Copper: Supply Tension Lifts the Red Metal

Aurelion Research — Macro Strategy Note | October 2025

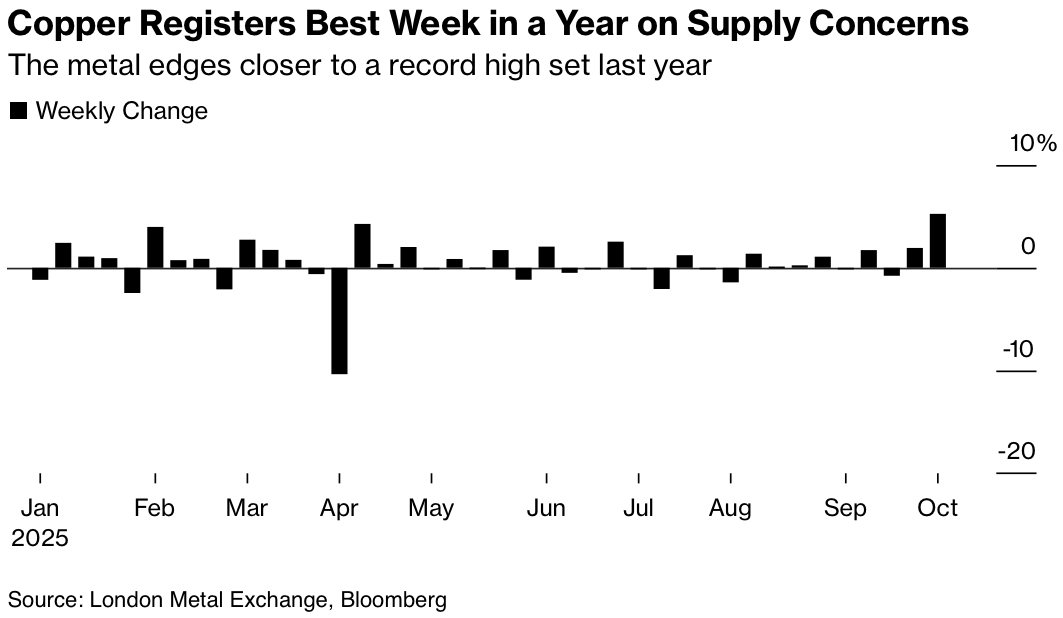

Copper has regained attention across global markets. Prices have climbed more than 20 percent this year and are approaching last year’s record high. Three-month futures on the LME ended the week at about US$10,700 per ton, the strongest weekly advance in a year. Supply interruptions, a softer U.S. dollar, and improving sentiment around long-term industrial use have all supported the rally, especially with investment rising in electrification and data infrastructure.

The latest advance has come on the back of a series of supply disruptions. Freeport-McMoRan’s force majeure at Grasberg, the world’s second-largest copper mine, has removed a major source of output after heavy flooding earlier this year.

Production in Chile, Peru, and the Democratic Republic of Congo has also been affected by weather events and labor disputes, keeping inventories under pressure and reinforcing expectations of a tighter market through year-end.

Easier monetary conditions have added another layer of support. The FED shift toward rate cuts has weakened the dollar and revived investor interest in cyclical assets. Copper now sits at the crossroads of reflation, infrastructure investment, and structural energy demand, giving the rally a broad base of financial and industrial momentum.

Supply Still Leads the Market

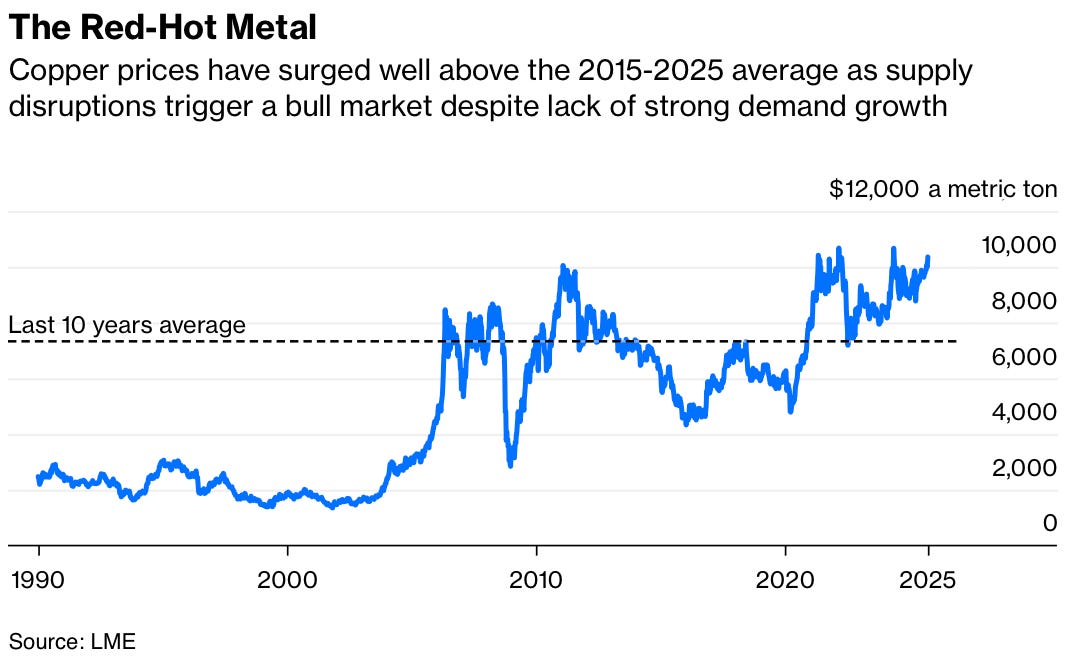

Prices remain well above the ten-year average as supply constraints continue to shape the market. Demand growth has been steady but limited, with Chinese construction still subdued and export orders uneven. The Shanghai premium, a useful gauge of physical buying, hovers near US$50 per ton, just under its 2020–2025 average. Overall, trading conditions point to a market that is firm but contained.

The longer-term outlook for copper continues to be supported by electrification, renewable power, and grid investment. These structural trends remain in place but will unfold gradually over the coming years. Price strength today is driven mainly by supply constraints, with little evidence of stronger industrial demand.

China Shapes the Outlook

China remains the main driver of global copper demand, accounting for about half of total consumption. The rest comes from Europe, the United States, Japan, and several other regions. Domestic construction has weakened, manufacturing activity is uneven, and export volumes remain under pressure, which together have kept buying interest subdued in recent months.

Policy choices in Beijing will set the tone for the next stage of the market. Broader support for construction, renewable energy, or electric-vehicle infrastructure would translate into a faster pickup in consumption. For now, demand remains stable, and prices continue to respond mainly to developments on the supply side.

Aurelion Research View

We see copper’s performance this year as the result of tight supply and shifting policy conditions across key markets. Production setbacks have shown how limited output flexibility remains in major mining regions, while easier U.S. monetary policy has improved liquidity and encouraged broader participation in commodities.

In our view, prices should stay firm through the remainder of the year, supported by low inventories and ongoing supply constraints. A lasting move above US$11,000 per ton would require stronger industrial demand from Asia, led by a clearer pickup in Chinese consumption.

We continue to regard copper as a key indicator of global economic momentum and an essential material for the long-term transition toward electrification and renewable infrastructure.