Global Drone Primer 2026: Navigating the Shift Toward Autonomous Defense

We are in the early innings of A high-growth market driven by defense spending, autonomy, and evolving security needs.

Given everything happening with Iran right now, you will not be surprised that we are focusing on drones today. It is an incredibly active sector.

We originally set out to write a broader defense primer, but drones kept swallowing every section we wrote. At some point it became obvious they deserved their own report, so that is what we built.

Between the Israel-Iran escalation and the ongoing war in Ukraine, NATO and the U.S. are buying these systems at an unprecedented rate. They constantly need to replenish their stocks and upgrade their fleets to keep up with the pace of technology. These systems are now treated as consumables instead of long-term assets, and that changes the demand profile entirely.

The real task now is finding the best companies to own to benefit from this cycle. That is exactly what we are doing today. But before getting into specific names, let us look at the broader thematic setup, which, quite frankly, looks fantastic.

Beyond the investment case, drones represent the first mass deployment of physical AI, and understanding how this technology is evolving tells you a great deal about where autonomous systems are headed across every industry.

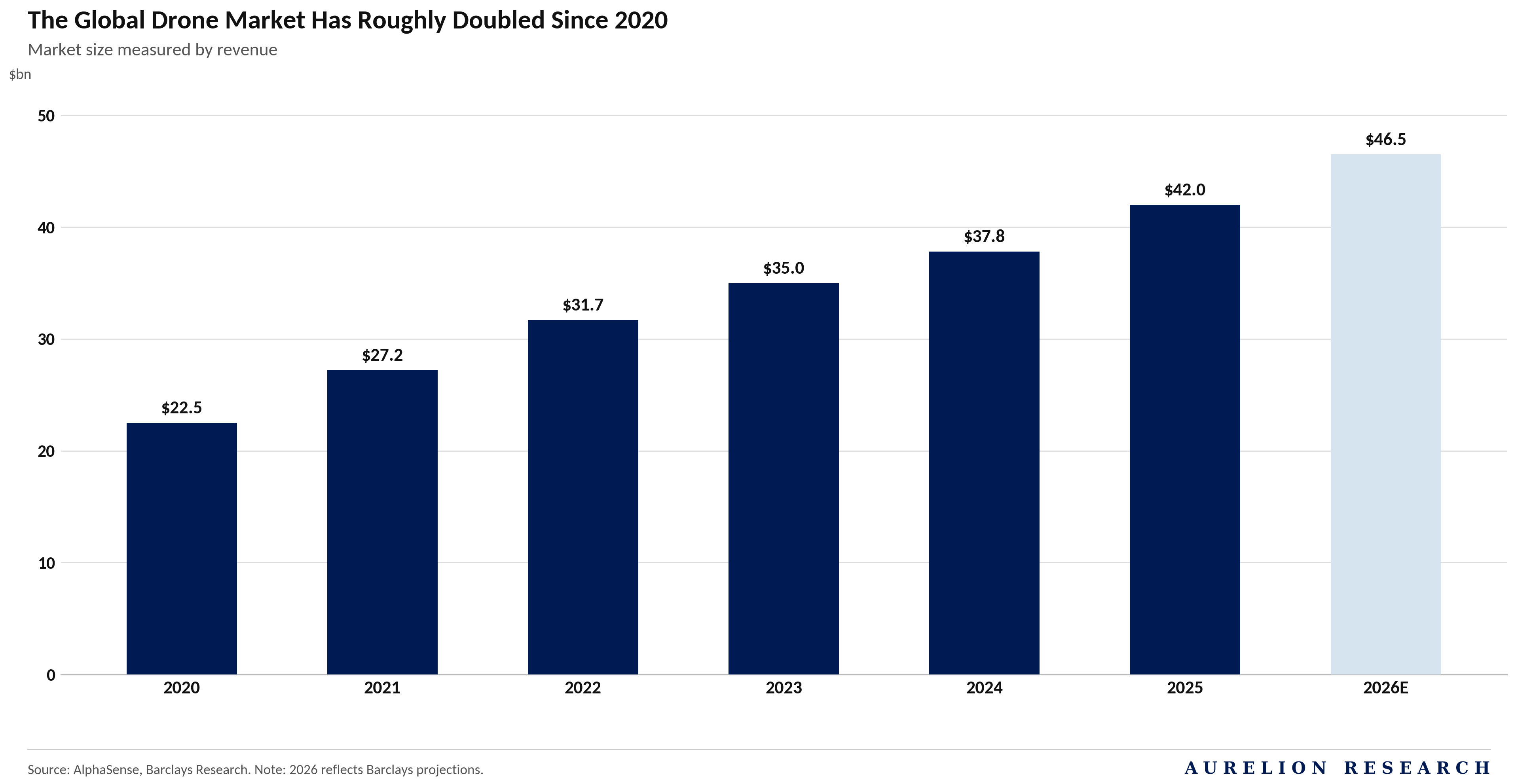

As you can see in the chart above, the global drone market has roughly doubled over a remarkably short period. Total industry revenue surged from $22.5bn in 2020 to $42.0bn in 2025, and it is firmly projected to reach $46.5bn by the end of 2026. Safe to say, this looks like an exceptionally good place to be positioned for the future.

Table of Contents

Why Drones, Why Now?

1.1 The Drone Industry Is Growing Fast

1.2 The Shift Toward Autonomous Defense

Drones: A $400B Market Opportunity

Understanding the Industry

3.1 Types of Drones Available Today

Our Top Takeaways

Market Overview & Technology Dynamics

5.1 Market Overview

5.2 Global Market Outlook

5.3 Public Defense Spending & Contract Trends

5.4 Private Capital & Funding Momentum

Our Top Picks

Favourable Regulatory Frameworks

Our Final Take

1. Why Drones, Why Now?

The backdrop speaks for itself. The world has more active conflicts today than it did five years ago, and drones are at the center of most of them. The war between Ukraine and Russia is the most closely watched, a conflict that has dragged on for years with no real end in sight and has become the largest real-world test of drone warfare we have ever seen. But demand goes well beyond that. Israel, Iran, and NATO members are all rushing to build up their inventories. Demand is strong and coming from everywhere.

The question we always ask ourselves when a theme starts getting attention is whether it actually has legs, or whether it is just momentum that fades once the headlines move on. For drones, we think the answer is pretty clear.

The fundamental appeal is simple: a drone does not come with a body bag. When one gets shot down, nobody dies. That changes everything about how willing governments are to use them, how often, at what scale, and how the population perceives attacks on other nations.

And on top of that, they keep getting cheaper and better every year. Countries are fundamentally rethinking how they defend themselves and project power, and drones are becoming a core part of that answer.

We think we are still early in that story.

1.1 The Drone Industry Is Growing Fast

The drone industry is expanding fast, driven by AI capabilities and geopolitical necessity. Modern autonomous drones eliminate the need for onboard pilots, removing casualty risk and keeping personnel off the front line. They operate as networked, intelligent systems that require minimal human input to execute missions.

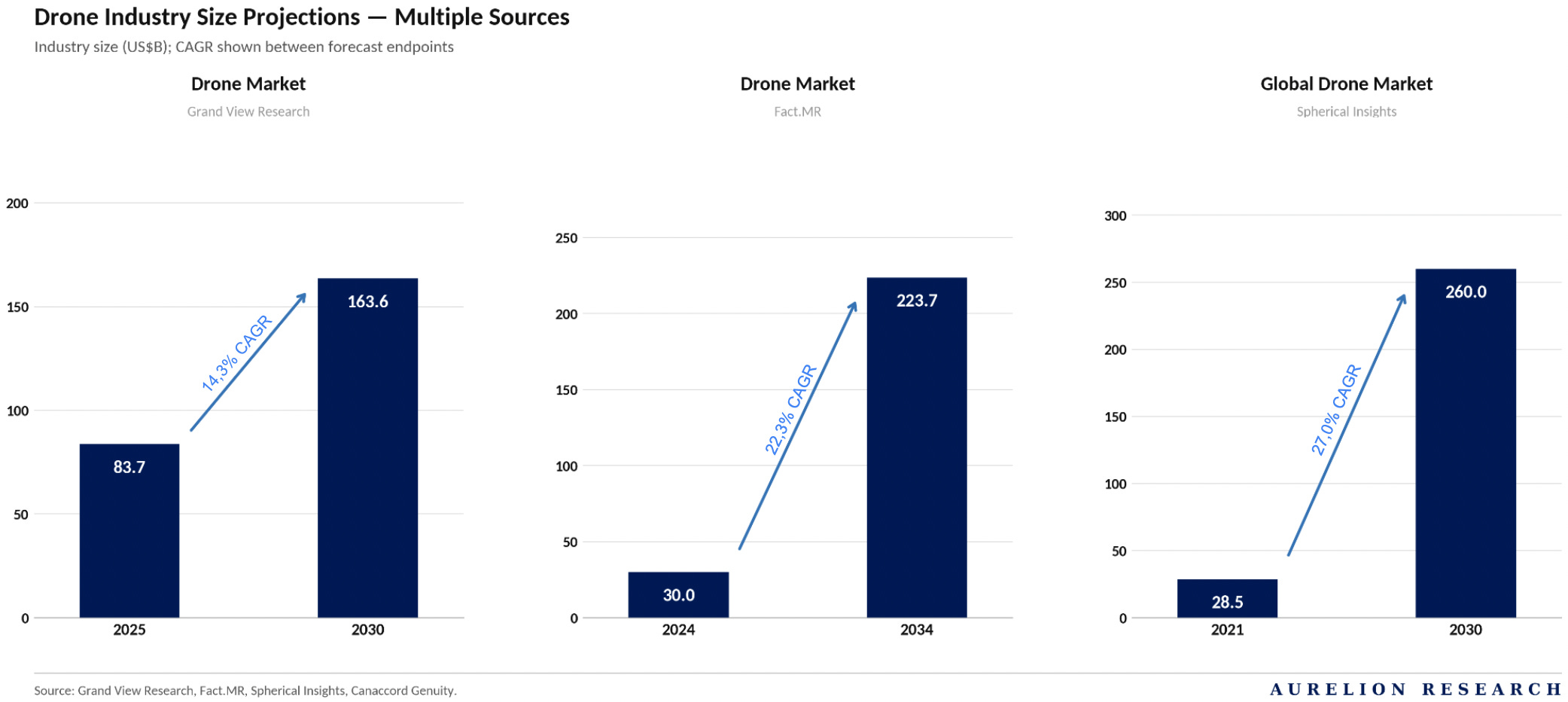

No matter the source, the drone market is expected to grow rapidly. Over the next decade, Oppenheimer expects total drone hardware, software, and services to grow tenfold, from $45B to $400B globally. Spending splits roughly evenly between multi-rotor systems (hover and manoeuvre) and fixed-wing craft (long distance coverage). Both categories are expanding.

Defense accounts for around 75% of total spending. Global military expenditures currently sit around $3.1T, up 50% over the last five years and on track to double within the next decade. Governments are actively shifting budget away from legacy hardware toward autonomous systems. If that pace holds, the drone market could reach $400B faster than consensus expects.

This growth is driven by three factors:

Evolving regulatory environment: Standardized frameworks for beyond-visual-line-of-sight (BVLOS) operations expand drone accessibility and enable remote operations across jurisdictions.

Commercial & industrial momentum: New applications including logistics, infrastructure inspection, and agriculture, combined with AI enabled automation, are accelerating adoption in private sectors.

Defense priorities: Global rearmament trends and heightened focus on sovereign defense capabilities are driving significant investment in drone technologies.

1.2 The Shift Toward Autonomous Defense

We are currently witnessing a massive shift toward autonomous defense, which is exactly why Oppenheimer expects military spending on these systems to eventually hit 10% of total defense budgets. That is huge for drones. They have become the fastest growing part of physical AI because they are so effective for scouting plus strike missions. Controlling the airspace is now essential for controlling the battlefield.

We see this clearly in Ukraine. Beyond the front lines, governments are rushing to support this tech because owning the drone supply chain has become a matter of national survival. This shift is part of a larger geopolitical race involving satellites, energy, plus AI. We believe this combination will disrupt the traditional defense industry. Future conflicts will likely move toward machine to machine warfare.

2. Drones: A $400B Market Opportunity

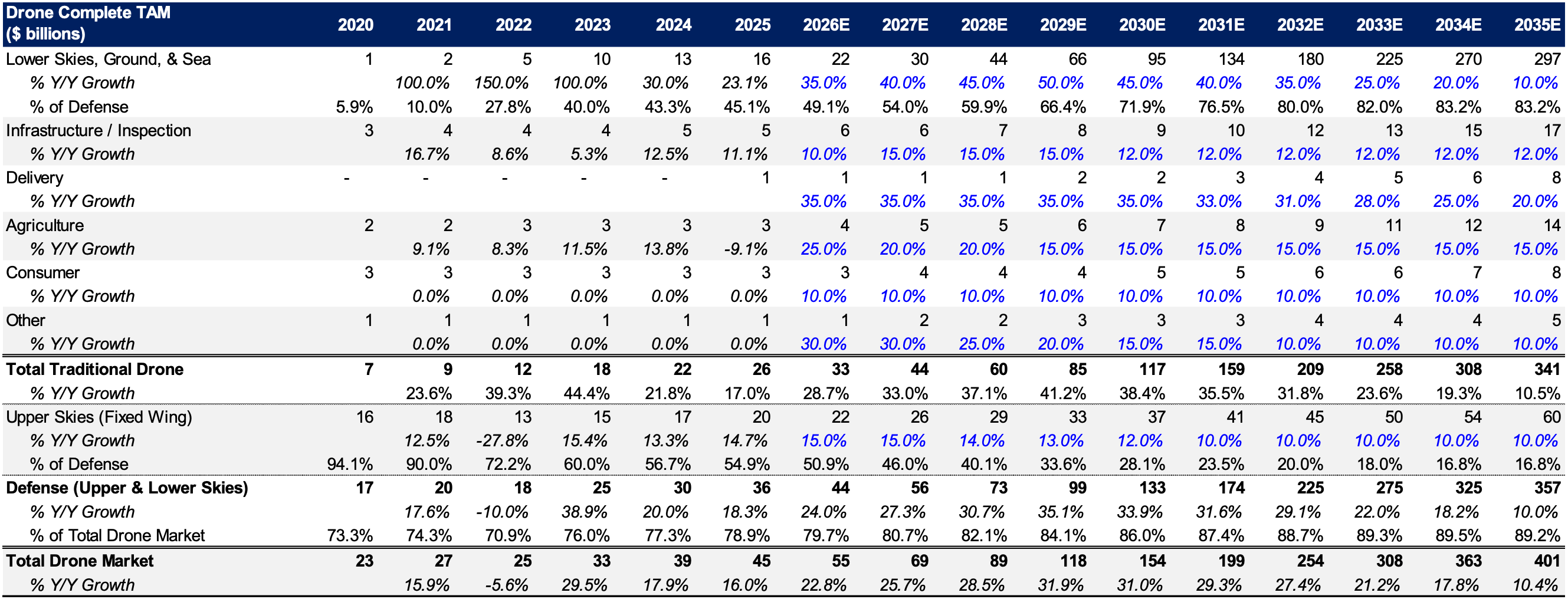

The model from Oppenheimer shows we are at a major turning point.

The real story here is the lower skies segment, which alone is expected to grow from $22B in 2026 to nearly $300B by 2035. That means this single category will make up about 75% of the entire industry plus represents nearly 20x growth on its own. Governments are reallocating budgets away from traditional hardware toward autonomous systems. If this pace continues, the drone market could reach those $400B targets far sooner than most expect.

Drone TAM Model ($bn)

The move toward drones marks a fundamental change in how the world works. It is the first time we are seeing physical AI, which are systems that can sense plus act in the real world, deployed on a massive scale. This is a foundational shift on par with the arrival of the internet or electricity.

As autonomy moves into the physical domain, it kicks off a decades long investment cycle focused on real world automation. In the short term, whoever perfects these systems first will likely hold the advantage in Ukraine. Once that technology is proven on the battlefield, we think it will quickly move into self driving transport plus other commercial industries.

Drones Are Expanding Into Industrial & Commercial Applications

Nations are now racing to build their own drone industries by bringing manufacturing back home plus sourcing materials from allies.

They are also moving away from slow engineering plus adopting a faster, tech focused approach. As costs drop plus rules change, drones will become practical for many commercial jobs. Over the long term, these systems will likely form a permanent infrastructure layer in our skies. This creates a massive sensing network that changes how we collect plus use data.

3. Understanding the Industry

Drones have a longer history than most people realize.

The concept traces back to 1849 when Austrian forces deployed explosive laden balloons in warfare. World War I saw early radio controlled aircraft emerge as precursors to modern UAVs. By World War II, drones were used extensively for reconnaissance and target practice. The Cold War accelerated technological development. The term "drone" itself became popular in the 1930s, inspired by the British DH.82B Queen Bee.

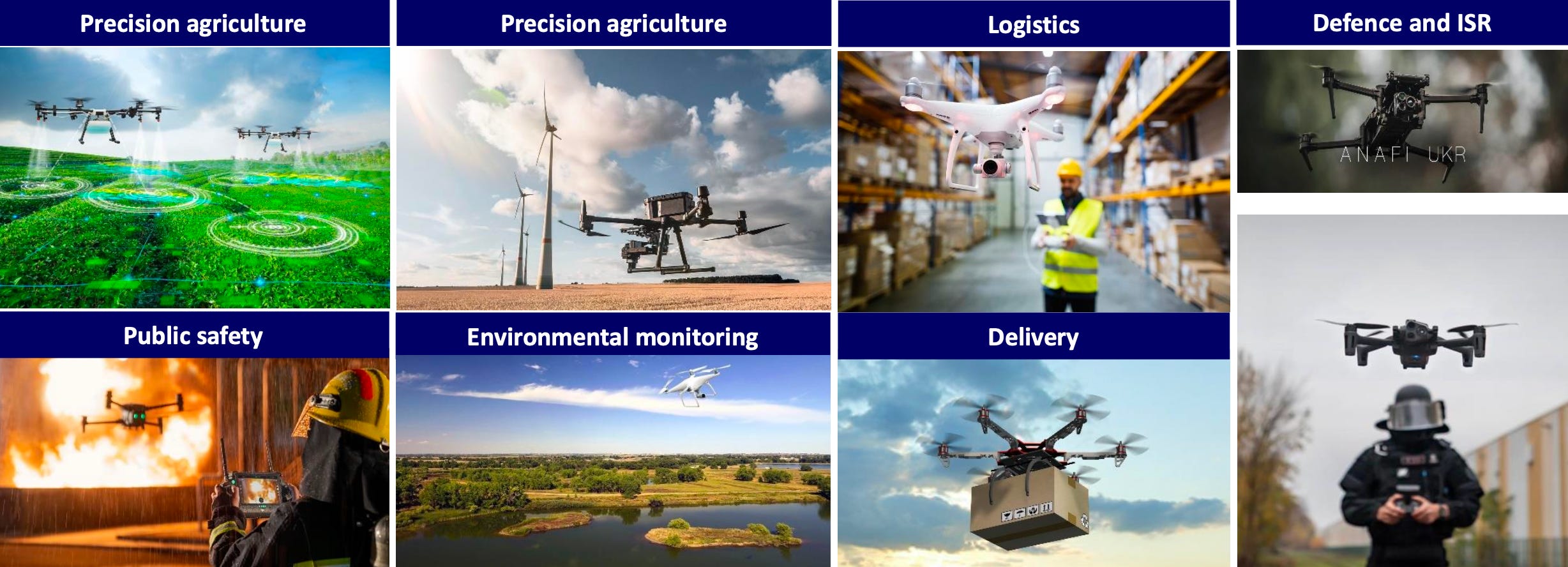

In recent decades, drones transitioned from purely military tools to commercial and recreational devices, expanding into photography, delivery, agriculture, and emergency response. We believe this diversification of use cases has grown the total addressable market significantly, and the expansion is far from complete. As regulatory frameworks mature and AI capabilities advance, new applications will continue to emerge, further expanding TAM across both commercial and defense segments.

Today’s drones serve multiple purposes. Military reconnaissance and targeted strikes remain core applications, but civilian uses now dominate volume: filmmaking, infrastructure inspection, environmental monitoring.

As you’d expect, AI and GPS integration have made drones smarter and more autonomous. Future trends point toward urban air mobility and autonomous delivery systems. The technology is only getting sharper. The industry has matured rapidly from experimental military technology into a multi-billion-dollar commercial sector. Regulatory frameworks and AI integration continue to shape the next frontier in urban mobility and autonomous operations.

3.1 Types of Drones Available Today

Drones are classified by design, function, size, weight, purpose, operational characteristics, autonomy level, and regulatory standards.

Multi rotor drones (quadcopters, hexacopters) dominate consumer and tactical applications. They offer high stability, ease of control, and excel at short range tasks like aerial photography and inspection. Their compact design enables vertical take-off and landing without runway requirements.

Fixed wing drones resemble aeroplanes. Built for long range missions like mapping and surveillance, they offer longer flight times but require runways for take-off and landing, limiting flexibility in constrained environments.

Single rotor drones operate like helicopters. More efficient for heavy payloads and longer endurance, but harder to fly and more expensive to operate and maintain. Hybrid VTOL drones combine vertical take-off capability with fixed wing efficiency. Advanced applications like search and rescue, agriculture, and military operations benefit from this hybrid approach. The trade-off is higher cost and system complexity.

Drones also classify by weight: nano (under 250g), micro (250g to 2kg), small (2kg to 25kg), medium (25kg to 150kg), and large (over 150kg).

These classifications determine regulatory requirements, operational limits, and licensing needs for both recreational and commercial use. Operational characteristics such as range, altitude, and power source (battery, fuel, hybrid, solar) influence mission type, flight duration, and regulatory scope.

The micro-drone segment has become strategically important where defense procurement, regulatory compliance, and software capabilities converge.

We believe this concentration of competitive intensity and margin opportunity reflects government spending priorities, established procurement cycles, and NATO compliance barriers that create competitive moats. Suppliers who clear those hurdles lock in customers and pricing power. This dynamic will only intensify as defense budgets expand and Western governments formalize their sovereign supply chain strategies.

4. Our Top Takeaways

4.1 The battlefield has rendered its verdict

Mass-produced, low-cost drones now deliver what billion-dollar weapons systems once handled exclusively. Military force structures are being rebuilt around that reality, and budgets are following.

4.2 Software is where value concentrates

Computer vision, edge AI, and autonomous navigation have turned drones into decision-making platforms capable of detecting, classifying, and acting with minimal human input in contested environments. Hardware has become almost secondary.

4.3 Supply chains are now a security imperative

Roughly 80% of drones are currently manufactured in China, with estimates suggesting nearly 30% of US military equipment relies on Chinese components. Governments have moved to make this unacceptable, and the push to reshore manufacturing is accelerating. For domestic producers, this represents significant tailwind.

4.4 Drone fleets are becoming critical data infrastructure

Combined with satellite observation, they generate real-world, continuous data that feeds next-generation AI models. The strategic value extends well beyond individual missions.

4.5 Demand will outpace supply for years

The primary bottleneck is onshore manufacturing capacity and the time required to build it. The gap between what governments need and what industry can currently deliver is where the investment opportunity exists.

5. Market Overview & Technology Dynamics

5.1 Market Overview

The drone market divides into four distinct categories optimized for different missions. Fixed wing platforms excel in long range surveillance and mapping by prioritizing endurance and distance over maneuverability.

Single rotor platforms function like traditional helicopters, providing longer flight times and heavier payload capacities suitable for cargo and agricultural operations. Hybrid vertical takeoff systems combine these capabilities for large scale operations, though they require significant capital and complexity.

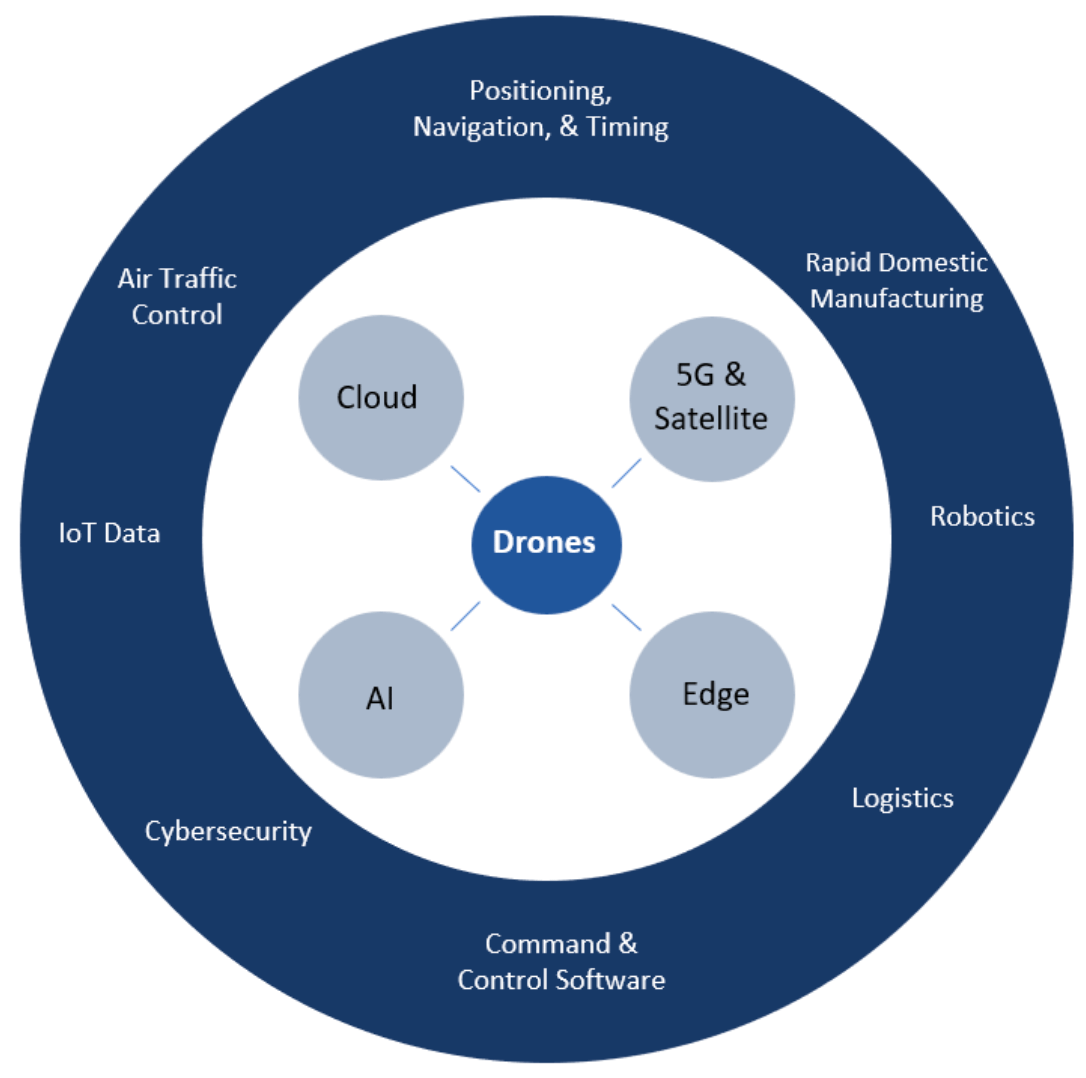

For defense applications, multi rotor micro drones stand out as the definitive choice. These highly agile, easily deployable systems dominate tactical operations, detailed inspections, and search and rescue missions.

As the fastest growing segment globally, they align with NATO procurement cycles and support deep software integration, acting as unified platforms that seamlessly connect artificial intelligence, edge computing, and cybersecurity.

Drone as a Platform

5.2 Global Market Outlook

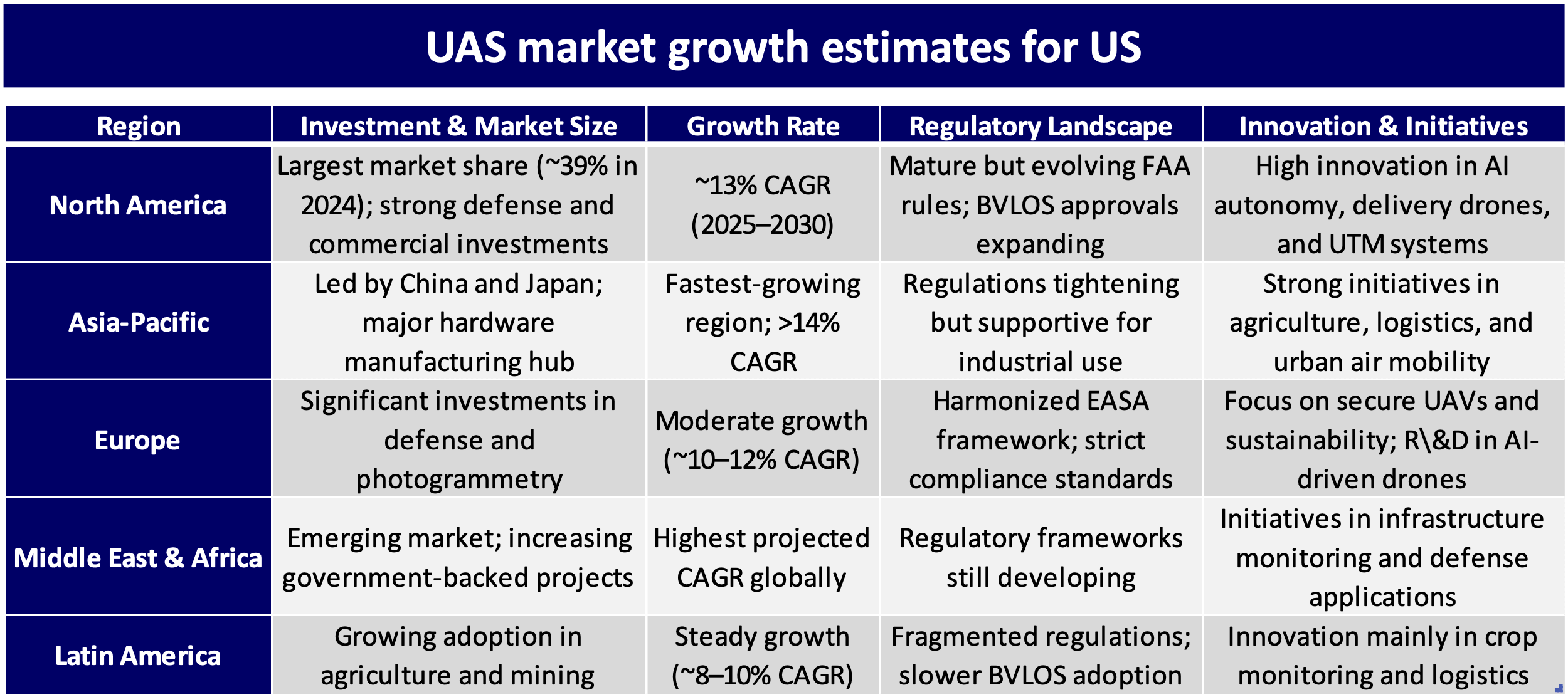

The unmanned aerial systems market is expanding rapidly worldwide, shaped by distinct regional growth drivers and regulatory environments. North America currently leads the sector, holding ~39% of the global market in 2024. Supported by strong commercial and defense investments, the region is projected to grow at a 13% annual rate through 2030 as aviation authorities expand approvals for flights operating beyond the visual line of sight.

The Asia Pacific region remains the fastest growing market globally, expanding at over 14% annually. Led by manufacturing powerhouses China and Japan, this volume driven market sees broad adoption across agriculture, logistics, and urban air mobility. Europe follows with a steady 10-12% annual growth rate, operating under a harmonized and strict aviation framework.

European investments are heavily concentrated on defense and photogrammetry, prioritizing secure and artificial intelligence driven platforms. Meanwhile, government backed infrastructure and surveillance projects in the Middle East and Africa are driving the highest projected growth rates in the world, whereas Latin America anticipates steady 8-10% growth, primarily in crop management, though fragmented regulations continue to slow broader deployment.

5.3 Public Defense Spending & Contract Trends

To understand genuine market demand across the ecosystem, researchers track official government contract obligations through public ledgers instead of immediate corporate revenue. These obligations reflect concrete funding commitments tied to multi year programs and task orders, serving as a highly reliable indicator of future deployments.

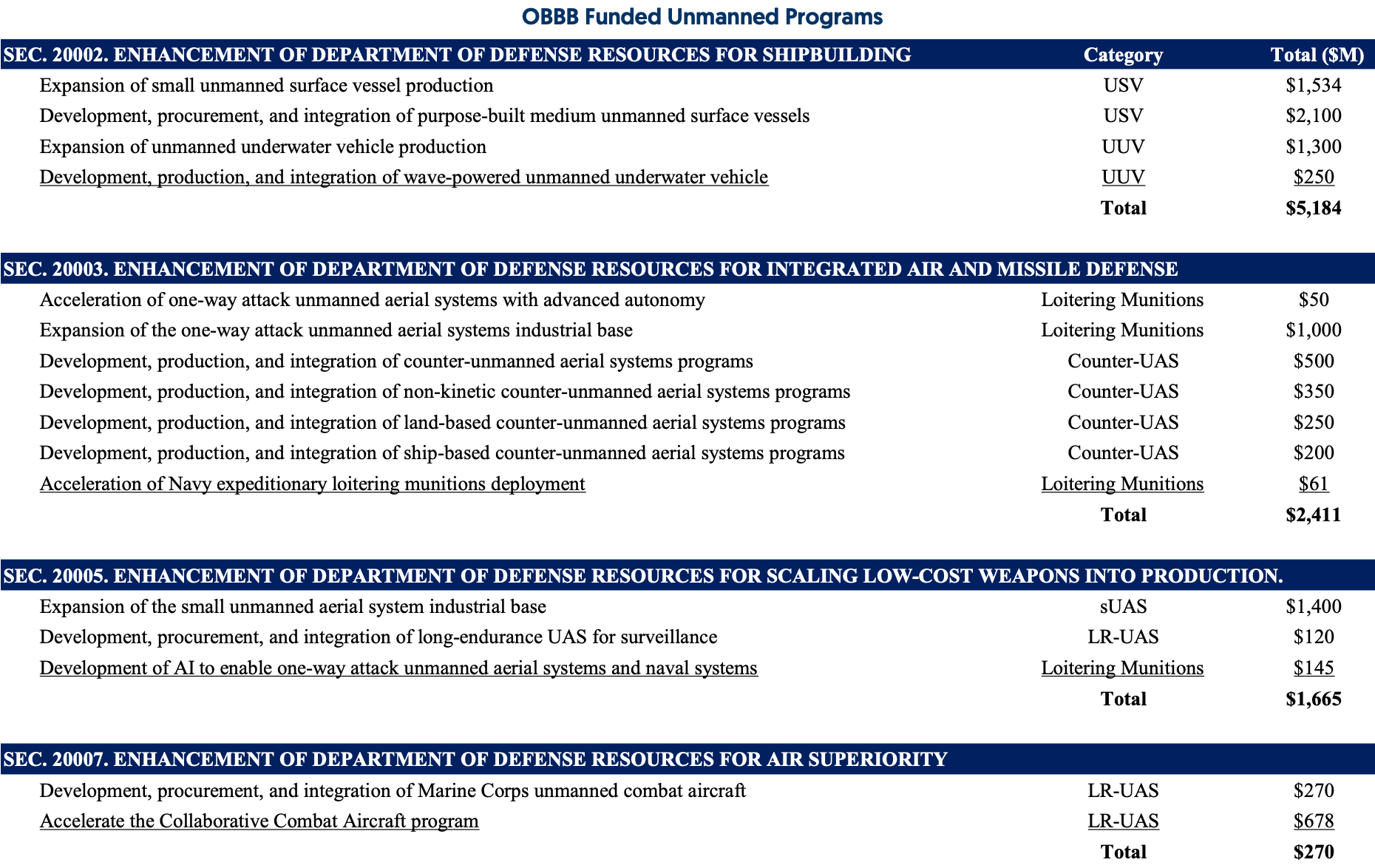

Current data reveals a massive influx of capital into unmanned defense programs. Recent allocations include $5.1B designated for shipbuilding initiatives such as unmanned surface and underwater vessels.

Another $2.4B is directed toward integrated air and missile defense, encompassing attack drones and counter drone programs, alongside an additional $1.6B for scaling the production of low cost surveillance drones.

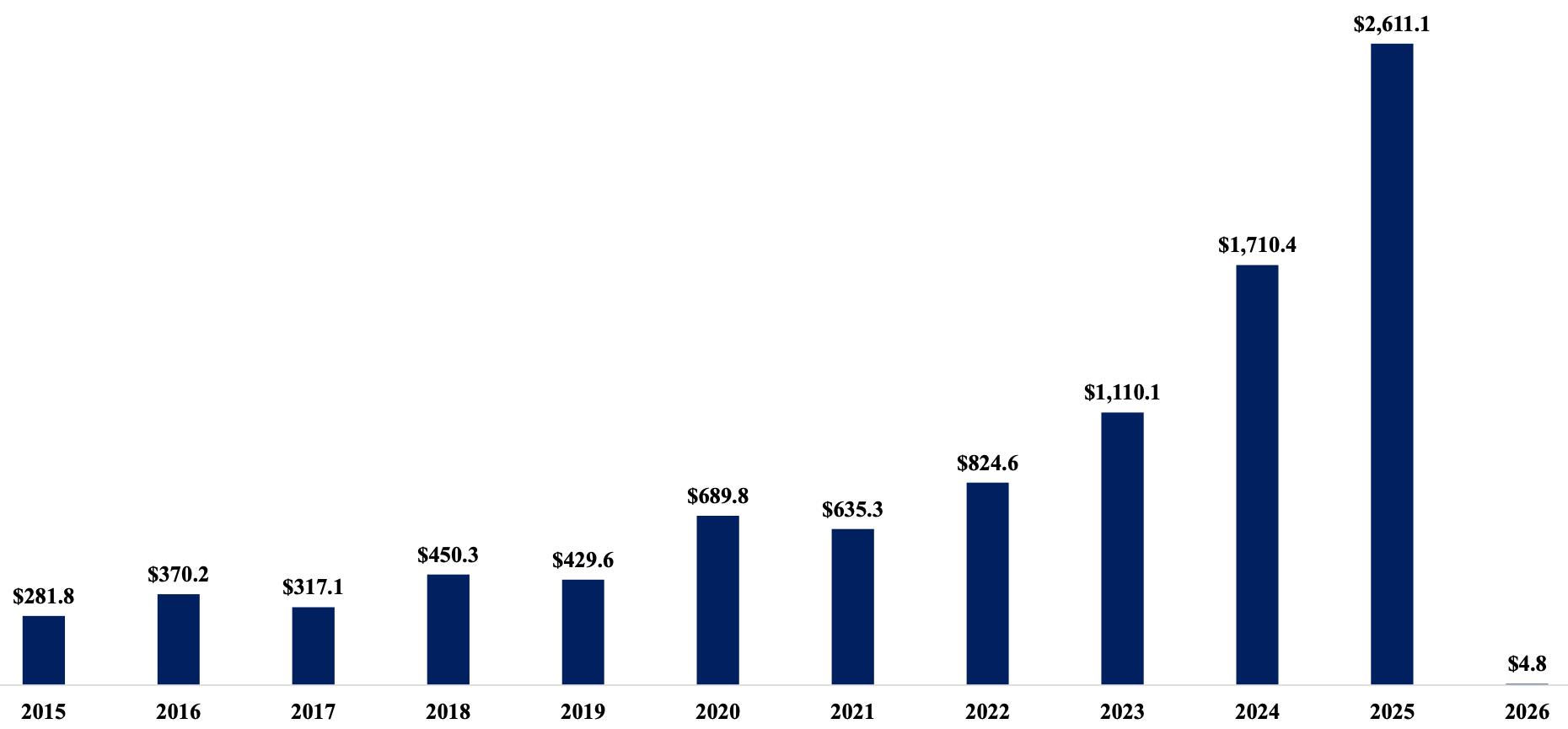

When looking at the historical trajectory, overall contract obligations for unmanned equipment manufacturers reached a record $2.6B in 2025, climbing sharply from just $281.8M a decade prior.

Total Contract Obligations Across Unmanned OEM Basket

While these figures do not capture classified research and development spending or awards routed through major prime integrators, they clearly demonstrate a broader industry truth. High level policy shifts and budget announcements are now successfully converting into funded, executable contracts across the entire defense ecosystem.

5.4 Private Capital & Funding Momentum

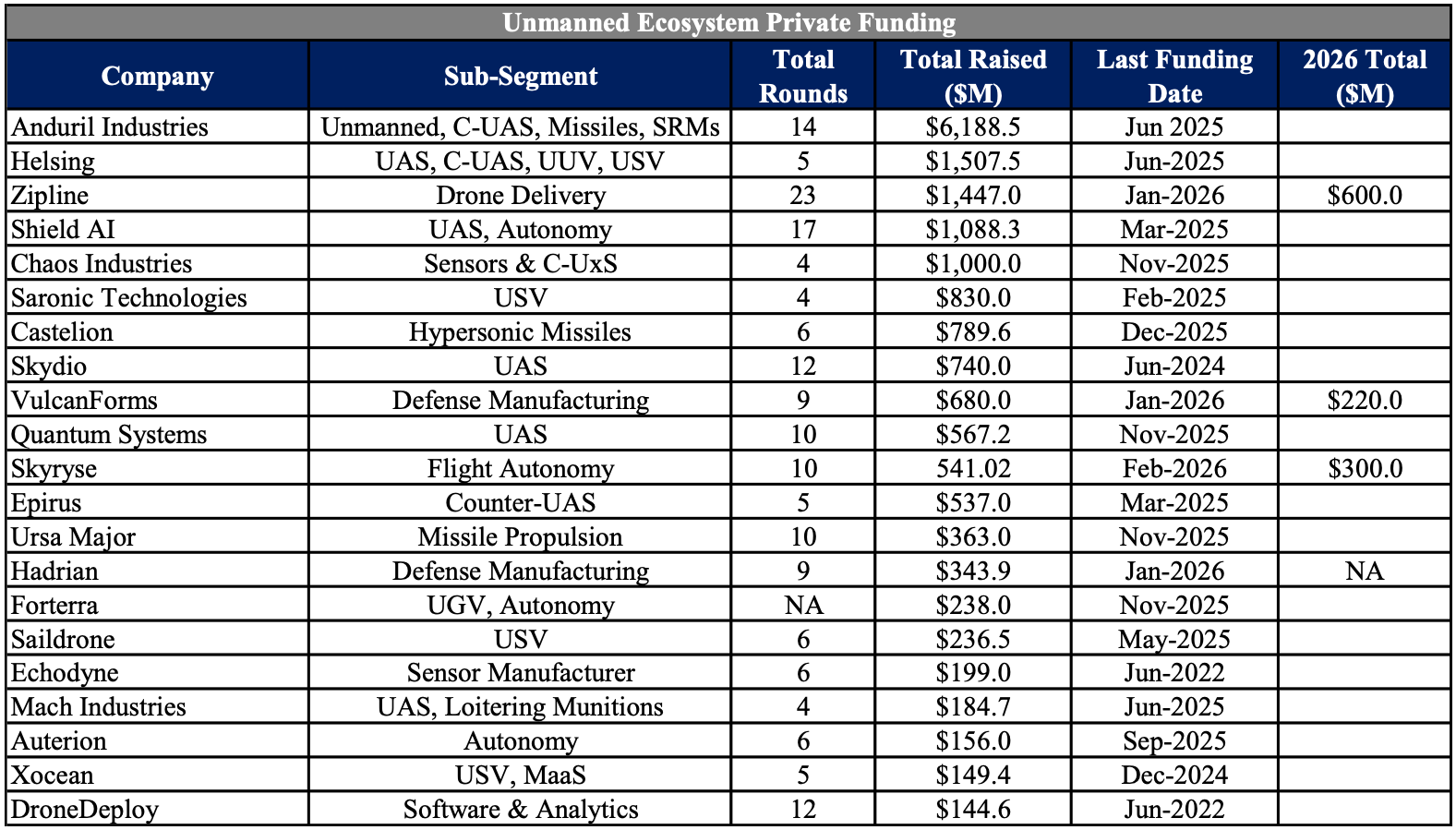

A significant portion of the innovation driving this unmanned supercycle stems from privately held companies. In early 2026 alone, private funding surged as capital concentrated around next generation defense technology.

Notable recent capital raises include Zipline securing $600M for its autonomous delivery network, Skyryse raising $300M for flight automation systems, and VulcanForms bringing in $220M for advanced defense manufacturing. Emerging players are also successfully raising millions to build mission adaptive software and advanced power systems.

The broader private ecosystem remains heavily capitalized. Leading defense technology firms have accumulated massive financial resources, with Anduril Industries raising over $6.1B historically, followed by European defense artificial intelligence firm Helsing with $1.5B, and autonomous systems developer Shield AI raising over $1.0B.

Furthermore, industry reports from early 2026 suggest Anduril and Shield AI are currently negotiating to raise billions more, underscoring the massive and sustained investor appetite for sovereign defense technologies.

The most important section of the report below.

We believe the rapid expansion of the defense technology sector is creating a rare, highly lucrative window for investors. The key is knowing exactly where the capital is flowing before the broader market catches on.

In the following section, we discuss our highest conviction ideas.