In Conversation: Cerebras Systems (CBRS)

Management on the OpenAI deal, Nvidia, and the inference race

The premise behind our work at Aurelion is that themes and market sentiment shape returns as much as fundamentals do. This is why, even if it is not a holding of ours, we frequently meet with management teams to better understand where the market is going. Sometimes the company is so attractive that it becomes a holding. We only share conversations that we believe add value.

In this case, this was one of the most interesting discussions we have had in a while, with this $50B semiconductor behemoth. Cerebras, a Silicon Valley-based AI computing company, IPO'd in May and is at the forefront of the industry.

In early July, we discussed with Sean J. Dorsey, Head of Investor Relations and Senior Director of Strategic Finance at Cerebras. Sean has been at Cerebras for five years and works directly with the CFO. Before joining Cerebras, he was a VP in equity research and investment banking, covering semiconductors at major banks. An ex-Wall Street guy, as he described himself.

Off topic from Cerebras; he gave us his thoughts on independent research and how much emphasis they put on leading Substacks. It’s simple, Substack is becoming the place to be for independent investment research:

Sean: “Major companies’ IR teams and management are increasingly approaching independent research platforms like Substack and X in a similar way to how they approach traditional sell-side analysts.

The reason is simple: independent research has become increasingly important, with the ability to influence investor perception and market sentiment. Management teams are listening and reading the research that is published on Substack.” (adapted and interpreted for context).

He brought up Dylan Patel (SemiAnalysis) and Irrational Analysis (publications we highly respect) as examples of why they want to engage more with leading Substacks because, he said, some forecasts were very different from what the company expected.

We begin with the company’s story, dive into our conversation with management, explore what it means for the broader AI infrastructure race, break down the bull and bear cases, and finish with our view on valuation.

We usually aim to give an actionable investment idea on a theme or a market. This is not the case for this report, but you’ll get some interesting insights on the AI trade, Cerebras, and independent research.

Methodology: we independently reaches out to company management teams. Aurelion Research does not receive compensation from any company covered. The answers from interviews are based on our notes and have been adapted and presented for clarity. They may not reflect the speakers’ exact words. We have selected the sections below that we believe are the most relevant parts of our discussion. All information discussed is believed to be publicly available. This content is for informational purposes only and is not investment advice or a recommendation to buy or sell any security.

Table of Contents

Company Intro: A Different Approach to AI Computing

In Conversation with Sean Dorsey

Implications for the AI Trade

The Debate: The Promise and the Challenges of Cerebras

4.1 The Bull Case: A New Path for AI Computing

4.2 The Bear Case: The Challenges Behind the Ambition

Valuation: An Analyst’s Nightmare

Our Final Thoughts on Cerebras

1. A Different Approach to AI Computing

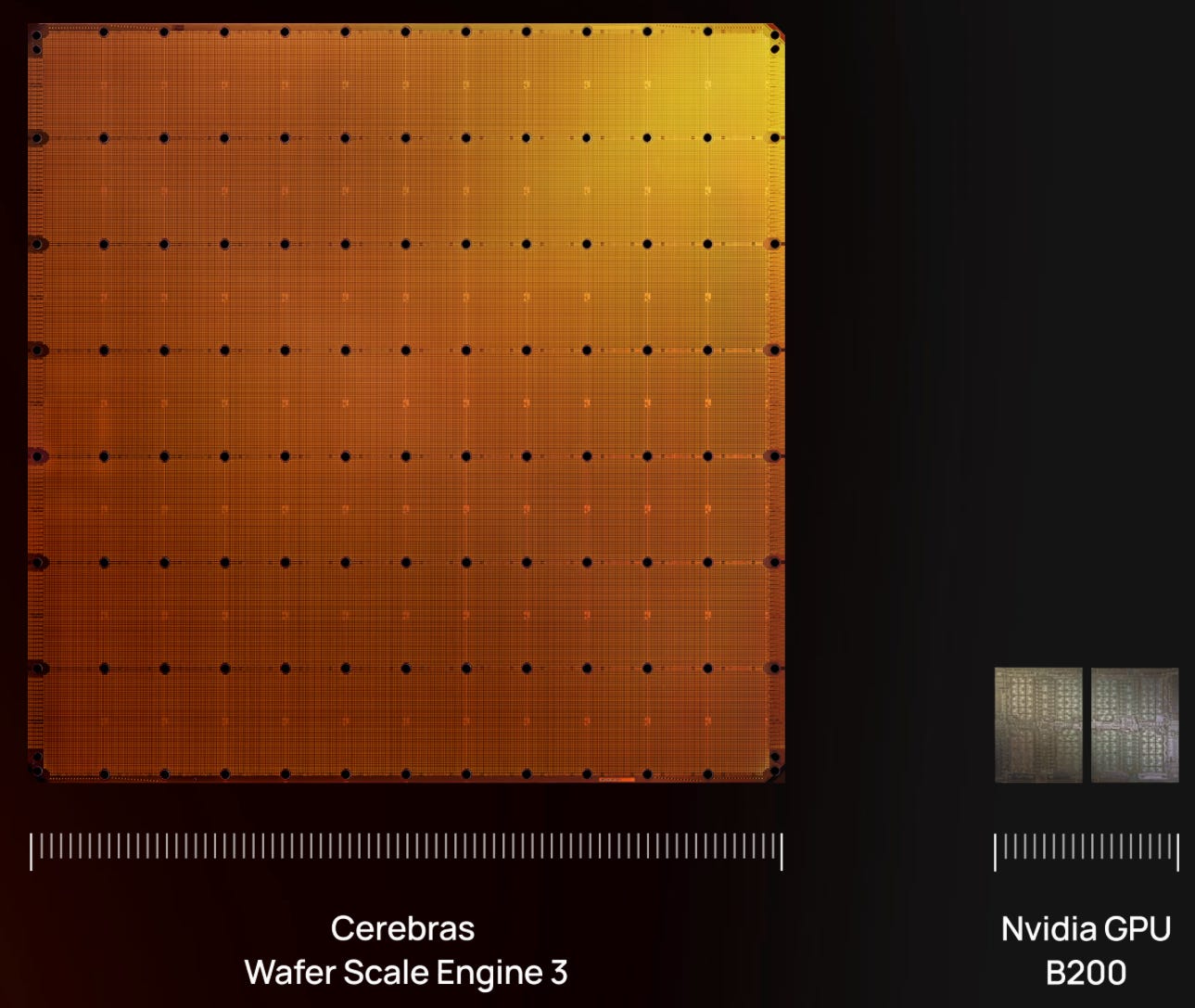

Cerebras is a semiconductor company that builds chips designed for AI processing. It went public in May 2026 and trades under the ticker CBRS.

Its main product is the Wafer-Scale Engine 3 (WSE-3), a massive AI chip built as one large piece instead of many smaller chips working together.

Traditional AI systems use many separate chips that need to constantly share information, which can slow things down. Cerebras takes a different approach by putting everything together in one place, allowing information to move faster and helping customers run large AI models more efficiently. The WSE-3 is designed to handle AI workloads that would normally require many traditional chips.

How Cerebras Is Riding the AI Compute Wave

The Silicon Valley company has two main revenue streams:

1. Direct Hardware Sales (57%)

The company sells its AI chips and computing systems directly to customers looking to build and operate their own AI infrastructure for large-scale workloads.

2. Cloud & Services (43%)

Cerebras Systems operates its own global network of AI data centers.

It offers cloud services, allowing customers to access its computing power without owning the hardware. Customers can either reserve dedicated computing capacity or pay based on the amount of computing power they use.

An important point to mention: just one year ago, the revenue mix was quite different. Around 70% of revenues came from hardware sales, while 30% came from its cloud offering. So, what happened?

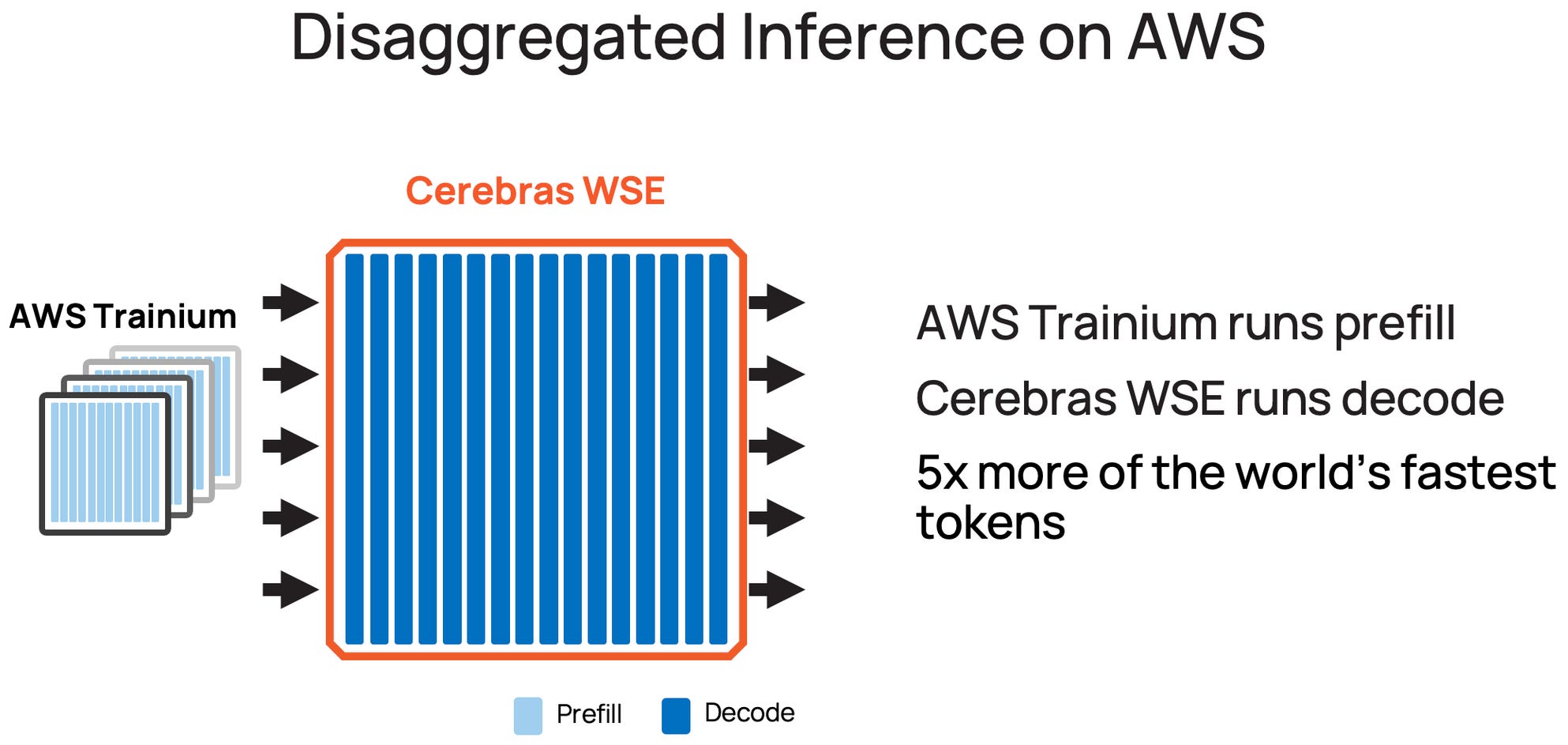

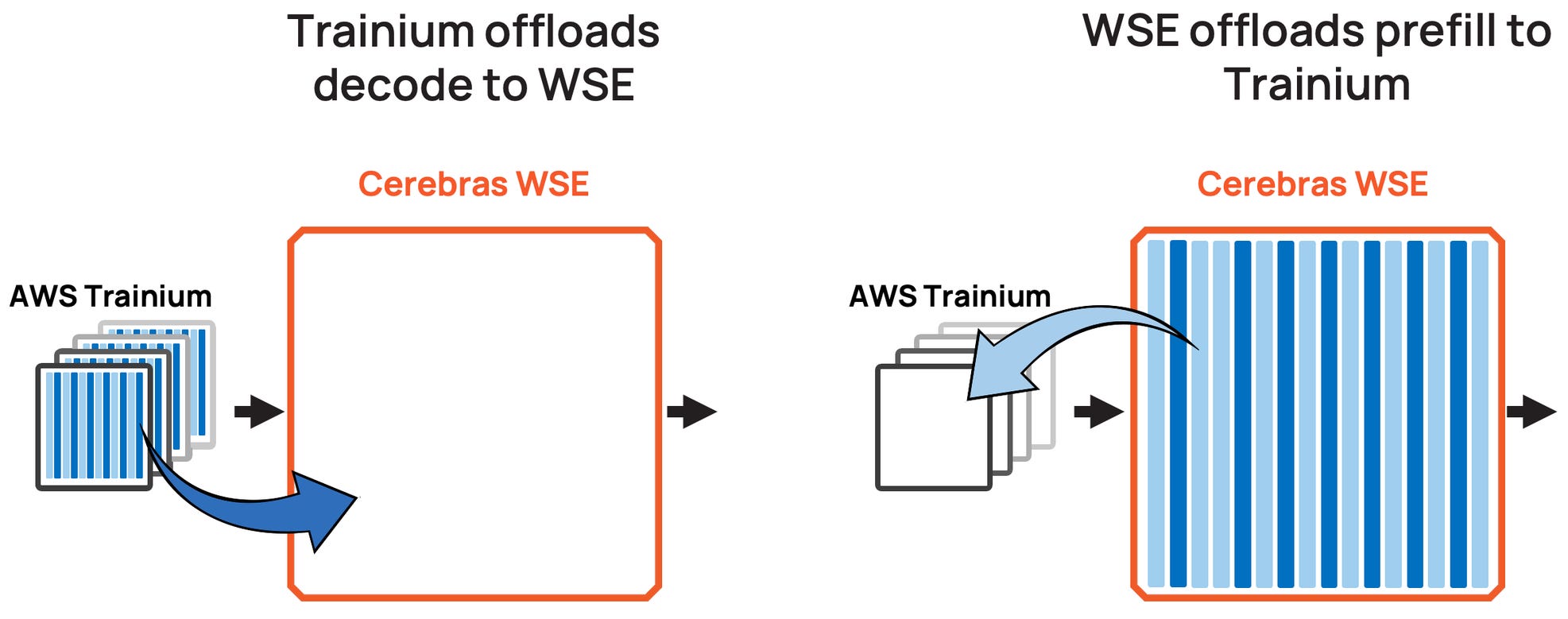

The change came from rapid growth in its cloud business, accelerated by a massive multi-year inference deal with OpenAI that began ramping in early 2026, combined with an Amazon cloud partnership. Instead of only selling the infrastructure, it is increasingly monetizing access to that infrastructure.

Customers can now use Cerebras’ computing power through the cloud without needing to purchase, install, and manage expensive AI hardware themselves. This should create a more recurring, service-based revenue stream while allowing Cerebras to benefit directly from the growing demand for AI compute.

The timing is also important because the AI industry is entering a new phase. Early AI spending was largely focused on training increasingly larger models, but we are now moving into an entirely new wave that is expected to be driven by inference as these models transition into real-world applications.

Here’s an interesting quote from AWS VP Compute & ML Services, David Brown.

“Inference is where AI delivers real value to customers, but speed remains a critical bottleneck for demanding workloads like real-time coding assistance and interactive applications. What we’re building with Cerebras solves that by splitting the inference workload across Trainium and CS-3, connected through Amazon’s Elastic Fabric Adapter. The result will be inference that is an order of magnitude faster and higher performance than what’s available today.”

Amazon and Cerebras are combining two different AI chips, with each one doing the job it is best at. By working together, they can generate AI responses much faster than traditional systems, making applications like coding assistants more responsive for users. This creates a win-win situation for both companies.

2. In Conversation with Sean Dorsey

Aurelion Research (AR): ‘‘Could you walk us through your role at Cerebras, your background, and how you got to where you are today?’’

Sean Dorsey

“I’ve been at Cerebras for five years, so I was here well before the company became public. I work closely with the CFO on financial matters and have also taken on investor relations responsibilities, which gives me a unique perspective on both the business and how investors view the company.”

Thoughts

Before joining Cerebras, Sean spent time on Wall Street, working in Equity Research and Investment Banking and covering the semiconductor industry at several major banks. In other words, he went from analyzing chip companies from the outside to helping build one from the inside, giving him a unique perspective on the industry.

AR: ‘‘How does Cerebras think about its customer strategy, and what drives customers to adopt its technology and build long-term partnerships?’’

Sean Dorsey

‘‘Our customers today are massive companies, like Amazon and OpenAI. These are not your typical customers. They are so large that, in some ways, you could almost think of them as resellers or distributors because of the scale at which they operate. We have a small number of very large customers, and that makes our go-to-market strategy quite unique. We do not need a massive sales force because we are focused on a handful of strategic accounts.

The advantage is that we know these customers extremely well, understand their needs, and can work closely with them. Because of that, we can operate with a relatively lean sales and marketing organization and allocate more resources toward engineering and product development.

We believe this is a competitive advantage for Cerebras. We also believe we have built a strong market engine. Even though we are a much smaller company, we have managed to position ourselves in the same conversations as some of the largest AI infrastructure companies in the world, including Nvidia.”

Thoughts

Cerebras’ customer strategy is interesting because the company is prioritizing depth over volume. Instead of trying to sell to thousands of customers, it is focusing on a small number of very large ones. This allows the company to stay lean and focus more resources on improving its products. The key question will be whether this strategy can continue to work as Cerebras grows.

AR: “There has been discussion around whether Cerebras’ approach to handling memory could face limitations as AI models continue to grow. How does the company think about this potential challenge, and how would it adapt if the industry shifts toward using more external memory solutions?”

Sean Dorsey

“I think some of the discussion around our architecture comes from people looking at Cerebras from the outside without having spent significant time using our compute or understanding all the nuances of the technology. They are doing their best to understand the product and the value proposition, but there are limits when you are not directly working with the system.

A recent example is the assumption that Cerebras would not be able to support very large models. We were a day-zero launch partner with OpenAI for its latest multi-trillion-parameter model, delivering it at up to 750 tokens per second, which is significantly faster than GPU-based alternatives. So clearly, there are still some misconceptions around what our architecture can and cannot do.

Building a wafer-scale chip was something that many people believed was not possible for decades. We proved that it was technically viable, and now we are proving that it can also be commercially viable. We have real customers making significant commitments to our technology, and our focus is to continue proving the doubters wrong over time.”

AR: ‘‘How does Cerebras think about attracting and retaining top talent, especially when competing against much larger semiconductor companies?’’

Sean Dorsey

“I think we’ve had a lot of success hiring people because we’re still the small guy that’s growing quickly, with a lot of momentum and opportunity ahead of us. Generally speaking, that is a very attractive position to be in compared to a much larger company that is trying to innovate in new markets.

We’re able to attract talent from some of the biggest technology companies in the world. We have people here from AWS, Meta, Apple, Google, Nvidia, and AMD. There are obviously many benefits to being a large company, but talent retention can also be a challenge when you’re operating at that scale.

I think the current environment has also created opportunities for us. While AI and semiconductor companies continue to invest and grow, other areas of technology have seen more pressure, which has created a strong talent pool for companies like Cerebras. Today, we have roughly doubled our headcount over the past 18 months and are approaching 1,000 full-time employees.

What’s also interesting is the composition of the team: around 80% of our employees are engineers, and 80% of those engineers are software engineers.

So despite competing against much larger companies, we’ve been able to attract strong technical talent because people want the opportunity to have a bigger impact, take on more responsibility, and help build something at an earlier stage.”

Thoughts

Talent is often overlooked when analyzing semiconductor companies, but we believe it can be a major competitive advantage. In AI infrastructure, where technology evolves quickly, the ability to innovate and execute depends heavily on the strength of the team behind the technology.

Cerebras remains much smaller than industry giants, but its ability to attract experienced engineers from leading technology companies shows that it has created an environment where people see an opportunity to make an impact. The key question is whether this advantage can continue as the company grows.

Then came the most interesting part: the new wave of research.

We mentioned this earlier in the article’s introduction. We learned that management teams at large companies like Cerebras are increasingly paying attention to research published on Substack and by influential accounts on X.

Why? Because they agree that research produced outside of the traditional sell-side ecosystem has become increasingly important, which is something we rarely hear from companies. This means that the work being done on these platforms is being read by major companies and market participants.

AR: ‘‘Do you think independent research platforms like Substack and X have become increasingly influential in shaping market sentiment?’’

Sean Dorsey

“I think it’s something that we’re all trying to rethink in terms of where we allocate time. We should probably be spending more time with the Substack community because whether or not we like it, whether they’re right or wrong, they have the ability to influence the market. We’ve spent so much time with some of the largest institutional investors in the world because they have the ability to move stocks as well. But so do people on X.

They have a microphone, and we should probably think about them in the same way that we think about top institutional investors like BlackRock.

They really understand our technology and our story, but just because some researchers don’t fully understand it today, that doesn’t mean we shouldn’t engage. We need to continue having thoughtful conversations, educating the market, and creating opportunities to explain why they may have missed something. Having that healthy debate in the market is usually a very good thing.”

AR: ‘‘How does Cerebras approach working with independent researchers when there are disagreements about the company or its technology?’’

Sean Dorsey

“It’s a fine line. You don’t want to insert your words on top of theirs or take ownership of their work. But if we can educate them on certain aspects, we want to do that. When SemiAnalysis was preparing its report ahead of our IPO, they sent us a 50-page document and gave us an opportunity to provide feedback.

We left a lot of comments around areas where we thought things were not quite right, lacked context, or were simply incorrect. The challenge is figuring out the right way to engage. If a Morgan Stanley analyst sent us a report, we wouldn’t edit their report. We would try to help improve their understanding of the business and technology.

That’s the same approach we want to take with Substack authors and writers on X. We can’t give preferential treatment just because someone is on Twitter. The same standards should apply to everyone.”

Thoughts

We found this particularly interesting given SemiAnalysis’ strong reputation within the semiconductor industry. Cerebras is also a well-known company in AI infrastructure, making this debate more about differing views on the technology rather than a lack of information. Hearing this perspective directly from someone who has been with CBRS for years provided valuable context and helped us better understand the other side of the discussion, the one we do not usually hear about.

AR: ‘‘What are some of the biggest misconceptions investors still have about Cerebras?’’

Sean Dorsey

“For 10 years, people have questioned whether what we were trying to do technically was possible. People said you wouldn’t be able to build the chip, you wouldn’t be able to cool it, power it, run large models on it, or scale the architecture. None of that is new. We will never convince every doubter, but we will continue to prove them wrong over time.

We have a fundamentally different architecture, and you can’t apply the same assumptions used for traditional chip design to what we are doing. I think we can do a better job educating people about that as we continue to grow.”

AR: ‘‘When well-known researchers misunderstand Cerebras’ technology, how do you think about addressing those misconceptions?’’

Sean Dorsey

“I think everyone’s got a point of view based on their own experience and how they’ve arrived at it. Dylan recently told us that his mental model of Cerebras and our architecture was wrong after speaking with our CTO and our CEO.

I’m a glass-half-full kind of guy, so I see that as an opportunity. If we can continue educating researchers like SemiAnalysis and other independent writers with large audiences, it’s an opportunity not only to improve public understanding of our architecture, but ultimately how the market values the company.”

Of course, we want to make clear that Dylan has been right far more times than wrong and is an exceptional voice for semiconductor analysis.

3. Implications for the AI Trade

Here are simple implications and inferences from the conversation.

1) Inference Is the New Race

For readers new to the AI market, it helps to understand the two phases of AI computing. Training is the process of building an AI model. A company feeds enormous amounts of data through thousands of chips over weeks or months, and the model learns from it. It is a one-time, upfront cost, similar to building a factory.

Inference is what happens after: every time you ask ChatGPT a question, generate an image, or use an AI coding assistant, the finished model is running a calculation to produce your answer. That is inference. It happens billions of times a day, and every single request consumes computing power.

The first wave of AI spending went into training ever-larger models. But a model only creates value when people actually use it, and usage is exploding.

Inference is expected to represent roughly two-thirds of all AI compute in 2026, up from one third in 2023. Unlike training, inference is a recurring cost that grows with adoption, which is exactly why speed and cost per request have become the new battleground. This is the wave Cerebras is positioned to ride: its chips are built to run models faster than traditional GPUs, and its deals with OpenAI and Amazon are inference deals, not training deals.

2) Nvidia’s Monopoly Is Starting to Weaken

For years, buying AI chips meant buying Nvidia. There was no real alternative, and that scarcity let Nvidia charge premium prices and earn exceptional margins.

That is starting to change. Amazon, one of the largest chip buyers in the world, now runs AI workloads on a combination of its own in-house chip (Trainium) and Cerebras hardware, using each one for what it does best. When the biggest customers start mixing and matching suppliers instead of depending on a single vendor, that tells you something.

Nvidia still dominates the market and its software ecosystem remains a huge advantage. But the “there is no alternative” premium that supported its valuation gets harder to justify when credible alternatives exist.

The winners from this shift are the challengers: specialized chipmakers like Cerebras and Groq, and the custom chips that Amazon, Google, and OpenAI are designing themselves. The AI chip market is moving from a monopoly toward an oligopoly, and that creates opportunities further down the food chain.

There was simply no way one company could make AI chips for the entire planet.

3) Customer Concentration Is a Feature of the AI Trade and a Systemic Risk

Sean described customers so large they’re “almost resellers or distributors.” The entire AI supply chain now hangs on a handful of buyers (OpenAI, Amazon, Meta, Google). If one slows spending, the shock propagates through every supplier simultaneously. Correlation across AI names is so high, probably higher than the headline suggests.

4) The Talent Migration Is Immense

Cerebras doubled headcount in 18 months, pulling engineers from AWS, Meta, Nvidia, and AMD, while “other areas of technology have seen more pressure.” Human capital is concentrating in AI infrastructure the way it concentrated in internet infrastructure in 1999. That’s bullish for near-term execution.

Yes, this is a classic late-cycle signal worth monitoring when comparing it to the dot-com bubble. However, at that time, cash flows were basically zero.

Now, the large companies in the AI trade, like Nvidia and the hyperscalers, are printing cash. If technology improves and more cash is generated over the long term, that’s not a bubble. When you have hundreds of thousands of the smartest brains in the world working on one new technology, it is simple to expect significant improvements in that technology.

5) Information Asymmetry in AI Names Is Shrinking

Management teams now treat top Substack and X researchers in the same way as institutional investors. When a company reviews a 50-page SemiAnalysis report pre-IPO and leaves comments, the edge is compressing.

Alpha in AI infrastructure will come less from information and more from interpretation, timing, and valuation discipline. Which is why we believe good research and contrarian thinking matter even more.

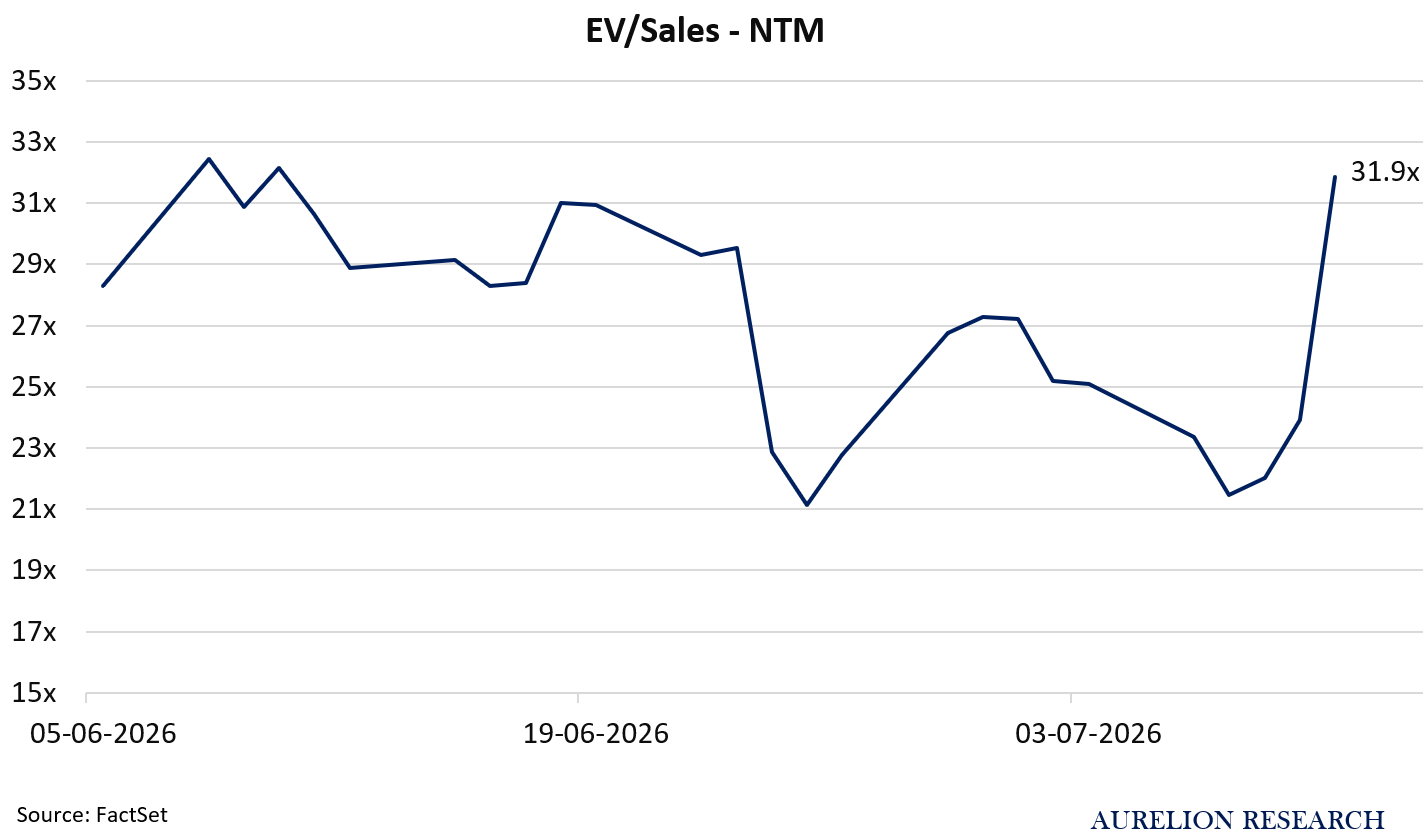

6) Valuation Is Narrative-Driven Until Cash Flows Arrive

That is an obvious one. With profitability not expected before 2027 and free cash flow in 2028, prices in this cohort trade on news flow and sentiment.

4. The Debate: The Promise and the Challenges of Cerebras

4.1 The Bull Case: A New Path for AI Computing

The bull case for Cerebras is built around one main idea: as AI models become larger and more complex, the industry may need new approaches to computing. Today, most AI systems rely on GPUs, but scaling these systems requires connecting many chips together, which can create performance limitations.

Cerebras takes a different approach by combining computing and memory on a single large chip, which bulls believe could help address some of the challenges created by increasingly complex AI models. The Silicon Valley-based company is competing in a rapidly growing AI infrastructure market alongside companies such as Nvidia, Groq, and SambaNova.

While Nvidia benefits from a strong software ecosystem built over many years, bulls believe Cerebras’ hardware design could give it an opportunity in areas where speed and efficiency are especially important.

The company is also expanding beyond hardware sales through cloud services, allowing customers to access its systems without purchasing the infrastructure themselves and potentially creating a more recurring revenue stream over time.

4.2 The Bear Case: The Challenges Behind the Ambition

The bear case for Cerebras is built around three main concerns:

Customer concentration

Software Ecosystem

Long-term scalability

First, Cerebras currently depends on a small number of large customers. While the company is working to expand its customer base, bears argue that relying on a few major contracts could make future revenue less predictable.

Second, Nvidia’s advantage extends beyond its chips. Its CUDA software platform, which allows developers to build and run AI applications on Nvidia hardware, has been developed over many years and is widely used across the AI industry. Bears believe this could make it more difficult for Cerebras to convince customers to switch to a different ecosystem.

Finally, some investors question whether Cerebras’ technology can continue to support the increasing demands of future AI models. Dylan Patel from SemiAnalysis has raised concerns around whether the company’s current approach can scale as AI systems become more complex. These questions remain an important part of the long-term debate around Cerebras.

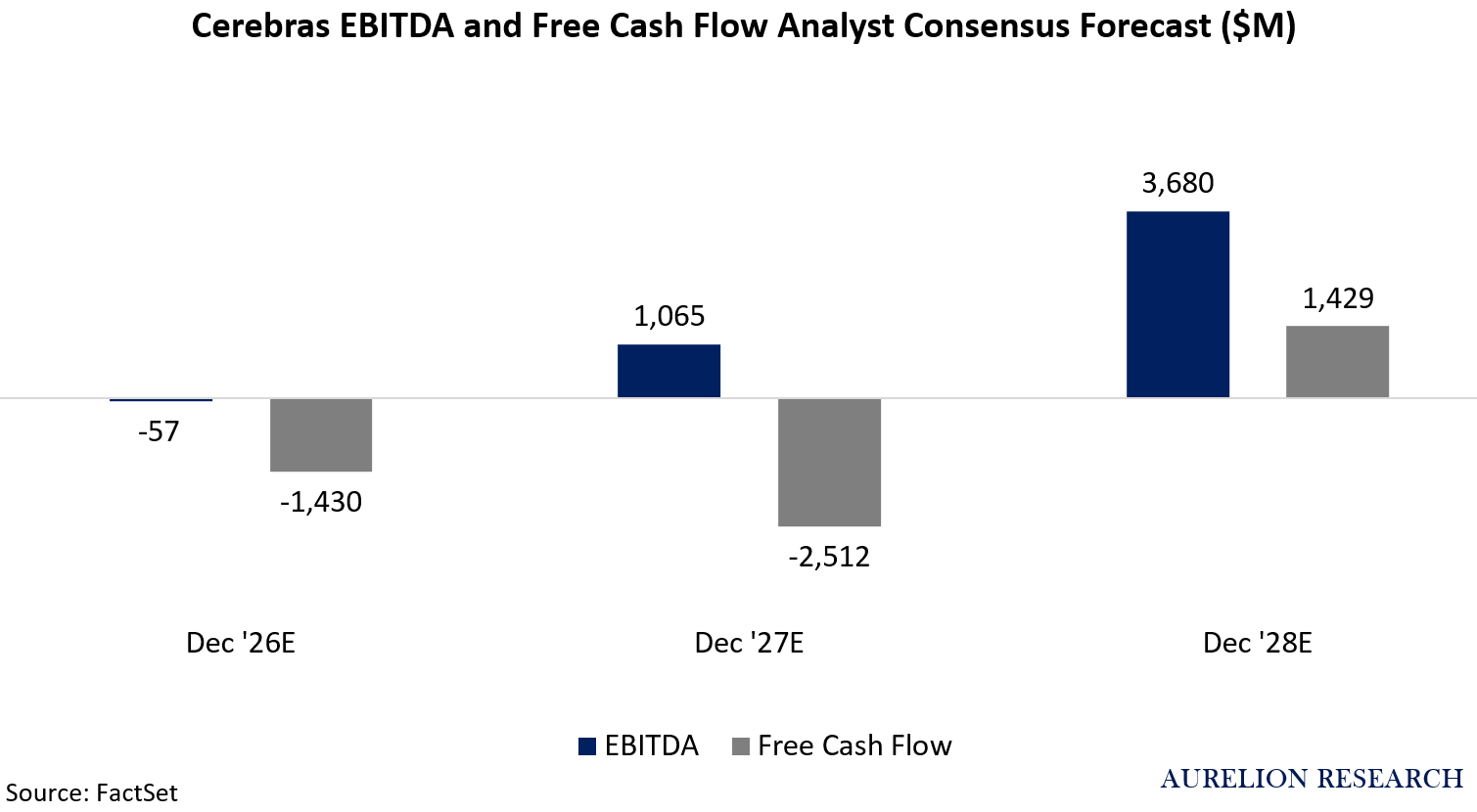

5. Valuation: An Analyst’s Nightmare

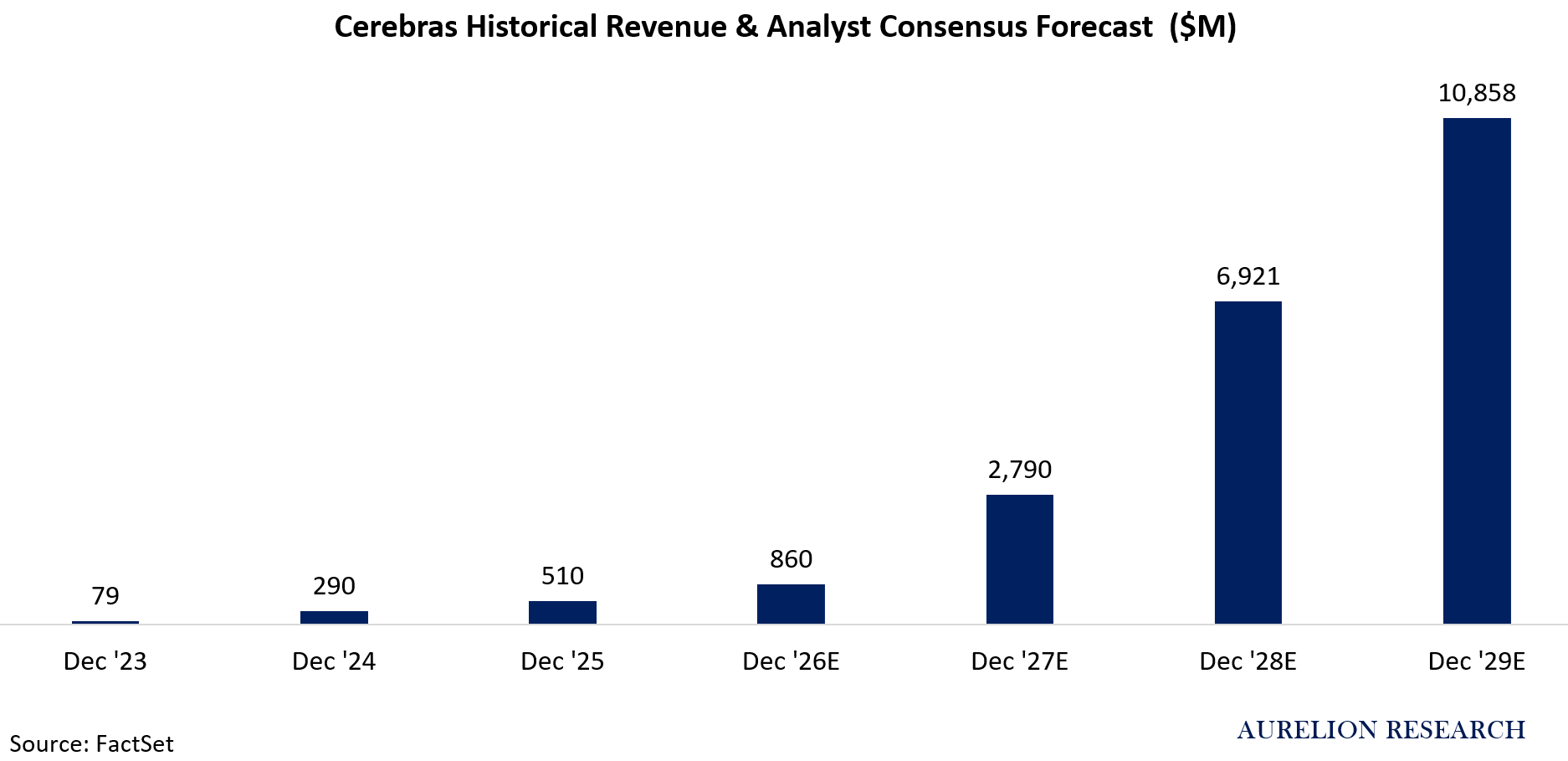

The company’s revenue growth is gigantic, expected to 20x over the next 4 years.

Wall Street expects this company to turn profitable in 2027 and for cash flows to be positive in 2028. On the positive side, the company has enough cash on the balance sheet to cover upcoming needs. The EBITDA forecast could make sense.

However, we are less confident about the cash flow forecast. The need for continuously investing and staying at the forefront of the AI race will persist, and we think the company will prefer to spend to continue trying to develop leading technologies rather than having cash generated and distributed to shareholders.

Is this company worth $20B, $50B, or $100B? Usually, it is quite easy to triangulate toward a valuation range when the company generates cash, but in this case, valuing the company with any confidence is tough enough that it makes the share price mainly dependent on short-term news.

6. Our Final Thoughts on Cerebras

The reason we are not currently adding Cerebras is that, while it operates in a highly attractive and growing sector, it has not yet proven that it can generate the level of free cash flow and profitability needed to justify its current valuation.

We believe Cerebras has built an impressive product with significant potential, but we would like to see the company demonstrate that it can successfully scale its business and translate its technology into sustainable financial results.

Another important factor is timing. At Aurelion Research, we are not only looking for great companies; we are also looking for the right moment to invest.

While we clearly see a compelling long-term opportunity, we believe it is still early in Cerebras’ journey as a public company. It has an interesting position in the AI infrastructure market, but the timing is not right yet.

The Aurelion Team

Questions? Reach us directly on Substack or at contact@aurelionresearch.com.