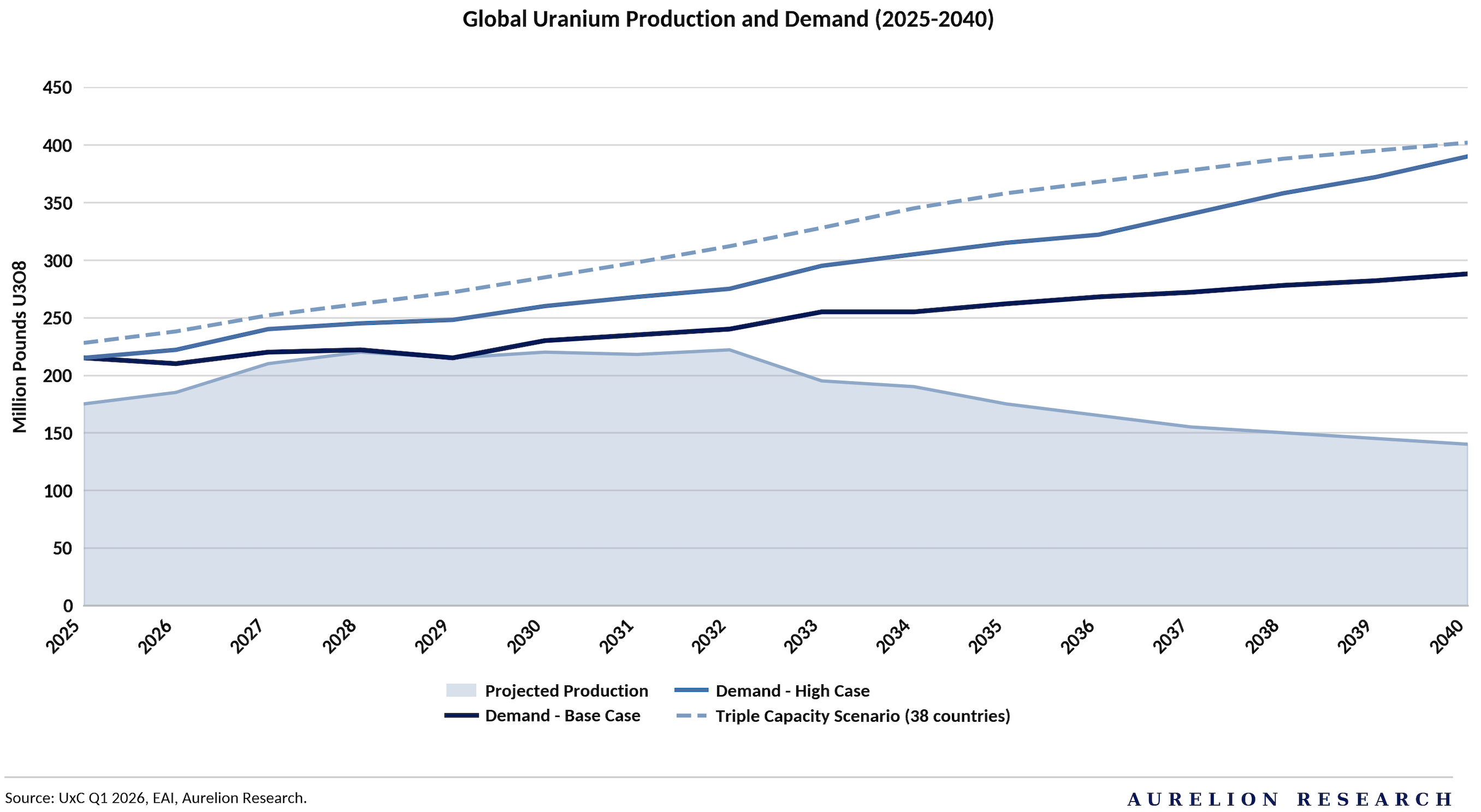

Now, let’s look at what this means for uranium. According to UxC, global nuclear capacity is expected to triple by 2050, driven by 38 countries committing to expansion. That is not a fringe scenario, that is the stated ambition of nearly four dozen nations moving in the same direction at the same time.

What stands out is the widening gap between projected supply and demand. Production, shown in green, is expected to peak in the mid 2030s before declining sharply, falling to roughly 130 to 140M pounds U3O8 by 2040.

Meanwhile, demand keeps climbing across every scenario.

Even in the base case, the most conservative outlook, demand rises from around 220M pounds today to nearly 290M by 2040. In the high case, it exceeds 320M pounds. And if we factor in the tripling ambition from those 38 countries, demand could approach 400M pounds before we even reach 2050.

What this tells us is that by the early 2030s, the uranium market is set to become very tight, and that tightness only deepens as we move through the decade. Production is simply not keeping pace in any scenario shown here.

Meeting demand would require significant new mine development, and that is before even considering the tripling case. By 2040, the annual shortfall could exceed 100M pounds, which is a very large number in a market of this size.

Bottom line: More reactors, running longer, across more countries, all consuming uranium at a rate that existing and projected production cannot match. That is the demand story, and it is one that is only getting stronger.

4.1 The U.S. Needs More Nuclear Power

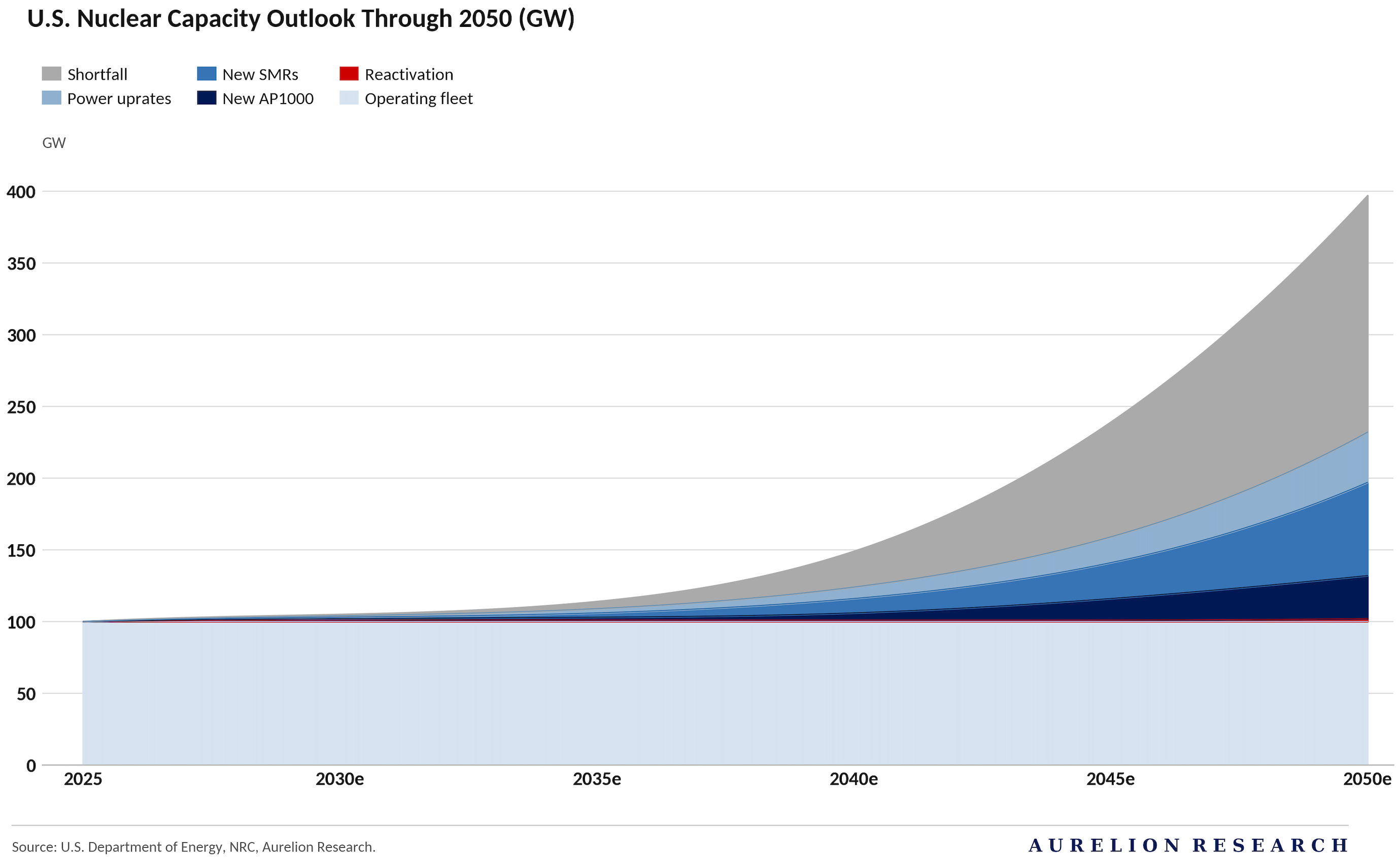

Now, let’s talk about what is happening at the policy level in the United States, because it adds a very important layer to everything we just covered. The Trump administration has set a target to grow U.S. nuclear capacity from ~100 GW today to 400 GW by 2050, a fourfold increase supported by near-term actions.

The Department of Energy is already backing the construction of 10 new large reactors, along with ~5 GW of upgrades to existing plants, with work expected to begin before 2030. That said, most new large reactors and small modular reactors are unlikely to come online before the 2030s, meaning construction will need to accelerate in the following decades to reach that target.

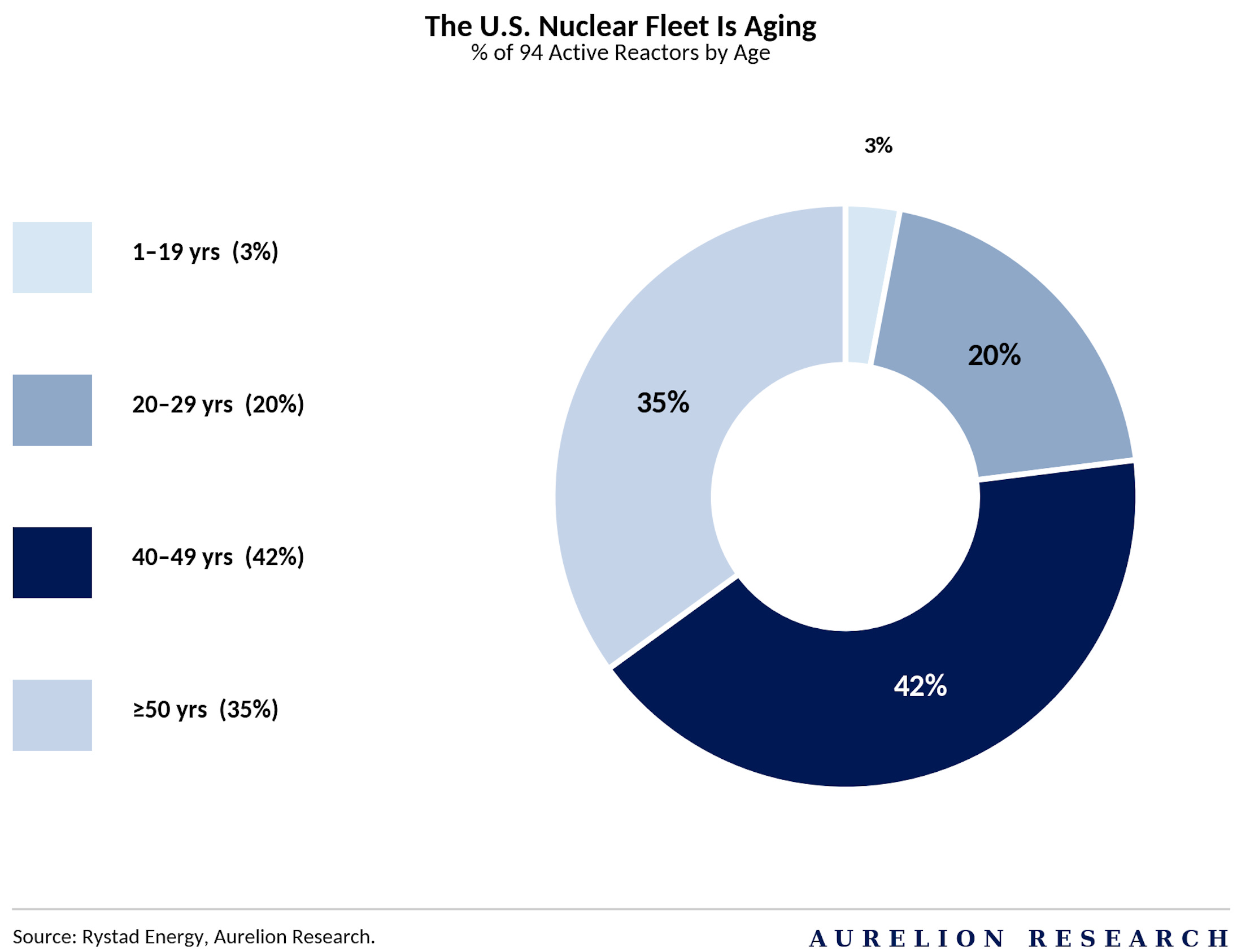

Now let’s talk about the U.S. nuclear fleet. As you can see in the exhibit below, the U.S. operates 94 commercial reactors, ranging from brand new units to plants as old as 56 years. Most of them are already over 40 years old, meaning they are operating under their first license renewal, which typically covers years 41 to 60.

What stands out is how far this life extension trend is going. Twenty reactors have already received a subsequent license renewal, extending operations out to 80 years. The NRC is currently reviewing five more applications, and another 22 are expected before the end of the decade. The momentum is clearly building.

These extensions are not just about keeping existing capacity online. They often allow for power uprates, increasing the amount of electricity a plant can produce, as well as major equipment upgrades that modernize decades-old infrastructure.

At a high level, this shows the US is doubling down on nuclear, extending, upgrading and reinforcing its existing fleet for decades to come, which has direct implications for long term uranium demand.

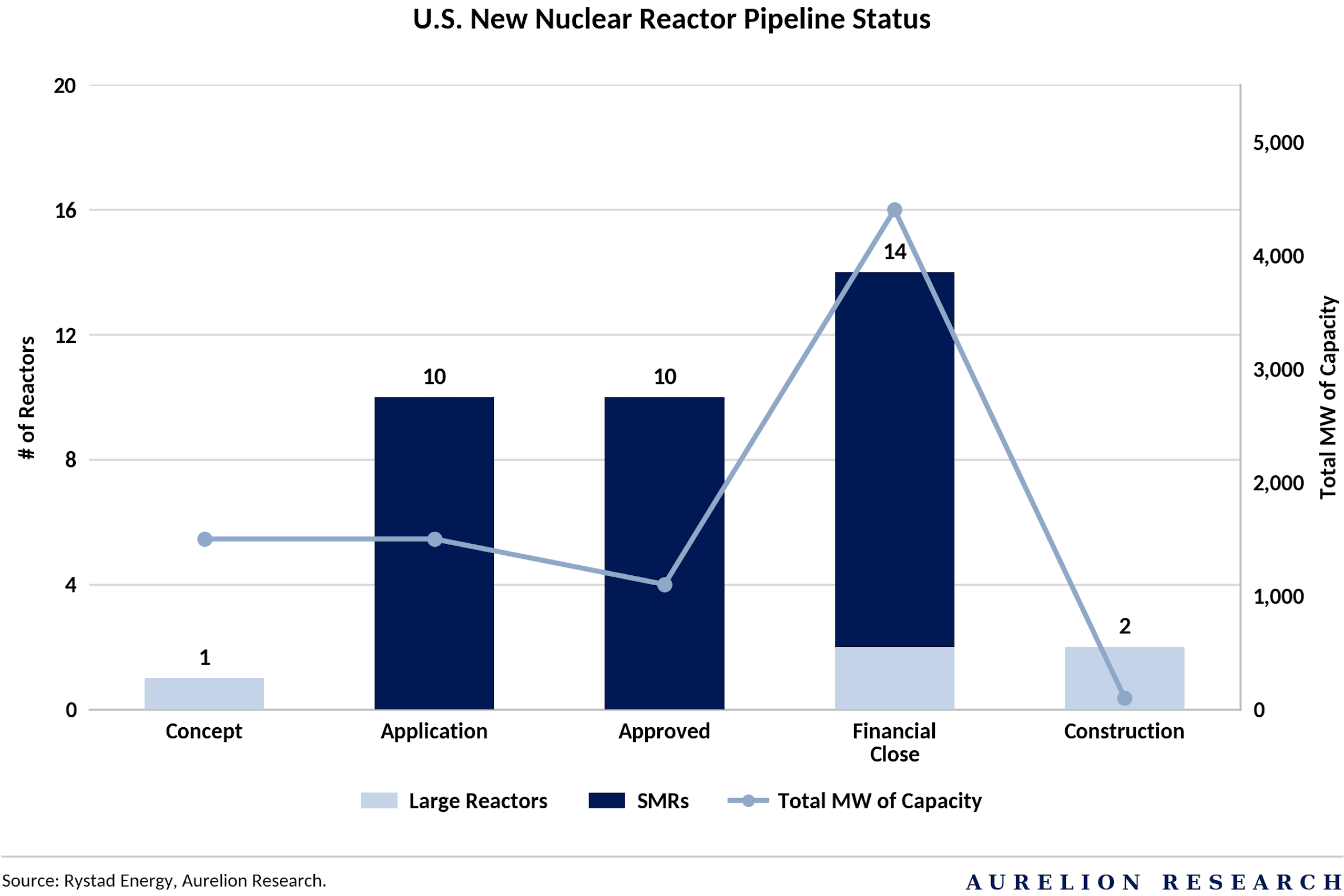

It is also interesting to look at the new reactor pipeline. According to Rystad Energy, which tracks projects across various stages of development, there are just over 8 GW of new nuclear capacity in the pipeline, excluding reactor restarts.

Important to note that this also does not include Fermi America’s separate plan to build 6 GW of nuclear generation by 2038, highlighting how limited near term additions remain relative to the scale of the challenge.

5. Uranium Global Supply Outlook

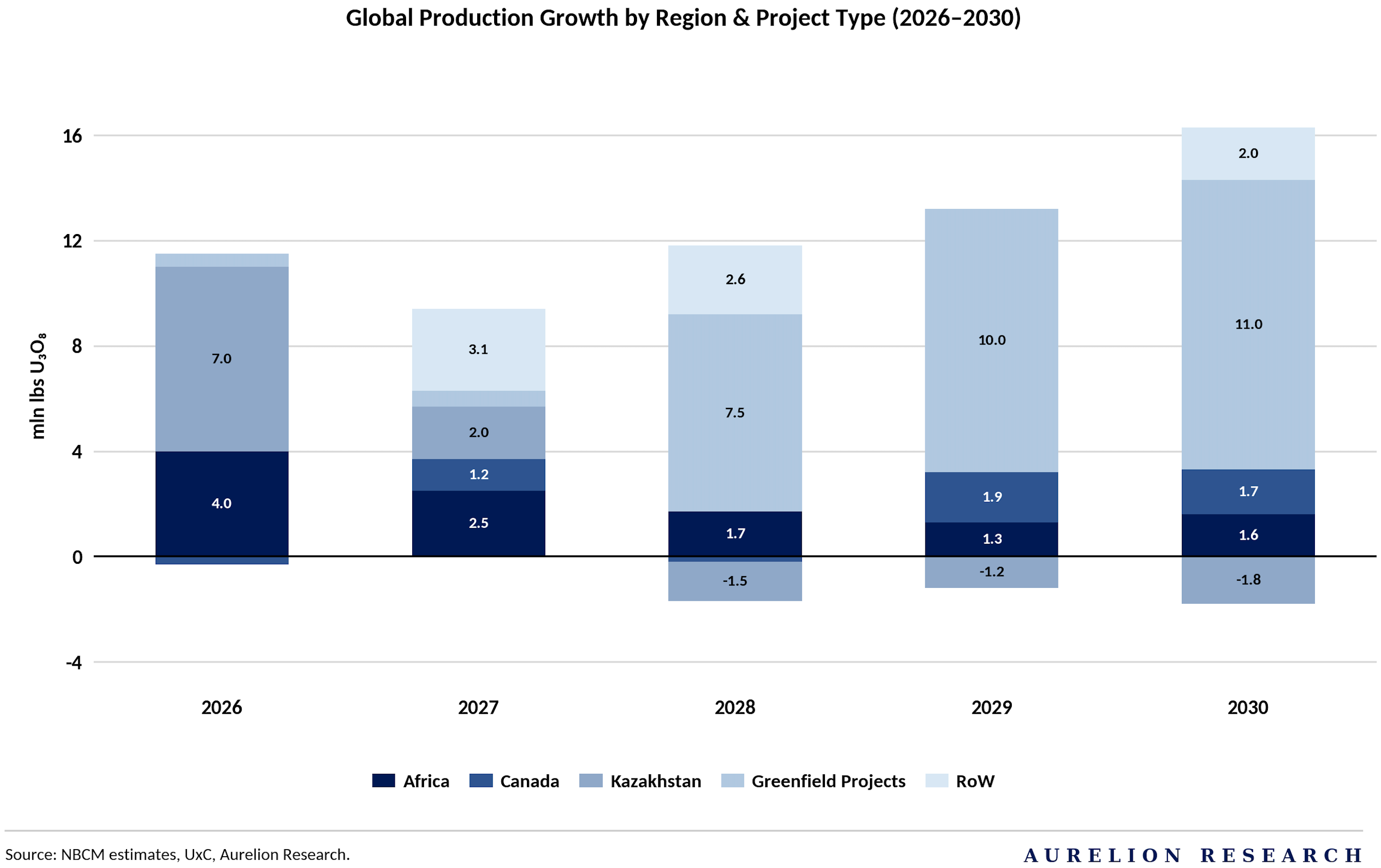

In the coming years, analysts expect a significant rise in annual uranium production as projects across major jurisdictions move forward. According to the data from UxC growth is anticipated in regions such as Kazakhstan, Canada, and Africa, with Kazakhstan alone projected to add 11M pounds of production by 2030. While this increase in global output is a positive development for the industry, it is unlikely to satisfy the rapidly accelerating demand.

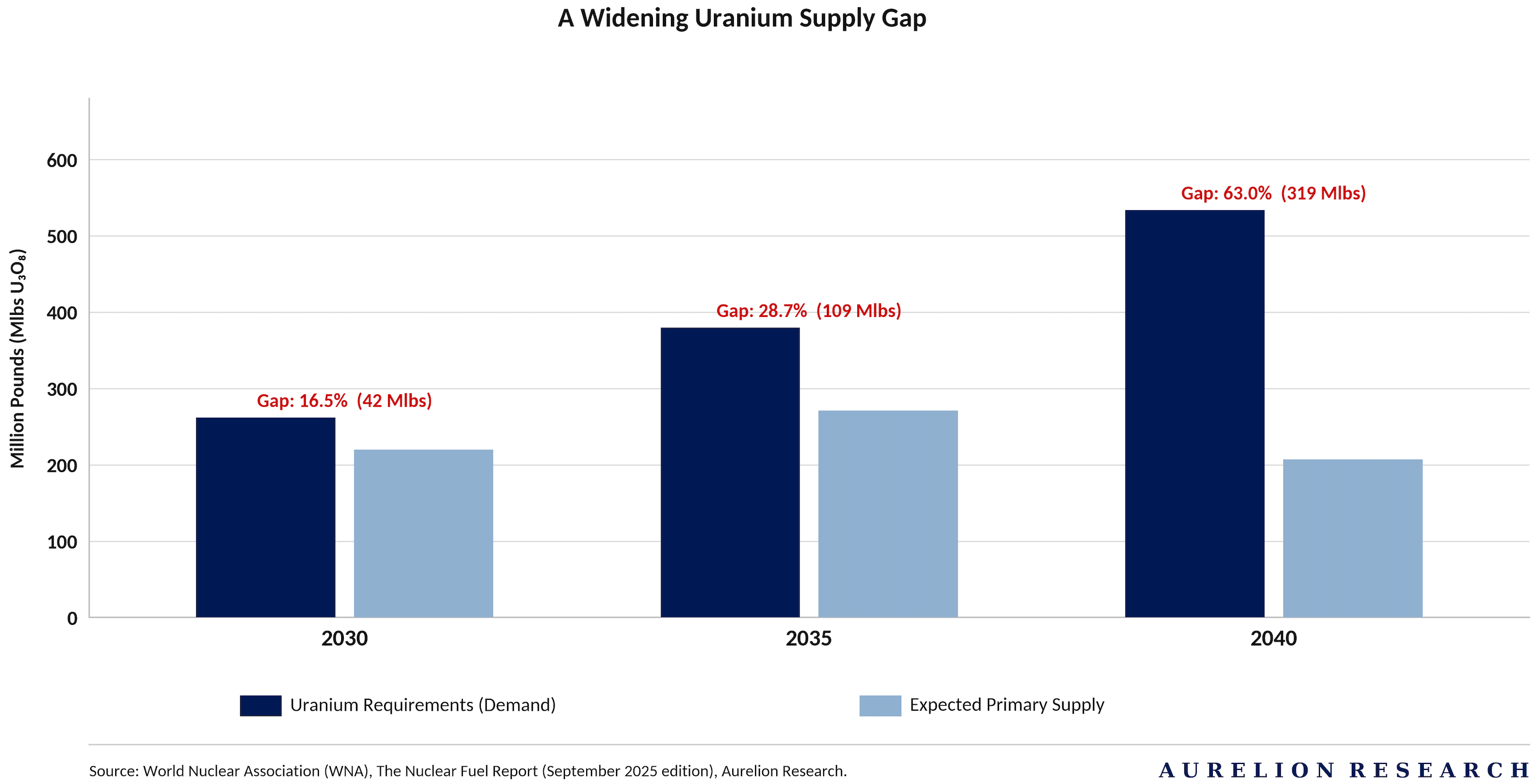

Now, here is where things get really interesting. By 2040, the uranium deficit is expected to reach 319M pounds per year. To put that in perspective, the entire world produces only around 160M pounds annually today, meaning global supply would need to more than double just to keep up with where demand is heading.

As shown in the following exhibit on the supply gap, this gap is set to widen progressively, reaching a 42M pound shortfall by 2030 and a 109M pound shortfall by 2035 before hitting a critical 63% deficit in 2040.

And here is the problem. Bringing a new uranium mine from discovery to production typically takes 15 to 20 years. This represents a real constraint in the industry. Even if every mining company on the planet broke ground tomorrow, the math simply does not work out in time to close that gap.

Which brings us to the uncomfortable truth. Unless governments act much faster than they historically have, and let’s be honest, they are known to be slow with the puck, supply just won’t be able to respond fast enough. We believe the deficit is effectively locked in given the timelines involved, with direct consequences for uranium prices in the years ahead.

5.1 The Supply Story Will Break

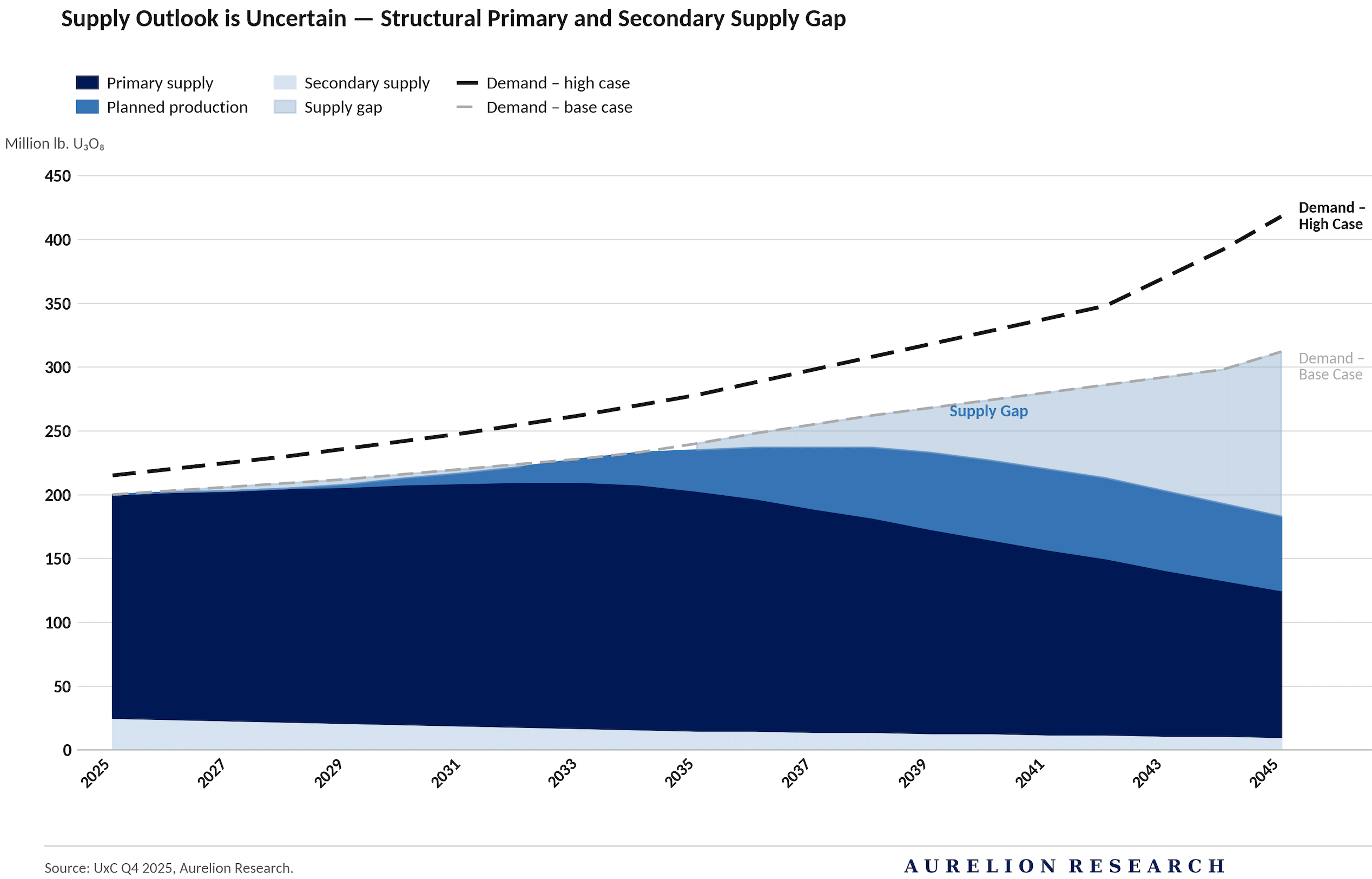

And these two following charts prove exactly that point.

The first one lays it all out clearly: even when primary supply, secondary sources, and planned production are combined, the market still falls short of meeting demand in both the base case and the high case. The supply gap begins opening in the late 2020s and continues to widen through 2045.

Closing the gap would require materially higher prices and accelerated project development.

The numbers simply do not work without a significant wave of new mine development, which typically takes 15 to 20 years to come online. The long development cycle is a key constraint that keeps the gap difficult to close, even with higher investment, so we believe it is likely that we are going to have a shortage of uranium, it is just a matter of time now.

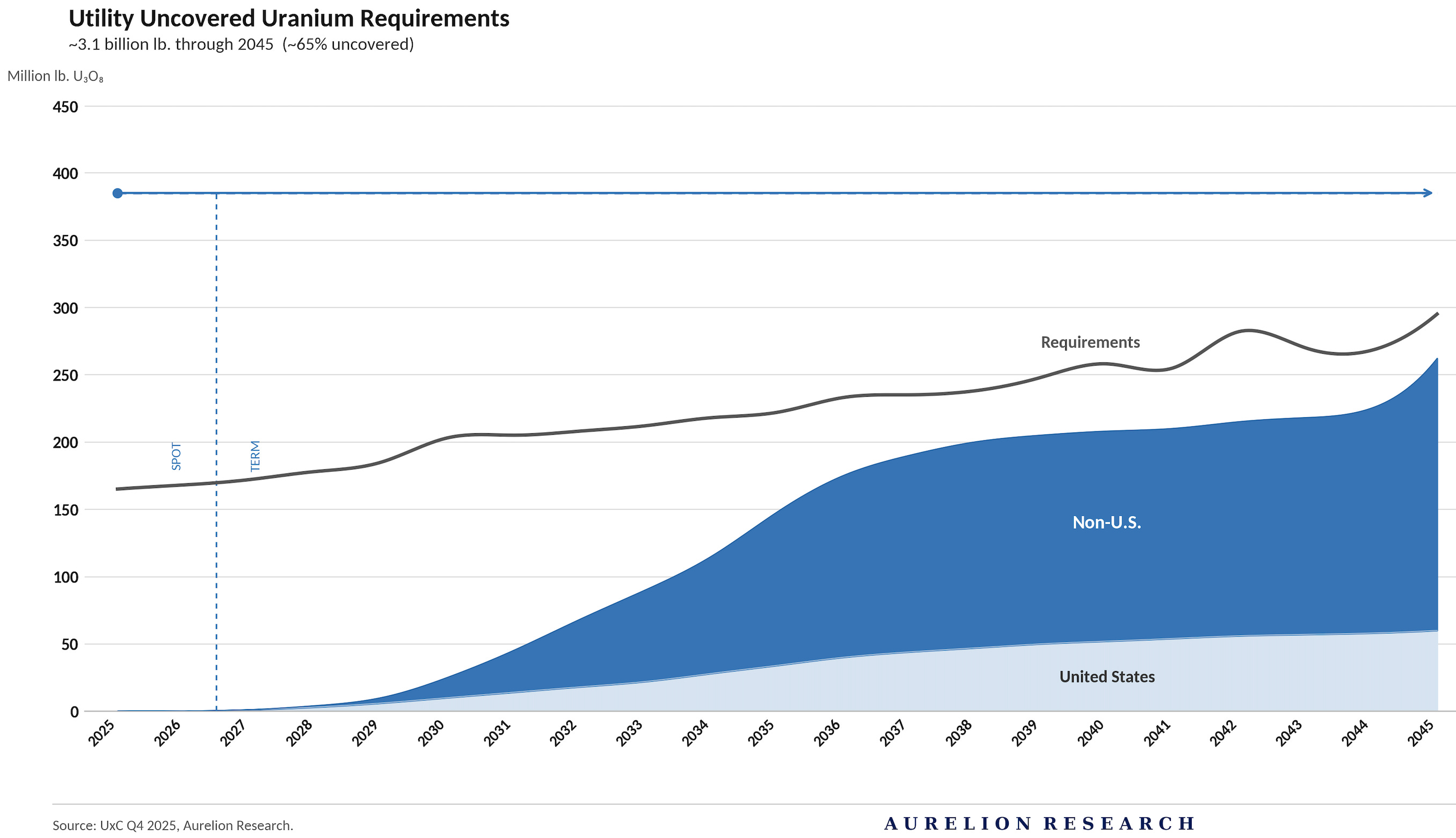

The second chart makes the situation more concrete. Utilities, the actual buyers of uranium, have roughly 3.1B pounds of requirements through 2045 that are currently uncovered. That is around 65% of total needs still uncontracted.

As you can see, both U.S. and international utilities are sitting on large uncovered positions, and as we approach the mid-2030s, that urgency is likely to increase. This large uncontracted volume represents a meaningful tailwind for the market as utilities eventually compete to secure fuel for the coming decades.

What this tells us is that utilities are going to need to come to market in a meaningful way, and they are going to need to do so sooner rather than later.

When that buying wave hits a market that already cannot produce enough, the conversation around uranium prices becomes a very different one. This is not a slow moving story anymore. The window to secure supply at reasonable prices is getting smaller by the year. And with that supply deficit, we already know what usually happens. It leads to a steady increase in uranium prices.

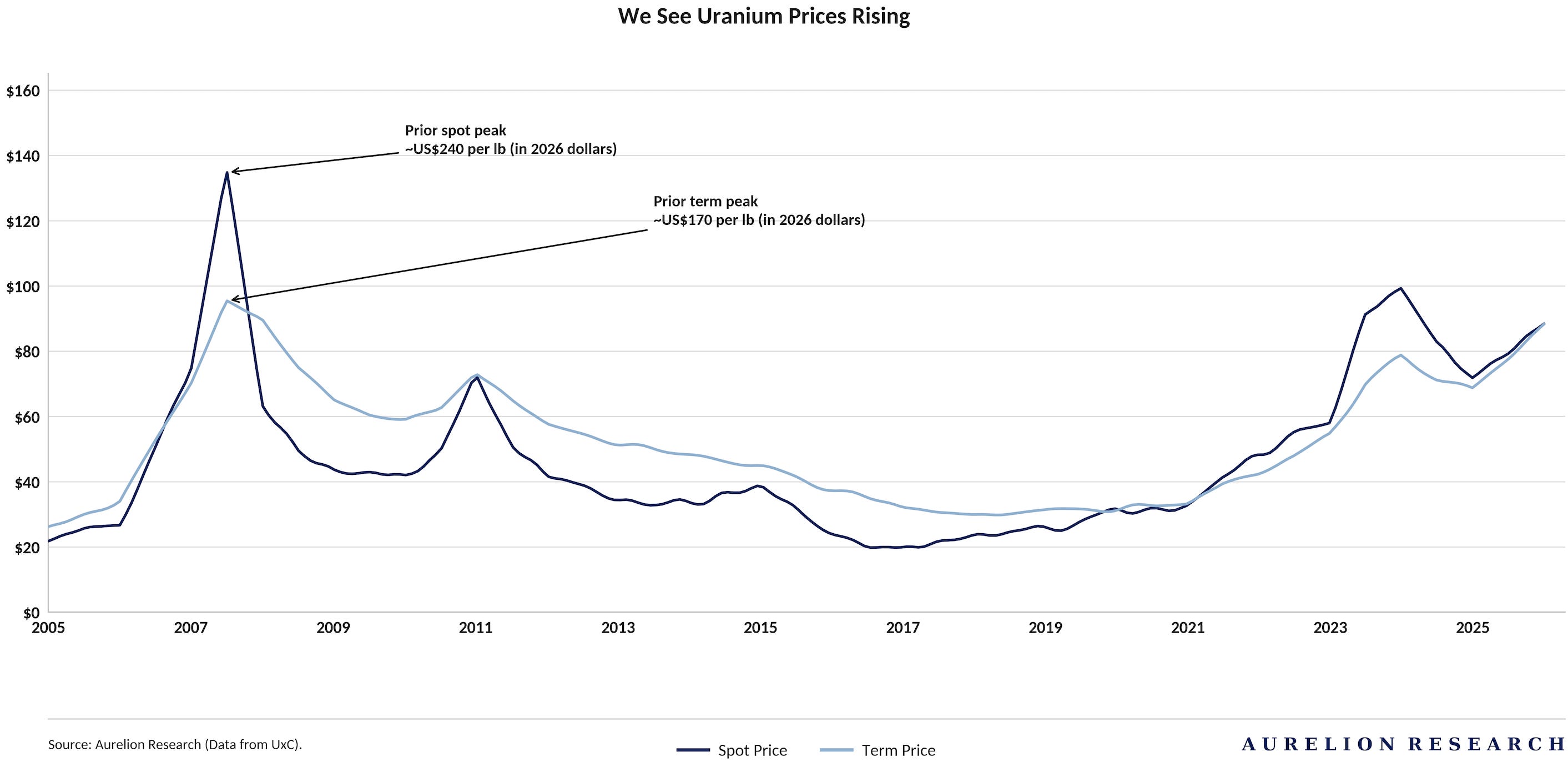

And this is the most important point of our uranium investment thesis: a growing supply deficit leads to higher prices, because the market needs to incentivize new supply to come online. It’s just macro, and it will happen again.

The chart below makes that history clear. Back in 2007, when the world last faced a major uranium supply crunch, spot prices reached the equivalent of roughly $240 per pound in today’s dollars.

Term prices, which utilities pay under long-term contracts, peaked at around $170 per pound. Following Fukushima, reactors went offline across Japan and demand collapsed, causing prices to grind lower for nearly a decade.

But look at what has happened since 2021. Prices have been climbing steadily and meaningfully, with spot already moving back toward the $100 per pound range. And here is the key point: we are still in the early stages of this supply deficit. The gap we just walked through has not fully materialized yet.

While the primary imbalance will likely show up in the 2030s, the current market still offers a strong opportunity to generate returns.

The market has navigated these cycles before, but we believe the setup today in nuclear energy equities appears more compelling than it was in 2007, because the runway is long.

6. Who Are the Big Players?

In the uranium space, the big players are limited, you can almost count them on one hand. You have Cameco, the Canadian giant, Kazatomprom, the Kazakhstan leader, and the French state-owned Orano. Beyond that, there are some players in Russia, Africa, and Uzbekistan, and a few in Australia, but that is pretty much it.

After the big three, the market becomes much more fragmented and less concentrated. This also means that the investable universe is not as broad as in other commodities. The number of high-quality businesses you can select to gain exposure to the theme is more limited, but that does not change our approach. We will still focus on the most relevant opportunities.

In the next section, we will cover two major publicly traded companies, then focus on our preferred name, along with another non-pure-play company that should still benefit from the current strength in nuclear energy.

6.1 Cameco (Canada)

Cameco stands as a global leader in the nuclear industry, and its influence extends far beyond mining. Its competitive advantage is built on ownership of some of the world’s most significant high-grade uranium reserves, primarily the McArthur River and Cigar Lake operations in northern Saskatchewan. These assets are among the highest-grade and lowest-cost in the sector, providing a stable foundation that is difficult for competitors to replicate.

The company has evolved into a more integrated energy player, expanding across the nuclear fuel cycle. Through its strategic partnership in Westinghouse Electric Company, Cameco now has direct exposure to the technology and services side of the industry, supporting both the existing global reactor fleet and new builds.

This is further reinforced by its interest in Global Laser Enrichment, which we believe positions the company for next-generation fuel technologies required for small modular reactors (SMRs). Utilities rely on this integration to secure both fuel and services for consistent, carbon-free power. As demand for reliable electricity continues to grow, driven by AI and broader electrification trends, we believe Cameco is well positioned to benefit from this trend.

Recent multi-billion dollar agreements, including a long-term supply deal with India, highlight the importance of its reserves in energy security. By controlling high-quality assets and investing in future technologies, Cameco is positioned as a full-cycle supplier in a market increasingly reliant on nuclear power.

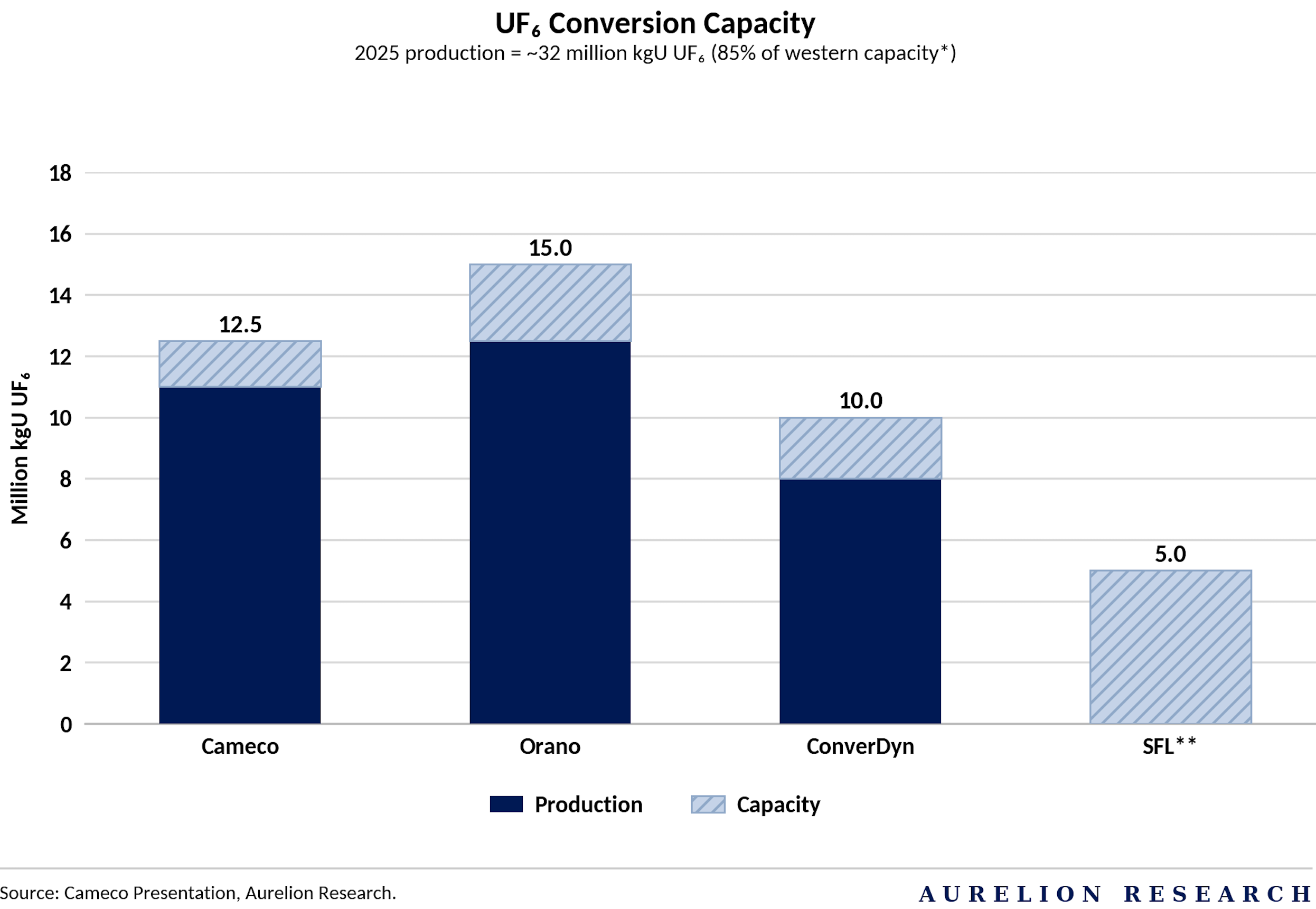

To illustrate its scale, Cameco accounts for ~18% of global uranium conversion capacity. It also plays a major role in Canada’s power system, with more than half of Ontario’s electricity generated using fuel supplied by the company.

When we look at the financial side of Cameco, the story only gets better.

Beyond mining, the company is also a key player in uranium conversion, an essential step in the nuclear fuel cycle. Global uranium hexafluoride production was about 32M kg in 2025, with roughly 85% coming from Western suppliers.

Cameco is one of the main producers alongside Orano, making it a critical supplier for utilities that depend on this part of the value chain.

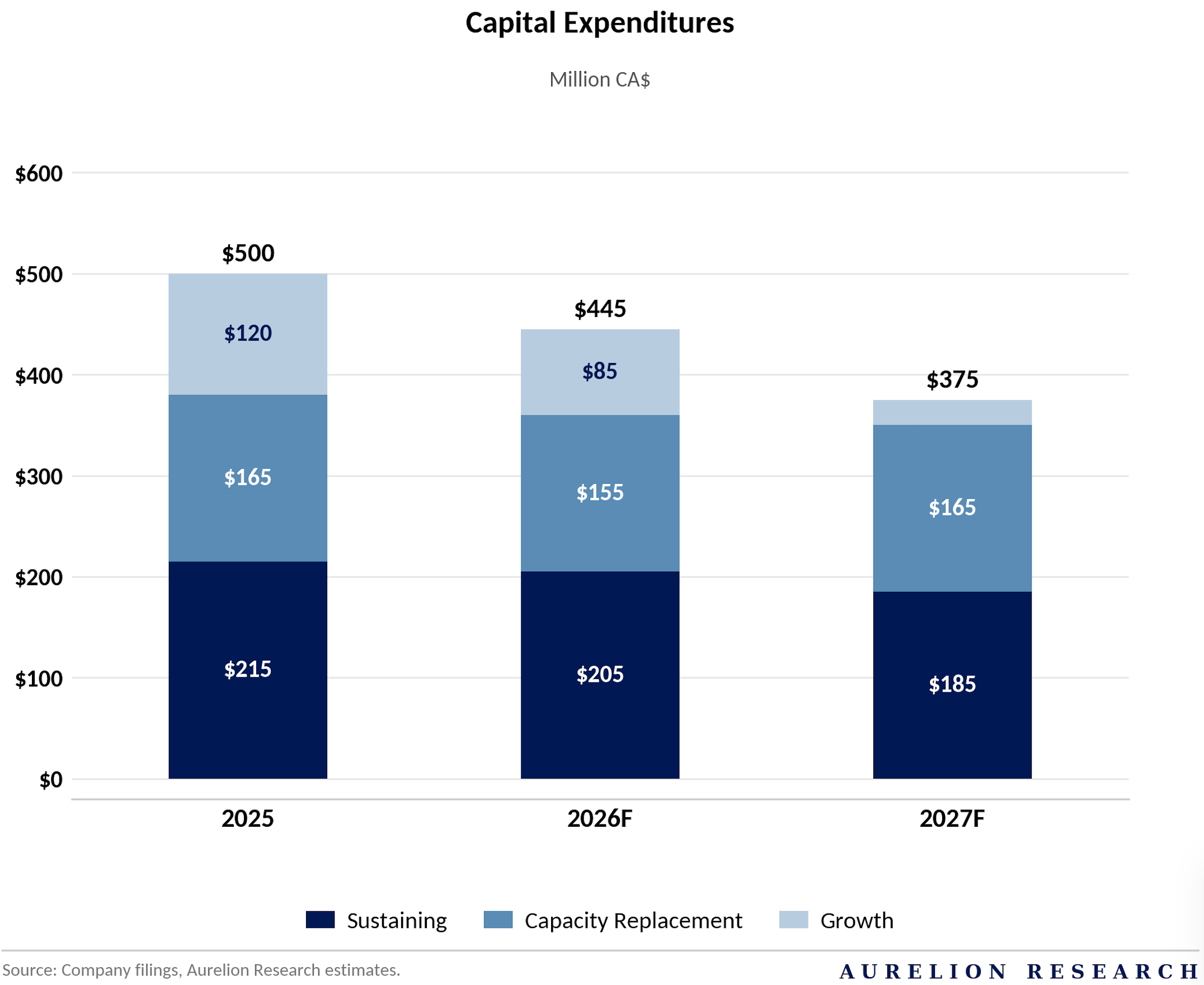

This position translates into strong and recurring cash flow, which the company is actively redeploying. In 2025, Cameco allocated ~$500M toward sustaining operations, replacing capacity, and supporting future growth.

Capital spending is expected to ease slightly into 2027 as major projects are completed, but the strategy remains unchanged. The company continues to invest ahead of demand rather than reacting to it.

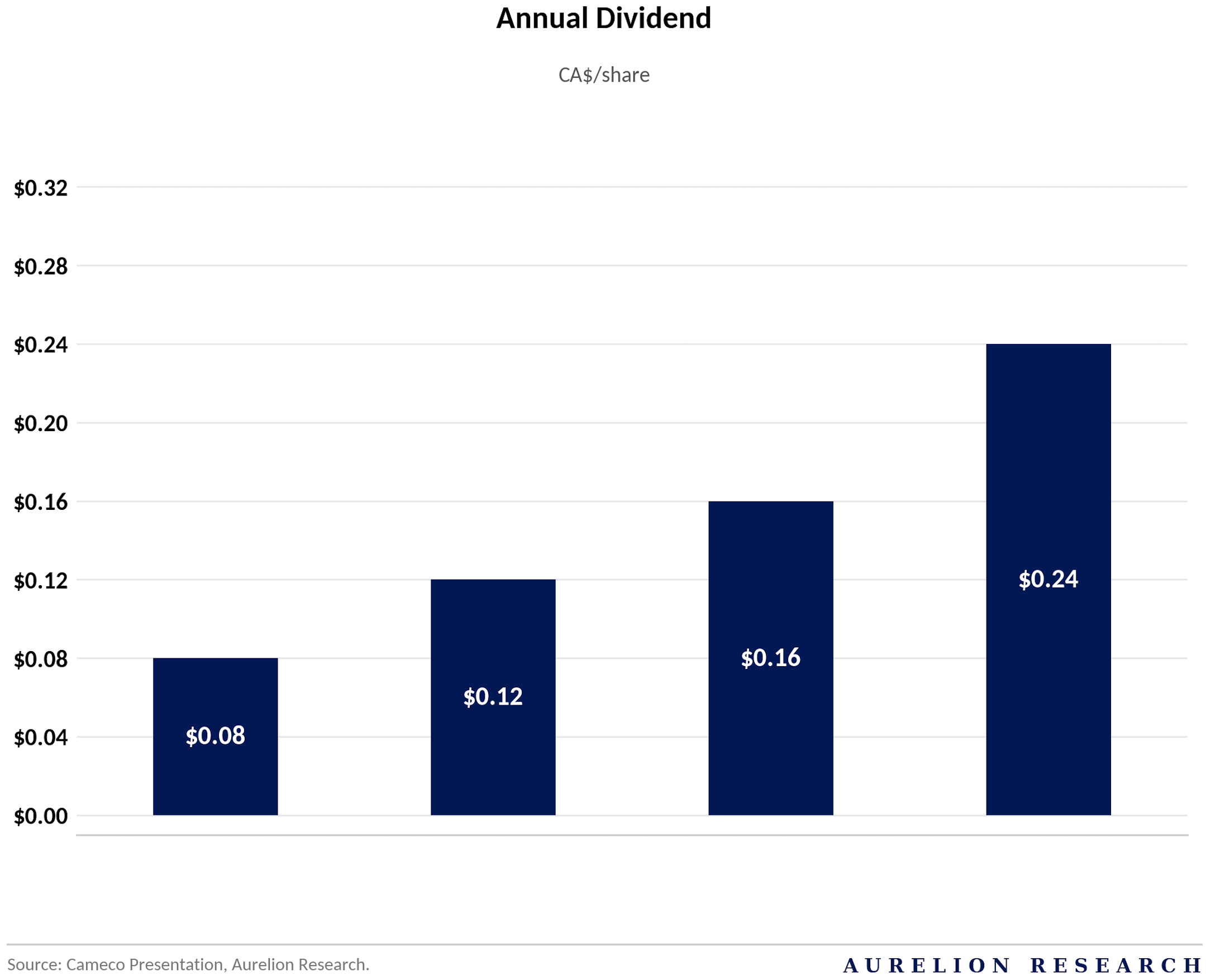

That discipline is also visible in shareholder returns. In 2025, management brought forward a dividend increase to $0.24 per share, originally expected in 2026. Stronger financial performance, helped in part by contributions from Westinghouse, allowed them to act earlier than planned. Since 2022, the dividend has roughly tripled, reflecting stronger cash generation.

Taken together, this highlights a company executing ahead of schedule. Cameco generates strong cash flow, which supports both reinvestment and shareholder returns, while positioning itself for sustained nuclear demand growth. It remains a relatively stable way to gain exposure to the uranium cycle.

6.2 Kazatomprom (Kazakhstan)

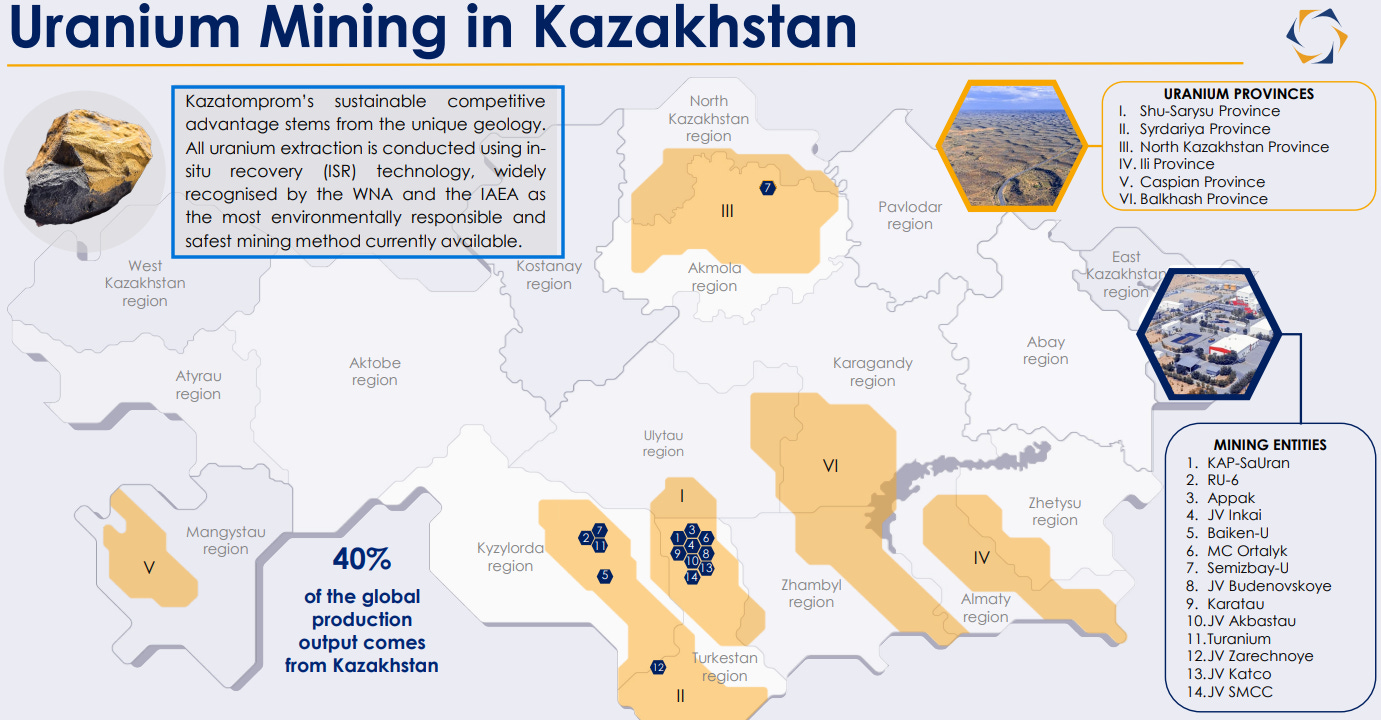

As the national operator for the Republic of Kazakhstan, Kazatomprom sits at the center of the country’s uranium exports, rare metals, and nuclear fuel production. Kazakhstan has been the world leader in natural uranium mining since 2009, and Kazatomprom holds priority rights over the nation’s vast reserve base. These rights were recently reinforced through 2026 legislation, further securing its leading position across new exploration and production projects in the country.

Kazatomprom’s primary competitive advantage is its exclusive use of the In-Situ Recovery (ISR) mining method. This technology allows the company to extract uranium at a significantly lower cost and with a smaller environmental footprint than traditional open-pit or underground mining. Because their operations are among the lowest-cost in the world, Kazatomprom remains highly resilient to market fluctuations while capturing significant upside as uranium prices rise.

The company’s assets cover the entire front-end of the nuclear fuel cycle. This integration includes everything from geological exploration and mining to the production of high-tech nuclear fuel components. Through its Ulba-FA plant, Kazatomprom produces finished fuel assemblies for international markets, providing a complete, vertically integrated solution for utilities worldwide.

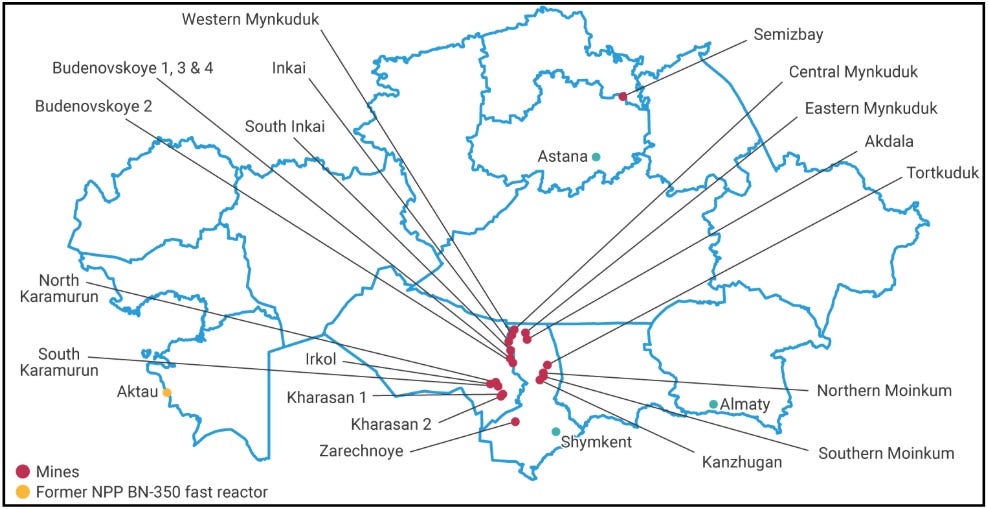

Kazakhstan: Uranium Mines & Nuclear Legacy Assets

Like we said earlier, Kazakhstan is the undisputed heavyweight of the uranium industry, with its operations concentrated across six major uranium provinces that effectively define the global supply landscape. These regions, including Shu-Sarysu, Syrdariya, and North Kazakhstan, host a network of 14 mining entities that form the backbone of global production.

While the country holds a dominant position, it has also built a broad international footprint by structuring 12 of these 14 operations as joint ventures. This brings in major partners from France, Canada, China, and Japan, keeping its assets closely tied to global nuclear supply chains.

The scale of these holdings is significant. Kazakhstan’s total uranium resources are estimated at over 954,000 tonnes. Key joint ventures such as Inkai, Katco, and Budenovskoye include some of the most important production assets globally.

This resource base is reinforced by a strong commitment to future development, with 75-85B KZT (~US$155–175M) allocated to exploration through 2030.

In practice, this makes Kazakhstan a central gatekeeper of global supply, with a level of influence very few producers can match. At the same time, the country is starting to evolve on the demand side. A national referendum in 2024 saw ~71% of voters support the development of Kazakhstan’s first nuclear power plants.

This marks a gradual shift from being almost exclusively an exporter to also becoming a domestic consumer of uranium. As plans move forward with international partners, Kazakhstan is reinforcing its position as a long-term pillar of the global nuclear fuel cycle and the broader shift toward carbon-free energy.

7. Where Uranium Prices Are Headed Next

The real question is where the new floor is being established.

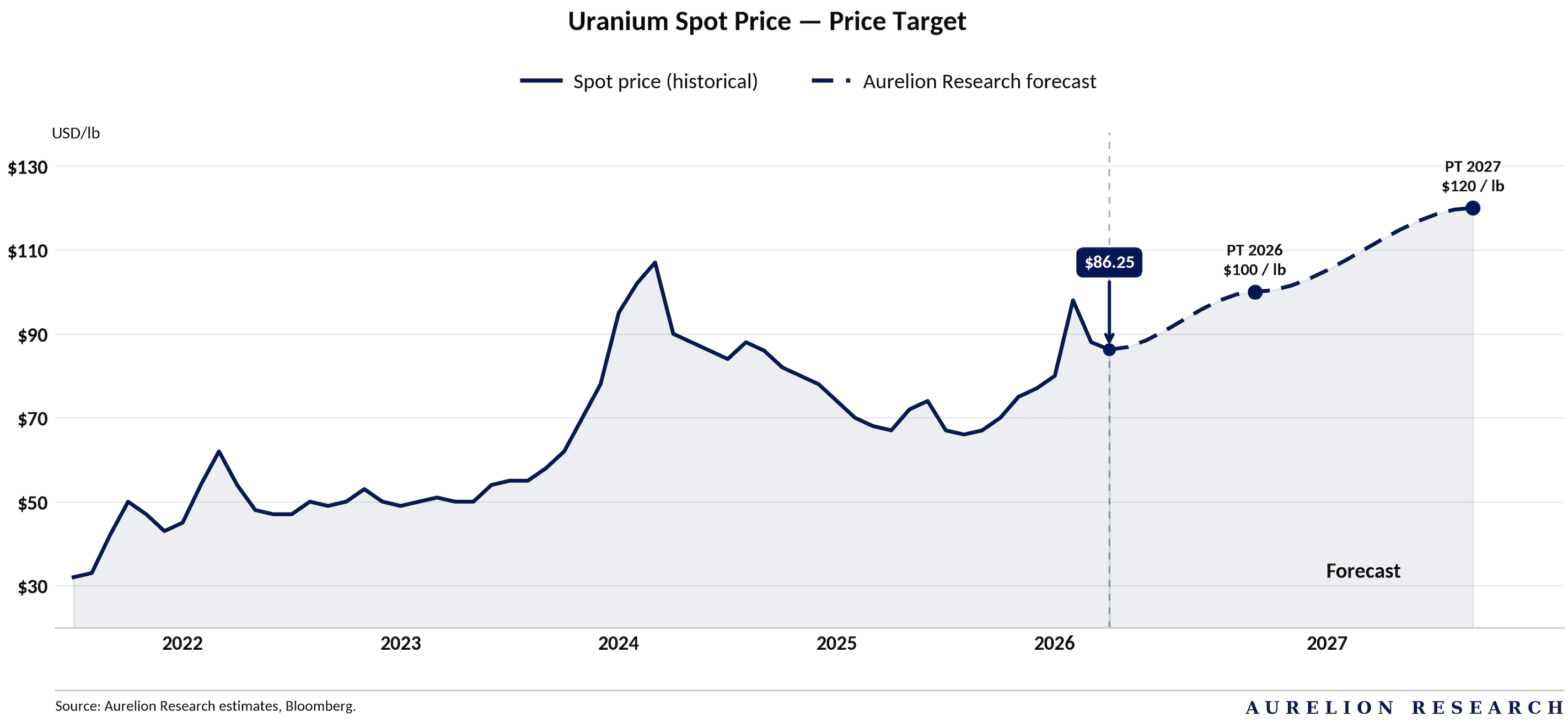

As of May 2026, the uranium spot price is holding around the $86 range, up more than 23% year over year. But the spot market is only part of the story.

The long-term contract price, where utilities secure the majority of their supply, has already reached $90 per pound, the highest level since 2008. To us, this signals that buyers are increasingly accepting that the era of cheap uranium is likely over.

We believe uranium prices could reach $100 in 2026.

This view is supported by analysts who expect a growing supply deficit over the next two decades. As the market tightens, higher prices will likely be needed to bring on enough new supply to meet demand.

What also makes this cycle different from 2007 is the source of demand.

This is no longer just about utilities. Large tech companies like Meta and Microsoft are now securing nuclear power to support AI data centers. Meta alone has signed deals tied to up to 7.8 GW of nuclear capacity. This adds a new layer of demand that barely existed a few years ago.

The broader setup remains difficult to ignore. Reaching the annual supply required over the next decade likely demands materially higher uranium prices to justify new mine development. We know it is not the first time we say it, but the issue is that new mines typically take 15 to 20 years to come online. In our view, that keeps the market in a position where deficits remain extremely difficult to close, supporting a much stronger long-term pricing environment for the sector.

8. Our Favorite Stock Ideas

In the sections that follow, we present our two favourite ideas to play the uranium cycle. We believe they are among the most effective ways to express this thesis and strong ways to gain exposure to the upside we see in the sector.