A Not-So-Boring Defensive Small-Cap Compounder in an Uncertain Market

We believe this new stock addition is the perfect way to capture alpha through defensive positioning in an uncertain macro environment.

Today, we are adding a new stock to the Aurelion Index.

In a market as uncertain as the one we face today, you may have noticed that we are adding more defensive names to our Index. This does not reflect a preference for lower returns or reduced upside elsewhere. In fact, we believe that as inflation persists and the consumer weakens, the market will increasingly reward defensive plays. We are currently navigating another energy shock driven by the conflict between the US and Iran in the Middle East. While the inflationary impact might not be as severe as the 2022 shock in Ukraine, the effect is already visible.

In this environment, we believe our “defensive” positions are tactical choices designed to capture alpha while the broader market struggles with volatility.

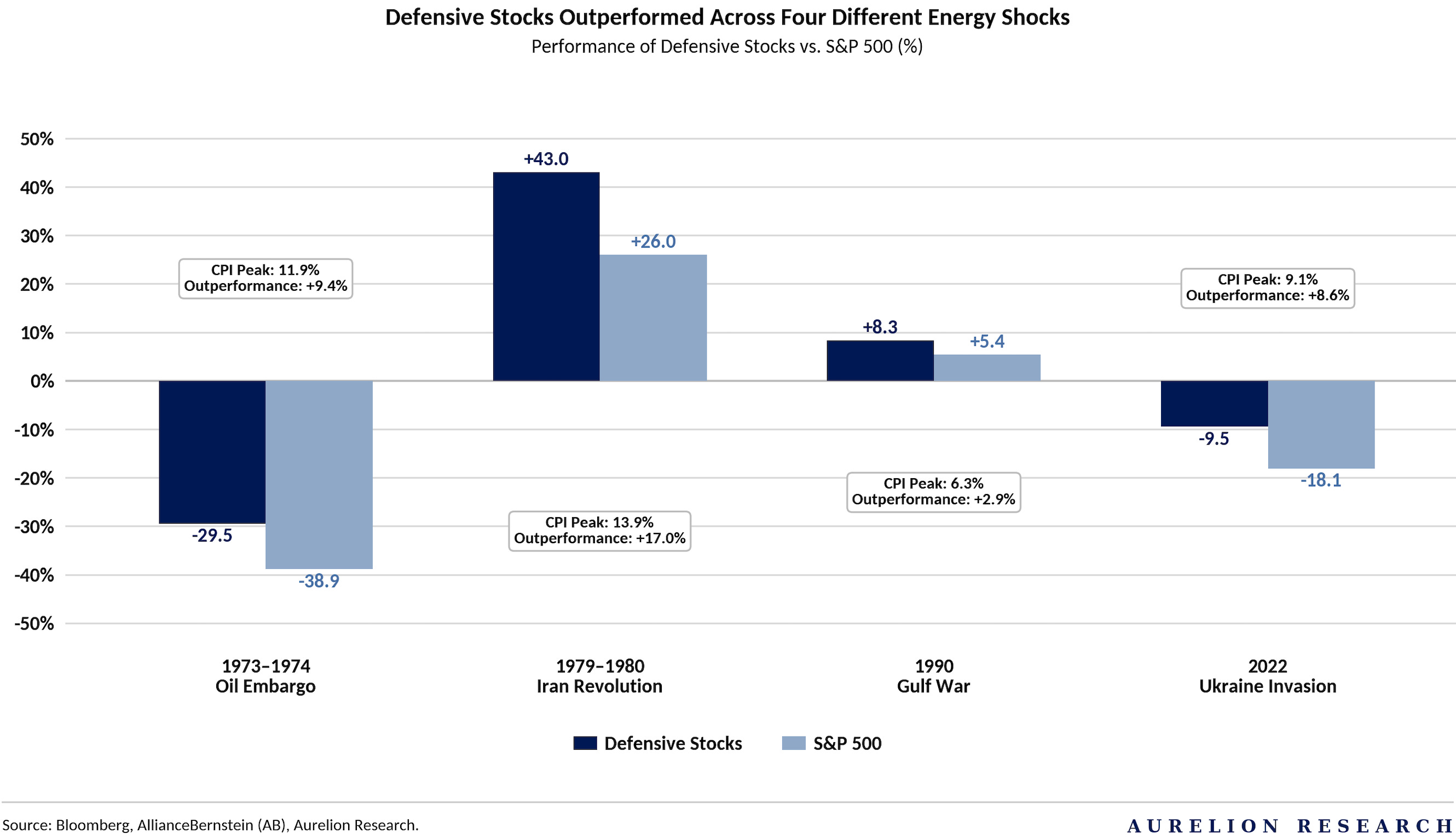

The data confirms our view that defensive stocks can extend beyond a simple safety net, and that, in fact, they can serve as a powerful tool for outperformance when energy costs spike. Looking at the four major energy shocks since 1973, defensive names have consistently beaten the S&P 500. During the 1979 Iran Revolution, these stocks delivered a 43% return.

As you can see above, they outperformed the broader market by 17% as inflation peaked. Even during more recent events such as the 2022 Ukraine invasion, defensive plays protected capital better than the average stock.

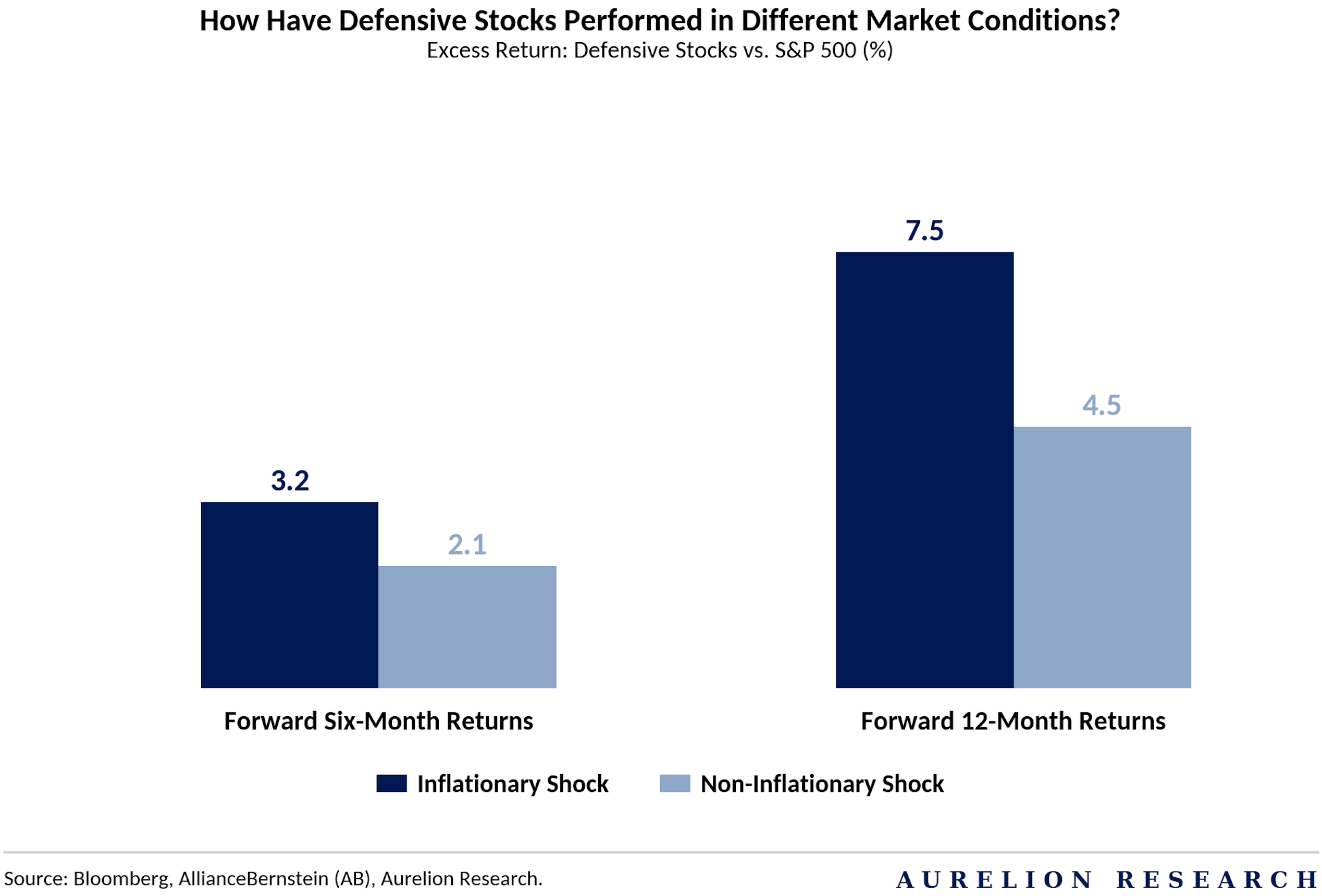

Performance in Inflationary Environments

The bottom chart shows that defensive stocks tend to perform better during inflationary shocks. When the economy faces rising prices, defensive names deliver forward 12-month returns of 7.5%. This is a significant increase compared to 4.5% in non-inflationary periods. This gap exists because these companies often have the pricing power to pass costs on to consumers.

As we navigate the current tensions in the Middle East, which appear far from over, history suggests that holding these positions is a smart way to stay ahead. They offer a combination of lower risk and higher relative returns while the rest of the market struggles with a weaker consumer and rising energy bills.

Table of Contents

New Position Overview

Investment Thesis

The Business Model

The Supply Gap Is Widening

Investment Market Overview

Development Monitor

Growth Strategy and the 2028 Plan

Capital Allocation & Portfolio Quality

Debt & Capital Structure Analysis

Valuation Analysis

Key Risks to Our Thesis

Our Final Take

This Real Estate company recently delivered another strong quarter, with margins once again outperforming. It is not a REIT or a pure real estate model, but a differentiated platform that gives it an edge and supports continued performance.

Its new assets are generating healthy margins of ~45%, which we believe reinforces management’s capital allocation ability and the earnings power of recent M&A. We see this as a well-run company that offers investors upside and durable earnings growth, while also providing downside protection supported by a strong net asset value (NAV).