New Stock: Riding China's Chip Revolution

U.S. export controls just created a clear AI trade in semiconductors.

We are adding a new stock to the Aurelion Index.

We do not add positions often. When we do, it is because we have done the work, the timing is right, and we have genuine conviction. This is one of those moments.

It operates in one of the most defensible corners of the semiconductor value chain. The kind of business where customers do not switch suppliers, where expertise takes decades to build, and where the AI infrastructure wave creates demand that has nowhere to go but up. Very few companies in the world can do what this one does, and that is precisely why we want to own it.

While the world debates which AI model wins, China is building the infrastructure to make the entire debate irrelevant. And while most investors are focused on who makes the chips, we think the real opportunity sits one step earlier. In what makes the chips possible in the first place.

China is quietly winning the chip war. Morgan Stanley estimates the domestic self-sufficiency ratio has gone from 10% in 2021 to 41% in 2026, with industry projections pointing to 86% by 2030.

We know that sounds optimistic. But think about BYD. A decade ago, most people in the West had never heard of them. Today they are the largest electric vehicle company in the world, outselling Tesla in most markets. That did not happen by accident. When China commits to leading a sector, things tend to move faster than the rest of the world expects.

Semiconductors are following the same path. US export restrictions only accelerated that by removing any remaining hesitation in Beijing. Cutting off access to leading edge technology turned chip self-sufficiency from a long term goal into a national obsession backed by unlimited resources.

We want to be clear about something. We are adding this name because the fundamentals and timing align, the way they always have at Aurelion. This has nothing to do with chasing AI momentum. We have been early on oil tankers, dry bulk, uranium, and financial companies. We apply the same discipline here.

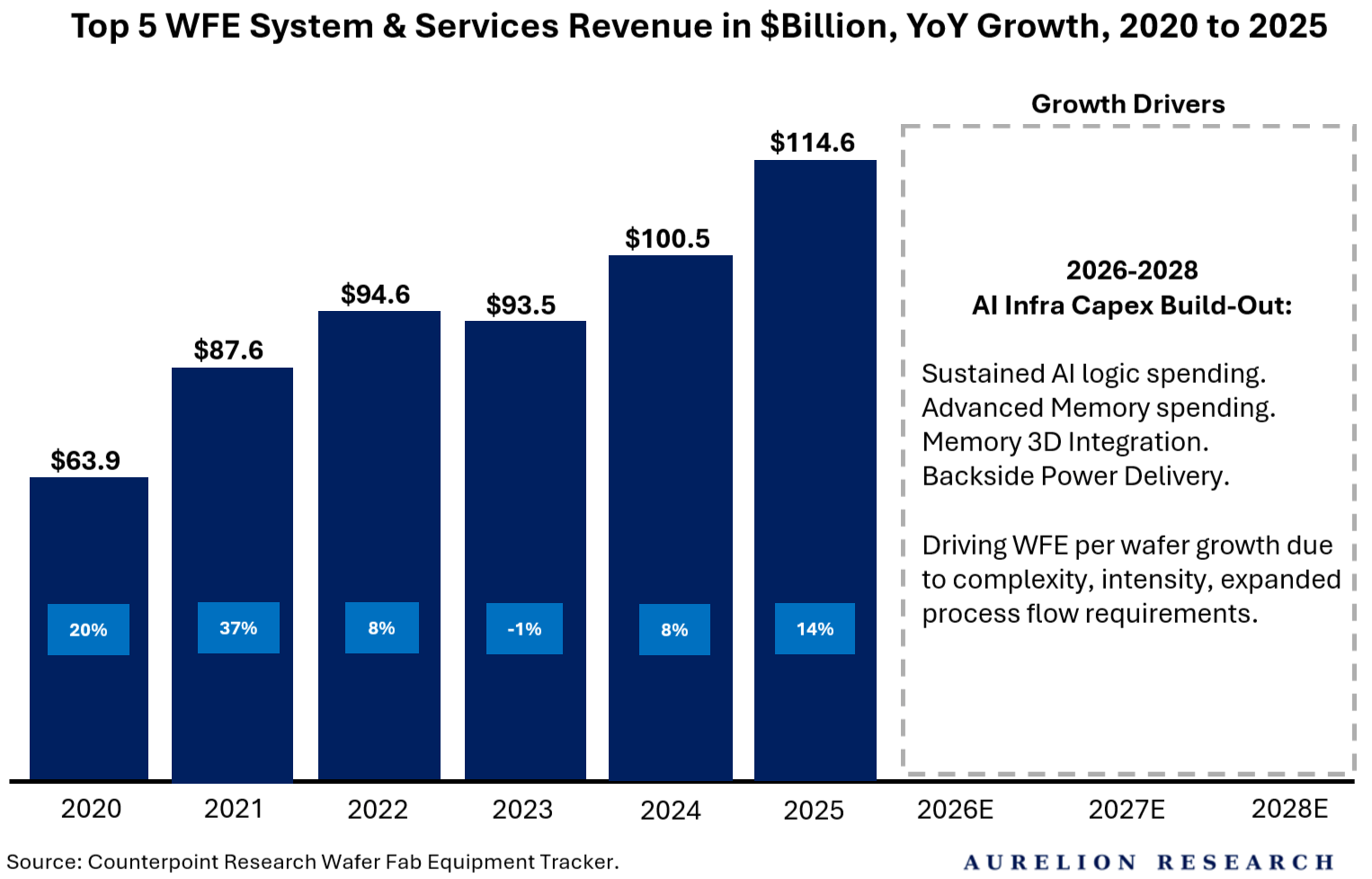

The segment we are most focused on within this theme is Wafer Fab Equipment, or WFE. Every time chip complexity increases, manufacturers need more equipment to process each wafer. That relationship is not going away.

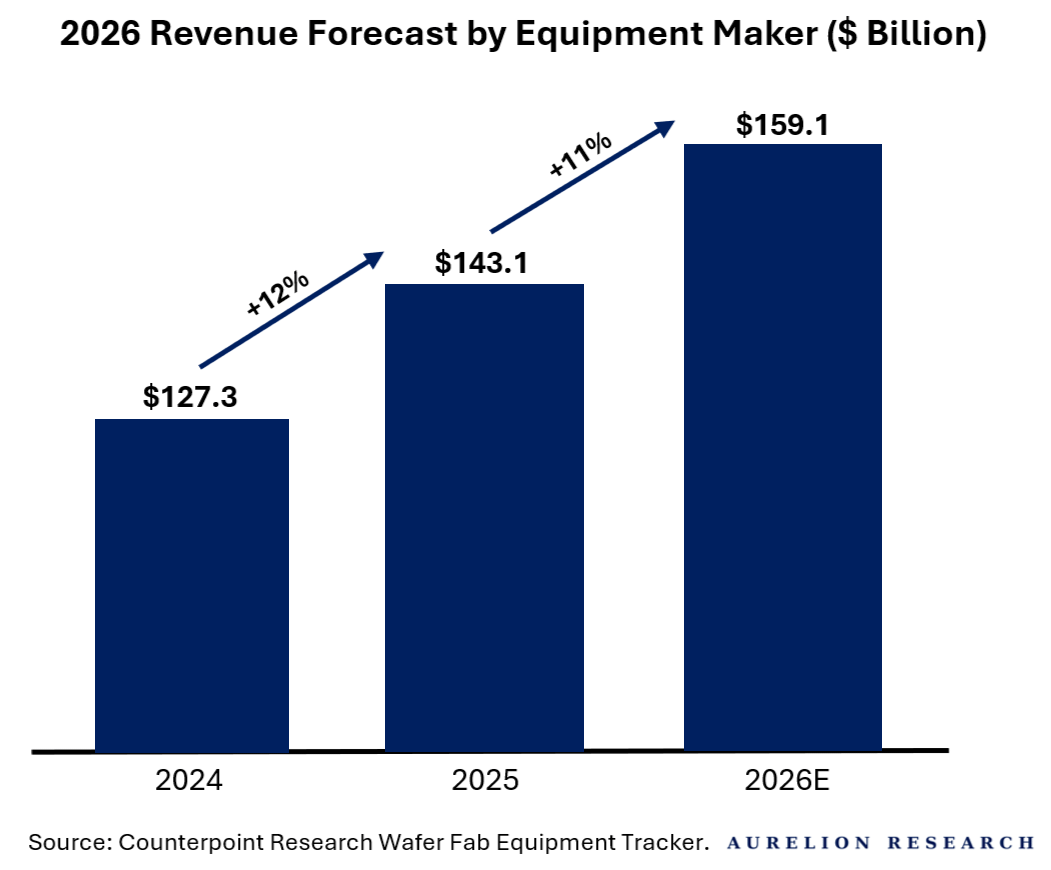

According to Counterpoint Research, total WFE revenues grew 12% YoY in 2025 to $143.1B, driven directly by AI infrastructure buildout and surging demand for leading edge logic, High Bandwidth Memory, and advanced packaging.

The top five manufacturers alone grew revenues 14% to $114.6B. Counterpoint forecasts another 11% growth in 2026, reaching $159.1B.

The more complex the chip, the more equipment it takes to build it. That is the thesis, and it compounds with every new generation.