Our Favorite Risk/Reward Idea for Japan

In-Depth Initiating Report on a Mispriced Japanese Operator

By Aurelion Research

Description: Global Small-Cap | Infrastructure Operator

We are adding the stock today to the Aurelion Index.

Introduction

If you read our recent article on Japan, published earlier this week, you already know why we believe the time has come to take a closer look at the market. Japanese equity valuations are attractive, sentiment is starting to turn, and the yen still appears undervalued in our view.

If you haven’t had the chance to read it yet, it would be a good idea to do so, as it helps explain why we are bullish on Japan. See below.

Capitalizing on the Recent Pullback

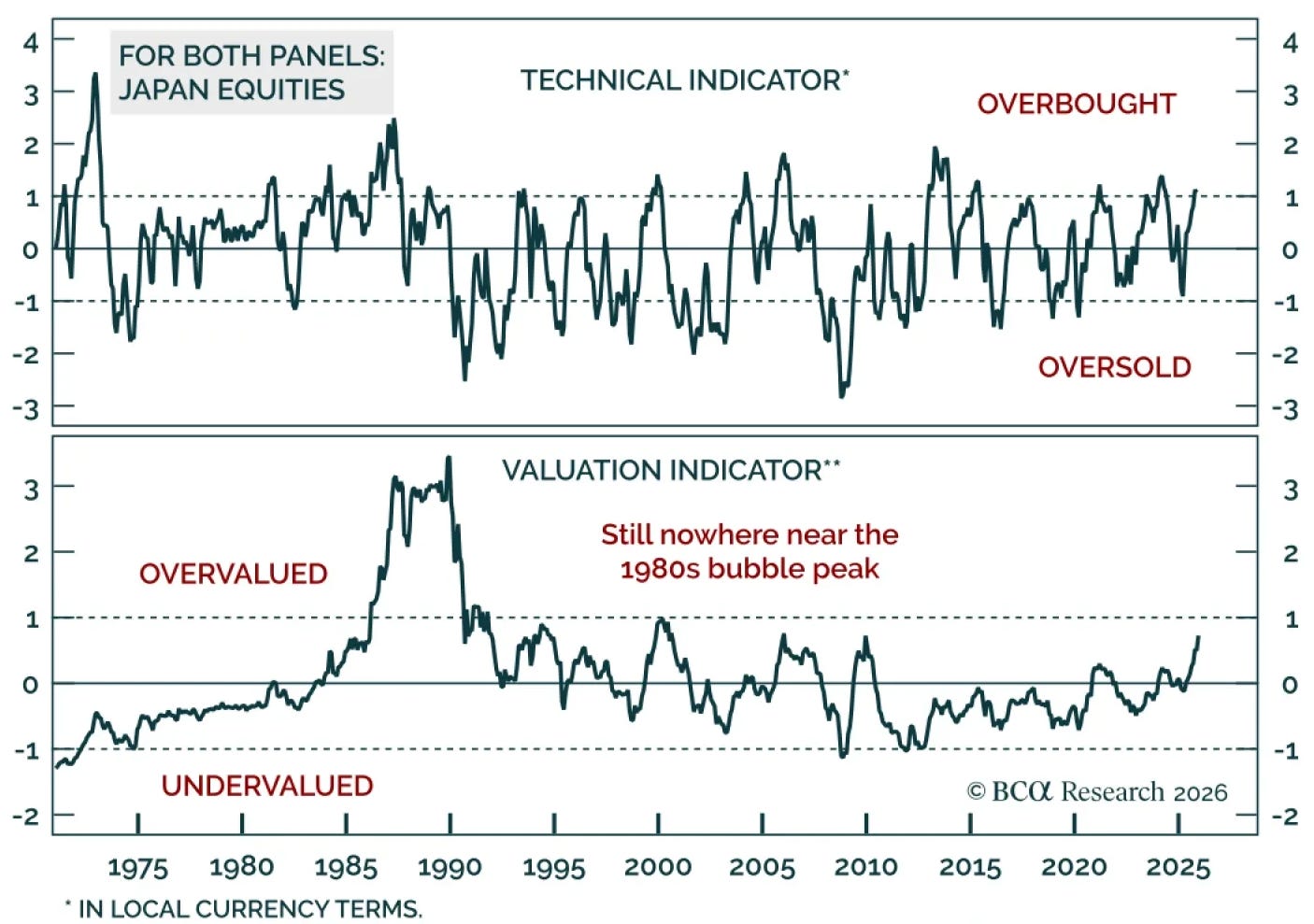

Japanese equities have recently entered a period of outperformance in both local and common currency terms. We share a high conviction view with BCA Research that recent market volatility offers a strategic entry point.

The technical indicator in the chart illustrates that the market has retreated from overbought levels toward an oversold state, representing a healthy correction that sets the stage for further gains. Because the valuation indicator remains well below the 1980s bubble peak, we believe the current trend rests on a solid foundation with significant growth potential and an opportunity to buy the dip.

Mean Reversion & Multi-Decade Value

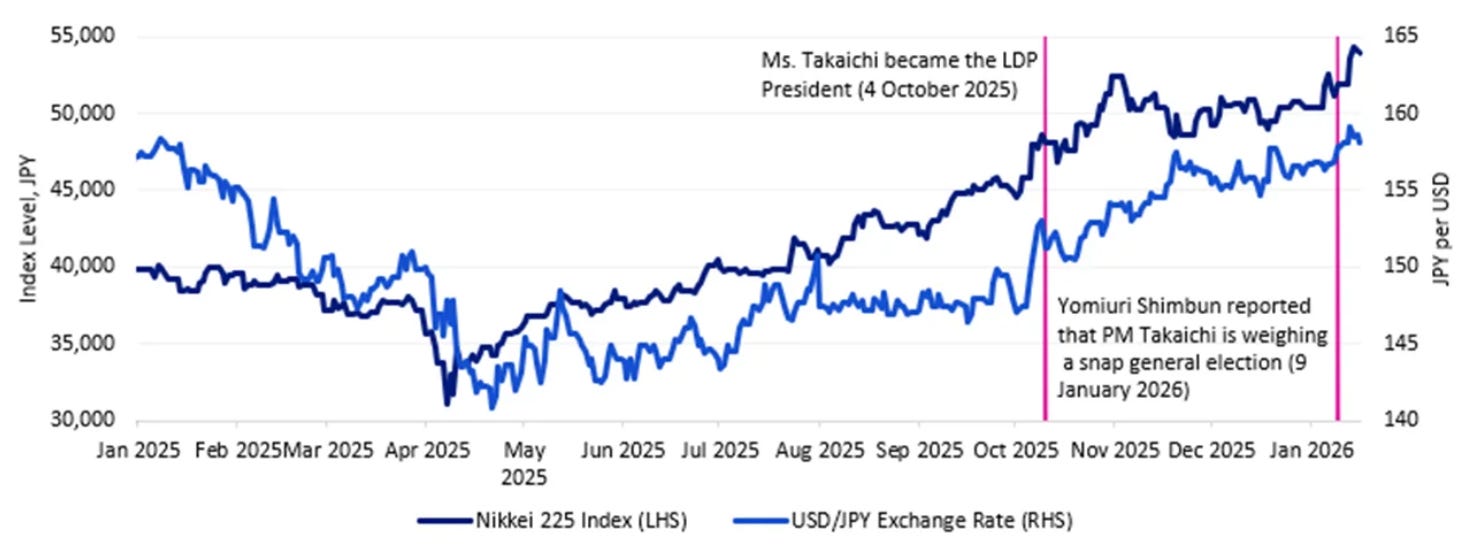

We are closely monitoring the political landscape following reports that PM Takaichi is weighing a snap general election. While political uncertainty often cause volatility, we view the correlation between the Nikkei 225 and the USD/JPY exchange rate as the more critical factor to watch.

We believe the market is mispricing the potential stability a consolidated administration could bring. We see any dip related to election headlines as a noise event rather than a fundamental deterioration of the thesis.

Nikkei 225 Index & USD/JPY Exchange Rate

We acknowledge that Japan’s equity risk premium has dropped to its lowest level since 2010. While some analysts interpret this decline as a clear sell signal, we think the exact opposite. Buy the Dip!

We view this shift as a structural re-rating of the Japanese market as it exits decades of deflation. In this environment, the premium for holding equities should naturally lower. We believe this dynamic validates our focus on specific high quality names within the broad index.

Japan’s Equity Risk Premium Drops to Lowest Since 2010

We view the industry of today’s new stock addition to the Aurelion Index as having a formidable moat and minimal competition. Barriers to entry are effectively absolute, making this a demand-driven thesis rather than one shaped by competitive dynamics.

This asset class has performed exceptionally well globally in recent years, yet it is distinct from the technology, AI, or semiconductor narratives.

We view the business model of our pick as fundamentally much simpler.