SaaS Primer: The New Industrial Order

Under AI disruption, we believe SaaS is shifting from capital-light compounding to capital-intensive maintenance. Here is our playbook for the fallout and the specific stocks we are positioning in.

The age of “Software Eating the World” is over. Today, AI is eating Software.

For twenty years, software was a capital-light dream: build once, sell forever, and enjoy 80% margins. Today, AI has driven the cost of writing code to zero, evaporating that traditional moat. As this violent transformation accelerates, we believe most of SaaS will behave like a heavy industrial business.

Many companies are entering a Red Queen’s Race, forced to spend aggressively on AI just to defend their existing positions. For these businesses, margins, cash flow, and valuation multiples are likely headed lower.

Yet not all software is doomed. A small group of companies, those with proprietary data, mission-critical workflows, and zero-fault execution, should emerge stronger. Recent indiscriminate selling has created significant opportunities among these future winners. We present 3 stocks, 2 US and 1 in Japan.

Most research on SaaS offer scenarios. We prefer to state our view clearly and put our money on the line through high-conviction stocks. Built on 7 logical premises, this report expands on our widely cited flash note (CNN), which only captured our view of a specific stock.

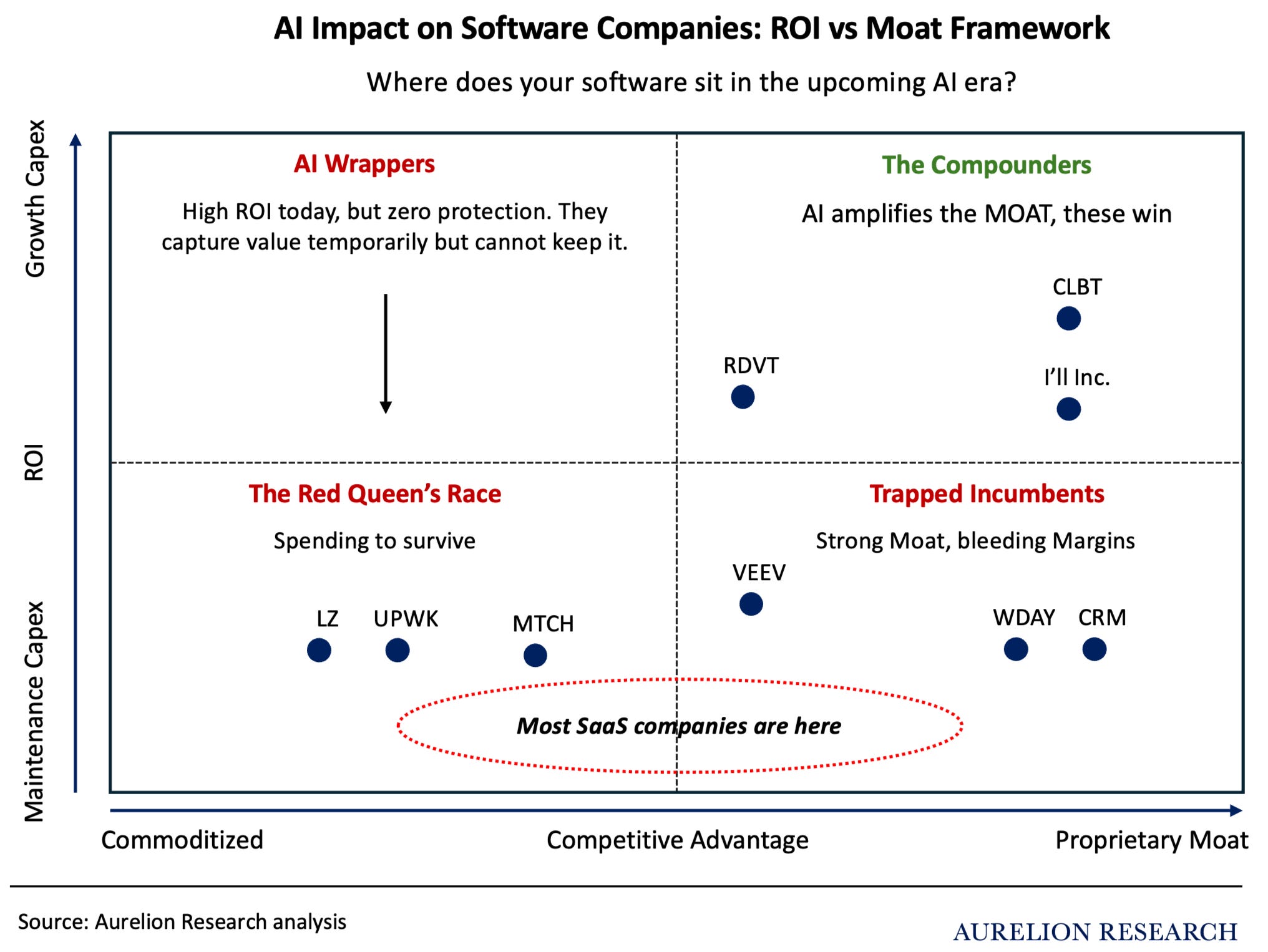

We start with our AI Risk and Opportunity Matrix.

This framework identifies which companies AI will crush and which will thrive.

The Vertical Axis (The Nature of the Spend): When a company invests in AI, does that money generate new, profitable growth (Growth Capex)? Or is it purely defensive spending required just to keep current customers from leaving (Maintenance Capex)?

The Horizontal Axis (The Defensibility of the Moat): Is the company selling generic code and basic dashboards that AI can now write for free? Or does it own assets like proprietary data, strict regulatory compliance, and integrated physical workflows?

Crossing these dimensions reveals 4 distinct destinies for software equities:

1. AI Wrappers (Top Left). Slick interfaces built on borrowed AI models. Lacking proprietary data, their initial success is a temporary illusion before competition drags them downward.

2. The Red Queen’s Race (Bottom Left). The brutal reality for most of SaaS. Forced to spend heavily just to survive against AI-enabled competitors, their margins are crushed by zero pricing power. (e.g., LegalZoom, Upwork)

3. Trapped Incumbents (Bottom Right). Entrenched systems of record. They won’t die tomorrow, but they will bleed profit margins paying an “AI Token Tax” just to defend their existing turf. (e.g., Salesforce, Workday)

4. The Compounders (Top Right). Only a few possess proprietary data or mission-critical workflows where failure is unacceptable. For these companies, AI is a force multiplier.

Table of Contents

AI vs SaaS: The Market Sentiment Shift

Software Was Eating the World

The Red Queen’s Race

SaaS Is The New Industrial

The Three-Tiered Price Action

Where the Value Shifts in the AI Era

Is Vertical SaaS More Resilient?

Why Incumbents Are Struggling

The Playbook: Where We Are Allocating Today

Software Pick #1: I’ll Inc. (3854.T)

Reiterating Our Cellebrite (CLBT) Thesis

Software Idea #2: Red Violet (RDVT)

Our Final Take on SaaS

1. AI vs SaaS: The Market Sentiment Shift

First, let’s frame the current AI versus SaaS debate and the sentiment driving the market. The application software selloff, often described as a SaaS apocalypse, stems from growing uncertainty around the ultimate future of the sector in the face of AI disruption. We saw the impact directly in share prices.

This ambiguity materially weakened confidence in long term assumptions, pushed discount rates higher, and left many investors on the sidelines. They increasingly view the space as difficult to underwrite and structurally challenged.

The debate goes far beyond a single dimension. Beyond whether generative AI and AI agents reduce demand for traditional software or simply reshape spending patterns, even investors who remain constructive on incumbent durability need to account for a second layer of risk. That risk remains completely real and unlikely to fade in the near term.

At the same time, certain software companies will undoubtedly benefit from AI, but we believe their number will fall far short of what many bullish narratives suggest. This includes the impact of AI driven transformation on existing software models, bringing potential acceleration in product redevelopment, margin pressure, and changes in pricing structures alongside workforce efficiencies. We saw these concerns becoming much more pronounced earlier this year as the market realized AI driven change is arriving much faster than initially expected across the software space.

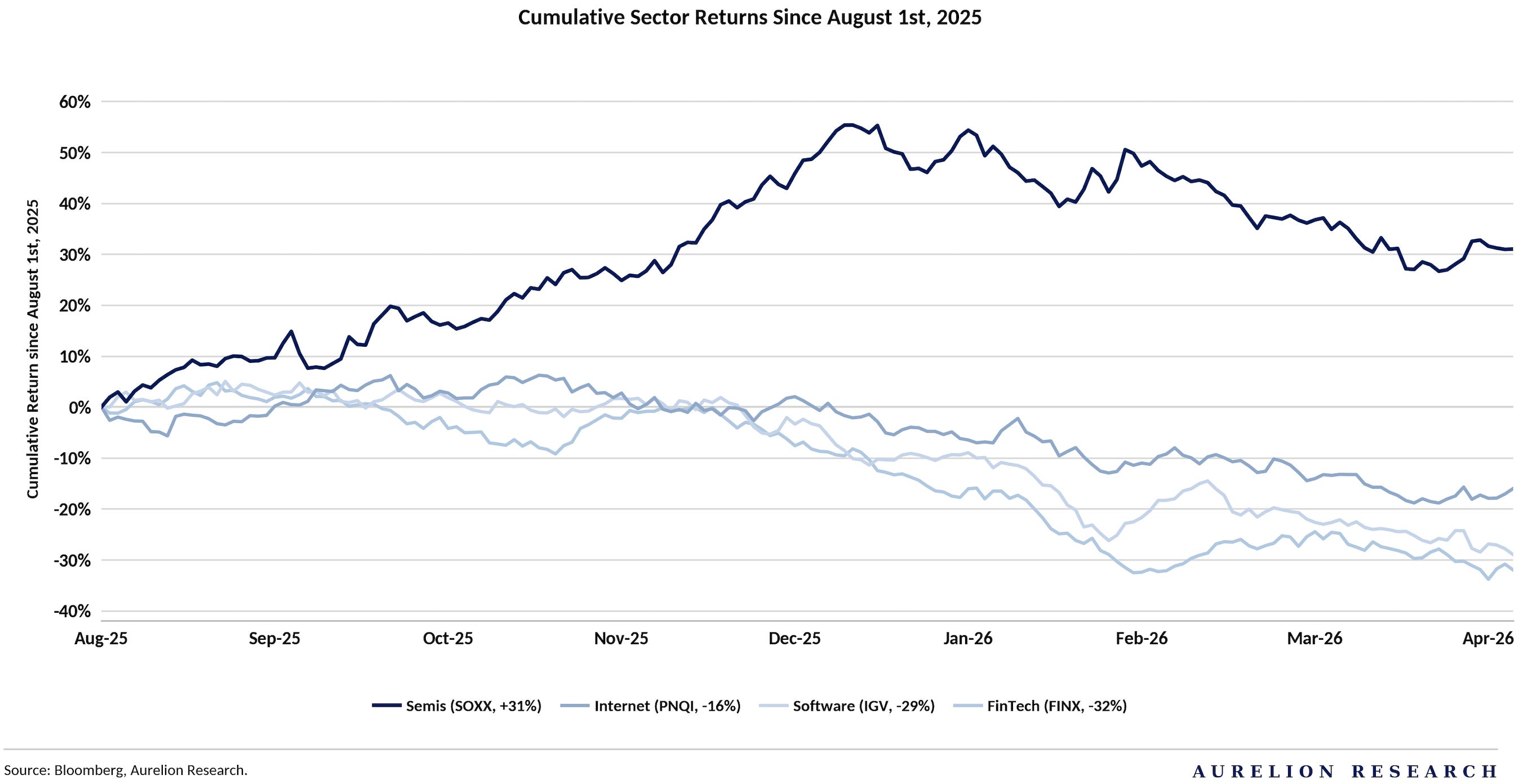

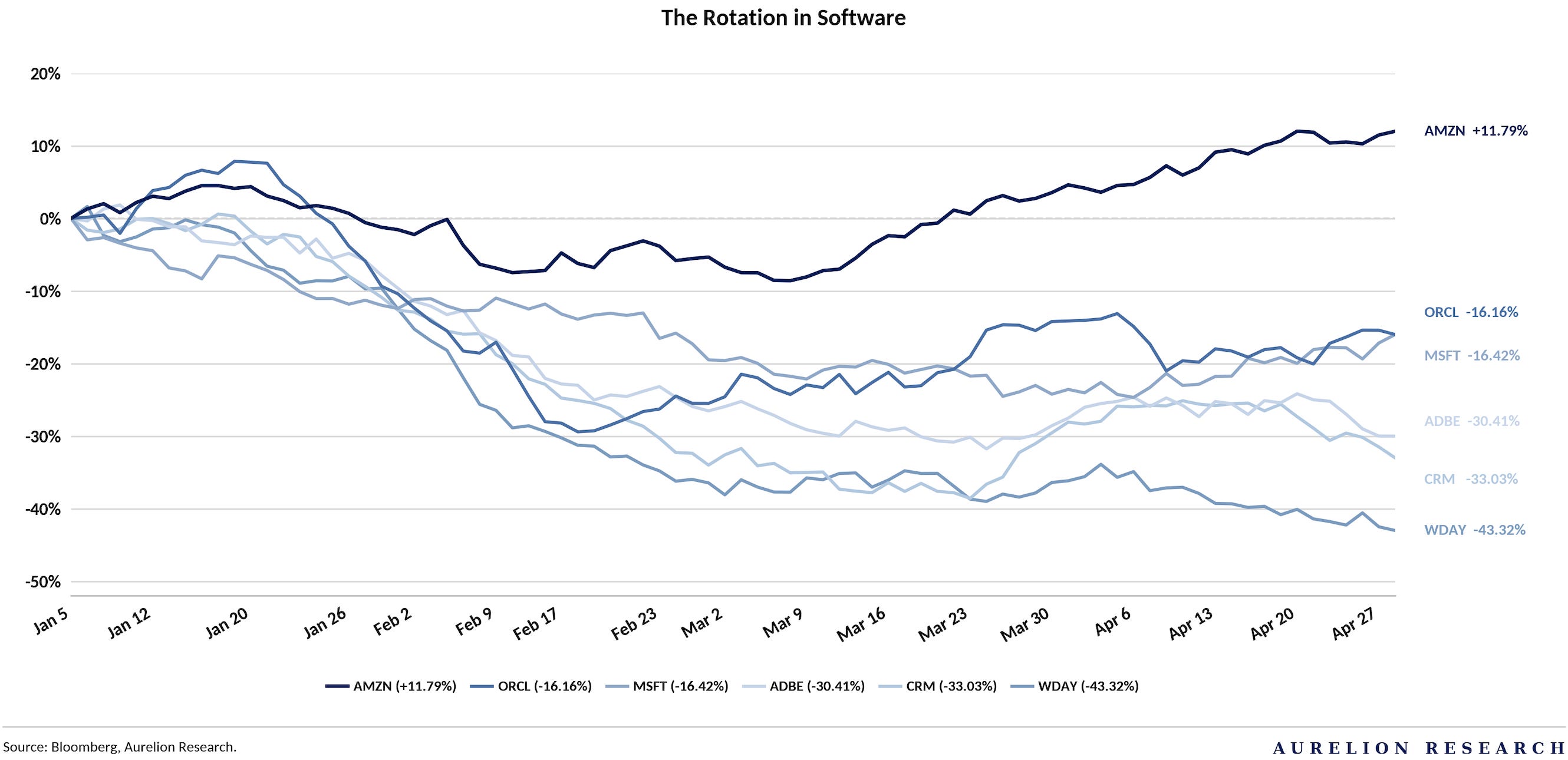

As you can see below, we are seeing a clear rotation within the sector.

Application software names like Adobe, Salesforce, and Workday are moving lower, while infrastructure, data, and security leaders like Amazon, Oracle, and Microsoft are moving higher since March.

Rapid advances in foundation models, rising competitive intensity across the ecosystem, and a steady stream of developments highlighting the overlap between AI platforms and traditional software offerings are reinforcing this shift. Accelerating enterprise adoption of AI tools only adds fuel to the fire.

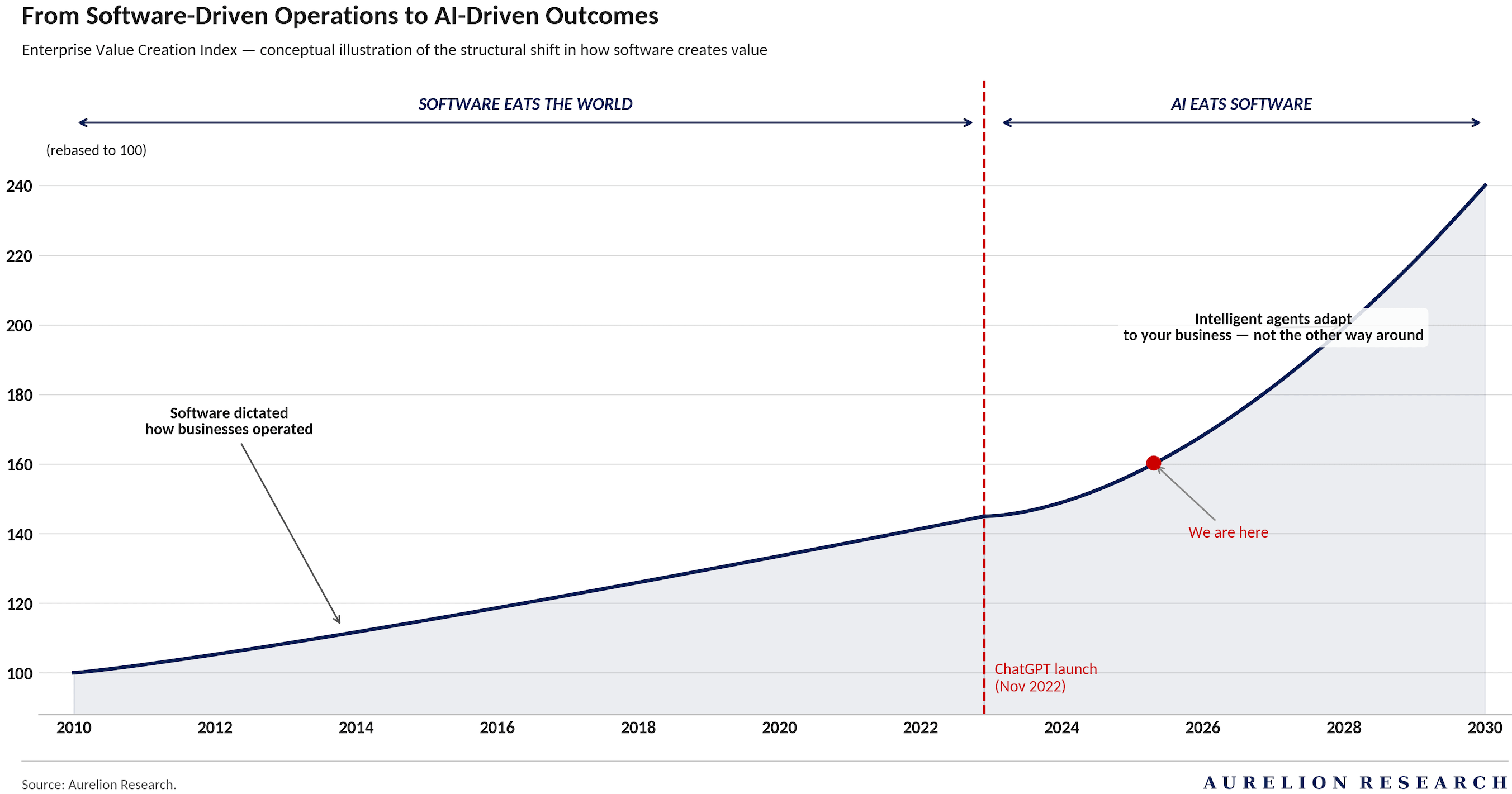

2. Software Was Eating the World

About three years ago, Artificial Intelligence (AI) emerged. It quickly became the most disruptive force in enterprise software since the rise of SaaS, so much so that companies around the world, including many of the largest across industries, are now racing to launch agent-based use cases and integrate AI into every workflow. Which leads us to this section theme: Software was eating the world.

When we say software was eating the world, we mean that digital applications swallowed up physical processes across every single industry over the last fifteen years. Companies bought specialized platforms for accounting, supply chains, and customer management. Human employees then had to learn those specific workflows. The software completely dictated how your business operated.

Generative AI flips that old model upside down. We are moving away from buying tools that help people work, toward deploying systems that actually do the work directly. AI consumes the very software we spent years building. You stop having to adapt your operations to fit a rigid platform. You deploy intelligent agents that adapt to your specific needs instead.

The whole economic foundation of enterprise technology changes here. Instead of licensing empty interfaces for humans to click through, companies will pay for executed tasks and actual business outcomes.

For years, the core investment thesis for enterprise software rested on its absolute indispensability. Robert Smith, Founder and CEO of Vista Equity Partners, famously captured this dynamic:

“Software contracts are better than first lien debt. You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.”

The software business model was, in theory, almost perfect. Under ideal conditions it represents an investor’s dream: highly scalable capital-light businesses with limited reinvestment requirements earning recurring revenue at 80% gross margins. If the market would place a premium multiple on anything, of course it would be software.

The software business can be categorized into two general phases:

Startup & initial scaling. This phase is categorized by high revenue growth and generally negative earnings as the business invests in sales and engineering talent to acquire as many customers as possible.

Out-year scaling. Once the base of high-margin recurring revenue has grown enough, margins normalize to positive and can scale to be very significant — highly desirable EBIT margins of 25-30% and beyond are common in mature software businesses. Given the buildup of recurring revenue eventually the law of large numbers kicks in and revenue growth normalizes as the business enters more of a “cash cow” phase.

Such a perfect business model always attracts competition, and software is no different. Eventually these capital-light businesses began competing to win client deals, to retain top engineering and sales talent. Much of the cost of the latter section of competition is visible in Stock-Based Compensation, common in software companies to incentivize employee retention. Some software companies particularly in small and mid-cap use so much stock-based compensation that the actual cash generated to shareholders of the business is slim to none.

Thus, this capital-light ideal business model was pressured through competition into many businesses that actually produce very little net cash flow at thin margins. Importantly, this competition is not new, it existed before the age of AI.

In 2022, everything changed with the launch of OpenAI’s ChatGPT.

Since then the entire software sector has been hit with two simultaneous crises:

The rapid advancement of AI technologies and their ability to automate many human tasks, particularly coding, lowering the barriers to new software creation, increasing competition, and reducing the TAM of seat-based software as AI increases productivity per employee at customer firms.

The market realization that many top software stocks had been trading at highly elevated multiples relative to the amount of Free Cash Flow to Shareholders produced, that is, FCF adjusted for Stock Based Compensation.

These two factors have led to crippling multiple compression across the vast majority of public software. Once a cohort of infinitely scalable capital-light darlings, software stocks are now heavily scrutinized.

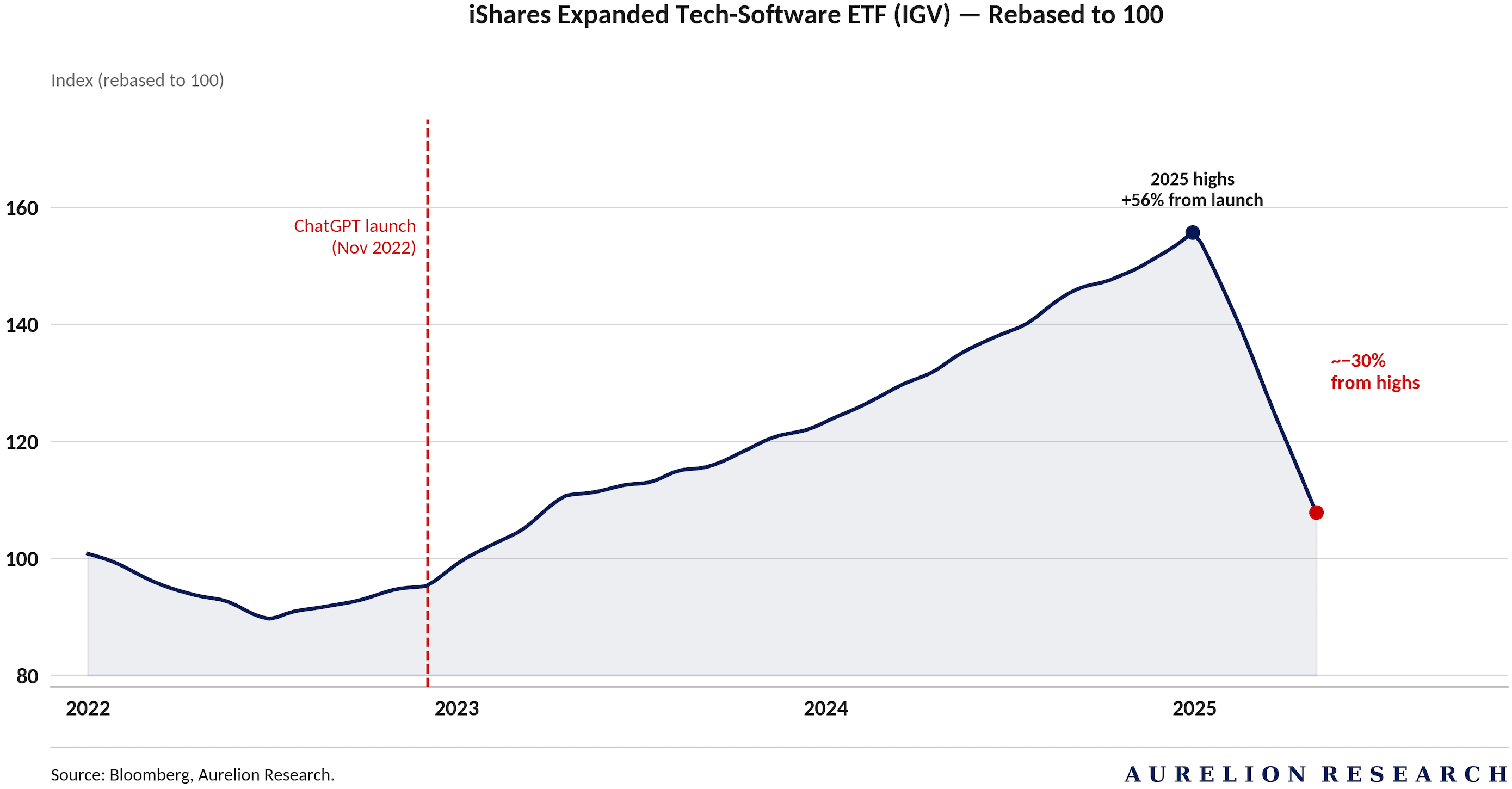

Private credit funds with software lending exposure are reclassifying healthcare software loans to just ‘healthcare’ to hide their true software exposure. Software ETF IGV is down almost 30% from 2025’s highs, though many individual names have performed significantly worse.

3. The Red Queen’s Race: Running Just to Stand Still

In evolutionary biology, the “Red Queen Hypothesis” describes a brutal reality: a species must relentlessly mutate and adapt, not to conquer its ecosystem, but simply to avoid being hunted to extinction by competitors who are evolving at the exact same time. As the Red Queen tells Alice in Through the Looking-Glass: “It takes all the running you can do, to keep in the same place.”

Today, we believe the legacy SaaS sector has entered a financial Red Queen’s Race.

The Logical View: Why Software Becomes a Heavy Industry

The re-rating of the SaaS sector comes down to a chain of financial logic:

Premise 1: The Historical Moat.

For the last two decades, writing complex software was expensive and required specialized talent. The code itself was the barrier to entry. Investors gladly awarded 25x earnings multiples because competitors could not easily replicate the product.

Premise 2: AI Commoditizes the Baseline.

Foundation models have driven the marginal cost of writing software to near zero. A leaner, AI-enhanced startup can now replicate a legacy UI or workflow dashboard in a matter of weeks.

Premise 3: The Existential Threat.

Because code is no longer a bottleneck, legacy SaaS companies relying on generic dashboards or seat-based pricing have lost their defensibility. They face immediate replacement not just from leaner startups, but from internal enterprise IT teams empowered by AI, and mega-cap tech giants bundling these commoditized features at no cost.

Premise 4: The Red Queen’s Capex.

To survive this threat, incumbents are forced into a two-front war on their cash flow. First, they must pay the “AI Token Tax” to hyperscalers just to integrate baseline AI functionality. Second, because every competitor has access to the same underlying AI models, the incumbent must constantly spend heavy R&D to build “something on top” to differentiate their interface.

However, because foundation models are constantly improving, yesterday’s unique feature becomes tomorrow’s baseline. If the incumbent stops spending this maintenance capex, a competitor will immediately match their offering. This creates an endless cycle of spending just to retain customers.

Premise 5: Low Pricing Power.

While some incumbents are currently enjoying a short-term “sugar high” by charging premium tiers for AI add-ons, this pricing power is transitory. As open-source models rapidly close the capability gap, the cost of intelligence trends toward zero. Because AI functionality and constant user interface updates are rapidly becoming basic “table stakes” across the industry, legacy vendors cannot charge a premium for them long-term. Customers will expect these continuous improvements by default.

Premise 6: The Maintenance Capex Trap.

Because they cannot raise prices, this surge in capital spending generates little to no incremental revenue. The return is largely defensive. When a company must invest heavily simply to protect its existing position, the economics deteriorate sharply. Value accrues upstream to AI infrastructure providers, while the software layer faces margin compression, weaker cash flow, and ultimately a lower valuation multiple.

4. SaaS is the New Industrial

For the last decade, the market gladly awarded legacy SaaS businesses a baseline multiple of 25x earnings (and frequently 25x sales at the peak), assuming infinite pricing power and sticky retention. We are arguing for a continued re-rating.

As AI drives the barriers to software creation to zero, SaaS companies lacking proprietary data or mission-critical integration will face severe commoditization. If you do nothing, you lose. We expect these displaced incumbents to see their multiples aggressively compress to ~10x earnings, effectively pricing them as declining assets rather than forever cash flows.

Before many of these companies even reach a 10x public market multiple, they will likely be taken private by buyout firms. Private Equity will treat them exactly like mature industrial assets; slashing SG&A, halting R&D, and aggressively harvesting whatever cash flows remain from trapped customers.

A 10x multiple aligns these software vendors with heavy industrial companies that must constantly invest in capital expenditures just to keep their factories running. The age of building software with a team of smart coders over five years, then milking that same product for a decade with near-zero improvements, is permanently over. If you do not continuously iterate, a smaller competitor will replicate your frontend in a few months and steal market share within a year.

Consequently, we expect cash flow conversion and operating margins to decline across the sector. Companies will be forced into a perpetual cycle of “maintenance capex”: spending heavily on compute, AI tokens, and constant R&D simply to maintain parity and prevent churn.

The sticky incumbents: bleeding, but not dying. To be clear, not all of the SaaS will compress to a 10x multiple. Some larger incumbents operating in zero-fault environments, managing complex government contracts, or sitting inside highly regulated systems will retain a higher multiple simply because a startup cannot legally or operationally replace them in a single year.

However, even these entrenched players will face margin compression. Their competitors will be able to close the feature gap much faster, and the constant investment required to make their software valuable enough to justify annual price hikes will be significantly higher. They warrant an impacted multiple, but they avoid terminal value collapse.

Where AI Amplifies the Moat

However, there is a distinct group of companies that will see earnings accelerate and their dominance expand. These are the companies where AI does not replace their value proposition, but amplifies it. Even with AI lowering the barrier to writing code, these businesses cannot be easily replicated due to a few critical advantages:

Proprietary Data Monopolies & The Flywheel: When code itself is commoditized, data becomes the ultimate moat. However, it is not just about hoarding historical data, the key is the feedback loop. Every time a customer uses the platform, the system captures new proprietary data exhaust. This continuously trains bespoke models, widening the moat every day in a way an out-of-the-box LLM cannot replicate. Companies that own these dynamic proprietary data lakes will thrive because an AI agent cannot “vibe-code” a decade of licensed, aggregated intelligence.

The Zero-Fault Tolerance Barrier: AI is notoriously prone to hallucinations. While a 95% accuracy rate is sufficient for drafting marketing emails or summarizing meeting notes, it is catastrophic for FDA compliance, criminal forensics, or real-time infrastructure management. Companies deeply involved in mission-critical workflows where the cost of failure is a lawsuit, regulatory action, or physical harm will thrive because enterprise buyers will not risk replacing a trusted system of record with a cheaper AI-generated alternative.

Action Over Observation: Most legacy SaaS is simply a database with a dashboard to observe information. The winners in the AI era will be software that actually executes complex physical or financial actions like moving money, routing physical supply chains, or altering physical operations. AI makes the decision-making faster, but the proprietary execution layer is more difficult to replace.

5. The Three-Tiered Price Action

Because the recent sell-off was largely indiscriminate, we expect a divergence into three distinct tiers of price action over the next 12 to 24 months:

1. The Basic Apps (More Falling to Come) While these generic apps that charge you “per person” have already seen their stock prices drop, they are still not a bargain. The market is currently making a mistake by valuing them based on how much they sell, rather than how much profit they actually keep.

As these companies enter the “Red Queen’s Race”, where they must constantly spend just to keep their current customers, their ability to set high prices will disappear.

The AI Token Tax: To stay relevant, these companies have to add AI features. Every time a customer uses those features, the company pays a fee (a “token tax”) to large AI providers like Microsoft or OpenAI, which directly eats into earnings.

A Never-Ending Arms Race: Because AI makes it easy for anyone to copy a basic app, these companies have to spend massive amounts on constant updates just to avoid being replaced by a cheaper competitor.

Because profits are being pressured by these rising costs, we expect these stocks to face continued multiple compression and eventually trade closer to 10x earnings, based on true earnings after stock-based compensation.

2. The Sticky Incumbents (Dead Money): For mega-cap incumbents tied to complex workflows, such as Salesforce and Workday, the recent 20 to 30% correction was likely justified. The market has begun pricing in a new reality: slower growth, lower margins, and rising reinvestment needs. These companies are unlikely to collapse, but they may struggle to generate meaningful returns as an increasing share of cash flow is reinvested to maintain their position.

3. The Compounders: This is where indiscriminate selling created a clear opportunity. The market punished these companies assuming all software faces the same AI commoditization risk.

Because these companies hold proprietary data monopolies and zero-fault execution moats, their AI spending is purely accretive growth capex. As they prove their ability to expand margins, we expect them to aggressively re-rate higher, decoupling from broader software indices.

What About AI Wrappers?

Premise 7: Companies that enjoy high early returns by simply “wrapping” external AI models face a unique risk. Since they do not own the underlying engine or data, their high ROI is temporary. As soon as the baseline technology improves, their “feature” is absorbed, and they are pushed into a defensive maintenance cycle.

6. Where the Value Shifts in the AI Era

The pattern repeats across industries: early success concentrated in a handful of leading firms attracts competition, which compresses margins and slows growth at the individual company level. With the rise of AI, we expect software will be no different. From here, most of the value is likely to accrue to AI-native companies.

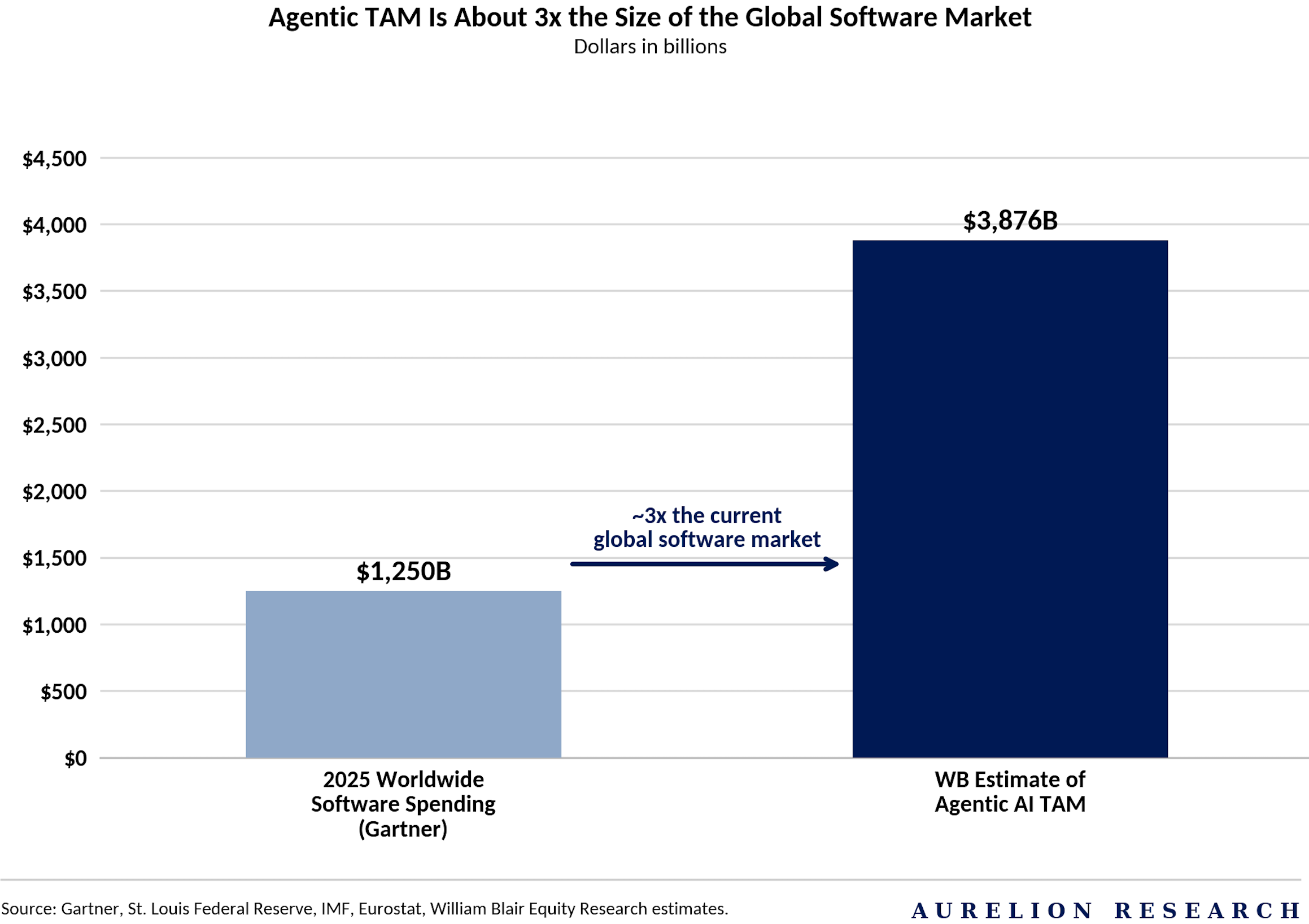

The TAM for AI-enabled Agentic Solutions Could be Huge

As you can see above, the market for AI agents represents a massive ~$4 trillion opportunity, roughly three times the size of the global software market.

While Gartner estimates total software spending at about $1.25 trillion by 2025, the rise of agentic AI expands this horizon. We see this shift as AI becoming a new layer of software, moving beyond simple tool replacement toward a broader expansion of the industry’s scope.

The real driver behind this transition is a fundamental change in enterprise budget allocation. Software is shifting from a tool employees use to a system that performs tasks directly. This allows AI and software vendors to capture a larger share of corporate spend by displacing traditional labor costs, effectively redirecting payroll dollars into software expenditure.

In this context, we expect most of the value creation to accrue toward AI-native players, including frontier model developers, as well as a smaller group of software companies that are early and effective adopters of AI.

In contrast, firms that simply layer outsourced AI onto existing products risk margin pressure over time, particularly as providers such as OpenAI and Anthropic normalize pricing and compute economics mature. If the majority of value creation in the space ultimately concentrates in AI, incumbent SaaS players will need to adapt quickly and decisively, or face increasing commoditization risk.

We see the main risk for software firms in those that manage generic workflows without proprietary data. These functions are more easily replicated by AI. While highly specific or regulated processes remain harder to automate today, that gap is narrowing quickly. These companies still have time to adapt, but they need to move fast as AI capabilities continue to expand.

Conversely, the most durable companies are those that control underlying data.

AI agents and models rely on context to function, and that context sits within established systems of record. Rather than replacing these databases, AI is being layered on top of them. This puts companies that own the data layer in a stronger position than those that only provide interfaces or basic workflow tools.

Thus, the focus on this report will be on software and software-adjacent companies that are not under threat from AI: they control proprietary data and hold clear advantages over newcomers, and they actually produce meaningful Cash Flow to Shareholders today, not in 5 or 10 years.

7. Is Vertical SaaS More Resilient?

Our research and the field checks we recently came across while looking into this space suggest that application software with governance, regulatory complexity, and high levels of customization is generally more resilient to AI disruption.

These systems sit within mission critical workflows that require trust, auditability, and compliance, which in turn creates high switching costs due to deep technical integration and significant operational change management.

Vertical SaaS typically sits at the center of these dynamics.

Its functionality is highly industry specific, and its customers operate in regulated environments such as healthcare, government, financial services, and construction. In these markets, software is not generic tooling but part of the operational backbone, which makes replacement considerably more complex.

A recurring theme from prior work is that domain expertise is becoming a key input in building effective AI systems. Translating general model capability into reliable, context aware decision making requires deep understanding of industry specific workflows and constraints.

It is therefore not surprising to us that many of the most prominent AI native startups are vertically focused, such as Harvey in legal and Abridge in clinical documentation, a point highlighted by several sell side analysts. We believe this trend is highly relevant for incumbents as well, particularly those able to translate proprietary industry knowledge into their AI offerings.

That said, it would be incorrect to assume vertical SaaS is insulated from disruption. These companies still need to adapt as AI capabilities evolve. For example, recent UBS research highlighted that pharmaceutical companies have already begun developing internal AI applications for workflows they previously relied on vendors such as Veeva Systems to provide. In some cases, enterprise customers are moving earlier than expected to internalize functionality.

Even so, vertical SaaS incumbents appear better positioned than most due to their deep industry entrenchment and accumulated domain expertise. These advantages provide a foundation for integrating AI in ways that enhance rather than displace their platforms, provided execution remains disciplined.

We believe vertically focused companies benefit from years of accumulated product depth, often built through highly specialized workflow components that are difficult to replicate. This allows them to add AI features more quickly and with greater relevance to end users compared to horizontal platforms.

However, investors must not mistake this entrenchment for absolute immunity. Domain expertise provides a critical head start, but it is no longer a permanent shield. If vertical incumbents grow complacent in their execution, the barrier to code creation is now low enough that enterprise clients will simply build bespoke AI solutions to bypass them entirely.

8. Why Incumbents Are Struggling

While industry participants generally agree that software incumbents benefit from important advantages such as strong customer relationships and control over systems of record, the financial results so far tell a more limited story.

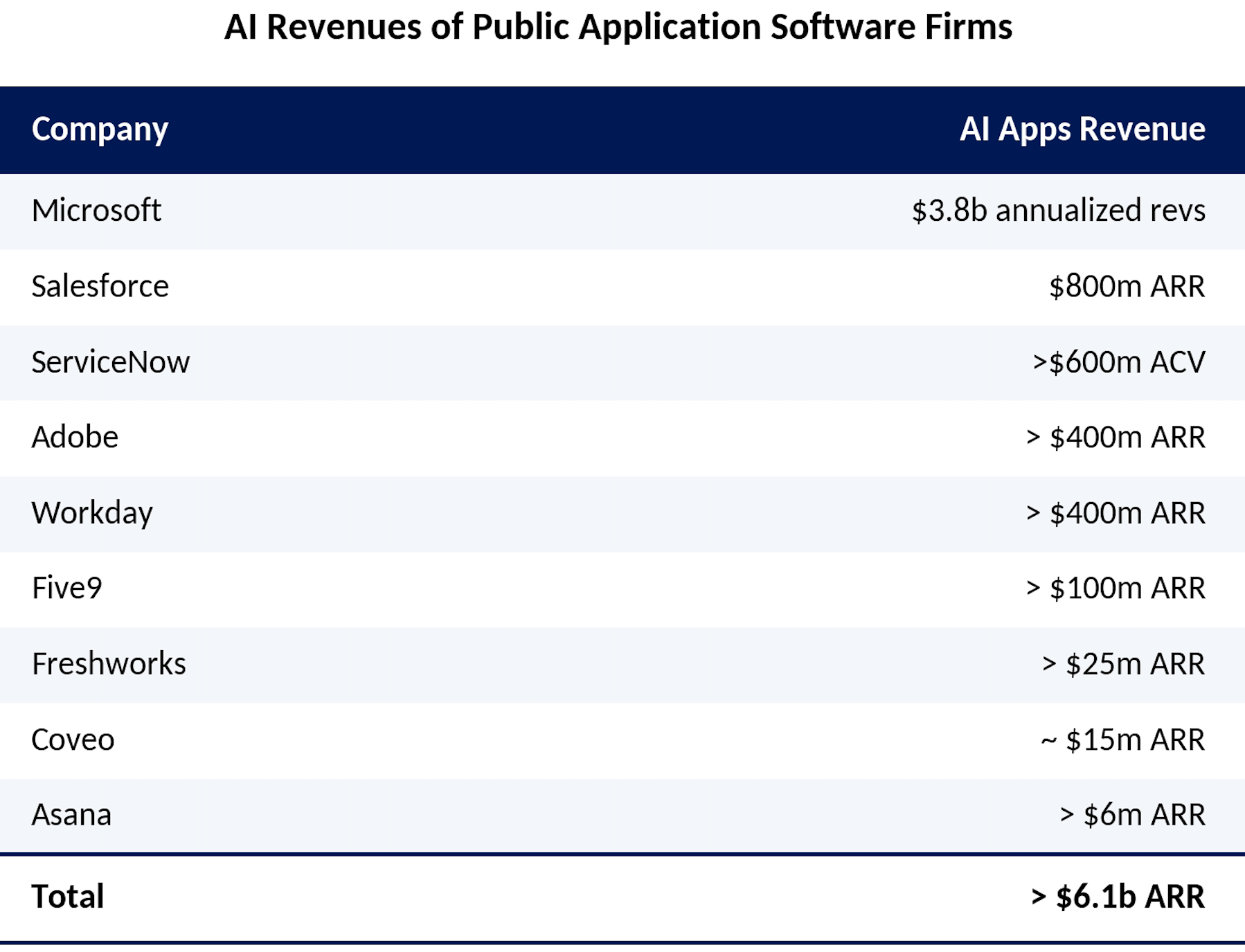

Total AI-related revenue reported across application software companies is estimated at around $6B. Excluding Microsoft, that number falls to roughly $2B. Against about $290B in combined revenue for the ten largest public SaaS companies, AI still represents only around 2%.

This gap raises an important question: why have these advantages not translated into stronger results yet? Even though enterprise adoption of AI is still early, incumbents are already trailing both AI-native startups and foundation model companies in growth. This suggests that scale, distribution, and installed customer bases have not yet translated into meaningful financial impact.

One reason is that many incumbent AI products are still early in their development. Market feedback often describes them as first-generation tools that lack depth, reliability, and consistency for mission-critical use. In some cases, they fail during pilot testing or do not meet security requirements needed for live production. As a result, some companies are choosing to build internal tools instead of relying on vendor solutions, mainly to keep pace with change.

Internal processes also slow things down. Large software companies must work through multiple layers of approval, coordination across teams, and strict governance, which reduces how quickly they can build and release new products.

In contrast, AI-native companies tend to operate with simpler teams and are more willing to experiment quickly. At the same time, incumbents still depend heavily on their core products for most of their revenue, which limits how much focus they can shift toward AI.

Pricing models add another challenge. Most legacy software companies still rely on per-seat pricing, but this becomes less effective as AI begins doing the work directly. In that setting, value depends more on output than on number of users. Over time, this is likely to lead to usage-based or hybrid pricing models.

However, this shift is happening slowly, and many companies are still offering AI features at little or no extra cost to encourage adoption. For example, Microsoft has bundled external model capabilities into its Copilot product without separate pricing, although this could change later.

Customer discussions also point to potential changes in workforce needs, with estimates of up to 30% reductions in areas like customer support, IT help desks, and engineering over the next two years. Even so, overall spending with software vendors is still expected to grow in the high single digits, as savings from labor are partly redirected toward software and new AI capabilities.

For now, most buyers are focused on reducing labor costs rather than cutting software budgets. The bigger risk for incumbents appears when customers bypass vendors completely by building internal tools or switching to AI-native alternatives, which would lead to lost revenue that is harder to replace.

Finally, there is an ongoing debate about whether incumbents need to rebuild core parts of their technology to fully adapt to AI. Most industry views suggest that a full rebuild is unlikely, but we are less convinced. In reality, meaningful upgrades alone may not be enough in many cases.

We think the more realistic path is layering AI into existing products, but at the same time fundamentally reshaping how they are used, with interfaces shifting away from dashboards toward natural language and agent-based workflows.

That said, not all companies are equally prepared. We see platforms like ServiceNow (NOW) as better positioned due to their unified data design, while companies such as SAP and Salesforce likely face more complex upgrades.

At a deeper level, the shift is from traditional rule-based systems built on structured data to AI systems that work with unstructured information, understand context, and carry out tasks dynamically. Bridging this gap remains one of the key challenges for established software companies.

9. The Playbook: Where We Are Allocating Today

Given our view of the software landscape, the mandate is simple: own proprietary data and mission-critical execution.