Macro Update: The Big Picture on Oil Markets

Why the market is drastically underpricing the worst oil supply shock in modern history.

Everyone is watching the recent developments in the Middle East and the massive economic impacts of the Strait of Hormuz closing.

We want to cut through the noise and look at how the global supply of oil has violently shifted compared to world demand over the past few months. We also want to highlight a hidden risk that could drive prices much higher due to unpredictable attacks on key infrastructure.

To be clear upfront, we do not believe oil prices will stay high forever. However, we see massive risk for prices to spike in the short term because current market prices completely fail to reflect the severe, real world shortage of oil happening right now.

This is a Pro-tier Macro update from Aurelion Research. On rare occasions, we share a preview of Pro content with all subscribers when the topic warrants broader visibility.

The Historic Supply Shock: Only the Beginning?

Just a few months ago, experts expected a massive oversupply of oil. Fast forward to the end of March, and the extreme fragility of the global energy trade is fully exposed. The closure of the Strait of Hormuz brought around 20% of daily global oil movement to a grinding halt. This instantly plunged the market into the largest supply shock in history.

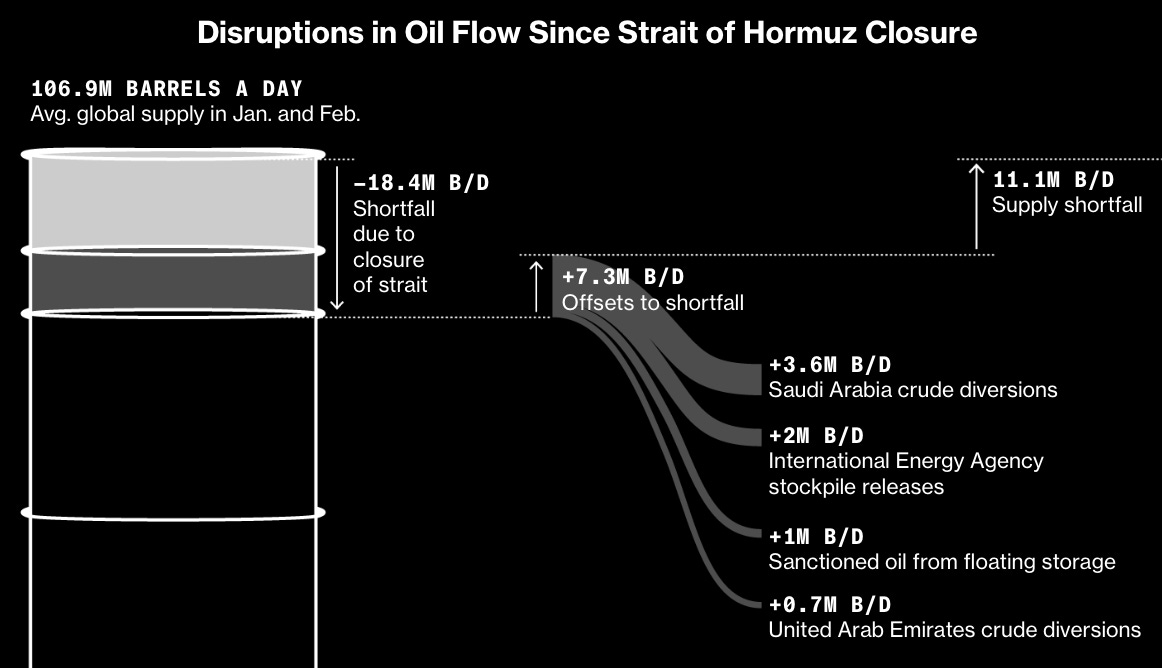

Quantifying the Massive Shortfall. As detailed in the exhibit below, the initial closure removed a staggering 18.4M barrels daily from the global market. Emergency actions and alternative pipelines have managed to replace a portion of this loss. However, the world still faces a massive net shortage of 11.1M barrels daily. This physical roadblock makes the vast majority of the global backup oil supply completely inaccessible.

A Market Underestimating the Risk. We are now one month into this crisis. The immediate economic impacts are already severe, characterized by surging global prices and physical fuel shortages across Asia. Yet, conversations with industry insiders reveal a clear consensus. The broader market still does not grasp the true severity of the situation.

The Crisis Spreads West. Experts are now drawing direct parallels to the historic oil shocks of the 1970s. They warn that a prolonged closure will trigger an even larger economic fallout.

The localized fuel shortages currently squeezing Asian markets will rapidly spread westward. Europe remains highly vulnerable and will likely face surging prices as nations desperately bid to secure any available energy cargoes. As the global supply chain fractures, European markets are at severe risk of experiencing outright physical diesel shortages in the coming weeks.

The True Consumption Gap & Exhausting Lifelines

While previous sections outlined the massive physical supply shortfalls, the actual consumption math remains grim. Even factoring in reduced demand from Asia, the global market still faces a net 9M barrel daily deficit compared to pre-war levels. To put the sheer scale of that shortage into perspective, this missing volume exceeds the total daily oil consumption of the UK, France, Germany, Spain, and Italy combined.

Running Out of Temporary Fixes. The market is quickly burning through its temporary safety nets. Exceptional measures, such as issuing U.S. waivers on Russian & Iranian oil sanctions, have bought the global economy some crucial time. However, these are strictly finite lifelines. Once these emergency options are completely exhausted, global leaders will have virtually no tools left to artificially suppress prices without physically reopening the waterway.

The Unique Threat to Natural Gas

While crude oil has at least a few alternative pipeline routes, the situation for liquefied natural gas is entirely rigid. The final ships carrying Middle Eastern gas are arriving at their international destinations right now. Once they are empty, there are virtually no alternative physical routes to get that stranded gas to global buyers. Making matters worse, there are almost no strategic global stockpiles available to cushion a natural gas shortfall.

The North American Fortress. Retail gasoline and diesel prices have certainly jumped domestically, but the U.S. is structurally positioned to weather this crisis better than any other region. Geographically removed from the conflict and far less reliant on Middle Eastern transit, the American energy market is heavily protected. Furthermore, as the absolute largest exporter of liquefied natural gas in the world, the massive domestic gas market remains deeply insulated from the unfolding global chaos.

Ignoring the Noise & Assessing the True Risk

Political Talk Versus Reality on the Ground. The White House continues using public statements to try and force prices lower, with President Trump recently pushing oil below $90 per barrel on social media by claiming the conflict is effectively over. However, we see a massive disconnect between this political rhetoric and the reality on the ground. A legitimate peace deal remains highly unlikely right now. Both sides are deeply entrenched in their demands, and the potential deployment of American forces into the region points toward severe escalation instead of a peaceful resolution.

The Escalating Threat to Backup Shipping Routes. Given their focus on unconventional warfare, Iran and its allies are highly likely to target backup global supply routes to apply maximum economic pressure. With the Houthis entering the conflict this past weekend, the risk to passing cargo ships and vital infrastructure continues to climb.

We view the following backup transit points as highly vulnerable targets:

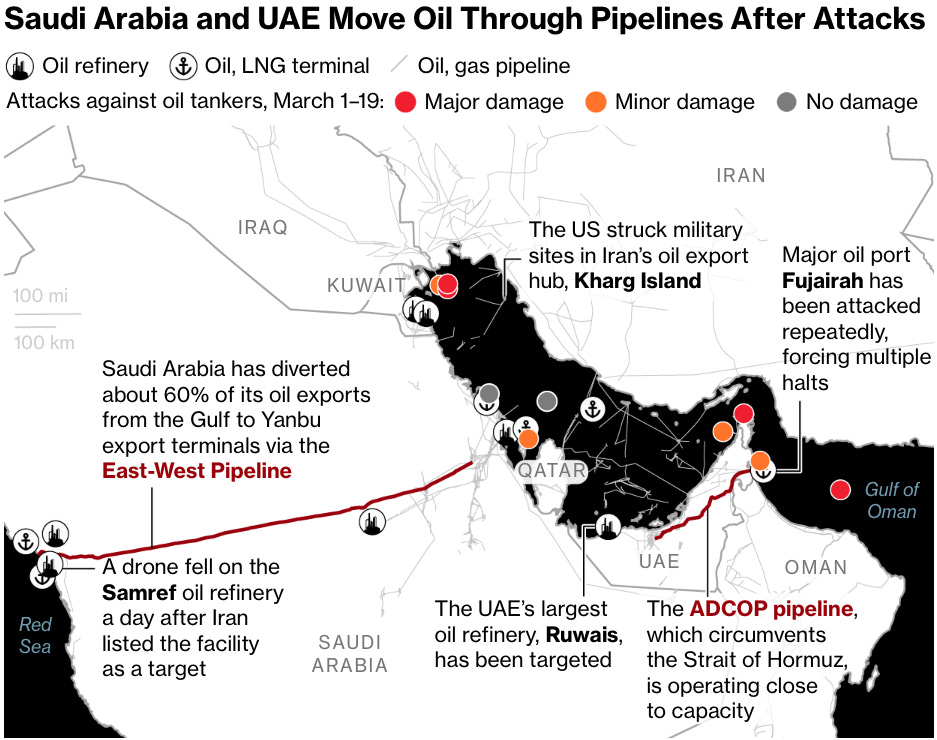

The Saudi East to West Pipeline & Yanbu Port: This critical infrastructure allows up to 7M barrels of Saudi oil per day to bypass the Strait of Hormuz and load directly onto ships in the Red Sea.

The Bab el Mandeb Strait: Located at the southern end of the Red Sea, this narrow passage historically handles 4 to 5M barrels daily. The number of potential targets here is currently very high because ships diverted from Saudi Arabia are crowding the area as they head south toward the Indian Ocean.

The UAE Bypass Pipeline: Carrying nearly 1.8M barrels of oil per day, this pipeline represents another highly attractive target for disrupting regional exports.

Middle East Crude Chokepoints: