Is It Too Late to Buy Petrobras (PBR)?

We believe Brazilian equities are ready to run

By Aurelion Research

Introduction

So, as the title says, is it too late to buy Petrobras? Well, that is a really good question and one we are going to try to answer in the best way possible.

First, if you aren’t familiar with the company, here’s a quick description.

Company Description: Petrobras is Brazil’s national oil company and is controlled by the Brazilian federal government. It holds a dominant position across the domestic value chain as the country’s largest oil producer and the owner of most refining capacity. The core of the investment case sits in the pre-salt portfolio, led by Búzios, and in the company’s large refining footprint concentrated in São Paulo and Rio de Janeiro.

Investment Thesis

Petrobras presents a compelling value proposition within the Latin American energy sector. Following the release of the 2026–30 strategic plan, we believe the equity offers strong fundamentals supported by five key drivers:

1. Dollarized Revenue Streams

The company’s revenue is primarily tied to USD linked international benchmarks, insulating the top line from Brazilian Real volatility and providing meaningful hard currency exposure.

2. Execution Strength

Production growth is supported by a high quality pre salt portfolio (deep offshore reservoirs located beneath thick salt layers), where lifting costs remain among the most competitive in the global offshore space.

3. Policy Predictability

The tax and regulatory backdrop is clearer, reducing uncertainty around cash flows and valuation. Recent tax changes are now largely understood, and we believe the current share price already reflects the updated fiscal regime.

4. Attractive Valuation

The equity trades at a discount across key multiples (EV/EBITDA, FCF) compared to regional peers, while offering a superior distribution yield.

Our Decision Regarding Petrobras

Based on the thesis points outlined above, our view is clear: we like Petrobras.

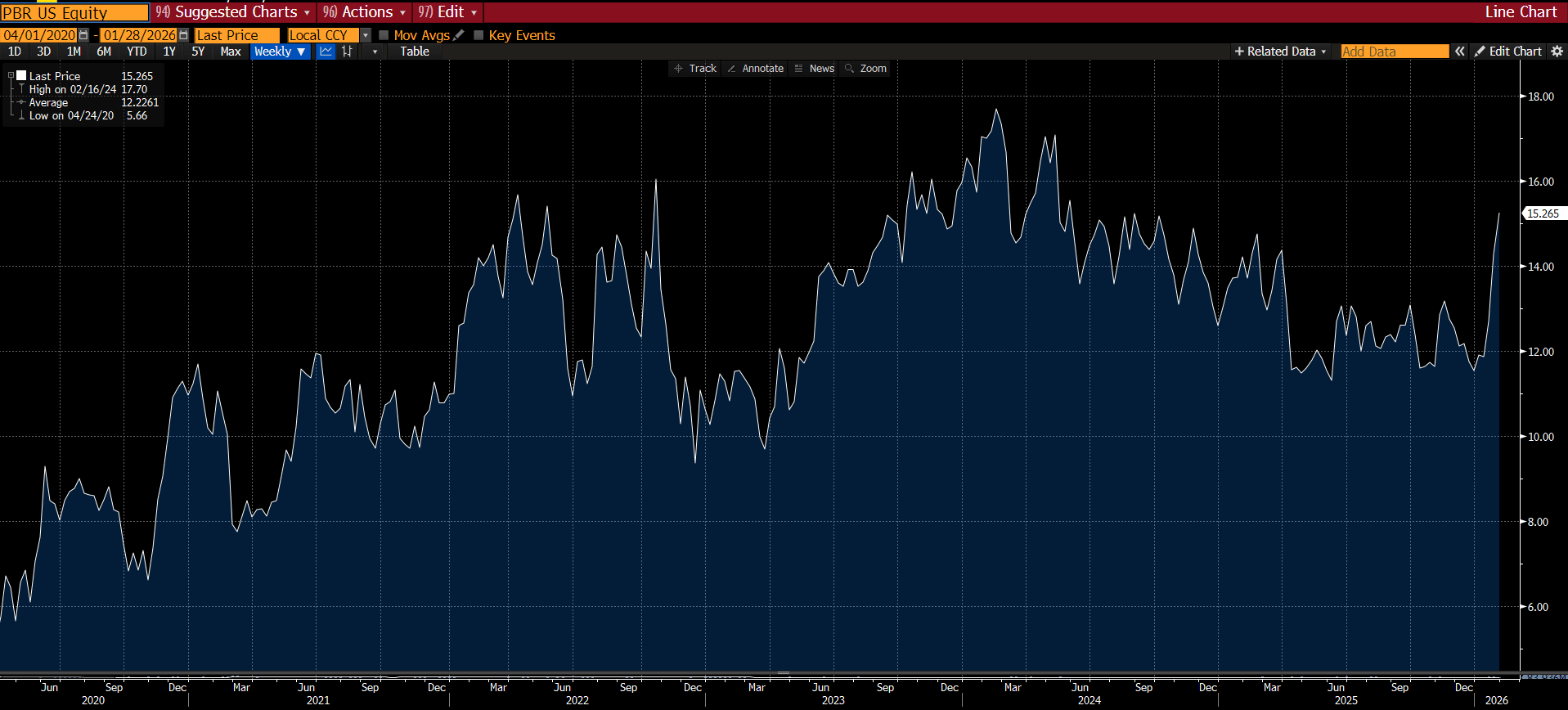

That said, it will not be added to our Index at this stage. As shown in the chart below, the stock has moved too far, too fast, rising from around $11 to above $15. We prefer to initiate positions when the entry point is more attractive, which could change on a pullback.

Petrobras (PBR) Share Price Performance

We believe the optimal entry window has passed. While we recognize the potential for significant appreciation of another 50% from current levels, it does not currently rival our highest-conviction ideas given the risk/reward. We view the stock as a compelling value play. However, on a relative basis, we have elected to pass.

However, we are still going to analyze it with you today because we are always willing to change our minds. We believe a key reason for our continued performance is that we have little to no ego. We listen to everything, filter what we hear, and move forward. We are always looking for the highest risk-adjusted alpha.

Brazil Macro Picture

Before analyzing Petrobras, it is essential to evaluate the current macro environment in Brazil, specifically interest rates, the economic cycle, and the political landscape. The October 2026 elections present clear optionality for regime change. However, the opposition currently lacks a unified candidate capable of challenging President Lula.

Consequently, we view his re-election as the base case. While the left is consolidated behind President Lula’s bid for re-election, the right remains fractured. Currently, Flavio Bolsonaro is the only prominent candidate on the right, though others are likely to join. The situation will only clarify once the candidate field is defined, which should occur by early April at the latest.

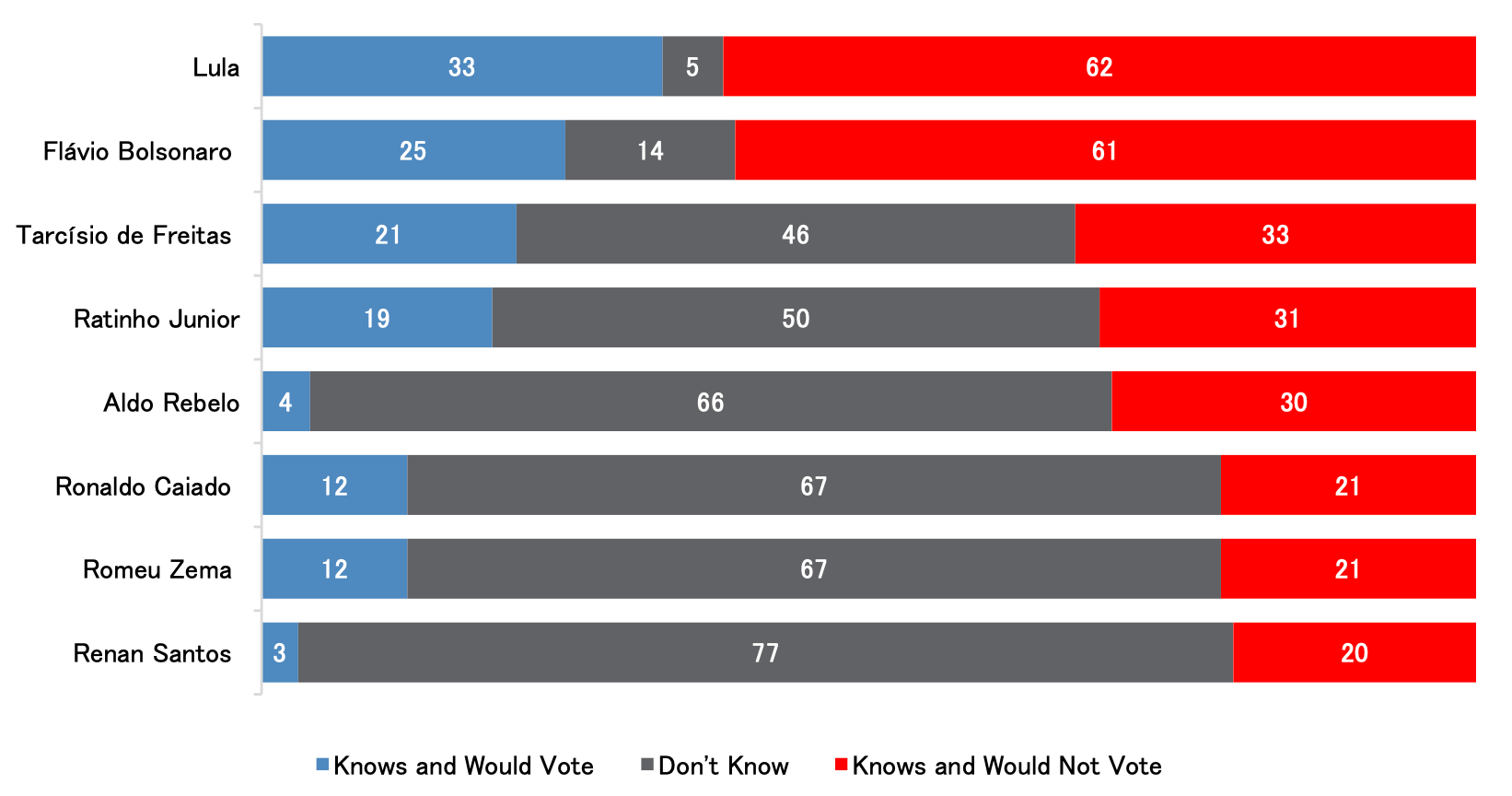

We turn to J.P. Morgan estimates to ground this view, as they provide high-quality data. As illustrated below, current polls indicate President Lula leading in voting intention across scenarios. Beyond the Bolsonaro family, Lula maintains the highest level of support.

Brazil: Voting Potential & Rejection Rates by Candidate (Jan 2026)

The Fiscal Reality

We believe government decisions on fiscal policy will be the ultimate differentiator for the economy in the coming years. While fiscal performance has recently topped expectations, it has been driven by resilient growth and tax revenue rather than actual spending cuts. This is why the market is demanding such a high premium to hold Brazilian assets.

There is a real concern that without further fiscal consolidation, current growth levels are not sustainable. If these dynamics don’t shift, the debt trajectory becomes difficult to justify. Even under a base case scenario, we do not see the debt-to-GDP ratio stabilizing within the next decade.

However, it is important to note that the growth of this debt is not expected to be explosive. In a low growth environment, stabilization would require long term interest rates to stay near 6% nominal. For the math to work in a high interest rate environment, we would need to see GDP growth reach at least 3%. Essentially, it will take a massive effort involving savings of over 12% of GDP through reforms to put the country on a truly credible fiscal path.

Market Dynamics & Strategy

Brazil enters 2026 at a pivotal moment. The stage is set for continued momentum as domestic liquidity rises and policy becomes more flexible. We expect Brazil to be among the most aggressive countries in easing monetary policy this year. The country has a lot going for it: clean energy, a massive role in global food production, and a tech-savvy financial system. These factors make it a strategic player that cannot be ignored.

Despite these strengths, the headwinds are real. Brazil carries one of the highest fiscal deficits in the emerging markets at ~9% of GDP, and government debt sits at 80% of GDP. This level of spending has kept real interest rates among the highest in the world.

However, the valuation is where it gets interesting. Brazil is currently trading at 9.3x forward earnings, which is a small discount compared to its 10x historical average. While earnings in energy and materials might look flat for 2026, we see the best opportunities in utilities, financials, and industrials, where growth is projected at 21% excluding commodities.

Brazilian Equities Are Ready to Run

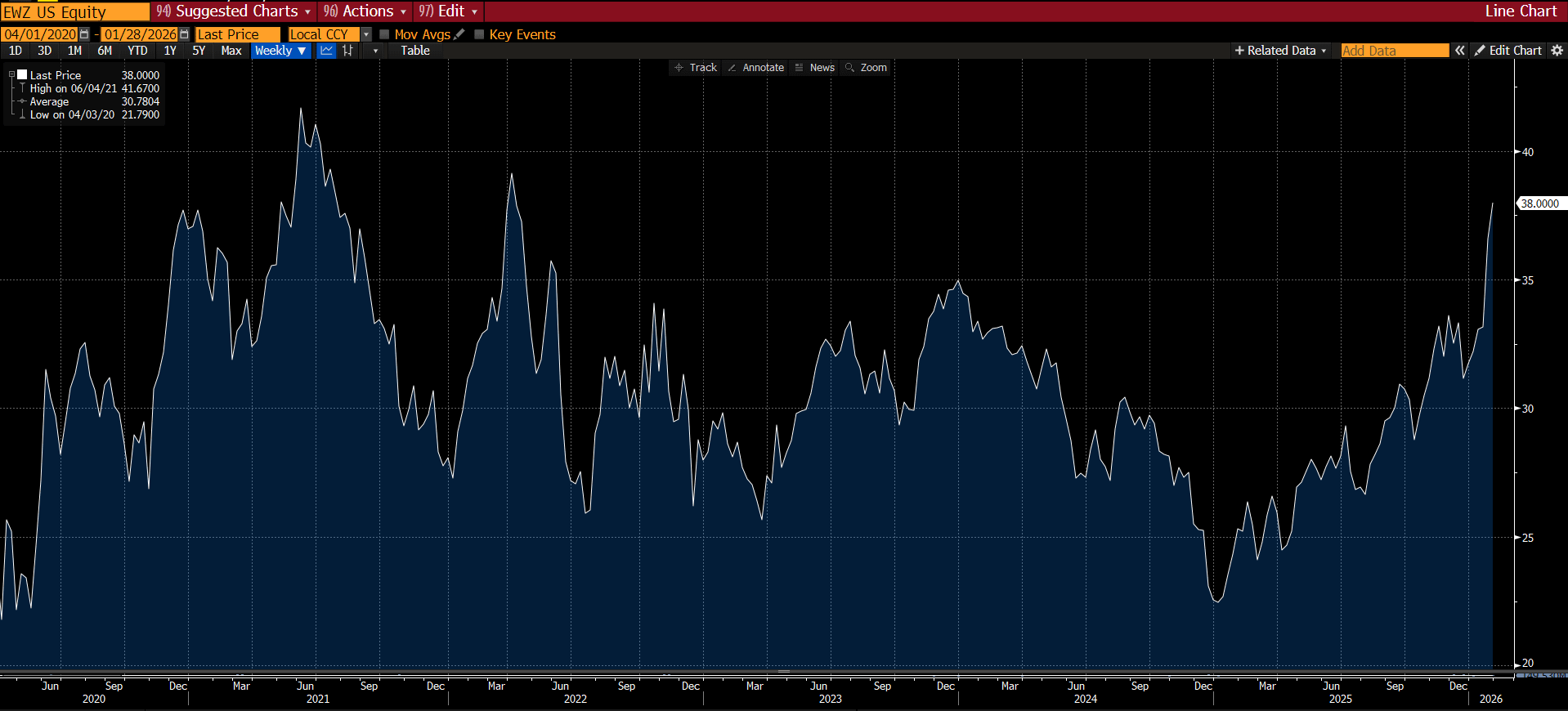

As shown below, Brazilian equities, as captured by the EWZ ETF, have performed exceptionally well since December 2024, with momentum accelerating since December 2025. Valuations are less compelling than they were, but we believe the move is already underway and the margin of safety at current levels is thinner than before. They are ready to run.

MSCI Brazil ETF (EWZ) Share Price Performance

We believe Brazil currently stands out as the most attractive market in the region, supported by the depth and maturity of its capital markets. While Argentina offers a wider risk-reward profile, we view Brazil as the superior allocation given the greater visibility into its future trajectory.

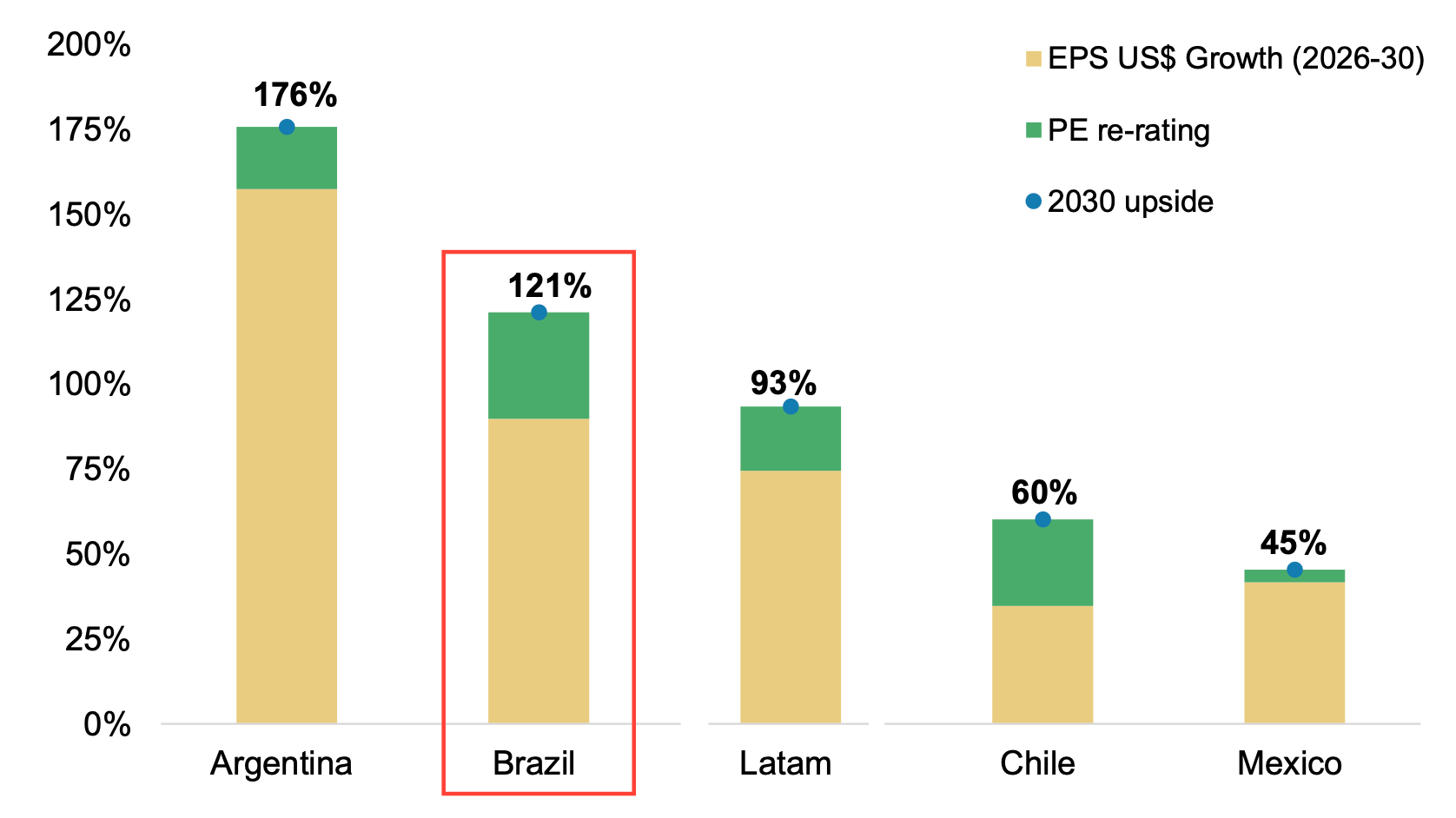

This preference is backed by significant upside potential. According to Morgan Stanley's analysis of regional equity gains, Brazil offers a 121% total upside through 2030. This growth is largely driven by EPS expansion, which accounts for ~80% of projected gains, while multiple re-rating contributes the remaining 20%. While Argentina demonstrates a higher absolute potential of 176%, we believe the inherent stability of the Brazilian market makes it the preferred play for consistent alpha.

MSCI Latin America: 2030 Spring Scenario Index Upside

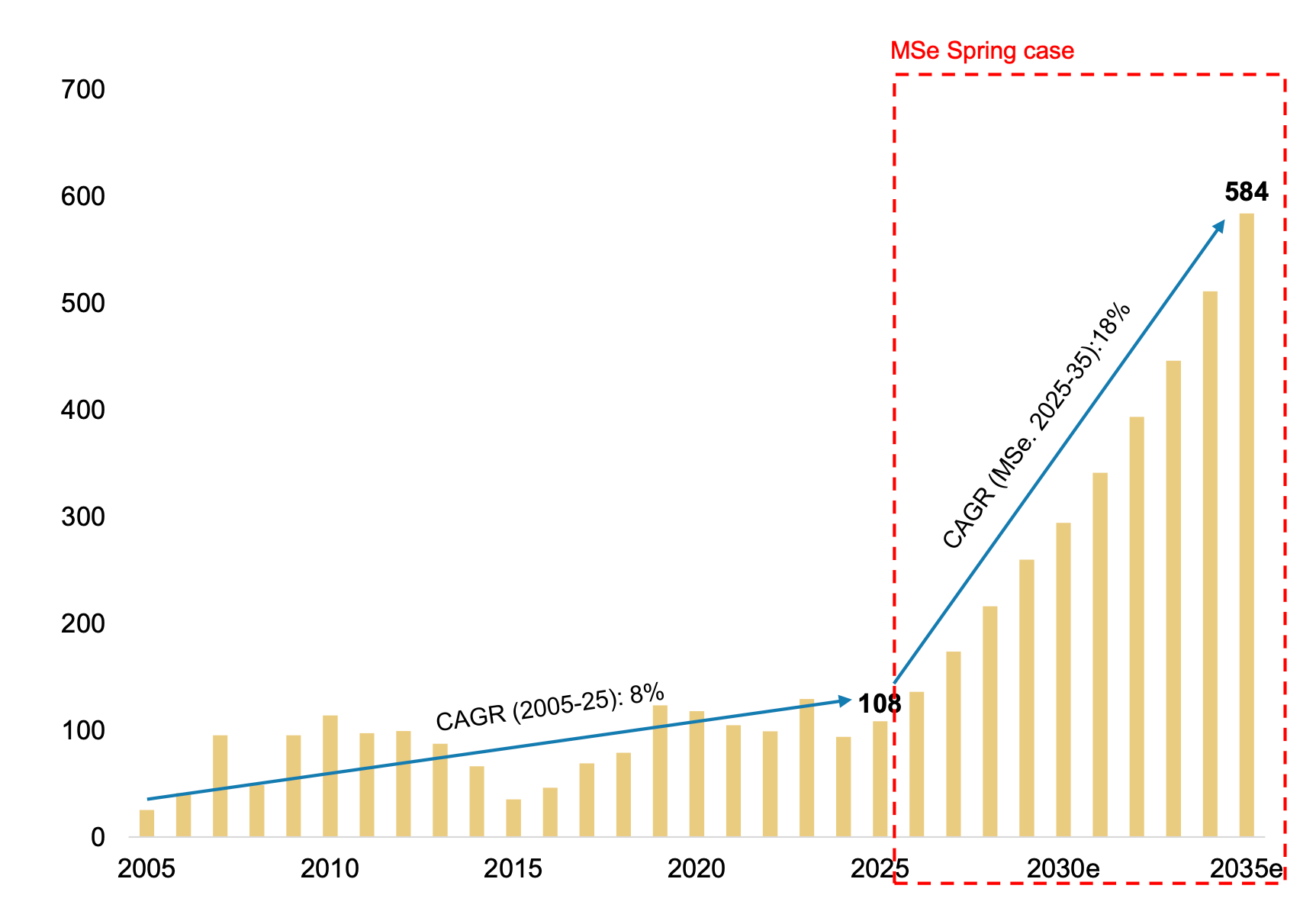

In a bullish spring case scenario, domestic Brazilian equity funds are projected to increase their AUM by ~6x by 2035. This represents a move from $100B to ~$584B, reflecting an 18% CAGR over the next decade. The surge in domestic participation would significantly deepen the market, far exceeding the 8% CAGR observed between 2005 and 2025.

Brazil Equity Funds: Spring Case AUM (US$ bn)

However, the macro thesis is not without challenges. Significant fiscal consolidation is required. We estimate that fiscal cuts equivalent to 3.4% points of GDP are necessary to stabilize the debt-to-GDP ratio. We believe investors should be aware that reversing these dynamics will likely be a prolonged process extending beyond a five-year horizon.

In contrast, the investment debate in Mexico is distinct. The focus there is not on fiscal repair but on institutional frameworks and the progression toward USMCA 2.0. Mexico is uniquely positioned to benefit from North American integration and the strategic decoupling from China, which serve as powerful catalysts for both brownfield and greenfield investment.

Mexico will be the subject of a future article. We look forward to sharing that analysis with you soon. Make sure to follow us!

Energy: Strategic Scenarios & Operational Realities

External analysis from the ITAU energy team explores a “What-If” scenario for the Brazilian upstream sector, specifically looking at how political shifts could catalyze capital reallocation. In this narrative, Petrobras would adopt a leaner, returns-driven approach by accelerating the divestment of mature onshore and offshore fields. We believe that a potential shift in the political landscape could serve as a catalyst for significant capital reallocation and a strategic refocus within the Brazilian energy sector.

This shift would create a significant opening for independent operators to step into the Campos Basin and other onshore opportunities. The ITAU framework suggests that prioritizing the Equatorial Margin frontier could involve ~$25B in incremental capital expenditure over the next decade.

We believe that such a transition would allow for the prioritization of high return assets while maintaining a leaner operational structure. This would support a high intensity exploration program, including the development of eight new FPSOs. According to this analysis, a more disciplined approach to non-core spending could lead to an incremental EBITDA of ~$25B over that window, allowing the asset base to compound beyond the next decade.

Operational Trends

Recent data shows a strong recovery in production. Following temporary FPSO shutdowns in late 2025, Petrobras production returned to 2.5M barrels per day in December. Average production for the year stands at 2.4 mbpd, which is 0.1 mbpd ahead of the targets set in the current strategic plan.

Capacity Gains: Petrobras has successfully increased capacity across six platforms, unlocking 115K barrels per day (kbpd) of additional capacity.

December Results: Of that new capacity, 77 kbpd was already reflected in the December production numbers.

Independent Producers: Mixed results. PRIO (the largest independent Brazilian operator) ended a five-month decline at the Frade Field (a 100% owned deepwater asset in the Campos Basin) in December. However, production at specific wells is still down significantly compared to last year, highlighting the volatility that comes with managing mature assets.

Production Outlook

The following operational data confirms a robust recovery in output, reinforcing our bullish view on Brazil’s oil sector and on PBR as the clear leader of that growth in the period ahead.

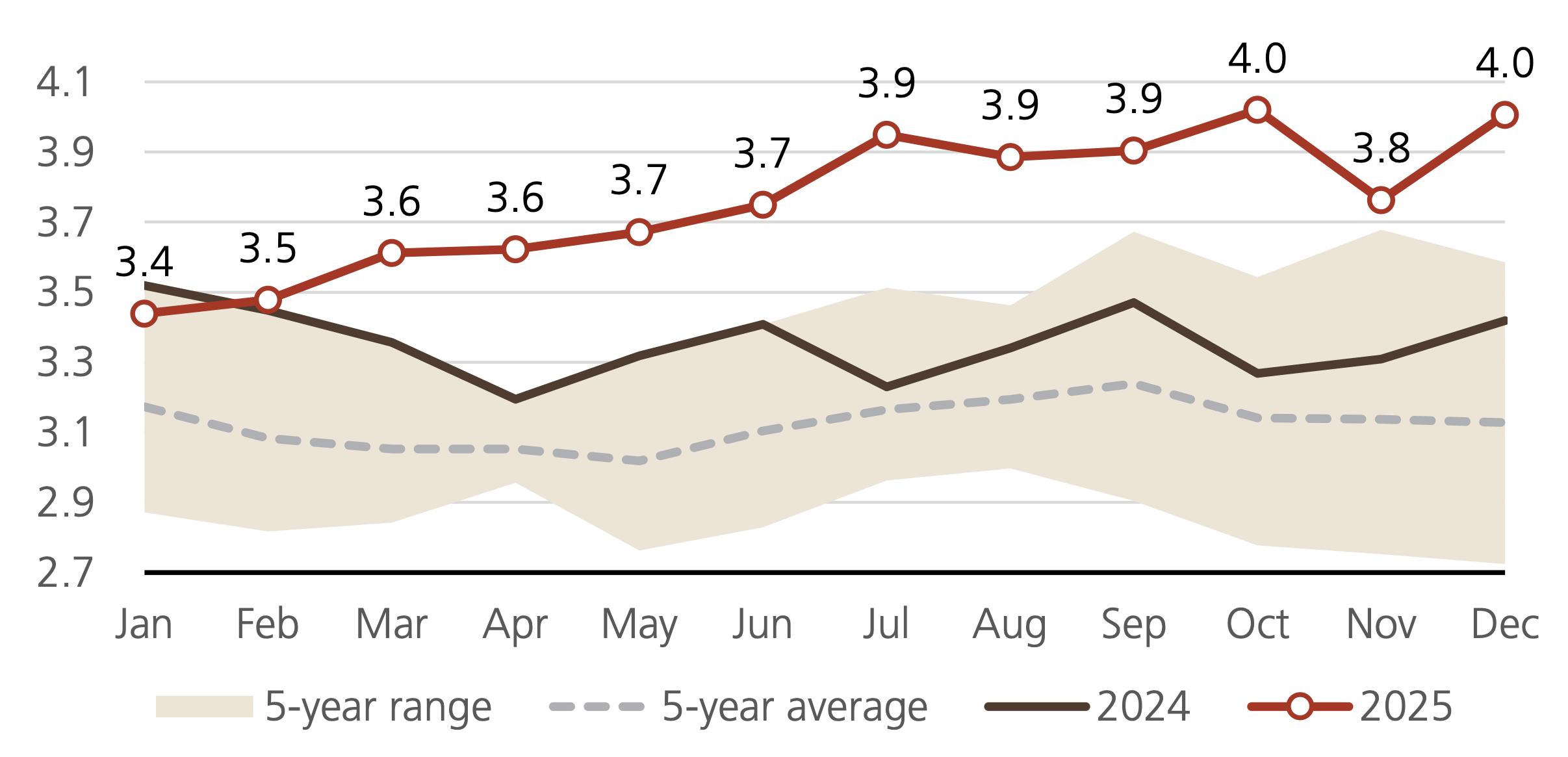

As shown in the chart below, PBR demonstrated significant resilience in the final quarter of 2025. After a temporary dip to 2.37 Mbd in November, production rebounded to 2.54 Mbd in December. This recovery allowed the company to meet its 2.40 Mbd annual target, and the 2.60 Mbd estimate for 2026 points to an ongoing acceleration in the growth phase.

Petrobras Oil Production vs UBS Estimates (Mbd)

The national picture, seen in this chart below, provides even greater confidence in the “local story”. Throughout 2025, total Brazilian output consistently stayed above the 5 year average and historical ranges. The jump to 4.0 Mbd in December confirms that Brazil is successfully moving into a new production tier, driven by the sustained performance of pre salt assets.

Brazil Oil Production vs Historical Ranges (Mbd)

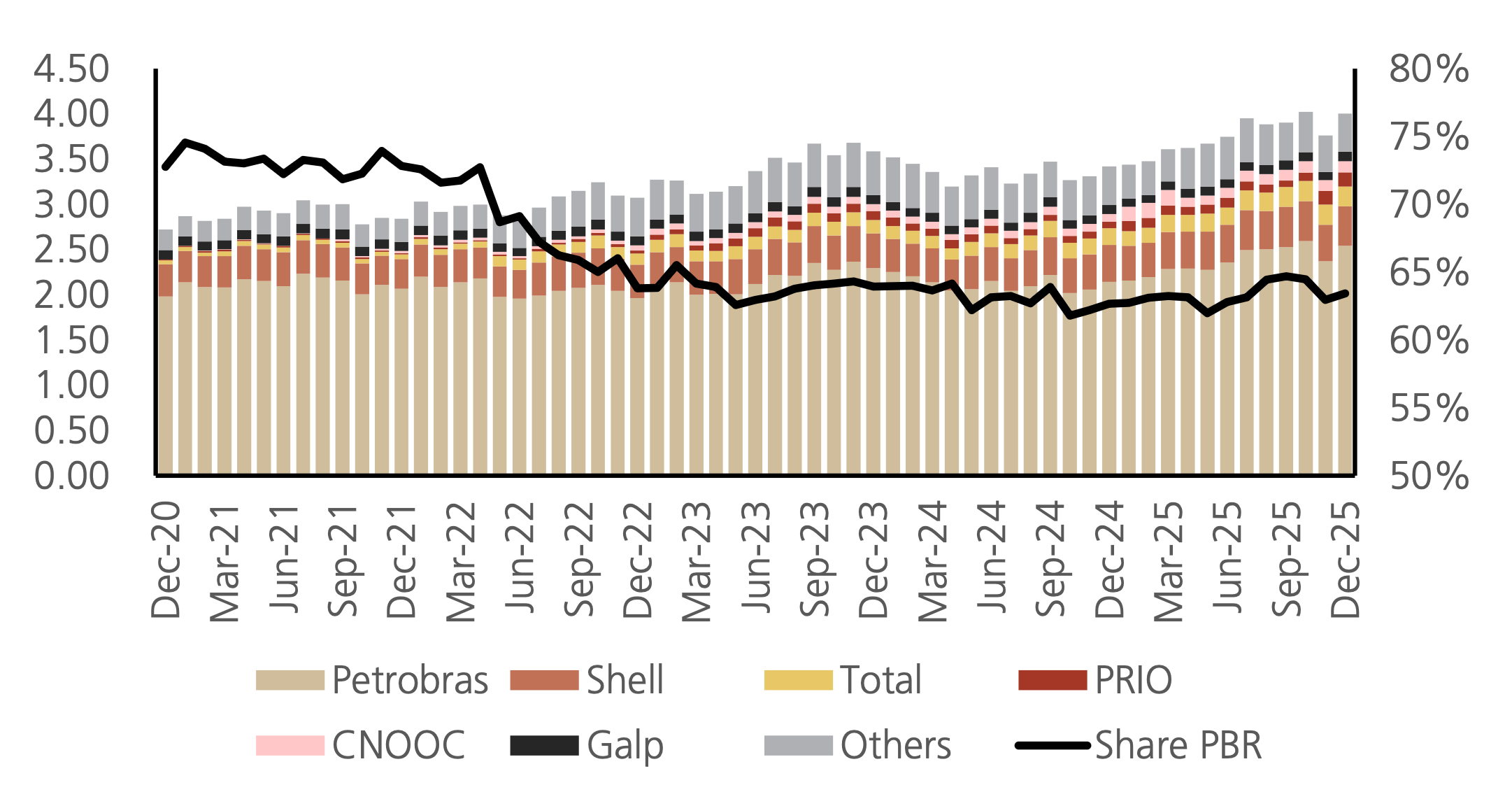

This chart illustrates why PBR remains the primary vehicle for this growth. With a 65% market share, it is the key driver for the entire basin.

While international majors and independents add to the base, the black line tracking Petrobras’ share highlights its central role in capturing Brazil’s resource upside, which makes us believe the stock remains the cleanest way to express our bullish view on Brazilian oil growth.

Per Player Brazil Oil Production (Mbd)

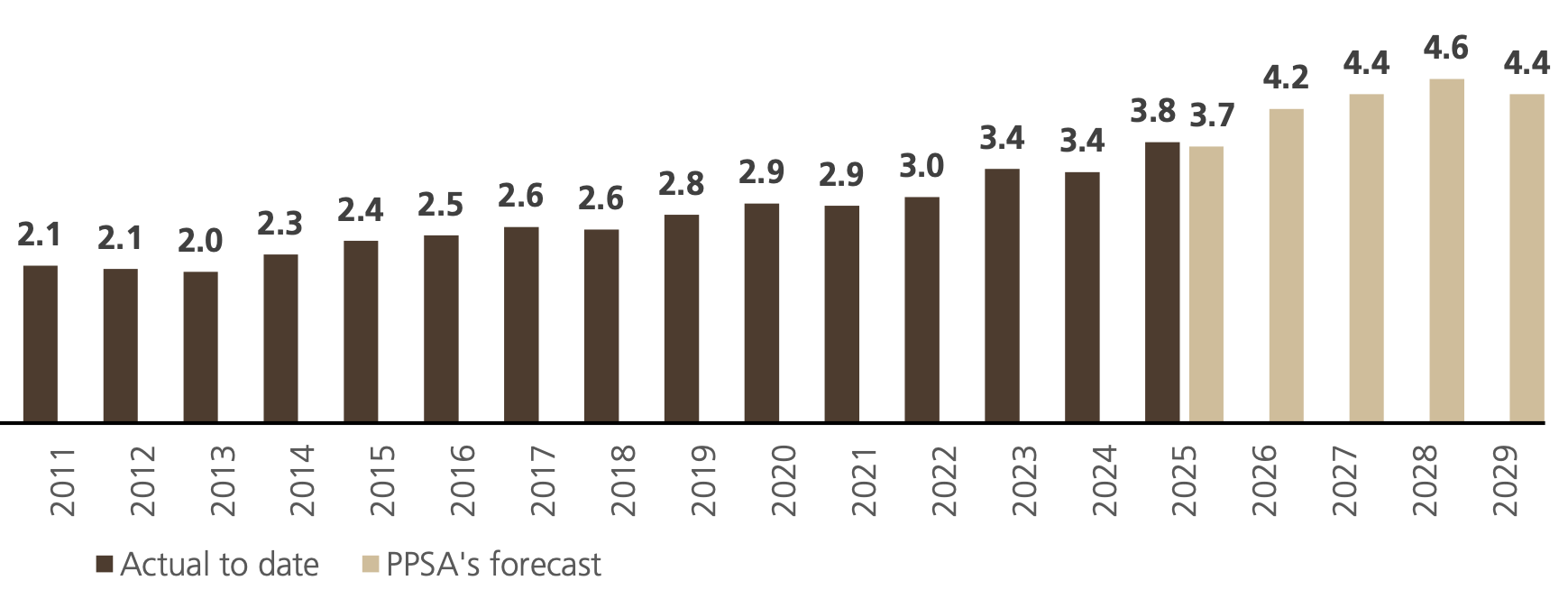

Finally, as shown in the chart, current momentum appears to be part of a multi year expansion. Production is forecast to rise from 3.7 Mbd in 2025 to a peak of 4.6 Mbd by 2028. We believe this extended growth window improves long term visibility and supports sustained capital allocation, suggesting Brazil’s production peak remains several years away.

Brazilian Annual Oil Production vs PPSA’s Forecast (Mbd)

Valuation Method

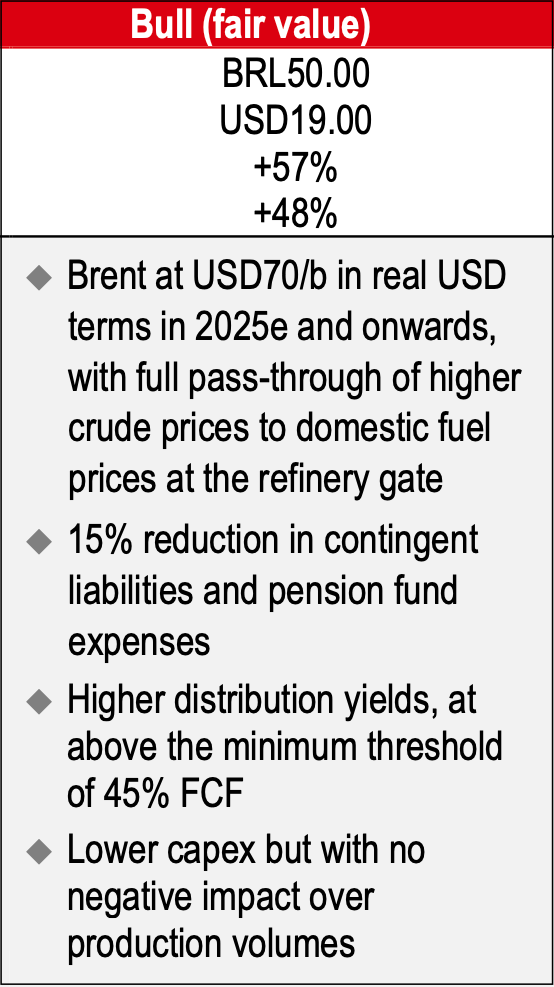

Since Petrobras is not being added to the Aurelion Index, we are not building a full model for a proprietary target. Instead, we frame valuation through external price targets and scenario work. We focus on 2 reference points: (1) HSBC’s bull case, which we view as a reasonable upside framework, and (2) Jefferies’ bull case, which represents a best case outcome.

Scenario 1: HSBC Bull Case

HSBC’s scenario implies a $19.00 price target for the ADR, or ~23% upside from today’s $15.40. The assumptions include Brent at ~$70 per barrel in real USD terms from 2025E onward, full pass through of higher crude prices into domestic refinery gate pricing, a 15% reduction in contingent liabilities and pension costs, higher cash distributions supported by the 45% FCF floor, and lower capex without sacrificing production volumes.

Scenario 2: Jefferies Bull Case

Jefferies’ bull case reflects a higher conviction operating setup. The scenario assumes production growth accelerates to more than 4% CAGR through 2030, domestic fuel pricing remains aligned with import parity, and long term Brent settles near $80 per barrel, which we believe remains plausible given the supply discipline required to sustain global offshore investment.

It also assumes Petrobras continues to fund gradual investment in low carbon initiatives and refining while preserving healthy free cash flow, with group capex held in the $15B to $20B per year range through 2030.

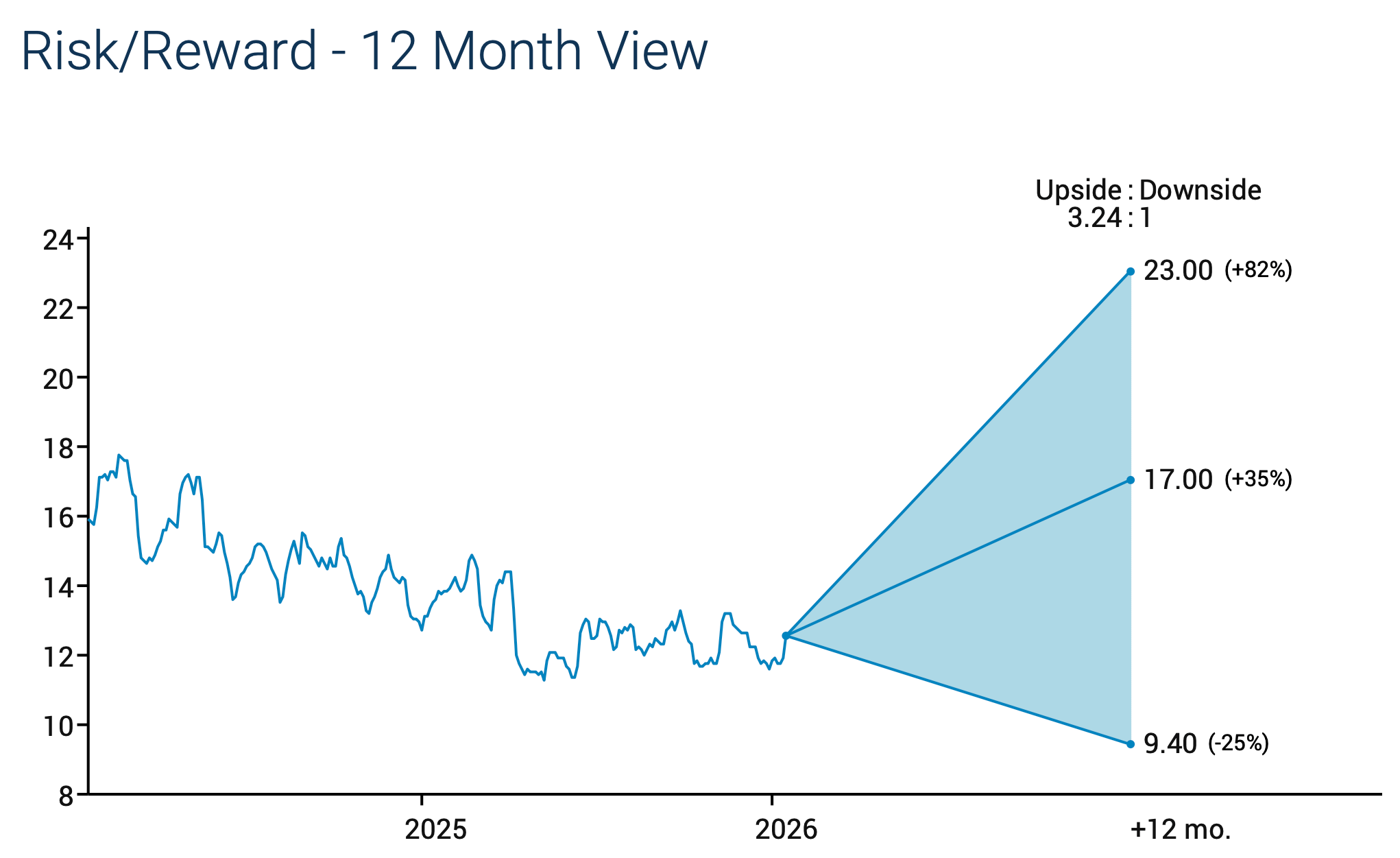

Now, translating this into a 12 month risk reward from today’s $15.40 price, the framework implies upside cases of ~$17.00 (+10%) and ~$23.00 (+49%), versus a downside case of ~$9.40 (-39%), which leaves the risk reward clearly favorable, as shown below.

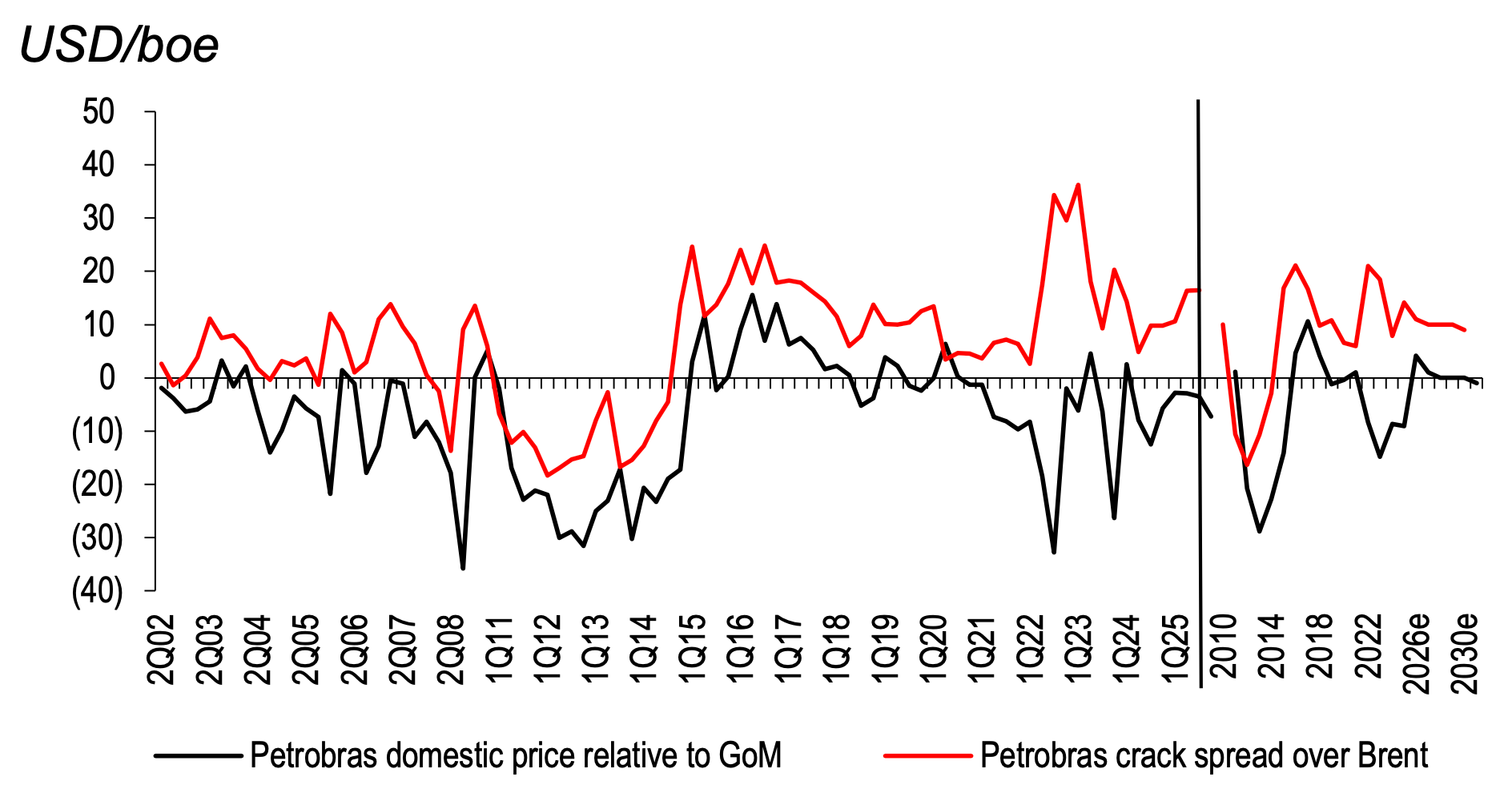

PBR Domestic Pricing vs. International Benchmarks

We believe that the pricing strategy of Petrobras is a critical factor in its financial performance, and the chart below helps to illustrate our thinking.

The key takeaway is that even when domestic pricing has been below international benchmarks at times, Petrobras has still generated a positive margin over Brent, which helps protect cash flow. That said, the black line also reminds you of the risk: domestic pricing policy can compress margins if discounts widen or persist. Petrobras has sold fuels mostly at lower than GoM prices but with positive margin over Brent.

The red line in the chart above shows that Petrobras has consistently maintained a positive crack spread over Brent, even during periods when its domestic prices (black line) were lower than the Gulf of Mexico (GoM) benchmark. This demonstrates the company’s ability to generate positive margins despite potential pricing pressures in the domestic market.

Petrobras Domestic Fuel Pricing & Margins

Key Risks

1. Primary downside risk is weaker commodity pricing. We believe a lower Brent environment, or weaker realized prices for refined products, would pressure cash flow and reduce distribution capacity.

2. A second risk is policy. Petrobras operates within a politically sensitive framework, and changes in Brazil’s regulatory stance, tax regime, or domestic fuel pricing policy could weigh on earnings and investor confidence.

3. Execution also matters. Slower production growth, operational disruptions, or cost inflation would weaken the volume and margin profile embedded in the bull cases.

4. Capital allocation remains a swing factor. We also believe higher capex, increased investment in lower return projects, or a shift in payout priorities could reduce free cash flow and weaken the equity case even if upstream fundamentals remain supportive.

Our Final Take

Brazil’s setup remains compelling. Production is still rising, hard currency revenue offers protection, and Petrobras remains the clear vehicle for the country’s multi year growth. The market has also started to reward that reality, with Brazil equities and PBR re rating sharply since late 2024.

Our view on Petrobras stays positive, but the risk/reward is not attractive enough. The stock has moved too far, too fast, and the margin of safety is thinner at current levels. We prefer to wait for a better entry point before adding it to the Aurelion Index. If a pullback develops, we would reassess quickly. For existing holders sitting on gains, we would continue to hold.

Disclosures & Methodology

Thank you for the excellent write-up. I´m also on the wait for the pullback camp.

$20 would be “too late”