Brazil Rare Earths: A Rare Opportunity

Brazil holds the second largest rare earth reserves in the world, yet production remains minimal with only one company currently operating.

The current landscape is shifting quickly, as over 20 mostly publicly listed companies explore new sites, while the government develops the policies and funding needed to support the industry’s growth. This leads to the ultimate question: Can Brazil become the rare earth champion of the Western Hemisphere?

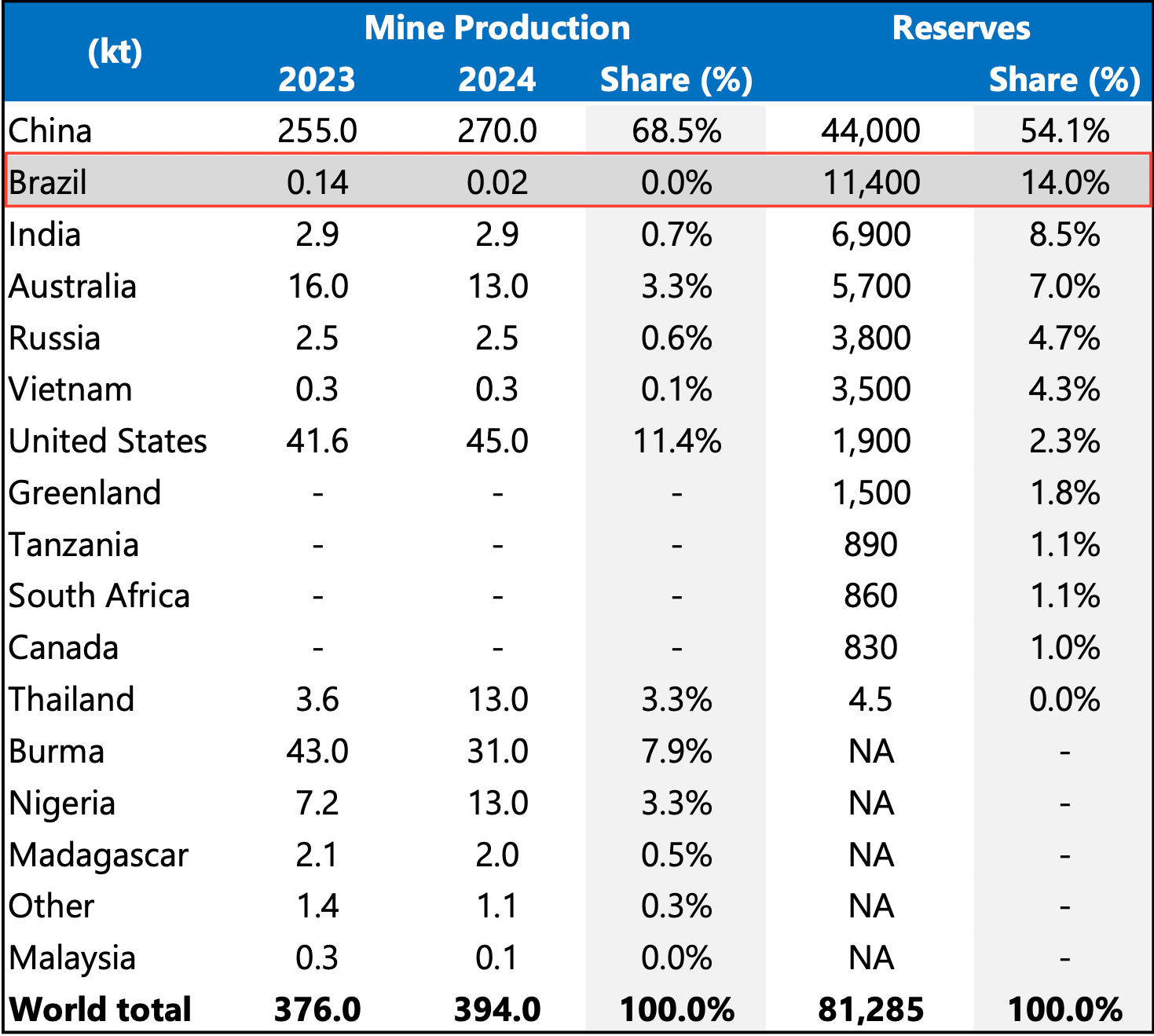

Brazil holds the world’s greatest untapped rare earth potential, but its current production is a tiny fraction of its massive resource base. In 2024, Brazil produced only 20 tonnes of rare earth oxides, while China dominated the market with 270,000 tonnes by leveraging over half of the world’s reserves.

The country currently produces almost nothing despite holding a massive share of the world's rare earth reserves. This creates a striking gap where Brazil sits on 14% of global reserves, second only to China, yet its production remains near zero. In contrast, the United States maintains an 11% global share of production despite holding a much smaller reserve base.

Brazil Rare Earths: Untapped Reserves

To bridge this gap, the Brazilian government is rolling out a broader strategy to turn the country into a major player. This includes the R5bn Critical Minerals Fund, the R1bn Strategic Minerals Investment Fund, and a R$1bn fund backed by BNDES and Vale. At the same time, new rules make it easier for mining projects to access tax incentives through special bond structures, while a national council provides financial guarantees to reduce risk.

We believe the long-term objective is simple: develop processing capacity at home and move Brazil higher up the global critical minerals supply chain.

Rare Earths 101

Before turning to Brazil and what we think comes next, let’s first look at some essential basics about rare earth elements and their uses.

Why Do They Matter?

Rare earth elements (REEs) are the backbone of the global energy transition. Their unique magnetic and chemical properties make them essential for electric vehicles, wind turbines, and advanced electronics.

While they are not actually rare in nature, it is very difficult to find them in high enough concentrations to mine profitably. As the world moves toward clean energy, securing a steady supply of these minerals has become a top priority for both governments and private companies.

What Are They?

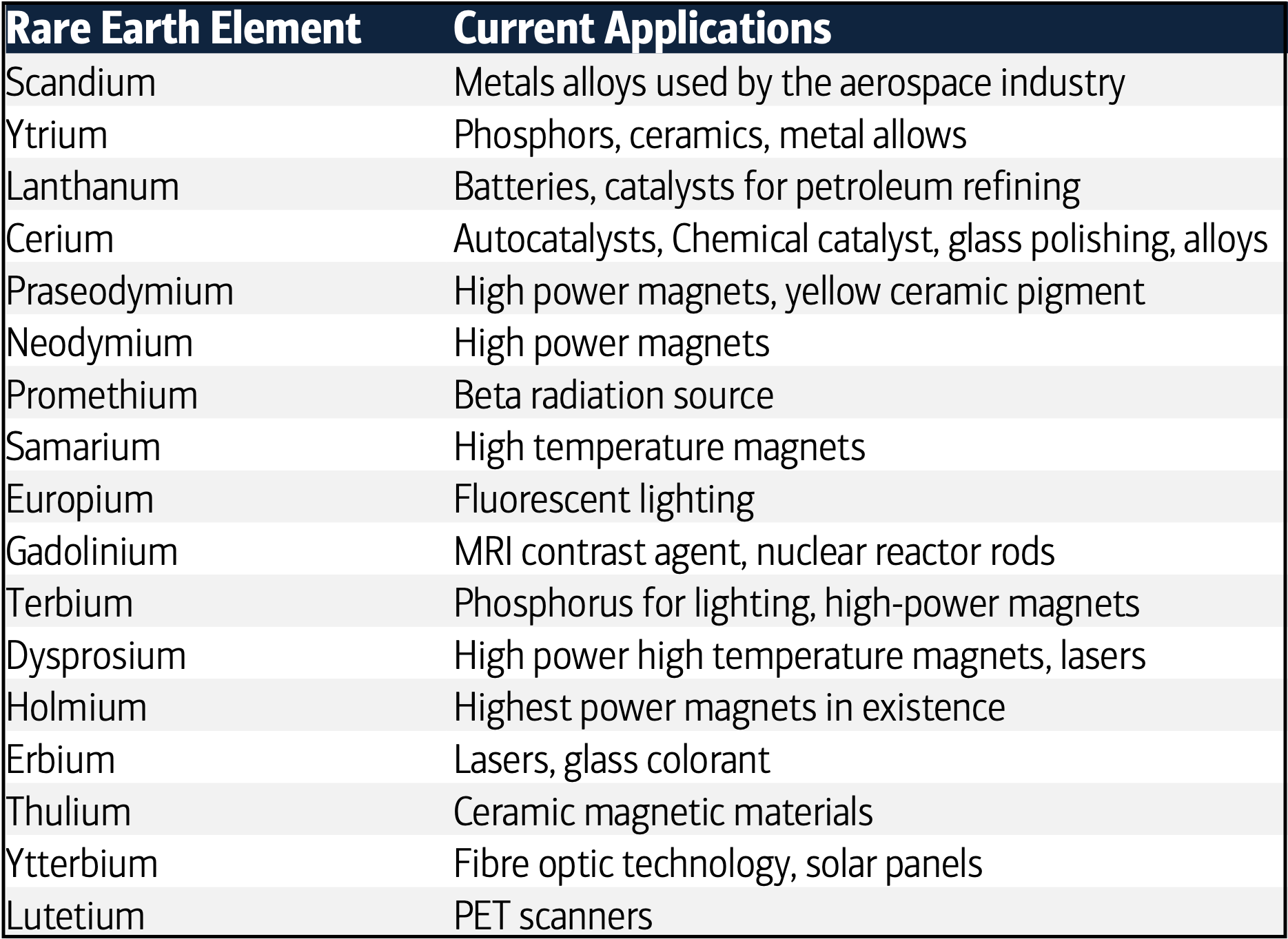

There are 17 rare earth elements in total. They are split into two main groups:

Light Rare Earths: These are more common and are often found in large rock deposits. This group includes elements like Neodymium, which is used in powerful magnets.

Heavy Rare Earths: These are much harder to find and usually come from specific clay deposits. Elements in this group, such as Dysprosium, are vital for high-tech applications because they can handle extreme heat.

Where Are They Found?

Even though rare earths are spread throughout the Earth’s crust, they are rarely found in large, concentrated batches. Most of the world’s light rare earths come from major mines in China, Australia, and the United States. Heavy rare earths are even more concentrated, with the majority of the global supply currently coming from southern China.

Key Applications

While REEs are used in everything from camera lenses to medical imaging, permanent magnets are the most valuable part of the market. These magnets allow EV motors to run efficiently and wind turbines to generate power. Even though they make up only a small part of the total volume of rare earths mined, they represent the vast majority of the industry’s economic value.

Magnets Are the Main Application

(Primary Uses of Each Rare Earth Element)

How Strong Is the Demand Outlook?

Global demand for rare earth elements is surging as the world shifts toward electric vehicles and renewable energy. A specific blend of elements called NdPr has become the industry’s biggest bottleneck. It is the essential ingredient for the high-efficiency magnets used in everything from EV motors and wind turbines to advanced robotics and defense systems.

1. Rising Demand Led by Permanent Magnets

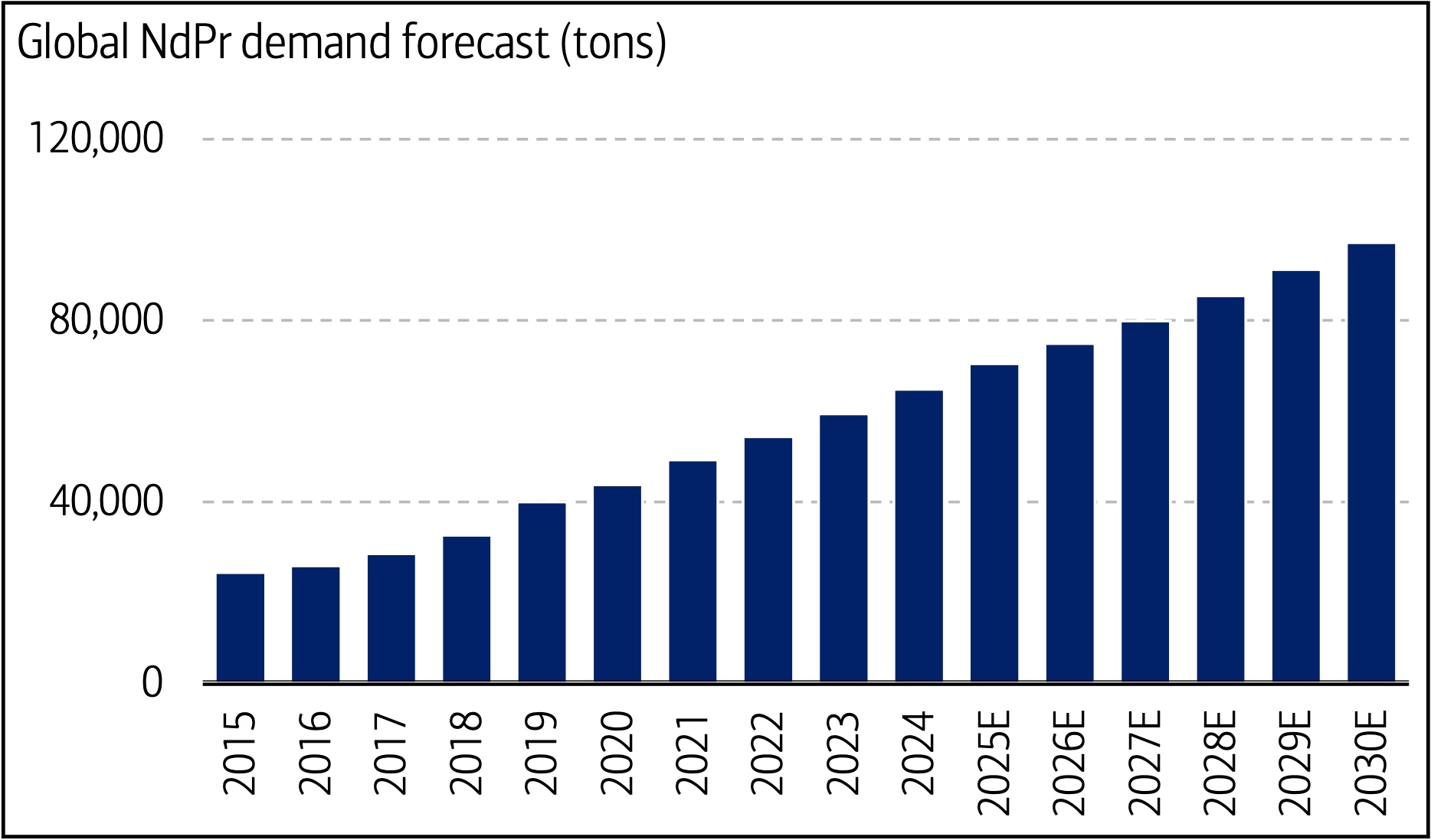

Experts forecast that demand for NdPr will grow by ~7% every year through 2030. By then, the world will likely need 97,000 tonnes of it annually, which is 50% more than what was needed in 2024. Most of this growth is driven by the transition to clean energy, with electric cars and wind power alone making up 75% of new demand. Meanwhile, rising global tensions are pushing governments to secure more of these minerals for strategic military use.

Bloomberg Sees ~97Kt NdPr Demand by 2030

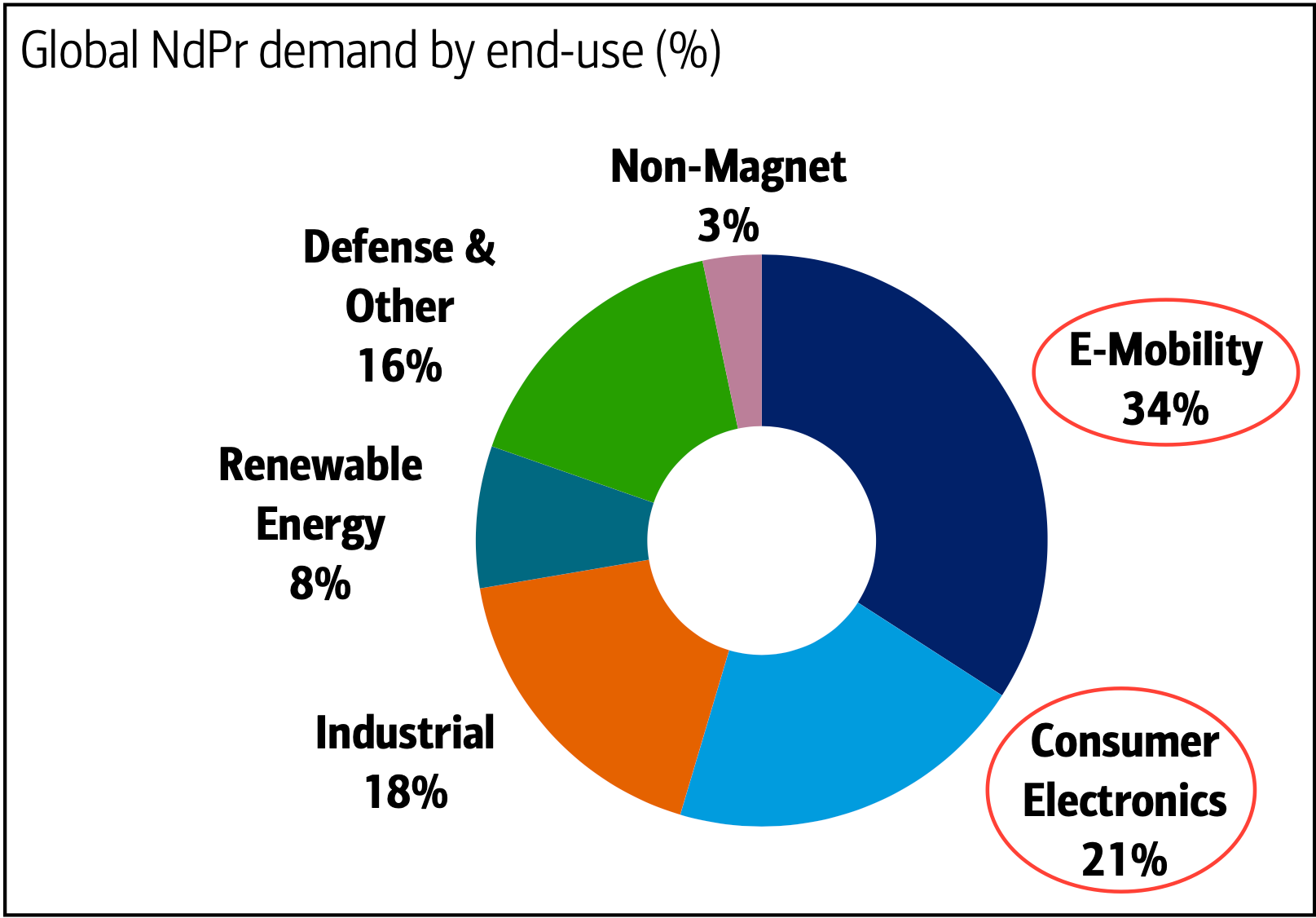

E-Mobility & Consumer Electronics Drive Demand

2. EVs: The Primary Catalyst for Demand

Electric vehicles are the most significant driver for rare earth magnet demand. Industry forecasts suggest that automotive requirements for neodymium and praseodymium could jump by over 80% between 2024 and 2030. Permanent magnet motors are the top choice for electric vehicle powertrains because they are highly efficient. Using just two kilograms of rare earth magnets in a motor can boost its efficiency by up to 5%.

Global EV Demand Set to Keep Rising

This is a massive advantage for car manufacturers. Better efficiency means they can reach their driving range targets with smaller and lighter battery packs. Since batteries are often the most expensive part of an electric car, reducing their size helps lower the total cost of the vehicle.

Why Isn’t Brazil a Rare Earth Powerhouse Yet?

Brazil’s rare earth sector faces structural barriers that slow its growth. The most immediate problem is financing. Unlike other major mining regions, Brazilian firms cannot use mining rights or future production as collateral. This limits domestic credit and forces developers to look for foreign funding. While public institutions like BNDES and Finep have created programs for strategic minerals, access remains difficult due to strict requirements.

Without flexible financing and with strong competition from countries that already have mature supply chains, Brazil struggles to move beyond early-stage production. Compounding these financial issues is the lack of a joined-up national strategy. The sector still lacks policies that connect mining with processing and manufacturing. This is a challenge because mining only represents 10 to 20% of the total value. Separation and refining capture about half of the value, and making magnets accounts for another 30 to 40%.

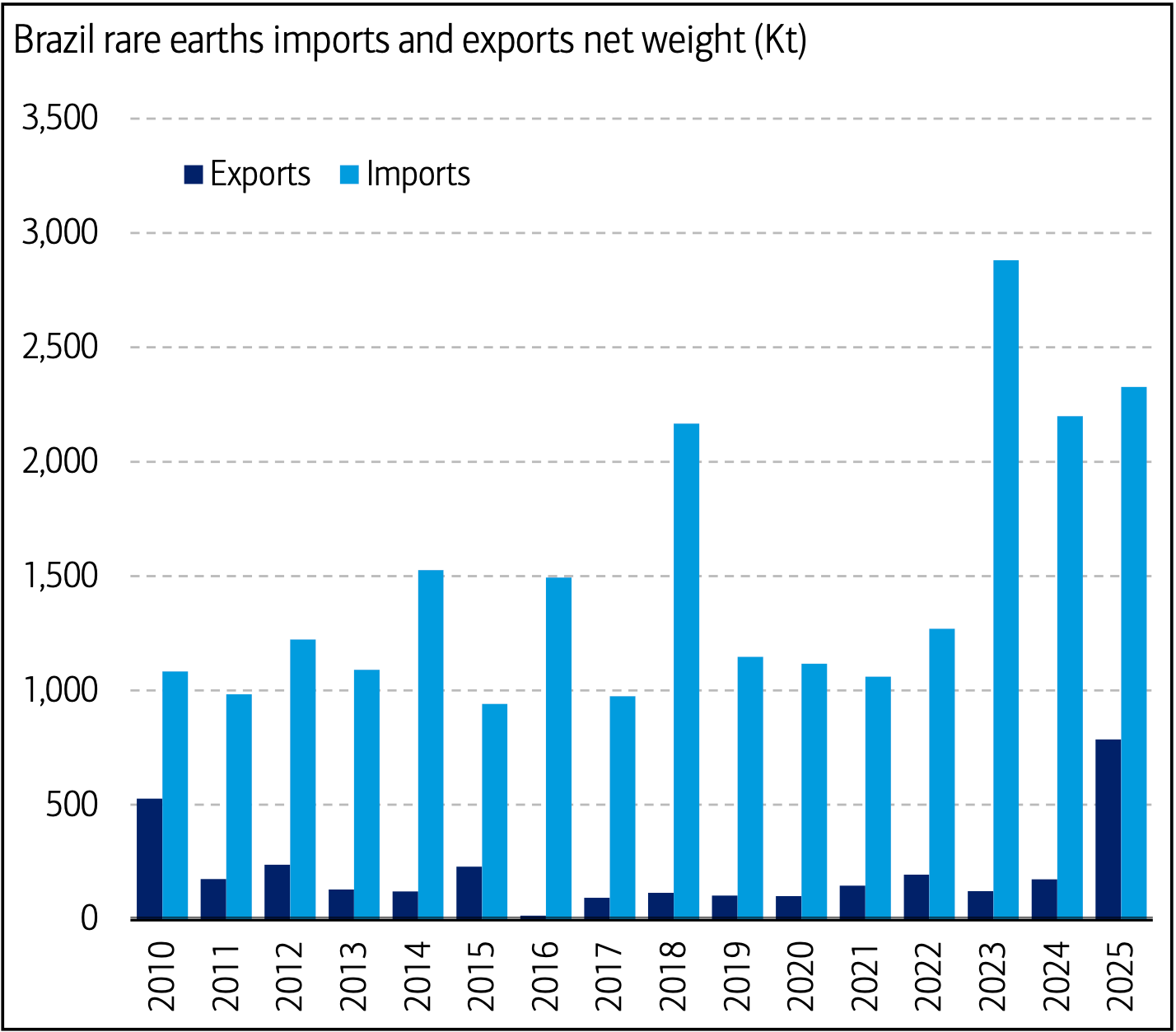

Trade data makes the situation even clearer. Brazil’s rare earth exports are almost entirely raw materials, showing that the domestic industry is still in its early stages. Because the country cannot yet refine or process these minerals at scale, it must import high-value oxides and compounds, mainly from China.

Brazil Remains a Net Rare Earth Importer

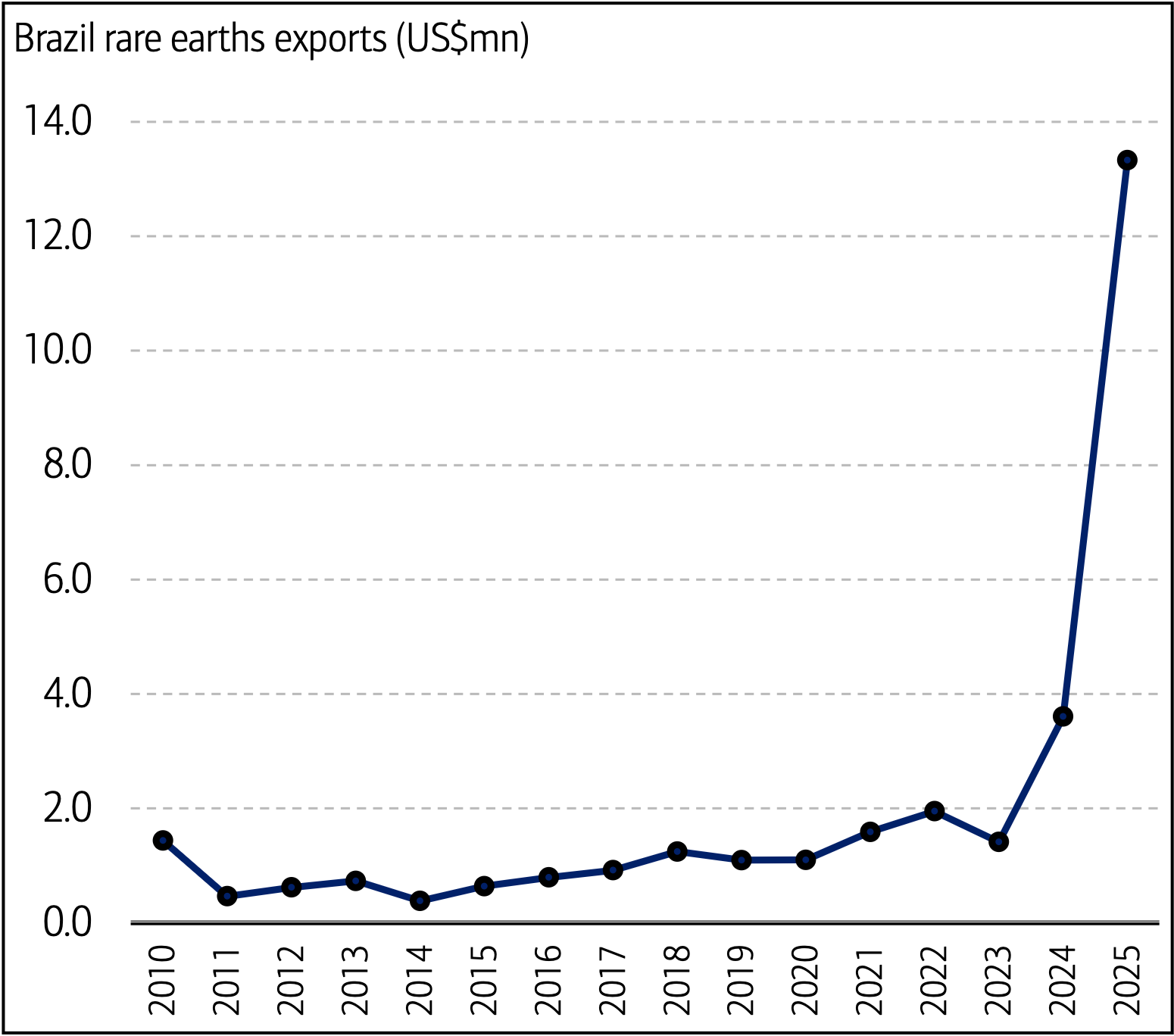

In 2025, Brazil’s rare earth exports reached a record $13.3M, a significant jump from $3.6M the year before. However, nearly all of these shipments went to China. This reflects the growth of Serra Verde, Brazil’s only major mine, but total production is still small compared to global demand.

As a result, Brazil exports raw materials while importing finished goods, including 84% of its hybrid vehicles. This dynamic prevents the country from capturing the full value of its own natural wealth.

2025 Exports Surged on Serra Verde Start-Up

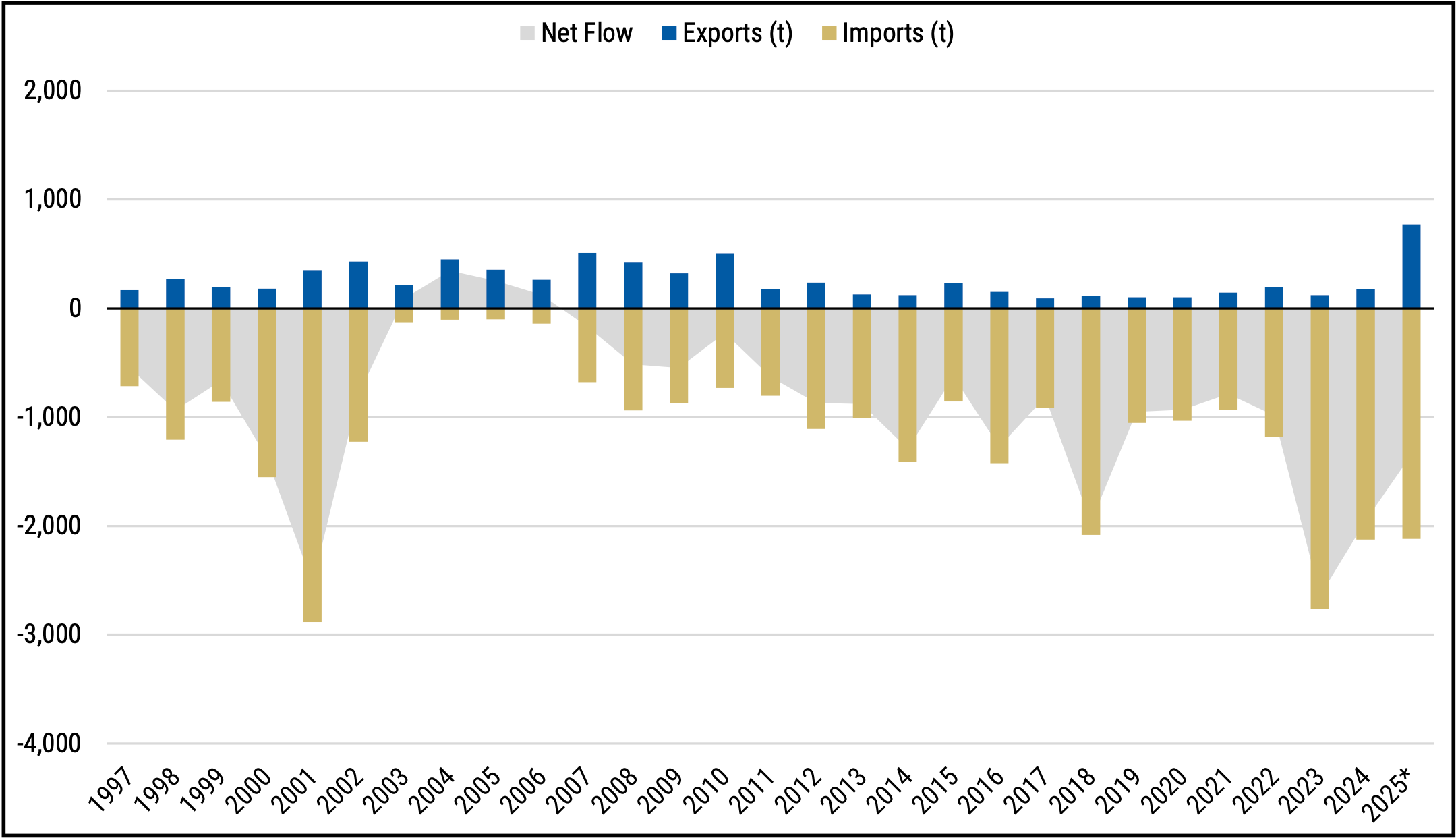

The export surge is only part of the story. While raw shipments jumped after Serra Verde began operations, Brazil still imports a huge volume of processed rare earth products. The trade balance for these high-value materials remains negative, highlighting the lack of local refining and magnet manufacturing.

Processed Rare Earths Minerals Trade Balance

Essentially, Brazil currently exports raw concentrates while relying on foreign refining for finished goods, a cycle we believe prevents the country from capturing the full economic value of its own mineral wealth.

Can Brazil Attract Global Trade Partners?

The United States is showing significant interest in Brazil to build alternative rare earth supply chains. Former officials point to Brazil as a critical mineral superpower and a strategic focus for reducing dependence on China.

This interest is backed by action: the US International Development Finance Corporation recently provided a $465M loan to Serra Verde. Following this deal, Serra Verde canceled its long-term contracts with Chinese buyers, with those shipments set to end by the close of 2026. Since China is the biggest producer of rare earths, why move away from them? The goal is not just about finding a better buyer, but about building a better partnership.

While China has been a reliable customer, the relationship has mostly focused on Brazil exporting raw materials and importing expensive finished goods. By shifting toward partners who offer technology and investment, Brazil can stop being just a supplier and start processing its own wealth.

At the same time, Brazil is expanding its partnerships beyond the West. In January 2026, Brazil and Saudi Arabia agreed to work together on strategic minerals. This agreement includes a joint working group to find new investment opportunities and expand geological mapping across Brazil.

A key part of this partnership involves Saudi Arabia’s Public Investment Fund (PIF) and Manara Minerals, which is already a partner in Vale Base Metals. Both countries are focused on building processing plants in Brazil so they can add more value to the minerals before they are exported.

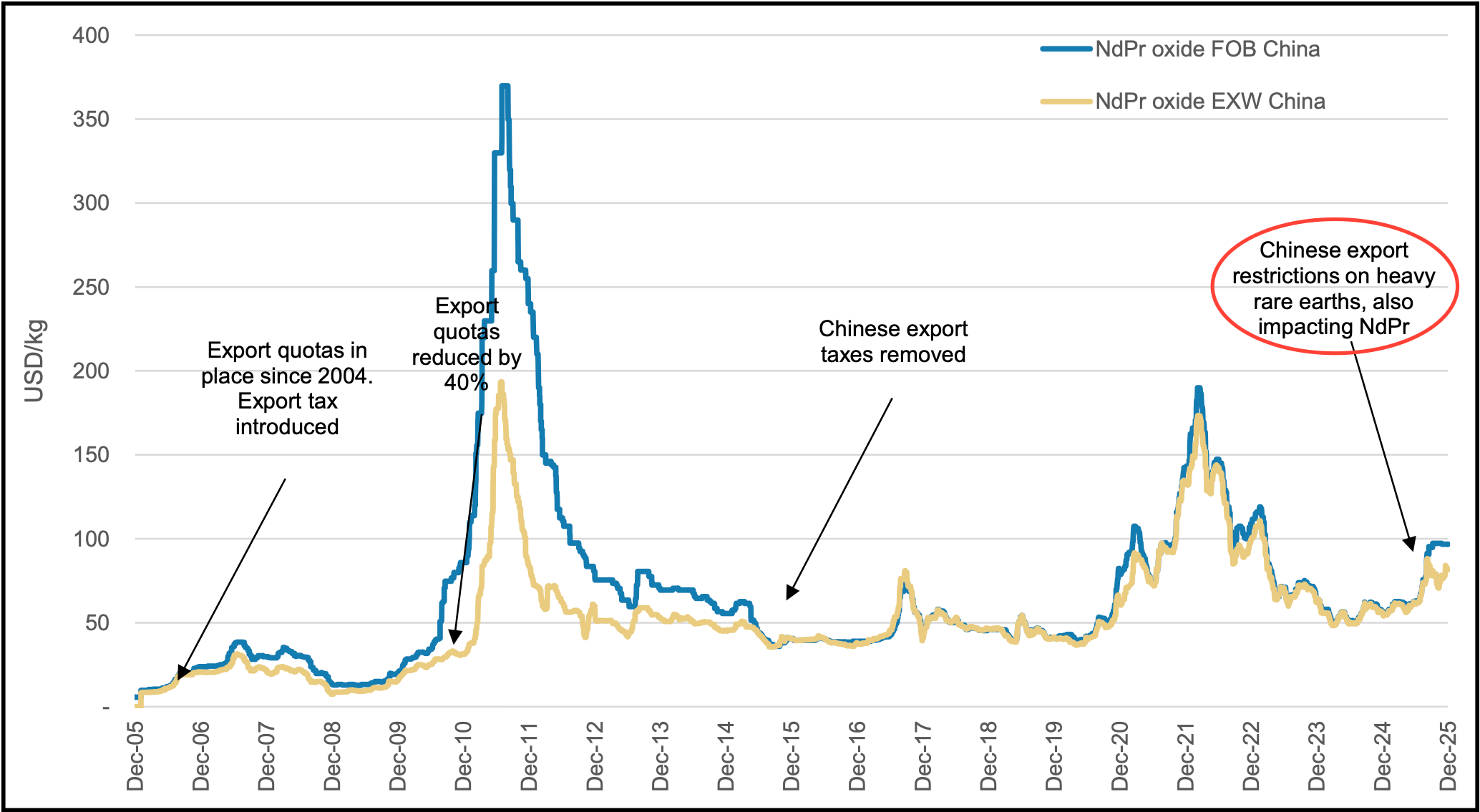

Market Volatility & China’s Pricing Gap

The global rare earth market is currently split by a massive price difference between China and the rest of the world. In early 2026, Chinese export controls have driven international prices for heavy rare earths like dysprosium and terbium to levels five times higher than those inside China.

China’s Influence on Rare Earth Pricing

For example, while dysprosium sells for around $200 per kilogram in China, it costs nearly $1,000 everywhere else. This price gap exists because China still refines around 90% of the world’s rare earths. By controlling the processing stage, China can keep domestic costs low for its own manufacturers while restricting the global supply. To fight this, the United States and its allies are creating price floors and new supply chains. We believe these efforts are designed to protect Western mining projects from price swings and ensure they remain competitive, even if China increases supply.

Summary of Brazil’s Main Projects

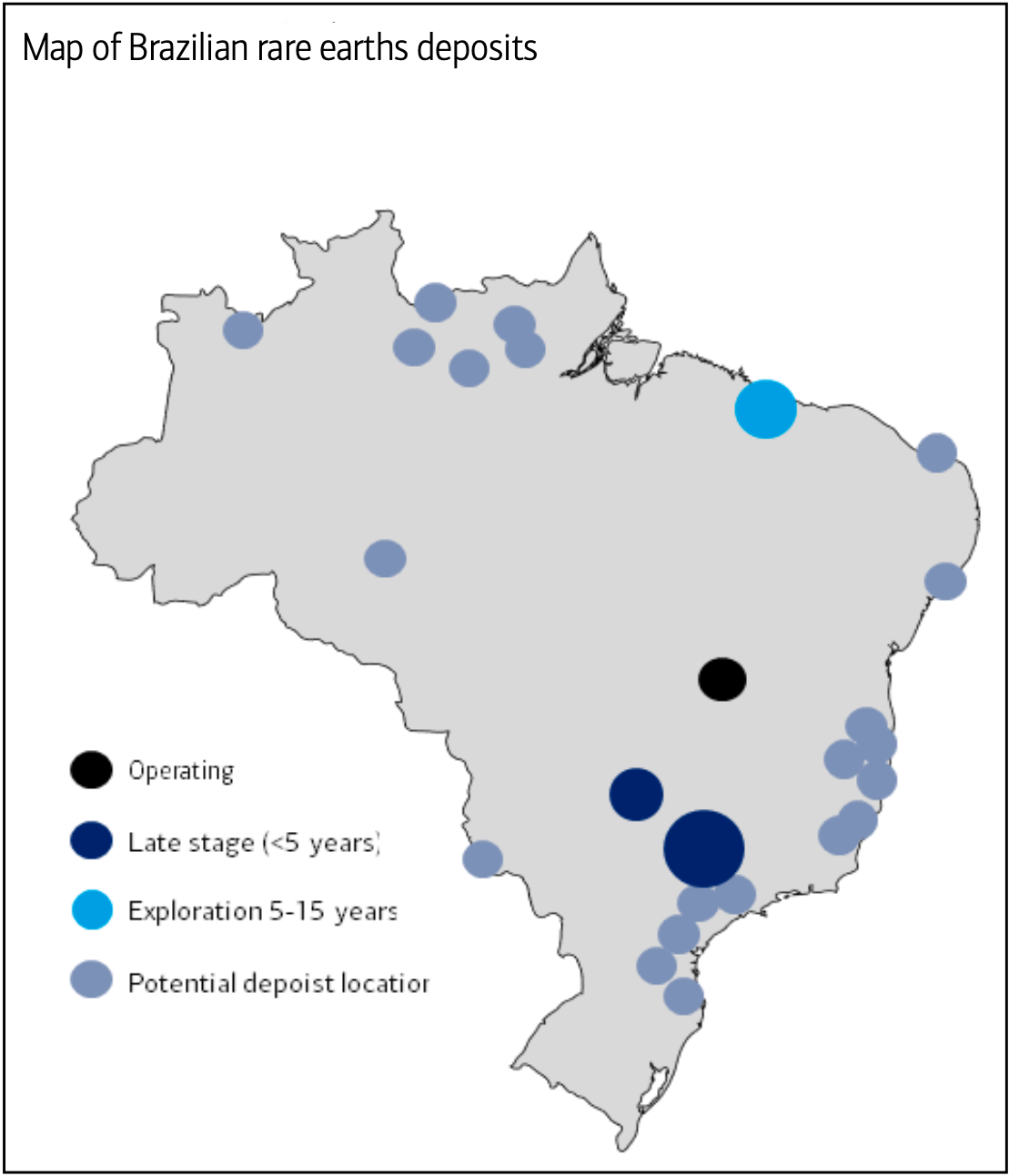

Brazil is currently positioning itself as a global leader in ionic clay rare earth projects, leveraging a favorable geological environment to develop multiple sites across the country. Early exploration has confirmed significant potential primarily in Minas Gerais, Goiás, and parts of Bahia.

Most Projects Are Concentrated in Minas Gerais and Goiás

In our view, the grades observed in these Brazilian ionic clay systems are highly competitive with global benchmarks. For instance, exploration in southern Minas Gerais has returned metallurgical recovery rates as high as 81.7% for total rare earth oxides, with magnetic rare earths accounting for over 60% of the yield. This high concentration of magnet metals is a critical advantage that we believe will accelerate Brazil’s transition from a raw material exporter to a central player in the global high-tech supply chain.

LREEO Dominates Project Share

Aclara Resources (ARA.TO): A Compelling Vertical Integration Play

Aclara Resources offers a differentiated strategy for gaining exposure to heavy rare earths. Listed on the TSX since 2021, the company maintains strong backing from major shareholders Hochschild Mining and CAP.

Aclara is advancing a "mine-to-magnet" strategy built around three core divisions that transition the business from simple resource extraction to high-value processing and end-market products.

Vertical Integration Strategy

Aclara is developing an integrated platform spanning mining, separation, and downstream metals and alloys to feed permanent magnet production. This strategy aims to control more of the value chain, enhance supply security for customers, and reduce reliance on China for critical processing steps.

1. Aclara Resources: Mining & Ionic Clay Assets

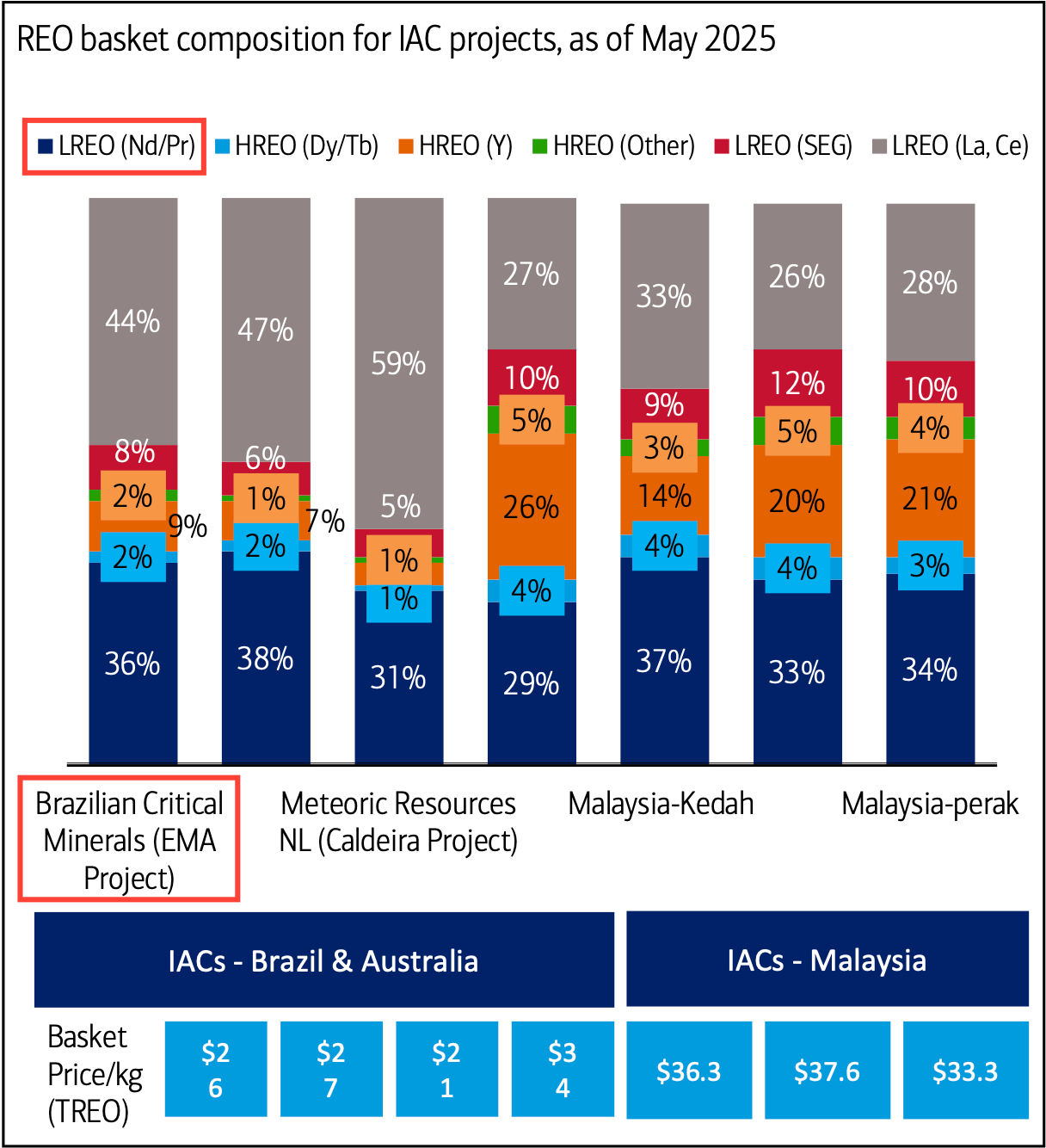

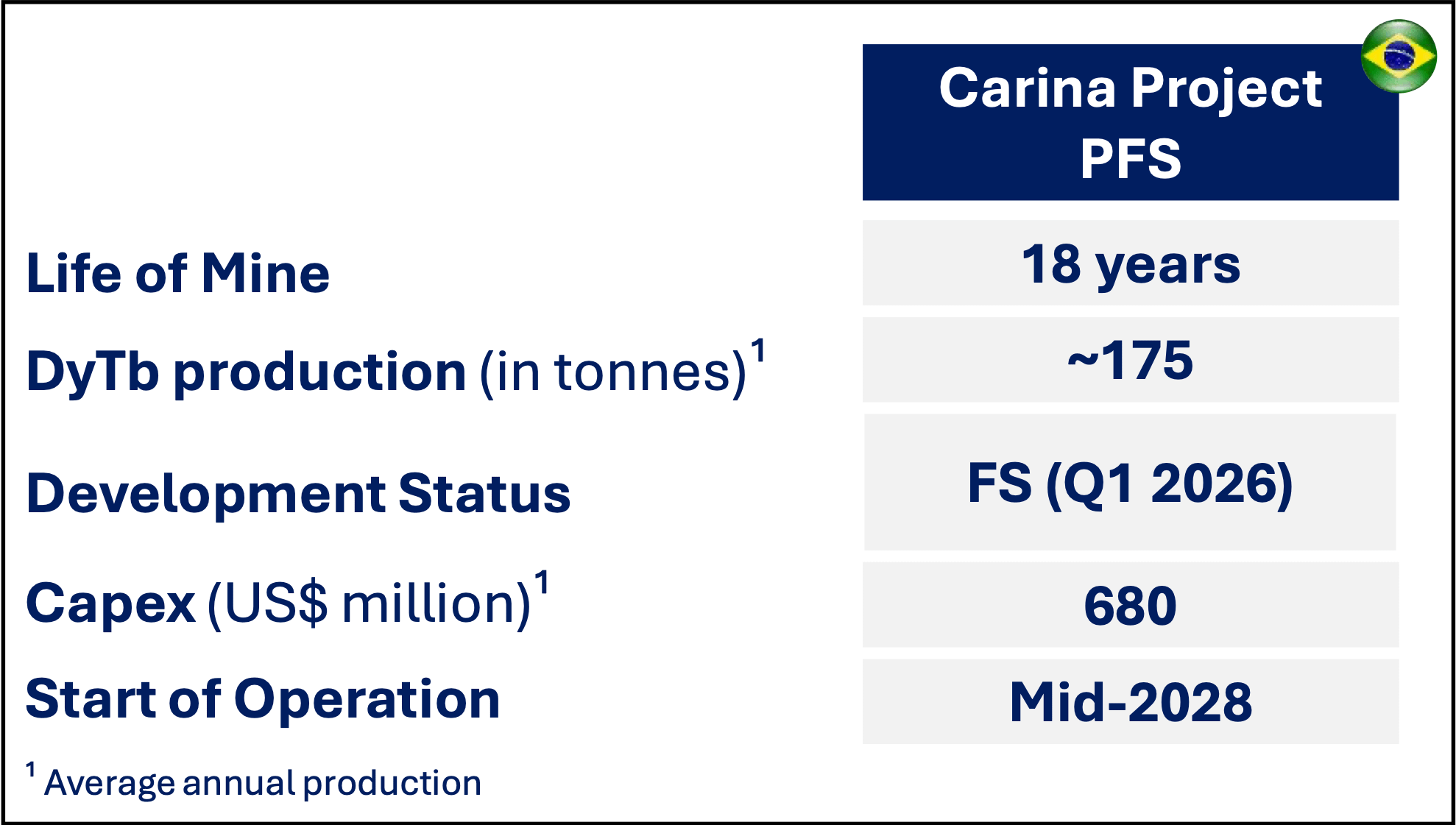

Aclara intends to produce mixed rare earth carbonates from two primary ionic clay deposits in Chile and Brazil. The Carina project in Nova Roma, Goiás, hosts probable reserves of 165.4M tonnes. These assets are significant due to their heavy rare earth weighting.

Carina Project

Production from these sites could represent ~16% of the dysprosium and terbium volumes produced by China in 2023. These elements are critical inputs for high-performance magnets that must remain reliable under extreme heat, and they are well represented in its resource base.

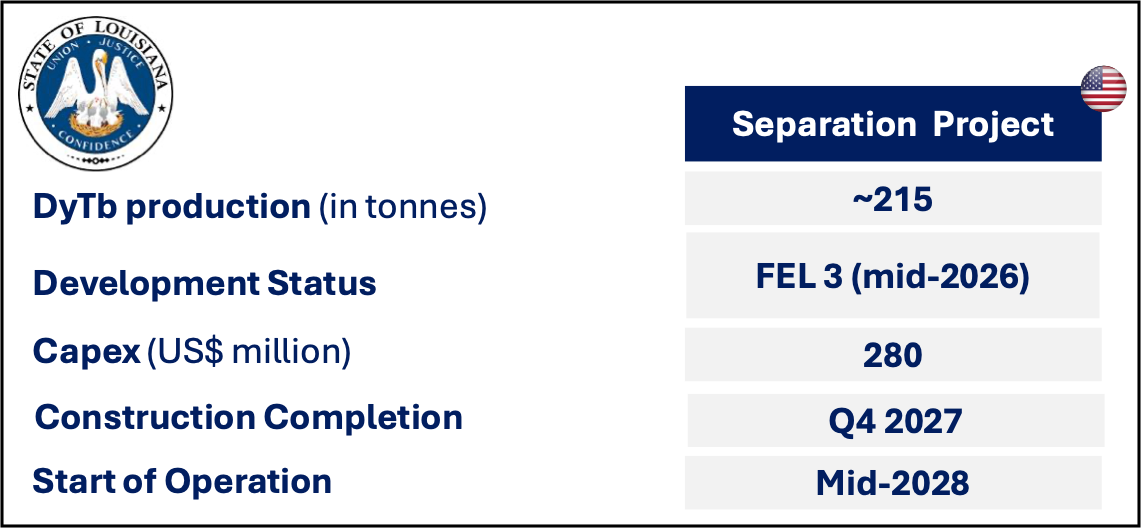

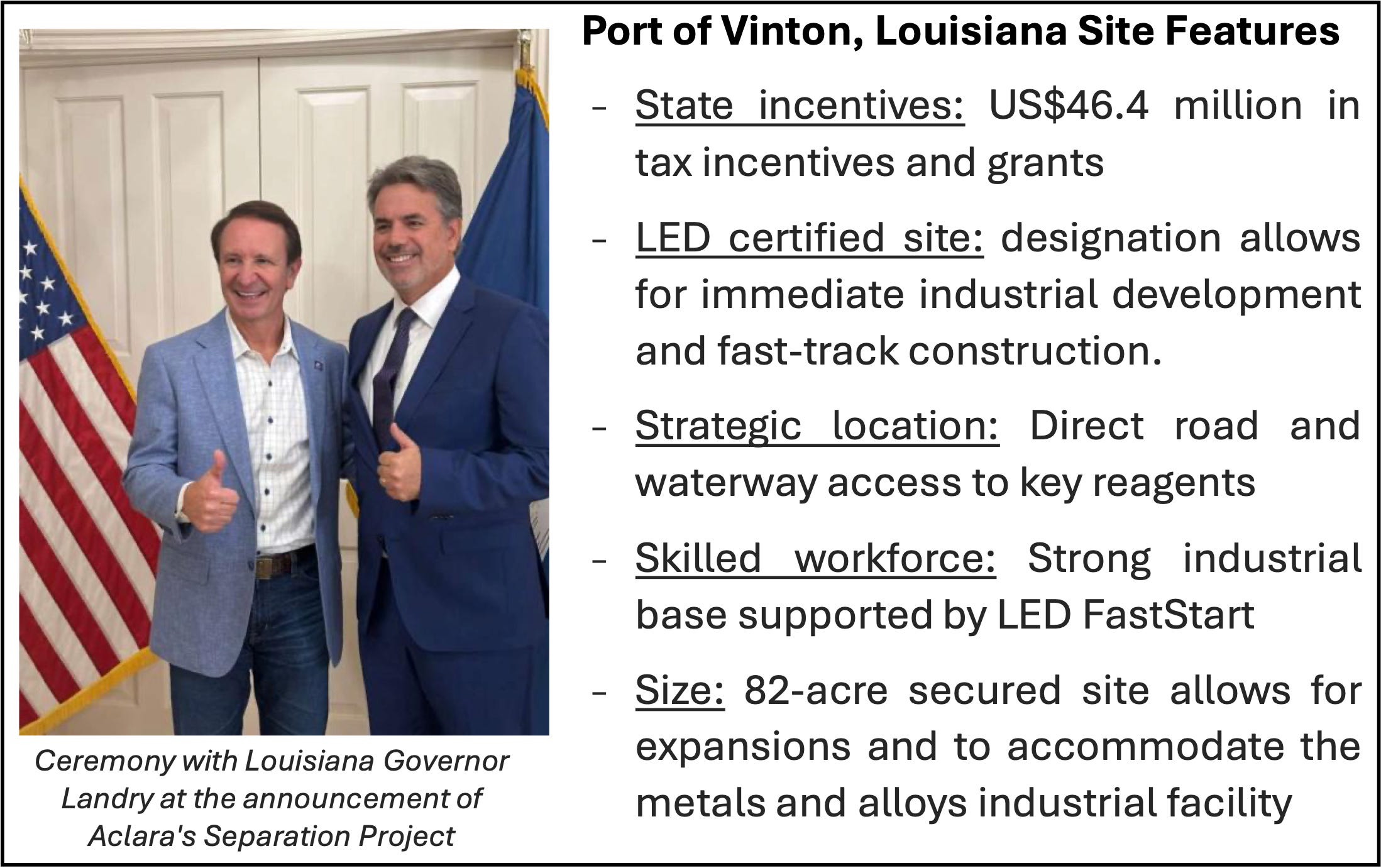

2. Aclara Technologies: U.S. Based Separation

Aclara Technologies focuses on converting mixed rare earth carbonates into high-purity rare earth oxides. The company is developing a separation facility in Louisiana, positioned as a key processing link in a Western supply chain.

Because separation remains a primary bottleneck outside China, we think a domestic facility would increase supply security, improve commercial flexibility, and strengthen Aclara’s competitive position as Western buyers seek dependable alternatives.

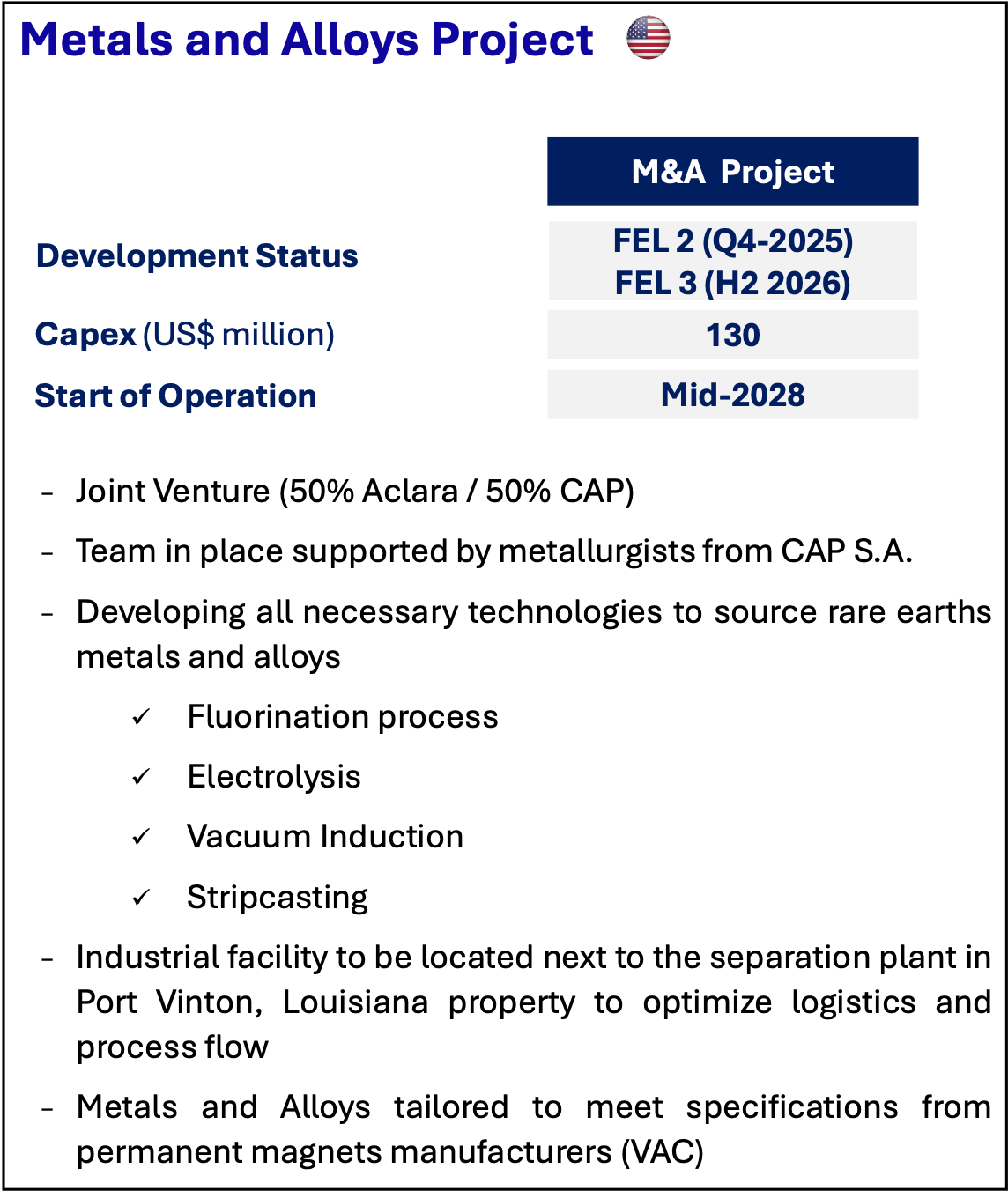

3. Aclara Metals: Alloys & Magnet Precursors

Through a joint venture with CAP, Aclara intends to produce the finished metals and alloys used by permanent magnet manufacturers, specifically targeting demand tied to electrification. A pilot facility in Chile is currently testing the metallization process using oxides from its own production.

We expect the full-scale metallization facility to be located alongside the separation plant in Louisiana, supporting a centralized U.S. manufacturing hub and optimizing logistics across the processing chain.

Financial Outlook & Operational Maturity

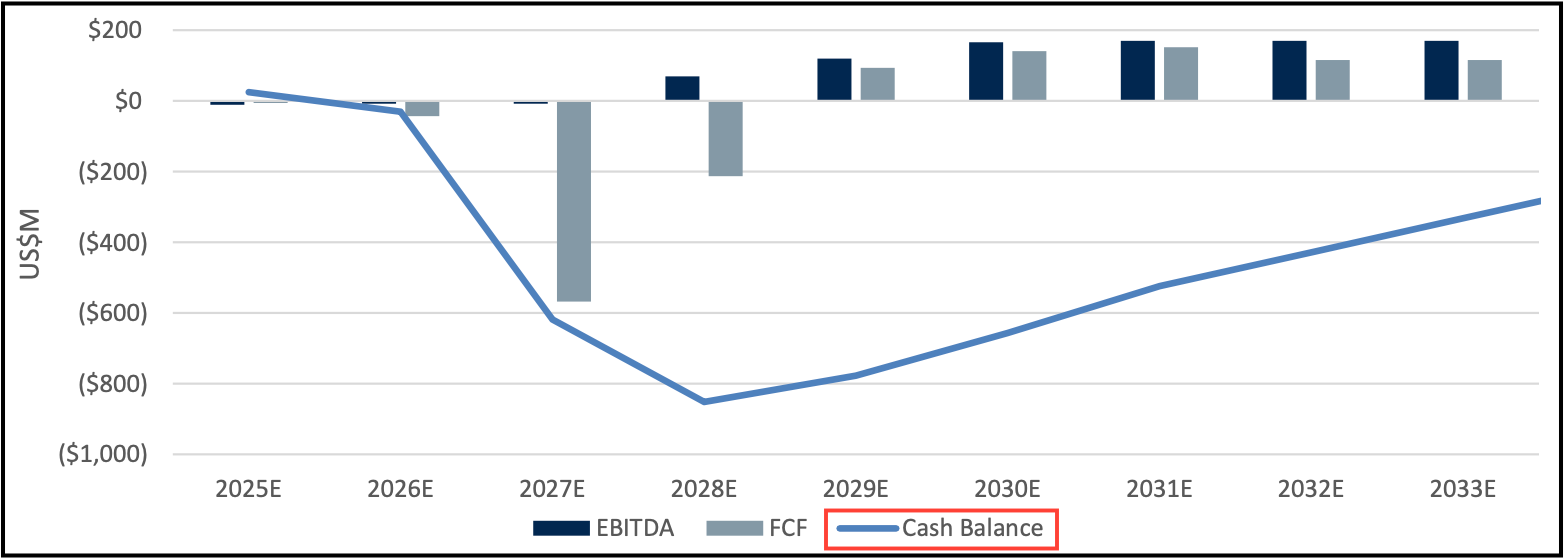

The company’s financial profile through 2033E reflects a shift from capital-intensive development to operational maturity. EBITDA is expected to turn positive in 2028E and grow steadily into the early 2030s as mining and processing reach full scale. Free cash flow follows is expected to follow the same path, moving from negative during the investment phase to sustained positive generation once the projects are fully operating.

The cash balance declines between 2026E and 2028E, bottoming in 2028E due to peak capital spending and development costs. From 2029E onward, cash begins to recover as EBITDA expands and free cash flow stays positive.

This follows a typical development curve for a high-quality mining asset. The near-term cash drawdown is needed to unlock operating leverage and long-term cash generation, positioning it as a leader in the heavy RE market.

EBITDA Growth & Balance Sheet Recovery (2025E-2033E)

Valuation & Upside Potential

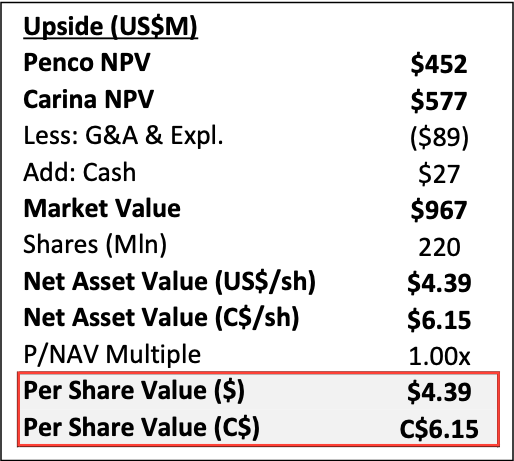

From a valuation perspective, analysts estimate a significant upside with a net asset value per share of $4.39, or C$6.15. This reflects the high economic potential of the Carina and Penco projects as they move toward production.

RBC Valuation Framework

In our view, this valuation framework highlights the massive latent value within Aclara’s portfolio. The company is currently trading at a level that we believe fails to account for its unique position as a vertically integrated heavy rare earth producer. As the market begins to price in the 2028 production milestones, we expect this valuation gap to close.

We are not buyers of Aclara yet, but we are watching it closely. The stock’s discount to NAV is not especially compelling for an asset that is still a few years from production, so we think caution is warranted. That said, it could become a strong opportunity later as the timeline de-risks.

Our Final Take

Brazil is now moving from potential to power. While the country has always had the reserves, it lacked the focus and the right partners to scale. Today, that has changed. With new 2026 agreements and massive funding from the United States and Saudi Arabia, we believe Brazil is building the foundations for high technology processing at home.

In our view, Brazil has the best chance in the Western Hemisphere to challenge the Chinese monopoly. They are the only ones with the right geology and a government willing to trade market access for technology.

While the road to full magnet production will be difficult, the current momentum suggests they will succeed. We think Brazil is finally ready to stop being a raw material supplier and start being a strategic leader.

The Aurelion Team

Disclosures & Methodology

you need to look at npk.to for rare earth Brazil exposure : Huge deposit, high PPM, no containments, low processing costs, easily accessible. Under the radar, but potentially the best resource in Brazil.

Verde AgriTech Reports New Best Intercept: 13.0 m at 0.83% TREO including 8.0 m at 1.01% TREO; 25% of Drilled Metres ≥0.40% TREO

Globe Newswire

jan 26, 2026

BELO HORIZONTE, Brazil / SINGAPORE – January 26, 2026 – Verde AgriTech Ltd. (TSX: NPK | OTCQX: VNPKF) (“Verde” or the “Company”) is pleased to report additional assay results from its ongoing drilling program at the Minas Americas Global Alliance Project (the “Project”) in Minas Gerais, Brazil.

“Our first drilling target (PT-34) is already delivering the combination that matters in rare earth discoveries: shallow thickness, repeated high grades, and a magnet‑rich rare earth basket,” said Cristiano Veloso, Founder and CEO of Verde. “With significant intercepts now extending across PT‑34 and multiple holes finishing in mineralization, we are prioritizing scale capture. Given the strength of results so far, the Board has approved expanding the resource definition footprint and drilling additional metres to better outline the district‑scale potential of the Project. Our objective is to define more tonnes of higher‑quality, magnet‑rich mineralization before finalizing scoping‑level economics.”

“In parallel, the Board has directed the Company to prepare the Project’s technical disclosure under Canadian NI 43‑101 and to develop U.S. SEC Regulation S‑K Subpart 1300 (S‑K 1300) aligned disclosure, including a Technical Report Summary as applicable,” added Mr. Veloso. “This dual‑track approach enhances comparability for global investors and preserves strategic flexibility as we advance the Project.”

This release reports assays from 24 additional holes totaling 244.7 m at the priority PT‑34 target, bringing drilling results reported to date to 27 holes totaling 279.8 m (280 assayed intervals).

Giant Red Flag for Aclara's Carina PFS was using price/revenue assumptions that are totally unrealistic and failing to use the current spot price as a scenario. I would only assume it is unprofitable at current prices.

Compare that to the Ionic Clay projects in Minas Gerais that are alluded to in the article, and more specifically the ASX listed Meteoric Resources (MEI) and Viridis Mining (VMM) which both were profitable when their PFS was released last July by using the then spot NdPr price of US$60/kg. Their capital intensities vs NdPr/DyTb output are also so much lower so banks would most likely prefer funding them. You could also buy both companies (US370m and US180m respectively) and still have change left over before you consider buying Aclara's market cap of US560m.