Special Tanker Report: US-Iran Impact

We explain why we believe tanker stocks are ignoring the current rate boom.

Today’s report is a highly relevant one. As the title suggests, we are looking at tankers, which is the primary focus for the market right now. We anwser 3 key questions:

1) Why tanker stocks are not rising despite record spot rates.

2) Whether the current tanker market strength is temporary or structural.

3) Which stocks are best positioned to benefit from the current market.

We bring expertise and a track record in the tanker industry to the table. This is rare in North America. While shipping analysts are usually found in Norway, Denmark, or Greece, they are scarce in the US, and in Canada, they are basically non-existent.

We currently see an exceptional tanker market. As many of you recognize, spot rates have jumped even higher. A red hot environment defines tanker shipping, and momentum remains clearly positive. The gap between available vessels and cargo demand widens fast. Rates have broken through previous highs, creating a profitable environment for owners of compliant ships. Some might view the move as a short-term spike, but a closer look reveals a global balance where limited ship supply keeps earnings high.

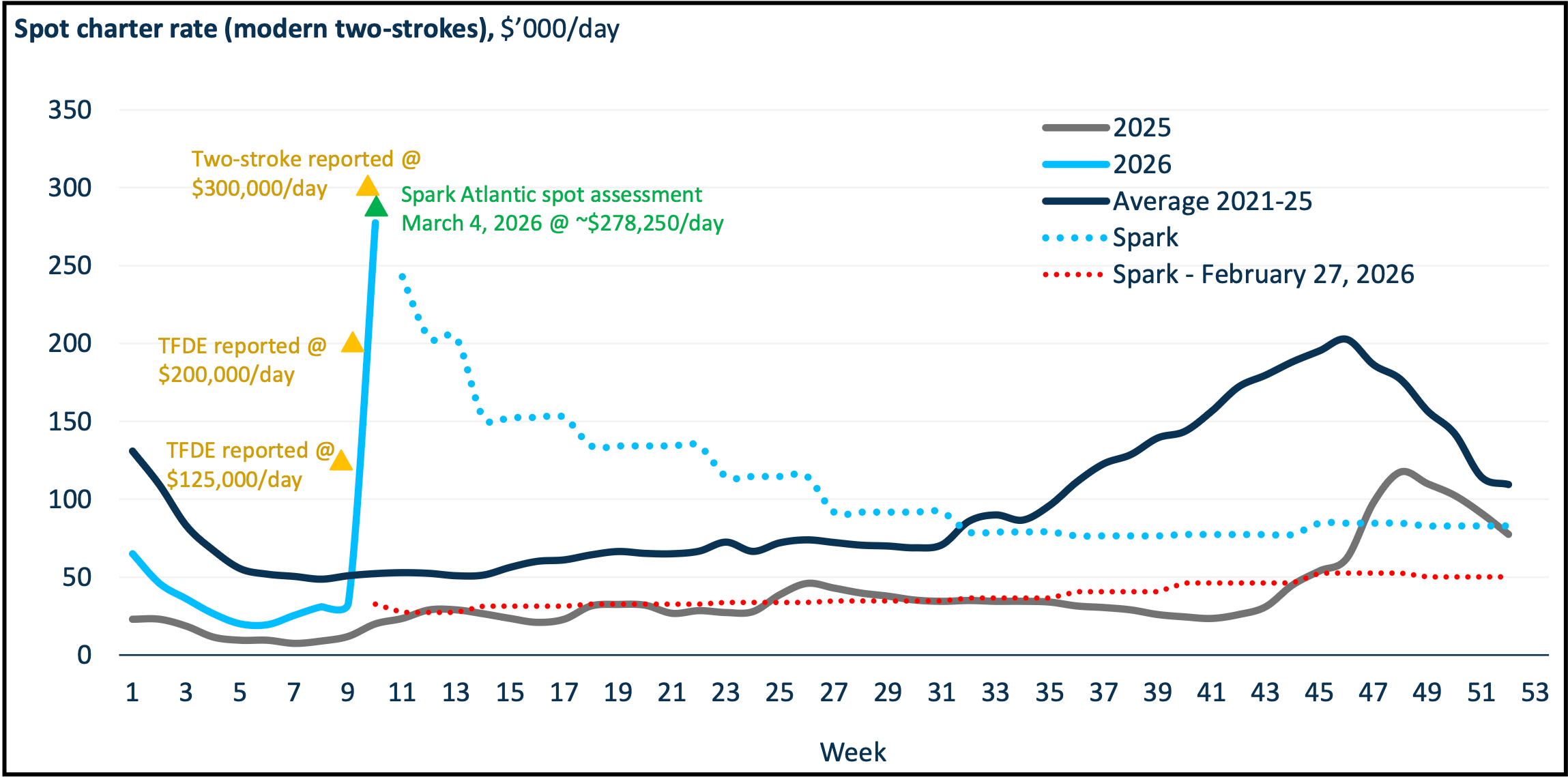

Red Hot Spot Market

The VLCC route from the Middle East to China recently topped $78,000 per day, marking a 12% increase in a single week. Suezmax rates from West Africa to Europe trade near $62 000, while Aframax rates in the North Sea hold at $55,000. Detours around risky or blocked routes are lengthening voyages, reducing available ship supply and driving tanker rates higher.

Because the demand to move oil over long distances grows faster than the fleet, the base for daily earnings has moved to a much higher level. This setup should allow top shipping companies to capture a larger share of a tight market, as the low supply of ships for immediate hire keeps rates elevated.

Now for the interesting part. Why are tanker equities down or flat while spot rates go up like crazy? We intend to go deep into this explanation in the following sections. Trust us, you do not want to miss this.

Why Tanker Stocks Are Ignoring the Rate Boom?

If tanker spot rates are skyrocketing, why are tanker equities not reacting in the same way? Most non-shipping experts would assume tanker stocks should be up like crazy right now. In reality, that is not happening at all.

Our take:

This is a hard question, but we believe it is purely a macro game, as is often the case in the shipping industry. You might think everything is perfect with geopolitical chaos, oil prices rising, less shadow fleet, and spot rates going crazy. Yet, stocks still do not react.

The situation is much more complicated than this. We do expect tanker stocks to get back to reality soon and go higher, but currently, people do not know how to react. A specific market dynamic exists, a market sentiment that only a handful of macro shipping guys could spot. We see that stock prices are not where they should be yet, but that the shift is coming soon.

Why Tanker Equities & Spot Rates Disconnect

Many people assume oil prices and tanker stocks move together. Actually, the link remains loose. When prices jump because of war risks and supply cuts while demand stays flat, the connection shifts. Stocks benefit from profitable voyages independent of the price of oil. When global tensions push prices up, investors ask if ships can travel safely, if owners can book new jobs, and if high rates will last long enough to show up in the earnings.

The situation in the Strait of Hormuz proves the point. While crude prices have jumped, these same events disrupt traffic, strand vessels, and lead insurers to pull war risk cover. This environment produces massive quoted spot rates while reducing the number of owners able to trade normally. Consequently, a geopolitical oil spike stays neutral or even negative for stocks.

A constrained Strait forces fewer normal fixtures plus more chaos. Reports from Bloomberg plus Reuters indicate that while traffic near Hormuz slows, broader equity markets sell off on inflation plus recession fears. In this setup, tanker names compete against a wide macro de-risking wave, preventing strong freight prints from driving share prices higher.

Equities also ignore a single extraordinary day-rate print. They price the earnings power investors believe stays sustainable over several quarters. Lloyd’s List plus analysts at DNB have noted that tanker equities often face pressure even during strong spot markets because investors focus on the eventual peak. Market belief in a quick unwind leads investors to ignore rates appearing extreme for only a few weeks.

Finally, a demand side problem emerges when oil prices get too high. When supply threats drive prices up, refiners plus importers face tighter margins plus may cut runs. Historically, as noted by Reuters, major importers like China pull back on purchases when oil rises too quickly. We believe this suggests a war driven spike can hurt the medium term cargo outlook even if it creates a short term freight squeeze.

External Insights We Found Valuable

Tanker demand functions through a specific calculation: tons multiplied by miles and average speed. While actual tons might decrease slightly, route inefficiencies now soar. Delays, congestion, and general confusion impact average speeds across the globe. J Mintzmyer, a prominent shipping analyst, reminds us that the freight increase was broad and began well before current events. Global tanker supply stays tight.

Rates reaching $300,000 to $500,000 per day would normally imply multi-bagger upside for stocks. No sane person expects those levels to last forever, but the current market misses the forest for the trees. Most investors focus on a few ships waiting in line while missing insanely strong markets and cascading inefficiency.

Our view aligns with this perspective. This narrow focus creates the valuation gap we see today. The broader market ignores the underlying strength while obsessing over minor details. As these inefficiencies continue to remove effective capacity from the water, the reality of these earnings will eventually become impossible to ignore.

Since April, when most shipping guys were saying that the bull cycle was ending, we entered a contrarian bullish trade by betting on crude oil tankers. In January, we doubled down by adding product tankers exposure. For 2026, we believe that having some exposure to dry bulk would be wise as well.

Our view so far has largely aligned with how the situation has developed, and we believe the same dynamics remain in place.

Global Oil Market Dynamics: Resilience Amid Volatility

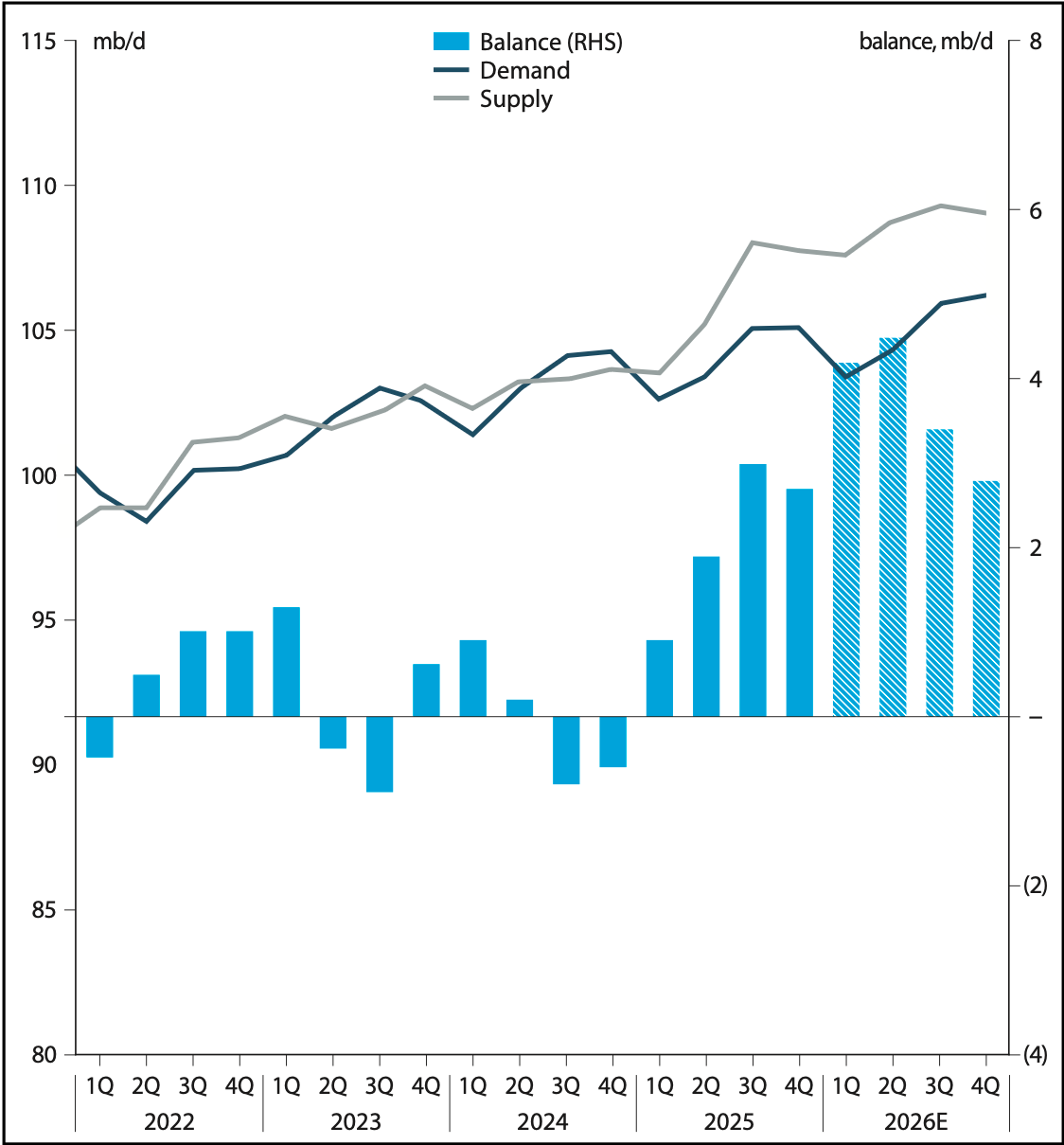

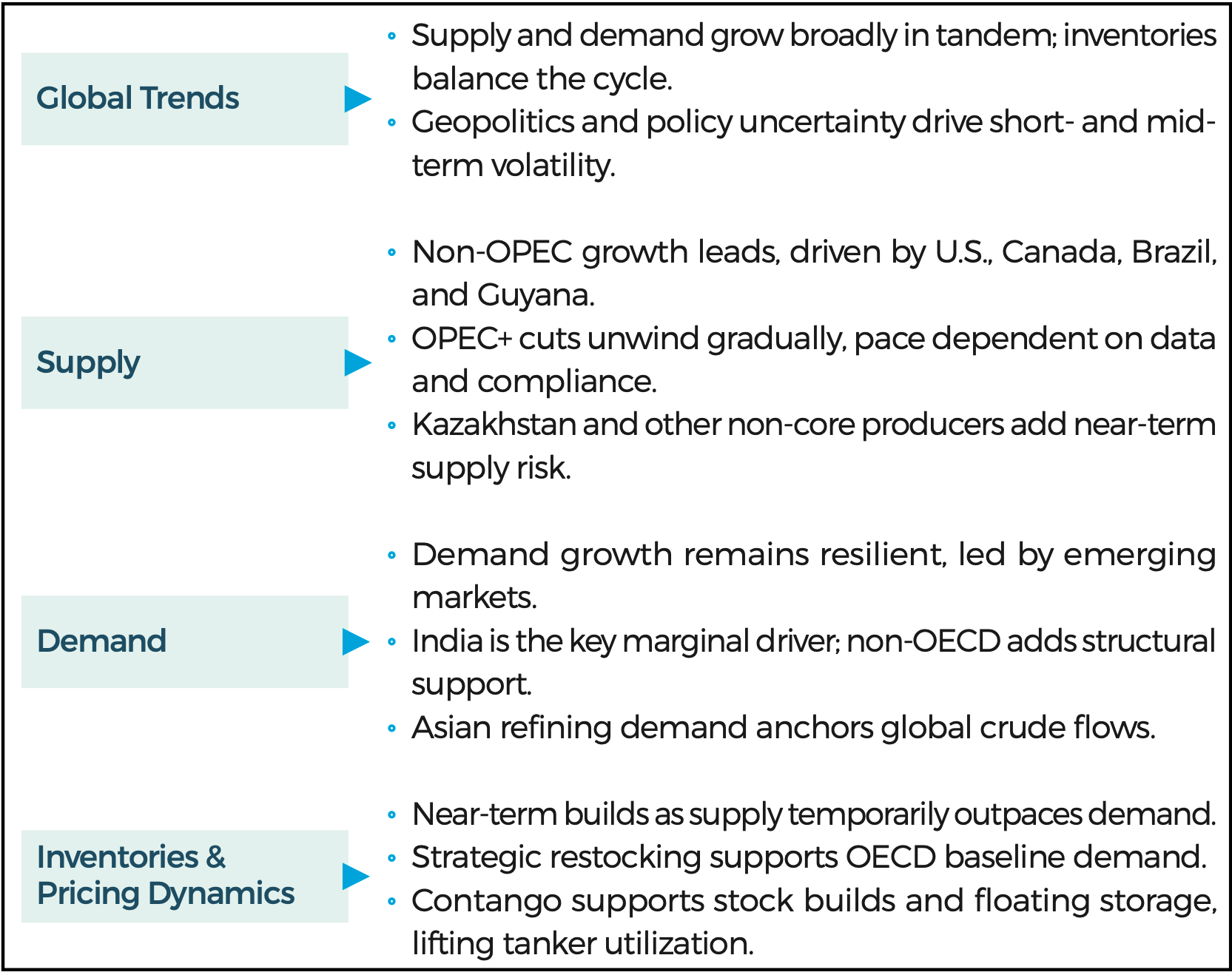

The IEA outlook points to an oil market that gradually becomes tighter through 2026. Demand is still moving higher, while supply growth looks less comfortable once you look past the headline numbers. The market may appear balanced for now, though that balance is becoming less forgiving.

IEA Oil Supply vs. Demand & Implied Balance

Inventories can still absorb part of the mismatch, but that buffer looks thinner as the year progresses. As that cushion fades, the market becomes more sensitive to even modest gaps between supply and demand, which raises the likelihood of firmer crude prices and a tighter physical backdrop.

What Is Driving Demand, Production, and Inventory Changes?

Part of the reason is that supply growth is not arriving with the same ease as the headline figures might suggest. Non-OPEC producers continue to add barrels, and OPEC+ is still in the process of returning supply, yet the path remains uneven. Timing, execution, and producer discipline all influence how much oil actually reaches the market. At the same time, demand continues to hold up well, with emerging markets still doing much of the heavy lifting. India remains an important source of incremental growth, and Asian refining demand continues to support global crude flows.

That leaves inventories in a more important role. They can still provide relief when supply briefly runs ahead of demand, though they are less able to absorb a prolonged tightening cycle. As balances tighten, inventory trends begin to matter more for price direction and for the broader tone of the market. Taken together, the picture is constructive. The market does not need a major disruption to move into a firmer setup. Continued demand growth, some friction on the supply side, and a smaller inventory cushion already point in that direction.

A Constructive Setup for Compliant Tonnage

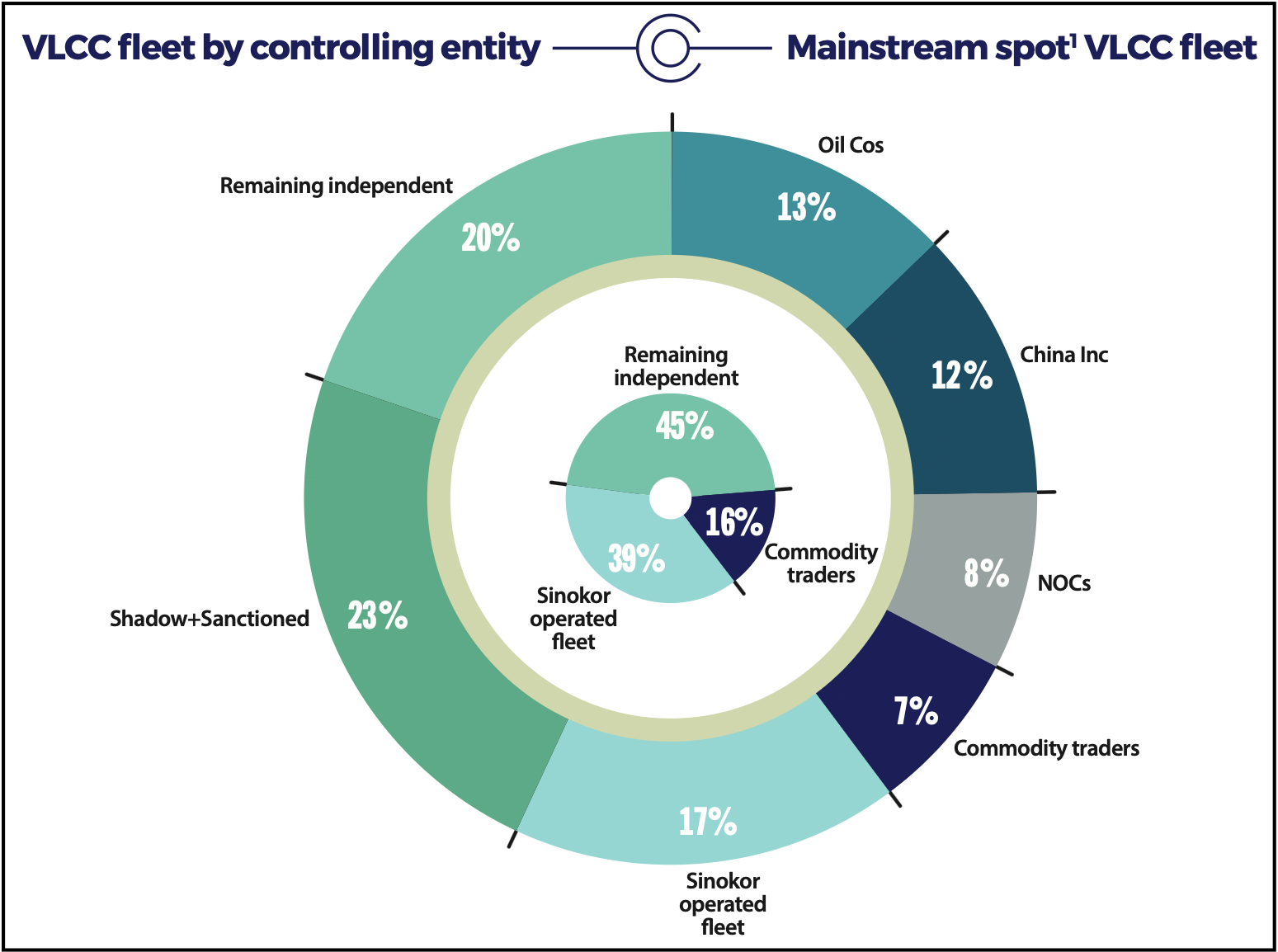

Export growth from sanctioned regions specifically Iran, Russia, and Venezuela has slowed significantly compared to overall global crude trade. This trend indicates a shrinking market share for sanctioned barrels, which reduces the industry’s reliance on the shadow fleet.

Non-Compliant Barrels Are Fading

We believe this shift represents excellent news for the compliant fleet as the market moves away from unregulated operators. As the volume of sanctioned oil declines, the demand for transparent and regulated shipping increases. Any sustained slowdown in these illicit trades directly benefits compliant vessels. This transition leads to higher utilization across the legitimate fleet and provides a strong foundation for firmer freight rates.

The reduction in shadow fleet activity removes a major source of inefficient competition from the global market. With fewer barrels moving through opaque channels, the “good guys” in the shipping industry are better positioned to capture a larger share of global trade. This setup creates a more stable and profitable environment for owners of compliant tonnage who operate within the established regulatory framework.

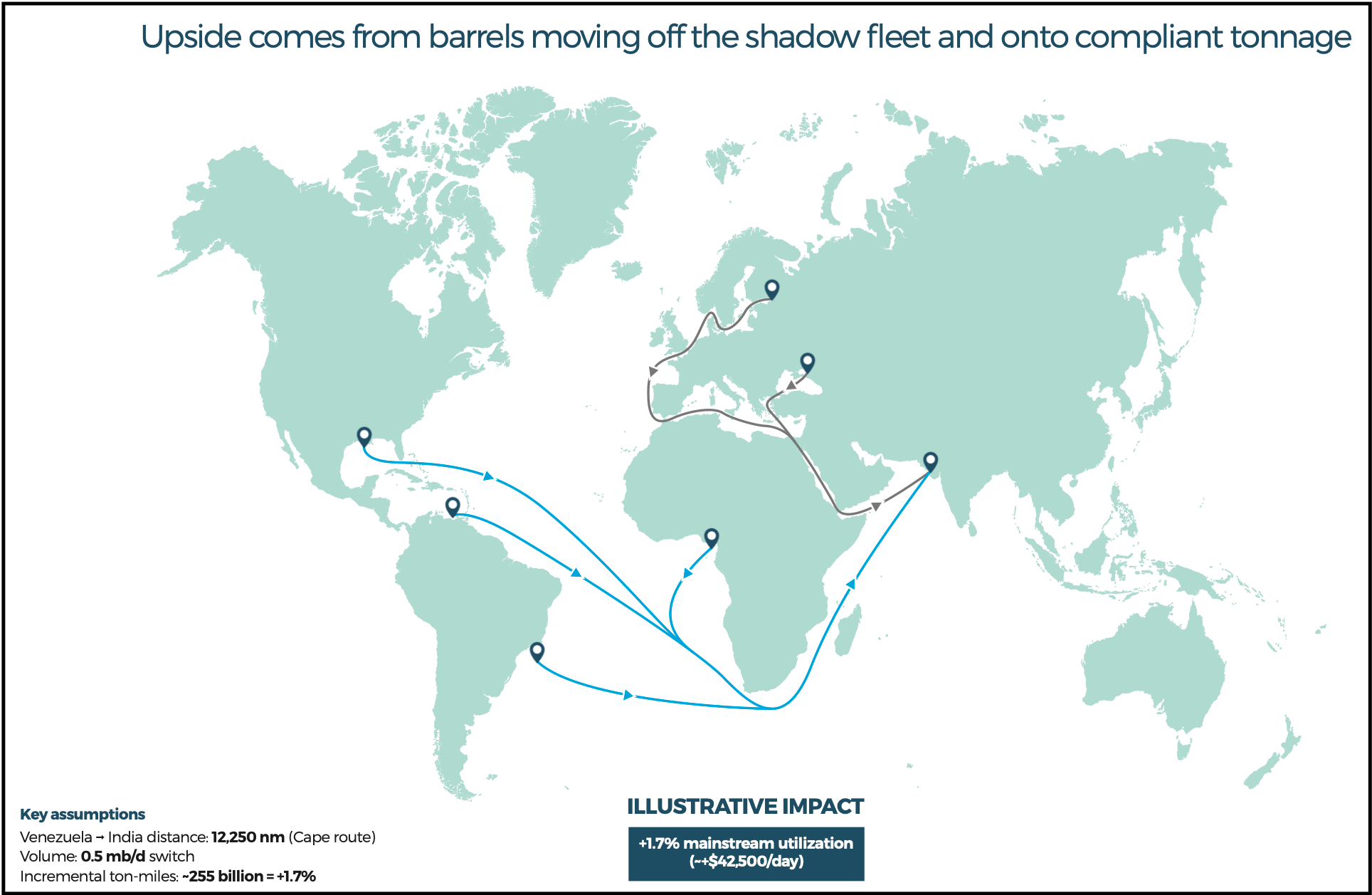

US–India Trade Deal: A Boost for Compliant Tankers

A potential trade deal between the US and India could create a significant tailwind for mainstream tankers. This upside stems from the shift of oil barrels moving away from the shadow fleet and onto compliant tonnage.

As sanctioned volumes decrease, the demand for transparent and regulated shipping increases. This transition directly benefits the “good guys” in the shipping industry by improving vessel utilization.

Upside as Barrels Move to Compliant Tonnage

The shift toward mainstream tankers creates a more stable environment for freight rates. Key assumptions for this transition include switching ~0.5M barrels per day from sanctioned sources to compliant routes.

For example, a switch on the Venezuela to India route, covering ~12,250 nautical miles via the Cape, would add 255B ton-miles. This represents a 1.7% increase in mainstream utilization, which could translate to an illustrative impact of over $42,500 per day in additional earnings. By reducing the reliance on unregulated operators, the market becomes more efficient for compliant owners. This setup positions legitimate shipping companies to capture a larger share of the growing trade between these two economies.

Export Rerouting Tightens Tanker Supply

Saudi Aramco recently loaded three Very Large Crude Carriers (VLCCs) simultaneously at its Yanbu and Al Muajjiz terminals on the Red Sea. This unprecedented scale of operation provides clear evidence that the producer is diverting as much oil as possible away from the Strait of Hormuz.

Similarly, Abu Dhabi’s state producer, Adnoc, loaded another VLCC at Fujairah, positioned outside the strait. As Bloomberg columnist Javier Blas notes, the sheer volume of these simultaneous loadings marks a significant shift in regional logistics. This strategic pivot forces longer voyages as barrels bypass the Persian Gulf, effectively soaking up more tanker capacity.

By using Red Sea and Gulf of Oman terminals, these producers are re-routing global energy flow, which further tightens the available supply of vessels. The move reinforces the current high-conviction environment, where every extra mile traveled helps maintain the elevated floor for spot rates.

Market Control Shifts in VLCC Supply

A privately coordinated platform is rapidly aggregating compliant VLCC spot tonnage at a scale large enough to change how the market functions. This coordination materially restricts the availability of ships for immediate hire. As this fleet grows, the effective supply of vessels tightens, which increases competition for the remaining ships and causes rates to settle at higher levels.

How Mainstream Fleet Supply Is Evolving

This change represents a fundamental shift in the market instead of a typical cycle. It reinforces the broader squeeze on compliant vessels caused by sanctions. Unlike the older fleets of many competitors, OET is best positioned to benefit from this environment. It owns the youngest fleet among its peers and maintains near-full spot exposure, allowing it to capture the upside from tighter availability and higher charter rates.

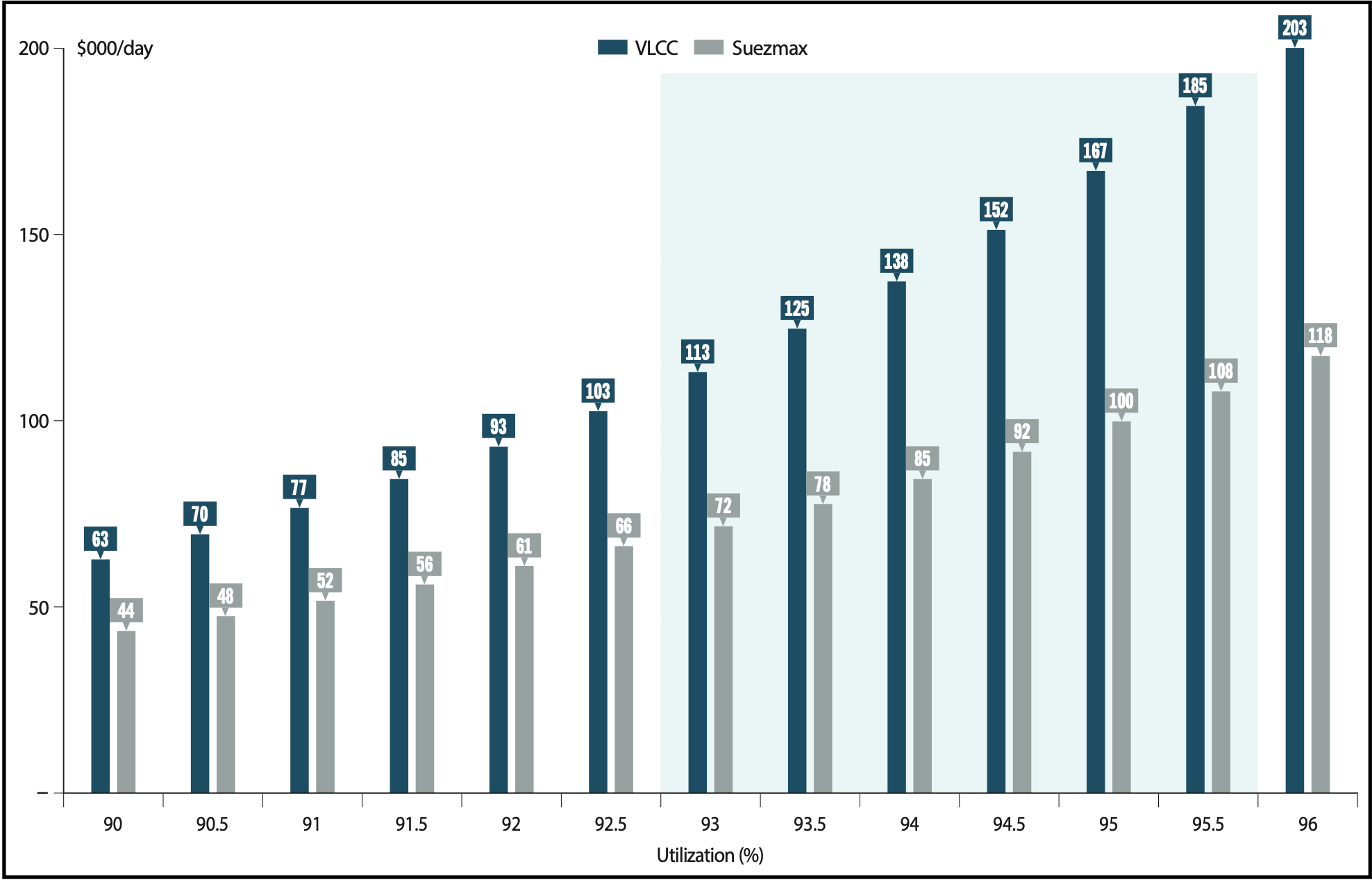

High Utilization Amplifies Freight Rate Volatility

The tanker market is entering a phase where small changes in supply and demand lead to massive swings in earnings. As the fleet reaches high utilization levels, every 1% increase in utilization could add nearly $25,000 per day for each VLCC and around $15,000 per day for each Suezmax vessel.

Rates vs. Utilization

We believe this extreme sensitivity highlights why the current market environment is so favorable for owners of compliant tonnage. This non-linear relationship between utilization and rates means that once the market passes the 93% threshold, daily earnings for VLCCs can quickly jump from $113,000 to over $200,000 as utilization nears 96%.

For Suezmax vessels, the impact is similarly dramatic, with rates potentially climbing from $72,000 to $118,000 per day in the same scenario. This dynamic creates a powerful setup for companies like OET, whose spot market exposure allows them to capture these rapid price increases directly.

Update on TRMD and ECO: Our Top Tanker Holdings

The tanker market remains red hot. Tight fundamentals plus the U.S. and Iran conflict make owning the sector more valuable than ever. With the Strait of Hormuz effectively paralyzed and rates skyrocketing, geopolitical tension drives market value.

To capture the environment, we stay long Torm (TRMD) for product tanker strength plus Okeanis Eco Tankers (ECO) for high conviction crude exposure.

Okeanis Tankers (ECO): Research Report

Torm (TRMD): Research Report

As noted before, specialists regard Okeanis as having the best management team in shipping. Their modern, eco-optimized fleet commands a premium. In a market where efficiency plus environmental compliance stay mandatory, their positioning stands out.

The pairing offers the optimal balance between refined product upside plus elite crude execution. We remain well positioned in the long trades with no plans to sell. We will provide updates if our outlook changes.

The Aurelion Team

Disclosures & Methodology