LatAm Oil & Gas: What About Fuel Prices?

With the war in Iran and oil prices moving higher, we know there is a lot of uncertainty around LatAm O&G right now, and we wanted to bring more clarity to the situation.

Our Core Thesis on Oil

To be clear, we know this is a big call, but we do not see oil staying higher for longer. We believe Iran is now too weakened to sustain this move. While the market is reacting to headlines, the reality of a diminished Iran will soon bring prices back down. The fundamentals simply do not support a permanent shift to triple-digit oil, and we expect this premium to fade.

Geopolitical Tensions Pressure LatAm Equities

Escalating conflict in the Middle East drove a broad risk-off move last week, with Latin American equities selling off sharply and underperforming the broader emerging market index. All key markets posted weekly losses, though with some dispersion. The geopolitical shock pushed oil prices toward $120 per barrel, providing relative support to more oil-sensitive markets.

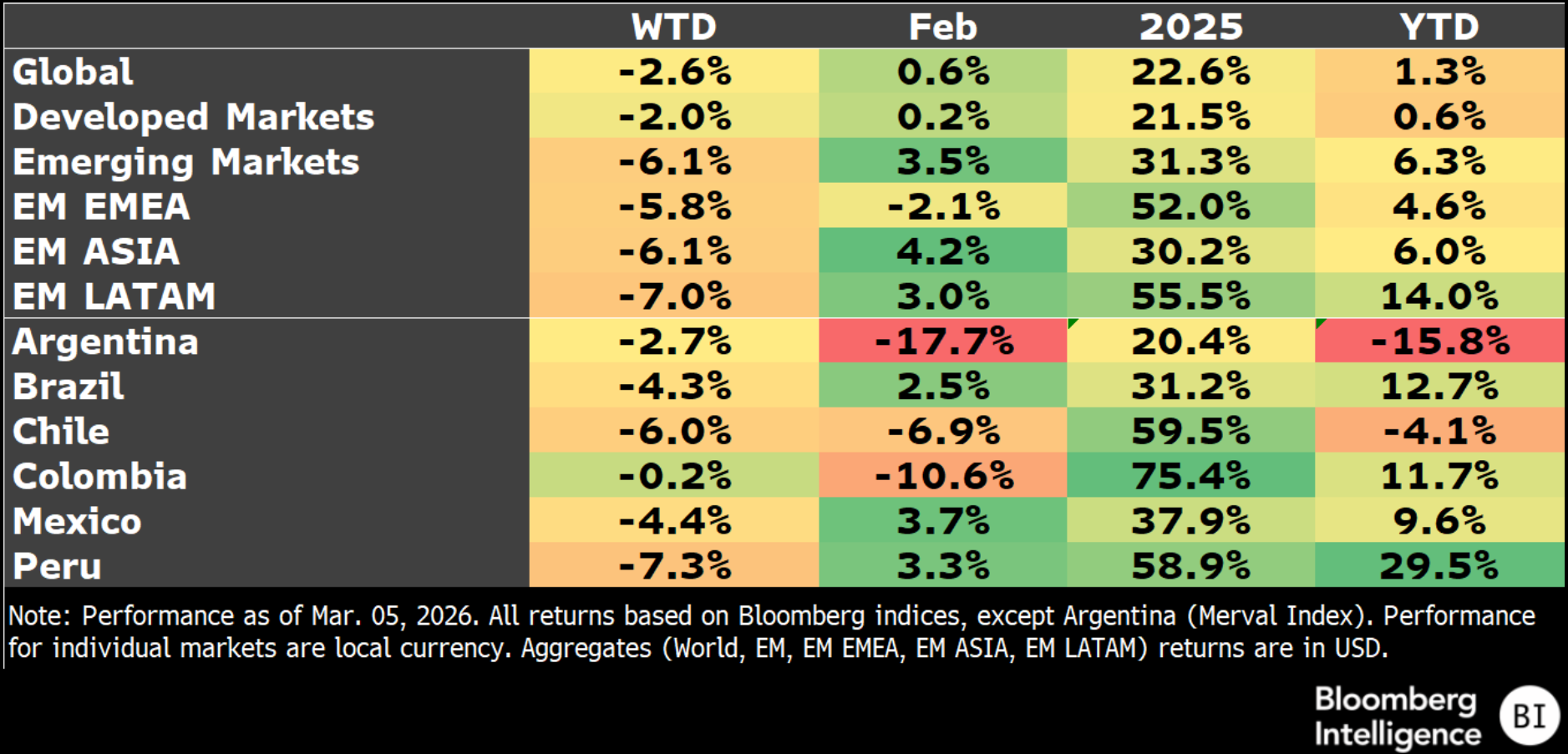

Bloomberg Country Index: Total Returns

Despite the recent setback, Latin America remains one of the best performing regions so far this year. Looking forward, the path will depend on the duration of the conflict and whether higher oil prices trigger inflation pressures that could slow down or reverse interest rate cuts. Even with those risks, we believe the region is well positioned to do just fine.

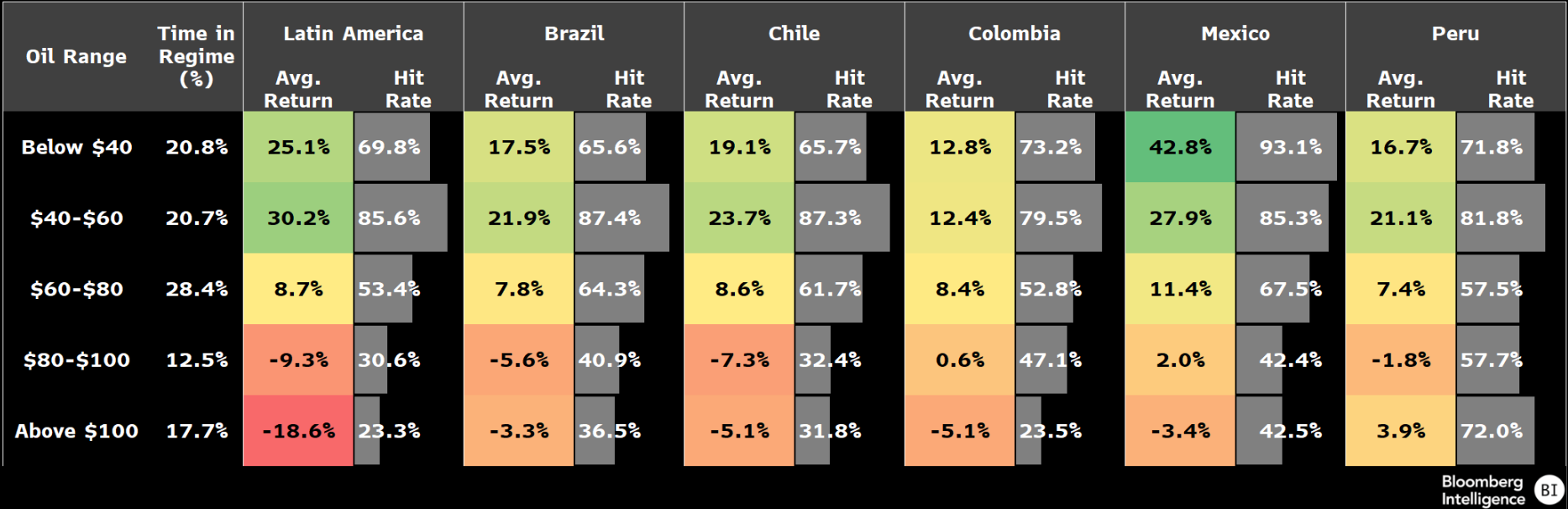

Does Oil at $80-100 Signals Weaker Returns Ahead?

Historical returns across oil regimes suggest prices above $100 per barrel would be a headwind for Latin American equities. Since 2000, the $40-$60 range has delivered the strongest average returns and hit ratios above 80% across key markets. Above $100, which Bloomberg Economics projects in a scenario of intensifying conflict, forward average returns have been the most negative for the regional index, though results diverge.

12M Fwd Returns by Oil Price Regime (Local FX)

Chile and Colombia underperformed, while Peru has posted positive returns on average with a hit ratio of 72%. With oil now in the $80 to $100 range, history suggests weaker performance ahead. A ceasefire that brings prices back toward $65 per barrel would offer a more supportive backdrop.

OUR TAKE ON OIL PRICES AND LATAM OIL & GAS

On our end, we don’t see oil staying higher for longer. We recently spoke with a top U.S. resources analyst who has a massive track record, including being short oil from $140 all the way down to $60. We always value his views plus find ourselves closely aligned with his take on aluminum, fertilizers, plus copper. Just like us, he believes Iran is now too weakened to sustain this move. We agree that oil prices won’t stay high for long.

Based on that, we think a long run range of $60 to $80 is a much more realistic baseline for the Latin American market. Because of this, we aren’t particularly worried about the $80 to $100 range that Bloomberg often points to as a danger zone for regional producers. Most major players in the region are far more resilient than they used to be. For example, Petrobras has managed to get its portfolio breakeven down to around $25 per barrel, while Ecopetrol is already planning its entire 2026 budget around a $60 Brent price.

This means they can still generate significant cash flow even if prices move toward the lower end of our range. The noise about higher prices being a “bad” thing for LatAm oil producers usually misses the fact that these companies have already lean-down their operations to thrive in a much lower price environment. Following the U.S.–Iran strikes, most of the market’s focus has gone to crude. For Brazil, the more immediate pressure sits in refined products. The country still relies on imported diesel and gasoline, so higher international prices feed quickly into domestic fuel economics. Petrobras stands at the center of that picture as Brazil’s largest fuel supplier.

Brazil Fuels: Price Increases Look More Likely

Our view is simple. If current oil prices held at these levels, Petrobras would eventually be forced to hike domestic fuel prices. However, since we expect oil to cool off plus return to the $60–$80 range, that pressure should subside before it triggers a major policy shift.

Since Petrobras adopted its new pricing framework in May 2023, it has moved away from reacting too quickly to global volatility. Instead, the company favors a smoothing strategy that allows domestic prices to lag international benchmarks during brief spikes. This approach works well for managing headlines plus uncertainty, but it becomes harder to sustain if the discount stays wide for too long.

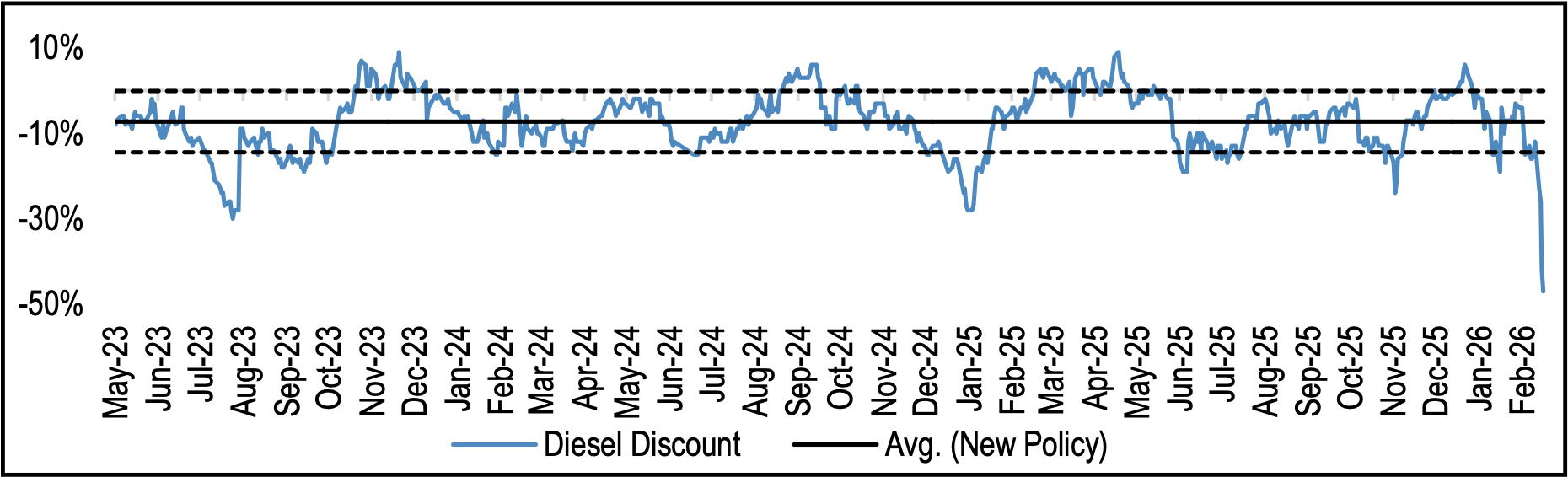

Diesel Still Trades at a 7% Discount

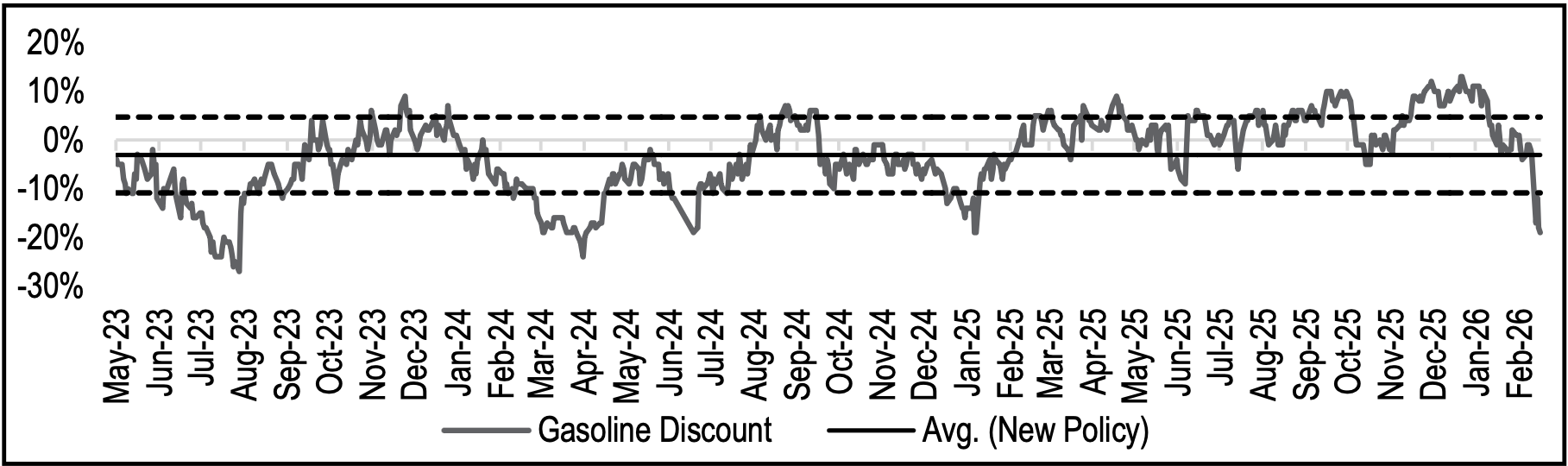

Gasoline Tracks Closer at a 3% Discount

As of early March 2026, the data shows that PBR is already leaning into this strategy. Diesel is currently trading at a 7% discount to international prices while Gasoline is tracking much closer with only a 3% discount. Because we view the current oil rally as a temporary reaction to the situation in Iran, we believe Petrobras can successfully bridge this gap without needing a major price hike. As global prices settle back into our target range, these discounts will naturally close, keeping the domestic market stable while protecting long-term margins.

2. Fuel Distribution: Sourcing Mix Gains Importance

The second order effect hits the fuel distributors. Brazil still relies on imported fuel to meet its domestic demand, which means the real cost of getting supply rises with global prices regardless of how slowly Petrobras reacts. In this environment, distributors with better access to the company’s volumes are in a much stronger position.

We see Vibra and Ultrapar as the clear winners in this setup. By sourcing more of their fuel from PBR, they gain a massive cost advantage over smaller competitors who have to buy on the expensive spot market. Even though we expect this oil price spike to be short lived, this temporary gap allows these market leaders to protect their margins while others struggle to keep up.

This dynamic is especially important right now. While a brief price move just creates noise, a more persistent gap changes the earnings setup across the entire distribution chain. Since we expect oil prices to move back toward the $60 to $80 range, this specific advantage might be short lived, but it still allows these leaders to solidify their market position while smaller competitors struggle with the temporary volatility.

Tail Risk: Fuel Availability & Global Aftershocks

The main downside risk to watch right now is a temporary supply squeeze, particularly in diesel. Petrobras is no longer the sole supplier in Brazil, and since imports now play a much larger role in meeting demand, any hit to import economics or logistics could trigger local shortages. Brazil’s transport system is heavily dependent on diesel, so any disruption there would move quickly through the rest of the economy.

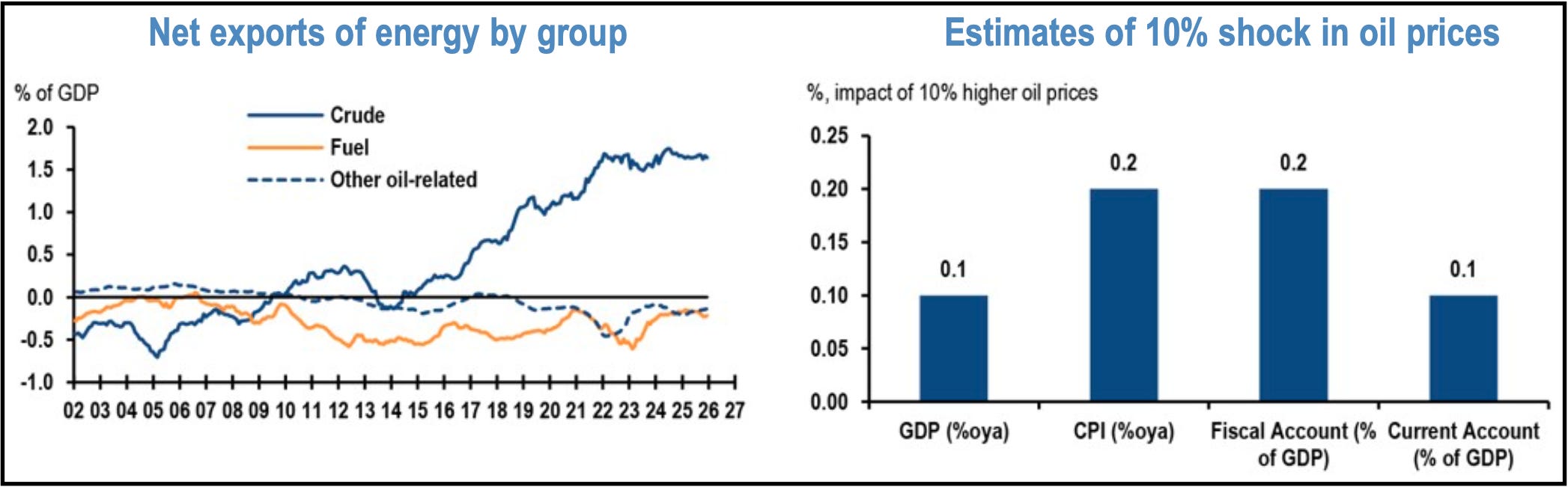

Even if we do not see this as the base case, it is a significant tail risk. On a broader scale, we are seeing global tsunamis but much smaller local effects. While the direct impact of the U.S. and Israeli operations against Iran has been somewhat limited in Latin America, net oil importers are still feeling the pinch in their trade balances.

The Monetary Impact

The main concern for the region is how central banks respond if higher oil prices begin to feed through more quickly into domestic inflation. If that happens, policymakers across LatAm could have much less room to ease than investors currently expect. That risk is especially relevant for Brazil, Chile, and Mexico, where rate cuts are already in focus. A renewed rise in fuel and energy costs could slow that process or pause it altogether.

For markets, the issue is clear: tighter policy for longer would weigh on growth and pressure the parts of the economy that are most exposed to financing costs.

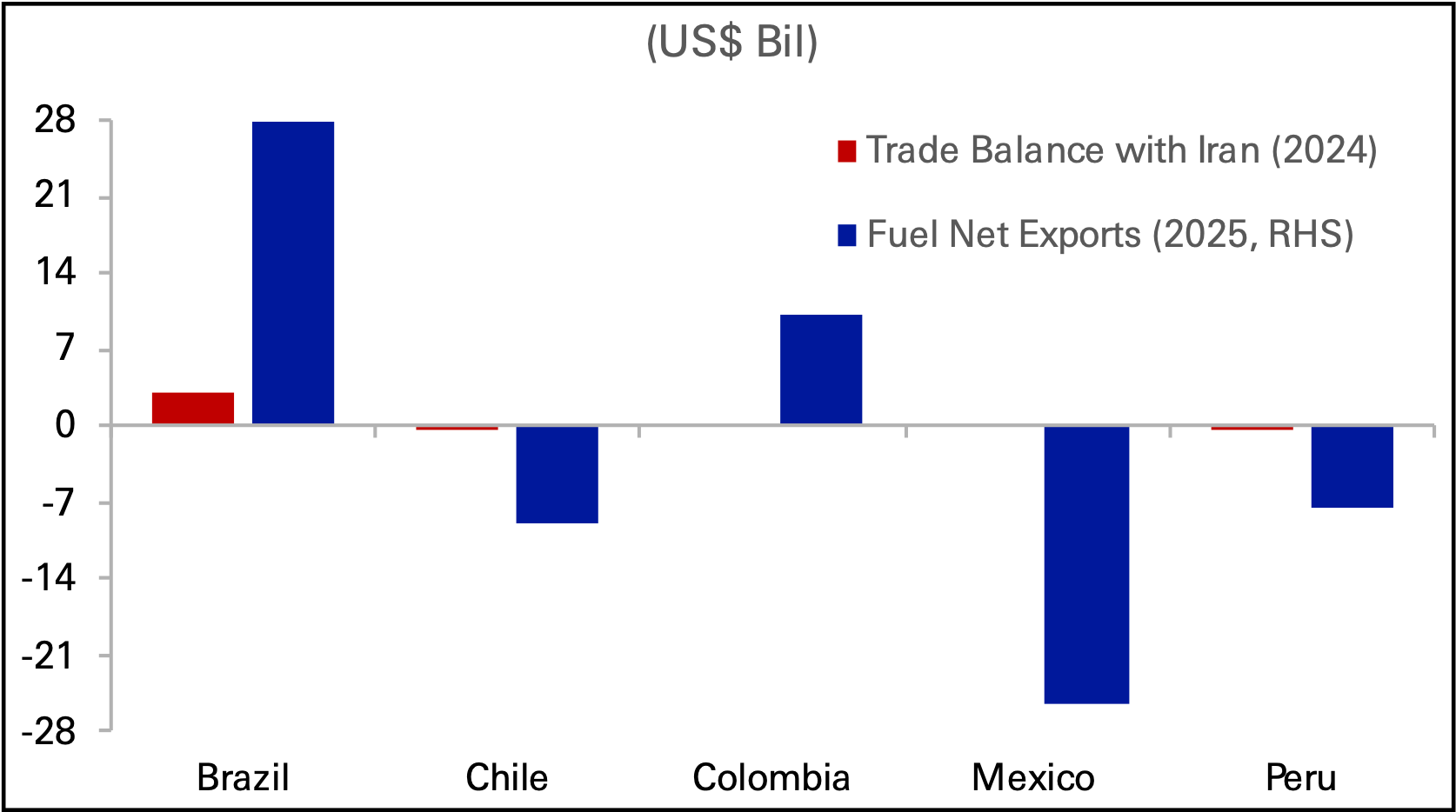

Trade with Iran & Net Fuel Exports

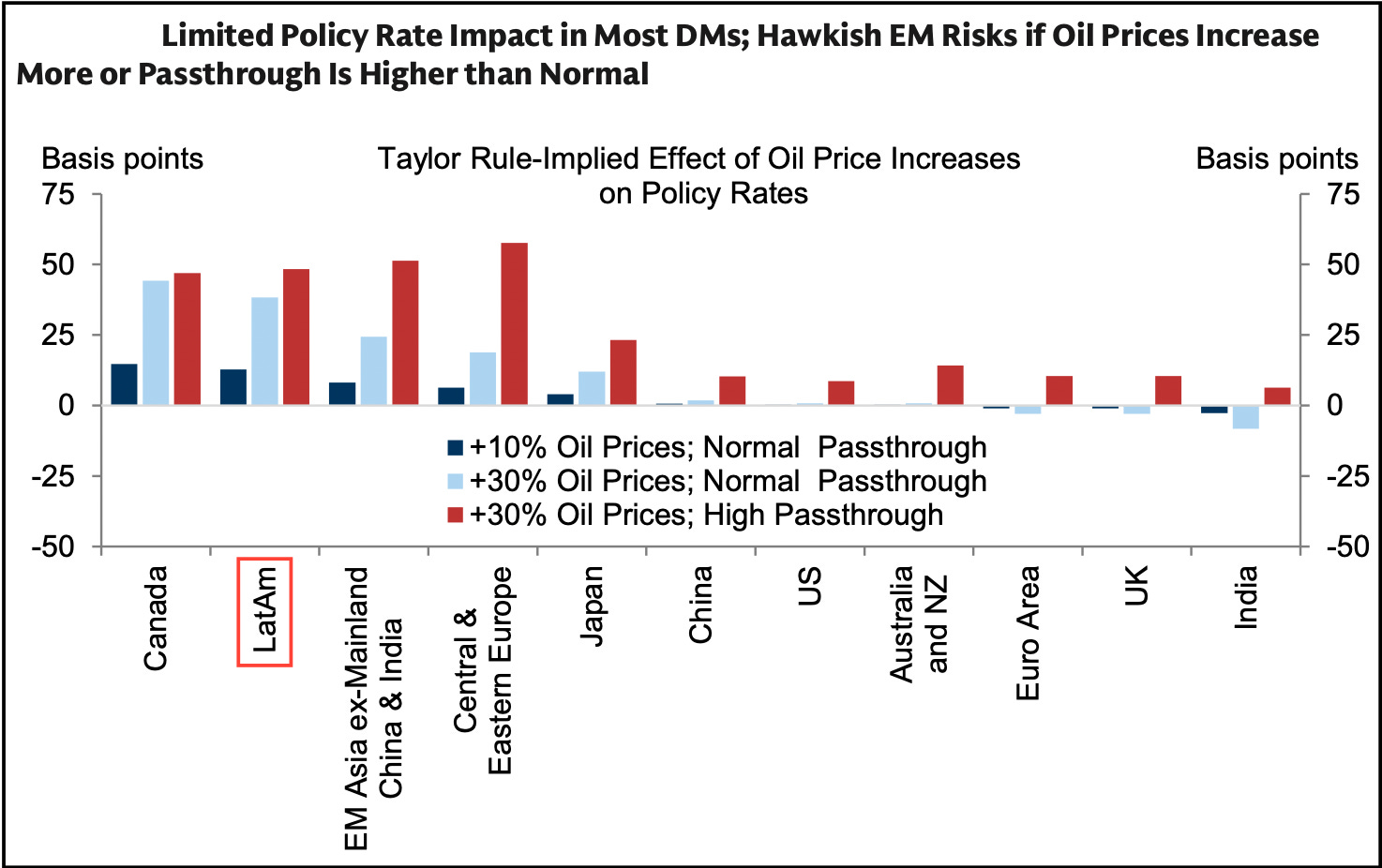

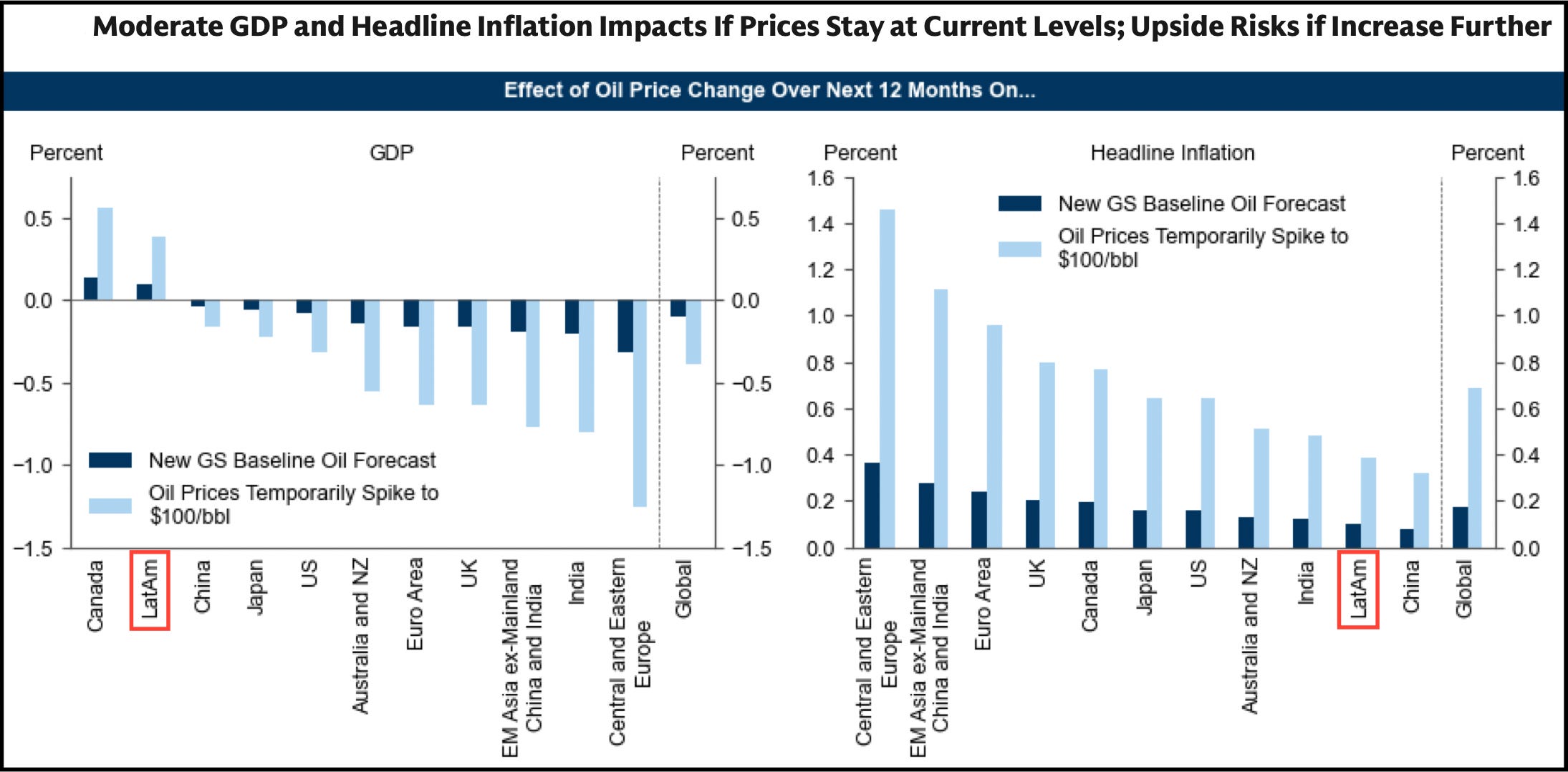

The regional exposure is uneven, but the broader takeaway is clear. LatAm is more sensitive to oil shocks than most developed markets, especially when pass through into local prices is faster than usual. The policy response implied by the data is meaningfully larger than what we see across most developed economies.

Trade with Iran & Fuel Net Exports

Higher oil prices also create a monetary risk for LatAm. The region is more sensitive to oil shocks than most developed markets, especially when pass through into local prices runs high. In that setup, central banks may have less room to ease than markets currently expect.

We believe the growth impact from current oil levels still looks manageable, but inflation is the bigger issue. If oil moves higher from here, the pressure on headline CPI rises more quickly, which increases the chance that policymakers in Brazil, Chile, and Mexico slow or pause their easing cycles.

As you can see in the exhibits above, that would tighten financial conditions at a time when the region was expecting more support from lower rates. Overall, the key point is that the first order effect of higher oil is not only energy. It could also delay monetary easing, and we think that would widen the impact across equities, credit, and domestic demand.

The Aurelion Team

Disclosures & Methodology

Excellent article. I also agree that oil prices won't stay elevated for long

"Forecasting is difficult, especially about the future", (attributed to, among others, Danish physicist Neils Bohr). Reality is Strait not open and no one can say when it will be. There is no clarity except what we see today. Delving into the physical reality, looking at forward price trends, among oil traders there's grudging but growing acknowledgement oil will be higher for longer and $70 bbl looking aspirational, more like a distant dream, a year or more out. The March/April futures shorting trade depressing oil price is no longer working so well. As of May 15, US-government derived intelligence claims Iran has around 70% of the missile capacity and 90% of underground storage and launch capability they had on Day 1. Thirty of 33 missile launch sites along the Strait of Hormuz are operational. If accurate, it's indicative of a group maintaining strategic leverage. They're at the poker table with a strong hand and know it, no reason yet to fold. Tanker owners and shipping insurers are certainly taking that into account. Prices for both are not diminishing anytime soon. For those countries without, strategic oil reserves likely in future plans; and for those with, they'll need refilling. There needs to be an oil glut to get prices down. The World is currently around 1.3 billion barrels down from where we would have been, with the number growing daily. Any way you slice it, the world is missing 10-11 million barrels a day and meaningful supply is not being added as quickly as needed.