Aerospace to the Moon? - Thematic Research & Small-Cap Idea

The Next Investment Supercycle

By Aurelion Research

Description: A look at how space is reshaping the aerospace cycle and creating more durable, cash-generative investment opportunities.

You may have read the title and thought this was about commercial aerospace, but that’s not what this is. The focus here is space. It is an interesting and sometimes complex industry, but also one of the most important areas of long-term technological and economic development. Don’t worry, we’ll keep it easy to follow. We’re not NASA engineers ourselves.

Aerospace is a long-cycle industry because time is the main constraint. Production capacity takes years to add, programs take time to qualify and certify, and supply chains adjust slowly due to tight process control.

These limits create persistence once demand turns. When activity picks up, the system cannot respond quickly enough, backlogs grow, and lead times extend. That is why upcycles tend to last.

Space is changing how this cycle works. Orbit-based capability is becoming a standard part of economic and security infrastructure. As launch and manufacturing become more repeatable, activity shifts away from one-time deployments toward ongoing fleet renewal. Demand becomes more recurring, driven by maintenance and refresh needs.

The market has been slow to adjust to this change. Capital is still often priced using older cycle assumptions, which can understate how durable cash flows have become. This report focuses on areas where fundamentals are strengthening faster than valuations reflect.

Now, let’s look at current aerospace valuation. On a next twelve month P/E basis, aerospace is trading at a clear premium to the S&P 500 and near the upper end of its range over the past 3 decades. The group has come down from the 2021 peak, yet it has held in the low 30s as backlog visibility and supply constraints continue to support confidence in forward earnings.

Aerospace Valuation History (1990-2026)

The key question is whether that premium already reflects cash flow durability, or whether dispersion across the group still leaves room for mispricing, which is the focus of this thematic report.

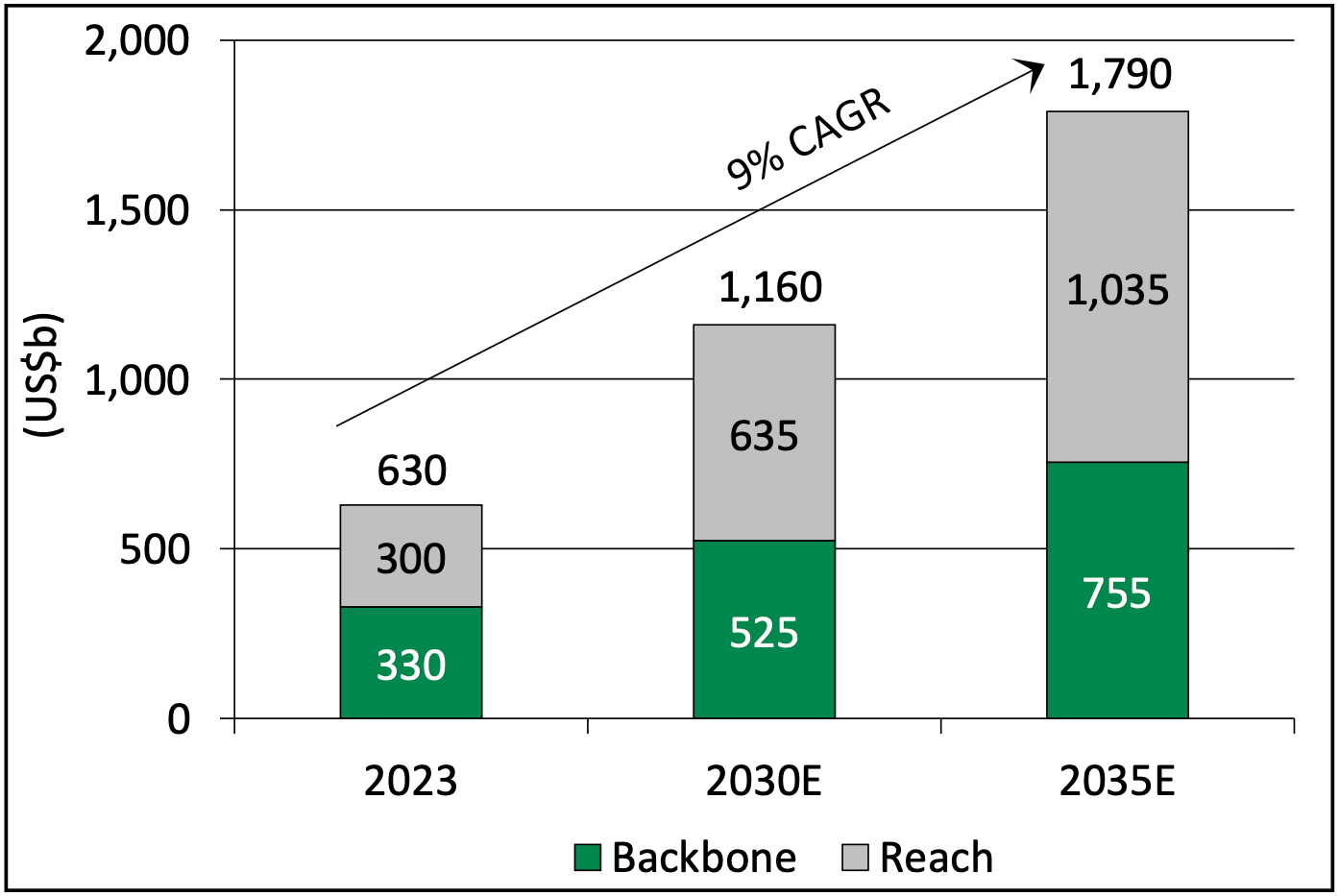

The space economy is split roughly evenly between backbone applications, forecast to grow at a 7% CAGR from 2023 to 2035, and reach markets, expected to grow at an 11% CAGR over the same period.

We believe the expanding range of space-enabled services supports a longer growth runway and creates room for companies to broaden their footprint and gain share across both private operators and government-led programs.

Forecast Growth of the Space Economy, 2023–2035E

In the chart above, the space economy expands from $630B in 2023 to $1.79T by 2035E, implying a ~9% CAGR, with backbone and reach markets remaining roughly balanced while reaching $755B and $1.04T, respectively.

We believe this profile supports a longer runway, as growth is driven by both the enabling layer and the industries that rely on it, supporting recurring demand over time. That backdrop should support our stock idea.

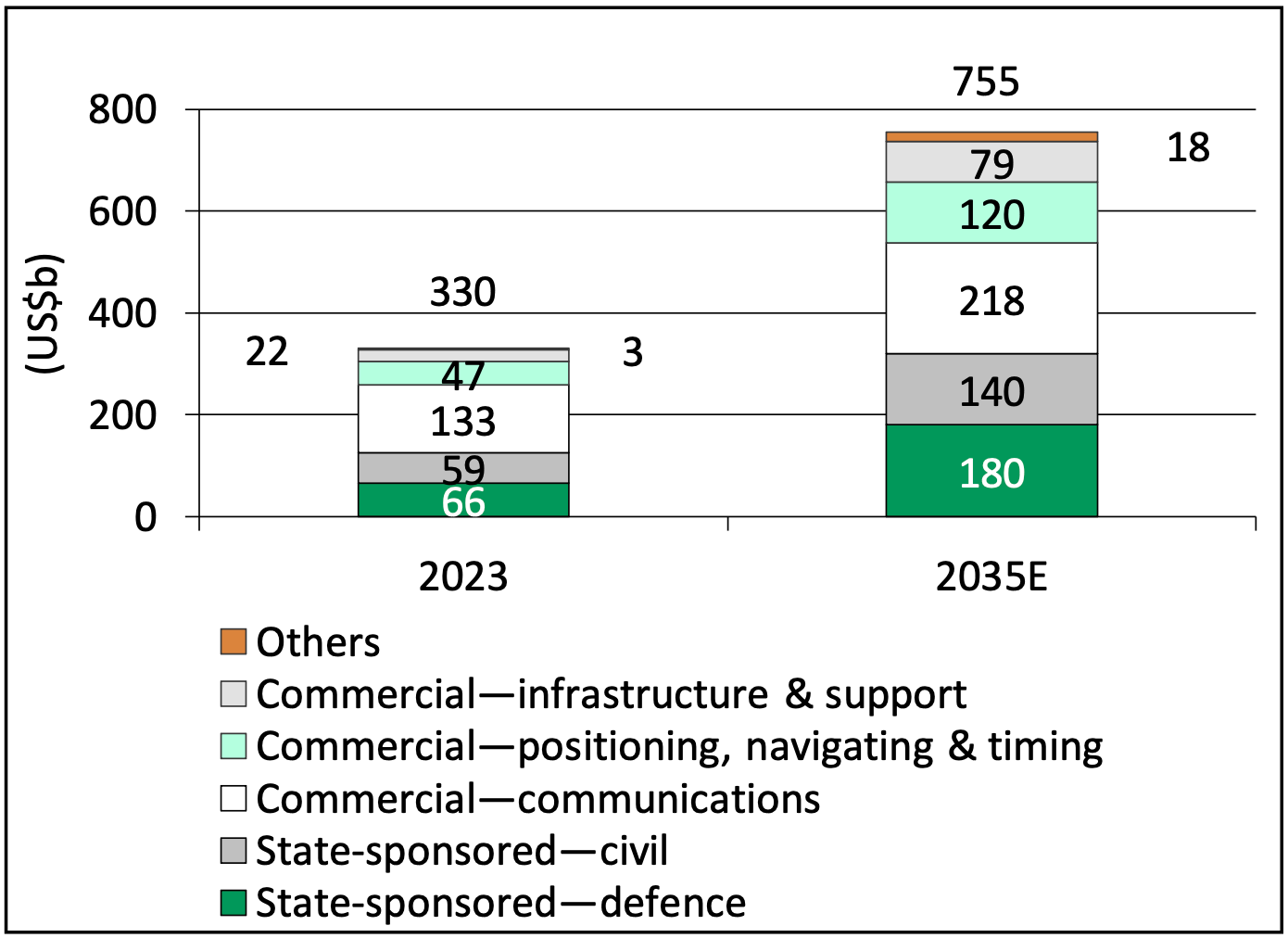

To support that view, we start with the backbone layer and break down where forecast growth is coming from through 2035E. As shown in the exhibit below, the mix reflects a broadening demand base, with state sponsored defense and civil spending expanding alongside commercial infrastructure, communications, and positioning, navigation, and timing.

Growth Breakdown of Backbone Applications, 2023–2035E

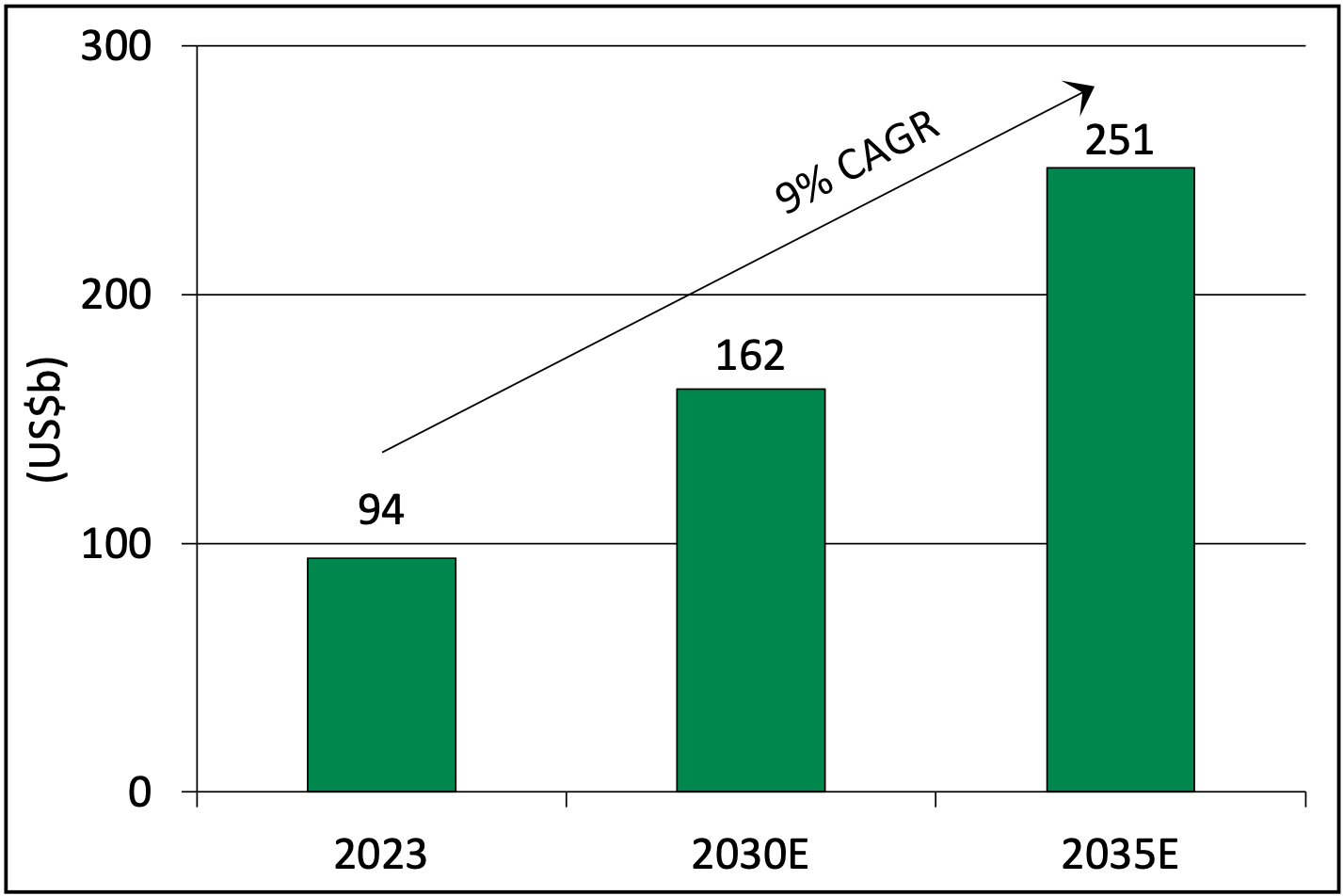

We now turn to the backbone layer, starting with state sponsored defense. As shown in the exhibit below, defense spending is forecast to rise from $94B in 2023 to $162B by 2030E and $251B by 2035E, implying a ~9% CAGR.

We believe this trajectory creates a durable demand floor, as procurement budgets support recurring activity and system upgrades that tend to persist even when commercial spending softens. We can see there is rising demand for space products and strong expected growth across the sector. The next question is whether state sponsored defense spending is expected to grow as well, since that can reinforce the demand base. The chart below suggests it is.

Growth in State Sponsored Defense Spending, 2023–2035E

Defense spending is forecast to rise from $94B in 2023 to $162B by 2030E and $251B by 2035E, implying a ~9% CAGR. We believe that pace supports a durable demand floor that can hold even when commercial spending varies.