Chemical Rebound Begins: What LYB Q3 Signals for Huntsman

Early signs of stabilization and margin recovery across the sector.

LyondellBasell reported its third-quarter 2025 results this Friday, delivering earnings that exceeded market expectations. LYB showed progress in cost control, operational reliability, and early signs of stronger demand in polyethylene and intermediates.

We believe these results confirm that the chemical sector is beginning to recover after a long downturn. Profitability is improving as companies focus on efficiency, capital discipline, and targeted growth.

For Huntsman, this is an encouraging sign. We hold the stock in the Aurelion Index and covered it in depth earlier this year, seeing it as one of the best positioned names for a cyclical recovery in chemicals.

The same forces driving LYB 0.00%↑ rebound, including firmer margins, a more focused portfolio, and improving demand, are starting to support HUN 0.00%↑ as well and point to a more positive outlook for 2026.

Market Environment & Demand Context

LYB reported that demand is still weak in most end markets in Europe and North America, especially in construction and automotive. Packaging and healthcare remain more stable, and polyethylene demand is starting to level off.

In the United States, polyethylene sales are beginning to recover after two years of decline, while in Europe, demand has grown about 3 percent since the start of the year.

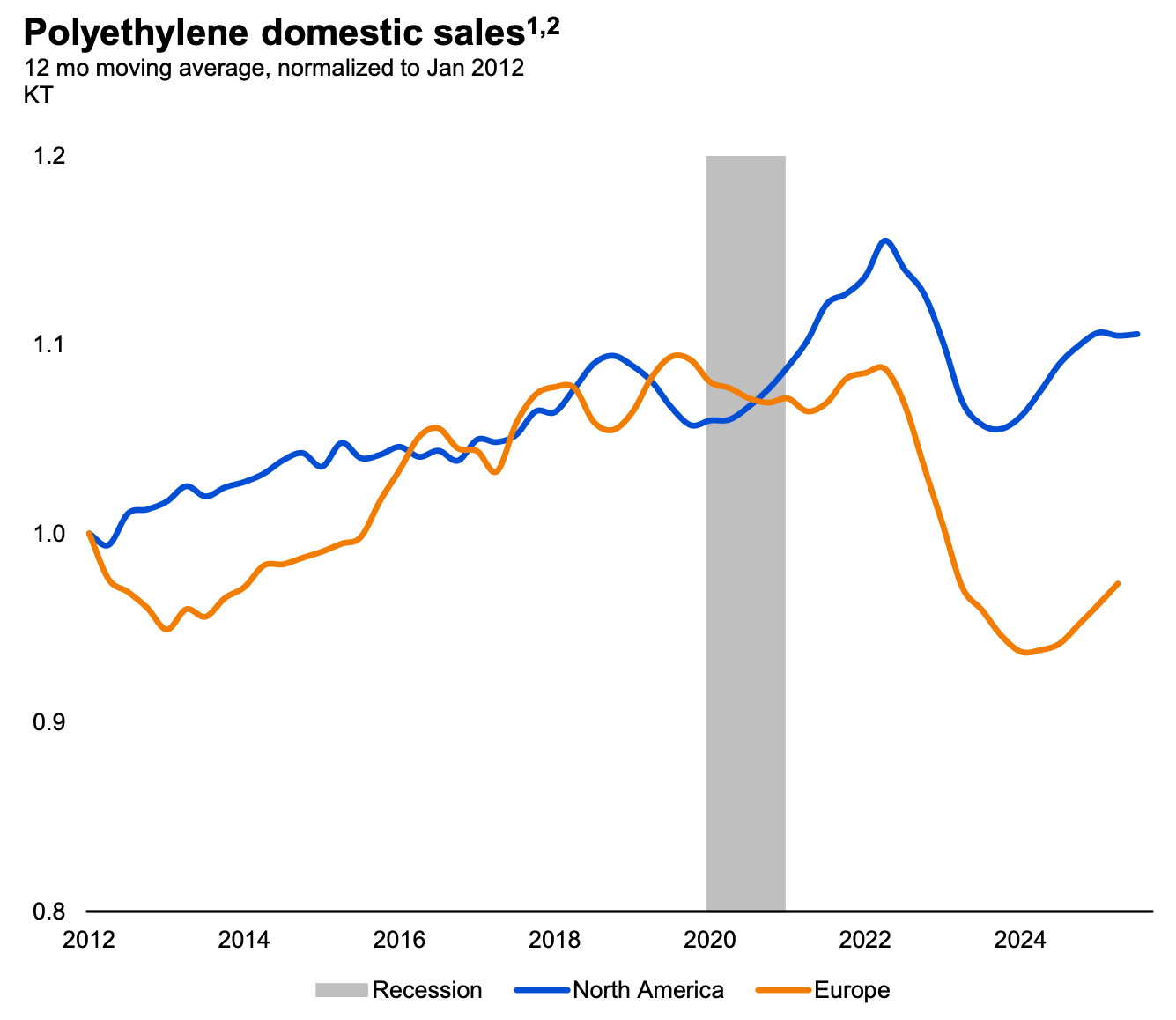

Figure 1: Mature Markets Showing Signs of Recovery

Commentary: This chart shows the first signs of a rebound in polyethylene volumes in both North America and Europe. The trend suggests that mature markets are starting to return to normal as downstream inventories are cleared.

We believe this early recovery indicates that the destocking cycle is mostly complete. For Huntsman, volumes in polyurethanes, coatings, and performance products should now be steady, with potential for gradual improvement through 2026.

Feedstock costs remain high in North America, and imports continue to pressure margins in Europe, but the focus across the industry has shifted toward efficiency and reliability. It’s cost discipline and broad product mix should help it protect earnings as market conditions slowly improve.

Global Demand Trends & Long-Term Drivers

LyondellBasell’s presentation highlighted the continued strength of global polyolefin demand. Over time, demand for polyethylene and polypropylene has consistently returned to its long-term growth trend after each slowdown.

Mature markets remain the largest consumers per capita, while emerging economies add most of the new growth through expanding populations and rising income levels.

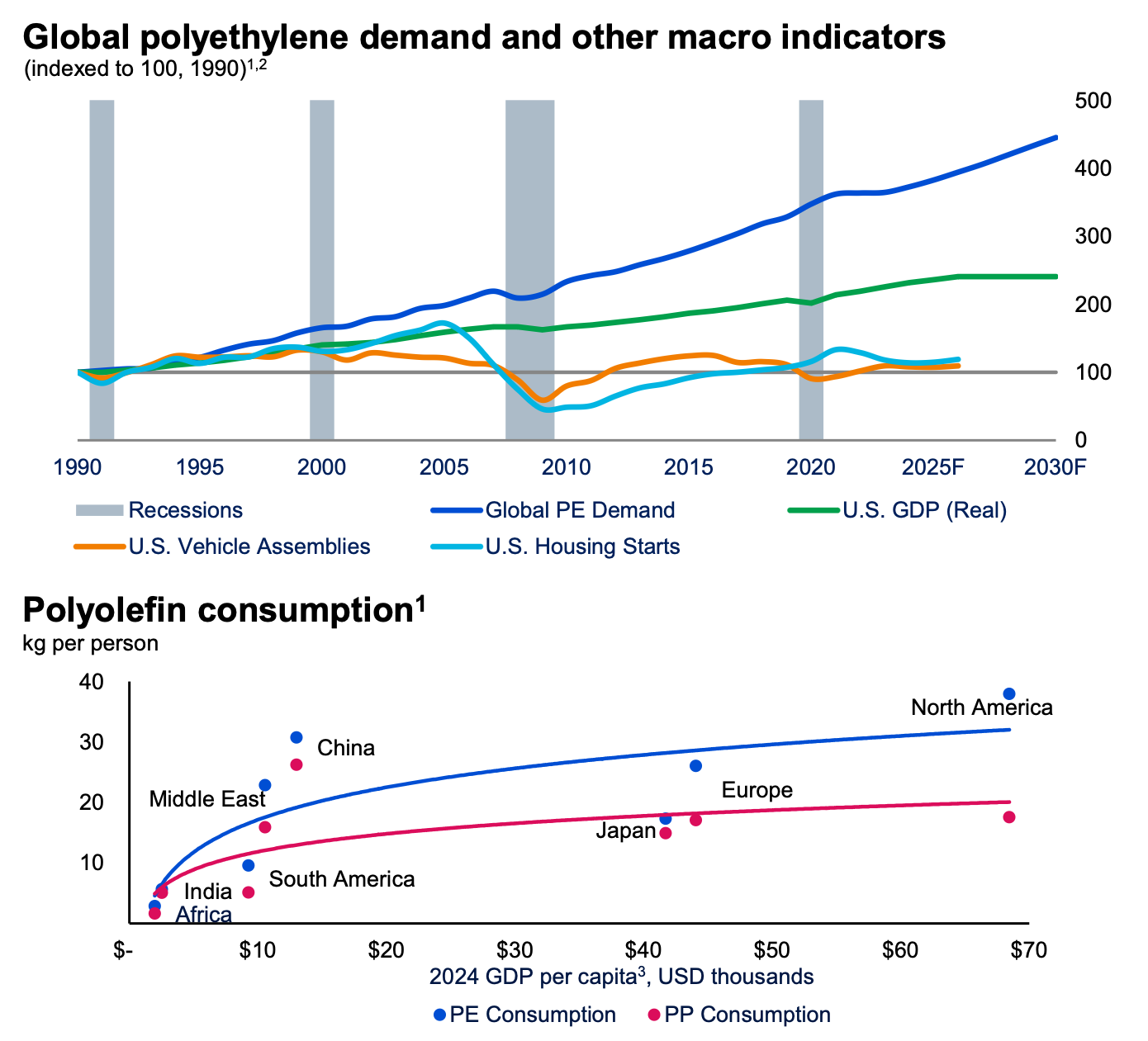

Figure 2: Resilient Global Demand Growth for Polyolefins

Commentary: This figure shows that global polyethylene demand keeps growing faster than GDP, driven by urbanization, higher consumer spending, and steady investment in infrastructure. These trends highlight how essential these materials are to everyday life and global development.

We believe this creates a strong foundation for long-term growth. Growing populations and better living standards in India, Africa, and Southeast Asia are lifting demand for basic materials, while mature markets are shifting toward uses in electrification, energy, healthcare, and mobility.

For Huntsman, this matters because its portfolio is increasingly focused on these higher-value areas such as coatings, insulation, and adhesives. This should help it capture growth as global demand gradually improves.

Capacity Rationalization & Industry Rebalancing

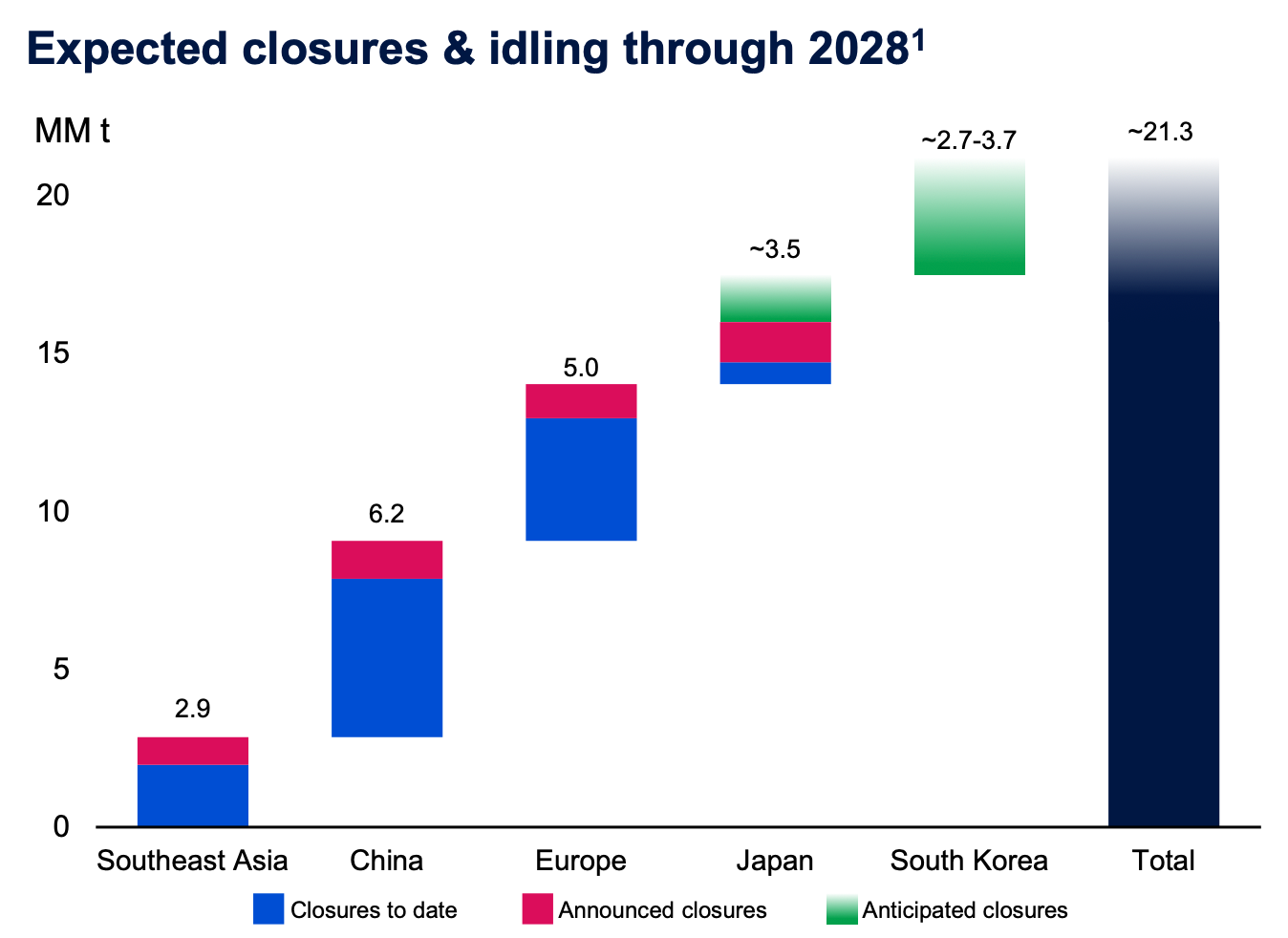

The most significant strategic signal from LyondellBasell’s quarter is the acceleration of capacity rationalization. Global ethylene closures and idling are expected to reach about 21M tonnes by 2028, representing roughly 10% of current supply.

Figure 3: Capacity Rationalization Trends Accelerating

Commentary: This figure shows the large wave of ethylene capacity cuts expected across Asia and Europe, led by China, Europe, and South Korea. China has already announced over 6M tonnes of closures, while Europe plans ~5M due to high costs and tighter regulations.

We believe this is a positive shift for the sector. Removing high-cost capacity will help tighten supply and support better pricing. For HUN, a more balanced feedstock market should improve profitability in propylene oxide and downstream materials, marking a move toward a healthier and more efficient global industry.

Strategic Direction & Peer Comparison

LyondellBasell remains focused on cost efficiency, reliability, and careful capital use. Management reported better uptime at the Channelview and Hyperzone plants and outlined a Cash Improvement Plan through 2026 to raise productivity.

HUN is also moving ahead with its MoReTec-1 recycling project in Germany, showing a clear shift toward recycling and higher-value growth. We believe this direction reflects what many producers across the sector are now doing. The focus is moving from growth to profitability, debt reduction, and better asset use.

Four themes stand out: tighter cost control, rationalization of high-cost capacity, a greater push into specialty products, and selective investment in recycling. This more disciplined approach is setting up the industry for a gradual and healthier recovery.

Sector Outlook & Our View

LyondellBasell expects market conditions to stay soft through late 2025, though signs of stabilization are emerging in North American polyethylene and intermediates. We believe the overall backdrop will be similar for the broader chemical space, with gradual demand improvement and firmer margins supported by ongoing cost discipline and tighter portfolios.

The sector is moving from contraction to normalization. Capacity reductions and more disciplined pricing should allow slow but steady progress even as demand remains uneven. Europe continues to lag, but lower supply is helping to restore balance and support margins.

For 2025, we see a transition period where volumes hold steady and efficiency gains begin to lift profitability. By 2026, the setup should be more favorable, with a gradual recovery in earnings as global markets strengthen.

Huntsman Corporation Trade

We believe the risk-reward is compelling at current levels. The industry appears to be bottoming, and Huntsman’s share price is near historical support. With supply tightening and margins set to recover, this looks like the right time to position before a potential re-rating.

Key Takeaways

Polyethylene demand in North America and Europe is recovering, signaling the end of the destocking phase.

Global polyolefin consumption continues to grow with population and income, supporting long-term stability.

About 10% of global ethylene capacity could close by 2028, tightening supply and improving pricing.

Cost control, capital discipline, and greater focus on specialty products are creating a stronger base for the next recovery cycle.

We believe the sector is entering a more constructive phase, with 2026 likely marking the start of a multi-year improvement in returns.