Canada: The Comeback

A decade of underperformance is reversing. New investment themes are emerging, and we play them through a fresh thematic equity basket.

Aurelion’s team was born and raised in Canada and have been investing in the market for more than a decade. We’ve never really covered Canada as a whole.

We had been waiting for the right moment.

Today, that changes, as we believe the country is (finally) reaching a turning point. While this has nothing to do with our timing, yesterday was Canada’s National Day. And what better way to mark it than with a thematic equity basket?

After being the country with the worst inflation in the G7, a housing crisis, and shrinking purchasing power for most citizens, investor expectations had fallen to the floor. Yet Canada is becoming an increasingly compelling place for capital markets… and Carney, our new Prime Minister, is changing things.

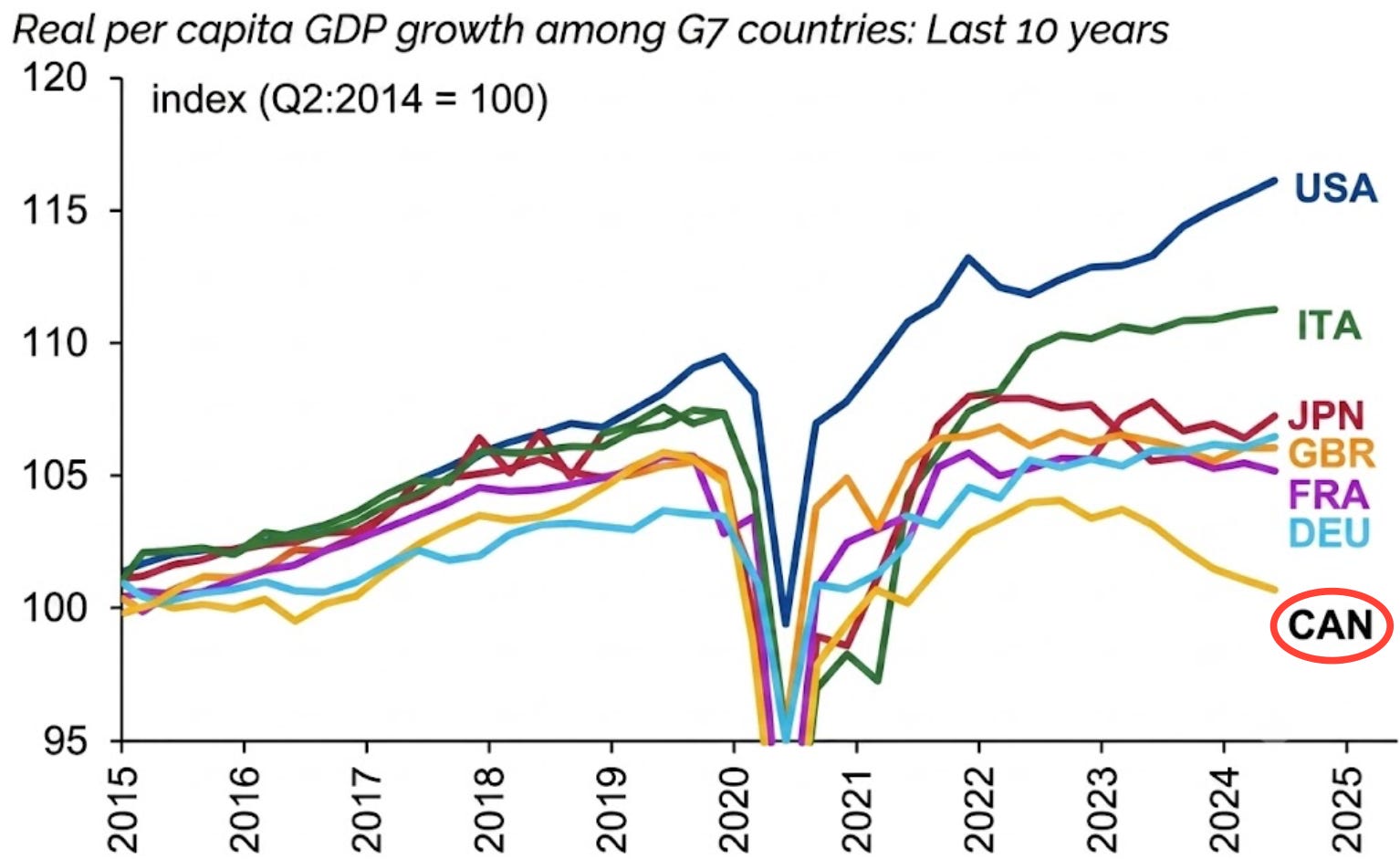

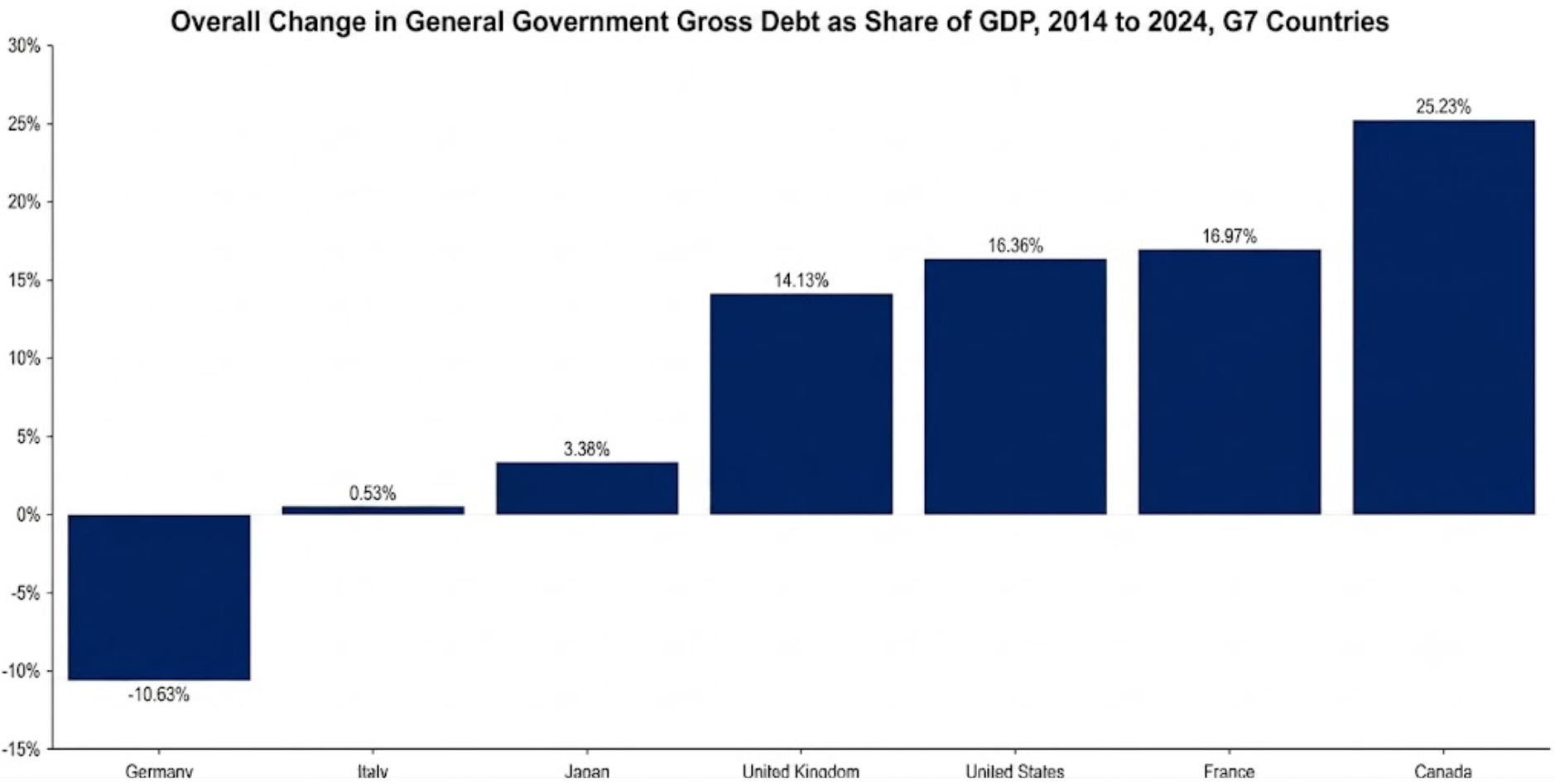

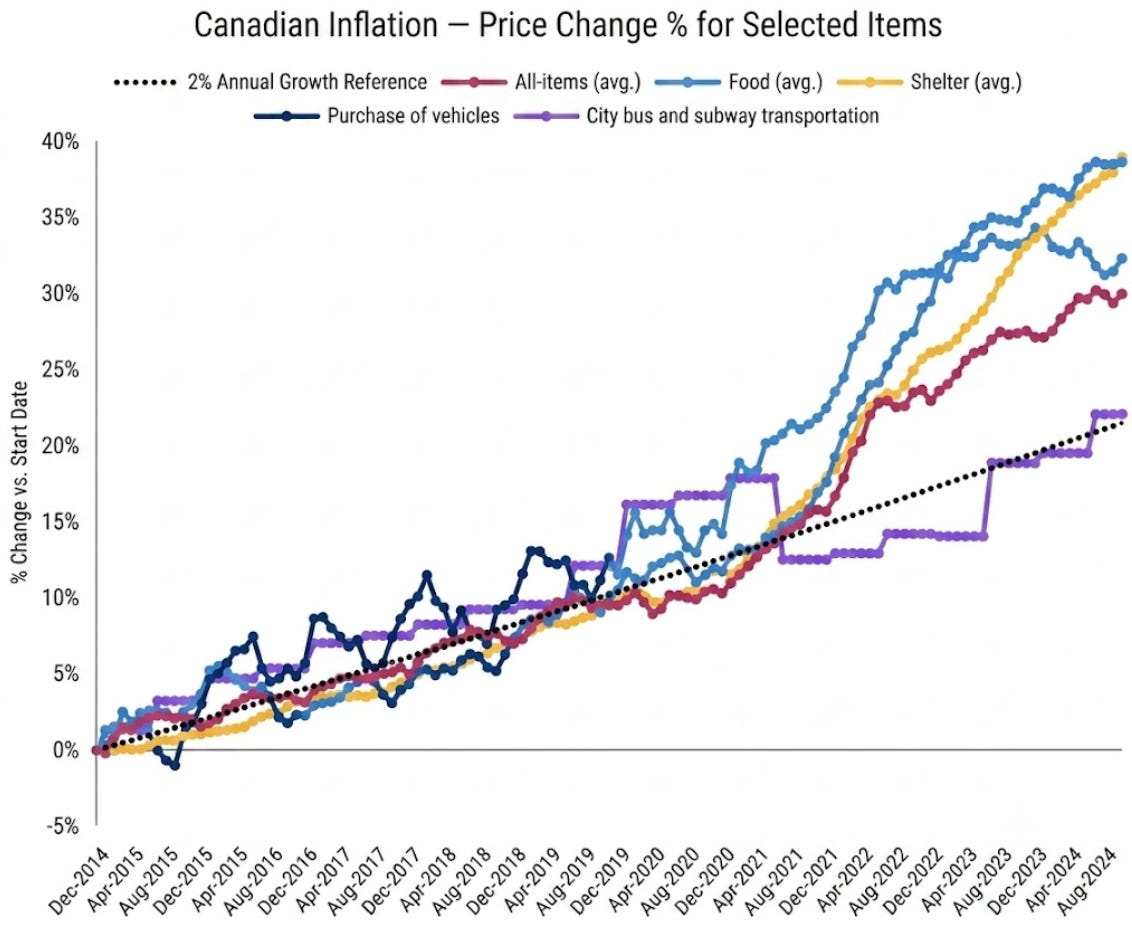

The three following charts show why the country’s economy has underperformed other G7 countries over the past decade:

First, since 2020, Canada’s GDP growth has been the lowest, and in fact declined before Carney came in. Unlike the United States, it did not recover quickly.

Second, Canada experienced the largest change in general government gross debt as a share of GDP, at 25%, and that is never something economists like to see…

Finally, Canadian inflation for the selected items shown below has been well above the 2% annual target, significantly affecting consumers.

We think sentiment toward Canada is at the bottom. While clear evidence and indications of this are still relatively weak for now, our experience suggests this could be the starting point for more and more positive policies to come.

In our view, when it comes to expressing a bullish view on the Canadian market, buying the broad index is very unproductive. More on that below.

Our thematic basket includes only the “asymmetric” trends across AI energy demand, renewed defence spending, materials, and much more.

While you can have a bullish view on Canada, you need to be allocated to the few specific sectors and companies that will actually see tangible benefits.

Table of Contents

The State of the Canadian Market

Why We Are Bullish on Canada

Growth Driver 1: Canada’s C$470 billion Defence Plan

Growth Driver 2: Importance of Canadian Pension Funds

Growth Driver 3: AI’s Power Problem Is Canada’s Opportunity

The State of the Canadian Economy

In Conversation

7.1 CIO of a Multi-Billion Dollar Canadian Fund

7.2 Buy-Side Financials Analyst

7.3 Canadian Portfolio Strategist

7.4 Banking Risk Analyst

Canadian Equity Basket

Key Risks

Our Final Take on Canada

1. The State of the Canadian Market

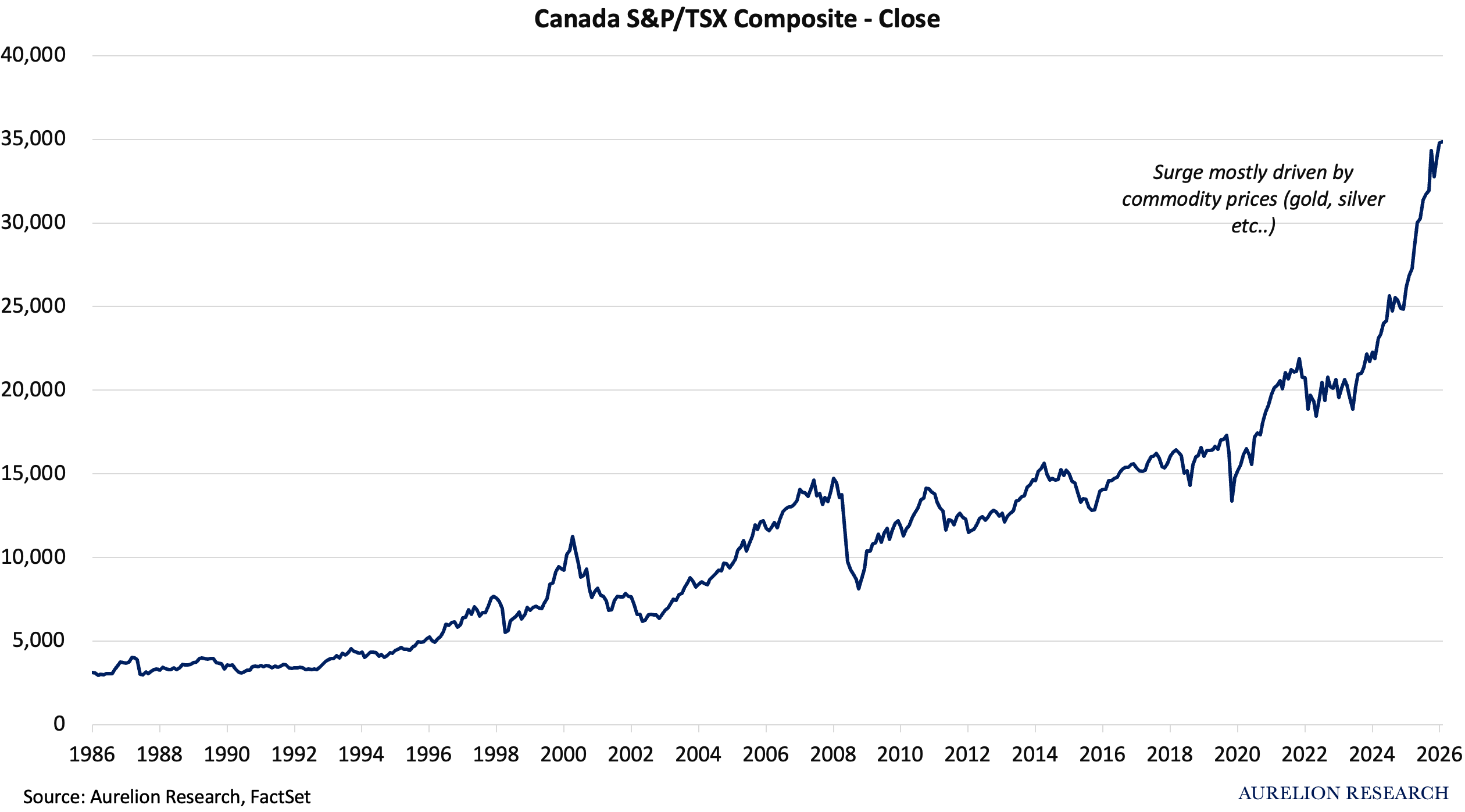

Currently, if investors look at Canada’s benchmark index, the S&P/TSX Composite Index, they might think they’ve already missed the move.

But there is a catch that we intend to exploit.

Based on our discussions with market participants, most investors believe the recent surge has been driven almost entirely by rising gold and silver prices, and that is true. However, this is precisely where we believe the opportunity lies.

The market believes the TSX is overvalued, but that is far from the case.

In fact, the remaining upside lies in companies outside of commodities. Buying the broader index also means taking on heavy, unpredictable exposure to commodity markets, which we view as a poor way to express this theme.

That is why we have built an equity basket designed to benefit from improving country dynamics. The Canadian Equity Basket is composed of 20 high-quality companies we have been following for the past five years, and in some cases with management teams we have met, each also trading at attractive standalone levels on a company-specific basis.

2. Why We Are Bullish on Canada

We believe that under the new government (Carney), a range of positive developments is emerging. From improved investment policies and a diminishing impact from U.S. tariffs, to increased defence spending and easing inflation.

These factors have only just begun to have a modest effect on the broader index.

We are seeing a new Canadian market, one with strong momentum and one that is increasingly viewed by investors as a relatively safe place to allocate capital.

This may be a controversial view, but when it comes to banks and financial institutions, we believe Canada deserves far more credit than it receives. Canadian banks are smaller than their U.S. peers, yet they have historically been more stable. The system is highly concentrated, tightly regulated, and has proven resilient across multiple economic cycles.

That is why we believe the “too big to fail” concept arguably applies even more to Canada than to the US. Canada’s major banks have consistently maintained strong balance sheets, durable profitability, and steady growth, making the Canadian financial system one of the most stable globally.

Beyond this, we also see additional tailwinds emerging. Higher pension fund allocations to domestic equities could become a meaningful source of demand for Canadian assets. At the same time, stronger defence spending would benefit industry and manufacturing. We also see rising power demand from data centers and AI-related infrastructure, which should support Canadian utilities.

3. Growth Driver 1: Canada’s C$470 billion Defence Plan

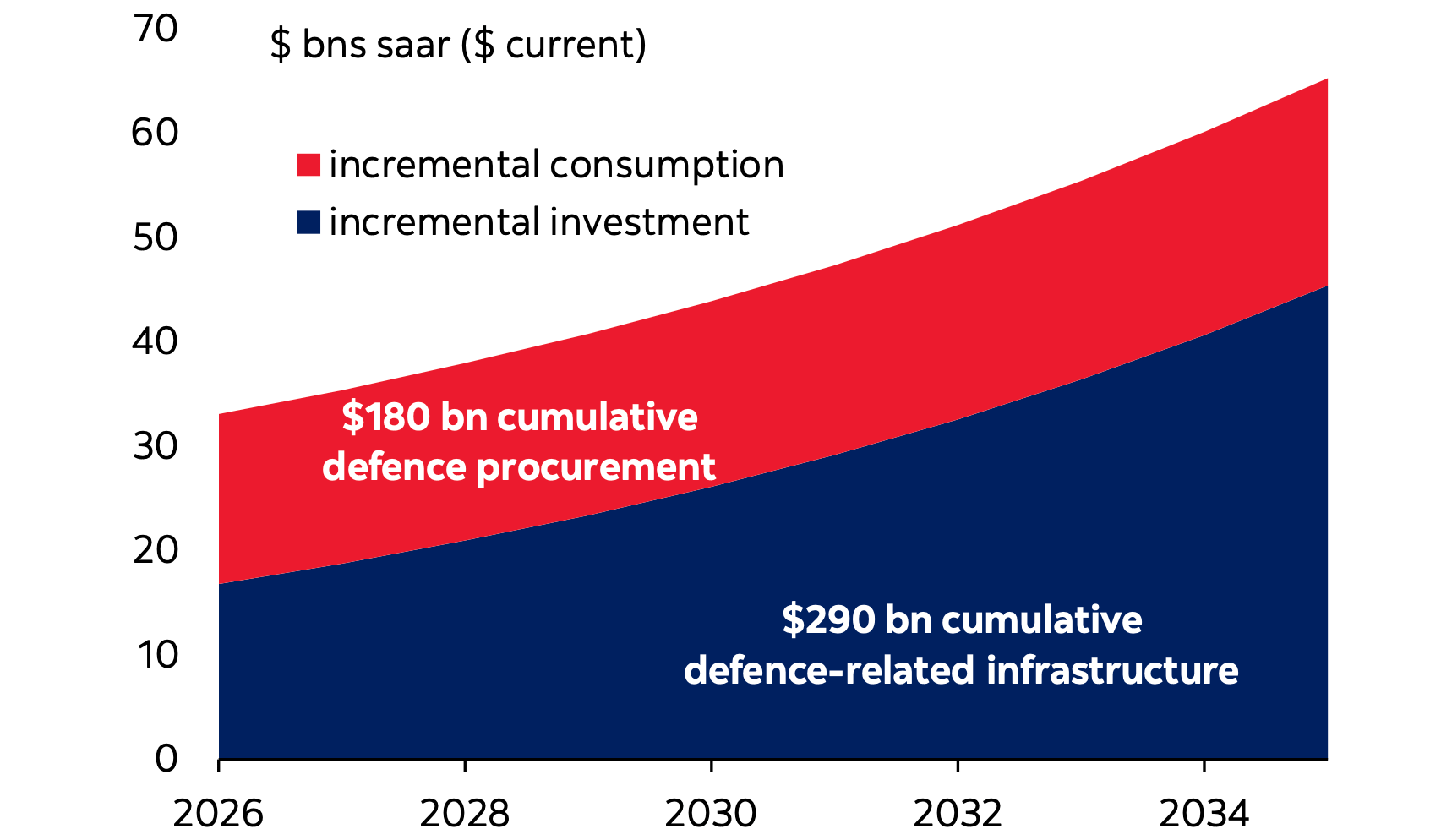

Canada’s federal Defence Industrial Strategy (DIS) announced a plan to invest C$470B in total defence-related spending over the next decade, including C$180B in procurement and C$290B in infrastructure.

How Defence Spending Is Increasing

This represents C$47B per year in new investment, with Canada also expecting a C$125B boost in economic activity and the creation of 125,000 jobs by 2035.

This is a major change in policy. We are seeing a country and government investing in the growth of its own economy (for once) while also moving toward greater military independence. This is a meaningful development.

Canada has only recently reached NATO’s 2% of GDP defence spending benchmark. Moving toward the 5% target by 2035 would imply about 11% annual growth in defence spending (which would be a lot) over the coming years.

The policy goals are ambitious.

But what are the Canadian government’s main targets?

70% domestic share of defence procurement

50% increase in defence exports

85% increase in defence-related R&D

More than 240% growth in industry revenues

We believe the policy direction under the Carney government points to an early-stage comeback, with a clear push to expand Canada’s domestic defence sector.

The setup is improving. Rising geopolitical tensions, increased Arctic activity, cyber risk, and the growing use of AI in military systems are all driving higher defence spending across NATO. In Canada, this is being used both to improve security and to support domestic industry, with effects across manufacturing, technology, and critical resources.

For example, Canada is working to break supply chain bottlenecks and improve trade flows. Carney’s goal is to double non-US exports by 2035. This will require infrastructure expansion, regulatory changes, and removing process bottlenecks, but broader reforms are already starting to take shape.

We spoke with several CEOs of Canadian defense companies this month at the Planet MicroCap Conference, and they are all expecting their best year in a long time.

4. Growth Driver 2: Importance of Canadian Pension Funds

Canada is far above its weight in the pension world.

Canadian pension fund assets rank third globally in size and second only to Switzerland relative to GDP, at roughly 165% of the country’s economy.

That’s a system large enough to move markets.

Much of this comes down to structure. Canada’s largest funds, known as the Maple Eight, collectively control roughly CA$2.7 trillion in assets and run what’s called the “Canadian model”: direct investment, managed in-house instead of outsourced. That gives them the flexibility to write large checks directly into infrastructure, private equity, and real assets, both at home and abroad.

Canada’s pension pool is so large because saving into it is not optional. Nearly every working Canadian contributes to the CPP at a mandatory 11.9% combined rate, a figure that has climbed steadily since it started at just 3.6% in 1966.

All of that money is invested in-house by professional teams instead of being handed to external managers, which keeps costs low and allows policy to influence where capital is allocated. The result is one of the best-funded pension systems in the world relative to the size of the economy, and it means Canada has an unusually large amount of patient, long-term capital available to deploy.

Employee Compensation Matters

Canada’s pension compensation for finance professionals is high and sometimes higher than the private sector. For example, in addition to better working hours, an entry-level analyst will make the same (~$160K) working at a leading private equity firm as at a pension’s private equity fund.

At pensions, in “front office” roles such as hedge funds, infrastructure, real estate, trading, etc., a 30–35-year-old vice president will make $500K+ while working 9 to 5. This is basically unseen in finance (and in the rest of the corporate world). That data comes from some of our friends in those exact positions for 2025.

We have seen several U.S. or European leading managers (Goldman, BlackRock, etc.) get recruited into leadership positions in Canadian pensions.

This system has led Canada’s pensions to actively pick single stocks, allocate by country, etc. This is extremely rare for pensions. The summary is that Canada’s pension compensation, reputation, and work-life balance attract top-tier talent across the world, which has led to a dominant system, large enough that its investments significantly move capital flows in the country.

A Massive Negative Driver in the Last Decade

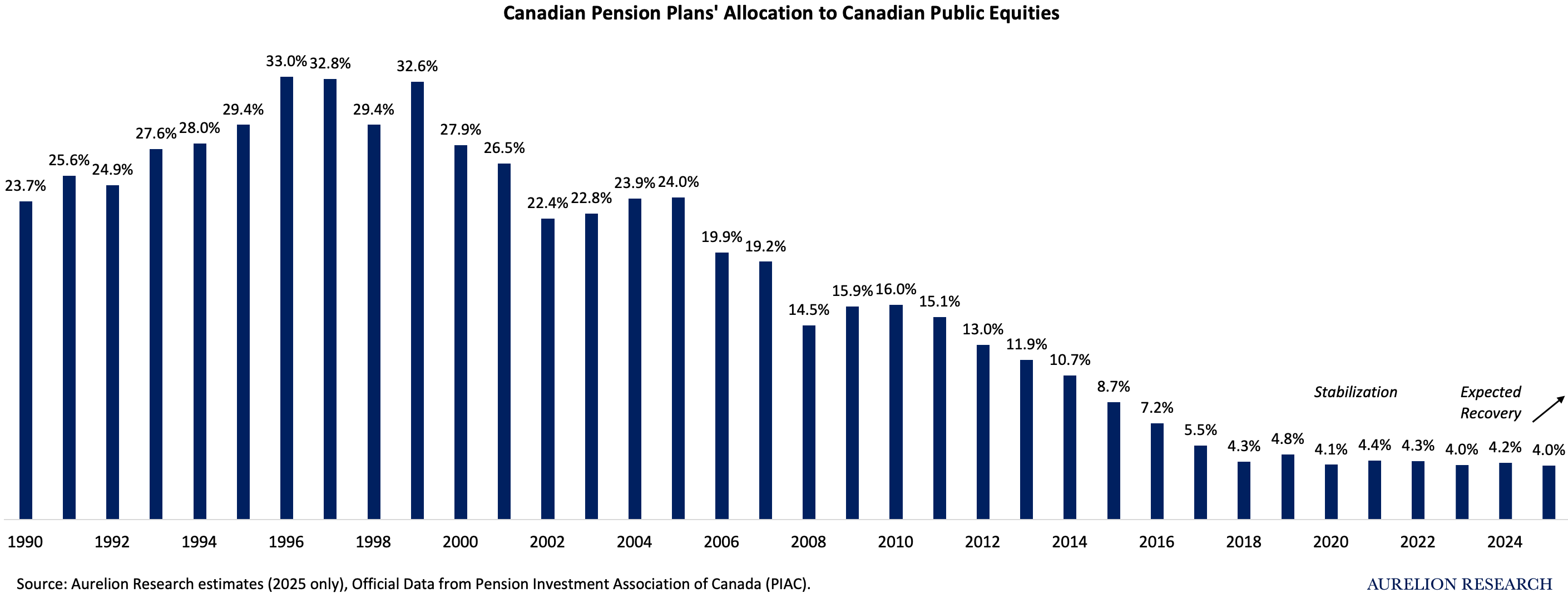

The Foreign Property Rule kept money in Canada until 2005.

From 1971, pension funds were legally required to hold 90% of assets domestically. That limit was gradually loosened, dropping to 80% in the 1990s and 70% around 2000-2001, before being eliminated entirely in 2005.

The Canadian model shifted the entire strategy, worsening the geography shift. Rather than sitting in public equities at all, Canada’s largest funds moved heavily into private equity, infrastructure, and real assets, managed in-house and increasingly deployed globally. Public equities, especially Canadian, became a smaller slice of these portfolios as private markets took a growing share.

Canada’s Pension Plan, one of Canada’s leading pension funds, shows this clearly.

A Changing Tone

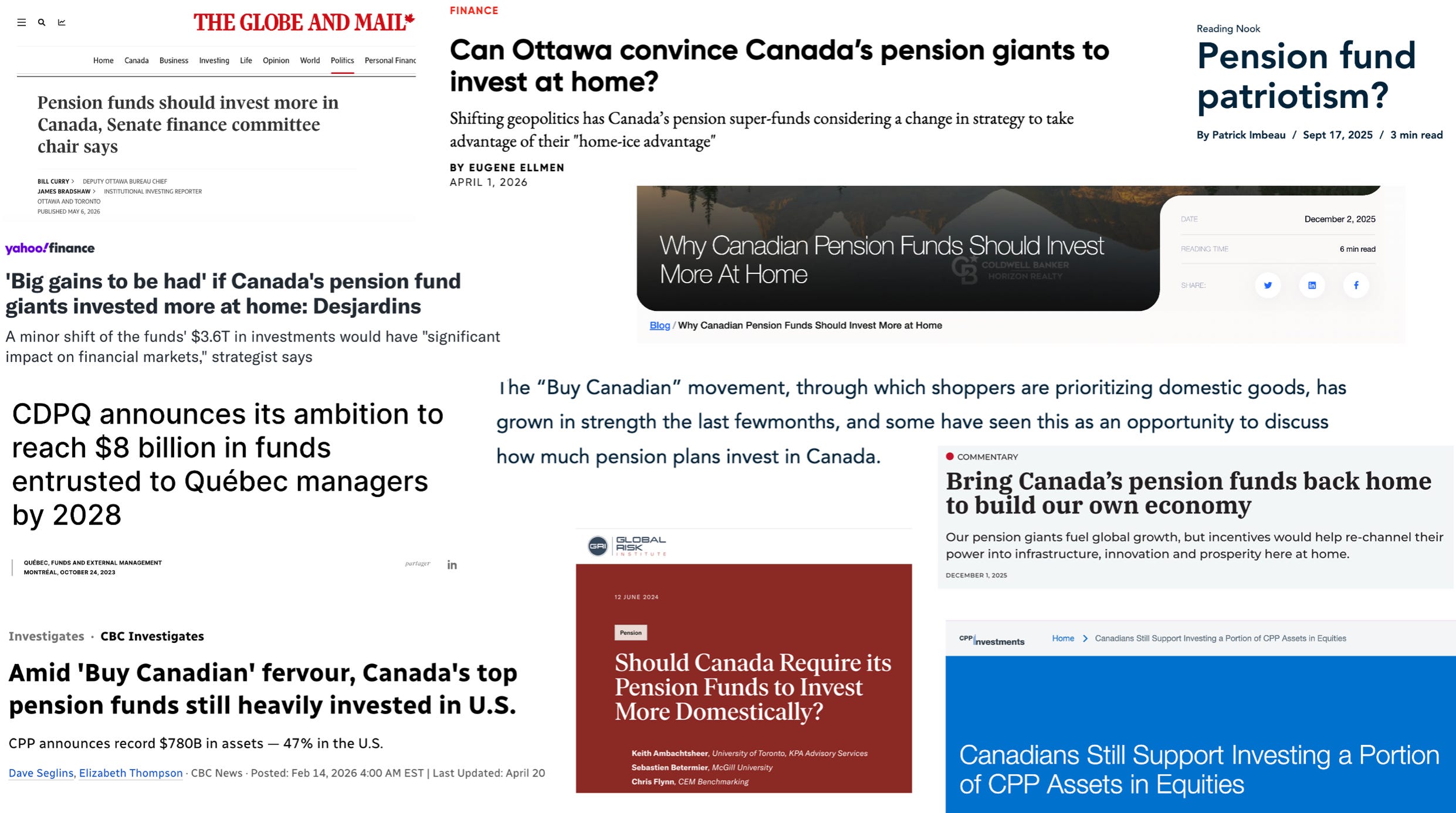

Federal and provincial governments are actively pushing large Canadian pension funds to redirect more of their massive capital pools back into Canada. Driven by rising trade barriers (U.S., mainly), and a desire to boost domestic productivity, the push involves a mix of policy shifts and voluntary commitments.

Mark Carney Unveils Historic $115B Strategy at Canada–UAE Investment Summit

Mark Carney’s (Prime Minister) “Canada Strong” approach is focused on improving Canada’s weak productivity and investment cycle by attracting more long-term capital into domestic growth opportunities.

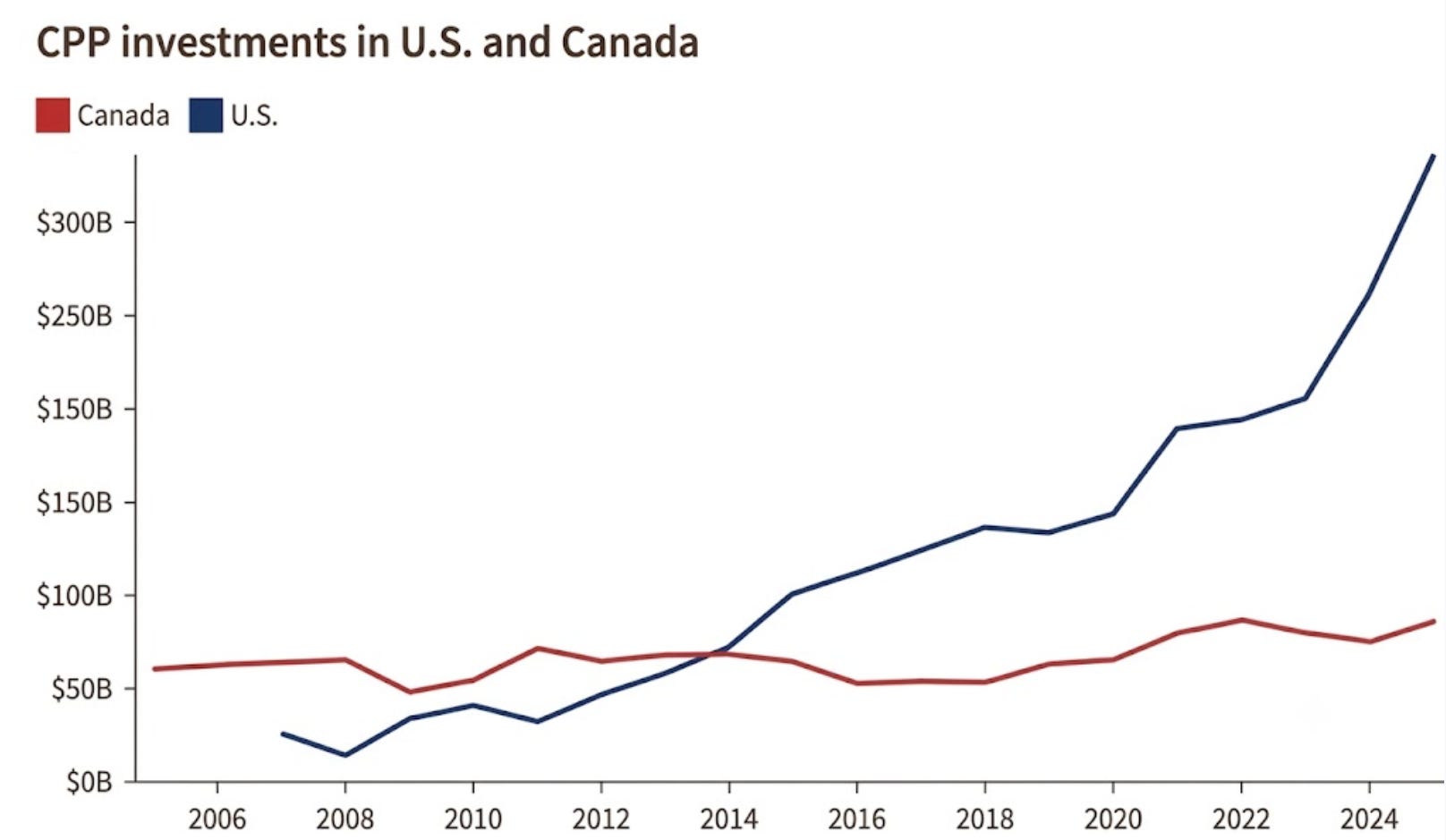

A key part of the context is that Canadian pension funds manage large pools of capital but allocate a relatively small share to Canadian public equities, preferring deeper and more liquid foreign markets like the U.S.

For now (while it could eventually become), the policy idea is not to force a change in allocation, but to make Canadian listed companies and domestic investment opportunities more attractive on a risk-adjusted basis.

That means improving conditions for capital formation, scaling domestic firms, and increasing the number of large, investable Canadian public companies through better economic policy and market development.

If successful, this would gradually increase the weight of Canadian public equities in pension portfolios. As domestic markets become deeper, more liquid, and more competitive globally, pension funds would naturally rebalance toward Canada without breaching their diversification mandates. We believe the shift would be driven by better opportunities instead of regulatory pressure.

Especially over the past year, during conferences in Montreal and Toronto, our conversations and hearing from key allocators in Canada have consistently highlighted a common theme: investing more domestically.

What stands out is that this is not just political rhetoric.

A portfolio manager at a pension fund telling us directly that they plan to increase allocations to Canada over the coming years carries far more credibility than policy discussions alone, and suggests a higher likelihood that these commitments actually translate into action.

Quantifying the Potential Impact (estimates)

If pensions moved allocation from 4% to 8%, that’s roughly $180B of fresh buying pressure entering, about a 5% increase in the total pool of capital chasing Canadian equities. On its own, that number is not dramatic.

But markets don’t move in a straight line with flows, a few percentage points of new demand can trigger a much bigger reaction:

Mainly, it could attract outside capital. Global asset allocators watch domestic flows as a signal. If Canada’s own pension funds, widely respected as sophisticated, patient capital, start buying back into the local market, that’s a credibility signal to foreign institutions who’ve been underweight Canada for years.

It could pull in passive money automatically. Index funds tracking MSCI / FTSE allocate to countries based on market size and performance, not discretion or preference. If pension buying pushes Canadian stock prices up, Canada becomes a bigger slice of global indexes, and passive funds have to buy more just to keep pace. The buying happens automatically.

It could disproportionately help smaller, less liquid names. The TSX is dominated by a handful of giant banks and energy companies. New buying doesn’t spread evenly. Mid/small-cap names, chronically underfollowed and thinly traded, could see an outsized price reaction from even modest new demand. It doesn’t take much volume to move a stock nobody is paying attention to.

It could lower the cost of capital for Canadian companies. In addition, with Carney’s measure, higher valuations and more buyers mean companies can raise equity more cheaply, and fund growth. They would have less reason to list or relocate abroad in search of deeper capital pools, a complaint that’s driven several Canadian companies to the US in recent years.

It could become self-reinforcing. Higher prices and stronger performance attract more attention from global managers and media, which brings in more capital, which supports prices further. Flow-driven markets can build real momentum once they get going, even from a starting point that looks small on paper. A perfect example is the Japanese market since the start of 2025.

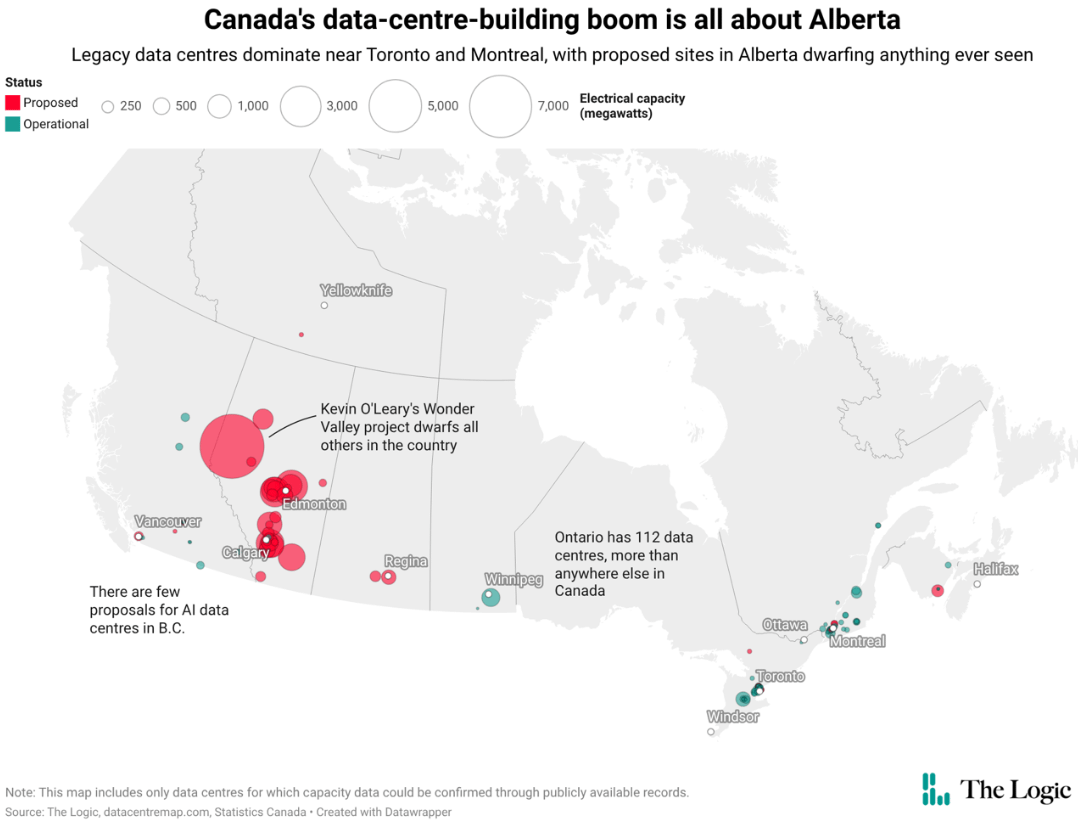

5. Growth Driver 3: AI’s Power Problem Is Canada’s Opportunity

AI is turning into an electricity story in Canada.

Data centers need enormous amounts of power, running around the clock, and the world doesn’t have enough of it. That’s creating a new kind of constraint, and Canada is one of the best-positioned countries to supply it.

Canada has cheap hydro power, abundant natural gas, and the highest-grade uranium deposits on the planet, roughly 100 times richer than the global average. Most countries have one or two of these advantages. Canada has all three.

This is already showing up in how the market is behaving. Tech companies that used to only care about chips and cloud contracts are now negotiating directly with power producers and uranium suppliers, locking in electricity years in advance because they know supply will be tight. Power is becoming a bottleneck for AI growth, and whoever controls reliable supply has real pricing power.

Data Center Buildout

Alberta is at the center of it. Active data centers in the province already total 1.6 gigawatts (GW) of capacity, but planned projects would increase that to 13.2 GW, about eight times more. As of early 2026, more than 30 AI data center projects were waiting for approval in the province.

Alberta has made itself the destination of choice by offering cheap natural gas power, a deregulated electricity market, and fast-tracked permitting, going as far as launching a dedicated “concierge team” to help investors get projects moving.

According to Mordor Intelligence, the Canadian data center market was valued at around $11.5B in 2025 and is expected to reach nearly $25B by 2031, a compound annual growth rate of about 14%. We see this as conservative. It includes the whole data center industry, not just AI-related projects, and forecasts like this are often revised higher as new hyperscale projects are announced.

Just for example the Alberta minister aims for C$100B.

Not every province is participating equally. Quebec, Ontario, and British Columbia have all started restricting new grid connections because they simply can’t keep up with demand, which is part of why so much of the new construction has shifted to Alberta instead. The AI buildout, in other words, is chasing whatever power is available fastest, not just the cleanest or cheapest.

We have seen that the usage of data center electricity is currently drawn from available sources. That shows that costs and political backlash are much lower because it does not raise electricity prices for the whole region yet.

For a market that’s spent the last two decades being defined by banks and energy exporters, having a genuine infrastructure growth story tied to the most talked-about theme in global markets is a real shift.

How We Think About Our Equity Basket

A year ago, Canadian utility names were seen as boring, defensive dividend payers. That’s changing. Companies that generate or distribute electricity are now in the middle of one of the biggest capital spending waves in history, as AI infrastructure gets built out globally and needs somewhere to plug in.

Names in our basket tied to power generation, utilities, and uranium are becoming growth exposure to AI, just approached from the supply side instead of the software side. That’s a meaningfully different investment case than the one most investors are still pricing in, and it’s a big part of why we think parts of this market are still undervalued relative to where the puck is going.

What’s great about them is that you get a mix of dividend income and potential upside from a thematic trend playing out in the stock price.

6. The State of the Canadian Economy

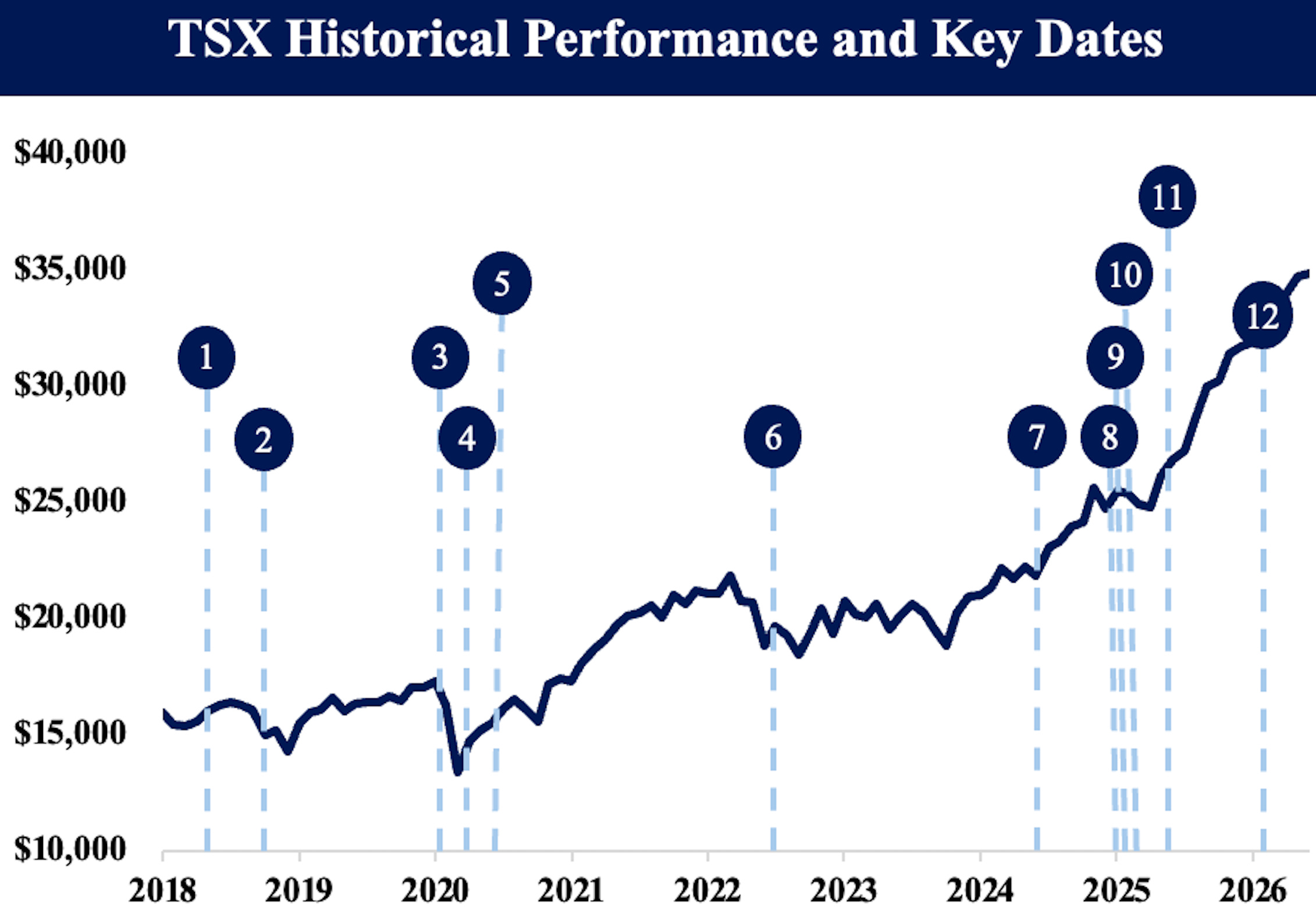

Sentiment toward Canadian equities has shifted from cautious optimism in late 2025 to a more volatility-aware, defensive tone in mid-2026, even as capital continues to flow into the asset class. To put this in context, we believe it helps to look back at how the TSX has performed since before COVID.

Since Carney won the election and became Prime Minister, and as we entered the year after significant value appreciation in 2025, large asset manager ClearBridge noted that it had adopted a more defensive strategy, even while expecting Canadian businesses to benefit from pro-growth government policies.

On that same note, the federal government maintained a positive tone in its most recent Spring fiscal update, noting that improved sentiment is supported by the country’s relative tariff advantage, federal incentives, and increased investment in infrastructure. This optimism, however, has been tested by macro-induced shocks.

A mining sector capital flows report from March 2026 described stagflation, energy fragility, and liquidity risks tied to Middle East macro exposure.

The report also noted that this environment drove retail and institutional capital out of technology and AI names into real assets like gold and critical minerals, where Canada is structurally overweight.

In June, a market outlook piece showed the prevailing mood as cautious optimism, with opportunity mixed with volatility due to Canada’s concentration in energy, mining, and dividend payers rather than US-like megacap tech.

Despite volatility, there has been record-breaking demand for Canadian equity products. Canadian ETFs saw more than $20B in capital inflows, more than double the average 2025 monthly flow, according to NBC Data.

This momentum persisted through the first half of 2026, with assets in Canadian ETFs reaching over $700 billion and year-to-date inflows exceeding $75B.

This is reinforced by capital formation trends. The Spring Economic Update shows Canada leads the G7 in per capita investment inflows, and the 2025 Kearney FDI Confidence Index ranks Canada second among 25 markets.

7. In Conversation:

This section summarizes our discussions with analysts, portfolio managers, and industry experts, and the key insights we took away on current market sentiment.