Amazon’s Moat: Fading or Getting Stronger?

Trading at One of the Lowest Valuation Multiples in Large-Cap Internet.

We will not add Amazon (AMZN) to the Aurelion Index because it exceeds our $50M to $15bn market cap mandate. That said, we find the current setup highly attractive. We are confident enough in this thesis to buy shares in our personal accounts, something we rarely do for mega-caps, as we typically find more edge in small caps.

Introduction

We almost never analyze mega-cap companies, but today we choose to cover Amazon. You might wonder why we are stepping outside our usual focus.

We believe the setup is favorable for a move higher.

We almost never look at the mega-cap giants, but we make an exception for Amazon today. The current setup looks too good. We believe the market mispriced the stock. Right now, it trades at 10.5x estimated earnings, which sits 44% below its 10-Y average of 18.6x. High-quality returns often happen when a market leader faces such a huge disconnect from its historical value.

Valuation Gap Extends to Retail: AMZN Below Walmart’s Average

We view this as a rare chance to get ahead. For the first time in a long time, Amazon appears significantly cheaper than Walmart. While WMT trades at 20.4x, AMZN sits at just 10.5x.

This rarely happens for a company that dominates tech and cloud computing. Instead of the typical high-growth premium, the market treats Amazon like it has less value than a standard grocery chain. We expect that gap to close as the company hits its stride and proves its earning power.

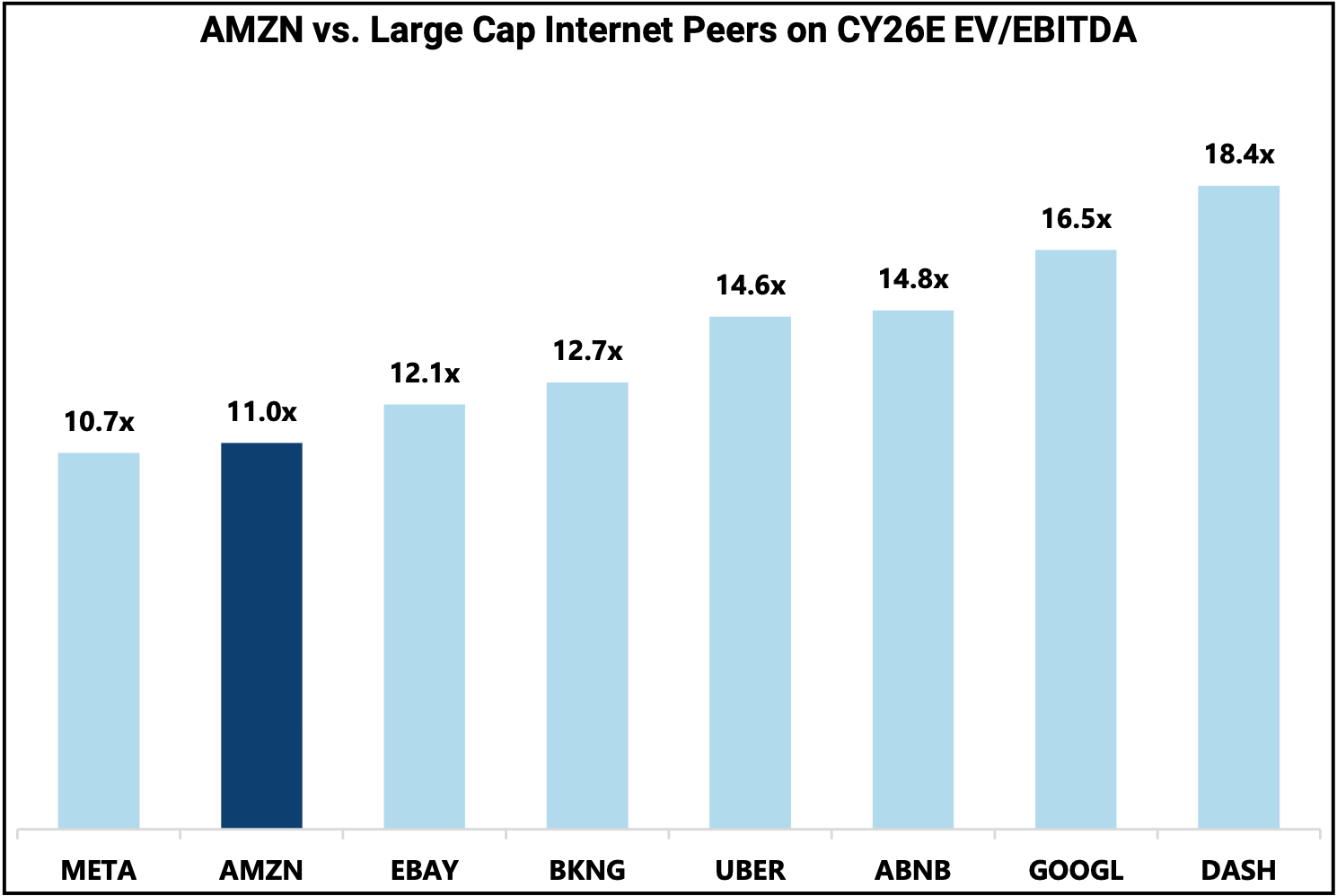

When you compare Amazon to its internet peers, the valuation looks even more disconnected. At 11.0x projected 2026 EBITDA, the stock trades at a discount to nearly everyone in the group. Companies like Uber, Airbnb, and Google all carry higher multiples. Even DoorDash trades at 18.4x, which is nearly double the valuation of AMZN. This price tells us the market expects a permanent slowdown, but our work suggests a recovery is coming. This low entry point should provide a safety net.

AWS: The Engine of Growth & Profit

AWS remains the most important segment for Amazon.

While the cloud business makes up 18% of the $717B in total sales, we estimate it provides 57% of the company’s operating income. In 2025, AWS generated $45.6B in operating profit with a 35% margin. Revenue for the segment grew 20% for the full year, with growth reaching 24% in the final quarter. As the dominant global cloud provider with a 30% market share, AWS serves as a strategic piece of the world’s AI infrastructure.

Resilience in the Retail Business

Amazon’s position in retail is still strengthening. We estimate the gap between it and competitors is widening. It now accounts for over 40% of the US eCommerce market. This massive scale lets them keep inventory closer to customers than any other player. Most of this logistics advantage now runs on autopilot, with robotics handling about 75% of global delivery volume.

This creates a cycle where higher volumes lead to faster deliveries and lower costs. These improvements naturally attract more shoppers. As they integrate more robots into retail, we project that efficiency will continue to climb.

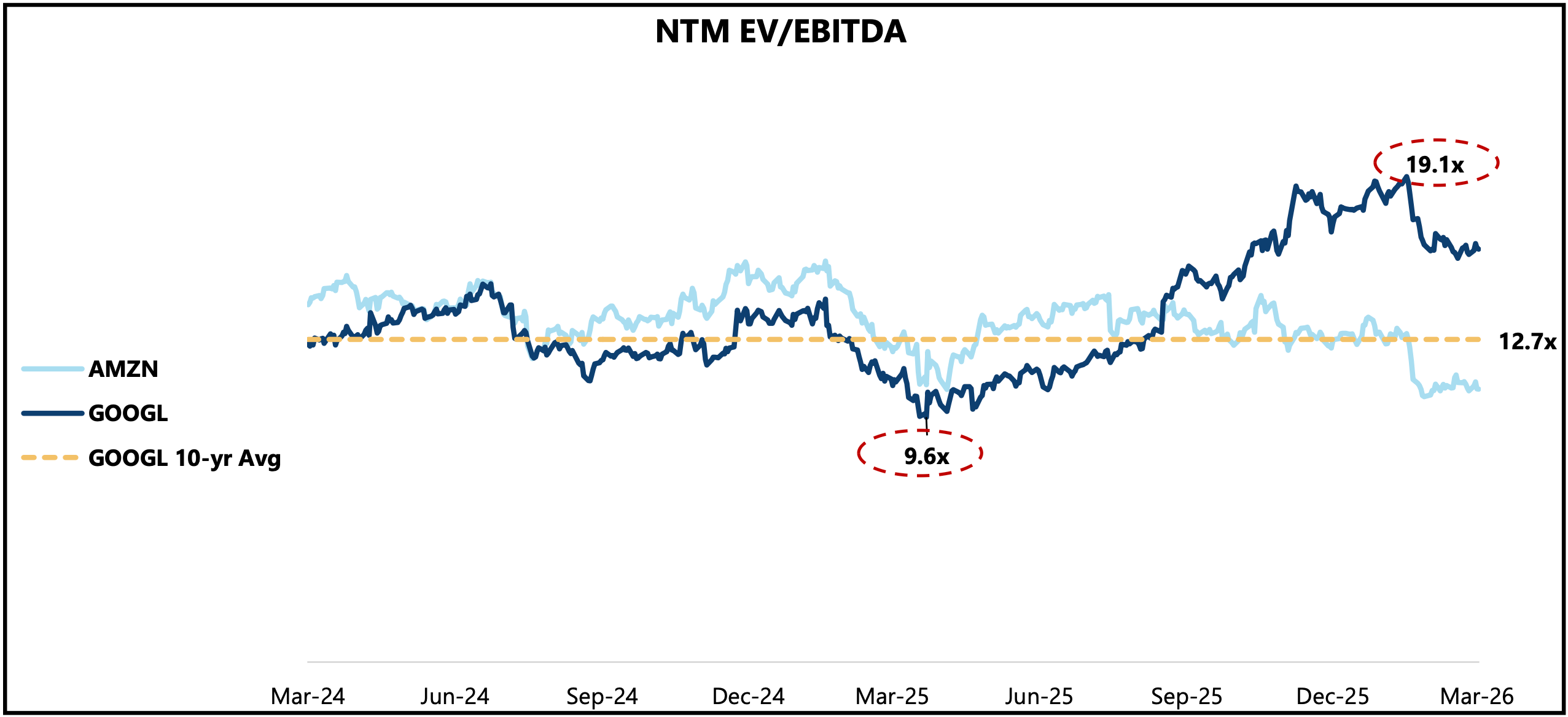

A Familiar Setup: GOOGL Then, AMZN Now

GOOGL sentiment bottomed in 1Q25 amid “AI loser” concerns and search disruption risks, then re-rated as Gemini progress validated its AI strategy, now trading well above its 10-year average.

We see a similar sentiment and valuation inflection emerging for AMZN.

Amazon’s Moat: Fading or Getting Stronger?

1. Retail Growth Dynamics

Amazon’s dominance in retail is widening rather than merely holding steady. While many traditional moats are being challenged by AI, Amazon is using technology to distance itself from the competition. With more than 40% of the US eCommerce market, the company has reached a level of scale that allows it to position inventory closer to consumers than any other player.

This logistics advantage is now heavily automated, with robotics playing a role in ~75% of global delivery volume. This creates a self reinforcing cycle where higher volumes lead to faster deliveries and lower costs, which in turn attract more customers. As robotics continue to be integrated into processes across the retail operations side, efficiency can continue to increase.

2. Capital Efficiency & ROIC

Amazon looks like a cash hungry machine because retail and AWS cost so much to build. However, the company generated a surprisingly high return on invested capital of 15% in 2025. This proves that the heavy spending on logistics and data centers actually pays off.

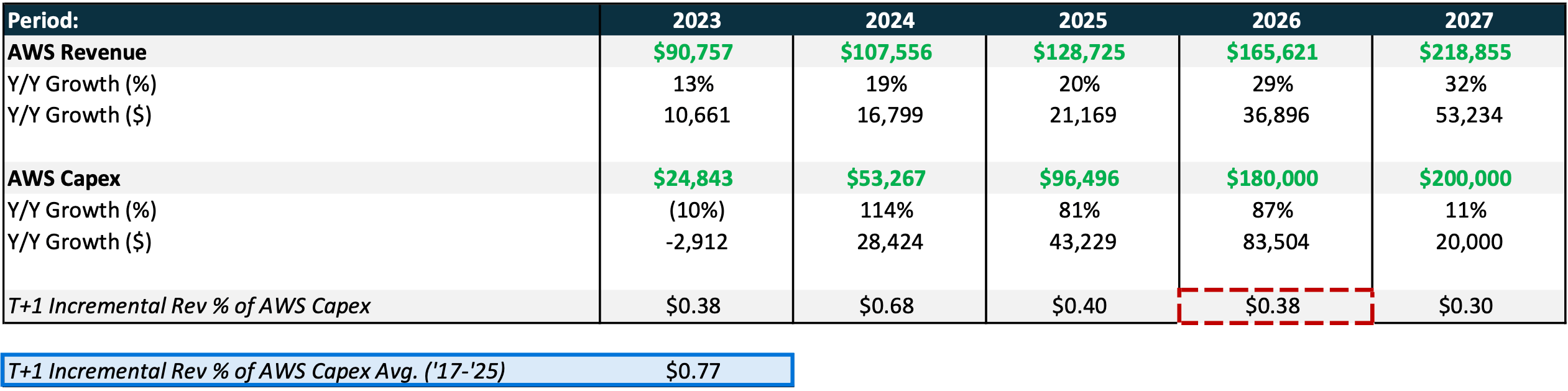

Incremental AWS Revenue & Capex

Oppenheimer expects AWS revenue to hit $194.8B by 2027.

By that time, AWS will likely account for 84% of total company spending. Between 2024 and 2027, Oppenheimer estimates that $104.1B in new revenue will outpace $100.9B in new spending. This points to an efficient investment cycle with strong returns. In retail, the setup allows suppliers to effectively fund growth. When revenue grows faster than spending, the infrastructure cycle is maturing and becoming more profitable.

3. The Valuation Anomaly

We find the most compelling part of the thesis in the current valuation disconnect. Applying the trading multiples of physical retailers like Walmart (43.5x NTM P/E) or Costco (48.4x NTM P/E) to Amazon’s retail and advertising segments implies the market assigns little to no value to AWS.

By that logic, anyone buying the stock effectively gets the world’s leading cloud platform and a $68.6B advertising business almost for free.

4. The Data Advantage

Amazon’s competitive edge is further solidified by a data advantage that physical retailers cannot replicate. Beyond knowing the purchase history of every customer, the platform tracks exactly what products were considered and then passed over. This first party data is now being extended beyond Amazon’s own properties through its DSP, allowing advertisers to target consumers across the open web with surgical precision.

How We See It

We view this as a massive dislocation in the market. The valuation gap looks extreme with the stock trading at 10.5x NTM EV/EBITDA.

This sits 43% below the 10-Y average and far below Walmart. While Walmart owns a massive global footprint and continues to build its own delivery networks, the retailer lacks an AWS equivalent. We believe this discount makes no sense. This offers an exceptional entry point for a business in the early stages of an AWS re-acceleration cycle as AI usage grows.

We think the market is offering an opportunity here.

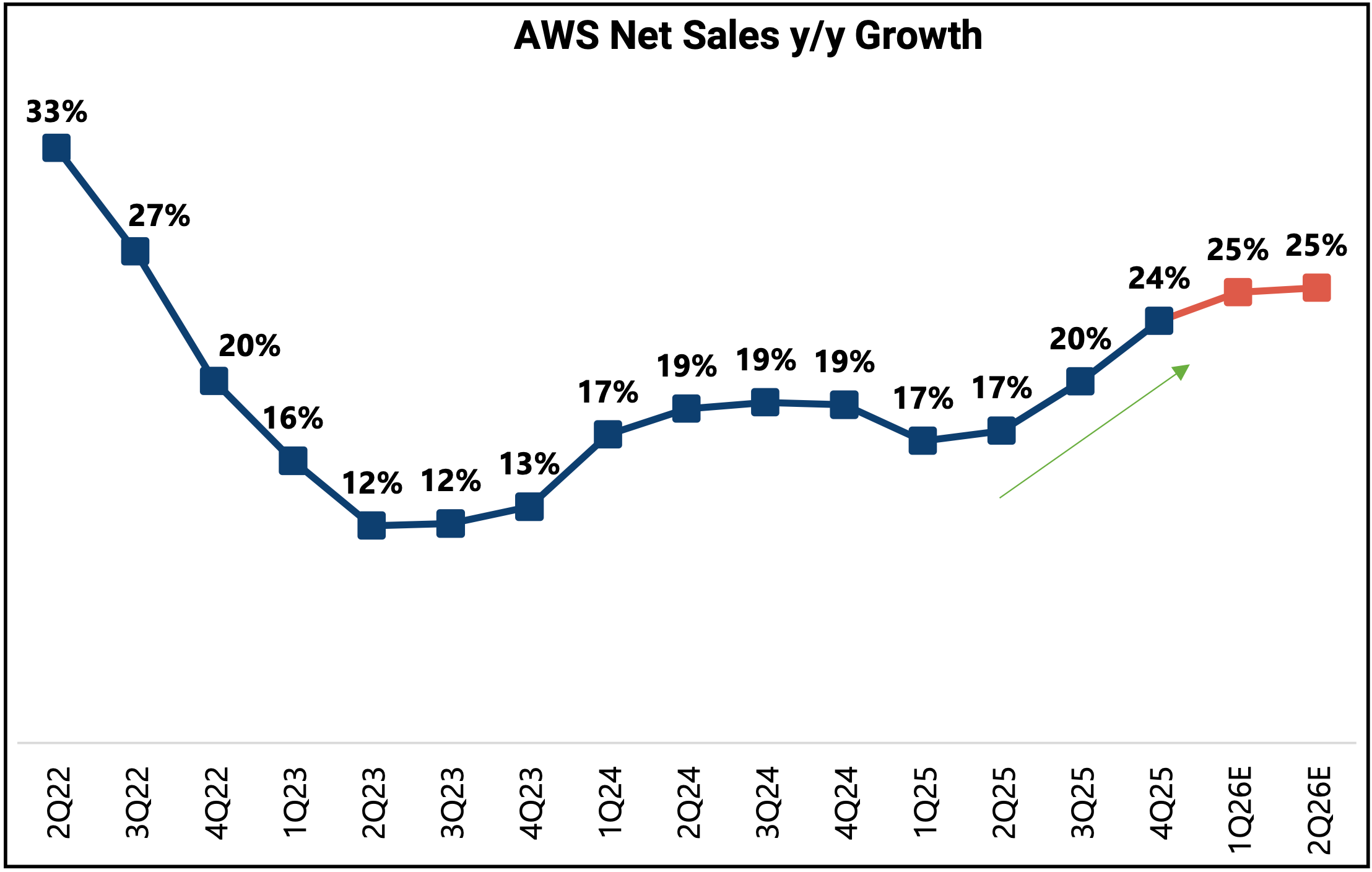

Favorable Set-up for an AWS Re-acceleration Cycle

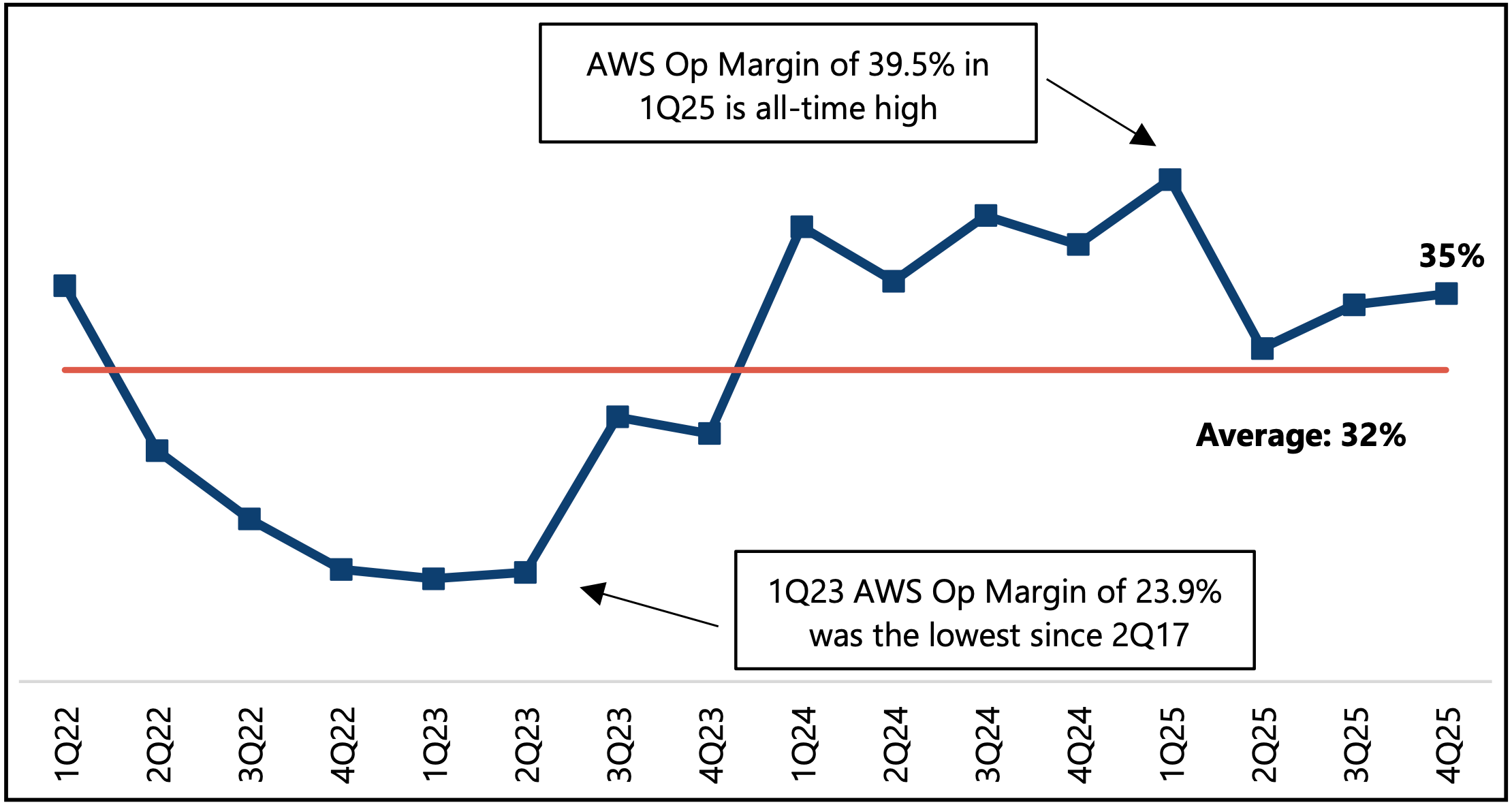

We believe the setup for AWS looks favorable as the segment enters a clear reacceleration cycle. After hitting a low of 12% growth in mid-2023, the business turned a corner. The trend climbed steadily upward, with growth rates returning to the 20% level as 2025 closed out. This indicates the slowdown has ended and the growth engine is running again.

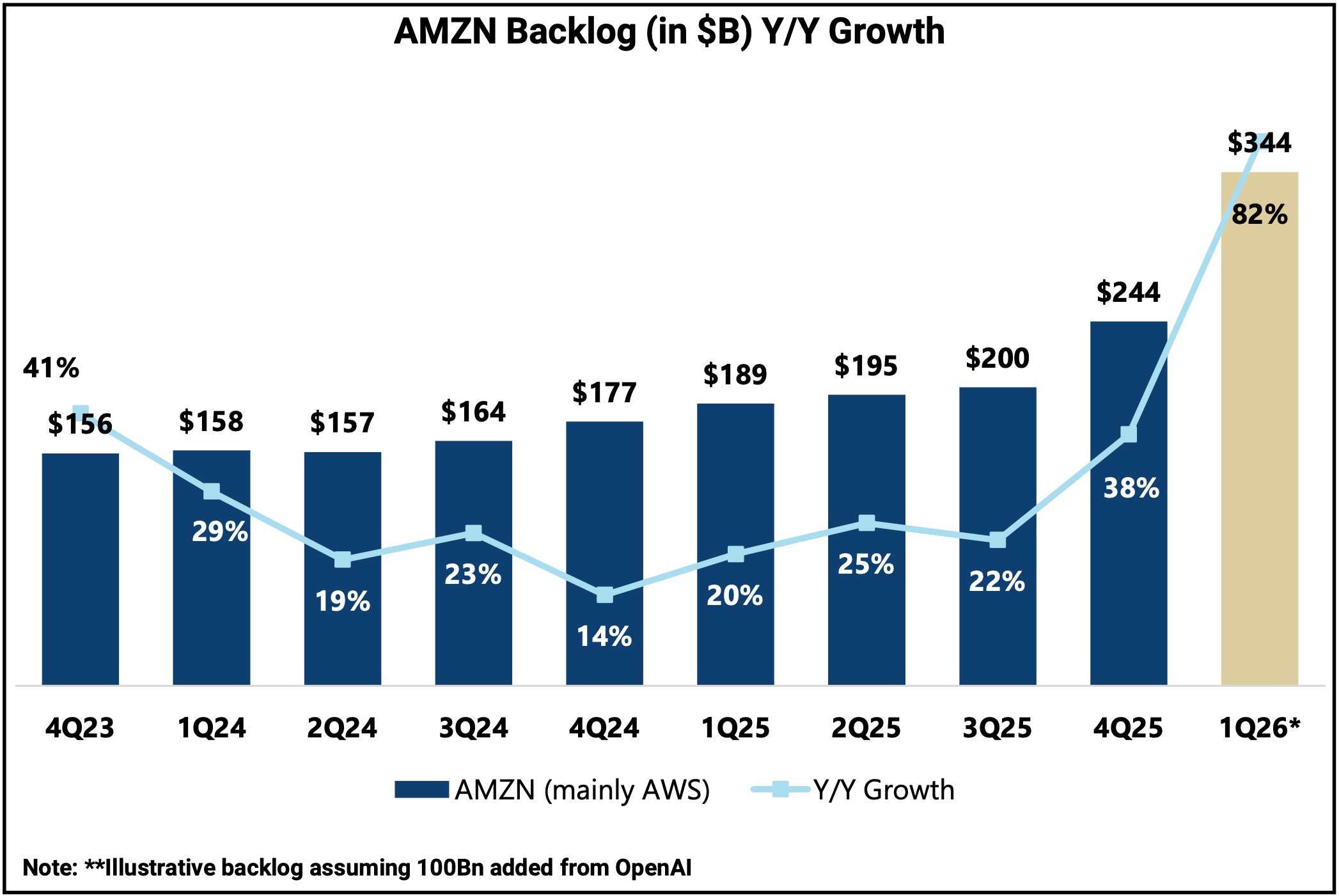

The backlog growth signals a massive revenue catch-up. The backlog reached $244B at the end of 2025, representing 38% growth. Jefferies projects a surge to $344B in early 2026, especially as major partnerships like OpenAI add to the pile. This pipeline provides a long runway for future revenue.

The profit story appears equally compelling. Operating margins recovered sharply from the lows of early 2023 when they dipped to around 24%.

We saw a strong bounce back with margins hitting record highs of 40% in early 2025. By the end of the year, they achieved a healthy 35%. This level sits comfortably above the long-term average of 32%.

AWS Margin Expands to 35%

Leadership remains confident in AI demand. The CEO notes capital spending follows workloads growing faster than expected. The CFO highlights that margins improved by 0.4% YoY. We believe these factors confirm that the investments in infrastructure already generate strong returns.

AWS Revenue Upside

When we look at Morgan Stanley’s revenue forecast, the estimates imply a yield on Capex that is ~50% below the long term average. This points to meaningful upside surprise potential, and we share that view.

AWS Yield on Capex Below Historical Average

Morgan Stanley’s current model assumes that for every dollar of Capex, the incremental revenue will be far lower than historical trends. Specifically, they project yields between $0.21 and $0.42. This is significantly lower than the long term average, which sits between $0.57 and $0.95. If AWS can deliver efficiency even partially closer to its historical standard, the actual revenue growth will likely exceed Morgan Stanley’s conservative estimates.

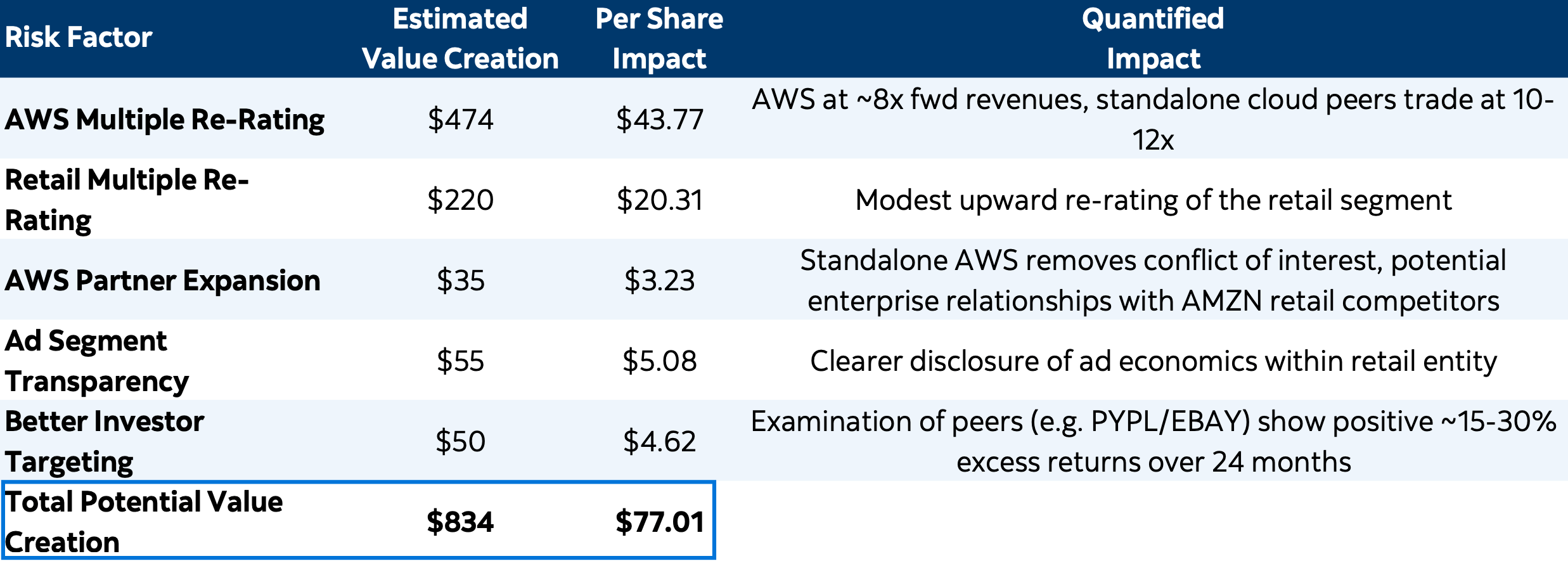

Quantifying the Upside of an AWS Separation

Scotia highlights the potential gains from spinning off AWS into its own company. A standalone AWS would likely trade at a higher price than it currently does as part of the consolidated group.

This premium comes from better investor clarity and the removal of retail spending from the valuation. More importantly, it allows AWS to sign cloud partnerships with retail competitors who currently avoid the platform because of conflicts of interest.

The retail business also benefits from a cleaner story. Management becomes directly accountable for how they spend money, and an independent board ensures the focus remains entirely on retail execution.

Historical data from other large-cap tech spinoffs suggests this move could lead to 15-30% in extra returns over the first 24 months. By simply removing the conglomerate discount, the market could surface several hundred billion dollars in total value.