An Overlooked AI Software Leader Generating Substantial Cash Flow

Differentiated Growth in a Post-Boom SaaS Environment.

We are adding this stock to the Aurelion Index today.

The company is an undervalued software leader that we believe should trade at a higher and more normalized multiple. It has not received the attention it deserves for its highly profitable business model and rapid AI innovation. This disconnect is exactly what makes it attractive to us.

Introduction

The software industry is maturing fast. Companies are investing heavily in digital tools to compete. Cloud software is now the backbone of business.

While giants like Microsoft and Salesforce led the early charge, the next phase of growth belongs to platforms that merge communication with customer engagement. Organizations are leaving fragmented systems behind for unified solutions that simplify modern business.

Artificial intelligence is also transforming the landscape. We are moving past simple automation to a world of Agentic AI. Intelligent tools now manage entire workflows rather than just repetitive tasks. This shift creates a massive opportunity for providers that can deliver high value intelligence beyond basic transcription. For industry leaders, the competitive edge now relies on product velocity and technical depth.

This year is a turning point for the sector. The way software is delivered and supported is changing. Recent analysis from Rosenblatt suggests the industry is moving away from a brokerage model of simply passing leads. It is shifting toward a framework built on being a Solution Trusted Advisor. In this new pay to perform environment the winners are those who can handle complex deployments while maintaining continuity through the entire sales cycle.

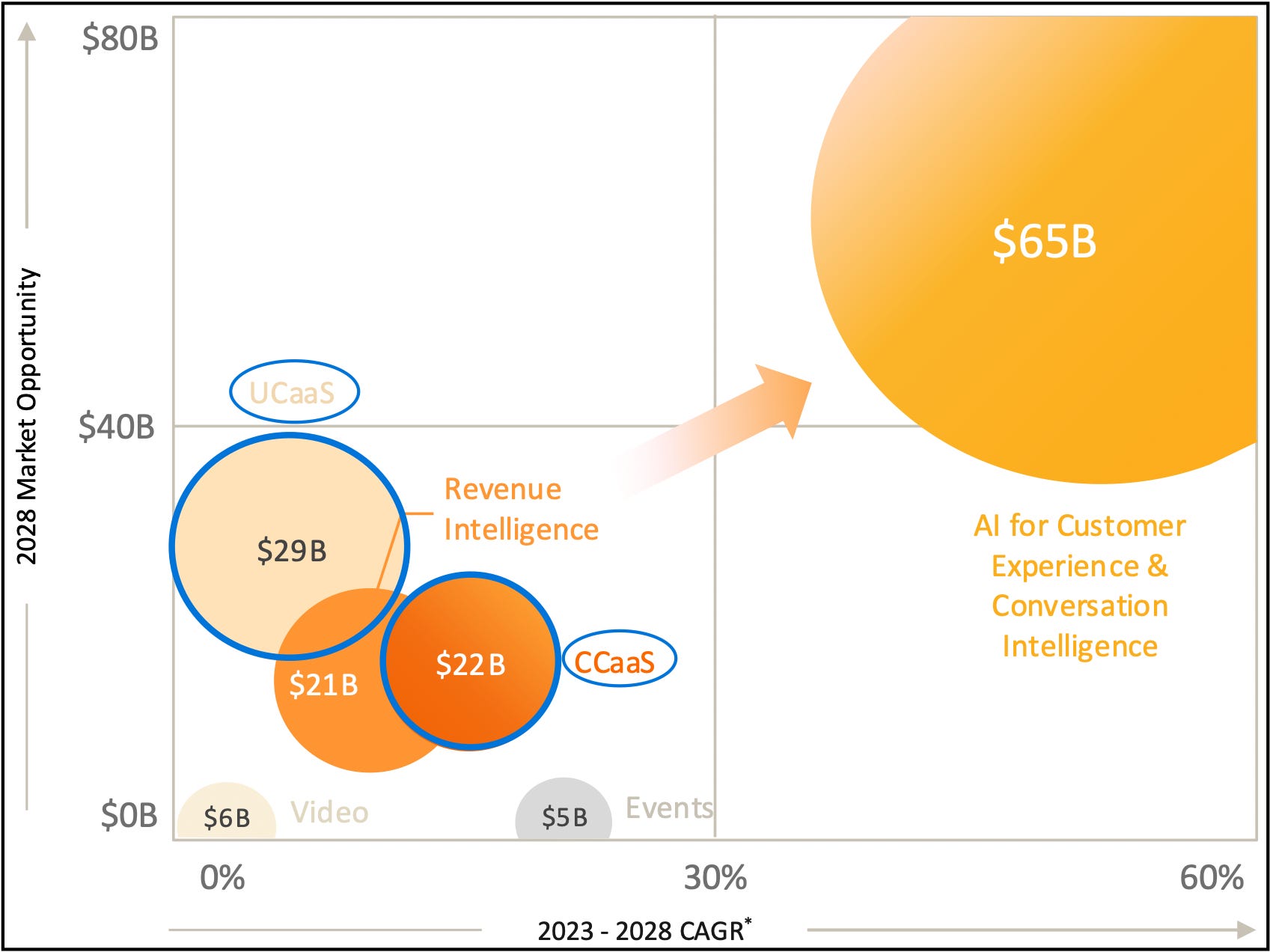

This evolution opens up a significant market opportunity. Bloomberg estimates the combined unified communications and contact center markets were valued at $44.7B in 2025. Projections indicate this figure will reach $59B globally by 2028. The company we analyze today currently holds a market share of ~6% within this space. While other industry evaluations place the current market size above $50B, this company’s management suggests that, adding AI, the total addressable opportunity exceeds $150B annually.

We believe that, given the current penetration rate in the total addressable market, there is still enough room for continued, significant sales growth for the foreseeable future.

The Market Opportunity is Large at ~$150B

In this changing landscape the stock we analyze today stands out as a primary disruptor by prioritizing research and development. Rosenblatt highlights that the company released ~1,600 features in the last year alone.

This aggressive focus on AI driven products like its new autonomous agent solution positions the firm to capture significant value in the intelligence market. Rosenblatt views the initial 2026 revenue guidance of 4% to 4.5% as conservative to account for macroeconomic caution but notes the underlying trend points to exceeding expectations. The firm has set a strategic target of reaching $1B in AI driven annual recurring revenue by 2028.

We believe this ambition proves it has the technical discipline to build a sophisticated enterprise communications engine in an AI first world.

Why This Opportunity Exists

Current market valuations reflect a level of caution that appears disconnected from the strengthening operational results. While investors have been fixated on the transition from high growth to stability the underlying financial performance continues to exceed expectations.

Independent analysis indicates the stock trades at a significant discount to its intrinsic quality with a price to sales ratio of ~0.90x compared to a software industry average near 4.50x.

This pessimism persists even as the company delivers record operating margins and has raised its FCF outlook to over $525M for the current FY. Management has also decisively addressed capital structure concerns by securing a path to handle its 2026 convertible notes and repurchasing $117M in stock. We believe this behavior actively mitigates the risk of future dilution.

The broader market shift creates a powerful tailwind. As hybrid work becomes permanent, organizations are consolidating their tools. They require the combination of voice, video, and messaging that this platform delivers. By integrating agentic AI, including the new autonomous AIR agent, directly into its core architecture, the company is positioning itself to capture greater revenues from the intelligence layer, alongside its core seat based model.

With a strategic roadmap to reach $1B in AI driven annual recurring revenue by 2028, the firm is evolving into a more profitable innovation leader. The stability of its recurring revenue base supports reinvestment into product development and growth. This creates a compelling entry point for investors focused on the platform’s long term potential.

Investment Thesis

We are initiating coverage of this software provider. The business operates on a strong recurring revenue foundation and trades at a valuation that we believe fails to reflect its powerful FCF and revenue scale.