New Position: An Overlooked Winner in a Weakening Consumer Cycle

Why this under-followed name can outperform through a weaker demand environment.

The average consumer in most developed markets has lost significant purchasing power since the pandemic. Inflation gutted the middle class. House prices went up, mortgage rates stayed high and salaries did not follow.

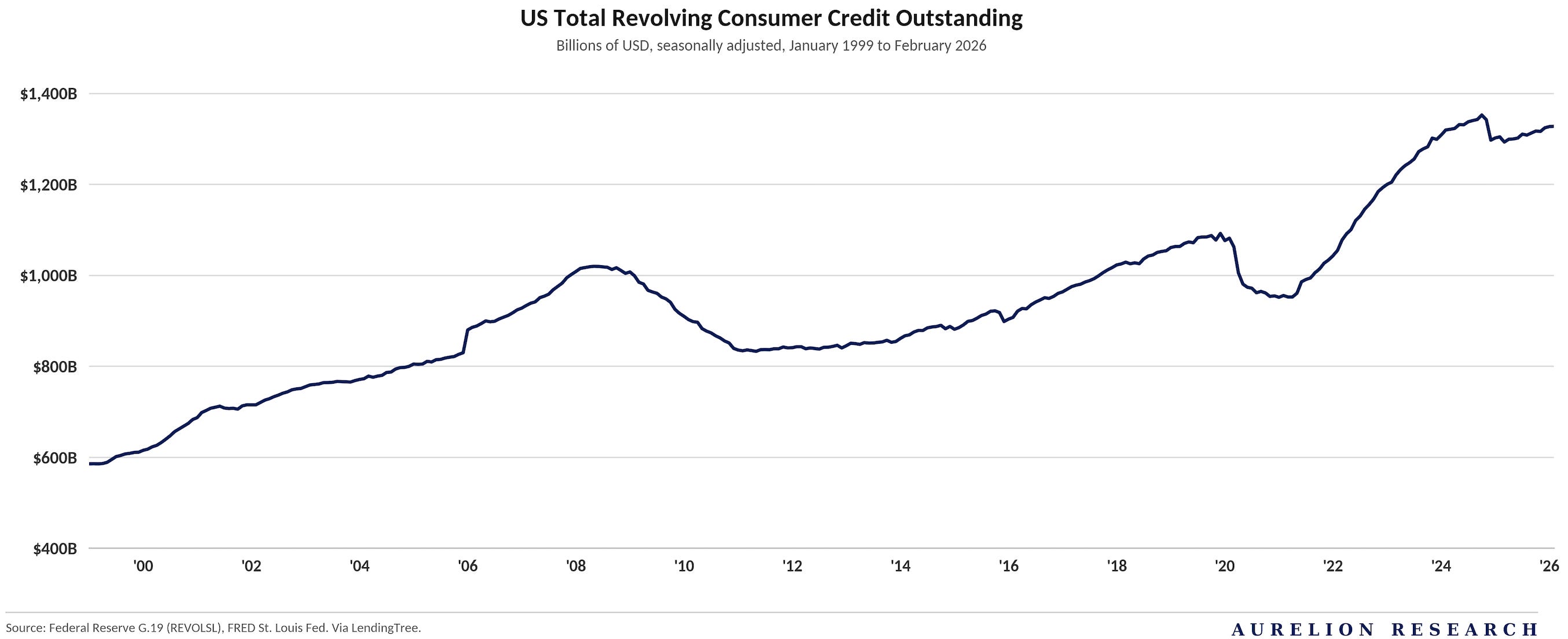

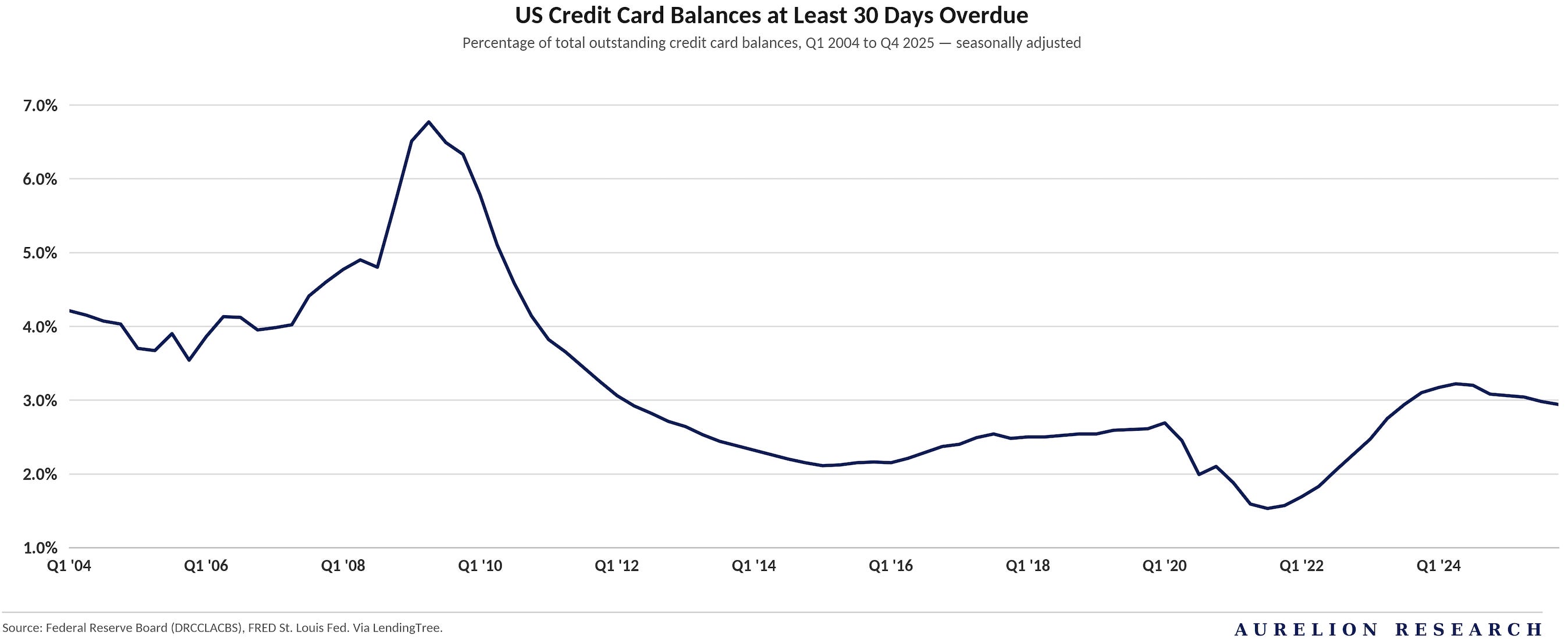

By 2024, US credit card debt had reached all-time highs and payment delinquencies were trending upward.

Buy Now, Pay Later boomed.

When consumers are financing even everyday purchases like a burrito, it speaks about the underlying health of the economy.

However, the situation was stabilizing. Fed rate cuts began to take effect and the AI boom was fueling optimism of productivity gains.

The new Republican administration was promising affordable homes, lower energy prices, and a growing job market. Consumer health and investor sentiment finally got a breath.

We can see in the data from the charts above and below that consumer health began to improve in late 2024.

2026: Consumer Health Weakens Again

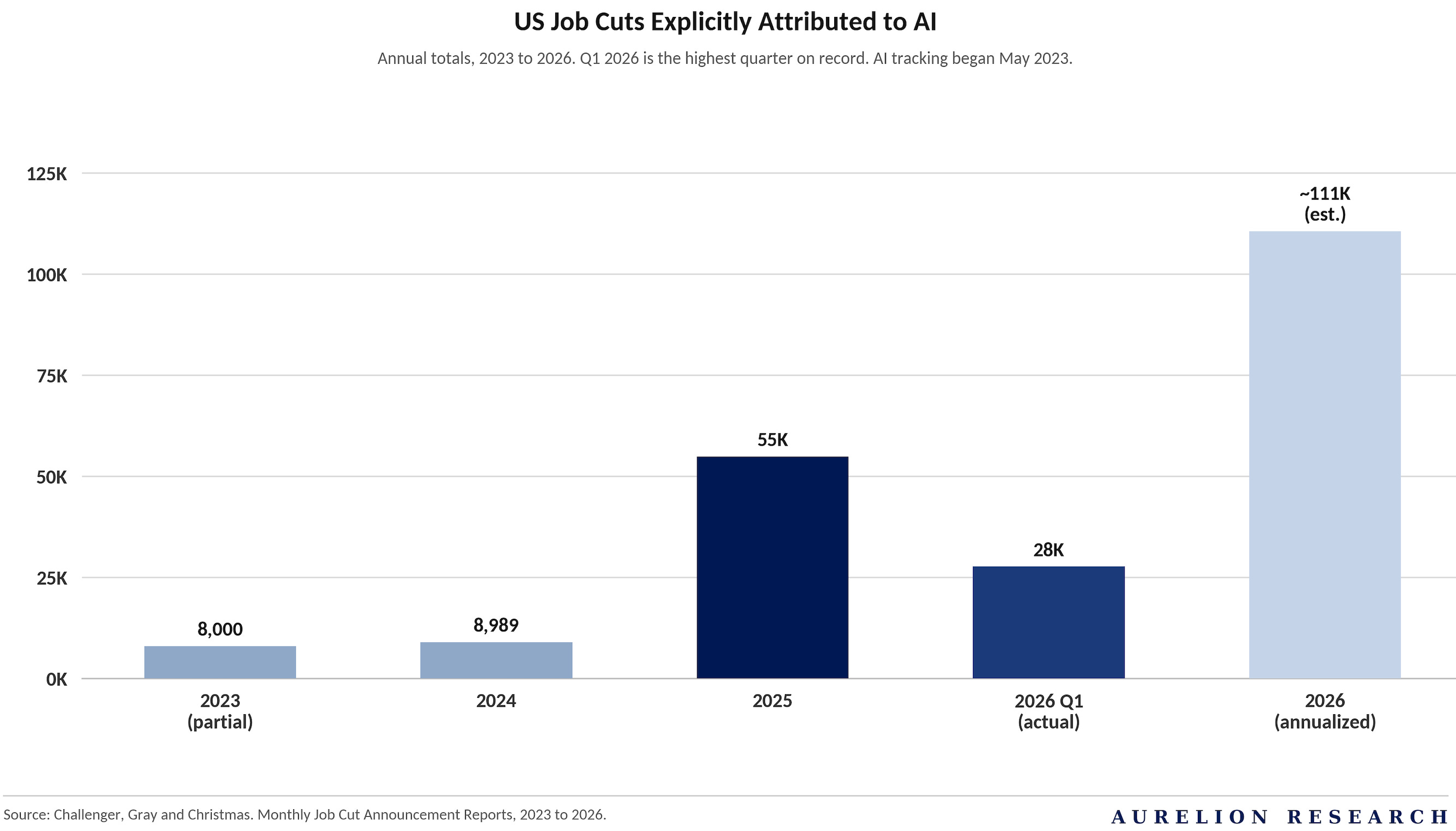

The two factors that have turned the recovery into what we believe is a continued period of weaker consumer health are AI and oil.

AI was supposed to be the “fix”. Productivity gains were expected to lift wages, justify high stock market valuations, and ultimately put money back into consumers’ pockets. That thesis is now under serious pressure.

First, AI driven job loss is looming over white-collar work. While some AI-related job cuts are simply a way for companies to explain broader layoffs aimed at improving margins, the overall trend is clear.

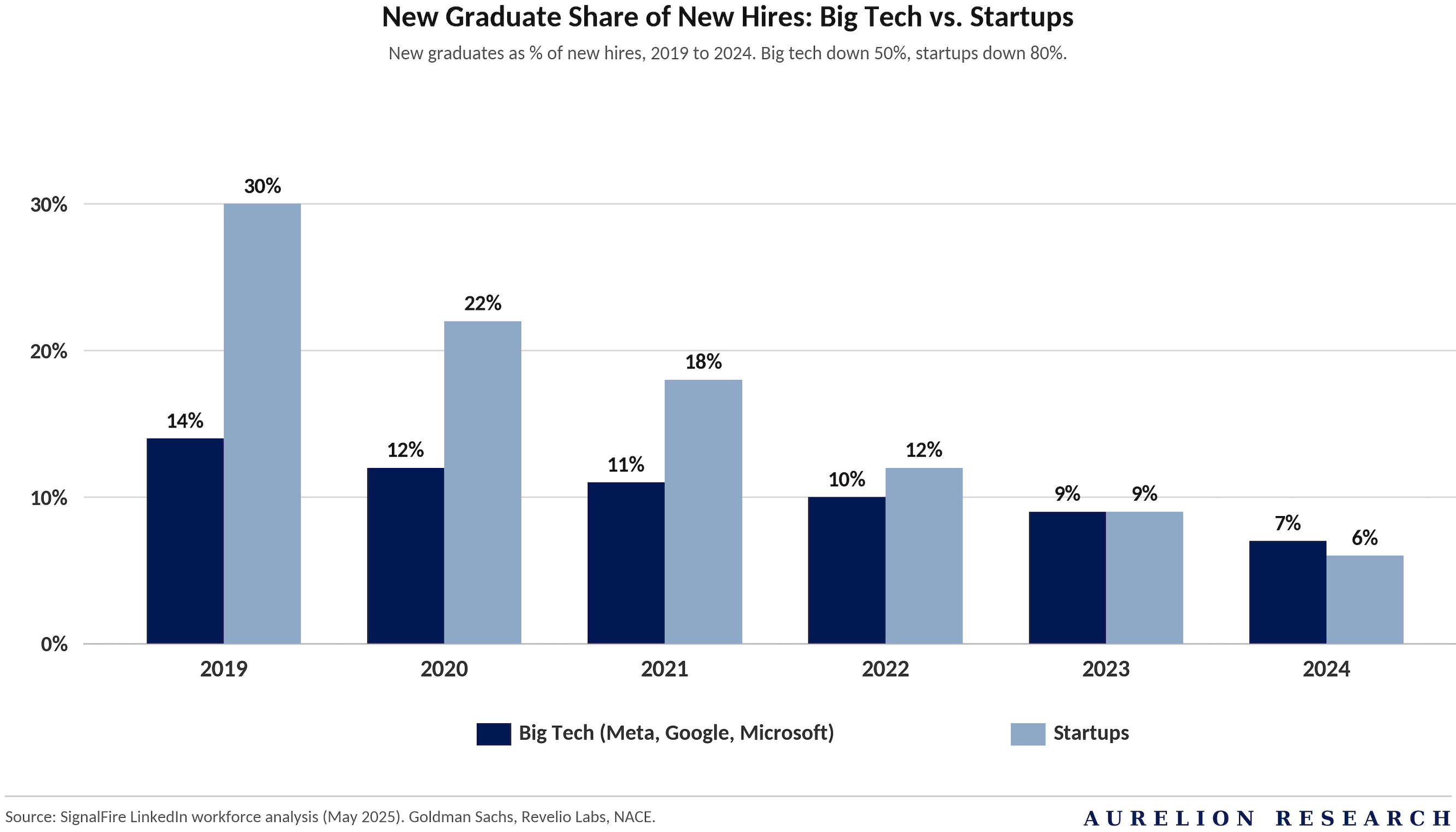

The real damage shows up in decreasing entry-level hiring. Roles that used to absorb hundreds of thousands of new graduates, such as junior analysts, entry-level coders, and compliance work, are now being done by AI tools.

The chart below shows the result: the share of new graduates among new hires has fallen sharply at both large tech firms and startups.

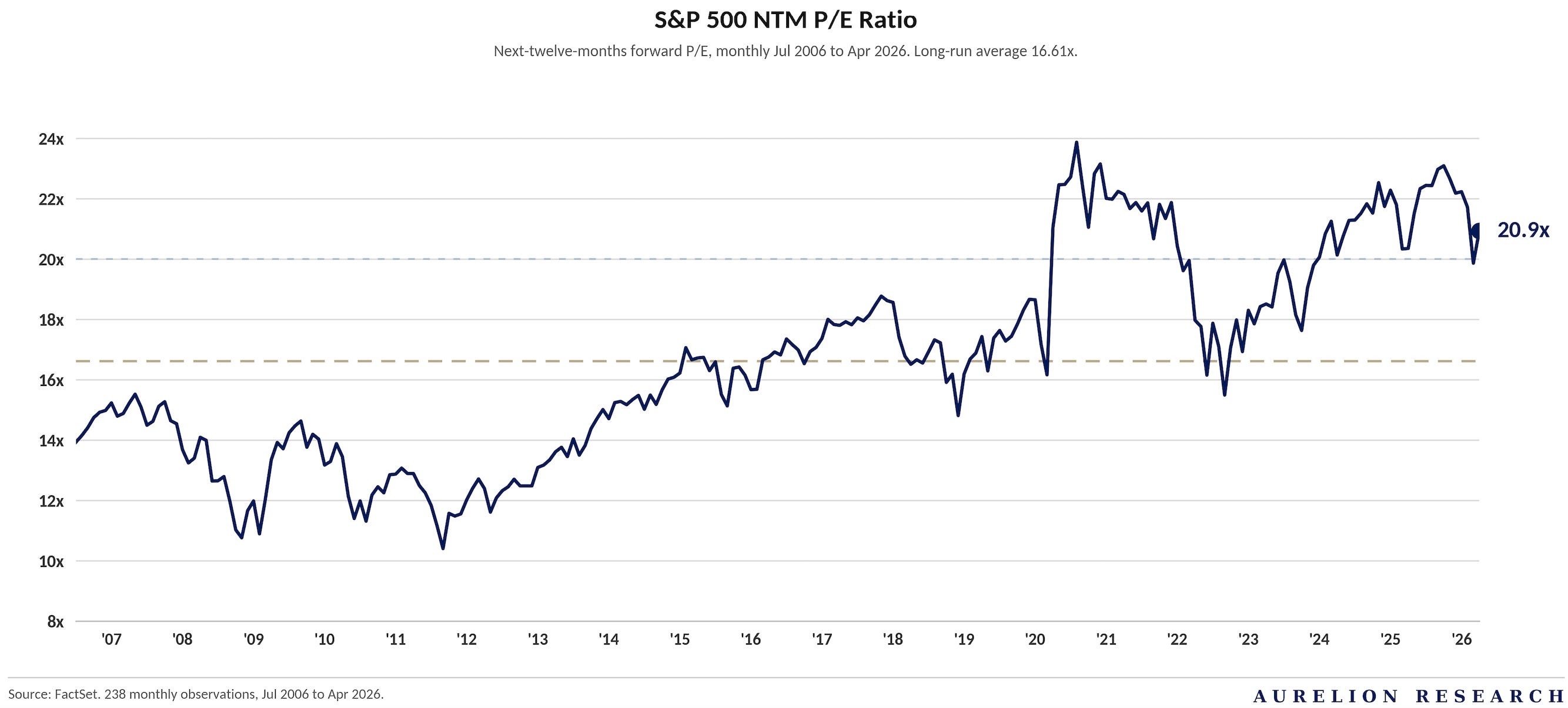

Meanwhile, the stock market continues to price in strong productivity gains. The S&P 500 trades at a forward P/E of 20.9x, elevated versus its long-run average of 16.6x. This premium implies sustained earnings growth, which in turn depends on meaningful productivity gains from AI.

However, the evidence so far points to diminishing near-term returns on AI investment. Companies are committing significant capital to infrastructure, yet the economic payoff at the consumer level has yet to materialize.

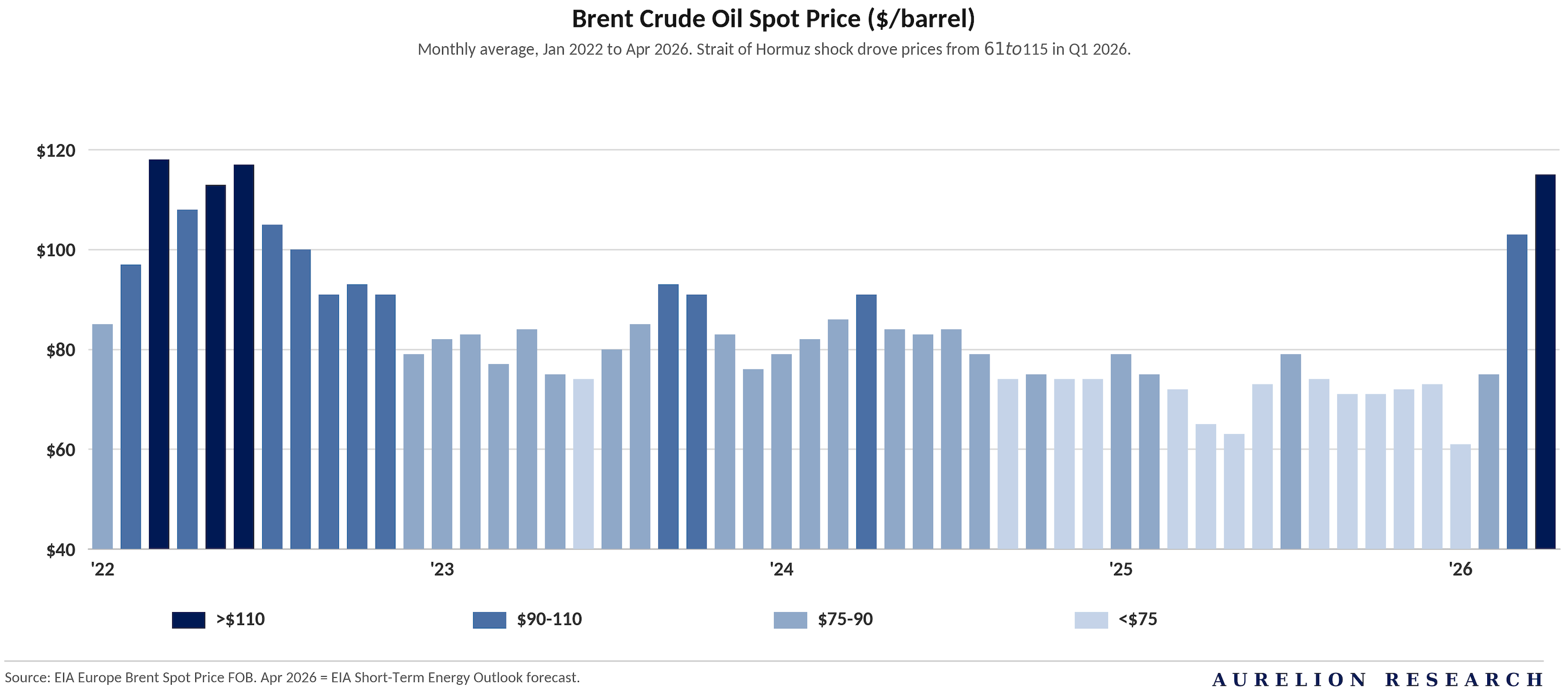

And now, disruptions in the Strait of Hormuz are driving oil prices higher, with consumers facing a potential 25–30% increase in fuel costs at the pump.

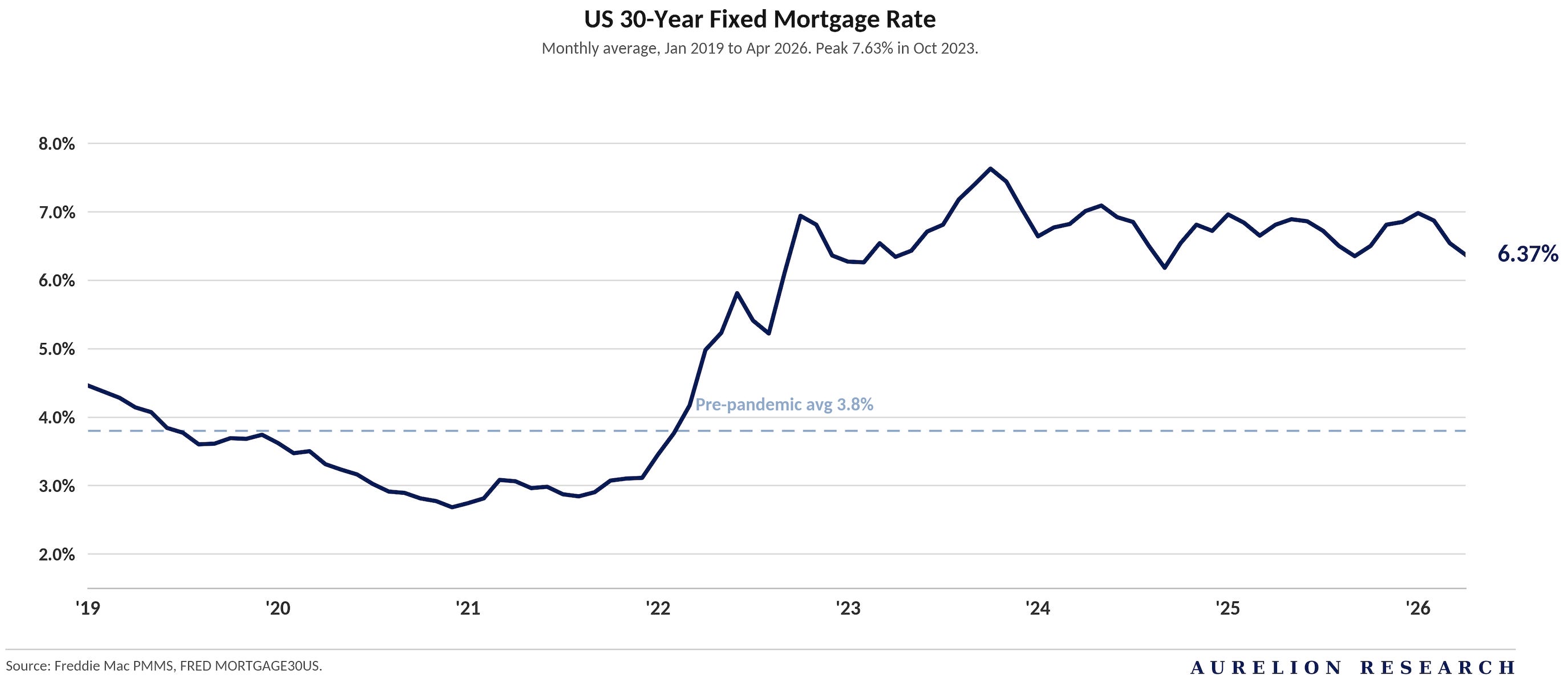

Despite rate cuts, mortgage rates have stayed higher than expected.

Right now, rising oil prices and inflation concerns are offsetting the mechanical impact of prior Fed rate cuts. This has kept housing in both the US and the broader G7 markets largely unaffordable for most households.

The Setup

We do not expect a significant market crash, but we believe this creates a very attractive setup to invest in companies that benefit from a weakened consumer. Rising debt, weak housing affordability, AI-driven job anxiety, and now a ~$100/barrel oil shock are all compressing real disposable income.

Historically, pawn shops, discount retailers, thrift stores, and dollar stores outperform in these types of environments. Certain defensive names have already started to move. The question is which high-quality names remain undervalued before the market reclassifies them as defensives.

The company we are adding to the Aurelion Index is an under the radar consumer defensive that we believe should trade at a higher, more normalized multiple. It has not received the attention it deserves. It is practically forbidden. That is exactly what makes it attractive to us.

Table of Contents

Company Description

Investment Thesis

Canadian Market Outlook

Business Overview

The Profit Advantage

Strategic Analysis

Best-in-Class Value Positioning

Macro Environment

US Market Overview

Operational Margin Pressures

Mitigating Factors & Efficiency Gains

Valuation & Price-Targets

Key Risks

Our Final Take