Is LatAm's Bull Market Still in Its Early Innings? We Believe It Is

Valuations, flows, and macro trends suggest the cycle is still early

Introduction

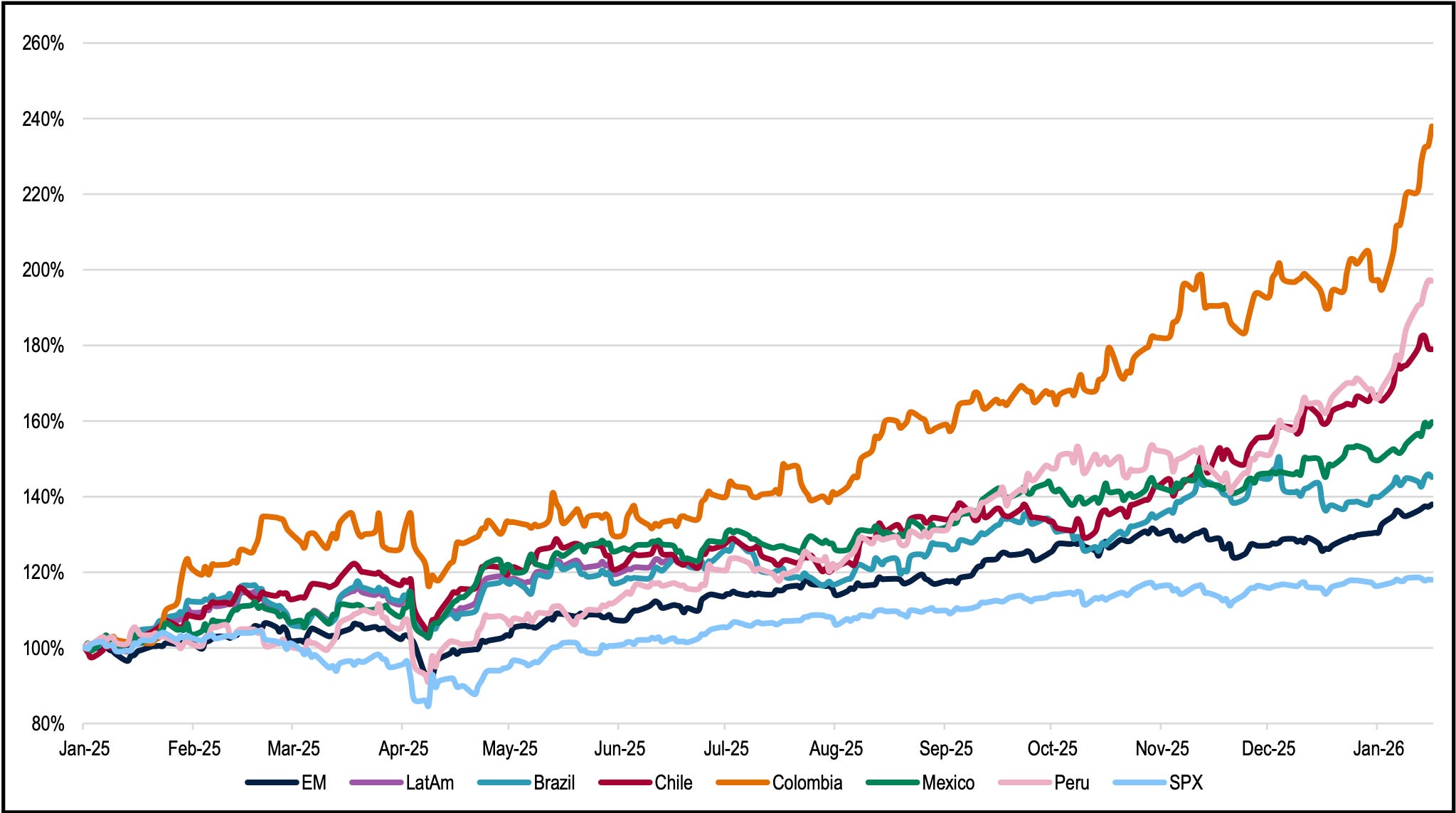

If you follow us on X, you probably already know that we are currently bullish on Latin American equities. Not all of them, but most. So, the goal of this post today is to analyze what is going on in LatAm and what we expect to happen in the future. Let’s start with how LatAm equities have performed since last year. In the chart below, we use country-specific ETFs to get a broad idea of how each country’s stock market has fared.

As you can see in the following chart, Colombia has performed amazingly, skyrocketing ~140%, followed by Chile with a gain of ~80%. More importantly, each has outperformed the S&P 500 by a wide margin. The index is up less than 20% over the same period, and we believe the gap can keep widening.

LatAm Performance since Jan 2025

LatAm markets are typically driven by politics and elections, which means getting the macro outlook correct is essential to avoid treating your portfolio like a lottery ticket. The region is currently poised for a significant political shift in 2026 as illustrated by the changing alignment in the maps below.

Latin America Poised for a 2026 Political Shift

As shown above, Latin America shifted from a largely Right leaning map in 1999 to a broad Left leaning majority by 2023. The areas marked on the 2026 map show where elections are coming up this year, including in key markets like Brazil, Mexico, Colombia, and Peru. We believe this busy election cycle points to higher volatility and another possible shift in the political landscape.

Latin America Strategy: The Second Supercycle

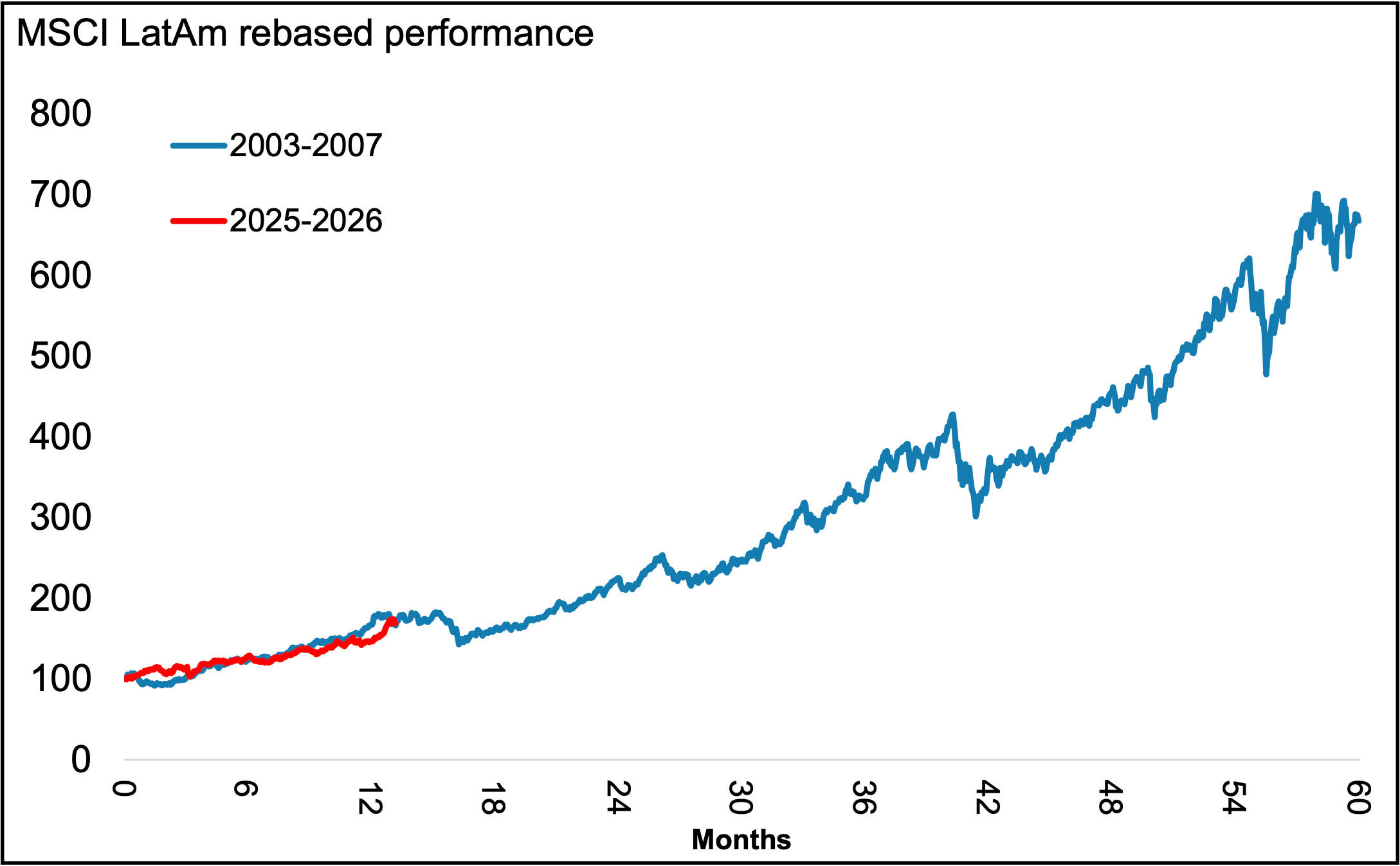

We maintain high conviction that the Latin American bull market remains in its initial stages. The current setup bears a striking resemblance to the cycle of 2003 to 2007 which was catalyzed by the entry of China into the WTO. The MSCI Latin America Index has returned 69% in USD since January 2025.

LatAm Bull Market Still in Early Stages

This performance tracks closely with the 66% gain observed during the first 13 months of the 2003 vintage. That period ultimately delivered a total return of around 570% over four years. We identify a similar catalyst today. The global economy is entering an intensive capital expenditure cycle centered on artificial intelligence. This shift will drive substantial demand for data centers and power generation capacity.

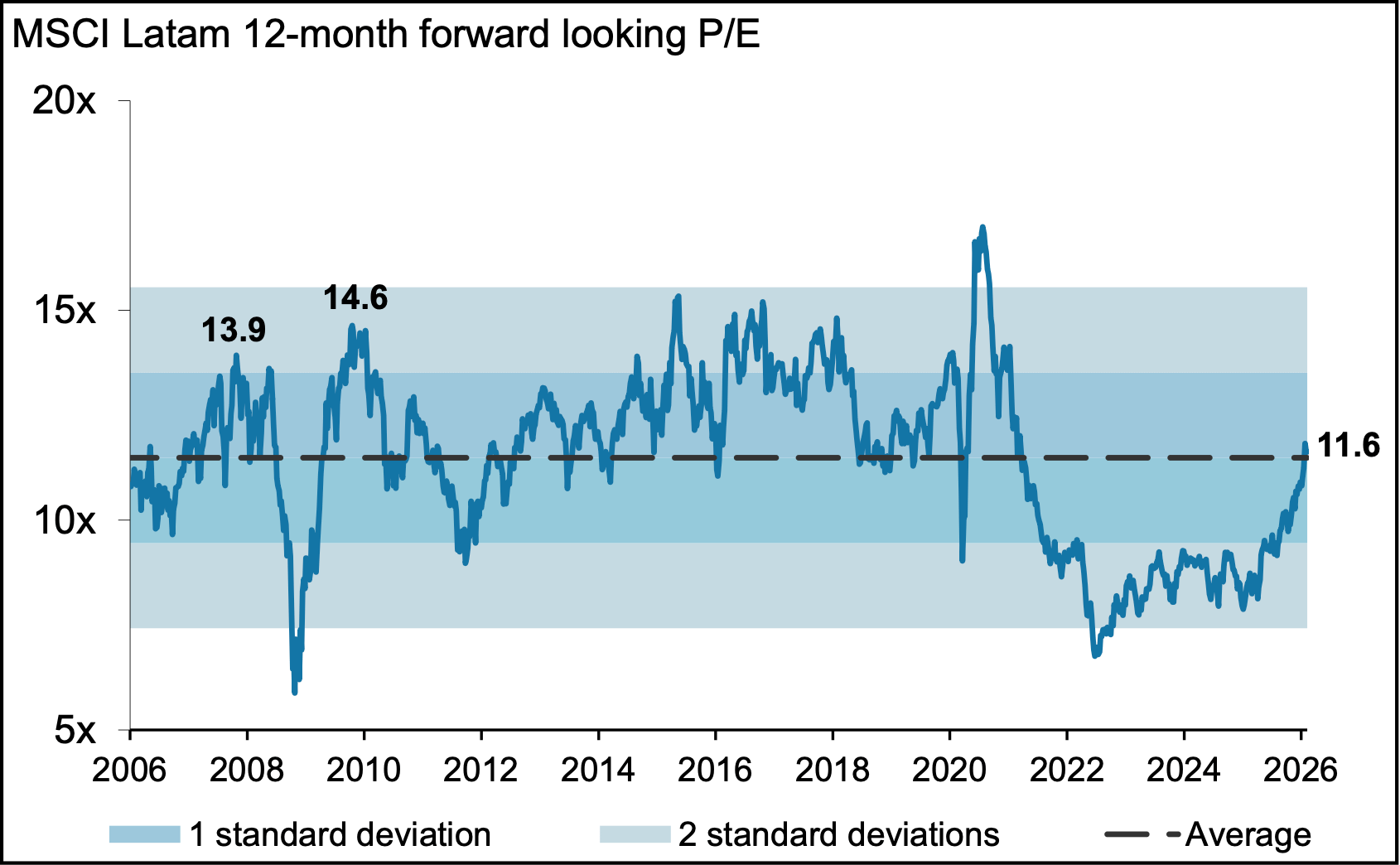

Valuation: Room for Re-Rating

Latin American equities retain significant scope for multiple expansion. The region currently trades at 11.6x forward earnings which aligns with the long term historical average. The previous major bull cycle of 2006 and 2007 saw valuations peak at 14x and subsequently reach nearly 15x in late 2009.

Morgan Stanley projects that Latin American equities could return to a 14x multiple by 2030. This re-rating is driven by a trifecta of catalysts including rapidly evolving geopolitics, the normalization of global interest rates, and pivotal elections across the region.

LatAm Valuations Near Historical Average

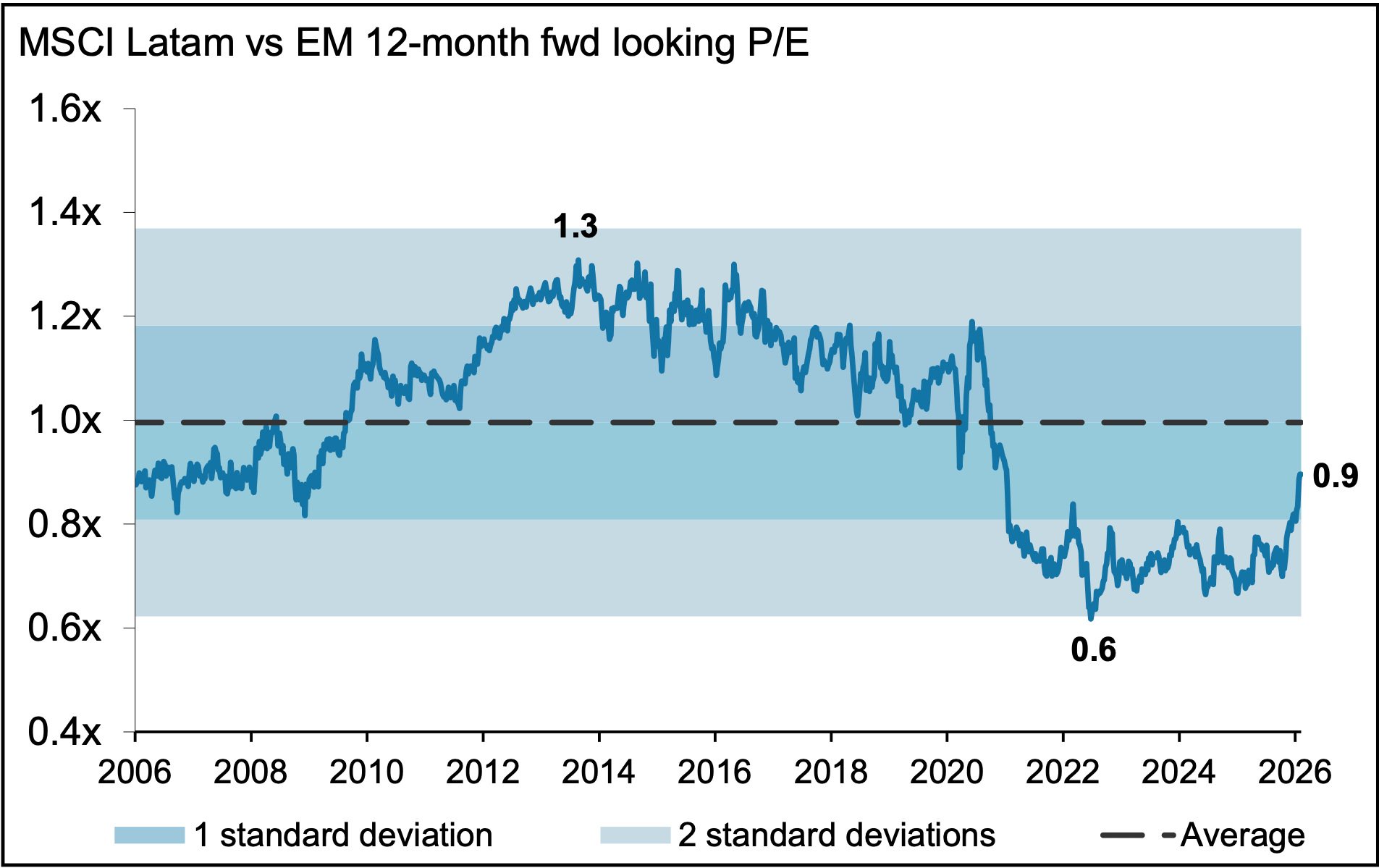

We believe the re-rating should occur relative to Emerging Markets and has already commenced. Latin American stocks currently trade at 0.9x their EM peers which is 0.5 standard deviations below the 20 year historical average. We note that for the majority of the 2010 to 2020 decade LatAm traded at a premium to EM and peaked at 1.3x in 2013.

LatAm Trades at a Discount to EM Peers

Global Flows: The Great Rotation

We are hearing from many hedge fund and asset managers in the US and Canada that they are finally positioning for Emerging Markets and specifically Latin America. They are arguably late to the party as usual. However the data confirms the trend. There has been a surge of interest as global funds have closed their underweight in Emerging Markets after nearly a decade.

Global Fund Flows Into EM Markets

We believe this rotation has further room to go and Latin America should be a top beneficiary. For reference global funds relative positioning in EM peaked at around 500 basis points overweight in 2002.

Local Flows: The Sleeping Giant

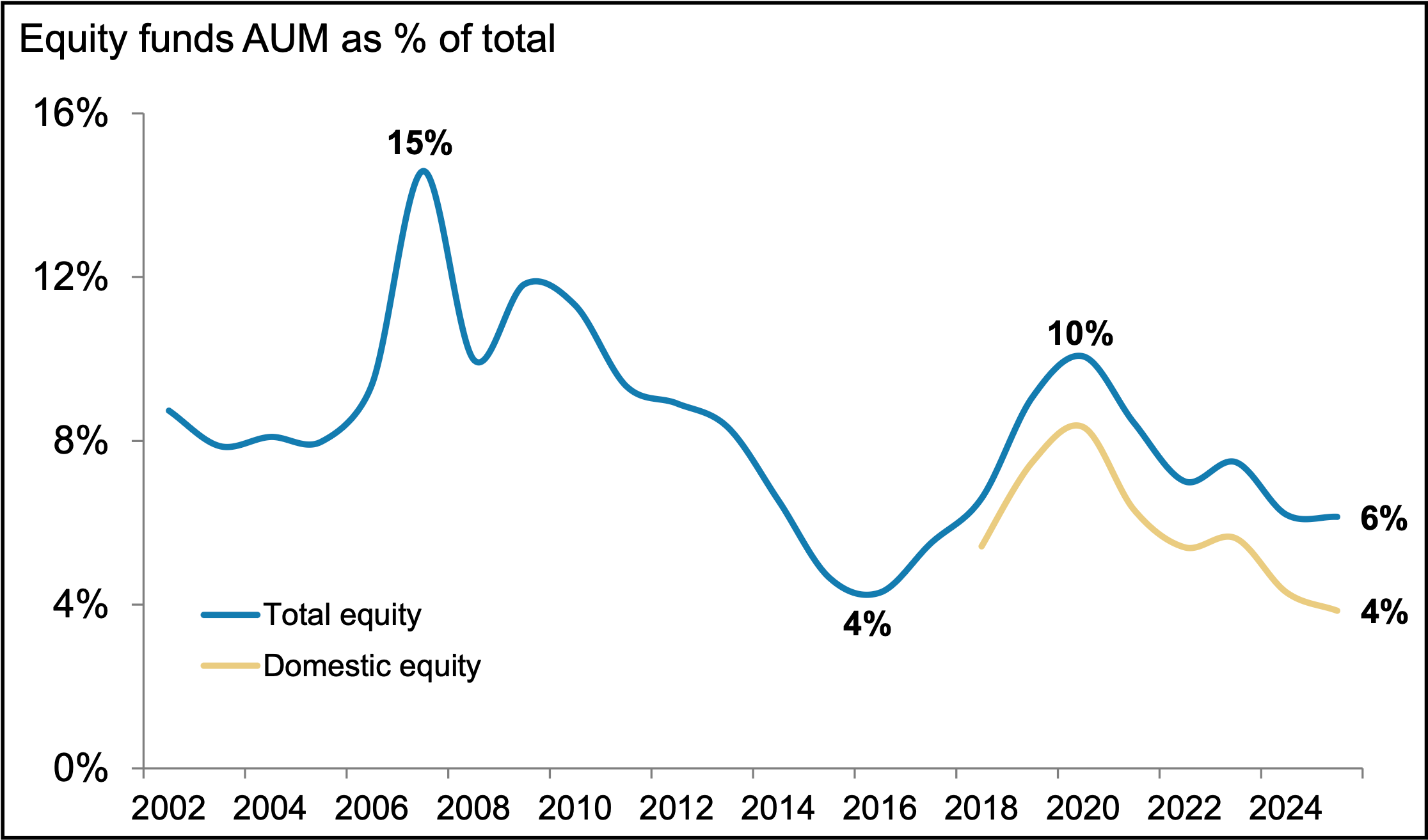

Domestic investors are missing the start of this cycle just as they did in the early stages of the 2003 to 2007 bull market. Current allocation to local equity funds sits at a depressed 6% of total industry assets.

Brazil Equity Fund AUM Remains Below 2003–2007 Levels

That figure drops to just 4% if we exclude international mandates. We recall that domestic allocation averaged 8% during the accumulation phase of 2003 to 2006 before surging to 15% in 2007. We also highlight that Latin America has become a negligible component of the global benchmark.

LatAm Represents ~8% of MSCI EM, Well Below 2008 Peak

The region currently holds an 8% weight in the MSCI Emerging Markets Index versus the 25% peak observed in 2008. This historical gap implies a massive runway for Brazil to regain relevance in global portfolios.

Brazil Is Our Top Pick

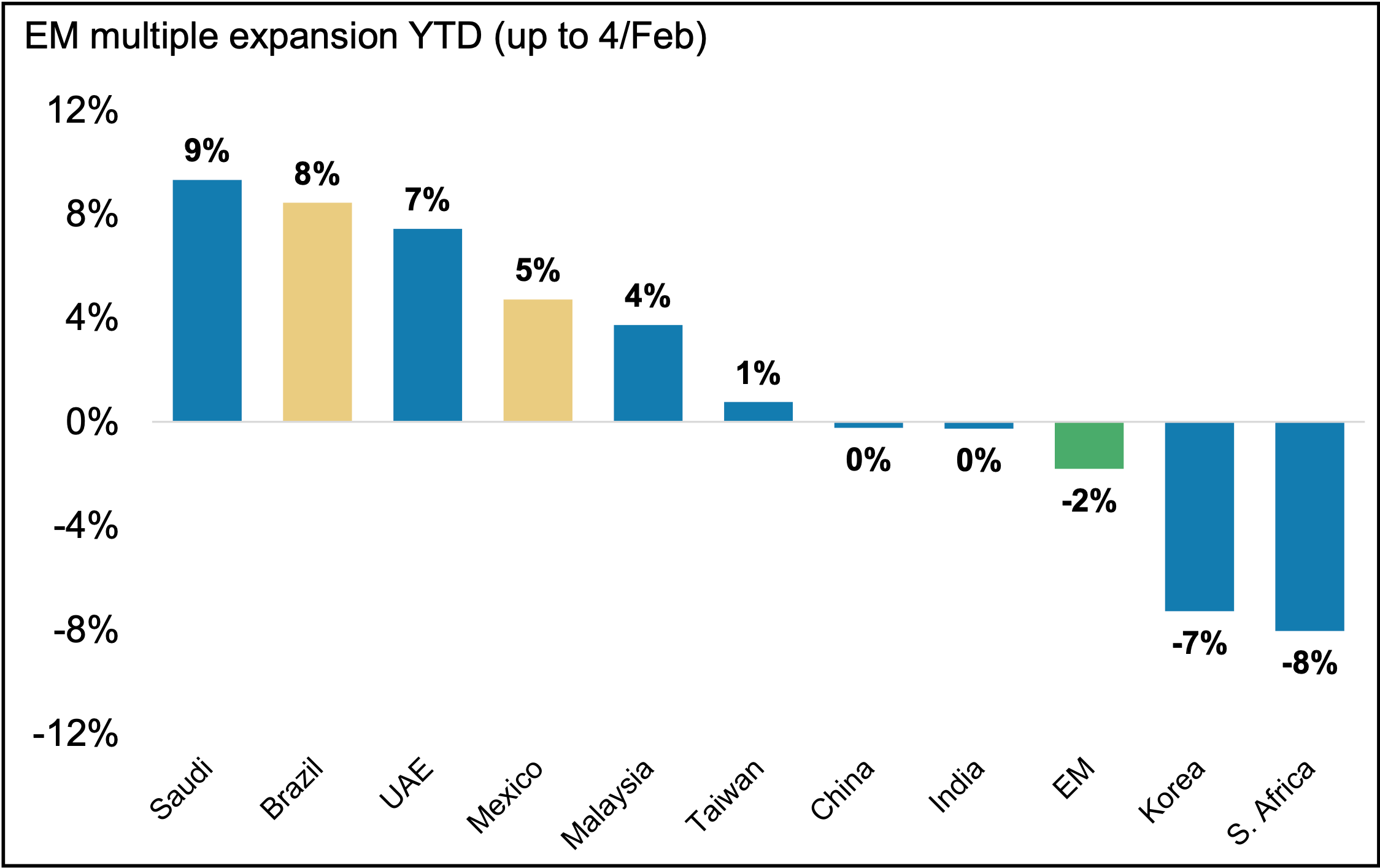

Brazil remains our preferred market in the region and has outperformed year to date. While a weaker USD typically benefits risk assets across the board we argue that the current move is idiosyncratic. Brazil has expanded its multiple more than peers during this early year rally and ranks second among the ten largest markets in the MSCI EM index while Mexico ranks fourth.

Brazil Outperforms LatAm Peers on Re-Rating YTD

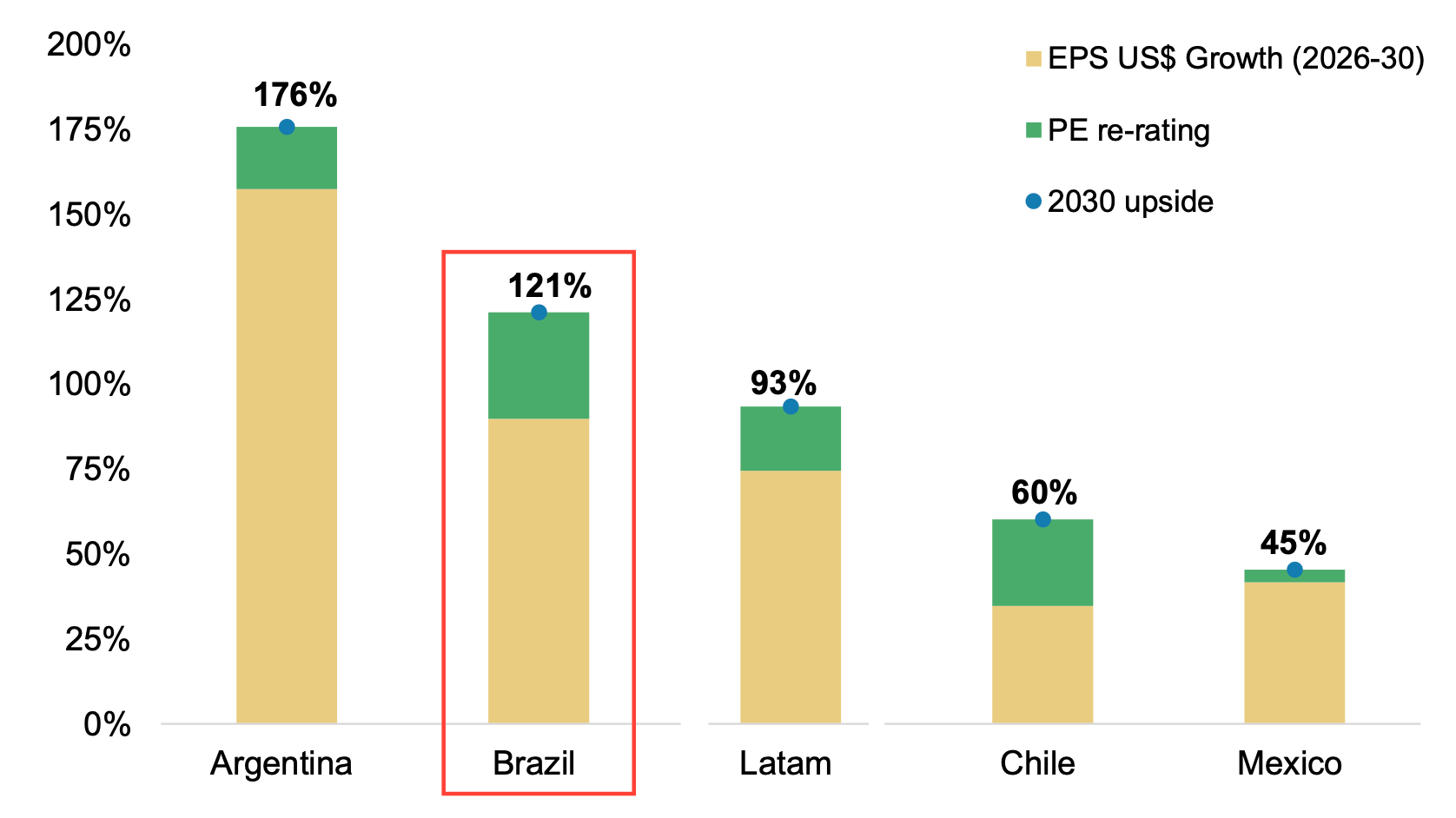

This preference is backed by significant upside potential. According to Morgan Stanley’s analysis of regional equity gains, Brazil offers a 121% total upside through 2030. This growth is largely driven by EPS expansion, which accounts for roughly 80% of projected gains, while multiple re-rating contributes the remaining 20%. While Argentina offers a higher absolute potential of 176%, we believe the inherent stability of the Brazilian market makes it the preferred play for consistent alpha.

MSCI Latin America: 2030 Spring Scenario Index Upside

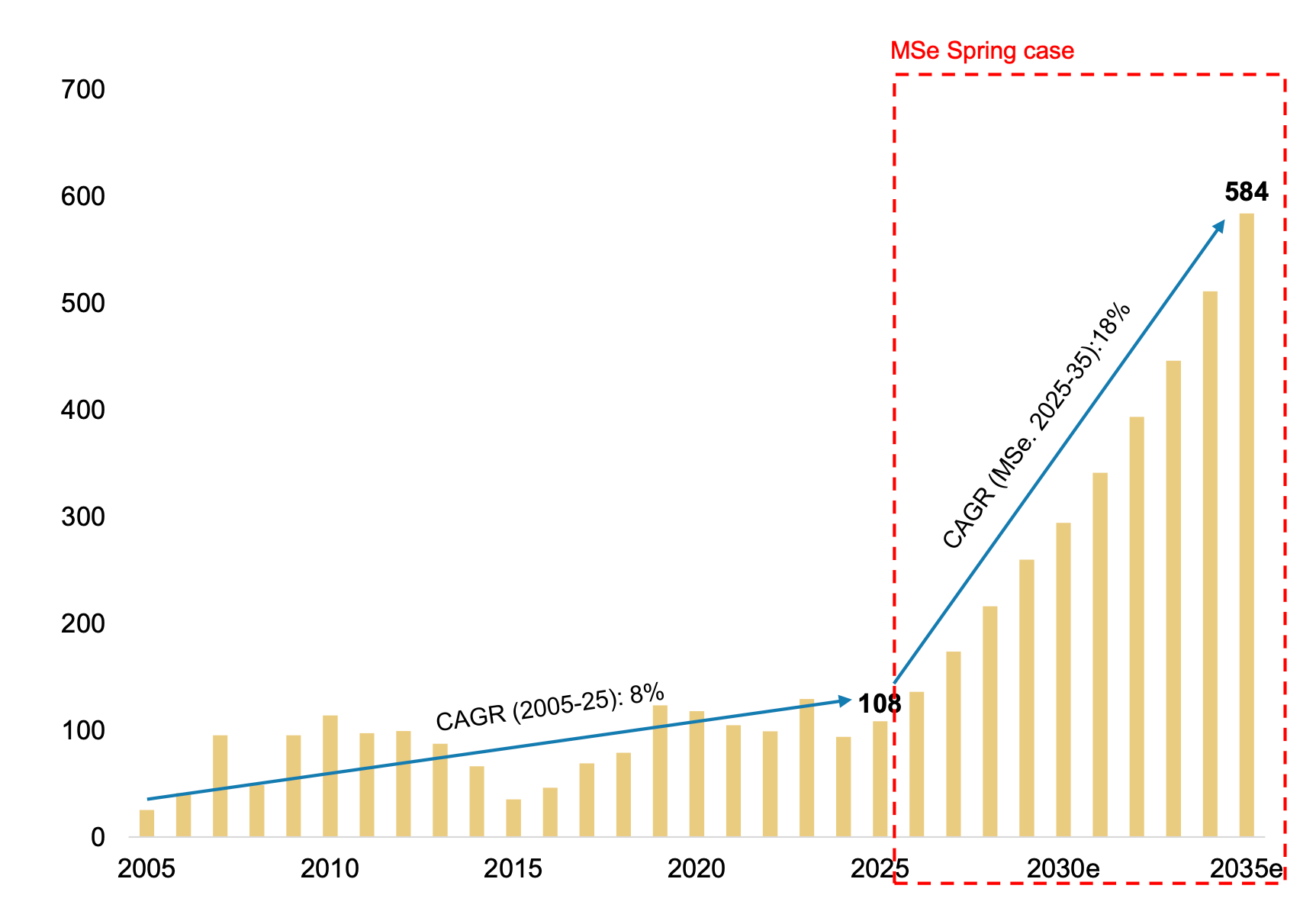

In a bullish spring case scenario, domestic Brazilian equity funds are projected to increase their AUM by ~6x by 2035. This represents a move from $100B to ~$584B, reflecting an 18% CAGR over the next decade. The surge in domestic participation would significantly deepen the market, far exceeding the 8% CAGR observed between 2005 and 2025.

Brazil Equity Funds: Spring Case AUM (US$ bn)

However, the macro thesis is not without challenges. Significant fiscal consolidation is required. We estimate that fiscal cuts equivalent to 3.4% points of GDP are necessary to stabilize the debt-to-GDP ratio. We believe investors should be aware that reversing these dynamics will likely be a prolonged process extending beyond a five-year horizon.

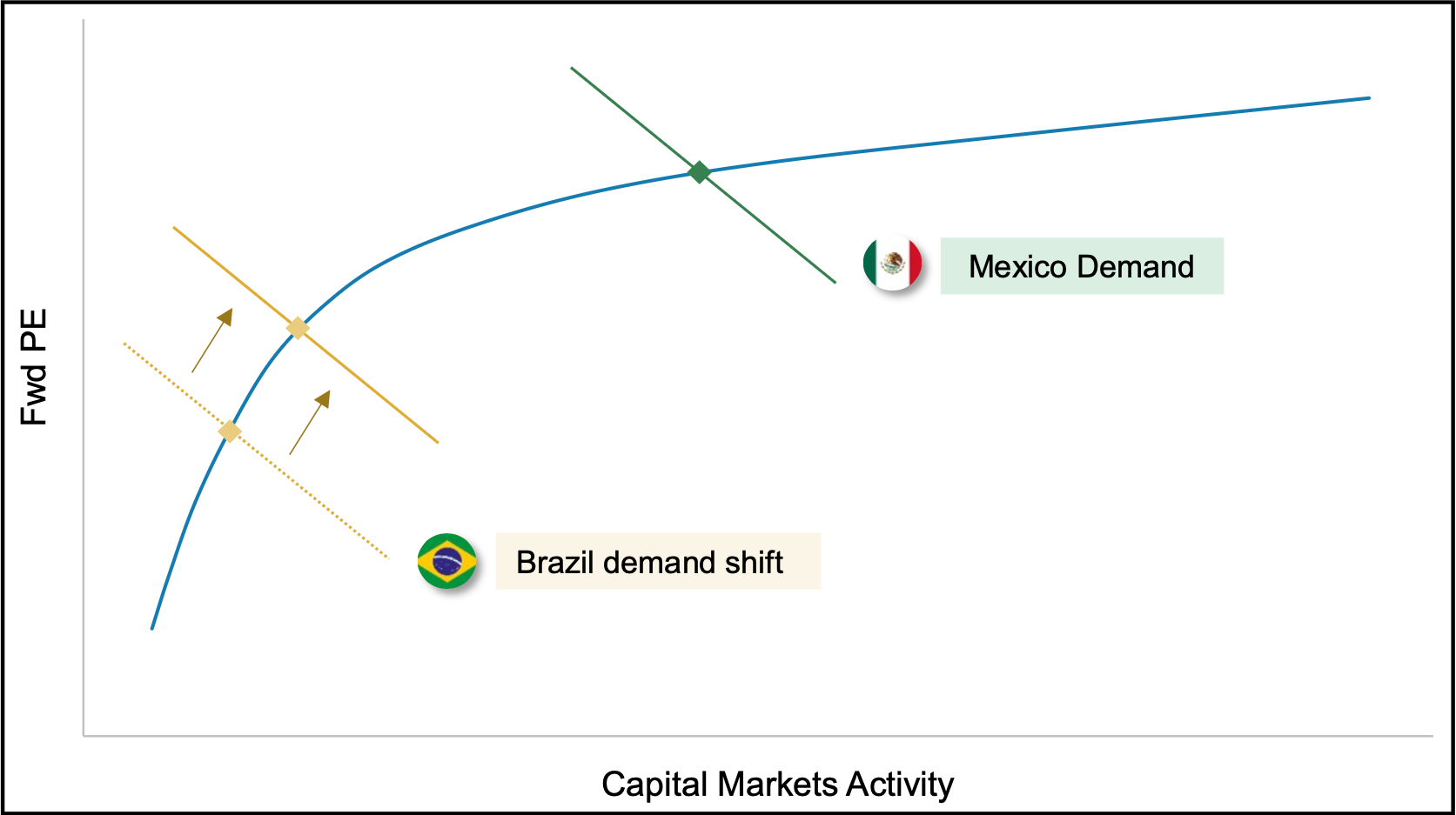

We are looking at a supply and demand setup that suggests Brazil has significantly further upside. The argument is centered on our unique supply curve proxy for LatAm equity which indicates we are currently sitting on the borderline vertical part of the curve. We believe this positioning is crucial because it means that any incoming demand shock would not just result in a gradual increase but could also cause a sharp “pop” in Brazilian equities as valuations expand and the risk premium compresses.

LatAm Equities: Supply vs Demand

When we analyze what could actually trigger this demand shock we identify three distinct catalysts that are either already occurring or imminent. The most significant factor is the higher probability of a policy shift that moves Brazil into a structural Bull Case. Alongside that political angle we have the monetary driver where peak interest rates and the start of a new easing cycle expected in March will force a rebalancing of Brazilian portfolios.

Finally we expect a broader reallocation of capital into emerging markets as global investors look to recalibrate and diversify their holdings.

Below, we show how LatAm valuations line up with capital markets activity.

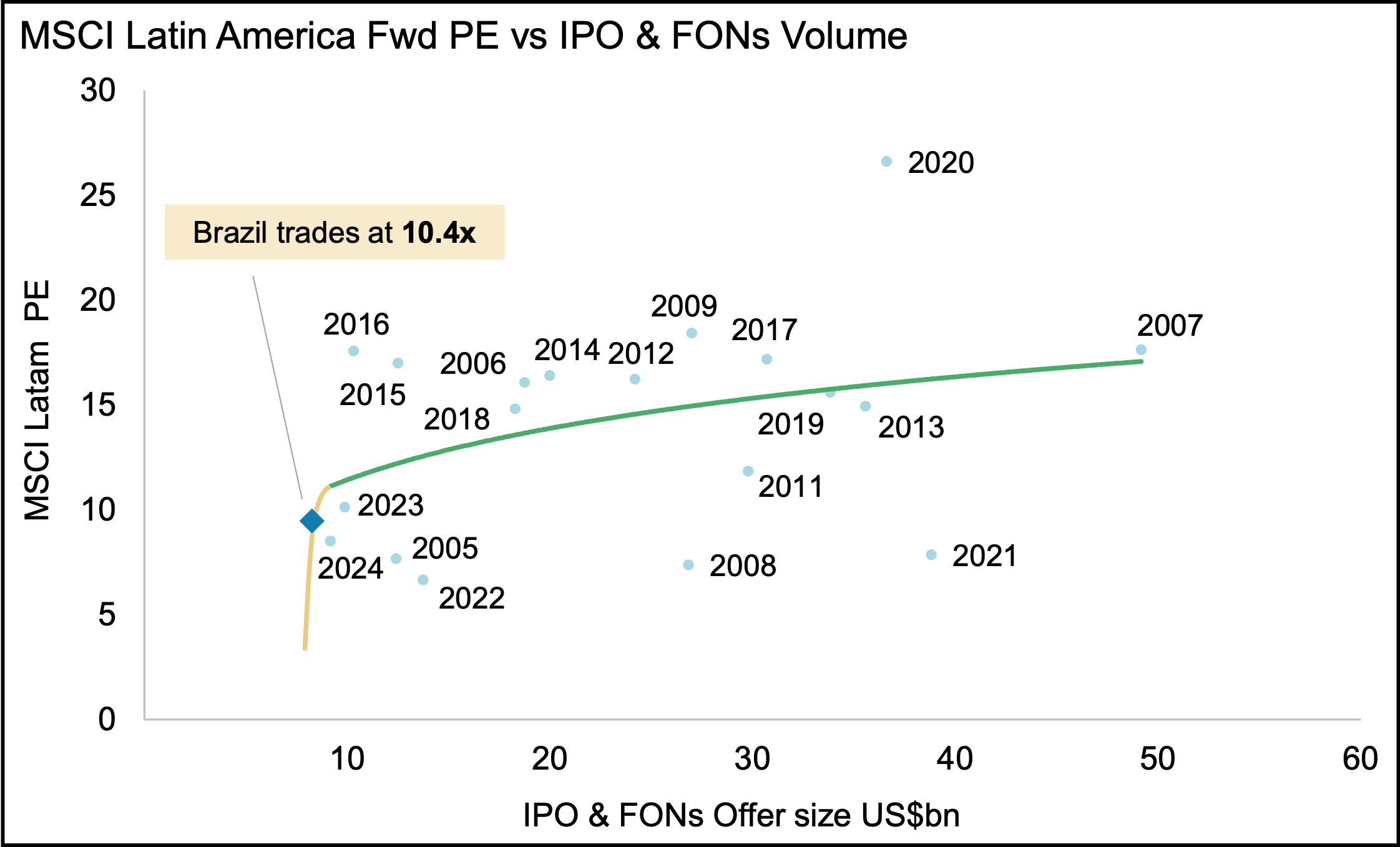

We are sitting in the vertical portion of this supply curve with Brazilian equities trading at around 10.4x forward earnings. At these depressed levels there is virtually no incentive for companies to issue new shares, meaning supply is effectively capped. This setup creates a powerful dynamic where any new demand cannot be met with new shares, which forces prices higher.

We believe this lack of supply will trigger a sharp jump toward a 12x multiple before IPOs return and market supply returns to normal, which aligns perfectly with our 2026 base case.

Supply Curve of Latin American Equities

The Path to 3% Inflation

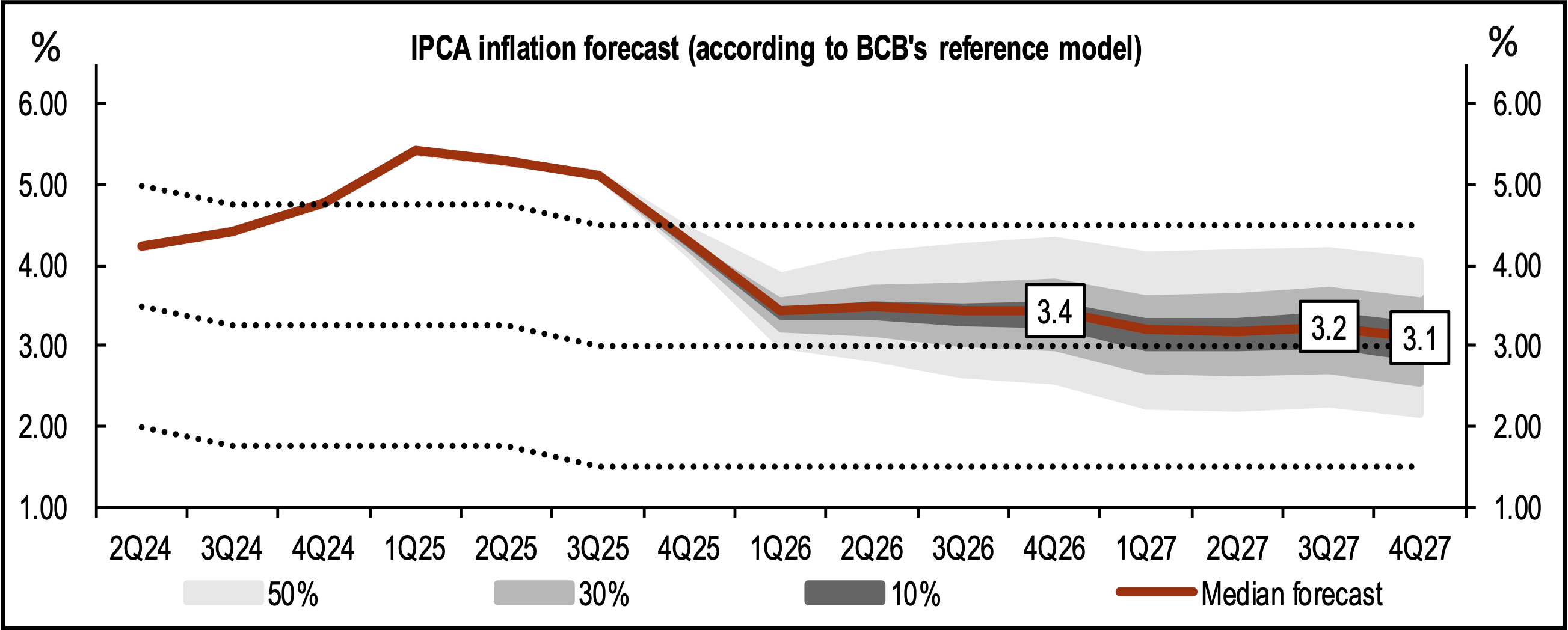

When investing in a country, we always look for inflation forecasts that are coming down or at least stable. This is exactly what we see in Brazil, which makes us like the setup even more. While the market was disappointed that rate cuts didn’t kick off in January, the driver here is actually quite constructive. The economy simply refused to slow down. Instead of hitting a wall in late 2025, we saw activity reaccelerate with PMIs pushing higher.

We saw some noise from currency volatility and oil prices, but the trend in the chart below tells the real story. Inflation forecasts are steadily grinding down toward the 3% range. This confirms that the move to the target is intact, driven by a resilient economy. We believe the path to 3% is clear, and this should provide the green light for easing cycle to finally begin in March.

Inflation Expected to Stay Stable

Inflation forecasts are steadily falling toward the 3% range. This confirms that the move to the target is intact, driven by a resilient economy instead of a collapsing one. We believe the path to 3% is locked in and this should provide the green light for the easing cycle to finally begin in March.

Next, we look at how rate cuts could extend the rally.

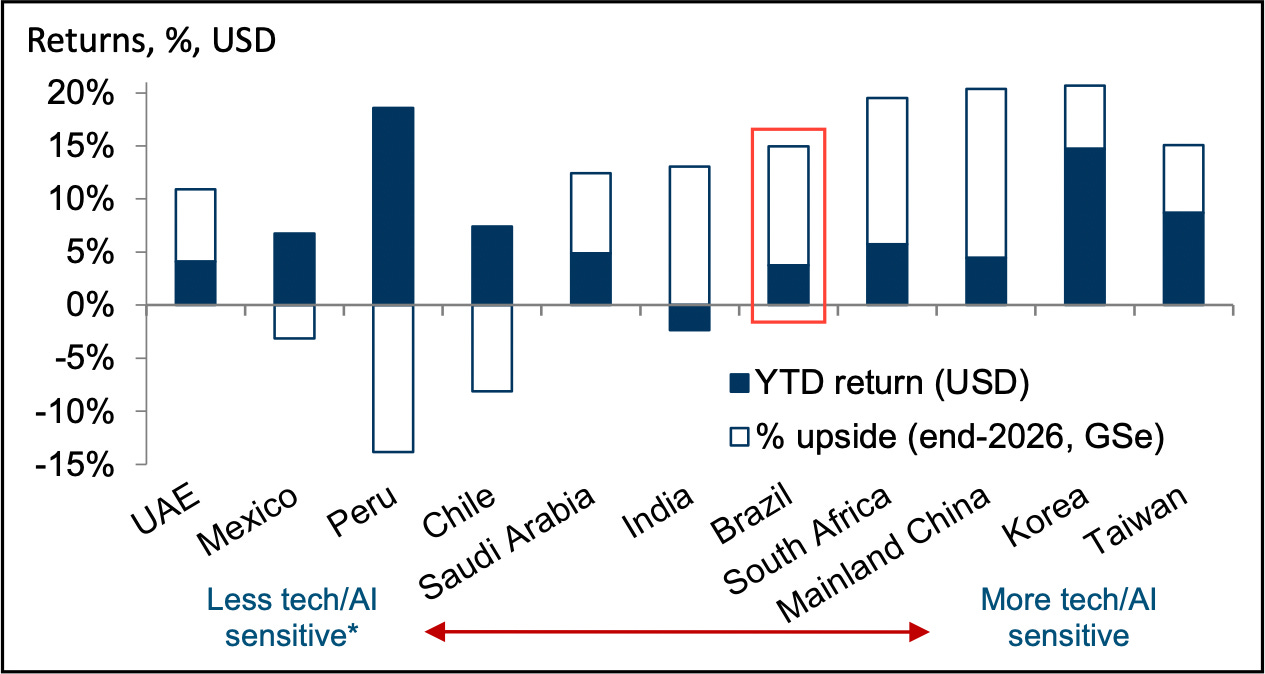

As the chart illustrates, Brazil is significantly more sensitive to the Tech and AI narrative than markets like Peru or Chile. However, the most compelling takeaway here is the potential for future returns. Goldman Sachs projects a strong upside for Brazil through the end of 2026, and with rate cuts expected to drive these further gains, we really like how that setup is looking.

EM: A Broad-Based Rally This Year

Another key element reinforcing our bullish stance on Brazil is the significant reduction in country risk. We monitor this through 5-year Credit Default Swaps (CDS), and the chart below highlights a very encouraging trend.

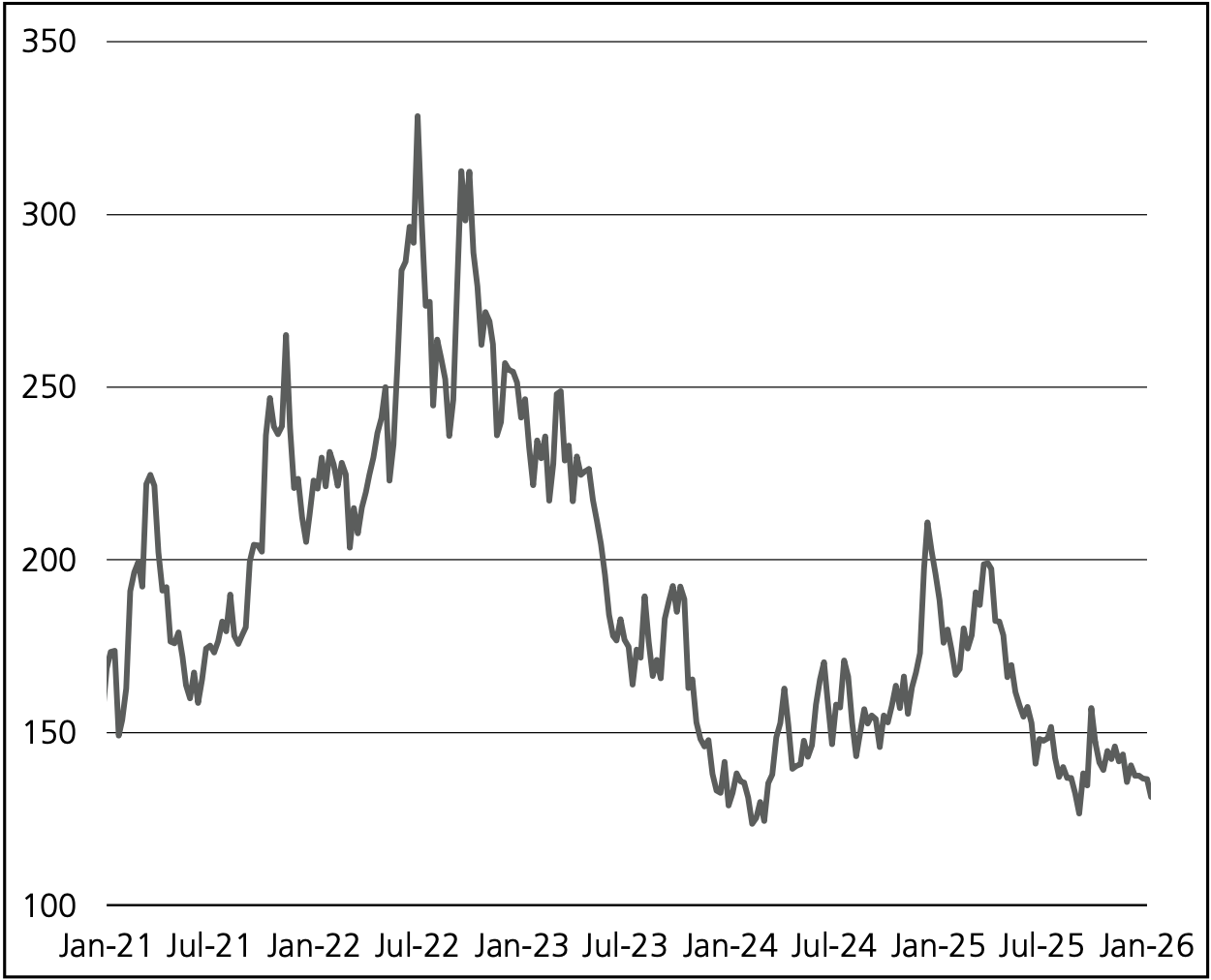

Brazil 5 Year CDS (bps)

After peaking above 300 basis points during the instability of 2022, Brazil’s risk premium has steadily evaporated and is now hovering near multi-year lows around 130 basis points. This collapse in perceived risk indicates that the market is pricing in far greater economic stability, which effectively lowers the cost of capital and invites further foreign investment into the region.

Brazil Macro Picture

Before being sure we are betting on the right horse, it is essential to evaluate Brazil’s current macro environment, specifically interest rates, the economic cycle, and the political landscape. The October 2026 elections present clear optionality for regime change. However, the opposition still lacks a unified candidate capable of seriously challenging President Lula.

Consequently, we view his re-election as the base case. While the left is consolidated behind President Lula’s bid for re-election, the right remains fractured. Currently, Flavio Bolsonaro is the only prominent candidate on the right, though others are likely to join. The situation will only clarify once the candidate field is defined, which should occur by early April at the latest.

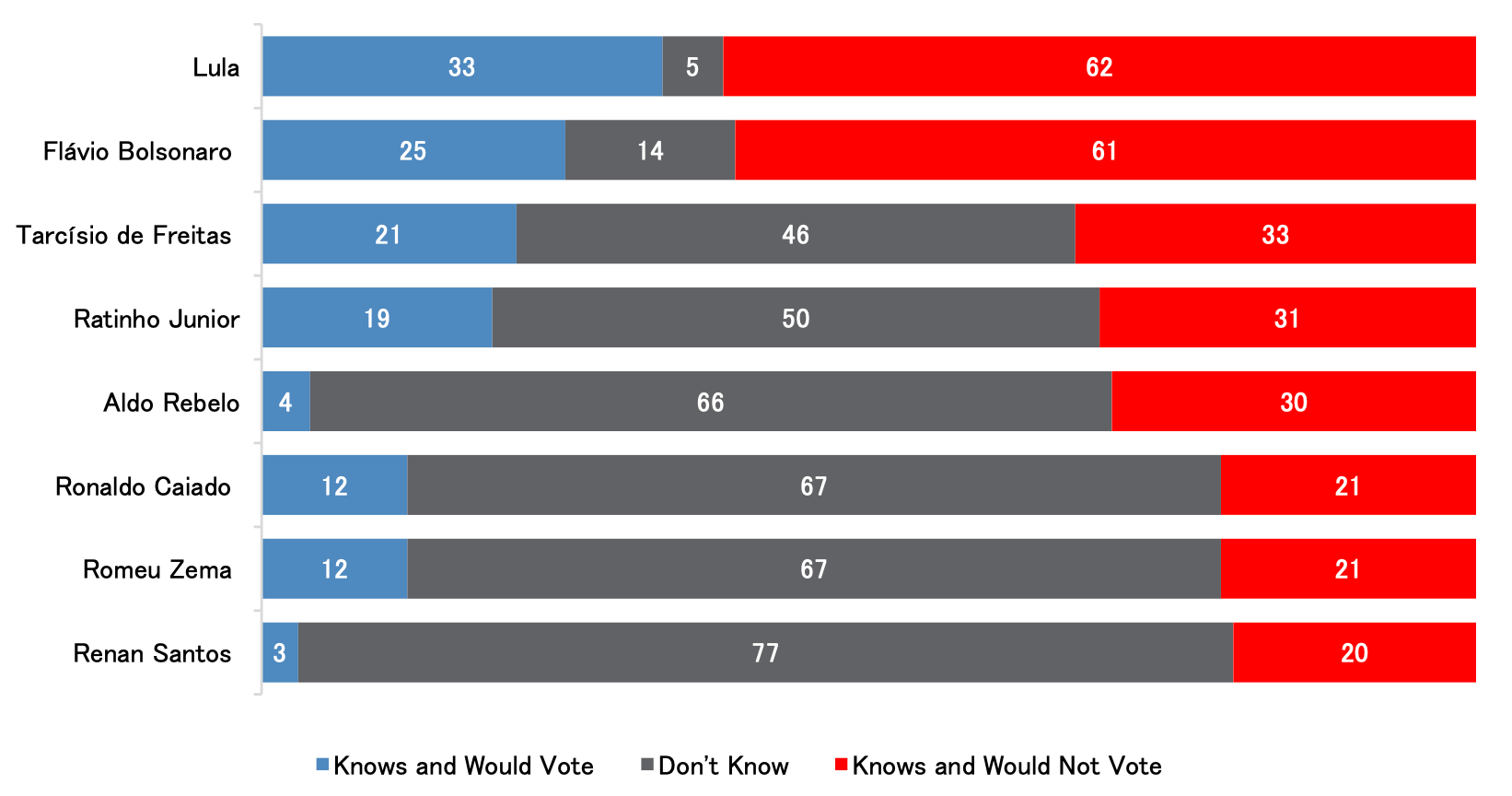

To ground this view, we turn to J.P. Morgan estimates. As illustrated below, current polls show President Lula leading in voting intention across every scenario. Outside the Bolsonaro family, he maintains the highest level of support, while the opposition remains fragmented and largely undefined.

Brazil: Voting Potential & Rejection Rates by Candidate (Jan 2026)

The chart confirms that President Lula leads voting intentions across every scenario. He commands the highest share of voters who know him and are ready to support him. While his rejection rate remains elevated, no alternative candidate currently matches his combination of support and national recognition. Outside the Bolsonaro family, the opposition remains fragmented. The high number of voters who are unfamiliar with the other names signals that the field has limited consolidation at this stage.

The Fiscal Reality

We believe government decisions on fiscal policy will be the ultimate differentiator for the economy in the coming years. While fiscal performance has recently topped expectations, it was driven by resilient growth and tax revenue instead of actual spending cuts. This is why the market is demanding such a high premium to hold Brazilian assets.

There is a real concern that without further fiscal consolidation, current growth levels are not sustainable. If these dynamics don’t shift, the debt trajectory becomes difficult to justify. Even under a base case scenario, we do not see the debt-to-GDP ratio stabilizing within the next decade.

However, it is important to note that the growth of this debt is not expected to be explosive. In a low growth environment, stabilization would require long term interest rates to stay near 6% nominal. For the math to work in a high interest rate environment, we would need to see GDP growth reach at least 3%. Essentially, it will take a massive effort involving savings of over 12% of GDP through reforms to put the country on a truly credible fiscal path.

Our Final Take on Brazil

We are heavily overweight Brazil for a few simple reasons. First, the political landscape is shifting. As the 2026 election cycle heats up, we see the potential for a move toward the center that could significantly reduce the risk premium currently baked into asset prices.

Second, the supply and demand setup is undeniable. Valuations are sitting at a point on the supply curve where sellers have exhausted themselves. There is virtually no new issuance coming to market, which means any incremental demand has nowhere to go but into price. We believe this lack of supply will drive a sharp re-rating higher long before we see IPOs return.

Finally, the macro outlook is turning in our favor. Inflation is steadily falling toward the 3% target and the economy has proven far more resilient than the bears expected. This stability gives the central bank the green light to finally begin its easing cycle in March. When you combine falling rates with a 121% projected upside through 2030, largely driven by earnings growth instead of multiple expansion, Brazil offers the best risk-adjusted return in the region.

We are buyers here and expect the market to wake up to this reality soon, and we believe the rally has a lot of room to run.

The Aurelion Team

Disclosures & Methodology

Excellent piece. Good to see Brazil being the "talk of the town" for all the right reasons! Thank you.

That JP Morgan chart sucks, FYI. It says left leaning but shows all red, then right leaning is blue. Lol, have they ever paid attention to a political ad?