Stevanato Group (STVN): Deep Dive Into an Attractive Long-Term Compounder

Multiple industry expert discussions, combined with our own analysis, point to a clear mispricing in Stevanato.

A deep dive into our recent new addition to the Aurelion Index

Stevanato has the hallmarks of a great compounder: a clear moat, strong revenue growth, and an attainable margin expansion story.

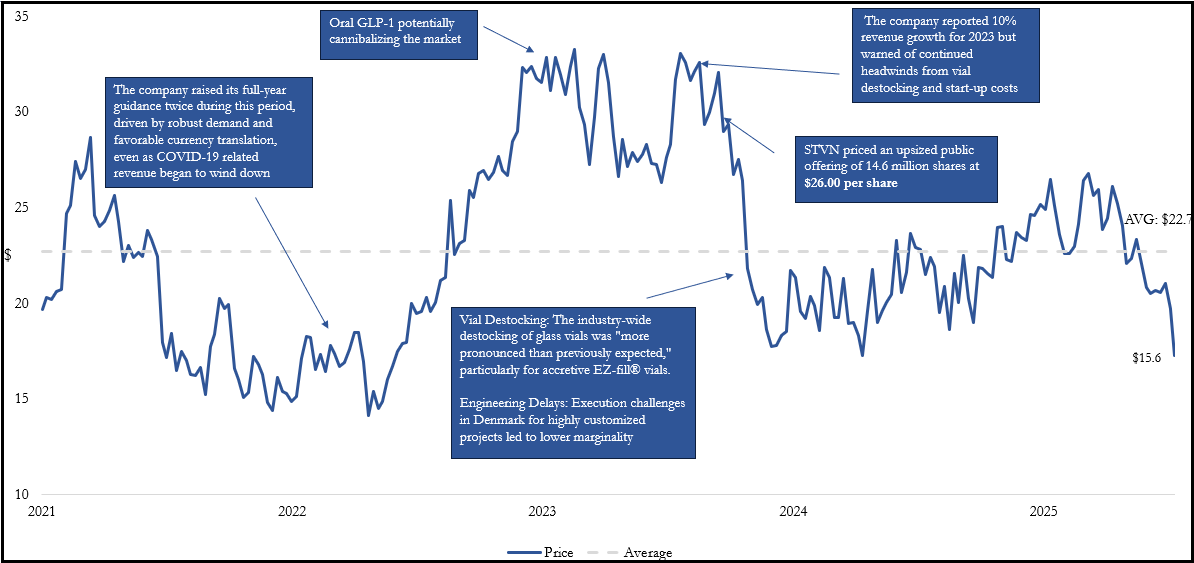

We added STVN to the portfolio on March 3rd, and the stock jumped 19% the following day after earnings. Since then, the stock has come down and is back close to previous levels, as discussions during the earnings call were slightly worse than the market expected. However, the main driver was the Iran-US conflict, which led equities down significantly.

This is the full deep dive we promised when we added STVN to the portfolio on March 3rd. It adds our complete financial model, price targets, and valuation framework to the initial note, along with a much deeper look at the industry, the products, and the competitive positioning.

We spoke with investor relations, an IQVIA researcher, and a practicing physician. You will find their insights throughout the report especially on GLP-1s giving us a different perspective than what the market currently reflects.

The mix of earnings growth and business quality is rarely seen in life sciences, and we believe this is the first time STVN has traded at such a discount to peers despite that growth outlook.

We were previously invested in the stock in late 2024, when the company was going through its destocking situation, and successfully exited in mid-2025. In our opinion, the stock often experiences strong swings that are not always warranted.

Table of Contents

Business & Operations Overview

Industry Overview

Geographic Footprint and Customer Proximity

GLP-1s: Analysis of the Impact

Takeaway of our Discussions with Industry Experts

Our view of Q4 2025 Earnings

Investment Thesis

Forecasts, Valuation & Price Targets

1. Business & Operations Overview

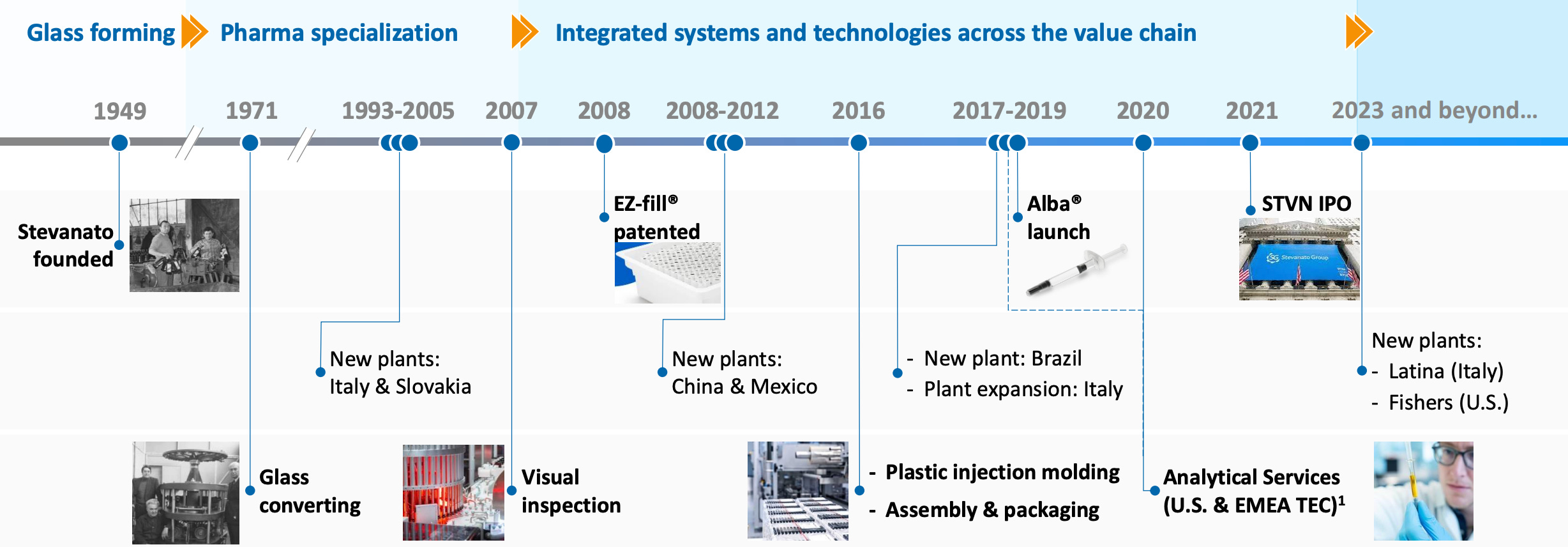

Stevanato Group (NYSE: STVN) is a leading global provider of integrated drug containment, delivery, and diagnostic solutions for the pharmaceutical and biotechnology industries. Founded in 1949 and headquartered in Italy, it serves as a strategic partner to the world’s top 25 pharmaceutical firms.

A simple example helps illustrate the role Stevanato plays. In a weight-loss injection pen, such as those used for GLP-1 drugs, Stevanato likely produced the internal glass cartridge, the specialized coating that helps prevent the drug from sticking to the glass, and potentially even the equipment used by the pharma company to fill that cartridge.

The Specced-In Moat

Most people hear “glass manufacturer” and think commodity. This is definitely not the case and important to address before analyzing this business.

The glass Stevanato produce is an engineered, drug-specific containment system, developed and validated in direct partnership with the drug it will carry for its entire commercial life. The business implications are major.

The Lock-In Starts Years Before a Drug Reaches the Market

When a biopharma company develops a new drug, it doesn’t just need to prove the molecule works. It needs to prove the entire delivery system works.

The syringe, the cartridge, the vial, all of it gets tested together with the drug for chemical compatibility, dimensional precision, and sterility integrity across the product’s full shelf life. This process runs through clinical trials, takes years, and costs millions.

Once Spec’d In, Switching Is Typically Irrational

Regulatory approval is tied to a specific manufacturing process, and that includes the primary packaging. Changing the container after approval is a full regulatory event. The biopharma company would need to file new applications, run new compatibility studies, and potentially redo clinical manufacturing batches. That process takes 2-4 years and costs tens of millions of dollars, for a change that often delivers zero clinical or commercial benefit. It is simply not a project that gets approved.

A Revenue Profile With Unusual Visibility

Once a drug launches, Stevanato ships containers for every dose sold, globally, for the entire life of that product. Volume scales directly with the drug’s commercial success. Management can map approved drugs across their customer base to projected dose volumes and model out revenue with a high confidence level. It functions less like traditional backlog and more like recurring demand.

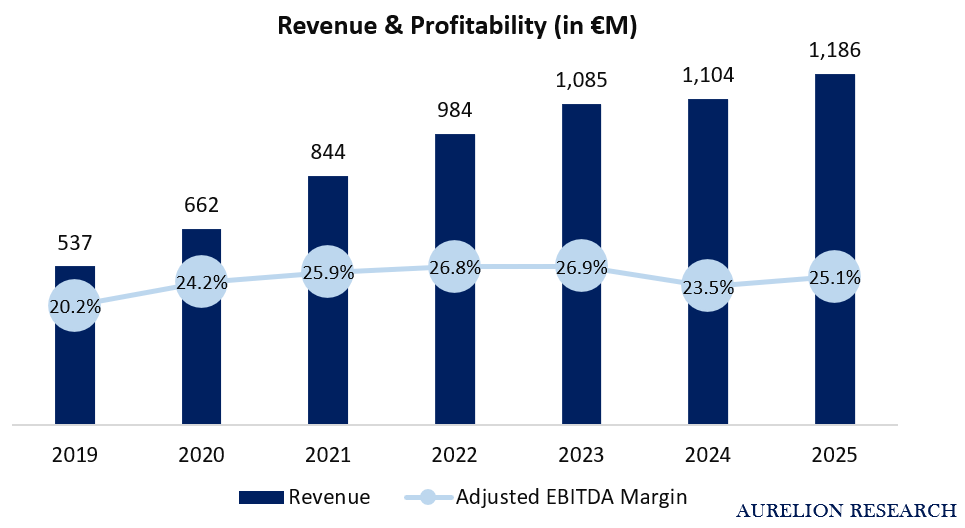

Despite a destocking headwind in 2024 and one of the heaviest capex cycles in its history, Stevanato has grown its revenue base consistently and held margins remarkably well.

The Moat in Plain Terms

A competitor can build a better glass factory and undercut on price. What they cannot easily do is displace Stevanato from an approved drug without asking the customer to spend years and tens of millions of dollars for no tangible benefit.

More Than Just a Container: Engineering Solutions

What makes this business model even more interesting is that the spec-in relationship doesn’t stop at the container. Once a biopharma company has validated a Stevanato container, they still need industrial equipment to fill it at commercial scale. Stevanato builds that equipment too.

Because the machinery is engineered around their own container specifications, a customer using a Stevanato vial is naturally pulled toward using Stevanato’s filling lines. Introducing third-party machinery means new compatibility testing and new regulatory risk, making Stevanato the default choice across the entire production chain.

Not All Containers Are Equal

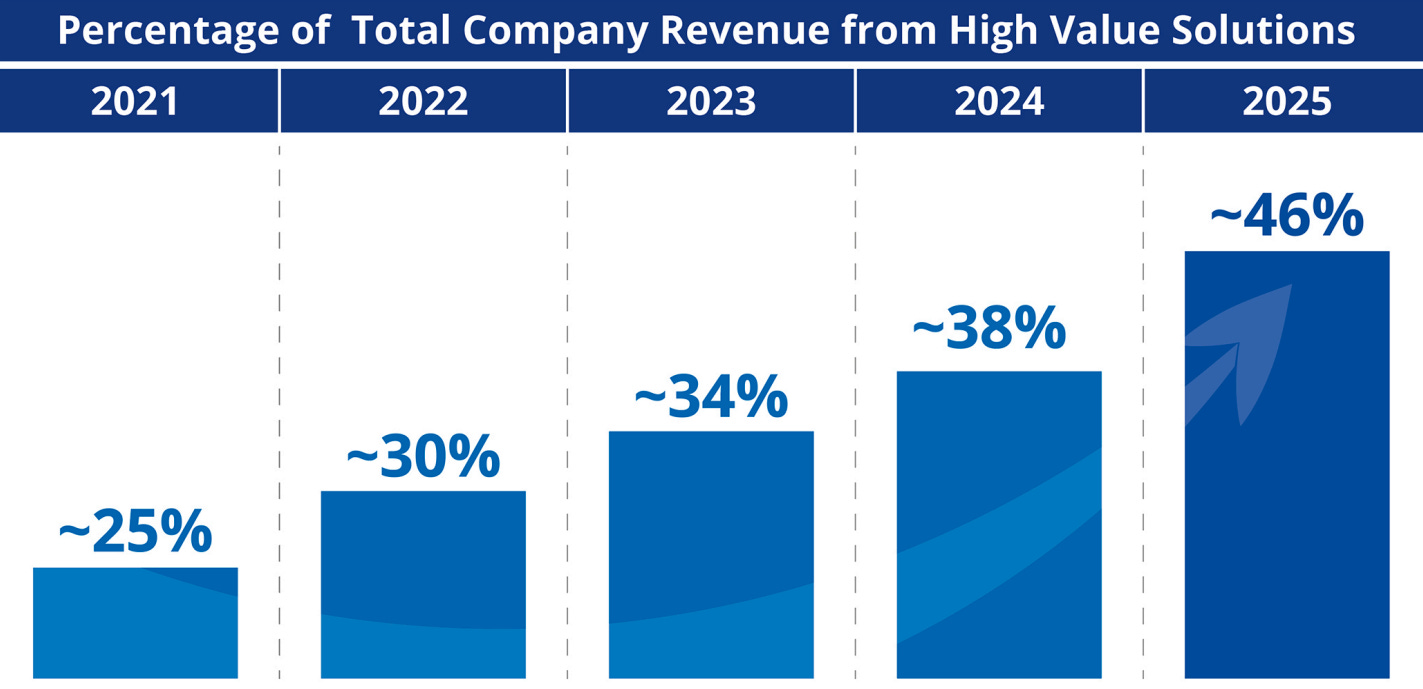

Stevanato has been steadily shifting its mix toward more sophisticated formats called High-Value Solutions, primarily ready-to-use, pre-sterilized containers that arrive at the pharma customer’s filling line already prepared, eliminating entire steps from their manufacturing process. These products are harder to make, harder to replicate, and are the preferred format for biologics, the fastest-growing class of injectable drugs.

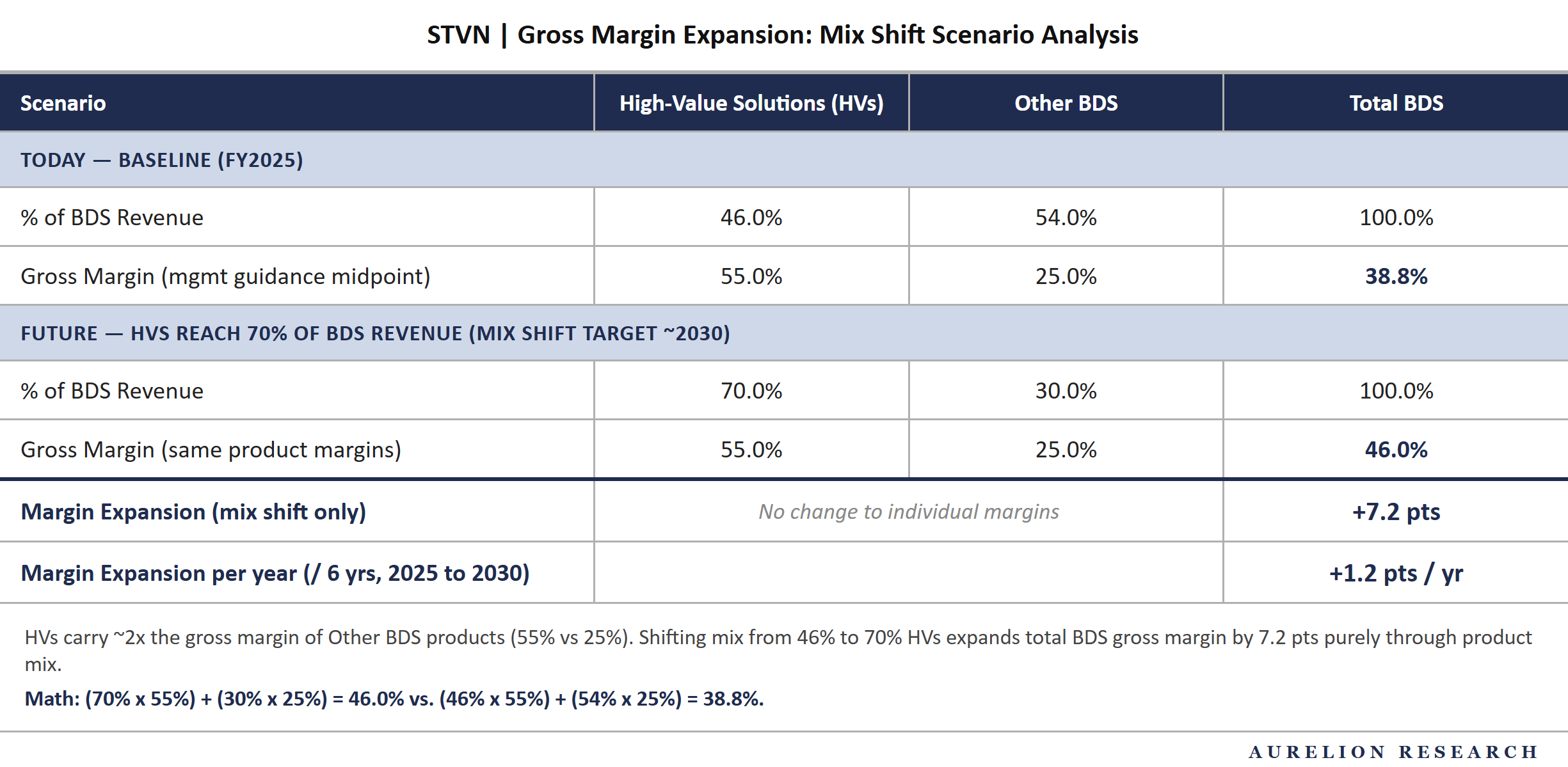

The economics reflect that clearly. Per our management discussion, gross margins on these premium products run at ~55%, compared to ~25% on standard containment. Every percentage point of mix shift toward premium formats has an outsized impact on profitability. In 2019 these premium products represented 17% of revenue. By 2025 they reached 46%.

Customers

Stevanato has high customer concentration.

The top-10 share jumped from 41.7% in 2021 to 53.6% in 2025, and the single largest customer crossed the 12% threshold. We believe this is a direct consequence of the GLP-1 boom concentrating more spend with one or two massive buyers (Novo Nordisk and Eli Lilly).

STVN does not officially disclose its top customers, but we can reasonably assume the following as key customers:

This leads to a simple conclusion we discuss later in the industry overview: STVN health and growth is highly correlated with large Pharma health.

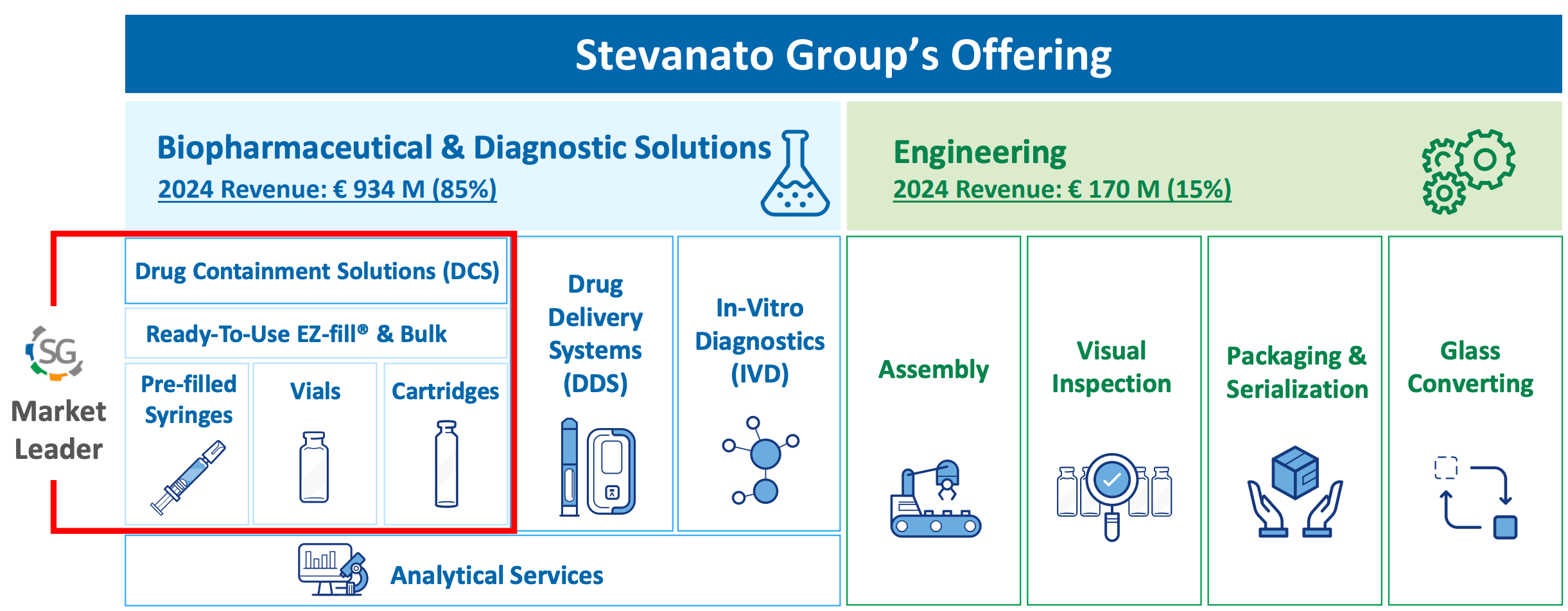

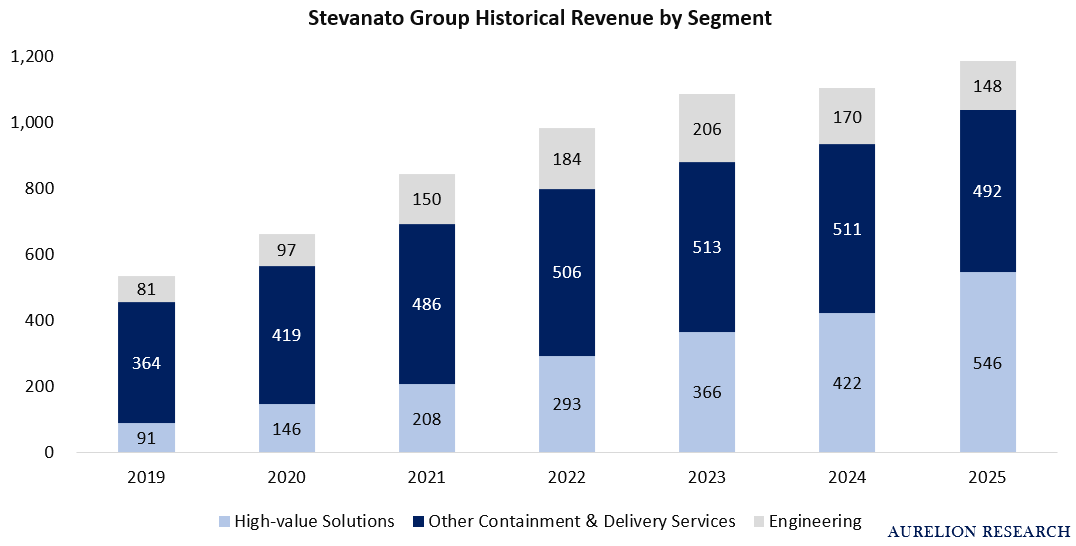

Company Segments

In addition to separating its revenue into 2 segments, Stevanato also reports its high-value solution revenue within the Biopharmaceutical & Diagnostic Solutions segment.

High-Value Solutions (46% of Revenue): The Main Engine

Three things explain the pricing power and the pace of growth:

1) Biologics are the fastest-growing drug class, and they are almost exclusively injectable. GLP-1s like Ozempic and Wegovy get most of the headlines, but the tailwind is broader: monoclonal antibodies, ADCs, biosimilars, and other complex therapies all require the highest-grade packaging that standard formats cannot provide.

2) HVS formats save pharma companies real money. Receiving pre-sterilized, pre-validated containers lets manufacturers eliminate entire steps from their fill-finish process. The higher unit price Stevanato charges is largely offset by cost savings on the customer’s end.

3) Customers rarely leave. Qualifying a new container for an approved drug is a multi-year, multi-million dollar regulatory exercise with no clinical upside. Nobody volunteers to do that twice. HVS formats are often co-developed alongside the drug itself and embedded directly into the customer’s production line, making switching almost unthinkable.

Other Containment & Delivery Solutions (41% of Revenue)

This bucket includes standard bulk vials, low-value syringes, cartridges, and in-vitro diagnostic containers. These are not exciting products, but essential ones.

The flattish to declining revenue in the last 2 years in other containment revenue has been driven partly by a deliberate transition, as the company shifts capacity toward a larger portfolio of high-value projects.

When Stevanato builds a new production line, it is increasingly choosing to fill it with premium formats rather than commodity vials. Some of what looks like “other containment” shrinkage is simply volume that has been upgraded and reclassified into the HVS bucket.

Engineering (12% of Revenue)

As you can see in the chart above, the engineering segment has been the problem child since 2023. However, per our conversations with management and other investors, and with the reaction we have seen in recent quarters, it is almost as if the market does not really care about its short-term performance.

For some quarters revenue misses significantly, but the investor base and, we believe, management have communicated well that revenues can be largely sloppy, and the stock does not move on significant beats or misses in that segment.

What we point out is that in 2023 and 2024 the company entered into a substantial amount of contracts that were not profitable. These contracts helped sign long-term revenue agreements and were positive for that purpose, but management has now decided to exit some of them as they were impacting the bottom line.

We do not put a high weight on this segment when analyzing the financials of the stock. Revenue and profitability will be sloppy. This segment is purely there to enhance the overall offering of the company.

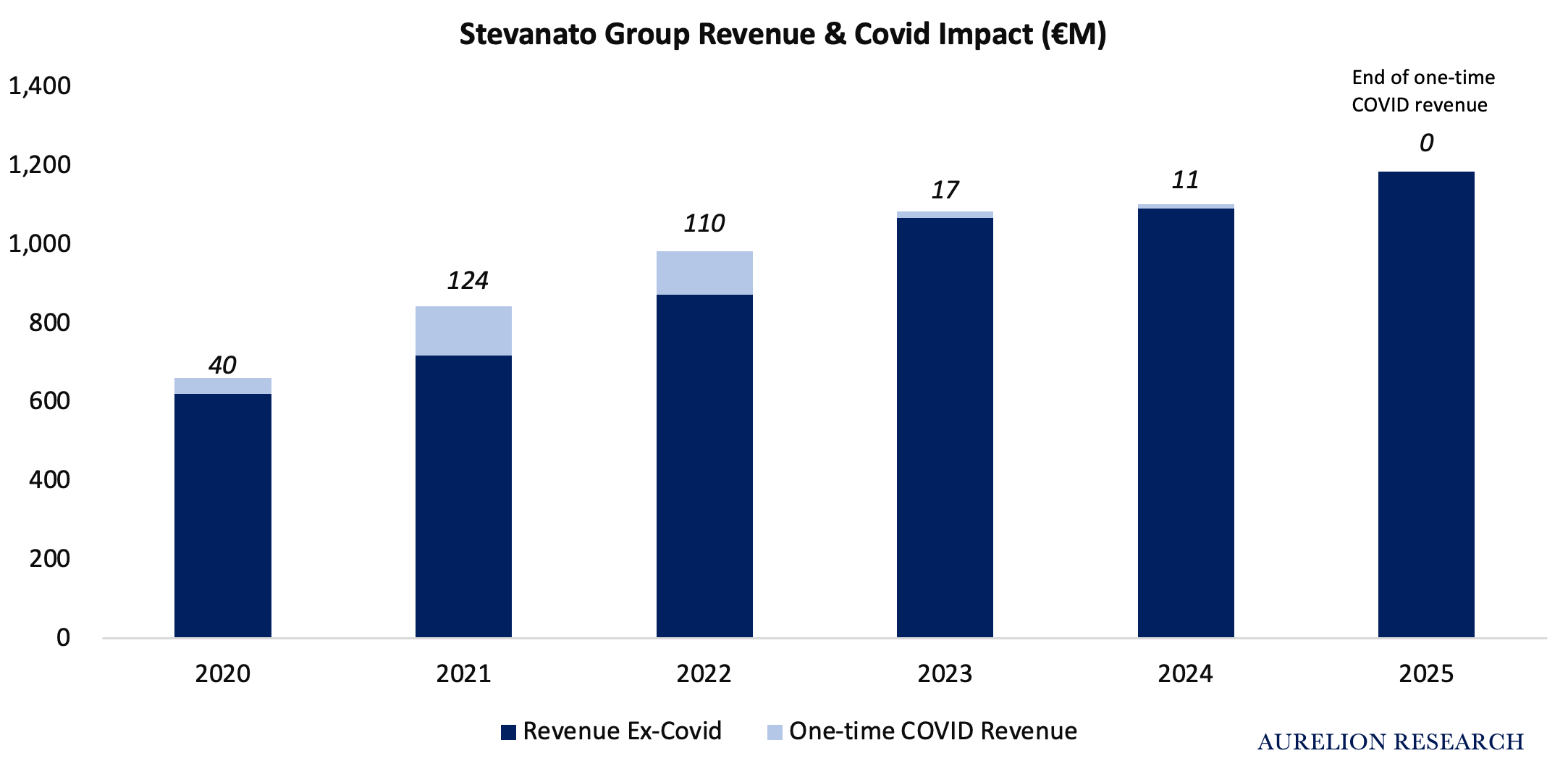

A Word on the Pandemic Impact

Stevanato capitalized on a perfect 2021 IPO window, riding the massive wave of vaccine demand.

However, it’s no longer a 'Covid stock.' We’ve seen those one-time gains be completely replaced by robust, sustainable growth starting in 2023. STVN has successfully moved past its pandemic dependencies and is now growing on the strength of its core business.

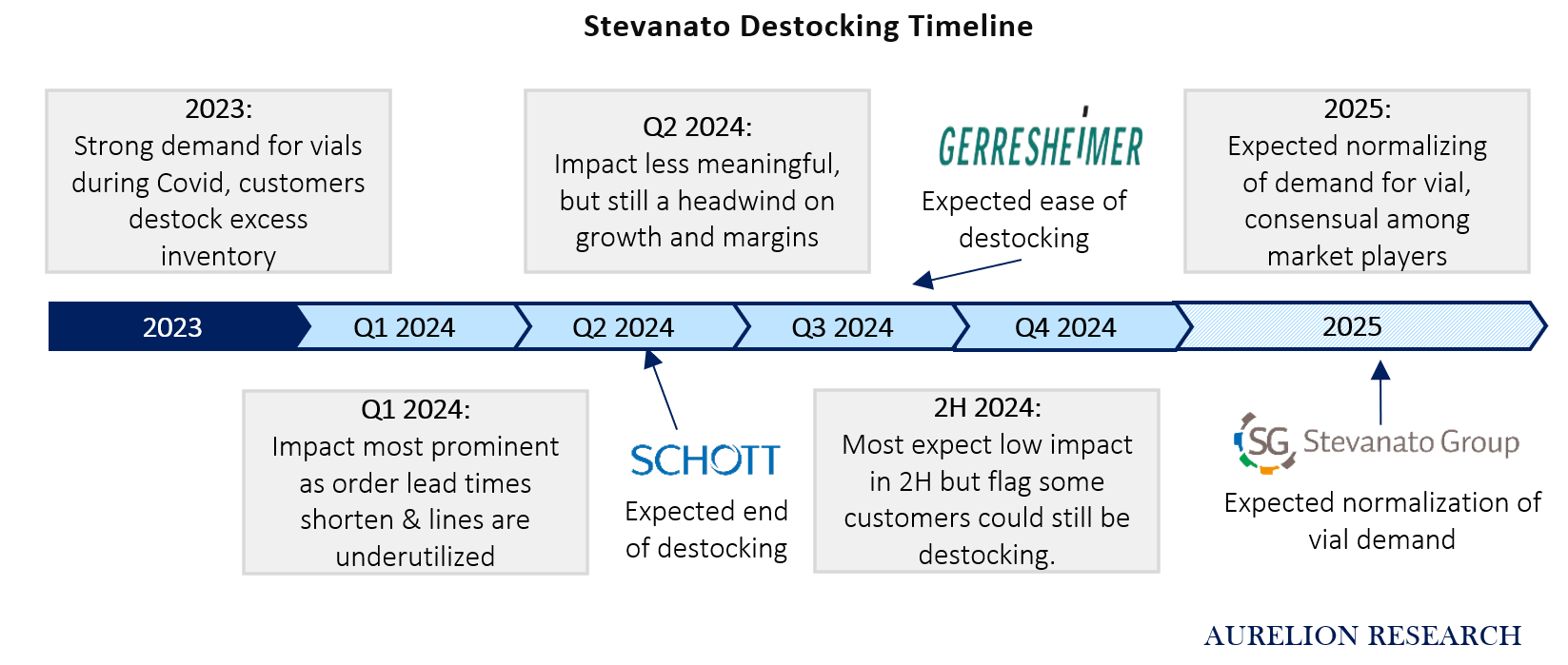

The Destocking Situation: Why We Owned the Stock Before

We personally researched the stock significantly in the early 2025 period because for us the destocking situation was very interesting.

The stock came down very significantly in late 2024 as the expectations for sustained >10% revenue growth stopped. The company was now entering a destocking phase with its large customer, simply meaning that large pharma had ordered too much during COVID and would now order less. We saw this as a short-term noise and bought at a cheap price.

Note that this research was done by an analyst on the team, not officially bought through the Aurelion Index portfolio.

Stevanato by the Numbers

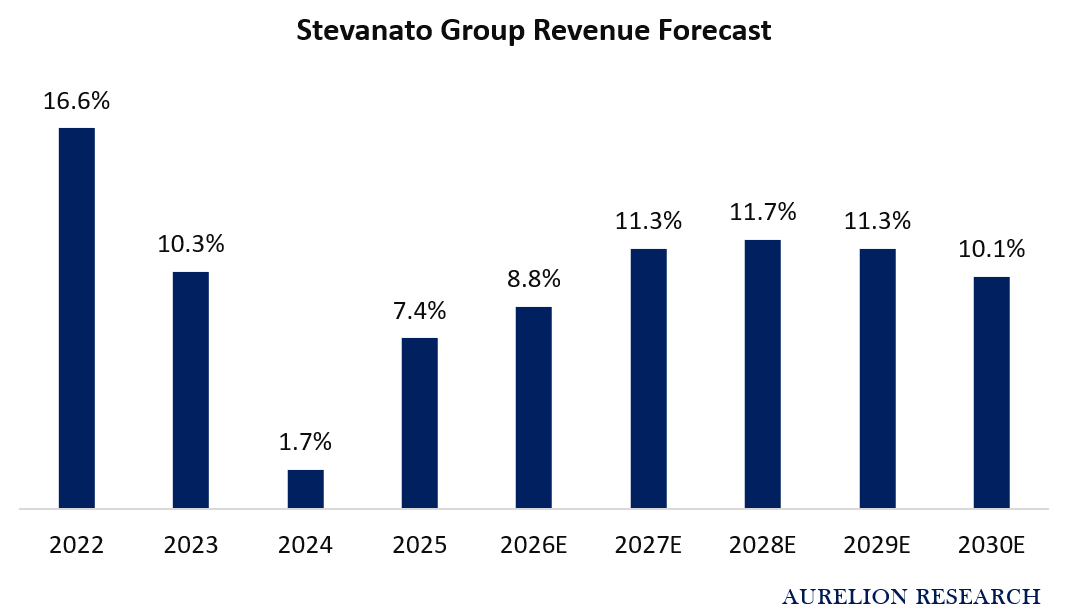

Revenue Targets

Management is currently targeting a return to low double-digit revenue growth of 10% to 12% following the weaker periods seen in 2024 and 2025. The main drivers are the continued mix shift toward high-value solutions and the strong growth of that segment.

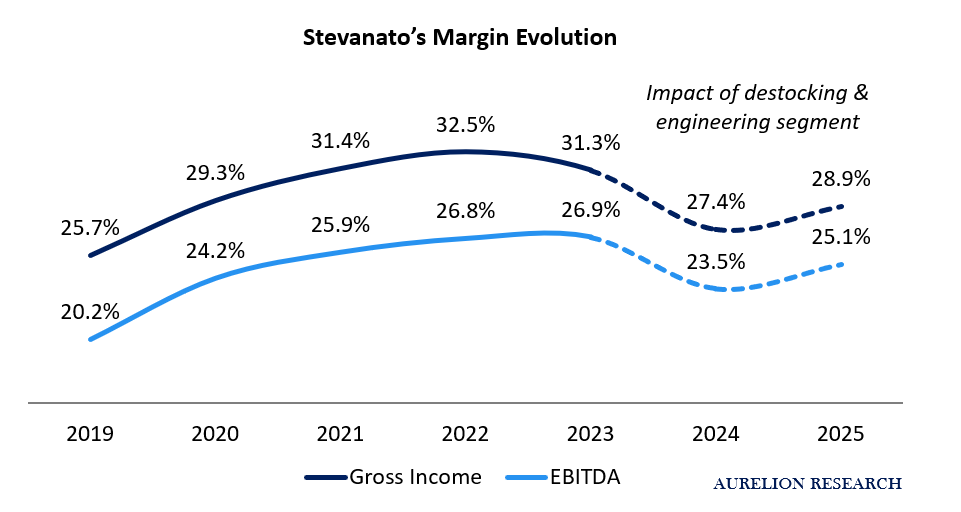

Margin Evolution

Our take: margins were artificially high in 2022 and 2023, then artificially low in 2024 and 2025, and we are now in recovery and expansion mode.

Here is how we see the evolution:

2022/2023 Inflated baseline: Margins were artificially boosted by COVID-driven vial demand. This was not the true earnings power of the business.

2024/2025 Double headwind: Margins then got hit from three sides at once, creating a trough deeper than the fundamentals deserved.

First, destocking crushed volumes. Large pharma had over-ordered during COVID and simply stopped buying, pushing revenue growth negative for the first time since the IPO.

Second, the engineering segment deteriorated, adding a drag on top of the volume headwind.

Third, Stevanato was mid-way through a massive capex cycle, ramping expensive new facilities before they were generating meaningful revenue. This is the classic trough of a capital-intensive business investing ahead of demand.

By 2025 recovery had already begun as destocking faded and the new facilities started contributing.

The path to 30% is therefore not just high-value solution expansion alone. It is normalization from short term issues (facilities now productive, destocking over) layered on top of the high-value shift.

Management Target: From 25 to 30% EBITDA Margins

Management has previously targeted 30% EBITDA margins by end of 2027.

They have since stopped formally discussing this 2027 goal.

We expect the 30% target to slide toward the 2028 timeframe as new facilities ramp up and the high-value mix continues to improve.

As a reminder, high-value solutions carry ~2x the margins of the rest of the business. We calculate ~1.2% of margin expansion per year through 2030 from mix shift alone, simply as a result of selling more high-margin products.

This driver requires no cost cutting, layoffs, or restructuring, and should meaningfully improve margins over the coming years.

We like setups like this because the execution burden is lower, which gives us greater confidence that the margin improvement will actually materialize.

Most companies talk about margin expansion. In our experience, a large share end up behind schedule or miss those targets entirely.

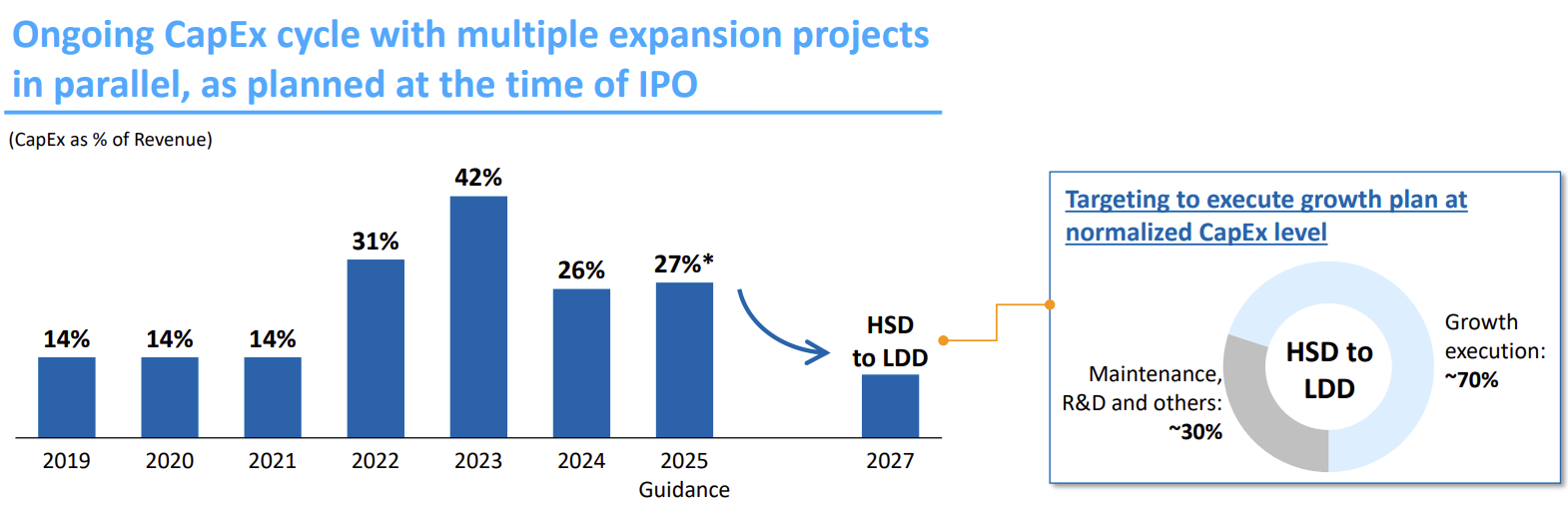

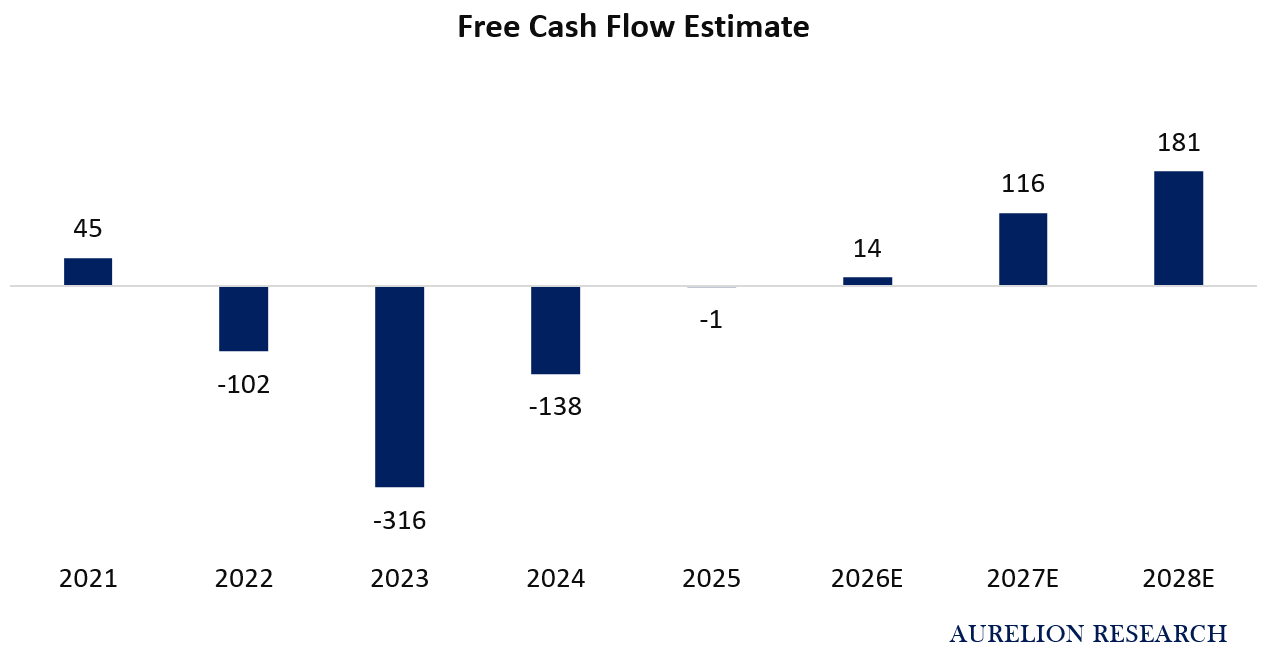

Cash Flow Generation

The chart below captures the story well. The buildout of new manufacturing facilities required an unusually heavy level of capital spending, which drove negative free cash flow for several years. We now appear to be approaching an inflection point, with the major facility investment cycle largely complete.

Stevanato will finally have cash to distribute to shareholders.

Stevanato’s free cash flow profile is finally starting to improve.

After several years of heavy outflows tied to an intense investment cycle, the company appears to be entering a phase where that spending begins to convert into cash generation. As capex normalizes, financial flexibility should improve, with more room to reinvest, strengthen the balance sheet, and potentially return capital to shareholders.

Management

Skin in the game is substantial. The family controls 93% of the voting rights and 80% of the economic interest, with no evidence of meaningful insider selling. This is a business built over 75 years by a family whose wealth remains tied to the stock.

That long-term alignment shows in the company’s history. Stevanato was founded in Venice in 1949 by Giovanni Stevanato. His son, Sergio, transformed it into a serious industrial company and was later awarded the title of Knight of Labor by the President of Italy, one of the country’s highest business honors.

Today, the business is led by Franco Stevanato, Sergio’s son and the company’s current CEO, who grew up visiting his grandfather’s factory on Saturdays. This is a family that has spent 75 years building deep expertise in a single industry and turning that focus into a world-class business.

2. Industry Overview

End-Markets Driving the Stock

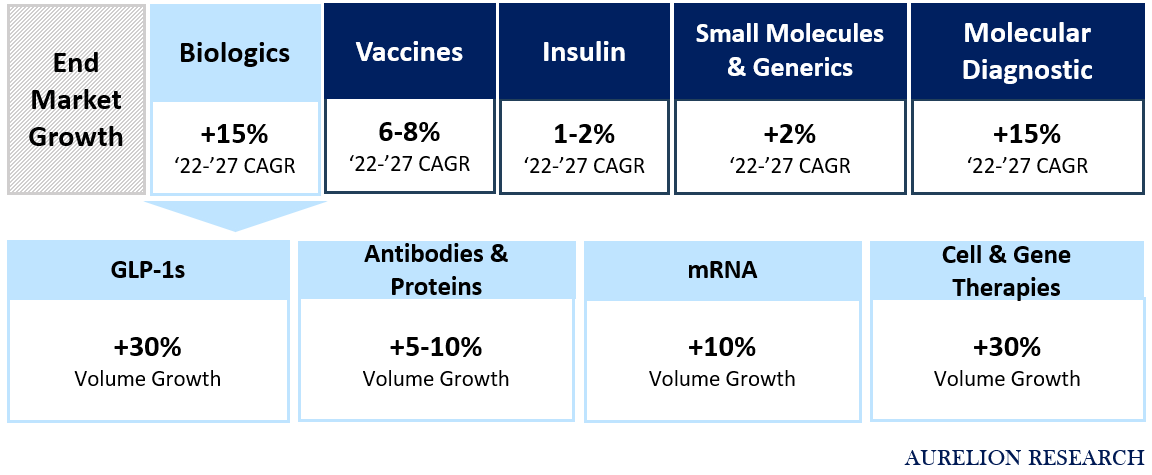

Stevanato is increasingly a biologics-driven business. High-value solutions, which are heavily tied to biologics and GLP-1 delivery formats, accounted for 46% of total company revenue in 2025 and grew 29% year over year.

The company is not evenly exposed across all end markets shown in the chart below. It is disproportionately positioned in the fastest-growing segments, specifically biologics at +15% CAGR and GLP-1s at +30% volume growth.

This is precisely what drives the revenue growth thesis and why Stevanato consistently grows 2 to 3x faster than the broader containment market.

Large Pharma Impact

Large pharma health matters, but less than many investors assume. The more important variable is biologics volume.

It is easy to link Stevanato’s performance to large pharma revenue, but that framing misses the core driver. Stevanato does not get paid when Eli Lilly or Novo Nordisk sells a drug. It gets paid when those companies manufacture and fill vials, syringes, and cartridges. That is ultimately a volume story. A pharma company can post a weak quarter because of pricing pressure or patent expirations and still be producing more units than ever.

For Stevanato, pipeline volume matters more than pharma profitability.

There are over 10,000 drug candidates currently in clinical development globally, with pharma companies spending over $300bn annually on R&D (IQVIA Institute for Human Data Science, 2024).

That pipeline has to be packaged, filled, and delivered. Biologics and gene therapies are forecast to represent over 60% of new drug approvals by 2030 (Deloitte Global Life Sciences Outlook, 2024). Stevanato is precisely positioned for that shift. Even in a world where large pharma margins compress, the volume of injectables being manufactured keeps climbing.

The scenario investors should watch is a prolonged collapse in large pharma R&D spending, which could slow new drug launches and reduce demand for high-value packaging formats. But this would need to be severe and sustained to meaningfully dent Stevanato’s trajectory, given how far ahead of current demand the pipeline is.

Our view is that investors should not spend much time worrying about pharma company’s quarterly earnings. The structural question is whether global biologics volume keeps growing. Every credible forecast says yes, and that is the only datapoint that truly matters for Stevanato’s long-term thesis.

Competitive Space

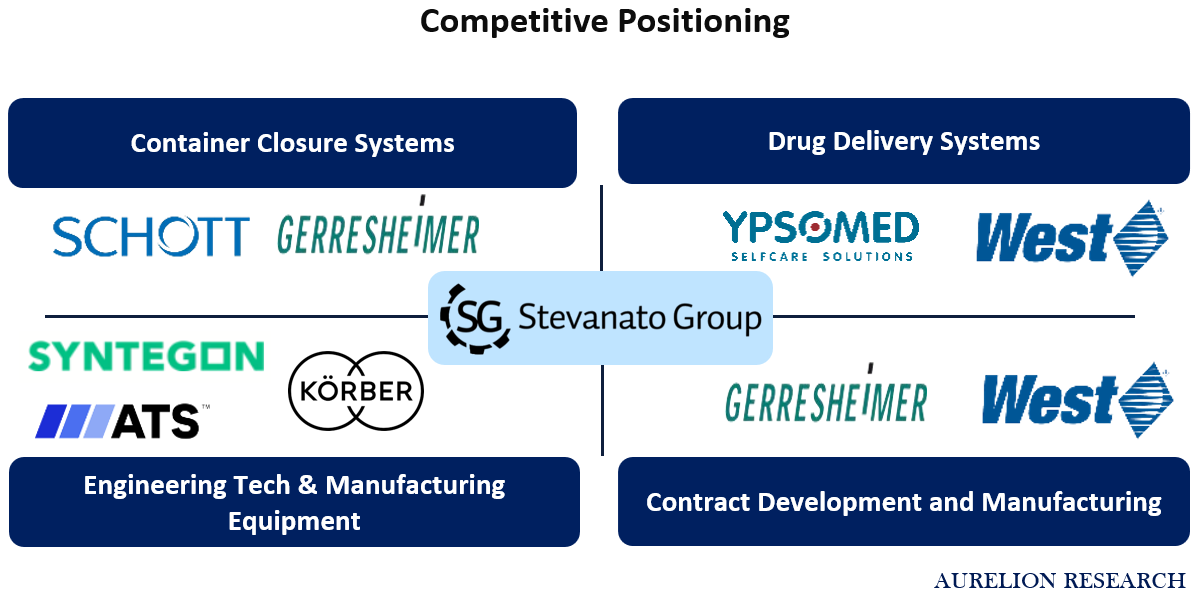

The competitive landscape is an oligopoly.

The companies capable of producing pharmaceutical-grade syringes and cartridges at commercial scale are essentially four: SCHOTT Pharma, Gerresheimer, Stevanato, and Nipro. Together they produce around 3 billion pharmaceutical syringes per year. This is not a fragmented market where a new entrant can show up and take share. It is a small club of highly specialized manufacturers with decades of regulatory history, validated processes, and deeply embedded customer relationships.

Worth noting: it is standard practice in pharma to qualify two suppliers for any given drug program, typically pairing two members of this oligopoly together, for example Stevanato alongside SCHOTT, to ensure supply chain resilience. This means Stevanato does not need to displace a competitor to win business. It simply needs to be one of the two approved suppliers.

Vertical integration separates Stevanato from the pack. Unlike peers, Stevanato controls around 80% of its supply chain, from glass forming to packaging machinery, enabling customized automation that materially reduces total cost of ownership for customers. Most competitors own one part of the value chain. Stevanato can offer containment, delivery format, and the manufacturing equipment to fill it, all under one roof.

The GLP-1 wave is making the oligopoly tighter. All four players are racing to add capacity simultaneously. SCHOTT Pharma announced a $371M facility in North Carolina targeting GLP-1 containers, expected operational in 2027. Gerresheimer acquired Bormioli Pharma for roughly €800M to consolidate its position. Stevanato is doing the same with its Fishers, Indiana facility.

As you can see above, the capital requirements to compete at this level are enormous, which reinforces the barriers to entry rather than weakening them. A new competitor would need to spend billions and wait a decade before being qualified by a major pharma company.

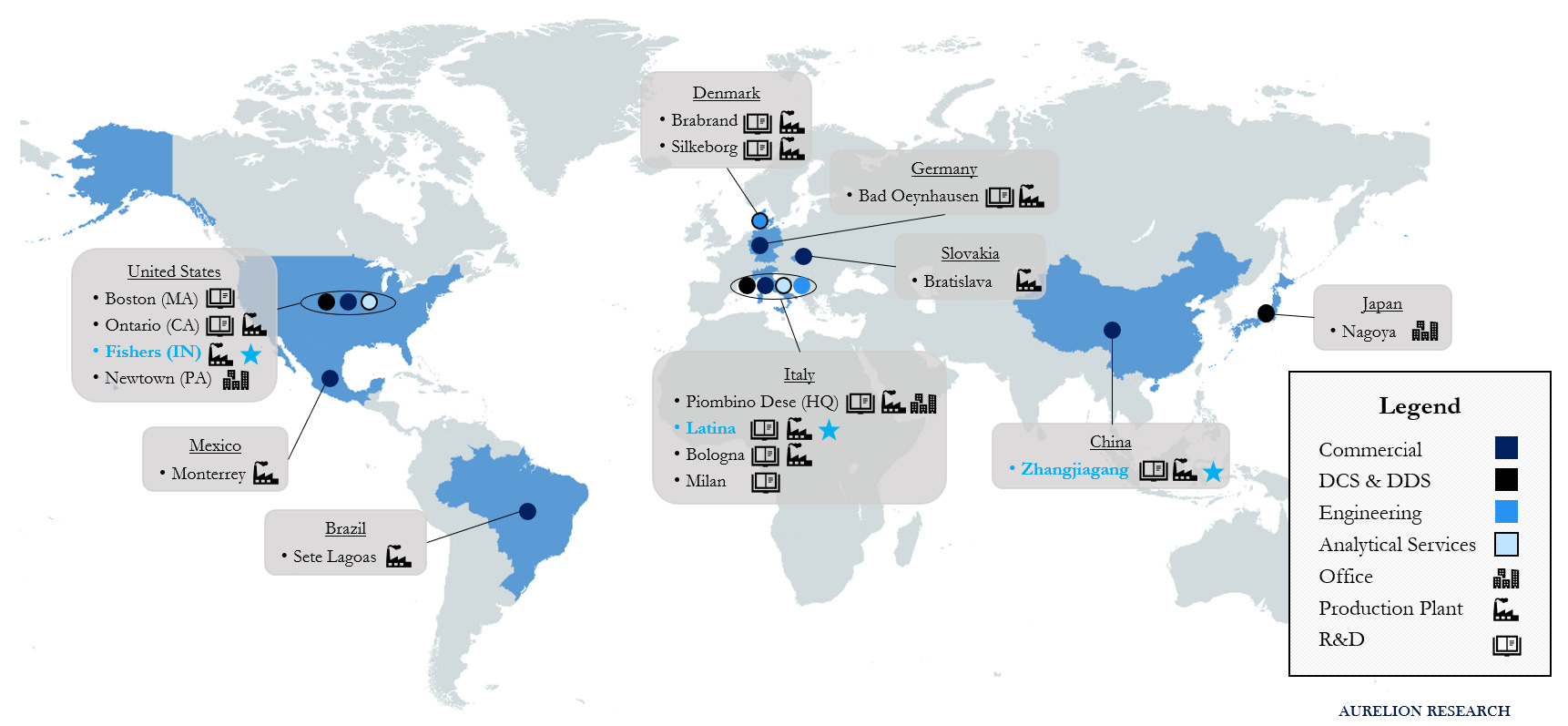

3. Geographic Footprint & Customer Proximity

Stevanato operates nine manufacturing plants globally. What is striking about this footprint is that the company has quietly built one of the most geographically strategic supplier networks in pharma packaging, with facilities in every major biologics manufacturing hub in the world.

Over the past several years, Stevanato has committed billions in capital to two regions: northern Italy and Fishers, Indiana. When you map those locations against where the world’s largest GLP-1 drug manufacturers are building their own production capacity, the overlap is clear.

Fishers sits 35 miles from Eli Lilly’s Lebanon, Indiana campus, where Lilly is spending up to $27 billion manufacturing Mounjaro and Zepbound.

We infer Lilly is the largest customer. We cannot confirm it, but we are comfortable making that call based on the geography, the product alignment, and the capital commitment timing on both sides.

This brings us to the GLP-1 risk. Stevanato has concentrated a significant portion of its new capacity in facilities that are, by our analysis, heavily oriented toward GLP-1 injectable demand. If that bet is right, Fishers becomes one of the most strategically valuable pharmaceutical packaging facilities in North America. If GLP-1 injectable volumes shrink, the ramp assumptions for that facility come under pressure. We discuss exactly that risk, and why we think it is overstated, in the section that follows.

4. GLP-1s: Analysis of the Impact

GLP-1 oral approval fears are the primary reason the stock has sold off since the start of 2026.

What are GLP-1s and Why do They Matter for Stevanato?

GLP-1s are the blockbuster weight-loss and diabetes drugs you have probably heard of: Ozempic, Wegovy, Mounjaro, Zepbound. They are injected, typically weekly, using a precision glass cartridge or syringe. Stevanato makes those containers. As GLP-1 demand exploded, Stevanato became one of the key beneficiaries, with management confirming that GLP-1 related products represented approximately 19-20% of total company revenue in 2025, growing more than 50% year over year.

Why is the Stock Down?

In late December 2025, the FDA approved an oral version of semaglutide, opening the door for some patients to take a pill instead of an injection. If that shift becomes meaningful, Stevanato would sell fewer glass cartridges. That is the core concern. It is easy to understand, and the stock sold off sharply on the announcement.

From the patient’s perspective, the appeal is also straightforward. Taking a pill is clearly more convenient than a weekly injection, especially for those who prefer to avoid needles.

The market’s question is therefore simple: if GLP-1 therapies move in an oral direction, does Stevanato’s growth story begin to weaken materially?

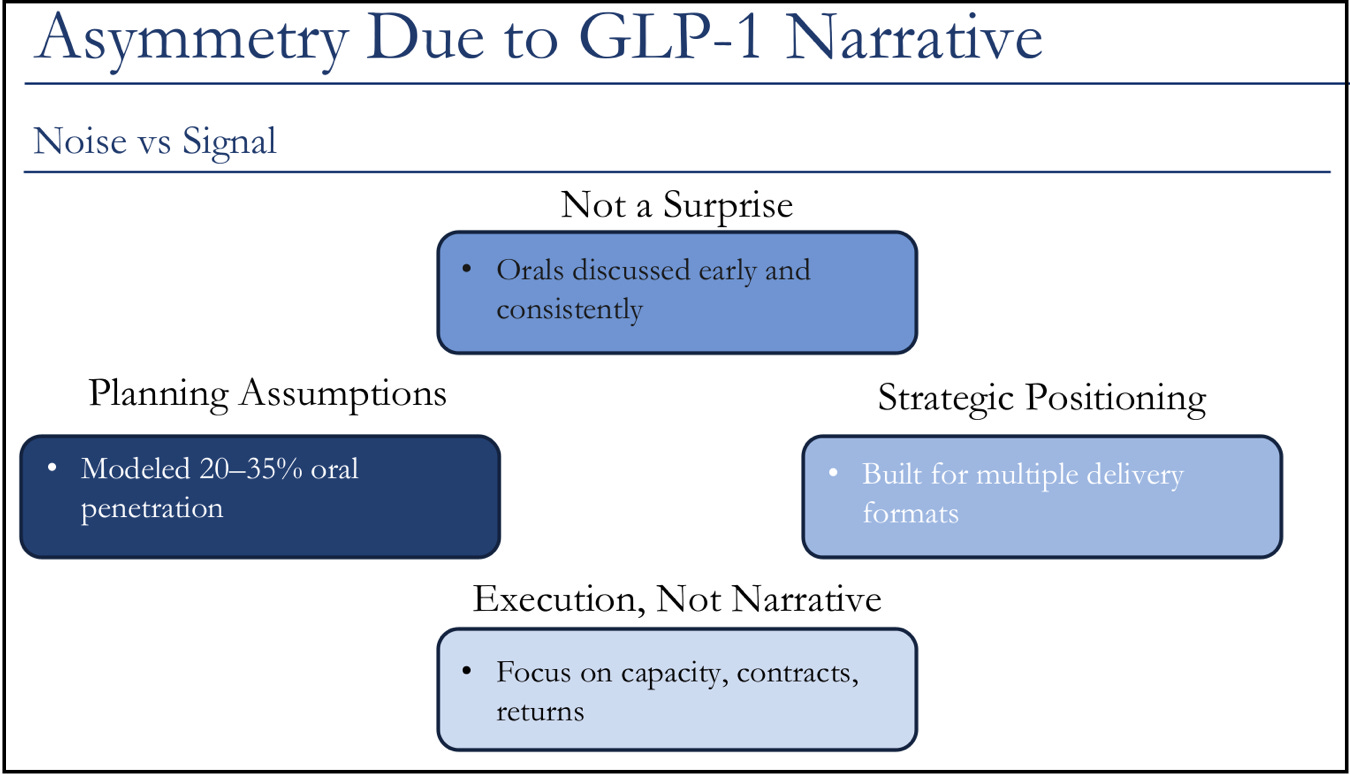

In short, our view is that this fear is real but significantly overstated, and the IQVIA research we cover in the next section explains why. The short version: orals and injectables serve different patient needs, the injectable volume already locked into approved programs is not going anywhere, and the total GLP-1 market is still in its earliest innings.

5. Takeaway of our Discussions with Industry Experts

IQVIA Researcher

What is IQVIA and why does it matter for this thesis. IQVIA is the gold standard data provider for pharmaceutical market intelligence. Stevanato itself uses IQVIA forecasts to plan capacity investments, meaning the same data shaping their internal decisions is available to us. We had a conversation with a researcher (we are keeping the name private) at the IQVIA Institute and also had access to their latest public report, “The Global Use of Medicines 2025: Outlook to 2029”, available freely on their website.

His take on the current efficacy of Oral GLP-1s. Oral bioavailability for peptides remains below 1% versus more than 50% for injectables. Oral semaglutide also requires ~70x more active pharmaceutical ingredient per dose, creating worse unit economics at scale. The compliance burden of daily oral dosing with strict fasting requirements is a real barrier, and the industry is actually moving toward longer-acting monthly injectables, which only deepens the moat for precision injectable packaging.

The IQVIA researcher was direct about Orals taking share. Orals will take share, particularly among needle-averse patients and those needing only modest weight loss. The pipeline has over 50 oral assets in development, and next-generation small molecule formats will be more competitive than today’s oral semaglutide. If oral penetration accelerates faster than expected, a portion of future injectable volume growth would simply be foregone.

On oral GLP-1 risk to Stevanato specifically, he was relaxed. Even if oral formats gain share over time, the transition would be gradual. The regulatory switching costs alone make a rapid format change essentially irrational for pharma companies mid-lifecycle.

He was also bullish on the biologics pipeline. Obesity drug spending is projected to grow at a 23% to 26% CAGR through 2029, while less than 10% of the obese population has been treated so far. Oncology spending is expected to reach $441bn annually by 2029. His framing was clear: this is not a demand issue, it is a capacity issue.

Practicing Physician

His take was that patients find the oral semaglutide routine genuinely difficult. Empty stomach, then 30 minutes with no food or liquids, every single day. Weekly injections are easier to stick to for older and chronic patients. In his view there is a use case for both. The industry has already acknowledged this, which is why the real innovation is heading toward monthly injectables, not away from injectables altogether.

Our Thoughts on GLP-1s

Let us be clear: oral GLP-1s are a headwind. If they never existed, the injectable volume story would be cleaner and the growth runway longer.

The stock does not currently deserve its $33 peak of 2023. The question is not whether orals create some competitive pressure, they do, but whether they actually displace injectable volume in any meaningful way. Our conclusion, is that they largely do not.

Another IQVIA publication, “Oral Obesity Therapies: Holding the Key to the Future” states that orals are best positioned as maintenance options following injectable induction, not as replacements. The two formats serve different roles in the journey.

On the broader GLP-1 volume story, IQVIA is unambiguously bullish.

In their November 2025 report “GLP-1 Impact: How GLP-1s Are Changing the Diabetes Treatment Paradigm,” IQVIA authors Luke Greenwalt and Jeff Thiesen document GLP-1s reaching $110bn in global sales in 2024. Yet less than 10% of the obese population has been treated by the drug. By May 2025, GLP-1s accounted for 52% of all diabetes prescriptions, up from just 18% in 2020. In our view the runway for volume growth remains enormous.

We believe GLP-1 injectable volumes will continue to grow, supported by expanding global demand, the large share of severe diabetes and obesity cases that still require injectable efficacy, and older or chronic patients who are more likely to remain on injectable therapies.

The stock does not deserve to return to its prior peak, in our view, because this is a real long-term headwind. At the same time, the selloff appears excessive, and we believe the shares are clearly oversold.

To put the oral GLP-1 concern in perspective, even if Stevanato were to lose 50% of its entire GLP-1 revenue tomorrow, the stock would still trade at roughly 13.8x EBITDA. The market was routinely willing to pay a higher multiple than that before GLP-1s were even part of the story.

We will continue to monitor pharmaceutical volume trends across oral and injectable GLP-1s closely as we stress test the thesis.

6. Our view of Q4 2025 Earnings

We added STVN to the portfolio on March 3rd, ahead of earnings, expecting a beat. That is what we got. The stock moved +19% the following day.

The Quarterly Numbers

The quarter was clean across the board. Revenue came in at €347M, ahead of estimates, driven entirely by the core business.

EBITDA came in at €98M, significantly above estimates at €92M.

Free cash flow was + €1.5M, versus estimates of negative €39M.

The engineering segment missed badly at negative 30% revenue growth, but as we discuss in the business overview, the market does not move on engineering and neither do we.

The GLP-1 Disclosure

The most important moment of the call was management finally disclosing their GLP-1 exposure directly. GLP-1 products represented 19 to 20% of total company revenue in 2025 and grew more than 50% YoY. This was the first time management put a specific number on it.

Equally important was management’s commentary on 2026. GLP-1 revenue is guided to grow at a mid-teens rate. Running the math, if GLP-1 represents 20% of revenue and grows 15%, that alone contributes ~3% to total growth.

With management guiding to ~7.5% total revenue growth, the implication is that the other 80% of the business is growing at ~5.6%. Moreover, the number of customers ordering premium syringes for non-GLP-1 biologics increased 40% year over year. The growth story is wider than GLP-1s.

2026 Guidance

2026 guidance came in slightly below expectations. Many investors were anticipating closer to low double-digit revenue growth, but management guided for only 7.5%. Capital expenditure expectations also came in still slightly higher than the market had hoped, with 89% of being growth capex.

Our Takeaway

The beat was broad-based, the GLP-1 disclosure removed a key uncertainty, and the broader contribution from non-GLP biologics came in as a positive surprise. Guidance was slightly softer, however, as GLP-1 is set to contribute less to growth than some had expected. Even so, nothing in the outlook changes our long-term view of the setup or the quality of the business.

7. Investment Thesis

Our conviction on the stock has not changed. The reasons we own it today are the same ones we outlined in our initial report in early 2025.

1. Valuation Does Not Reflect Earnings Power

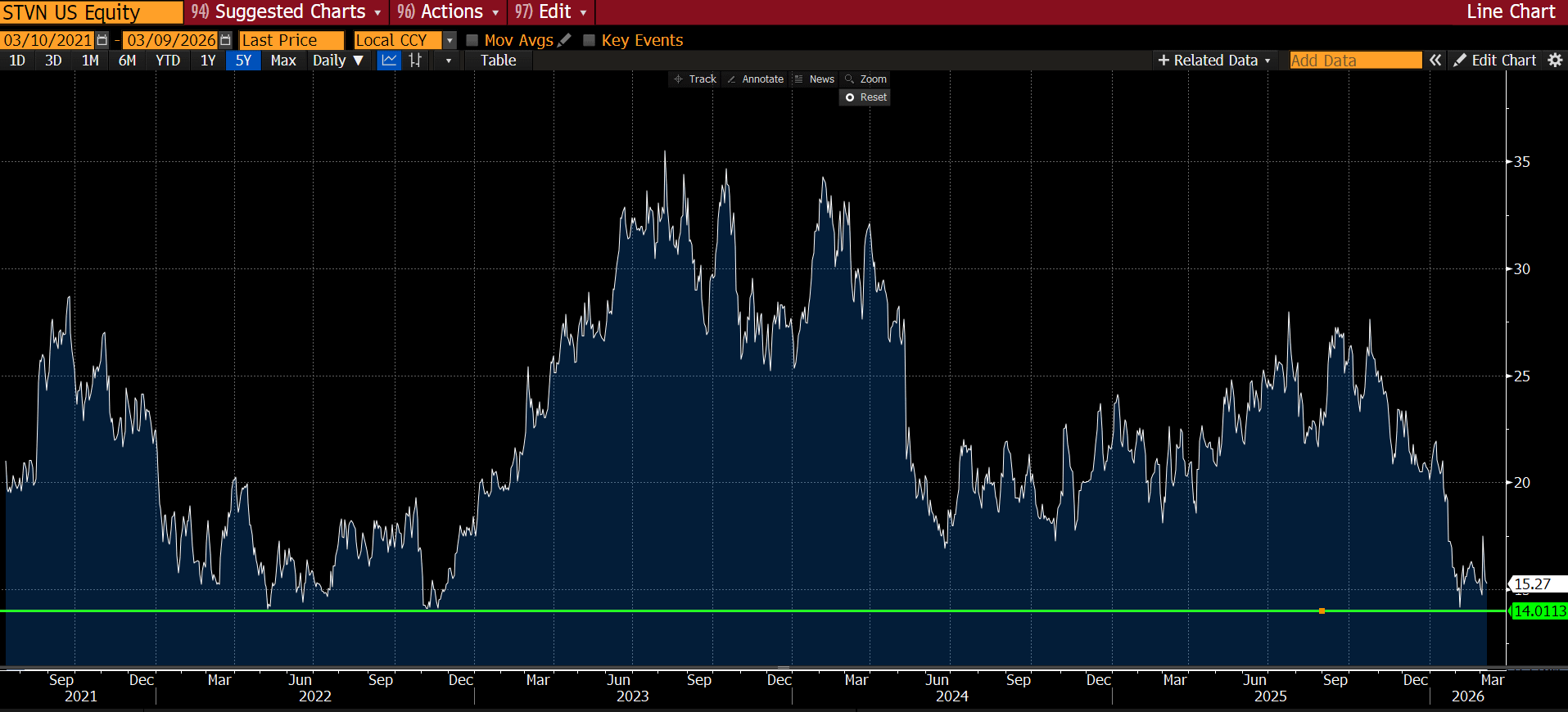

This impact is clear in the price history. Shares have traded in a wide range since 2021 and currently sit well below previous peaks. This compression happened even as revenue continued to grow and long-term demand remained generally steady. In our view, the market has priced in a permanent state of weakness instead of a temporary return to normal levels.

2. A Strong Free Cash Flow Inflection

At the same time, the financial profile is reaching a turning point. Free cash flow hit its lowest point in 2023 when capital spending peaked at nearly 40% of revenue during a major global expansion. That investment cycle is now largely complete. This shift changes the story of STVN from one that consumes capital to one that generates cash.

3. GLP-1 Fears Are Overblown

The debate around new drug delivery formats also adds to the opportunity. Management has already planned for these shifts by building flexibility into their production. These developments are well understood by the company and are not a surprise.

We see a business moving into a period of higher margins and cash generation while the stock price still reflects peak uncertainty. As spending declines and cash flow rises, we expect the valuation to follow.

8. Forecasts, Valuation & Price Targets

Financial Forecasts

Our revenue forecast is broadly in line with management’s target for low double-digit growth, while also reflecting lower expected growth from GLP-1. The main driver remains the continued expansion of high-value solutions.

We think this forecast appropriately ties revenue growth to the capital spending needed to support it. All of that growth is organic and does not rely on acquisitions. We are also around 1% above Bloomberg’s current revenue growth consensus.

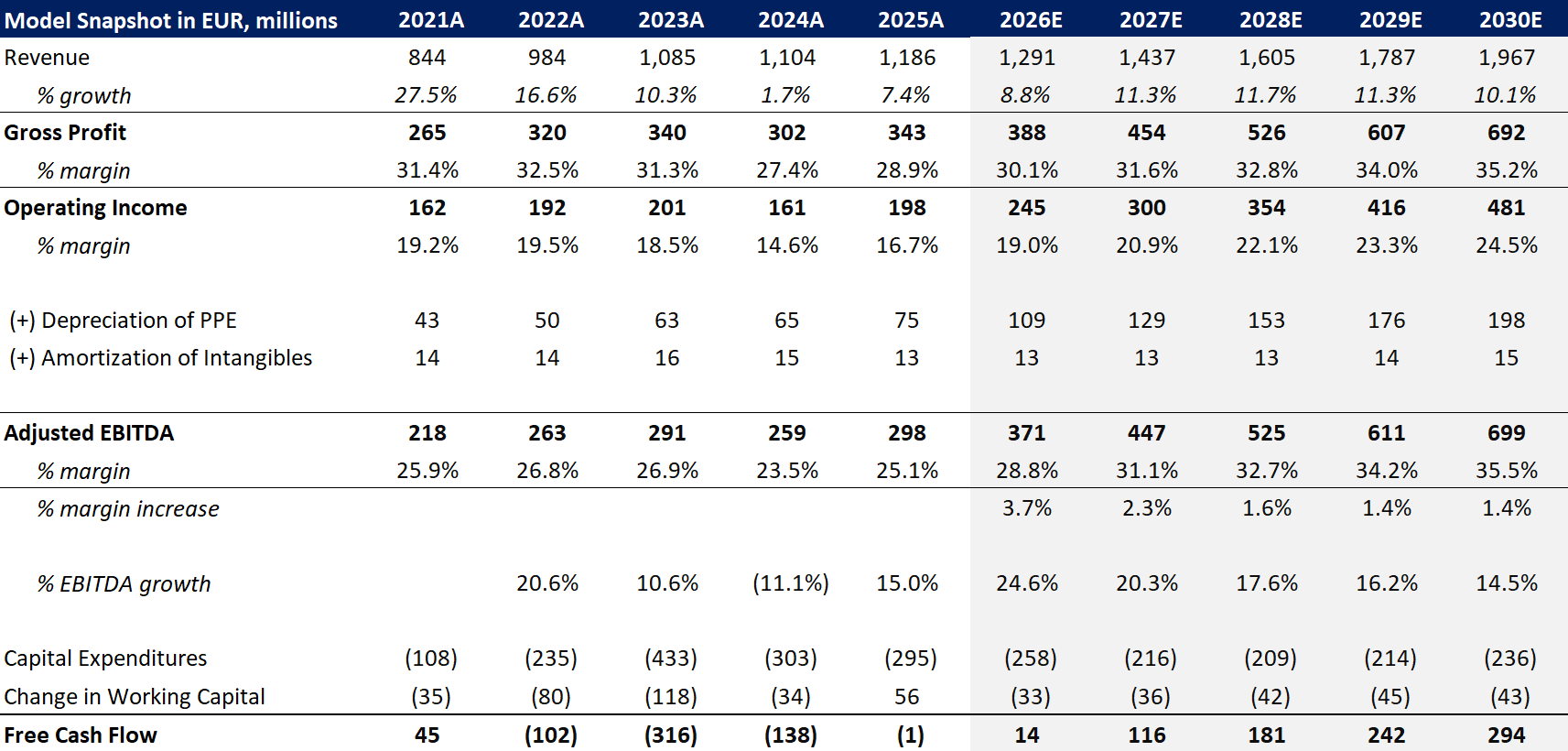

Below is a snapshot of our financial model.

As you can see, our forecast implies a 18.6% earnings CAGR.

This is pretty much one of the highest in scaled life science companies.

Stevanato Financial Model Snapshot

Margins: We forecast margin expansion to come primarily from a richer mix of high-value solutions, with little contribution from other sources of improvement.

Depreciation Expense: Given the heavy capital spending over the past few years, we expect depreciation expense to keep rising and remain a drag on reported earnings.

Free Cash Flow: As noted earlier, FCF should turn positive as capital expenditures normalize. We estimate normalized EBITDA-to-free-cash-flow conversion at ~40% to 50%, which is reflected in our valuation. This remains a business that needs ongoing capital spending to support growth.

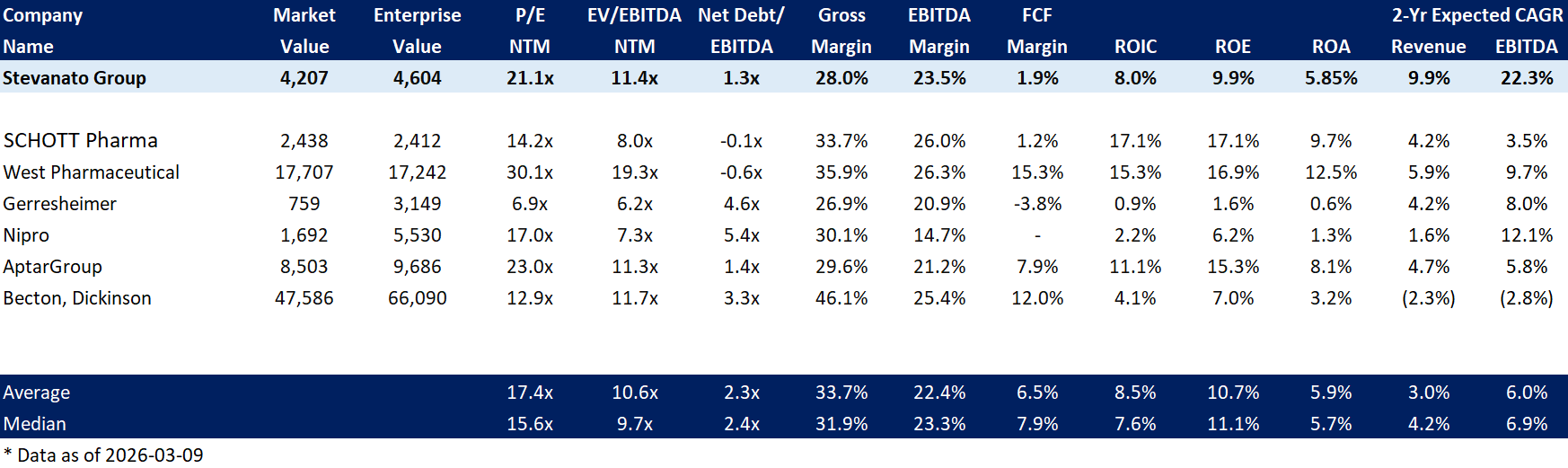

Our Valuation of Stevanato

There are important valuation implications to STVN requiring substantial capital investment to grow. The 40-50% cash conversion implies that at an 11.0x EBITDA multiple, we are effectively paying for a 22.0x FCF company. In our view this is warranted, as STVN is a high-growth, high-quality business.

However, a return to the prior 20.0x EBITDA multiple would imply roughly 40x FCF, a level we consider excessive.

As you can see below, historical valuation has averaged ~20x EBITDA, which at normalized free cash flow conversion implies ~40x free cash flow.

We think there are 3 significant drivers that institutional money managers like, that used to drive up the valuation.

The long-term contracts and specced-in moat give significant long-term visibility into the business continuing to exist, meaning we can be more certain applying a high multiple in 5-10 years.

A substantial biologics growth story. It is an easy trend to believe. Not only GLP-1, but many biologics require STVN, and STVN is undoubtedly very strong in their specific corner of the container industry.

An easy-to-believe margin expansion opportunity. The switch to high-value solutions is an easy sell for investors, as the company doesn’t even need to cut costs to significantly expand margins.

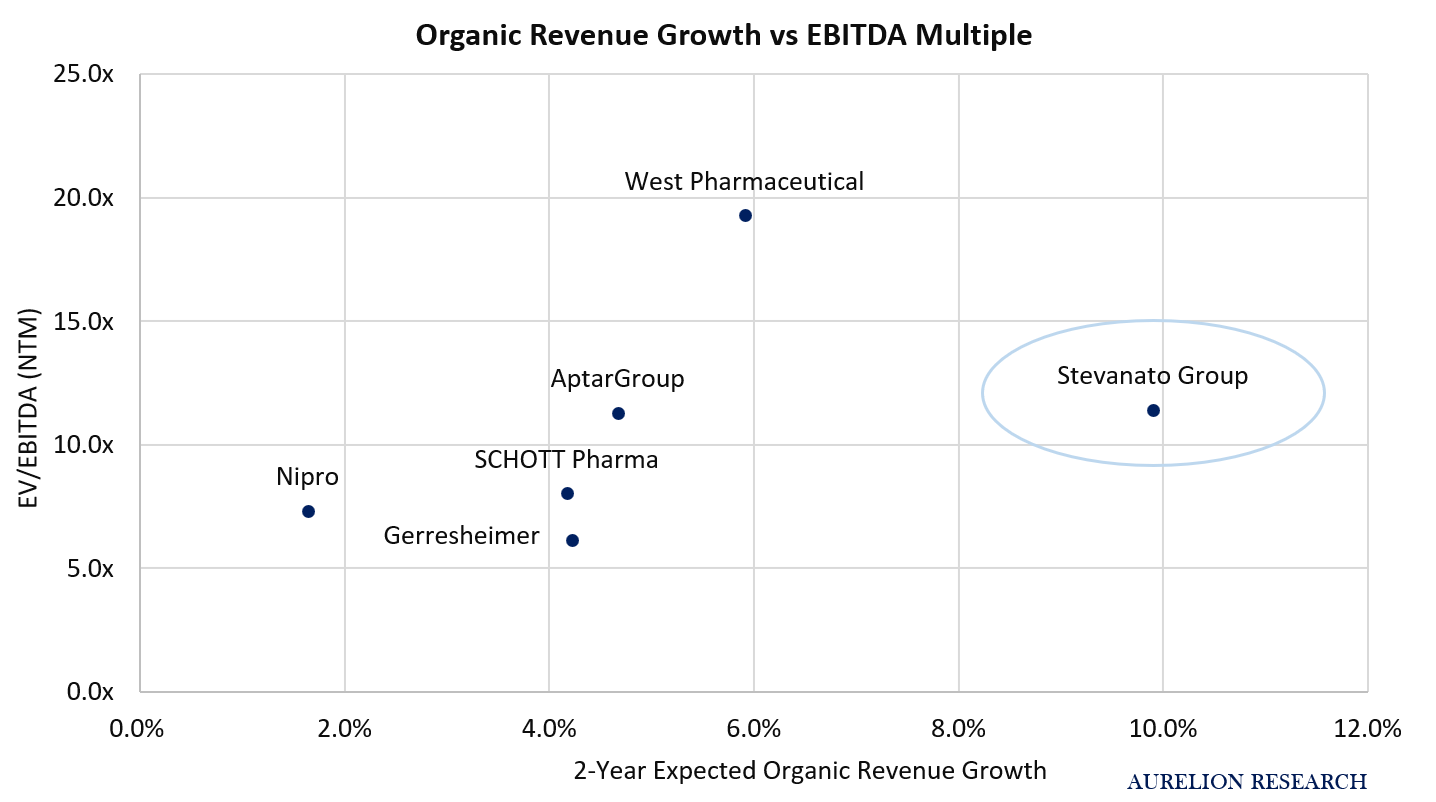

Below, we compare Stevanato with competitors and other companies operating in similar parts of the market. What stands out is that the stock trades at a higher valuation, but that premium is supported by meaningfully stronger revenue and earnings growth than most comparables, which in our view leaves the risk-reward compelling.

Stevanato vs. Peers

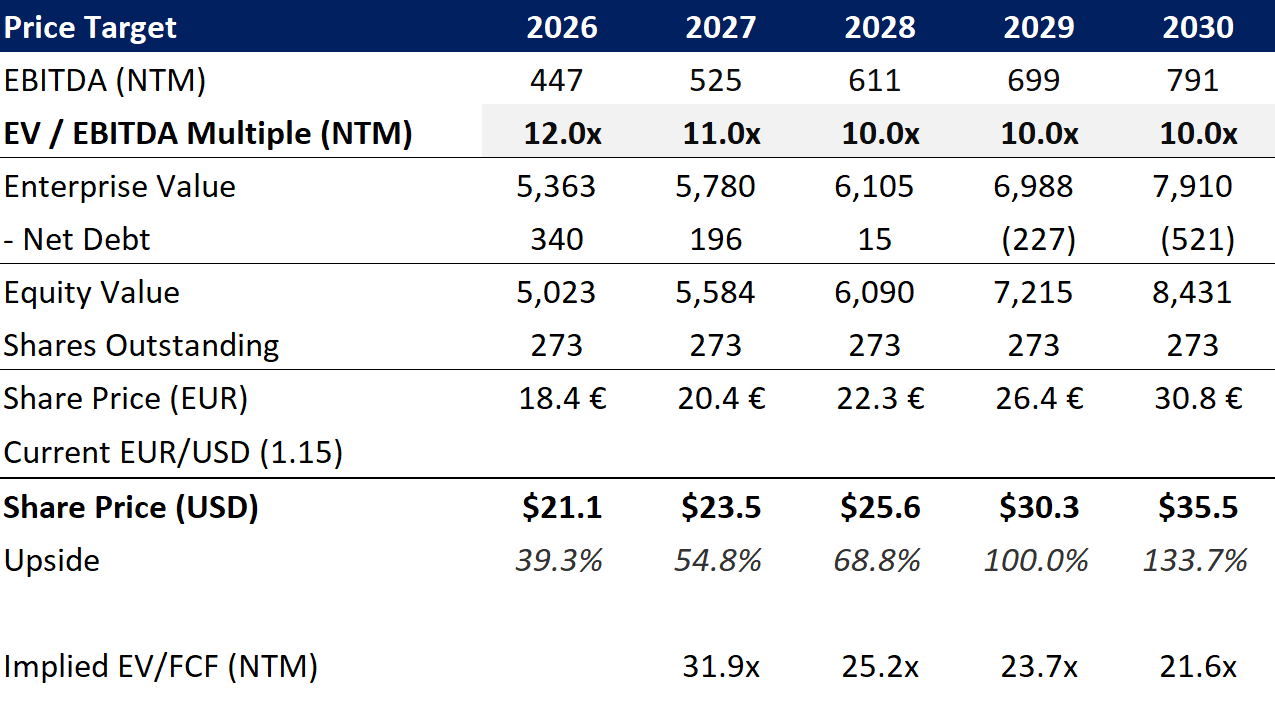

We use a long-term multiple of 10.0x EBITDA, reflecting where we think the stock will trade in 2030, implying ~22x free cash flow. We do not expect a sustained 20.0x EBITDA multiple like in the 2022-2023 period.

However, continued revenue growth, stronger cash generation, and a solid moat in the space support our confident use of that 10x multiple. This is also still below larger scaled peers, which is what Stevanato should increasingly resemble over time.

How Much Upside Do We See?

1-Year Price Target: $21 (39% upside)

5-Year Price Target: $36 (134% upside over a 5 year period)

$14 has been the floor the market has been willing to accept since the IPO in 2021. We are not technical traders, but we believe it is reasonable to say the business would need to deteriorate meaningfully from current levels to break below that threshold.

This is a loved stock among many funds, and we believe investors are simply waiting for perceived headwinds to clear before buying back in. In our view, a return to a $20 stock price is the most likely scenario, with limited downside at $15.

At this point we do not think we are catching a falling knife. The stock appears to have stabilized following the peak of GLP-1 fears.

Importantly, we view this stock as set for a sharp move on a positive catalyst. The most recent earnings were good, not amazing, and the stock still moved +19% in a single day. This is precisely why we like the risk/reward here. If the company misses next quarter we do not expect a similarly sharp decline, but if they beat expectations or raise guidance, we see the upside reaction as disproportionately large.

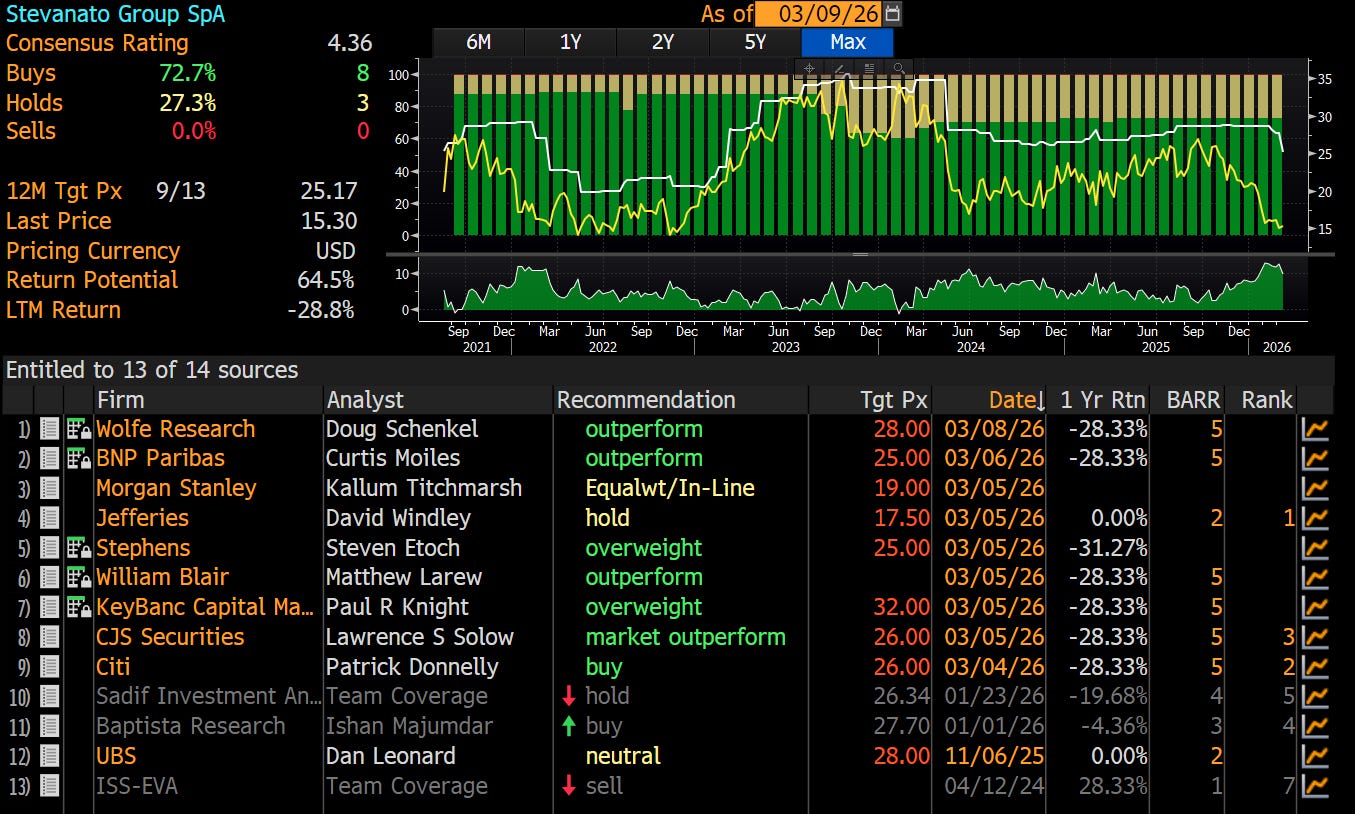

Current Analyst Recommendations

Analyst recommendations remain broadly unchanged despite the stock being down 28% year to date, with most maintaining Buy or Outperform ratings.

Key Risks

Key man risk. Franco Stevanato is both CEO and the embodiment of the family’s long-term vision. A leadership transition would create significant uncertainty around strategy and ownership.

US tariff and currency headwinds. Stevanato is an Italian company with significant US revenue exposure, making it vulnerable to both foreign exchange moves and evolving US trade policy.

Oral GLP-1 almost completely replaces injectables. If next-generation oral formats gain meaningful share in induction therapy, injectable volume growth would be heavily impaired. This is the risk we monitor most closely.

Our Final Take on STVN

Stevanato is a rare combination of business quality, earnings growth, and a mispriced valuation. The oral GLP-1 fear is real but overstated in our view, the destocking headwind is behind them, and the capex cycle that weighed on cash flow for years is nearly complete. The business is entering a period of higher margins and free cash flow generation for the first time since the IPO.

We hold the stock and will monitor GLP-1 injectable volumes closely as the key variable to stress-test the thesis.

The Aurelion Team

Disclosures & Methodology

Another great idea and good write up.

Business looks solid, owner-operated, produces a critical product in the pharma value chain (not getting distrupted anytime soon). Company adds capacity based on customer demand, vertically integrated.

Want to discuss the risks:

Only major risk i see is shift towards orals for biologics. Why is the market so much worried about that?

Reading about this transition, the oral is in fact beneficial to the company's growth.

Patients start with orals if they had needle phobia but orals have limitations, it works for a few weeks and hits a plateau. To continue getting better results, looks like patients have to transition to injectables. If this is true, STVN is sitting on a huge opportunity ahead.

I am humbled to realize i dont know what the market knows regarding the recent slide.

Also, the float is super low (18%) with 82% held by the founding family.

If sentiment is weak, it could push the stock easily down. But if the sentiment gets better, it could go up easily.

Bought STVN 3 months past. Waiting patiently whilst monitoring the thesis and rerate environment. Earnings upcoming will add some color .